Sample Category Title

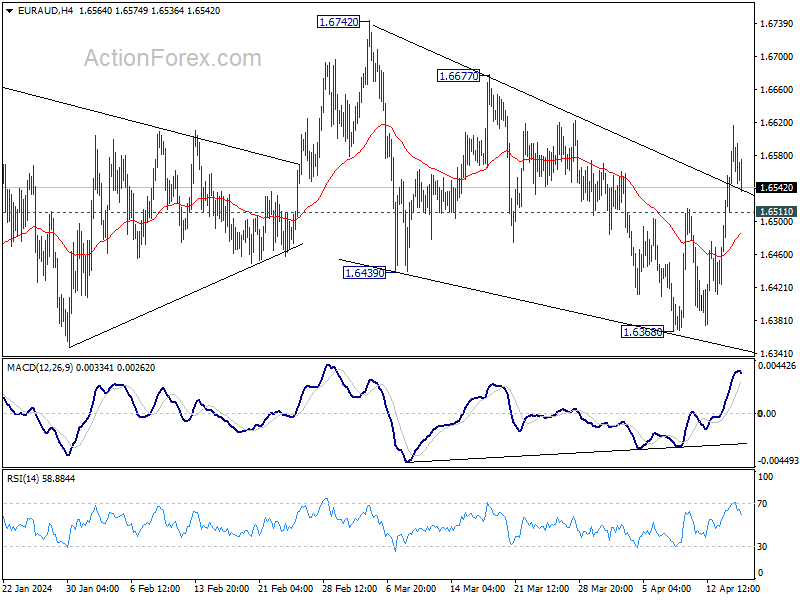

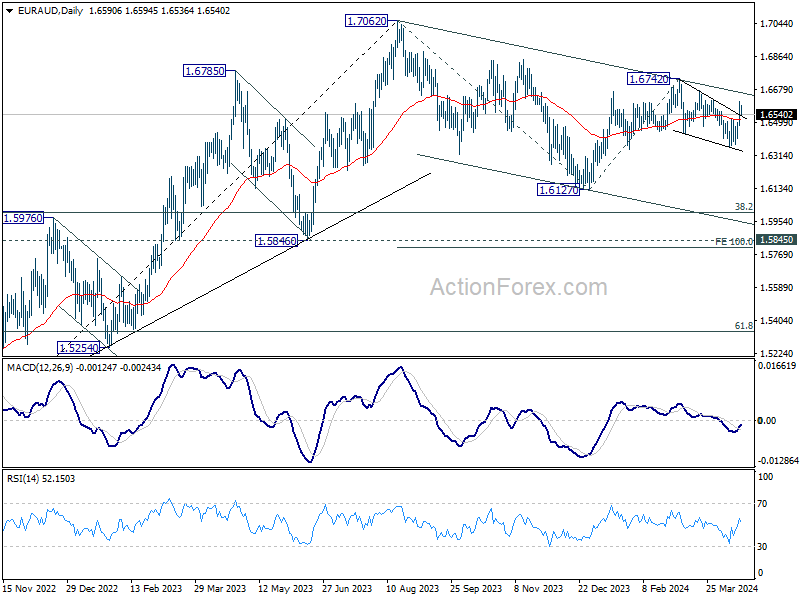

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6502; (P) 1.6560; (R1) 1.6648; More...

Intraday bias in EUR/AUD stays mildly on the upside at this point. Rise from 1.6368 would target 1.6677 resistance next. Break there will confirm that correction from 1.6742 has completed, and bring further rally through this high. On the downside, though, below 1.6511 minor support will turn intraday bias neutral again first.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). The correction is probably still in progress with fall from 1.6742 as the third leg. Strong support is expected around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

Oil Risks Remain Tilted to the Upside

He said it. Federal Reserve (Fed) President Jerome Powell said that the Fed may delay its first rate cut due to the lack of progress in cooling inflation following a rapid decline observed by the end of last year. The three straight month of rising inflation in the US convinced the Fed Chair - as many other Fed members - that cutting the interest rates in summer may be a bad idea.

