Sample Category Title

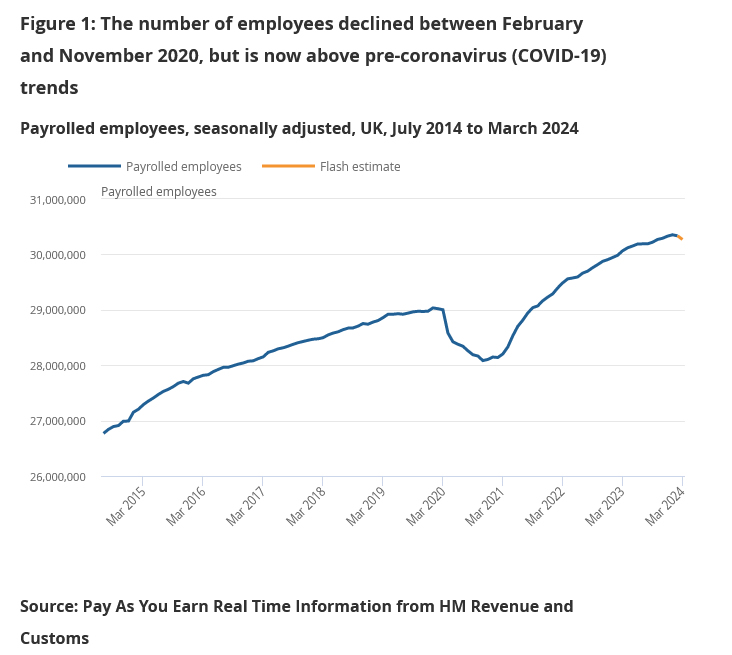

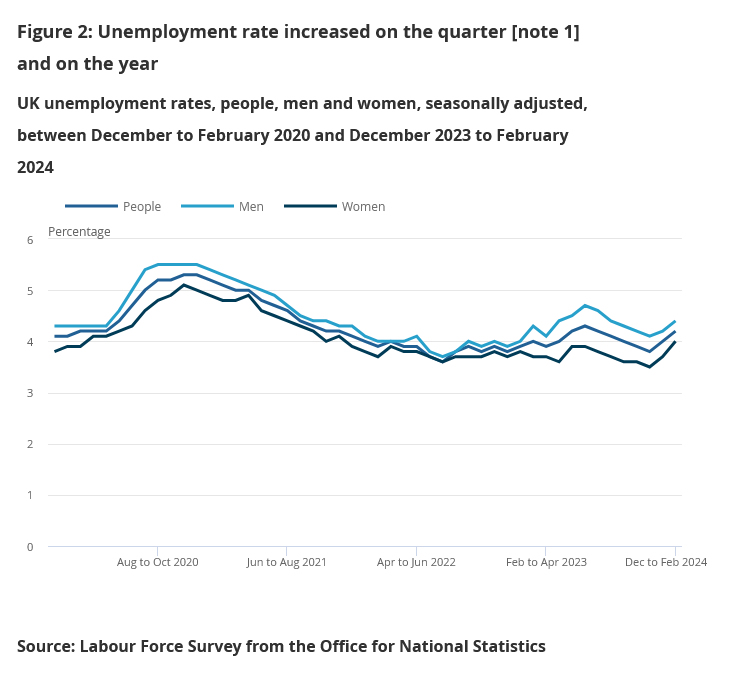

UK payrolled employment falls -67k in Mar, unemployment rate rises to 4.2% in Feb

UK payrolled employment fell -67k or -0.2% mom in March. Median monthly pay rose 5.6% yoy, slowed from prior month's 6.2% yoy. Claimant count rose 10.9k, below expectation of 17.2k.

In the three months to February, unemployment rate rose from 4.0% to 4.2%, above expectation of 4.0%. Average earnings including bonus rose 5.6% yoy, unchanged from prior month's rate. Average earnings excluding bonus rose 6.0%, down slightly from January's 6.1% yoy.

Hard to Justify a Cut

A stronger-than-expected retail sales data from the US cemented the idea that the US economy remains too strong for the Federal Reserve (Fed) to cut the rates in summer. Retail sales jumped 0.7% in March on a monthly basis, more than 4% on a yearly basis, the 3 and 6-month bill auctions were weak, and Atlanta Fed’s GDPNow forecast rebounded to 2.8%. Not bad.

Then, China posted a surprisingly stronger-than-expected GDP number this morning, showing that the Chinese economy grew 5.3% in the first quarter, comfortably higher than a 4.8% growth penciled in by analysts. But the sky is not blue in China. The industrial production missed estimates, house prices continue to fall and consumer spending slowed significantly during March, hinting that the underlying problems – like property crisis and weak consumer confidence - are not going away. Remember, Fitch cut the country’s outlook to negative last week citing risks to public finances, while in contrast Goldman and Morgan Stanley raised their outlook for the country’s economic growth pointing at improved factory activity and recovery in exports. But the EU started a deluge of investigations on China that could hurt the country’s export outlook, along with the risk of seeing Donald Trump become the next US president. The contradictory expectations and mixed data explained why the CSI 300 slid despite a 5.3% GDP growth. Shanghai’s Composite fell almost 1.5%.

