Sample Category Title

BoE Stays Quiet But Data Could Speak Volumes

- BoE stuck between strong US data and the ECB rate cut

- Labour market data could support August rate cut expectations

- All eyes on average earnings growth

- Could the pound maintain its recent gains?

BoE remains on the sidelines

While the ECB announced its first rate cut since 2019 and the Fed is preparing for Wednesday’s gathering, the Bank of England has been forced to stay on the sidelines. Its next meeting is scheduled for June 20, but the upcoming parliamentary elections exclude the possibility of a rate cut.

Having said that, the BoE could turn more dovish, but such a reaction could be misinterpreted ahead of the July 4 elections. Talking about a slowing economy in need of a less restrictive monetary policy stance could be seen as intervening in the elections by offering another argument to the Labour party’s arsenal and causing the wrath of Tory officials.

Despite the fact that the BoE members’ public appearances are kept to a minimum, the BoE has not gone into hibernation. It remains vigilant and prepares for the key August 1 gathering. This meeting includes both the quarterly projections and a press conference to explain any likely rate change or prepare the ground for a move in September.

UK data has been positive recently

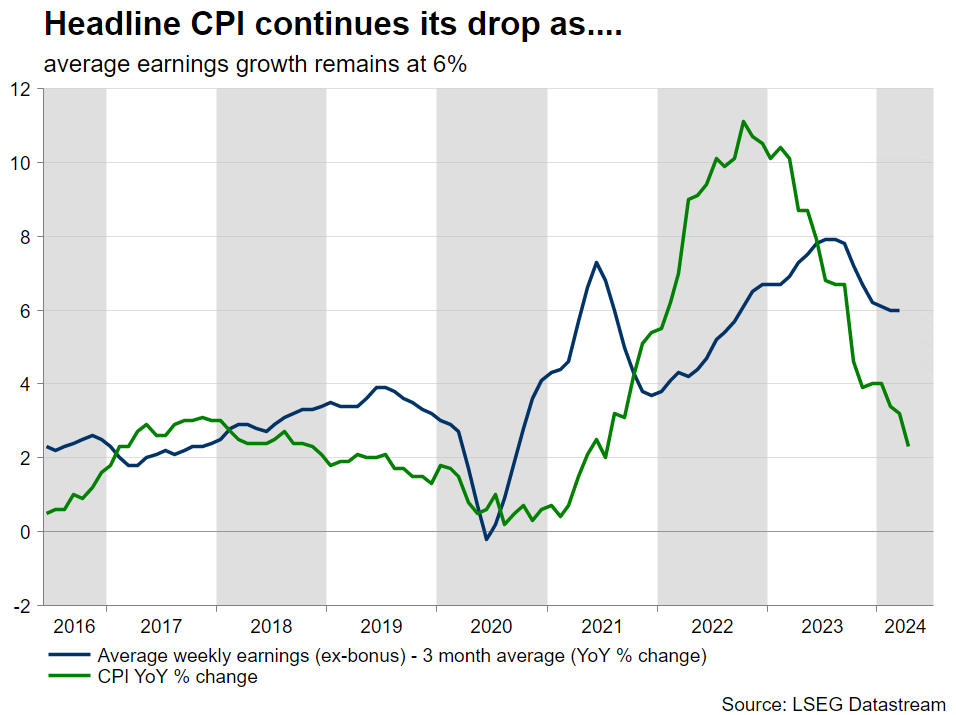

The April headline CPI figure showed an aggressive easing in inflationary pressures, but it fell short of BoE’s expectations. Interestingly, the core indicator jumped to 3.9% yoy, essentially reminding the market that inflation remains the BoE’s main problem. Coupled with the recent hotter PMI surveys and the various house price indices showing further signs of stabilization, the UK economy might not be screaming for a rate cut at this juncture.

With most investment houses convinced that the first rate cut by the BoE will be delivered in August, this week’s data could open the door to a more dovish rhetoric at next week’s gathering. On Tuesday, the May claimant count change could surprise on the downside, but the focus will be on the average earnings growth data.

The indicator that excludes bonuses is expected to remain stable at 6% year-on-year growth and hence signal that domestic demand could be strong going forward. Interestingly, with the European football championship starting this week, anecdotal evidence points to increased economic activity whenever the English team performs well in the tournament, thus potentially fueling further consumer spending.

On Wednesday, production data and the monthly GDP figure for April will offer more evidence on the ongoing recovery of the UK economy, but the market’s mind will probably be already running ahead to the June 19 CPI report, one day before the BoE meeting.