On a side note, I saw a Bloomberg article suggesting that the rate hikes in the US boosted the economy instead of pushing it into recession as many economic actors have their borrowing costs locked at low levels but benefit from rising interest on their savings etc. But the Fed’s balance sheet -which is trending lower but remains significantly higher compared to the pre-pandemic levels, and the massive fiscal spending from the US - with national debt rising at a sustainable speed toward the $35 trillion mark, explain why the US economy is performing so well despite higher rates.

Anyway, the June rate cut expectation fell to around 15%, the July cut expectation retreated to around 41%, the US 2-year yield jumped past the 5% level, where it sees some resistance, as BoFA’s MOVE index, which is a gauge of volatility in US treasuries, is on a rise. I believe that we will see the 2-year yield fluctuate between 4.75/5.25% range as the Fed will bring the ‘higher for longer’ rhetoric back on the table.

For the FX

… it means that the US dollar has room for more gains, provided the Fed’s major peers don’t share the same inflationary worries than the Fed does. They are, on the contrary, sticking to their rate cut plans into this summer. The Bank of England (BoE) Governor Bailey said yesterday that the UK might be able to lower its rates before the Fed as the inflation dynamics in their economies diverge. The selloff in Cable accelerated, as the pair tested the 1.24 level on the back of loosening jobs numbers but the wages growth remained stubbornly high. Inflation numbers released this morning in the UK showed further easing in both headline and core inflation, though both figures came in slightly higher than expected by analysts. Cable made a very small positive attempt just after the data but the dovish BoE expectations remain intact and UK’s falling inflation toward target strengthens the case for a rate cut sooner rather than later for the BoE. As such, the outlook for Cable remains negative.

Across the Channel, the ECB Chief Christine Lagarde can’t be clearer when she says that the ECB is closing in on a rate cut as long as shocks don’t derail the slowing in inflation. The EURUSD is testing the 1.06 level to the downside ahead of this morning’s inflation data, which is expected to reveal a certain rise on a monthly basis due to rising oil prices and the dollar appreciation, but is expected to continue to fall on a yearly basis. The major risk to the EURUSD and Cable’s bearish trend is indeed a shock – the most obvious being a further jump in oil prices due to rising tensions in the Middle East as Iran is getting involved into the conflict. Also, the dollar appreciation will likely complicate the inflation battle for the rest of the world as the prices of pretty much everything will increase due to a broadly stronger US dollar.

In Japan, the USDJPY is preparing to test the 155 level as traders are left wondering when the Japanese authorities will intervene.

Oil risks remain tilted to the upside

The barrel of US crude remains offered on geopolitical news, or the lack thereof, after Iran attacked Israel this weekend. Israel said at the start of the week that there will be a response, even though the US and allies are putting a lot of effort to prevent a further escalation of tensions with Iran. This being said, Yellen said that there will be more sanctions against Iran for daring to hit Israel. I am not a political expert but the situation in Gaza is already frustrating the supporters of Biden, and I believe that rising tensions in the Middle East on top if it – which would result in higher energy prices - will be offering the presidency on a silver plate to Donald Trump. Therefore, the Biden administration has all the interest in the world to cool tensions, but Israel has been ignoring US’ warnings/recommendations since the beginning of the Gaza conflict. At this point, risks remain tilted to the upside for oil prices. Any escalation with Iran has the potential to send US crude past the $90pb.

Golden hedge

The IMF is optimistic that the world economy will do just fine this year as they upped their growth forecast by 0.1 percentage point to 3.2% this year, but warned that this outlook remain cautious due to persistent inflation and geopolitical risks. And indeed, the latter – persistent inflation and rising geopolitical tensions - keep gold appetite intact near record levels despite rising US yields. Gold is perceived as a good hedge against rising geopolitical tensions and against a potential meltdown in risk appetite due to a more hawkish Fed. Any disappointment in corporate earnings could accelerate the risk selloff and strengthen the gold’s bullish trend.

Focus Turns to Final March Inflation for Euro Area

In focus today

Today, focus is on the final inflation data for March in the euro area. We particularly look out for inflation components that reflect domestic demand as service inflation remained elevated in March. The final data will also allow us to estimate how much the timing of Easter impacted the March numbers and to what extent we should expect an effect on the April numbers.

