Sample Category Title

EURGBP’s Double Bottom Still Waits for Confirmation

- EURGBP faces difficulty in completing a double bottom pattern above 0.8579

- Technical indicators reflect a lack of bullish momentum

- ECB rate decision could generate fresh volatility at 12:15 GMT

- ECB governor Lagarde holds press conference at 14:15 GMT

EURGBP drifted lower after it got another rejection from November’s resistance trendline and the 38.2% Fibonacci retracement of December-February downleg at 0.8579 earlier this week.

The series of higher lows that began in March and the rising 20-day simple moving average (SMA), which is currently distancing itself above the 50-day SMA, are maintaining optimism that the double bottom pattern around 0.8500 could develop into a bullish trend above 0.8579. The negative momentum in the technical indicators, however, suggests that any potential improvement could come with some delay.

If the price closes clearly above 0.8589, the 200-day SMA could be the next obstacle near the 50% Fibonacci mark of 0.8600. A break higher could peak within the 0.8620-0.8630 region, which includes the 61.8% Fibonacci level, or pick up steam towards the 78.6% Fibonacci of 0.8670.

In the event the bears squeeze the price below the nearby 0.8550 support area, where the 23.6% Fibonacci and the 50-day SMA are placed, the spotlight will fall on the 0.8528 restrictive zone. A step lower would violate the bullish double bottom pattern, bringing the critical base of 0.8500 under examination. If the bears resume the downtrend below that floor, selling pressures could intensify towards the 0.8400-0.8435 area.

Summing up, EURGBP cannot warrant an immediate bullish breakout above the tough 0.8579 barrier, despite the improved trend signals. Yet, only a slide below 0.8528 would increase selling interest.

What’s Behind the US Economy’s Resilience?

- US economy is still sizzling, outperforming other regions

- Several factors behind this strength, such as heavy public spending

- For US dollar to enjoy a massive rally, it may also need risk aversion

Why is the US economy still so strong?

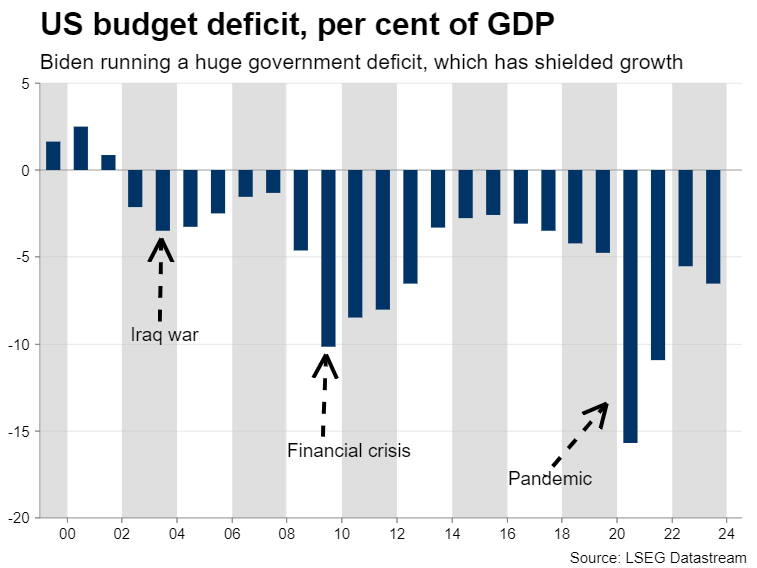

One of the most striking developments over the past year has been the extraordinary resilience of the US economy, despite the highest interest rates in a generation. The United States grew 2.5% last year, much faster than any other advanced economy, and by all indications continues to outperform in early 2024.

Several elements lie behind this strength. First and foremost, the US government is running an astronomical budget deficit, which amounted to more than 6% of GDP last year. This enormous public spending has shielded economic growth, but has also raised concerns about debt sustainability.

In contrast, most European nations are running much smaller deficits, which helps explain why growth in the euro area has been so anemic lately.