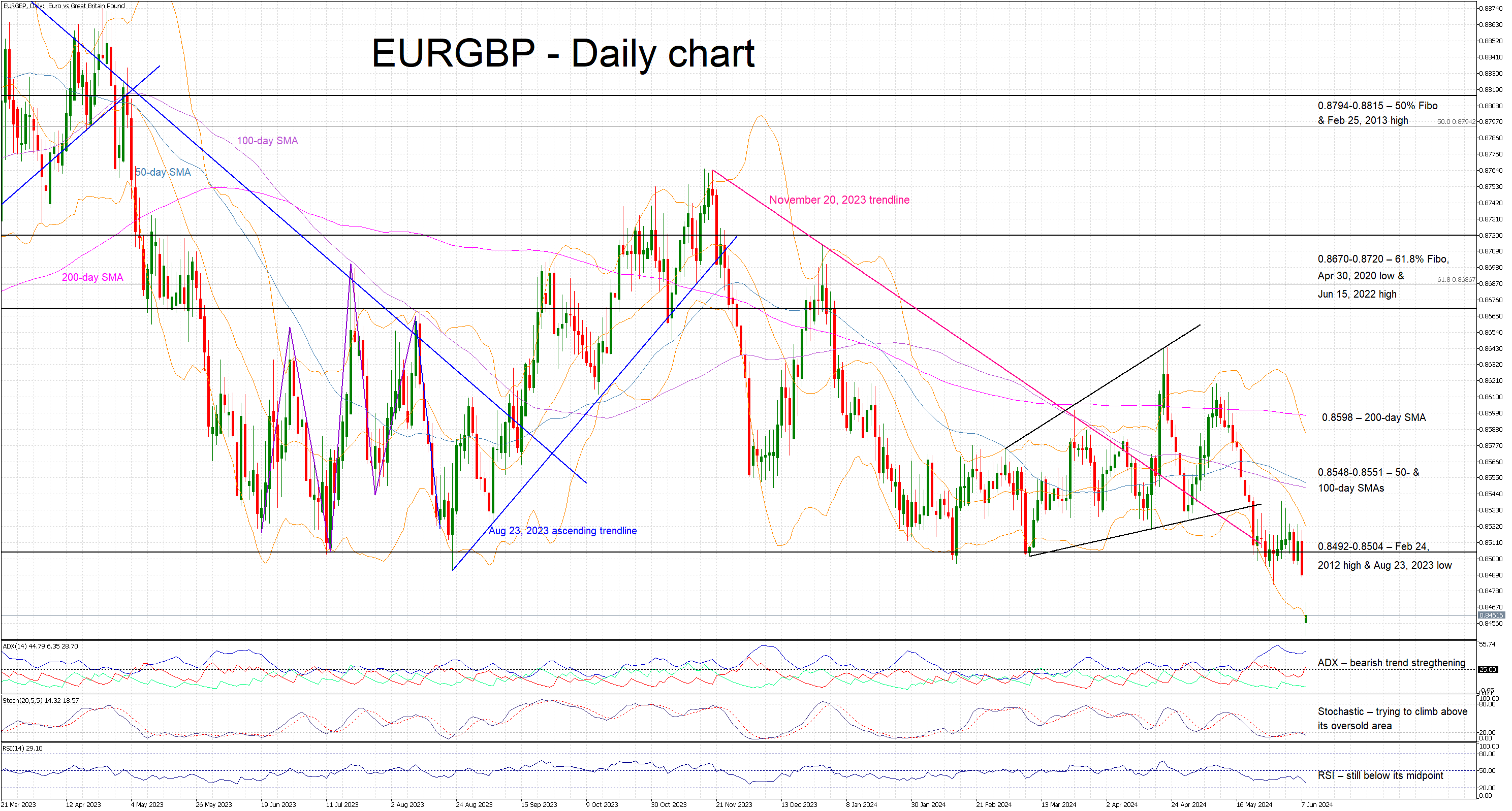

Could the pound maintain its recent gains?

It has been a relatively good period for the pound, gaining around 2% against the euro since April. Following the European elections’ results, the euro/pound pair dropped aggressively lower, breaking the 0.8492-0.8504 range that has acted as strong support over the past 12 months, and it is now trading at the lowest level since August 2022.

With the ECB unclear about its next move, the pound needs a fresh catalyst to record a decisive move lower. This week’s data, and particularly Tuesday’s average earnings figures, have the potential to surprise on the upside and help the euro/pound pair maintain its recent gains and set sail for the 0.8304 level.

On the flip side, a weak set of data could further support the investment houses’ expectations for a summer rate cut and thus allow the euro/pound pair to retest the 0.8492-0.8504 range and then climb even higher.

US Indices: Something for Optimists

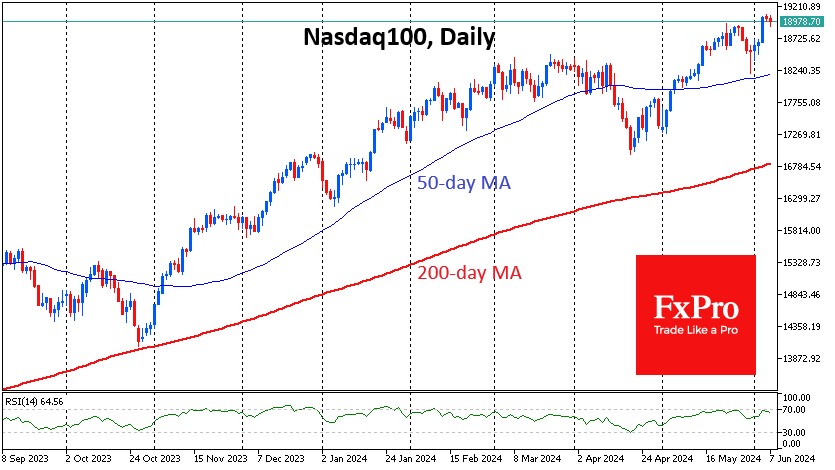

The US indices, S&P500 and Nasdaq100, closed Wednesday at record highs, taking a decisive step up, adding over 1.1% and 2%, respectively. The Dow Jones index lagged, adding just 0.25% for the day and is 3% off all-time highs. The Nasdaq-100 and S&P500 defended tops on Thursday, which seems more like a rest before rising rather than a downward reversal signal.