A strong Chinese GDP may have not boosted appetite for Chinese stocks, but it sure boosts worries that rising Chinese growth – regardless of where growth comes from – will fuel global inflation and make major central banks think twice about their rate cutting plans. While the European Central Bank (ECB) and the Bank of England (BoE) are seen cutting the rates between summer and fall respectively, the outlook becomes complicated for the US. Provided that the economic growth and jobs market remain robust and inflation is heating up, the idea that the Fed’s next move will be a rate hike starts cooking in many investors’ minds. UBS now thinks that the Fed could increase borrowing costs to 6.5% next year to combat inflation. The fading Fed cut expectations continue to pressure the treasury market. The US 2-year yield is preparing to jump sustainably above the 5% level, the 10-year yield advanced past the 4.60% and the US dollar index extends gains. The EURUSD is trading a touch below the 1.0615 this morning with euro bears eyeing a further decline to 1.05 level, while the USDJPY spiked above 154 – the unthinkable at the start of the year – as the yen bears defy the Japanese authorities intervention threats and T. Rowe Price calls for another 10% slide in the Japanese yen.

In equities, the S&P500 had a bad start to the week with a 1.20% decline, as technology stocks led losses. Nasdaq fell 1.65%. Both the indices slipped below their 50-DMA following yesterday’s selloff. While strong economic data is not necessarily bad news for company earnings – as consumers continue to spend – the rising inflation, the fading dovish Fed expectations, and the latest optimism regarding earnings expectations could limit the upside potential in major stock indices, if company results fail to beat high expectations. The fear sets in and the VIX index rises rapidly.

Earnings

Goldman Sachs surprised in the Q1 with a 28% jump in profit, but JPM and Wells Fargo’s first quarter results didn’t enchant investors. BoFA and Morgan Stanley will release their quarterly results in the coming hours. BoFA may announce a narrowing net interest margin, as did JPM and Wells Fargo, while Morgan Stanley is expected to post its 9th consecutive quarterly drop in earnings. Later this week, Netflix will begin the dance for the major tech earnings, Tesla is due to reveal its Q1 results next week.

Tesla said that it will cut 10% of its workforce globally to adjust to slowing EV demand. In fact, the company has had a bad quarter, deliveries fell 8.5% while the global EV sales increased less than 3%. Tesla lost market share despite cutting the prices of its electric cars. Losing market share despite lowering prices calls for immediate action to increase profitability. Price increases and cost cutting are the first aid measures that should soothe investors’ nerves, while bringing forward new revenue streams like robotaxis should keep investors dreaming for a bright future. Yet, the context of slowing EV growth and rising competition will likely continue to weigh on profits, and robotaxis are a niche and a slowly growing segment which won’t show in the bottom line in the immediate future. Therefore, Tesla – which has a PE ratio of nearly 62, has room to extend losses to settle at a more reasonable valuation. A slide toward the 100 is possible.

Mixed Signals Indicate China Still Muddling Through

In focus today

We continue to follow the developments in the Middle East after Iran's strike on Israel in the weekend. It will be key to watch for signals on the extent of an Israeli retaliation. So far, Israel has said it will "exact a price" from Iran, while the US, France, and the UK have all urged restraint. See more below.

We also look out for the German ZEW data for April. The assessment of the current business situation has stabilised in the recent months while expectations have risen, which suggests a bottoming out of activity Germany. It will be interesting to see if the April data further point to an improvement in activity. See more in Research Germany - Worst is over in German manufacturing, 15 April. Yesterday we also published Research Global - Manufacturing recovery to continue into the summer, 15 April, where we look at the lift to the global manufacturing cycle.

Economic and market news

What happened overnight

Chinese data releases overnight were a mixed bag. On the positive side GDP for Q1 surprised to the upside showing an increase in growth from 5.2% to 5.3% (consensus 4.8%). This puts the government on track for its 5% growth target and still leaves upside risk to our forecast of 4.5% for this year. However, growth is still much dependent on stimulus and public investments. Retail sales for March disappointed with growth of only 3.1% y/y in March versus consensus expectations of 4.8% y/y. Industrial production also surprised to the downside. After a strong start in Jan/Feb at 7% growth, March dropped to 4.5% y/y (consensus 6.0% y/y). On the slightly positive side, housing data showed a few rays of light with home sales improving as the three-month average increased to 108.2 million square meters (using our own seasonal adjustment) up from 70 million square meters in January. Overall housing is still weak, though and provides the main drag on the economy as it has a negative spill-over to private consumption. China is preparing new stimulus with a trade-in scheme for consumer goods coming soon, which may hold consumption in the short term before the scheme kicks in. Overall, developments continue to be in line with our muddling through scenario for Chinese growth.