In Sweden, Deputy Governor Martin Flodén will talk about monetary policy communication in an uncertain world. Since he is one of the board members who has expressed the greatest concern about the SEK it will be interesting to hear what he has to say about the fact that its current development has put it not far from 3% below the Riksbank forecast and made it the worst performer in G10 since the Riksbank March meeting. Last Friday, the low inflation print took its fair toll on the SEK, stressing the Riksbank-SEK correlation, and on Monday the risk-off sentiment pushed EUR/SEK and USD/SEK to new year highs.

We continue to monitor the developments in the Middle East. Yesterday brought no signals in terms of a retaliation from Israel as the war cabinet was still deciding on a response. The cabinet is set to meet again today.

Economic and market news

What happened yesterday

Another day of diverging US/EU rate signals, as Fed chair Powell said that recent data has indicated that "it is likely to take longer than expected" to gain confidence that inflation is on track to target, while the Fed's Jefferson said if inflation proves to be more persistent than expected, the Fed was ready to keep the current stance for longer. Conversely, ECB President Lagarde said the bank was moving towards a moderation of current policy while Bank of France's Villeroy said the ECB should "decide a first rate cut in June" if things developed as expected.

Sanctions against Iran are on the way, as Janet Yellen said the US would use sanctions in conjunction with allies to disrupt Iran's "malign and destabilizing activity". UK PM Rishi Sunak said that the G7 was working on a package of sanctions while German FM Annalena Baerbock said several EU countries were reviewing their current sanctions.

German ZEW showed a continued weak assessment of the current economic situation while expectations for the future economy have risen. This was in line with other indicators suggesting weak near-term growth but that the worst is behind us as the cyclical headwinds have started to turn. Read more in Research Germany - Worst is over in German manufacturing sector, 15 April.

Equities: Global equities were lower again yesterday, despite a slight comeback in the tech sector. Yesterday's sell-off centred around Asia and Europe, mostly reflecting the catch-up to the US cash session on Monday. Interestingly, we saw US yields ticking higher, with the sum of macro data being positive. This is ultimately a positive sign for the economy but presents a short-term challenge for equities, as yields are increasing too much, too fast for equity investors to be confident. After the latest tiny setback in equities, we are now seeing many pundits calling for a high likelihood of correction, but they do not back up their claims with action. In our opinion, it is cheap talk, a sign of uncertainty, and a cover in case equities should turn lower. We see a below-average risk of a correction and a higher likelihood of equities going 10% higher from here than 10% lower.

FI: Absent market significant news, rates traded higher from the long end in a bearish steepening move, in the European trading session. 10y Bunds briefly traded above 2.5% but ended below the mark. Last night, Powell said that the recent data 'have clearly not given us greater confidence and instead indicate that it is likely to take longer than expected to achieve that confidence,' in a pull-back on rate cut expectations and added that due to the labour market strength and inflation progress 'it is appropriate to allow restrictive policy further time to work and let the data and the evolving outlook guide us,'. Market's reaction to the comments was relatively muted. The Dec24 Fed pricing was only 1bp higher to 43bp cut.

FX: Yesterday, we published our monthly in FX Forecast Update - Gear up for prolonged NOK slump, 16 April. We see the case for lower USD rates as we believe markets underestimate the potential for more than one to two rate cuts in 2024. In the near term, this should weigh on the broad USD and in isolation bolster risk sentiment. In the process we see room for a temporary rebound of the risk-sensitive and from a relative-rates perspective oversold SEK. Over the medium term, we still see the USD moving higher. Overnight, EUR/USD has stayed above 1.06 while EUR/SEK and EUR/NOK have been flat around 11.64 and 11.67, respectively. USD/JPY is flat yet elevate at above 154.50 as the market mulls the intervention risk.

