Sample Category Title

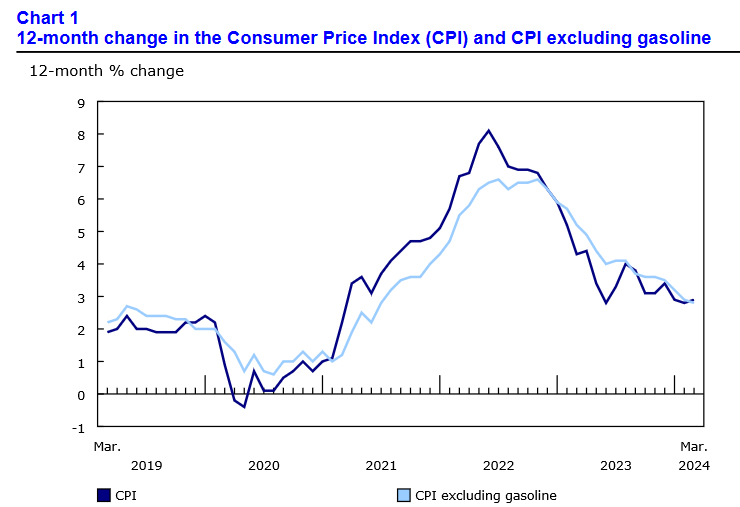

Canada’s CPI edges up to 2.9%, but core measures slow

In March, Canada's CPI saw a slight increase, rising from 2.8% yoy to 2.9% yoy. However, when excluding gasoline, CPI actually slowed from 2.9% yoy to 2.8% yoy.

A closer look at the components reveals that services prices experienced a sharper increase, rising from 4.2% yoy to 4.5% yoy. This outpaced the change in goods prices, which decelerated slightly from 1.2% yoy to 1.1% .

Further dissecting the inflation data, the core inflation measures indicated a cooling trend. Median CPI decreased from 3.0% yoy to 2.8% yoy, while Trimmed CPI reduced slightly from 3.2% yoy to 3.1% yoy. Additionally, Common CPI, which tracks common price changes across categories, also slowed from 3.1% yoy to 2.9% yoy.

Currency War and Geopolitical Risk are Deadly Concoctions for Risk Assets

- The odds have inched higher for a currency war scenario where the Chinese yuan may be weakened further to drive export growth due to its latest decelerating growth trend in China’s retail sales and persistent weak housing prices.

- Export-oriented countries may be forced to enact “beggar-thy-neighbour” typed monetary policies to deliberately weaken their respective currencies.

- A heightened currency war-liked scenario is likely to trigger another layer of US dollar strength.

- A persistent US dollar strength may not bode well for global stock markets in the medium term.

China’s domestic economy has continued to be in the doldrums as growth in retail sales for March decelerated significantly to 3.1% y/y from 5.5% y/y in February, its softest pace of gain since July 2023 and below consensus expectations of 4.5% which suggests that China’s consumer confidence has remained lackluster due to the year-long plus of deflationary risk spiral.

A persistently weak housing market supports the ongoing presence of deflationary pressures in China as the latest data of new home prices for March continued to tumble by 2.2% y/y, faster than a 1.4% y/y drop recorded in February. So far, it has been nine consecutive months of decline in home prices and its steepest pace since August 2015.

Home properties form a significant store of wealth for China’s citizens, triggering an adverse wealth effect on consumer confidence and spending in the past two years.