While the Fed has backed away from its original plan and is in no rush to cut rates, other major central banks have roughly stayed on the trajectory announced at the start of the year. Earlier in the week, the ECB and Bank of Canada cut their rates. The SNB made its policy easing move in March.

These actual moves by their colleagues, in addition to less strong economic data, stabilised expectations for the Fed Funds rate. Now, market participants, on average, expect two cuts totalling 50 points by the end of the year. This is a realistic midpoint in the range from the 5-6 rate cuts expected at the beginning of the year to the fears of a hike like we saw last month.

The start of a rate cut cycle and even a shift in medium-term expectations in that direction is favourable for risk appetite. This is the necessary fuel for further gains in equities.

With the S&P500 hovering near its highs, it is surprising to see the Fear and Greed Index degrade to “fear.” It has fallen from 48 to 44 in one week as its Breadth and Strength components of stock price are in “extreme fear.” Safe Haven Demand and Junk Bond Demand points to “fear”.

This is a clear indication that a few heavyweights are now providing stock growth. The optimistic view is that these components have room to recover to normal, which can feed further index gains. A solid bounce off the 50-day average at the end of May is also in the bulls’ favour.

However, the pessimist’s view also has a valid point. Signs of insufficient breadth and strength of gains in equities could be the first warning bells of the global rally’s exhaustion. Also, on the S&P500 chart, a sequence of higher highs corresponds to a sequence of lower peaks, which is a significant bearish factor.

Who will win this battle? We will only be able to judge this at the end of trading next Wednesday following the market reaction to CPI and FOMC.

Sunset Market Commentary

Markets

Elections for the European Parliament this time didn’t pass unnoticed on European markets. They clearly left investors with quite a degree of unease. The ‘gamble’ of French President Macron to call snap elections in an attempt to block the ascent of the far-right Rassemblement National (RN) illustrates the difficulties of center parties to politically stay in the driver’s seat and to execute their (reform) programs. The situation in countries like Germany (steep loss for the ruling coalition and gain of far right) or Italy (Brothers of Italy win) is not unequivocally the same, but there are some resemblances. Anyway, this context might reduce visibility on the budgetary and debt trajectory for the countries involved. Whatever the analysis, risk premia on European assets rose today. The Eurostoxx 50 is ceding more 1%. French equities underperform (-1.6%). EUR/USD maintains weekend losses to trade near 1.0750. 10-y spreads vs Germany for the likes of France and Italy are rising 6 bps and this trend in a more benign way also applies to most other intra-EMU bonds. Still, this broader E(M)U risk-off doesn’t help Bunds to play a safe haven role. German yields also add between 0.5 bps (2-y) and 7.5 bps (30-y). Evidently, considerations on future ECB monetary policy are also in play as a potential explanation for the rise in European/German yields. In this respect, ECB members tempered expectations for further ECB rate cuts. German Bundesbank Nagel indicated that the ECB is not necessarily at the starting point of a protracted rate cut cycle yet. ECB’s Kazimir put forward the September meeting/forecasts as a next evaluation point to see whether the ECB can cut rates again. Still EMU bonds largely underperform Treasuries even after strong US payrolls last Friday and with US markets counting down to US May CPI release and the Fed policy decision (including new projections/dots) both scheduled on Wednesday. In a steepening move, US yields are changing between -1 bp (2-y) and +3 bps (30-y). Economic data are close to non-existent today but later, the US Treasury will start its refinancing operation selling $58bn of 3-y notes. Recall that the previous series (2, 5 and 7-y bonds) two weeks ago only met mediocre investor interest. Brent oil after losses early last week, extends its rebound north of $80/b.

The EMU-related risk-off not only keeps the euro in the defensive against the dollar but also against most smaller regional currencies. The Swiss franc resumes it rebound since late May (EUR/CHF 0.9337). Sterling decisively cleared the EUR/GBP 0.85 barrier, currently trading below 0.845. Even the likes of the Swedish krone outperform, despite a series of unconvincing Swedish data published today (EUR/SEK 11.336). CE currency prove more vulnerable to the overall risk-off context (cf infra).