What happened yesterday

Fears of an immediate further escalation of the Israel/Iran conflict diminished slightly yesterday, and oil prices posted a modest decline during the day but reversed losses overnight to stay flat. Markets were characterized by a degree of caution as they waited for signals from the conflict. Israel has made it clear that it intends to respond, but it has yet to decide on how and by how much and has stated that it will seek support from its allies. When and how are the key questions, including whether it will be by proxy or a direct confrontation, where the latter would be a very significant escalation. Several major powers (incl. the US and Germany) have sought to deescalate the situation by urging restraint. An escalation of the conflict could spark major unrest in the region and have global economic consequences, with an analysis from Bloomberg indicating that a direct war would raise the oil price by some USD 64 and lower GDP growth by 1 percentage point.

Opposite signed macro surprises from the US and euro area as figures for US retail sales showed a 0.7% m/m increase (cons: 0.3%) in March. The figure is somewhat clouded by technical factors (seasonal adjustment) but indicates the continuation of a steady growth trend. Conversely, euro area industrial production declined 6.4% y/y (cons: -5.7%) in February which together with a large decline in January means production will likely be a significant drag on growth in Q1 2024. US yields gained with the 10Y up 13bp as of last night, while the reaction to the euro area data was more muted.

The yen weakened against major currencies (again) during Monday's session with USD/JPY moving past the 154 mark (+0.6%) to hit its lowest level for the yen since 1990 as of last night. The strong US retail sales was one factor as this supports delayed Fed rate cuts. The Japanese finance minister reiterated warnings about a possible intervention, but he is in a tough spot as the recent development has largely been due to upside US surprises since the yen is sensitive to US rates, which puts the sustainability of the effects of an intervention into question.

Equities: Global equities were lower yesterday as US yields once again spoiled the party. The European and US equity cash sessions looked very different both in direction and rotations as the yield spike came relatively late in the European cash session. The global impact is of course biggest from the US development and hence the part to focus on. Sharply higher real yields and a steeper curve "finally" resulted in big tech and long duration stocks underperforming and thereby signalling that the recent lift to yields is more than equities can absorb short-term. The flipside was defensive value outperforming with banks joining after a very strong result from Goldman Sachs. VIX jumped to 19, reflecting the uncertainty arising from yields moving higher and financial conditions tightening. In US yesterday, Dow -0.7%, S&P 500 -1.2%, Nasdaq -1.8% and Russell 2000 -1.4%. Asian markets are sharply lower this morning led by Japan, South Korea and Taiwan reflecting the tech and cyclical sell-off. Chinese markets are doing better on mixed data out of China this morning. GDP came out very strong while industrial production and retails sales numbers disappointed. European and US futures are lower this morning as well.

FI: Global yields moved higher across the board as fear of escalation of the Middle Eastern conflict faded and thus markets have almost reversed the rally it recorded on Friday, despite the news over the weekend. 10y Bunds rose 6bp to 2.44% yesterday. US retail sales was stronger than anticipated. Currently, rates markets are caught in a directionless range currently as markets are waiting for a catalyst.

FX: The USD and the CHF, two safe havens, outperform the rest of G10 amid tensions in the Middle East. EUR/USD hits year-lows just shy of breaking below 1.06, while USD/JPY makes new year highs flirting with 154.50. Initially, EUR/SEK has weathered the storm, although the topside remains vulnerable to deteriorating risk sentiment. NOK/SEK down from parity to around 0.9950 as EUR/NOK edged higher. Brent oil is at USD 90.6/bbl this morning.

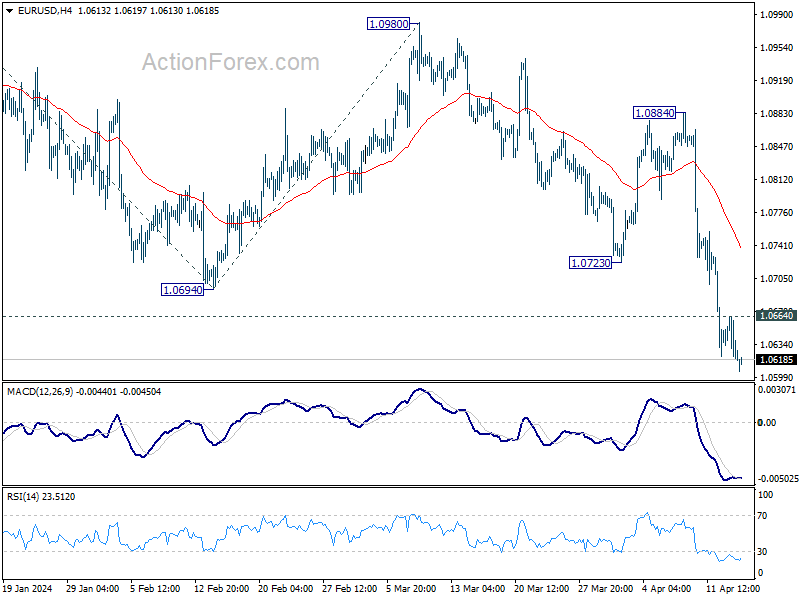

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0608; (P) 1.0636; (R1) 1.0653; More...