A weaker Chinese yuan is likely the solution to offset weak domestic demand

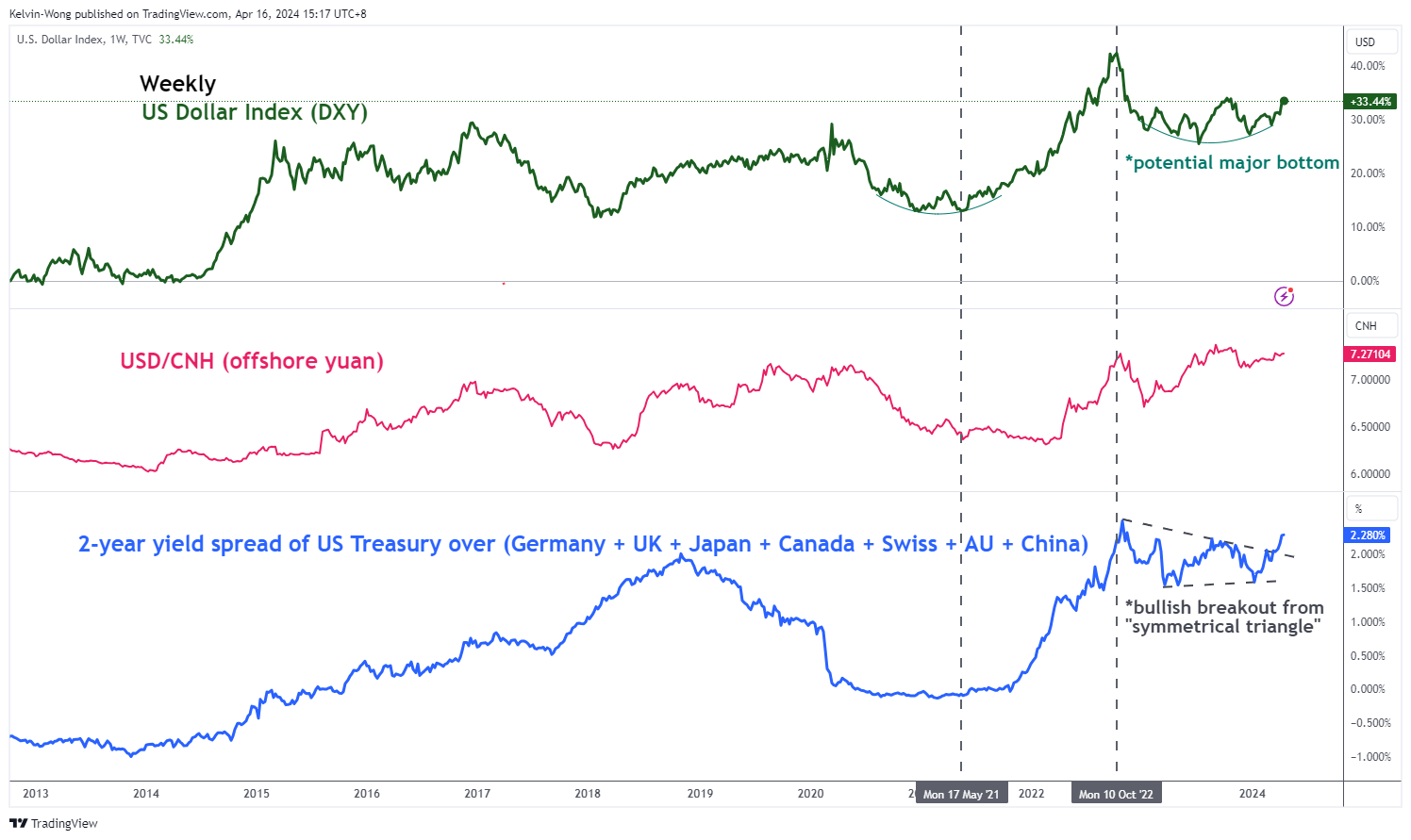

Fig 1: Major trends of US Dollar Index, USD/CNH & 2-YR US Treasury yield spread over rest of the world as of 16 Apr 2024 (Source: TradingView, click to enlarge chart)

China’s top policymakers have set a lofty GDP growth target of around 5% for this year and with the reluctance to deploy significant fiscal and monetary stimulus measures to jump-start internal demand; the other avenue to achieve such an economic growth trajectory is via the external sector from exports growth through a devaluation of the yuan.

A persistent bout of yuan weakness coupled with the US Federal Reserve’s current less dovish stance versus other major developed nations’ central banks is likely to create another layer of US dollar strength via an increase in yield premiums of US Treasuries over the rest of the world sovereign bonds (see Fig 1).

Asian stock indices are likely to continue to face downside pressure in a weak yuan environment

Fig 2: USD/CNH major & medium-term trends as of 16 Apr 2024 (Source: TradingView, click to enlarge chart)