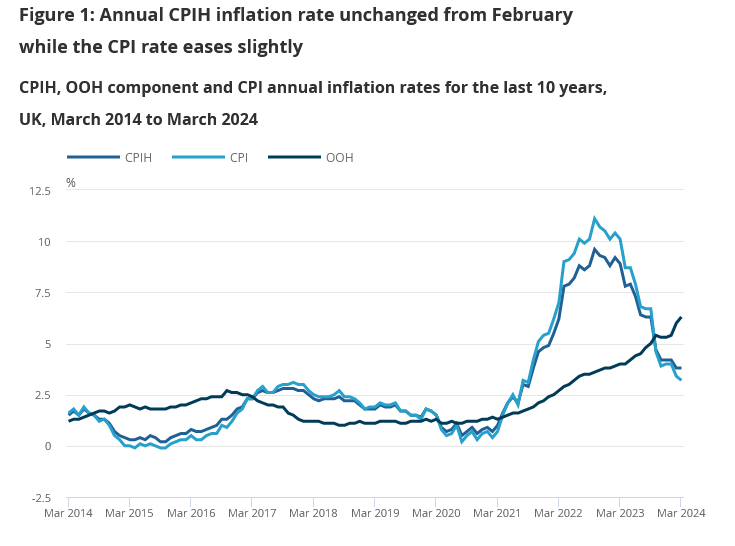

UK CPI slows less than expected to 3.2% yoy in Mar

UK CPI slowed from 3.4% yoy to 3.2% yoy in March, above expectation of 3.1% yoy. CPI core (excluding energy, food, alcohol and tobacco) decelerated from 4.5% yoy to 4.2% yoy, above expectation of 4.1% yoy. CPI goods slowed from 1.1% yoy to 0.8% yoy. CPI serviced eased marginally from 6.1% yoy to 6.0% yoy. For the month, CPI rose 0.6% mom.

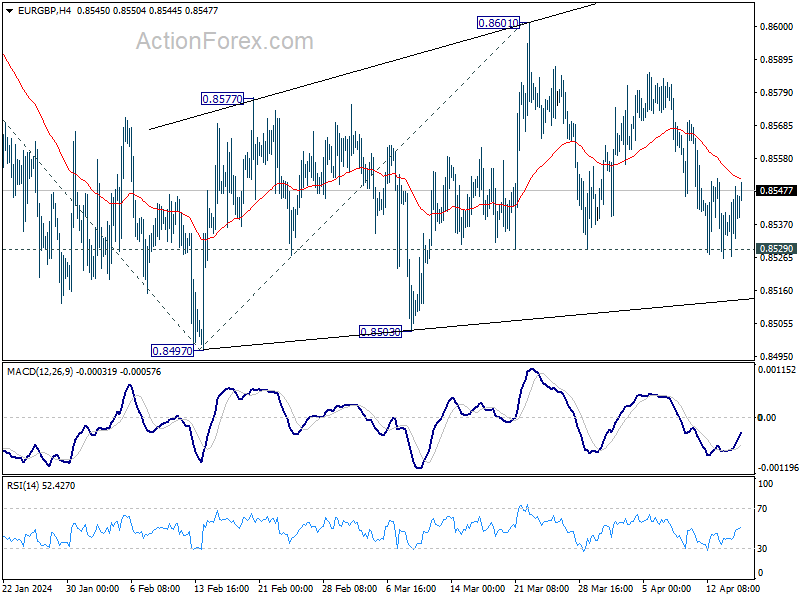

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8533; (P) 0.8541; (R1) 0.8555; More...

Intraday bias in EUR/GBP remains neutral at this point. On the downside, firm break of 0.8529 support will argue that the corrective recovery from 0.8497 has completed at 0.8601. Intraday bias will be back on the downside for retesting 0.8497 low next. On the upside, break of 0.8601 will resume the rebound instead.