News & Views

Hungarian prices fell by 0.1% M/M in May while consensus expected a 0.1% increase. The highest price increase of 0.9% was measured for services. Food became 0.1% more expensive on average. Electricity, gas and other fuel prices fell by 0.9% M/M with fuel prices down 4.4%. On an annual basis, Hungary inflation as a result rose less than forecast (4% Y/Y from 3.7% vs 4.2% expected). Services prices are 9.5% more expensive while food is up 1%. Consumers paid 1.7% less for consumer durables. Electricity, gas and other fuels became 2.9% cheaper. The Hungarian forint lost significant ground even against a weaker euro. EUR/HUF rose from 390 to 394.50, the weakest HUF-level since the end of April. Significantly higher core bond yields are at least as accountable the inflation numbers. The likes of the Czech koruna (EUR/CZK 24.66) and Polish zloty (EUR/PLN 4.33) also face selling pressure today.

Norwegian inflation fell by 0.1% M/M as well in May with the Y/Y-disinflation process continuing from 3.6% to 3.3% for the headline number (lowest since July 2021). Housing, water, electricity, gas and other fuels prices were the main culprit (-2% M/M) with communications being the sole other price category in decline (-0.6% M/M). Underlying core inflation rose as expected by 0.5% M/M with the Y/Y-figure slowing from 4.4% to 4.1% (lowest since June 2022). The underlying core inflation pace strengthens the Norges Bank view that the current policy rate (4.5%) may remain in place for somewhat longer than previously envisaged (first rate cut in winter rather than autumn). The krone didn’t respond to the data with EUR/NOK a tad softer at 11.52.

Graphs

EMU 10-y swap rate: LT EMU yields jump on higher risk premia after EU parliamentary elections

EUR/USD nosedives in 1.06/1.09 trading range on both USD strength and euro weakness

EUR/HUF: forint under pressure on softer-than-expected inflation and global EU-related risk-off

CAC 40 tumbles below first important support as president Macron makes the gamble of snap elections

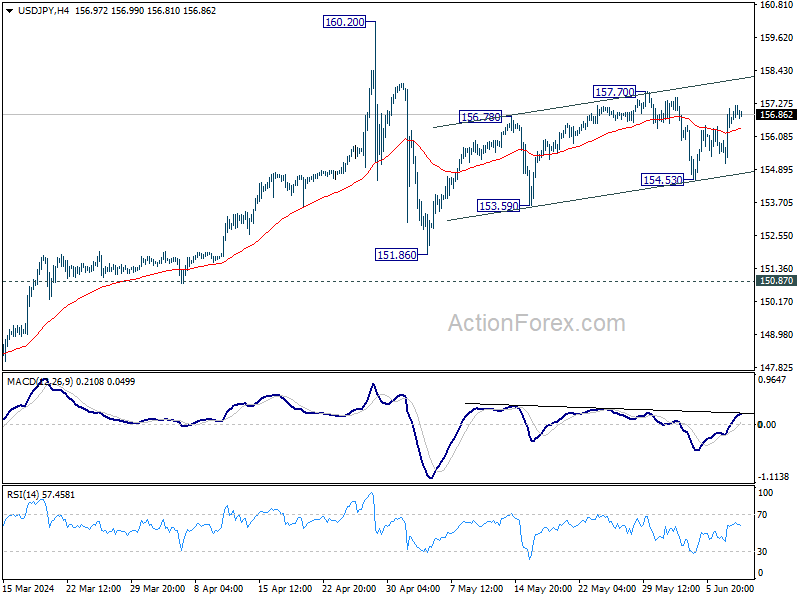

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.57; (P) 156.33; (R1) 157.52; More...

Intraday bias in USD/JPY stays neutral at this point. On the upside, break of 157.70 will resume the whole rise from 151.86 and target 160.20 high. Nevertheless, break of 154.53 will turn bias to the downside for 151.86 support and possibly below, as the third leg of the corrective pattern from 160.20.

In the bigger picture, a medium term top might be formed at 160.20. As long as 55 W EMA (now at 147.77) holds, fall from 160.20 is seen as correcting the rise from 140.25 only. However, sustained break of 55 W EMA will argue that larger correction is possibly underway, and target 146.47 support next.

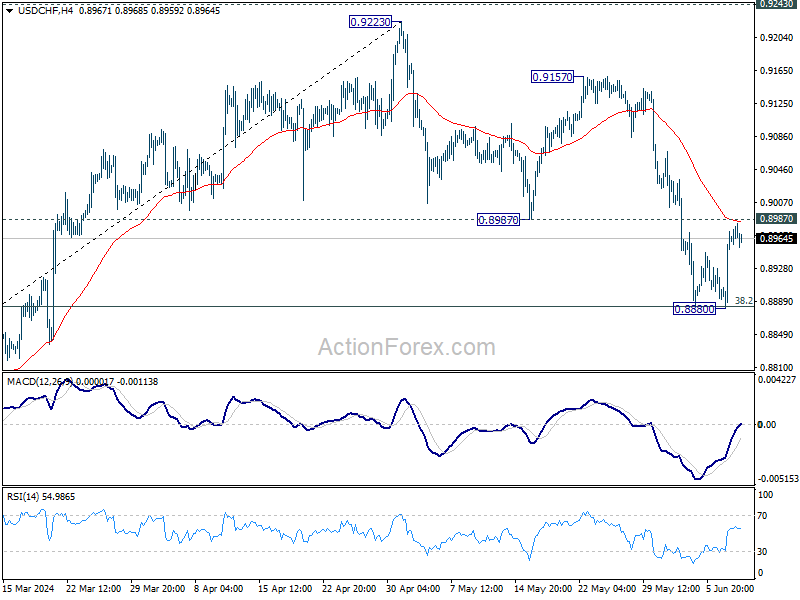

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8906; (P) 0.8940; (R1) 0.8998; More….