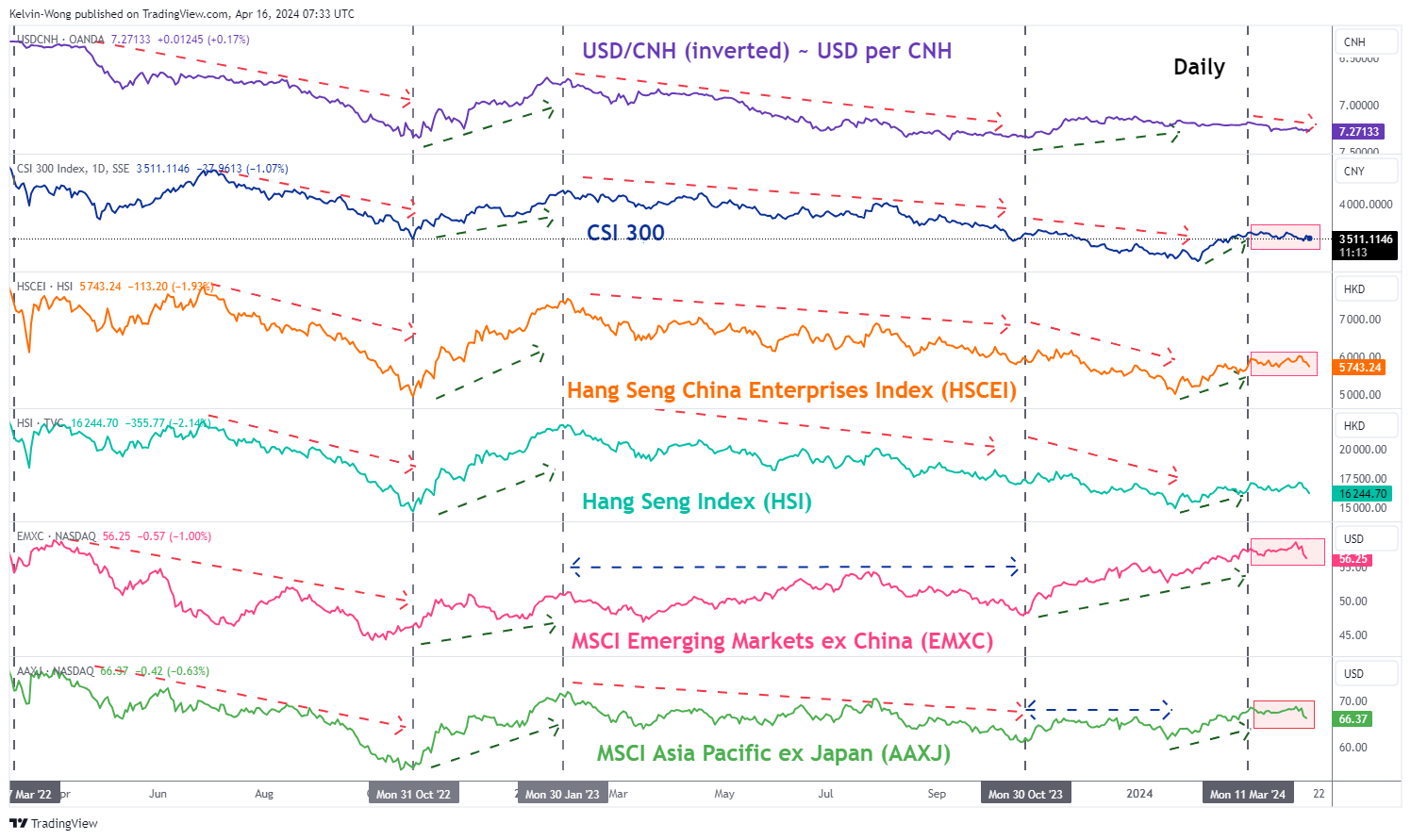

Fig 3: CNH/USD direct correlation with CSI 300, HSCEI, HSI, EMXC & AAXJ as of 15 Apr 2024 (Source: TradingView, click to enlarge chart)

In our previous article dated 25 March 2024, we wrote about the potential bearish implications on the Hang Seng stock indices and China’s CSI 300 triggered by a weakening offshore yuan (CNH) trend. Click here for a recap.

In the past week, the USD/CNH has traded firmly above its upward-slopping 50-day and 200-day moving averages, and in today’s Asian session, it probed again the key near-term resistance of 7.2770. A clear break above 7.2770 is likely to revive a potential bullish impulsive upmove sequence of the USD/CNH within its major uptrend phase (yuan weakness) (see Fig 2).

Hence, an adverse feedback loop is likely to take form as major exporting countries such as South Korea, Taiwan, Malaysia, and Singapore may face the pressure to engage in “beggar-thy-neighbour” currency war-liked monetary policies (deliberately weaken their respective domestic currencies) to maintain export competitiveness.

All in all, a persistent trend of Chinese yuan (CNH) weakness is likely to increase the odds of an impending medium-term bearish trend in Asian stock indices as indicated by the recent movements of the MSCI Asia Pacific ex Japan exchange-traded fund (AAXJ) since 11 March 2024 (see Fig 3).

The US stock market is unlikely to be immune from a persistent strong US dollar trend

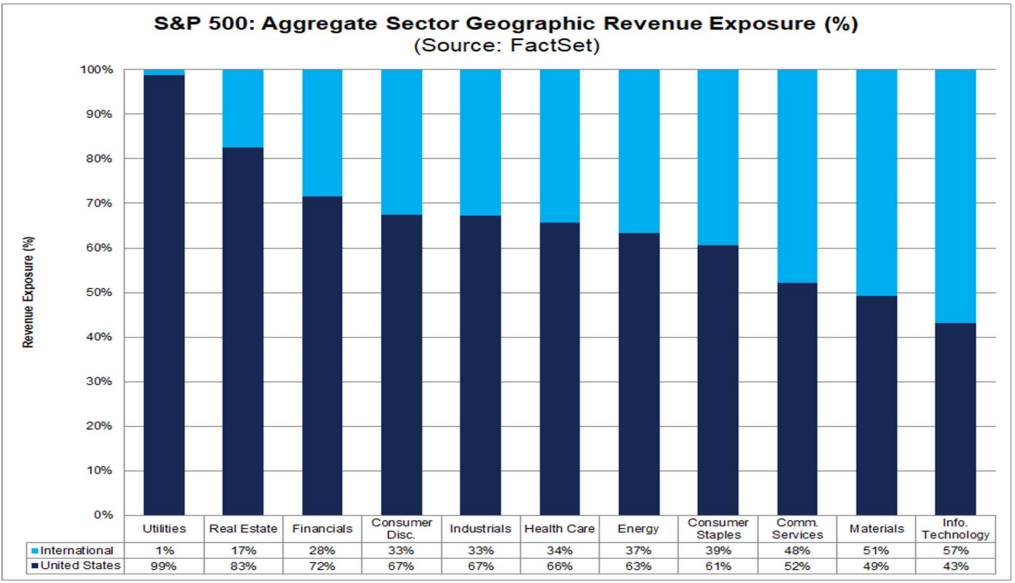

Fig 4: S&P 500 11 industry sectors’ geographical revenue weightage (Source: FactSet as of 12 Apr 2024, click to enlarge chart)