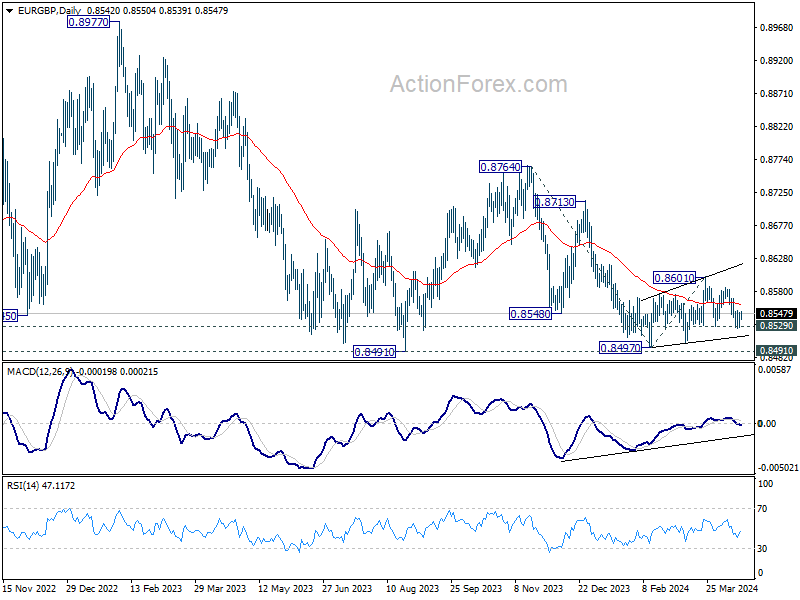

In the bigger picture, there is no clear sign that down trend from 0.9267 has completed, despite loss of downside momentum as seen in D MACD. As long as 0.8601 resistance holds, the down trend will remain in favor to resume through 0.8491 low at la later stage.

Dollar Rally Cooling Off, Kiwi Rebounds Post-CPI

Dollar's rally appeared to be slowing a little despite extended rally in benchmark treasury yields, the selloff in US stocks could be stabilizing too. Fed Chair Jerome Powell's comment that interest rate could stay at current level for longer if inflation persist triggered little reactions in the market. This is actually a given now considering recent strong consumption, inflation, and employment data. Fed's Beige Book report today would likely reinforce the view that the economy remains robust while inflationary pressure is not gone.

New Zealand Dollar recovers broadly today after Q1 inflation data. While headline inflation slowed, it remained well above RBNZ's target band. More importantly, domestic price pressure as seen in non-tradeable inflation remains elevated and made little progress down. It's still a long way before RBNZ could start cutting interest rates.

Sterling is the main focus today as CPI data from UK is featured. BoE Governor Andrew Bailey acknowledged the "strong evidence" that disinflation is working its way through the economy. Continuing progress, if displayed by today's data, would likely give more confidence to BoE for rate reductions later in the year.

Overall for the week, Swiss Franc is currently the best performer, followed by Dollar, and then Euro. Yen is the worst, followed by Aussie , and the Kiwi. Sterling and Canadian Dollar are positioned in the middle.

Technically, NZD/USD should have formed a temporary low at 0.5858 with today's recovery. That came after drawing support from 100% projection of 0.6368 to 0.6037 from 0.6215 at 0.5884, as well as near term falling channel support. Some consolidations would be seen first. Further break of 0.5938 support turned resistance will indicate short term bottoming, and bring stronger rebound.

In Asia, at the time of writing, Nikkei is down -0.06%. Hong Kong HSI is down -0.07%. China Shanghai SSE is up 1.24%. Singapore Strait Times is up 0.49%. Japan 10-year JGB yield is up 0.0061 at 0.879. Overnight, DOW rose 0.17%. S&P 500 fell -0.21%. NASDAQ fell -0.12%. 10-year yield rose 0.031 to 4.659.

Powell asserts Fed will hold rates steady if inflation persists

Fed Chair Jerome Powell acknowledged that recent economic data have not bolstered confidence in disinflation. He signaled the readiness to keep rates elevated for an extended period if inflationary pressure persists.

"Recent data have clearly not given us greater confidence that inflation is coming fully under control. Instead, they indicate that it's likely to take longer than expected to achieve that confidence," Powell said at a conference overnight. .

"Given the strength of the labor market and progress on inflation so far, it is appropriate to allow restrictive policy further time to work," he added.

"If higher inflation does persist, we can maintain the current level of interest rates for as long as needed," Powell noted.

At the same conference, BoC Governor Tiff Macklem said that March inflation data released yesterday suggests that underlying inflationary pressures in Canada continued to ease. He added that the bank is looking for sustained evidence of cooling inflation before starting to cut its interest rates.

BoE's Bailey sees strong evidence of disinflation progress in UK

BoE Governor Andrew Bailey pointed to "strong evidence" that disinflation process is "working its way" through the UK economy, suggesting that the previous monetary tightening is having the intended effects.