Intraday bias in USD/CHF remains neutral and outlook is unchanged. On the upside, firm break of 0.8987 support turned resistance will argue that correction from 0.9223 has completed, after drawing support from 0.8883 fibonacci level. Intraday bias will be back on the upside for 0.9157/9223 resistance zone. Nevertheless, sustained break of 0.8883 fibonacci level will carry larger bearish implications and bring deeper decline.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

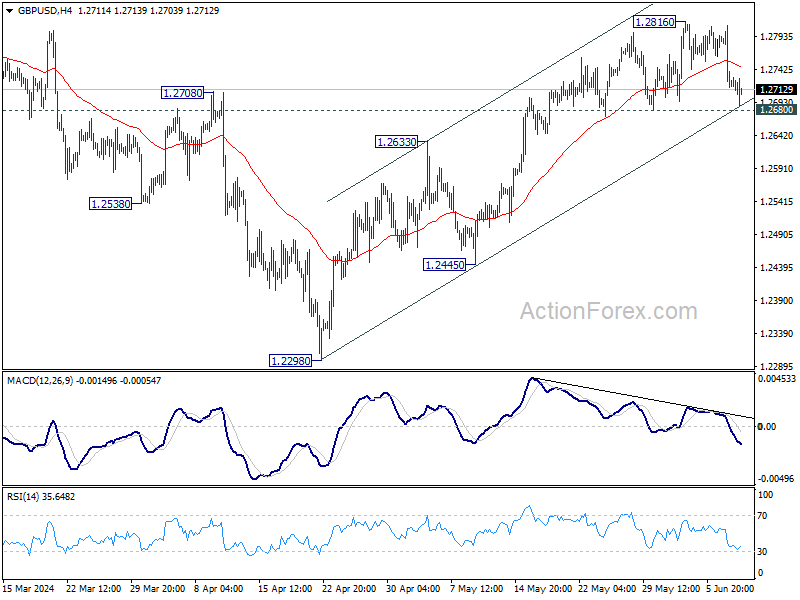

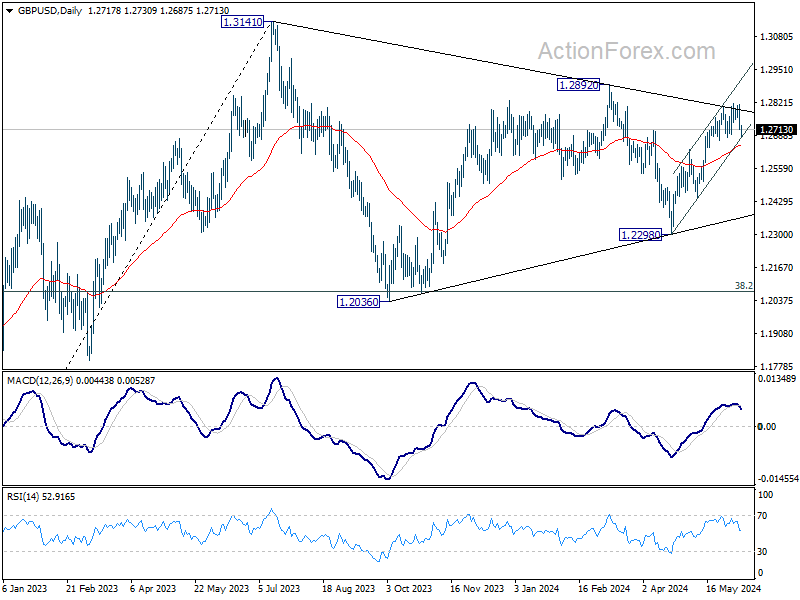

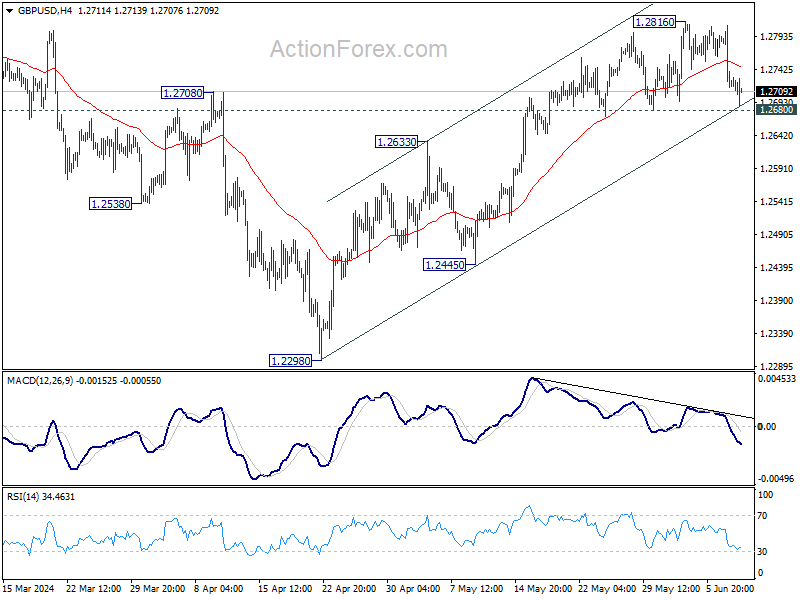

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2688; (P) 1.2750; (R1) 1.2784; More...