Fig 5: Major trend of S&P 500 with US Dollar Index as of 15 Apr 2024 (Source: TradingView, click to enlarge chart)

The S&P 500, a key benchmark stock index in the US as well as globally, is made up of the top 500 companies from eleven industry sectors, and the Information Technology sector has the highest skewed weightage of around 30% in terms of market capitalization.

Therefore, the price action movements of technology stocks within the S&P 500 will have a much more significant impact on the directional bias of the S&P 500 which can also trigger pronounced feedback loops into the wider US stock market.

Based on the latest data from FactSet as of 12 April, the Information Technology sector of the S&P 500 has the highest portion of aggregate revenue derived from international markets standing at 57% which suggests that any significant US dollar appreciation against the rest of the world currencies will likely to have a negative drag on the total revenue flows of US technology stocks when converted back to US dollars in terms of financial reporting (see Fig 4).

In addition, the previous recent episodes of persistent US dollar strength (represented by the movements of the US Dollar Index) seen from January 2022 to October 2022, and July 2023 to October 2023 have corresponded with significant corrections of -27% and -11% inflicted on the S&P 500 over the similar periods (see Fig 5).

We have written several articles on the S&P 500 that highlighted the risk of an impending medium-term corrective downmove sequence, the latest one was published on 8 April, click here for a recap.

So far, the S&P 500 has dropped by -4% from its current all-time high of 5,265 printed in late March, and yesterday, 15 April it recorded a close below its 50-day moving average for the first time since 2 November 2023.

Perhaps, a looming persistent US dollar strength may be the final death knell to kickstart the potential medium-term corrective decline in the US S&P 500 which may transform into a negative cascading waterfall effect on global stock markets.

CADJPY Elliott Wave : Forecasting the Rally After 3 Waves Pull Back

In this technical blog we’re going to take a quick look at the Elliott Wave charts of CADJPY , published in members area of the website. As our members know we are favoring the long side in YEN pairs. Recently the pair has given us 3 waves pull back that found buyers right at the equal legs area. In the further text we are going to explain the Elliott Wave forecast.

CADJPY H4 Weekend Update 04.13.2024

CADJPY is giving us 4 red pullback against the 108.653 low. The current outlook indicates that the pullback may be evolving as an Elliott Wave Expanded Flat pattern. It’s crucial to observe that the extreme zone has already been reached at 111.168-110.358. We anticipate buyers to emerge in this area, potentially driving a further rally towards new highs or at least generating a three-wave bounce.

CADJPY H4 Update 04.13.2024

CADJPY has given us a nice reaction from the Equal Legs-Buyers zone as expected. We count wave 4 red pullback completed at the 110.854 low. Now, we would like to see a break of the 3 red peak to confirm that the next leg up is in progress. We don’t recommend selling the pair in any proposed pullback, and favor the long side.

GBP/USD Dips After Weak Employment Data

The British pound dropped 0.30% after today’s UK employment report but has recovered most of these losses. In the European session, GBP/USD is trading at 1.2452, up 0.05%.

UK job growth slides, unemployment rises

The UK employment report was weaker than expected. Job growth took a hard hit in the three months to February as the economy shed 156,000 jobs, following a 21,000 decline in the previous period. The market forecast of 110,000 new jobs was nowhere near the mark. As well, the unemployment rate rose to 4.2% in the three months to February, up from 4% in the period through January, the highest level since mid-2023.

The soft job numbers show that the labor market has cooled down due to the Bank of England’s prolonged rate policy of “higher for longer”, which has kept the cash rate of 5.25%. However, the employment report also indicated that pay growth remains stubbornly high, as it ticked lower to 6.0% in the three months to February, compared to 6.1% in the previous period.

This puts the BoE in a bind, as the labor market is cooling but wage growth, a driver of inflation, remains sticky. The BoE is under pressure to help provide relief to the private sector by lowering rates but is concerned that inflation could rebound if it moves to early.

The markets expect the BoE to pause at the May meeting with June a possible date for a first rate cut. The BoE decision will be dependent on the data and Wednesday’s inflation report will be part of that decision. Inflation is expected to have dropped to 3.1% y/y in March, down from 3.4% in February.