"Our judgement with interest rates is how much do we need to see now to be confident of the process," Bailey stated at an IMF conference overnight, indicating that BoE is looking for further signs of sustained disinflation before considering any reductions in interest rates.

Bailey also drew distinctions between the inflation dynamics in the UK and those observed in the US. The UK is still navigating the aftermath of "big supply shocks", including those stemming from the global pandemic and geopolitical tensions, notably the war impacts. He contrasted this with the US, where there is a greater element of "demand-led inflation pressure".

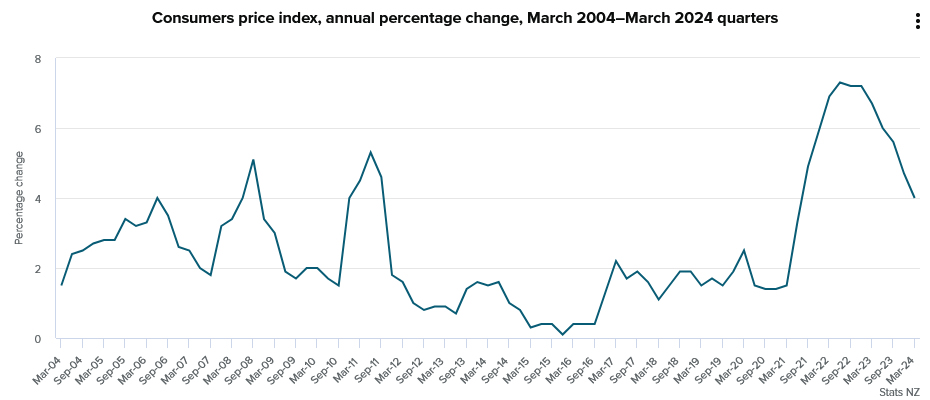

New Zealand's CPI eases to 4.0% yet exceeds target, driven by housing costs

New Zealand CPI rose 0.6% qoq in Q1, while annual inflation rate decelerated from 4.7% yoy to 4.0% yoy. This marks the lowest annual inflation rate since Q2 2021 but still remains above RBNZ's target band of 1-3%.

The most significant pressure on the annual inflation rate came from the housing and household utilities sector. Record increases in rent, which rose by 4.7% yoy, along with 3.3% yoy rise in the construction costs of new houses and 9.8% yoy hike in rates, were the primary drivers behind the sustained inflationary pressures.

In terms of inflation categories, there was a notable divergence between non-tradeable and tradeable inflation. Non-tradeable inflation, which includes goods and services that do not face foreign competition and thus reflect domestic supply and demand conditions, slightly decreased from 5.9% yoy to 5.8% yoy.

In contrast, tradeable inflation, which is influenced by foreign markets and includes goods and services that compete with foreign imports, experienced a more significant slowdown from 3.0% yoy to 1.6% yoy.

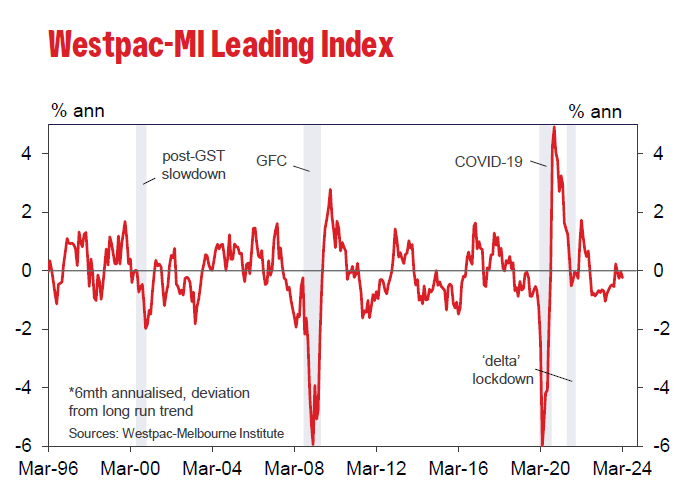

Australia's Westpac leading index indicates sub-trend growth to continue

Australia's economic outlook appears subdued for the remainder of 2024, according to the latest data from Westpac's leading index, which fell from -0.03% to -0.23% in March. This decline signals continuation of "sub-trend" growth, as characterized by Westpac, suggesting that the economic performance may not reach the usual growth standards expected within the country.