Intraday bias in EUR/USD stays on the downside at this point. Current fall is part of the decline from 1.1138. Next target is 100% projection of 1.1138 to 1.0694 from 1.0980 at 1.0536 next. On the upside, above 1.0664 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Current fall from 1.1138 is seen as the third leg. While deeper decline is would be seen to 1.0447 and possibly below. Strong support should emerge from 61.8% retracement of 0.9534 to 1.1274 at 1.0199 to complete the correction.

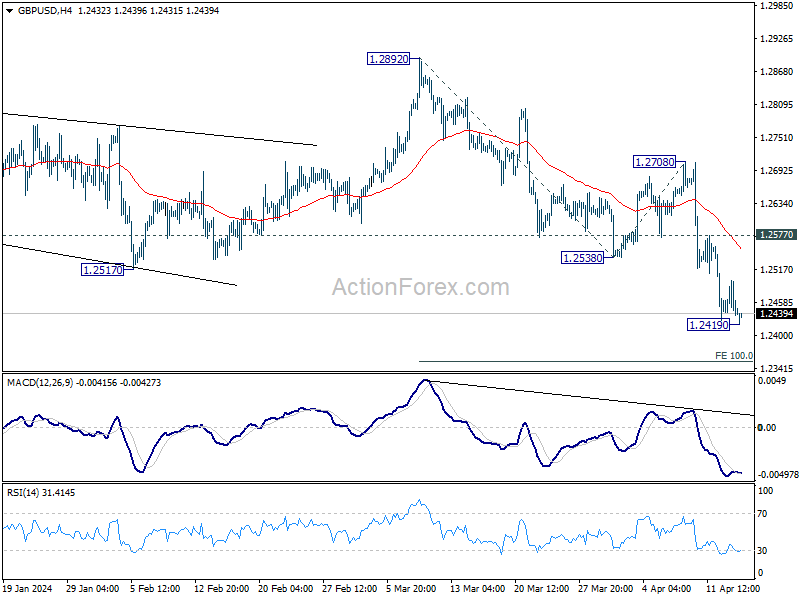

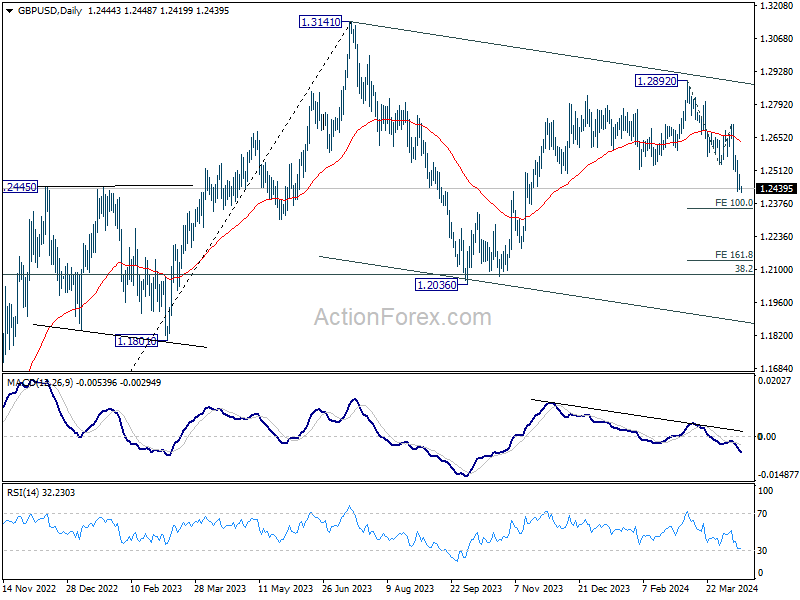

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2421; (P) 1.2460; (R1) 1.2484; More...

Intraday bias in GBP/USD stays neutral first and more consolidations could be seen. But recovery recovery should be limited by 1.2577 minor resistance to bring another fall. On the downside, firm break of 1.2419 will resume the decline from 1.2892 to 100% projection of 1.2892 to 1.2538 from 1.2708 at 1.2354. Firm break there will target 161.8% projection at 1.2207 next.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Fall from 1.2892 is seen as the third leg. Deeper decline would be seen to 1.2036 support and possibly below. But strong support should emerge from 61.8% retracement of 1.0351 to 1.2452 at 1.1417 to complete the correction.