GBP/USD Technical

- GBP/USD tested support at 1.2421 earlier. Below, there is support at 1.2397

- There is resistance at 1.2460 and 1.2484

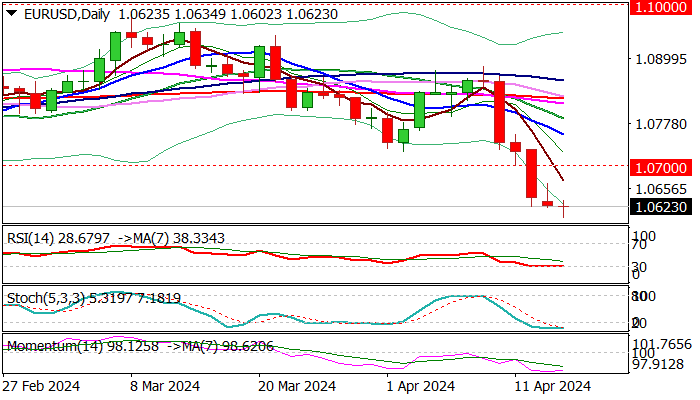

EUR/USD: Limited Consolidation to Precede Fresh Push Lower

EURUSD edges higher from new 5 ½ month low 1.0602) on Tuesday, as strongly oversold daily studies prompted profit-taking.

Near-term sentiment turned fully bearish, and the action weighed by a large weekly bearish candle (the par was down 1.8% last week).

Upticks should provide better selling levels, with solid barriers at 1.0700 zone (former low of Feb 14 / psychological / Fibo 38.2% of 1.0885/1.0602 bear-leg) to ideally cap.

Violation of pivots at 1.0600 zone (fresh low / Fibo 38.2% of 1.0052/1.1275 rally) to open way for test of weekly cloud base (1.0502) and Oct 13 low (1.0495).

Res: 1.0665; 1.0695; 1.0710; 1.0743.

Sup: 1.0602; 1.0516; 1.0495; 1.0448.

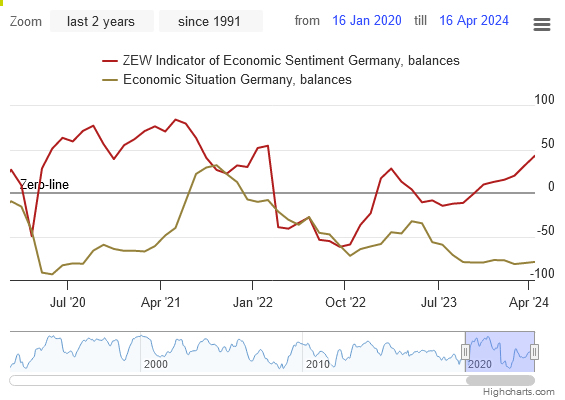

German ZEW jumps to 42.9, euro’s depreciation helps

German ZEW Economic Sentiment jumped from 31.7 to 42.9 in April, well above expectation of 35.1, and marks the highest level since March 2022. But Current Situation Index improved just slightly from -80.5 to -79.2.

Eurozone ZEW Economic Sentiment also surged from 33.5 to 43.9, above expectation of 37.2. Current Situation Index climbed 6.0 pts to -48.8.

ZEW President Achim Wambach noted, "A recovering global economy is boosting expectations for Germany, with half of the respondents anticipating the country's economy to pick up over the next six months."

This optimism is largely driven by improved assessments of the economic situations in Germany's major export destinations. The positive outlook is further buoyed by the expected "appreciation of the US dollar against the euro", which could benefit Eurozone exporters by making their goods more competitive in international markets.

NZD Hits Five-Month Low Against Strong US Dollar

The New Zealand dollar has plummeted to a five-month low, with the NZD/USD pair touching the 0.5890 mark. This decline was triggered by the release of robust American retail sales data, which raised concerns that the Federal Reserve might delay interest rate cuts expected in 2024.

The prevailing expectation in the stock market is that the Fed will begin its monetary policy easing cycle in September, diverging from the earlier forecast of June. This expectation adjustment has bolstered the US dollar's position, exerting additional pressure on other currencies.

The Reserve Bank of New Zealand (RBNZ) has maintained its interest rate steady for six consecutive meetings, including a neutral stance in its April meeting. The central bank's primary objectives are alleviating production capacity pressures and mitigating inflation's economic impact. Despite signs of weakening economic activity, New Zealand's annual inflation rate dropped to 4.7% in the quarter ending December – the lowest since Q2 2021. However, inflation remains significantly above the RBNZ's 1-3% target range.

There are indications that the New Zealand economy entered a technical recession in Q3 2023, with more recent data still awaited.