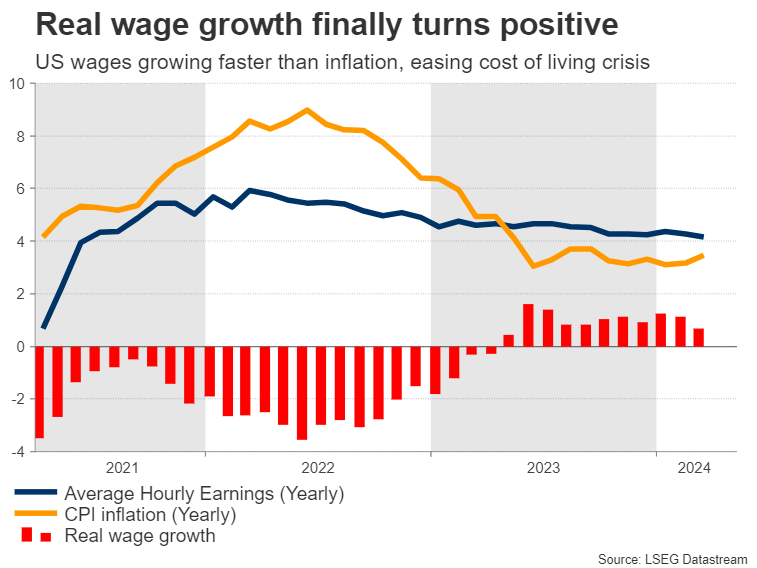

Immigration flows have powered the US economic machine too. With an influx of migrant workers coming in, the labor market continues to boom, cushioning consumer spending. And with wage growth finally surpassing inflation, the cost of living crisis has started to ease.

How the loan market is structured played a huge role as well. In the US, most mortgages are given at a fixed rate for 30 years. As such, many people locked in extremely low borrowing costs during the pandemic, insulating them from the sharp increase in interest rates that ensued.

Most other countries operate with adjustable rate mortgages, where payments reset every few years depending on interest rates. Therefore, many homeowners in Europe have started to pay higher monthly costs on their loans, squeezing spending even further.

Beyond all of this, America’s energy independence also helped safeguard consumers from the worst effects of soaring oil and gas prices following the invasion of Ukraine.

So why hasn’t the dollar skyrocketed?

With the US economy being stronger than other regions, this begs the question of why the dollar hasn’t mounted a tremendous rally. If the market was purely trading economic fundamentals, the dollar seems like the most attractive G10 currency at this stage.

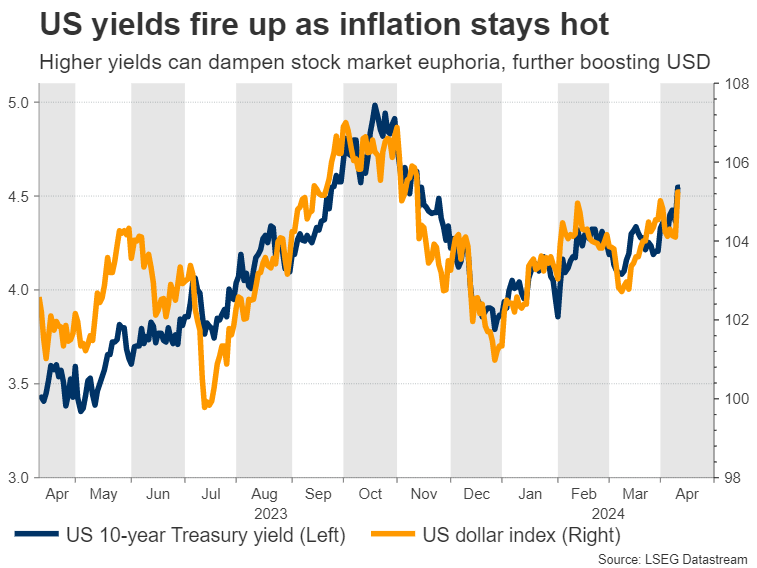

It appears that developments in other financial markets have been holding the dollar back. The dollar often acts like a safe haven asset, since it is the world’s reserve currency. As such, the recent euphoria in stock markets has probably curbed demand for the greenback, preventing it from staging a fierce rally.

Another ‘problem’ for the dollar has been the collapse in natural gas prices, mostly because that is bullish for the euro. The Eurozone imports nearly all its gas, so when prices drop so dramatically, the euro receives a boost through the trade channel. This has allowed the euro to remain above water despite a deteriorating economy, in turn limiting the dollar’s advances.

What’s next?