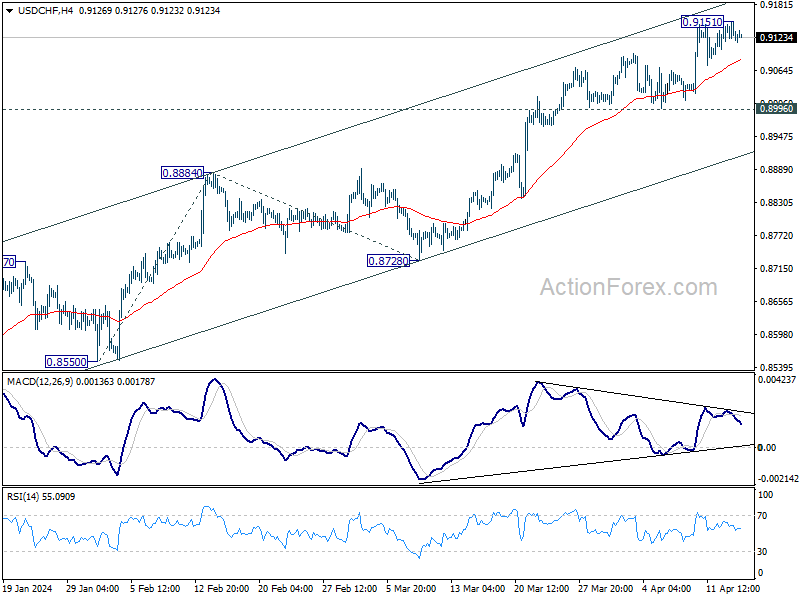

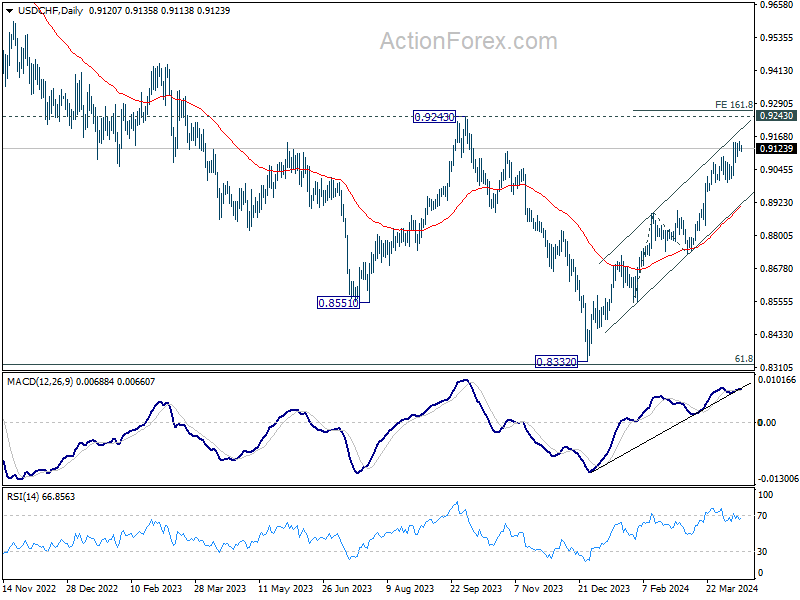

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9101; (P) 0.9126; (R1) 0.9141; More....

Intraday bias in USD/CHF remains neutral and more consolidations could be seen. But further rally is expected as long as 0.8996 support holds. Firm break of 0.9151 will target 161.8% projection of 0.8550 to 0.8884 from 0.8728 at 0.9268.

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish.