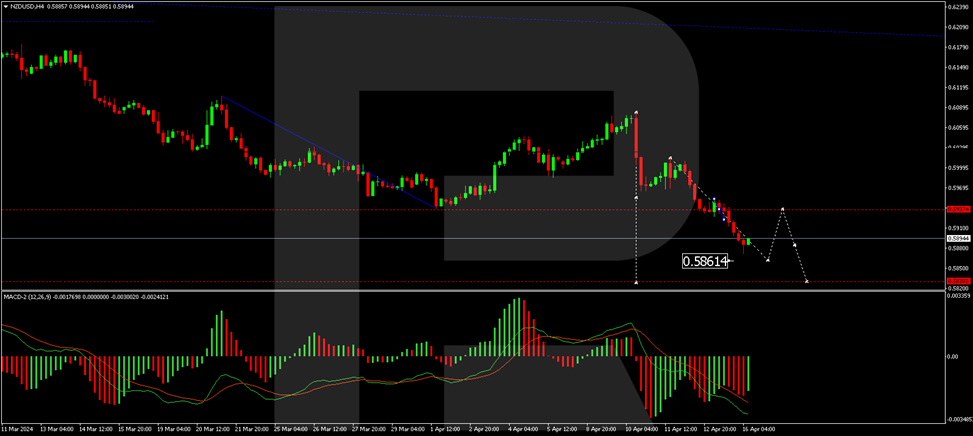

Technical analysis of NZD/USD

The H4 chart of NZD/USD shows that a consolidation range was established around the 0.5937 level, followed by a downward move to 0.5872. A corrective move back to 0.5900 is possible (testing from below), after which a further decline to 0.5830 is anticipated. This bearish scenario is supported by the MACD indicator, with its signal line positioned below zero and pointing downwards.

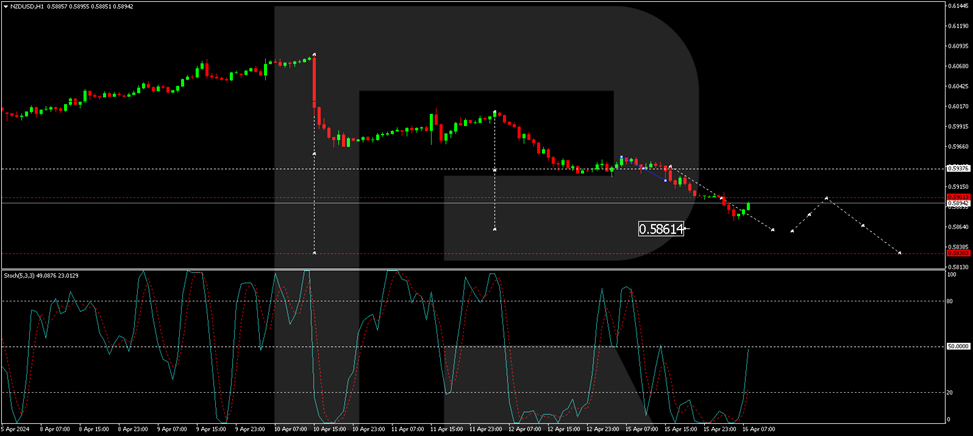

On the H1 chart, the NZD/USD pair continues its downward trajectory towards 0.5854. After completing the decline to 0.5872, a corrective movement to 0.5900 is likely. Subsequently, a new downward phase could target 0.5854, potentially extending towards 0.5830. This outlook is confirmed by the Stochastic oscillator, currently below 20, with an expected rise to 50, indicating the potential for a temporary corrective upswing before continuing the downward trend.