Looking ahead, we seem to be entering a period where the resilience of the US economy translates into persistently hot inflationary pressures, which might delay any rate cuts by the Federal Reserve.

The latest readings on inflation and the labor market certainly pointed in this direction, boosting the dollar in the process as traders dialed back on their rate-cut bets.

But if the price action over the last few months is any guide, economic fundamentals alone might not be enough to turbocharge the dollar. Instead, a full-blown rally might also require a period of risk aversion in the markets that fuels demand for safe havens like the dollar.

The stock market has looked bulletproof so far this year, as hopes of a soft economic landing joined forces with a rush to gain exposure to artificial intelligence shares. That said, equity valuations seem overstretched and a sustained unwinding of Fed rate cut bets that pushes bond yields even higher might be enough to trigger a sizable correction in riskier assets.

That might be the missing ingredient for the dollar to stage a fierce rally, especially if it happens during a period when foreign central banks begin to slash their rates.

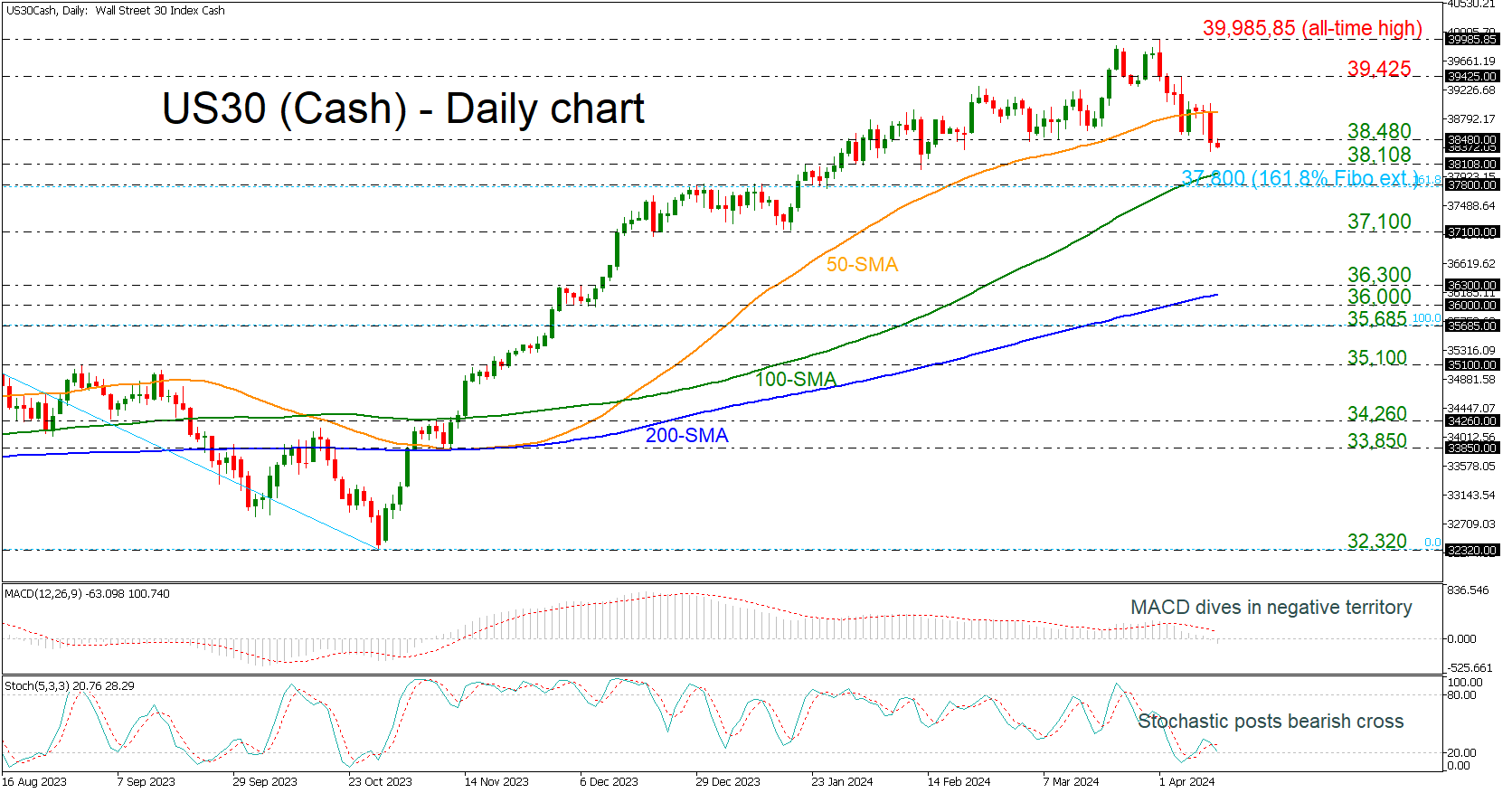

US 30 Index Slides Below 50-day SMA

- US 30 index in bearish mode in very short-term

- MACD and stochastics indicate negative correction

The US 30 cash index has lost its positive momentum after the pullback from the all-time high of 39,985.85, easing beneath the 50-day simple moving average (SMA). In the short-term, the market could retain the range-bound trading as the MACD is falling beneath its trigger and zero lines, while the stochastic posted a bearish crossover.

Should the pair stretch south, the 38,108 level could provide immediate support before the index touches the 20-day SMA at 37,950 barrier. A step lower could hit the 37,800 barrier ahead of the 37,100 area.

On the flip side, the 50-day SMA at 38,900 may halt upside movements but a successful climb above it could open the way for a retest of the 39,425 resistance and the record peak of 39,985.85.