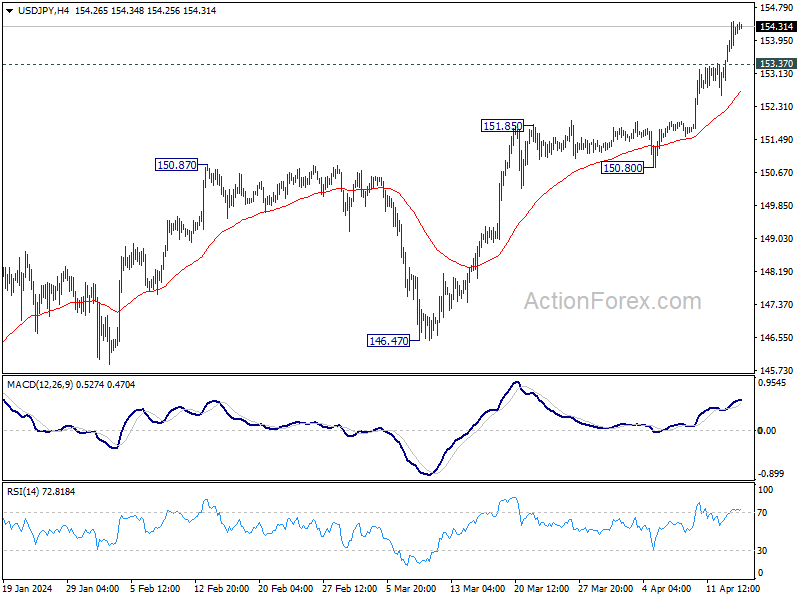

USD/JPY Daily Outlook

Daily Pivots: (S1) 153.34; (P) 153.89; (R1) 154.83; More...

Intraday bias in USD/JPY remains on the upside for the moment. Current up trend is in progress for 155.20 fibonacci projection level next. On the downside, below 153.37 minor support will turn intraday bias neutral and bring consolidations again, before staging another rally.

In the bigger picture, current rise from 140.25 is seen as the third leg of the up trend from 127.20 (2023 low). Next target is 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. Outlook will now remain bullish as long as 146.47 support holds, even in case of deep pullback.

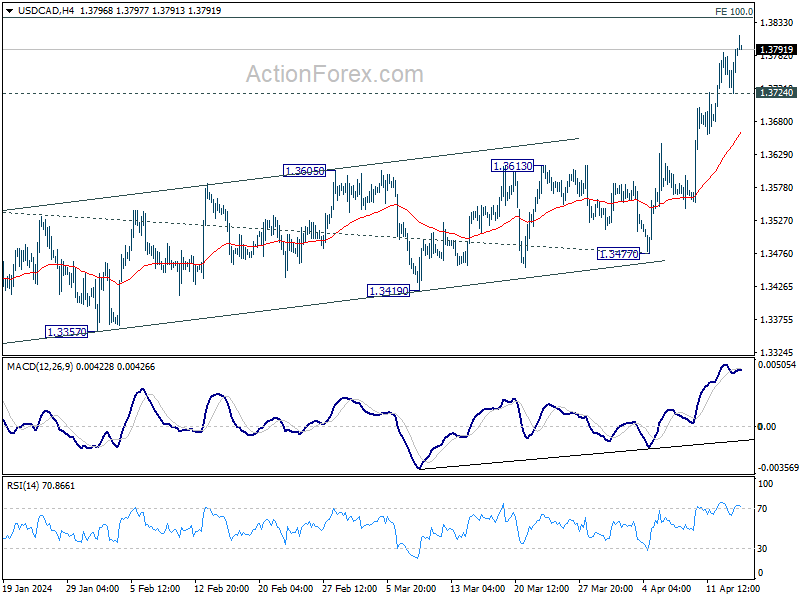

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3744; (P) 1.3769; (R1) 1.3814; More...

USD/CAD's rally is still in progress and intraday bias stays on the upside. Current rally from 1.3176 would target 100% projection of 1.3176 to 1.3540 from 1.3477 at 1.3841. On the downside, below 1.3724 minor support will turn intraday bias neutral and bring consolidations first, before staging another rise.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

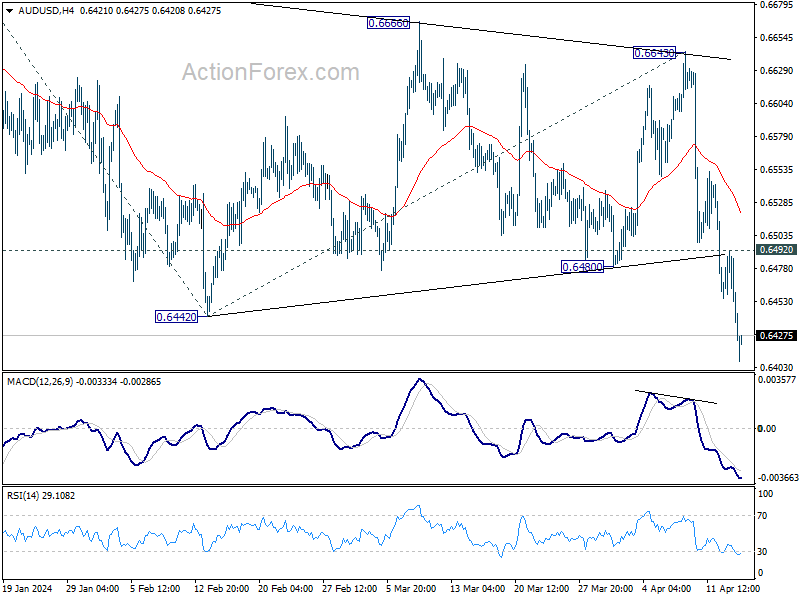

AUD/USD Daily Report

Daily Pivots: (S1) 0.6422; (P) 0.6458; (R1) 0.6477; More...