Westpac projected that Australia's GDP growth will remain modest at of 1.6% for 2024. This follows a similarly soft performance in 2023, where GDP grew only by 1.5%. Such figures are notably below the typical "trend" growth rate of around 2.5%.

Looking ahead, the focus shifts to the upcoming Q1 CPI data, set to be released on April 24. Westpac anticipates that this report will show deceleration in inflation to 3.5%, a development that could reinforce RBA confidence that inflation is on path back to target range of 2-3%.

However, the decision for RBA to shift to a more definitively "on hold" stance regarding interest rates will hinge on the specifics of the price updates and a broader assessment of risks.

Japan's export rises 7.3% yoy in Mar, fourth month of growth

Japan's exports marked the fourth consecutive month of growth with a 7.3% yoy increase to JPY 9470B in March, slightly surpassing expected 7.0%. This growth was largely fueled by robust performances in automotive and semiconductor & electronic parts, which reported gains of 7.1% yoy and 11.3% yoy respectively. T

Regionally, exports to China accelerated to 12.6% yoy, from just 2.5% yoy in the previous month. However, exports to the US and Europe saw a slowdown, growing at 8.5% and 3.0% respectively.

Import contracted -4.9% yoy to JPY 9103B, which was slightly better anticipated -5.1% yoy. Overall trade balance for March showed a surplus of JPY 366.5B.

In seasonally adjusted term, exports rose 2.6% mom to JPY 8768B. Imports rose 3.9% mom to JPY 9470B. Trade balance came in at JPY -701B.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8533; (P) 0.8541; (R1) 0.8555; More...

Intraday bias in EUR/GBP remains neutral at this point. On the downside, firm break of 0.8529 support will argue that the corrective recovery from 0.8497 has completed at 0.8601. Intraday bias will be back on the downside for retesting 0.8497 low next. On the upside, break of 0.8601 will resume the rebound instead.

In the bigger picture, there is no clear sign that down trend from 0.9267 has completed, despite loss of downside momentum as seen in D MACD. As long as 0.8601 resistance holds, the down trend will remain in favor to resume through 0.8491 low at la later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | CPI Q/Q Q1 | 0.60% | 0.60% | 0.50% | |

| 22:45 | NZD | CPI Y/Y Q1 | 4.00% | 4.70% | ||

| 23:50 | JPY | Trade Balance (JPY) Mar | -0.70T | -0.28T | -0.45T | -0.57T |

| 01:00 | AUD | Westpac Leading Index M/M Mar | -0.10% | 0.10% | ||

| 06:00 | GBP | CPI M/M Mar | 0.60% | |||

| 06:00 | GBP | CPI Y/Y Mar | 3.10% | 3.40% | ||

| 06:00 | GBP | CPI Core Y/Y Mar | 4.10% | 4.50% | ||

| 06:00 | GBP | RPI M/M Mar | 0.80% | |||

| 06:00 | GBP | RPI Y/Y Mar | 4.20% | 4.50% | ||

| 06:00 | GBP | PPI Input M/M Mar | 0.00% | -0.40% | ||

| 06:00 | GBP | PPI Input Y/Y Mar | -2.70% | |||

| 06:00 | GBP | PPI Output M/M Mar | 0.20% | 0.30% | ||

| 06:00 | GBP | PPI Output Y/Y Mar | 0.40% | |||

| 06:00 | GBP | PPI Core Output M/M Mar | 0.20% | |||

| 06:00 | GBP | PPI Core Output Y/Y Mar | 0.20% | 0.30% | ||

| 09:00 | EUR | Eurozone CPI Y/Y Mar F | 2.90% | 2.90% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Mar F | 2.40% | 2.40% | ||

| 14:30 | USD | Crude Oil Inventories | 1.6M | 5.8M | ||

| 18:00 | USD | Fed's Beige Book |

Nikkei (NKD) Has Reached Support Zone

Short term Elliott Wave view in Nikkei Futures (NKD) suggests that rally to 40960 ended wave 3. Pullback in wave 4 is currently in progress as a double three Elliott Wave structure. Down from wave 3, wave (a) ended at 40025 and wave (b) ended at 40805. Wave (c) lower ended at 39285 and this completed wave ((w)) in higher degree. The Index then bounced in wave ((x)) which ended at 40324 as the 1 hour chart below shows.