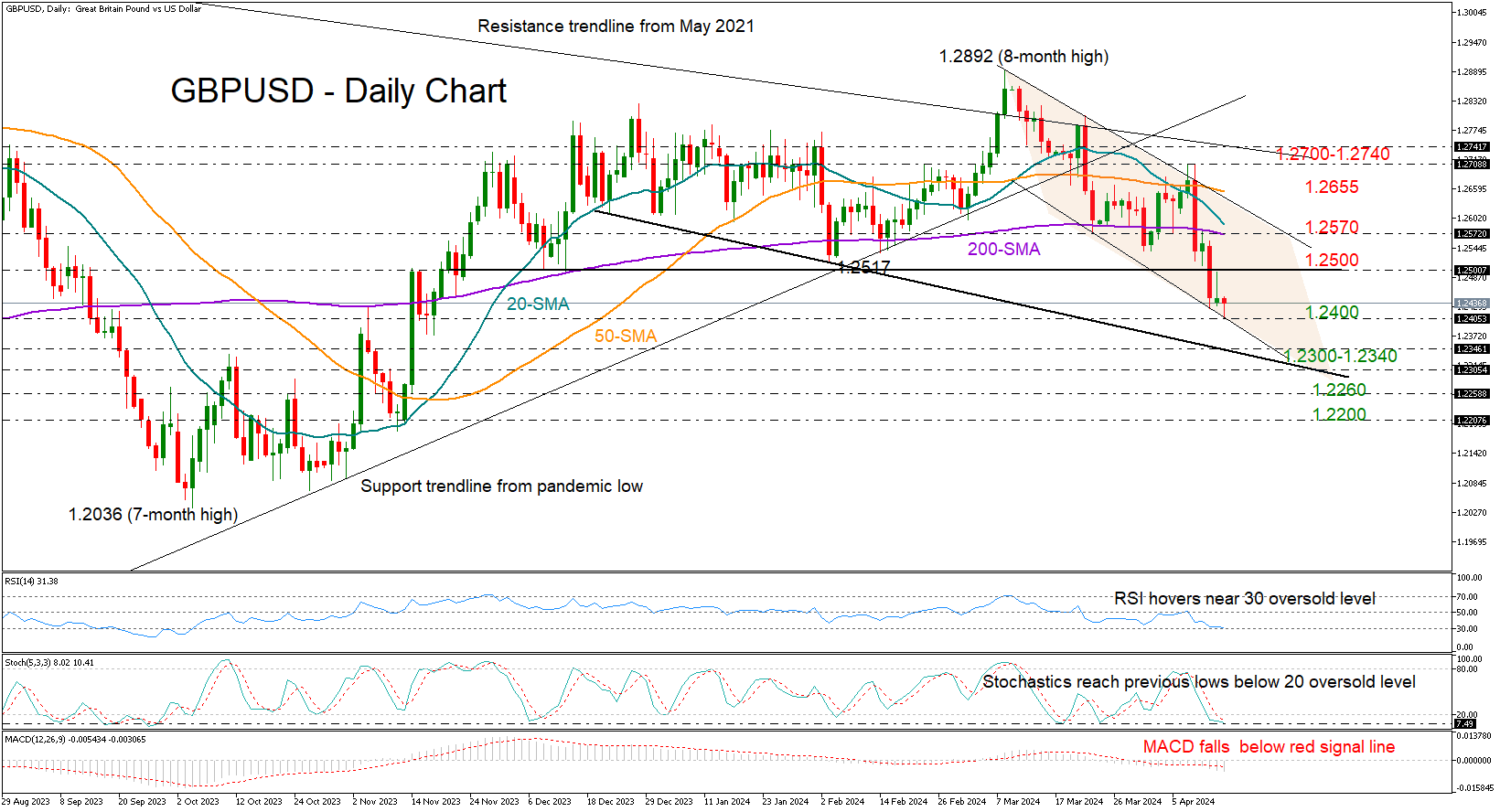

GBPUSD Pulls Back into the Negative Zone

- GBPUSD inches down to a new five-month low

- An extension below 1.2400 could generate fresh selling interest

GBPUSD tried to breach the psychological barrier at 1.2500 and re-establish itself within the 1.2488-1.2892 range. But its efforts proved unsuccessful, with the pair charting a new lower low of 1.2405 during Tuesday’s early trading hours – the lowest level since November 2023.

The bears might take a breather soon as the stochastic oscillator has reached its previous support area below 20, and the RSI is hovering around the 30 oversold level, suggesting the bulls could be on their way.

However, the short-term outlook will remain negative until the price runs sustainably above the downward-sloping channel and the 50-day SMA at 1.2655. Discouragingly, the weakening SMAs and the narrowing gap between the 20- and 200-day SMAs are currently dampening hopes for a bullish trend reversal. Nonetheless, if the bulls succeed in taking charge above 1.2655, the spotlight will shift to the 1.2700-1.2740 level. Another victory there is expected to result in a test near the broken support trendline from the pandemic low near 1.2820.

If selling forces persist, the pair could tumble towards the tentative support line at 1.2340, while a steeper decline could even challenge the 1.2300 round level. A continuation lower could then examine the former constraining region of 1.2260 ahead of the 1.2200 psychological mark.

In summary, the rejection near the 1.2500 number on Tuesday suggested the bearish wave has yet to bottom out. While some consolidation cannot be excluded, a close below 1.2400 could clear the way towards 1.2340.

Frightened Crypto Market Chooses a Path

Market picture

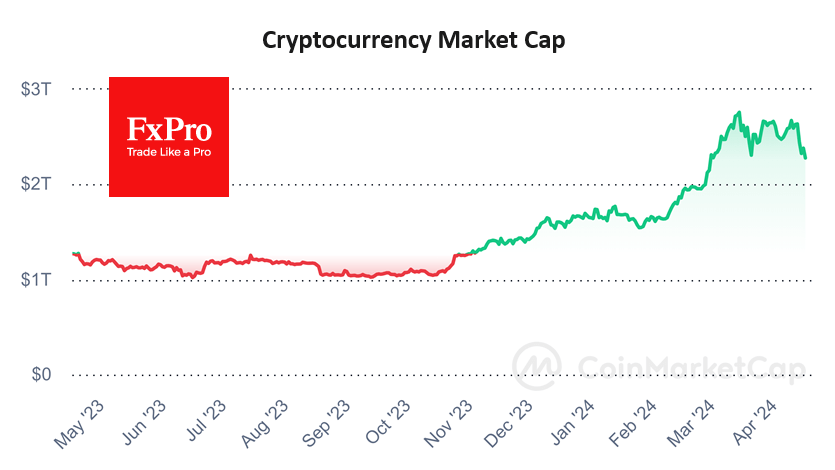

The sell-off in US stock markets affected global risk appetite late on Monday, reversing initial positivity. As a result, crypto market capitalisation fell 5.4% in 24 hours to 2.29 trillion, back near the weekend lows. The market is hovering near the lows of March. This is a key moment in choosing the market’s direction for the coming weeks. A bounce out of this area will allow for the expectation of an early recovery to the recent highs. A dip below would likely trigger a broader liquidation of positions.