AUD/USD's break of 0.6442 support confirms resumption of whole fall from 0.6870. Intraday bias remains on the downside for 61.8% projection of 0.6870 to 0.6442 from 0.6643 at 0.6378. Decisive break there will pave the way to 0.6269 low, and possibly further to 100% projection at 0.6215. On the upside, above 0.6429 minor resistance will turn intraday bias and bring consolidations, before staging another fall.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which is still in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

Dollar Maintains Dominance as Global Markets Wrestle with Risk Aversion

Dollar is capitalizing on its strong position and extends its rally om Asian session today, as risk aversion grips global markets. US stocks, which initially showed gains overnight, ultimately closed significantly lower as Treasury yields climbed in response to robust economic data. The sentiment continued in Asia, with major markets opening lower, and followed by extended decline. lower open.

Amid these developments, China's economic data presented a mixed picture, providing little to uplift overall market sentiment. Strong Q1 GDP from China was overshadowed by a batch of weak March data. Further dampening sentiment, S&P Global downgraded the credit rating of Chinese developer Longfor from BBB- to BBB+ yesterday, assigning a negative outlook. These developments in China have cast a shadow over global market sentiment.

In the currency markets, Dollar stands out as the strongest performer of the day, with Japanese Yen and Canadian Dollar also showing resilience. Conversely, Australian Dollar is facing the most significant pressure, followed by New Zealand Dollar and Swiss Franc. Euro and Sterling are holding middle ground as market participants shift their focus to upcoming economic releases, including UK employment data and wage growth, German ZEW economic sentiment, and Canadian CPI.

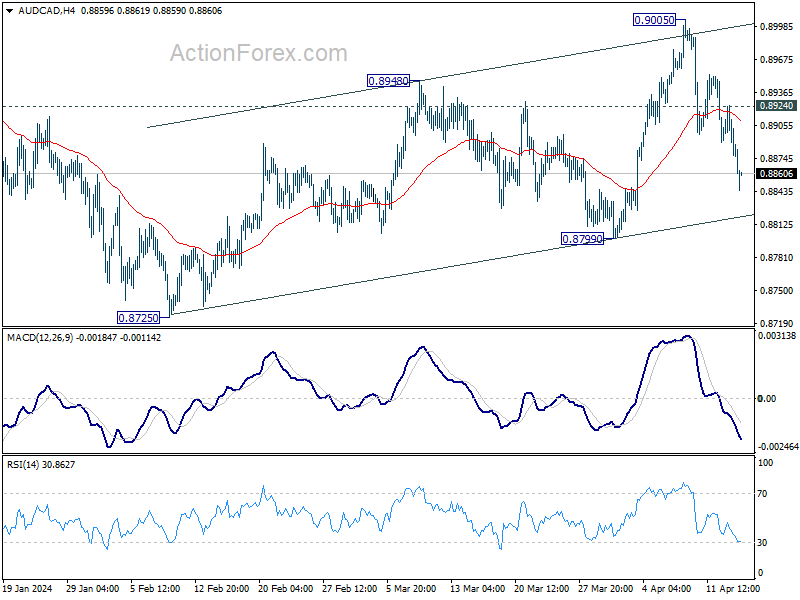

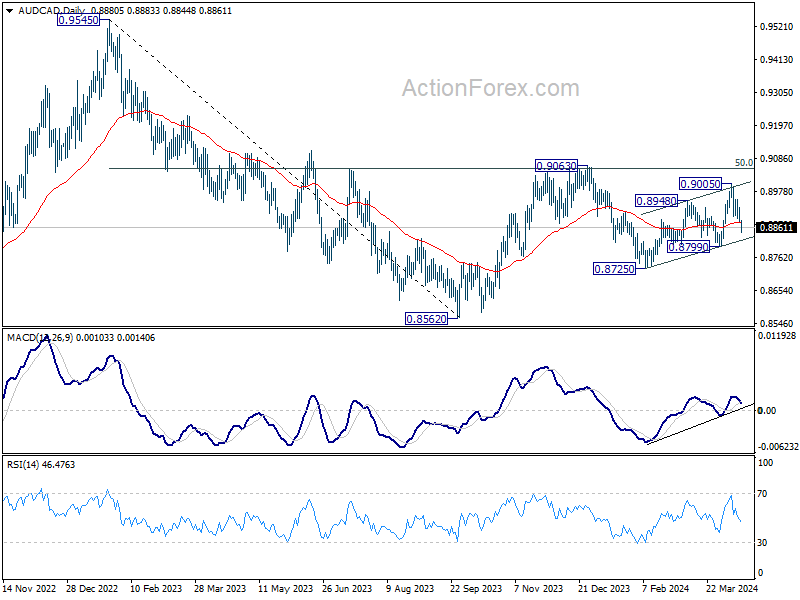

Technically, AUD/CAD's extended decline affirms that case that corrective recovery from 0.8725 has completed with three waves up to 0.9005. Deeper decline would be seen to 0.8799 support next. Firm break there will argue that whole fall from 0.9063 is ready to resume through 0.8725 support. Let's see if Canadian CPI today would prompt the downside breakout.