Intraday bias in GBP/USD remains neutral at this point and outlook is unchanged. . Considering bearish divergence condition in 4H MACD, firm break of 1.2680 support will turn bias back to the downside for 55 D EMA (now at 1.2651) and possibly below. Nevertheless, break of 1.2816 will resume the rise from 1.2298 to 1.2892 resistance.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2445 support will extend the corrective pattern with another decline instead.

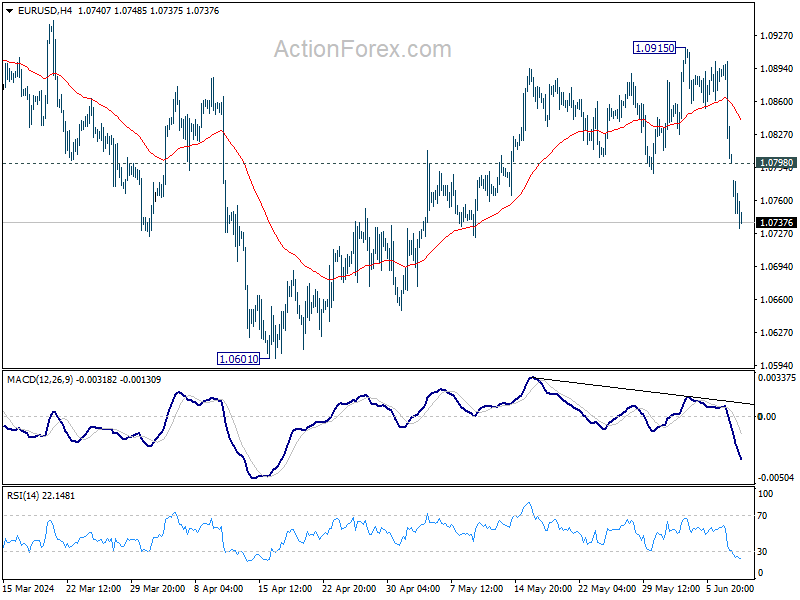

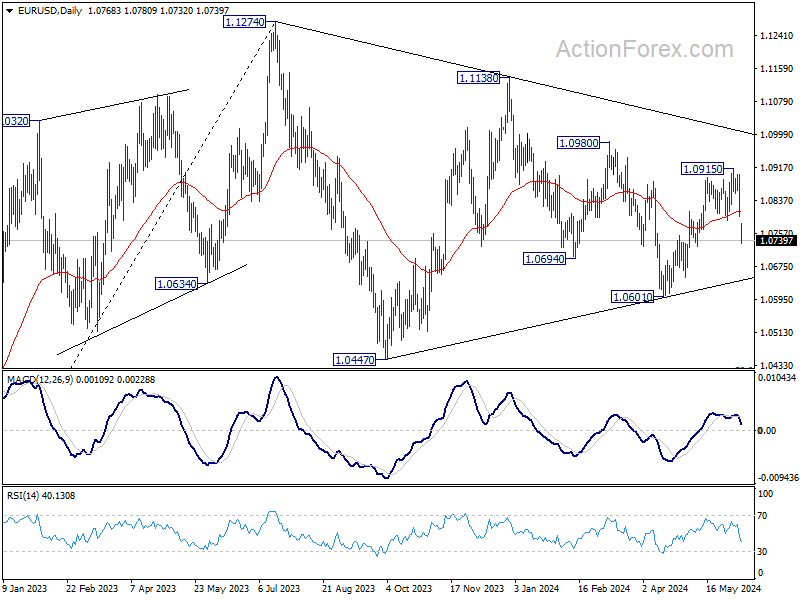

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0768; (P) 1.0835; (R1) 1.0870; More....

Intraday bias in EUR/USD stays on the downside at this point. Rebound from 1.0601 might have completed at 1.0915 already. Fall from there could be another falling leg of the corrective pattern from 1.1274. Further decline could be seen to retest 1.0601 support next. On the upside, above 1.0798 minor resistance will turn intraday bias neutral first. But risk will be mildly on the downside as long as 1.0915 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern, which might still be in progress. Break of 1.0601 will target 1.0447 support and possibly below. Nevertheless, on the upside, firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high.

Euro Staying Pressured Under Pressure Amid Yield Volatility

As US session begins, Euro continues to face significant downward pressure, largely influenced by political developments in France. The call for a snap election following the far-right National Rally party's gains in the EU election has sparked concerns among investors, driving French 10-year yield to its highest level since November. Additionally, the spread between French and German benchmark yields has widened, reaching the largest margin seen this year, further exacerbating Euro's volatility.