The Index extended lower in wave ((y)). Internal subdivision of wave ((y)) is unfolding as a zigzag structure. Down from wave ((x)), wave (a) ended at 38815 and wave (b) ended at 39995. Wave (c) lower is in progress as a 5 waves. Down from wave (b), wave i ended at 38830 and wave ii ended at 39540. Wave iii lower ended at 38335 and wave iv ended at 38695. Expect the Index to soon end wave v of (c) of ((y)). This should complete wave 4 in higher degree as well. Afterwards, the Index should extend higher or turn higher in 3 waves at least. The support area comes at 37582 – 38626 blue box area where the Index may potentially find buyers.

Nikkei (NKD) 60 Minutes Elliott Wave Chart

NKD Elliott Wave Video

https://www.youtube.com/watch?v=SUHmqeQ5wiY

Japan’s export rises 7.3% yoy in Mar, fourth month of growth

Japan's exports marked the fourth consecutive month of growth with a 7.3% yoy increase to JPY 9470B in March, slightly surpassing expected 7.0%. This growth was largely fueled by robust performances in automotive and semiconductor & electronic parts, which reported gains of 7.1% yoy and 11.3% yoy respectively.

Regionally, exports to China accelerated to 12.6% yoy, from just 2.5% yoy in the previous month. However, exports to the US and Europe saw a slowdown, growing at 8.5% and 3.0% respectively.

Import contracted -4.9% yoy to JPY 9103B, which was slightly better anticipated -5.1% yoy. Overall trade balance for March showed a surplus of JPY 366.5B.

In seasonally adjusted term, exports rose 2.6% mom to JPY 8768B. Imports rose 3.9% mom to JPY 9470B. Trade balance came in at JPY -701B.

Australia’s Westpac leading index indicates sub-trend growth to continue

Australia's economic outlook appears subdued for the remainder of 2024, according to the latest data from Westpac's leading index, which fell from -0.03% to -0.23% in March. This decline signals continuation of "sub-trend" growth, as characterized by Westpac, suggesting that the economic performance may not reach the usual growth standards expected within the country.

Westpac projected that Australia's GDP growth will remain modest at of 1.6% for 2024. This follows a similarly soft performance in 2023, where GDP grew only by 1.5%. Such figures are notably below the typical "trend" growth rate of around 2.5%.

Looking ahead, the focus shifts to the upcoming Q1 CPI data, set to be released on April 24. Westpac anticipates that this report will show deceleration in inflation to 3.5%, a development that could reinforce RBA confidence that inflation is on path back to target range of 2-3%.

However, the decision for RBA to shift to a more definitively "on hold" stance regarding interest rates will hinge on the specifics of the price updates and a broader assessment of risks.

New Zealand’s CPI eases to 4.0% yet exceeds target, driven by housing costs

New Zealand CPI rose 0.6% qoq in Q1, while annual inflation rate decelerated from 4.7% yoy to 4.0% yoy. This marks the lowest annual inflation rate since Q2 2021 but still remains above RBNZ's target band of 1-3%.

The most significant pressure on the annual inflation rate came from the housing and household utilities sector. Record increases in rent, which rose by 4.7% yoy, along with 3.3% yoy rise in the construction costs of new houses and 9.8% yoy hike in rates, were the primary drivers behind the sustained inflationary pressures.

In terms of inflation categories, there was a notable divergence between non-tradeable and tradeable inflation. Non-tradeable inflation, which includes goods and services that do not face foreign competition and thus reflect domestic supply and demand conditions, slightly decreased from 5.9% yoy to 5.8% yoy.

In contrast, tradeable inflation, which is influenced by foreign markets and includes goods and services that compete with foreign imports, experienced a more significant slowdown from 3.0% yoy to 1.6% yoy.