In Asia, at the time of writing, Nikkei is down -2.22%. Hong Kong HSI is down -1.93%. China Shanghai SSE is down -1.42%. Singapore Strait Times is down -1.29%. Japan 10-year JGB yield is up 0.0089 at 0.875. Overnight, DOW fell -0.65%. S&P 500 fell -1.20%. NASDAQ fell -1.79%. 10-year yield rose 0.129 to 4.628.

Fed's Daly stresses patience on rate cuts, no urgency required

San Francisco Fed President Mary Daly emphasized a cautious approach to interest rate reductions. Given the current economic and labor market strength, coupled with persistently high inflation rates, she highlighted the lack of urgency to lower interest rate policy.

"The worst thing to do is act urgently when urgency is not required," Daly remarked at an event.

Daly also expressed her reservations about the consequences of misjudging the necessary intensity of policy adjustments. She requires more evidence of inflation consistently moving towards 2% target before considering easing monetary policy.

China's GDP grows 5.3% yoy in Q1, but March data weak

China's GDP grew 5.3% yoy in Q1, above expectation of 5.0% yoy. Comparing to Q4, GDP grew 1.6% yoy. By sector, primary industry was up 3.3% yoy, secondary industry rose 6.0% yoy, tertiary industry rose 5.0% yoy.

In March, retail sales rose 3.1% yoy, below expectation of 5.1% yoy. Industrial production rose 4.5% yoy, below expectation of 6.0% yoy. Fixed asset investment rose 4.5% ytd yoy, above expectation of 4.3%.

USD/CNH is steady after the release with focus on 7.2815 resistance. firm break there will resume whole rebound from 7.0870 and target 100% projection of 7.0870 to 7.2318 from 7.1715 at 7.3163. For now, outlook will stay bullish as long as 7.2354 support holds, in case of retreat.

Looking ahead

UK employment and German ZEW economic sentiment are the main focus in European session. Later in the day, Canada CPI will take center stage. US will release housing starts and building permits, and industrial production.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6422; (P) 0.6458; (R1) 0.6477; More...

AUD/USD's break of 0.6442 support confirms resumption of whole fall from 0.6870. Intraday bias remains on the downside for 61.8% projection of 0.6870 to 0.6442 from 0.6643 at 0.6378. Decisive break there will pave the way to 0.6269 low, and possibly further to 100% projection at 0.6215. On the upside, above 0.6429 minor resistance will turn intraday bias and bring consolidations, before staging another fall.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which is still in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 02:00 | CNY | GDP Y/Y Q1 | 5.30% | 5.00% | 5.20% | |

| 02:00 | CNY | Retail Sales Y/Y Mar | 3.10% | 5.10% | 5.50% | |

| 02:00 | CNY | Industrial Production Y/Y Mar | 4.50% | 6.00% | 7.00% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Mar | 4.50% | 4.30% | 4.20% | |

| 06:00 | GBP | Claimant Count Change Mar | 17.2K | 16.8K | ||

| 06:00 | GBP | ILO Unemployment Rate (3M) Feb | 4.00% | 3.90% | ||

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Feb | 5.50% | 5.60% | ||

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Feb | 6.10% | |||

| 09:00 | EUR | Eurozone Trade Balance (EUR) Feb | 27.3B | 28.1B | ||

| 09:00 | EUR | Germany ZEW Economic Sentiment Apr | 35.1 | 31.7 | ||

| 09:00 | EUR | Germany ZEW Current Situation Apr | -80.5 | |||

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Apr | 37.2 | 33.5 | ||

| 12:30 | CAD | CPI M/M Mar | 0.70% | 0.30% | ||

| 12:30 | CAD | CPI Y/Y Mar | 2.80% | |||

| 12:30 | CAD | CPI Median Y/Y Mar | 3.00% | 3.10% | ||

| 12:30 | CAD | CPI Trimmed Y/Y Mar | 3.20% | 3.20% | ||

| 12:30 | CAD | CPI Common Y/Y Mar | 3.10% | 3.10% | ||

| 12:30 | USD | Building Permits Mar | 1.51M | 1.52M | ||

| 12:30 | USD | Housing Starts Mar | 1.48M | 1.52M | ||

| 13:15 | USD | Industrial Production M/M Mar | 0.40% | 0.10% | ||

| 13:15 | USD | Capacity Utilization Mar | 78.50% | 78.30% |