Italy's and Spain's bond markets are also experiencing turbulence, with Italy's 10-year yield surging past 4% mark and Spain's benchmark yield climbing above 3.4%. These movements in the bond markets reflect a broader sense of unease that is currently dominating the Eurozone's financial landscape.

In contrast, the broader forex markets are displaying relative stability, attributed to slow news flow and a light economic calendar. Australian and New Zealand Dollars are emerging as the stronger currencies, with Dollar also holding its ground. Japanese Yen and Swiss Franc are trailing behind, even though they're making notable gains against the struggling Euro. British Pound and Canadian Dollar are finding themselves in a more neutral position within the currency spectrum.

Technically, GBP/USD is still holding above 1.2680 support, as well as staying inside near term rising channel. Another rally through 1.2816 resistance is still in favor. However, sustained break of this support level will argue that rise from 1.2298 is possibly completed already, and bring deeper fall back to 1.2445/2633 support zone next. This down move could be triggered by further downside acceleration in EUR/USD or by poor GDP and employment data from the UK.

In Europe, at the time of writing, FTSE is down -0.29%. DAX is down -0.68%. CAC is down -1.71%. UK 10-year yield is up 0.046 at 4.310. Germany 10-year yield is up 0.052 at 2.669. Earlier in Asia, Nikkei rose 0.92%. Japan 10-year JGB yield rose 0.0668 to 1.039. Singapore Strait Times fell -0.26%. Hong Kong and China were on holiday.

ECB's Nagel urges caution on rate cuts

In a speech today, ECB Governing Council member Joachim Nagel stressed the importance of caution in making further interest rate cuts, citing ongoing economic uncertainty and persistent inflation pressures.

Nagel remarked, "I don't see us on a mountain top from which we will inevitably come down. Rather, I see us on a ridge where we still have to find the right point for a further descent," indicating the need for a measured approach on monetary policy.

Nagel projected that inflation in Eurozne area would gradually decrease towards the ECB's target, reaching 2% by the end of 2025, albeit later than previously expected. This suggests a longer path to achieving stable inflation, necessitating careful policy decisions.

Earlier today, fellow Governing Council member Peter Kazimir underscored the ongoing battle against inflation, referring to it as the "inflation beast." Kazimir emphasized that the upcoming September meeting will be pivotal for determining the necessity of further rate cuts.

Eurozone Sentix rises to 0.3, recovery continues but lacks momentum

In June, Eurozone Sentix Investor Confidence improved to 0.3 from -3.6, exceeding the expected -1.9. This marks the eighth consecutive monthly increase and the highest reading since February 2022. Current Situation Index also rose for the eighth month in a row, reaching -9.0 from -14.3, its highest level since May 2023. Similarly, Expectations Index increased to 10.0 from 7.8, the ninth consecutive rise and the highest since February 2022.

Sentix commented that while the recovery is ongoing, the "upswing lacks momentum". The increase in expectations offers some optimism that this positive trend could continue in the coming weeks. However, a stronger signal from Germany's economy is needed to boost this momentum, which has yet to emerge.

The slow pace of improvement in the current situation supports the case for ECB to consider further interest rate cuts. Nonetheless, the opportunity for such cuts appears limited. Sentix inflation barometer indicates an unfavorable inflation environment, putting additional pressure on ECB.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0768; (P) 1.0835; (R1) 1.0870; More....

Intraday bias in EUR/USD stays on the downside at this point. Rebound from 1.0601 might have completed at 1.0915 already. Fall from there could be another falling leg of the corrective pattern from 1.1274. Further decline could be seen to retest 1.0601 support next. On the upside, above 1.0798 minor resistance will turn intraday bias neutral first. But risk will be mildly on the downside as long as 1.0915 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern, which might still be in progress. Break of 1.0601 will target 1.0447 support and possibly below. Nevertheless, on the upside, firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y May | 3.00% | 3.10% | 3.10% | |

| 23:50 | JPY | GDP Q/Q Q1 F | -0.50% | -0.50% | -0.50% | |

| 23:50 | JPY | GDP Deflator Y/Y Q1 F | 3.40% | 3.70% | 3.60% | |

| 23:50 | JPY | Current Account (JPY) Apr | 2.52T | 2.06T | 2.01T | |

| 05:00 | JPY | Eco Watchers Survey: Current May | 45.7 | 48.9 | 47.4 | |

| 08:00 | EUR | Itay Industrial Output M/M Apr | -1.00% | 0.30% | -0.50% | |

| 08:30 | EUR | Eurozone Sentix Investor Confidence Jun | 0.3 | -1.9 | -3.6 |

ECB’s Nagel urges caution on rate cuts

In a speech today, ECB Governing Council member Joachim Nagel stressed the importance of caution in making further interest rate cuts, citing ongoing economic uncertainty and persistent inflation pressures.

Nagel remarked, "I don't see us on a mountain top from which we will inevitably come down. Rather, I see us on a ridge where we still have to find the right point for a further descent," indicating the need for a measured approach on monetary policy.

Nagel projected that inflation in Eurozone area would gradually decrease towards the ECB's target, reaching 2% by the end of 2025, albeit later than previously expected. This suggests a longer path to achieving stable inflation, necessitating careful policy decisions.