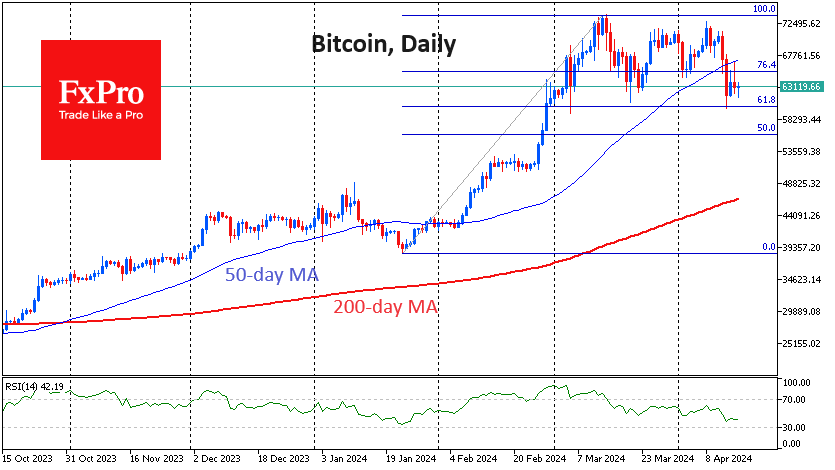

Bitcoin has returned to the area of the lows of the past seven weeks, coinciding with the 61.8% retracement level of the rally from the January lows. Like the crypto market, Bitcoin is choosing between a loosely controlled deepening of the decline or a reversal to growth. On the negative side, the 50-day moving average triggered resistance on Monday.

According to CoinShares, crypto fund investments fell by $126 million last week after inflows of $646 million a week earlier; the small outflow came after two weeks of growth in the index. Bitcoin investments decreased by $110 million, Ethereum – by $29 million, and Solana – by $4 million.

News background

If Bitcoin falls below short-term holders’ support at $58,900, the market risks going into a bearish phase, said analyst and CMCC Crest co-founder Willie Wu. He noted that almost every cycle prior to halving has seen a bear phase due to the ‘overaccumulation’ of the first cryptocurrency.

As a result of the Bitcoin halving, only 20 per cent of the world’s mining companies will be able to maintain their revenues at levels comparable to the previous period, TheMinerMag calculated. As a result, the mining industry could lose around $10 billion a year of revenue.

After the halving, miners could potentially liquidate $5bn worth of Bitcoin inventory, putting pressure on the price, 10x Research warned. The overhang of this sell-off could last four to six months.

The Hong Kong Securities and Futures Commission (SFC) has approved applications to launch spot bitcoin and Ethereum-ETFs. Matrixport estimates that demand for Bitcoin-ETFs in Hong Kong will reach $25bn.

Bitcoin mining companies will try to mine the first block that appears after the halving to get an ‘epic’ satoshi with an estimated value of several million dollars, CoinDesk reported.

XAU/USD Gold Price Reaches an Important Resistance Zone

The XAU/USD gold chart today indicates that the historical record price of the metal is above USD 2,400 per ounce.

In addition to fears of a new round of inflation due to rising commodity prices, geopolitical tensions are seen as the most important reason for the growth. At the moment, there are both active military conflicts on the planet (Ukraine, Israel-Iran), and there is a threat of creating new ones (Taiwan, for example). The US national debt and upcoming elections may also act as a destabilizing factor.

Therefore, gold acts as a traditional safe-haven asset. According to Goldman Sachs analysts, gold is in an “unshakable bull market”, so they raised their gold price forecast from USD 2,300 to USD 2,700.

Since the beginning of 2024, the price of XAU/USD has risen 15%, setting a new all-time high of USD 2,425. Could the bull run continue further?

Although the fundamental backdrop remains tense, from a technical analysis perspective on gold prices, there are 4 important headwinds to consider:

→ the ascending channel (shown in blue). Today XAU/USD is near its upper line. As the arrow shows, the price of gold reacts to this line as resistance.

→ Psychological round level 2,400. Having exceeded it, the price quickly returned back.

→ The RSI indicator indicates that the market is overbought.

→ Fibonacci proportions. If we take impulse A→B as 100%, then the impulse price growth from point C has already exceeded the level = 1.618 (around 2,335), which could be the target.

On April 3, we wrote that the price of gold could rise to the level of 2,380. Now, in addition to the listed factors, it is worth taking into account the motive of some traders to take profits after a period of rising prices, which may contribute to the formation of a correction in the market - for example, to the lower intermediate channel lines (shown in black).

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.