Earlier today, fellow Governing Council member Peter Kazimir underscored the ongoing battle against inflation, referring to it as the "inflation beast." Kazimir emphasized that the upcoming September meeting will be pivotal for determining the necessity of further rate cuts.

Euro Falls to Four-Week Low: Politicians to Blame

EUR/USD plummeted below 1.0800 and is currently hovering around 1.0796 on Monday morning. This development came amid heightened political tensions in France. President Emmanuel Macron called for early elections on Sunday in the wake of his party's crushing defeat and Marine Le Pen's party's resounding victory in the European Parliament elections. The far-right, which secured twice as many votes as its closest competitors, has won and now has significant influence in France. The defeat of the country's pro-presidential forces has profoundly impacted the euro's position.

Furthermore, the euro was also under pressure from the US dollar ahead of this week's Federal Reserve meeting. Robust employment statistics in the US for May had already led the market to lower its expectations of a Fed interest rate cut.

Last week, the European Central Bank lowered its interest rate for the first time in five years. However, it is adopting an overly cautious stance on further rate cuts. In its comments, the ECB acknowledged the continued price pressures and projected that inflation will exceed targets this year and next. The regulator is refraining from making any specific commitments on a clear rate trajectory, indicating that all future ECB actions will have to be based on incoming statistics one way or another.

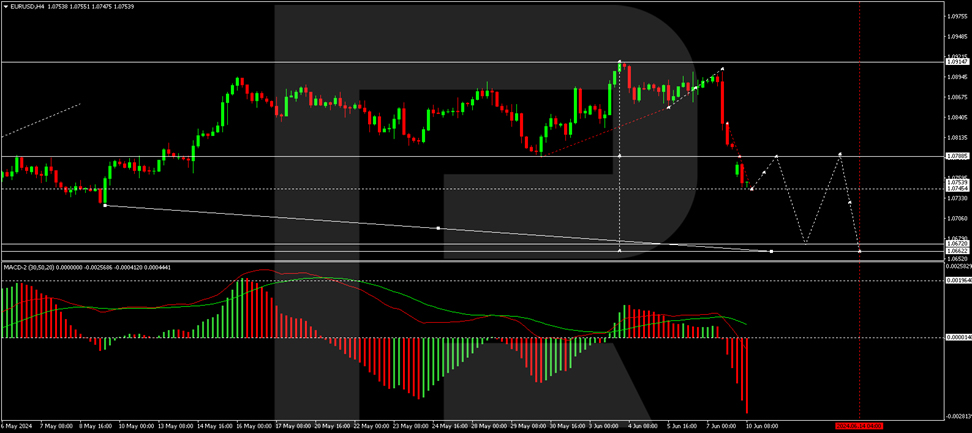

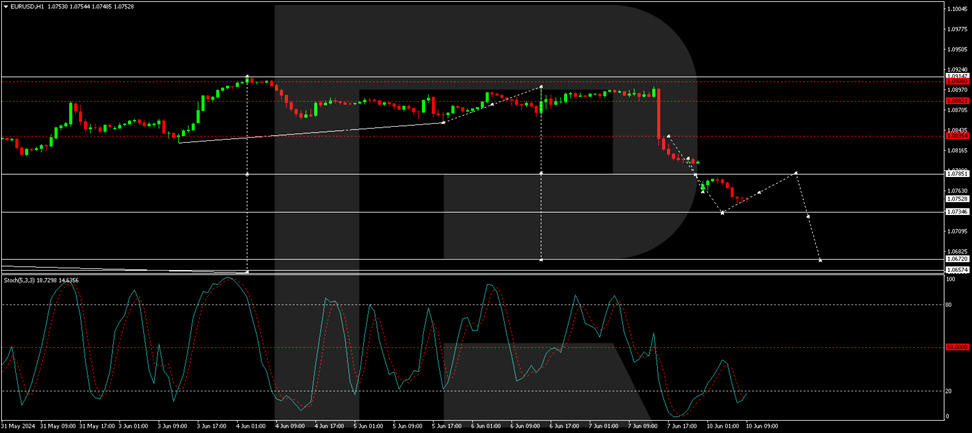

Technical analysis of EUR/USD

On the H4 chart of EUR/USD, the market completed the correction at 1.0901 and started the development of a new wave of decline. The downward impulse to the level of 1.0835 is fulfilled at the moment. A consolidation range around this level was formed, and the structure of the wave to 1.0747 was worked out with a downward exit. Today, we will consider the probability of a decline to 1.0735. After working off this level, the growth link to 1.0785 (test from below) is possible, with a further decline to 1.0672, representing the local target. Technically, this scenario is confirmed by the MACD indicator, whose signal line is below zero and is directed strictly downwards.

On the H1 EUR/USD chart, the market continues to develop a structure of decline to 1.0734. After working off this level, a correction to 1.0785 is possible. Further, we will consider the probability of a decline to 1.0672, the first target of the downward trend. Technically, this scenario is confirmed by the Stochastic oscillator, whose signal line is under the level of 20. We expect the beginning of growth to the level of 50.