In the very short-term picture, the index has been trading in a bearish mode for the past couple of weeks. However, in the broader outlook the tendency is still positive.

USD/JPY Technical: Rising US Treasury-JGB Yield Spreads Outweigh BoJ’s Intervention Risk

- A firmer March’s US CPI has altered the relative fundamentals narrative between the US & Japan.

- Reduces the risk of FX intervention from Japanese authorities to prop up a weaker JPY due to the lack of supporting fundamentals.

- The bullish reversal seen in the 10-year yield spread of the US Treasury over JGB may act as an impetus to support further US dollar strength.

- Watch the next intermediate resistances of 153.50 & 154.25 on the USD/JPY.

The USD/JPY has managed to decisively punch above its 151.95 major resistance yesterday, 10 April ex-post US CPI data release to print a daily close of 153.15, its highest level since June 1990.

The US inflation data release has come in firmer than expected, the core CPI rate (excluding food & energy) rose to 3.8% y/y in March, above the consensus of 3.7% y/y. In addition, the subcomponent services inflation accelerated to 5.3% y/y in March from 4.9% y/y in February, making it the highest rate of increase since August 2023.

In the past six months, the 151.95 level on the USD/JPY is considered pivotal as it managed to create a “floor” to prevent the JPY from seeing further weakness against the US dollar due to a slew of constant verbal interventions from Japan’s Ministry of Finance (MoF) officials when it traded close to the 151.95 level.

Also, the most recent actual intervention in the foreign exchange market by Japanese authorities took place previously on 21 October 2022 when the USD/JPY hit an intraday high of 151.95 before the Bank of Japan (BoJ) under the instructions of the MoF sold US dollars against JPY that led to a significant decline of -16% in the next four months on the USD/JPY, and it tumbled to a low of 127.22 on 16 January 2023.

FX intervention operations may be futile now due to a change in fundamentals

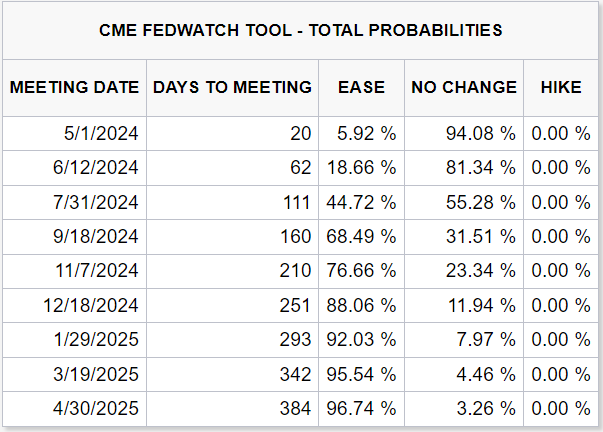

Fig 1: Probability of Fed funds rate outcome as of 11 Apr 2024 (Source: CME FedWatch Tool, click to enlarge chart)

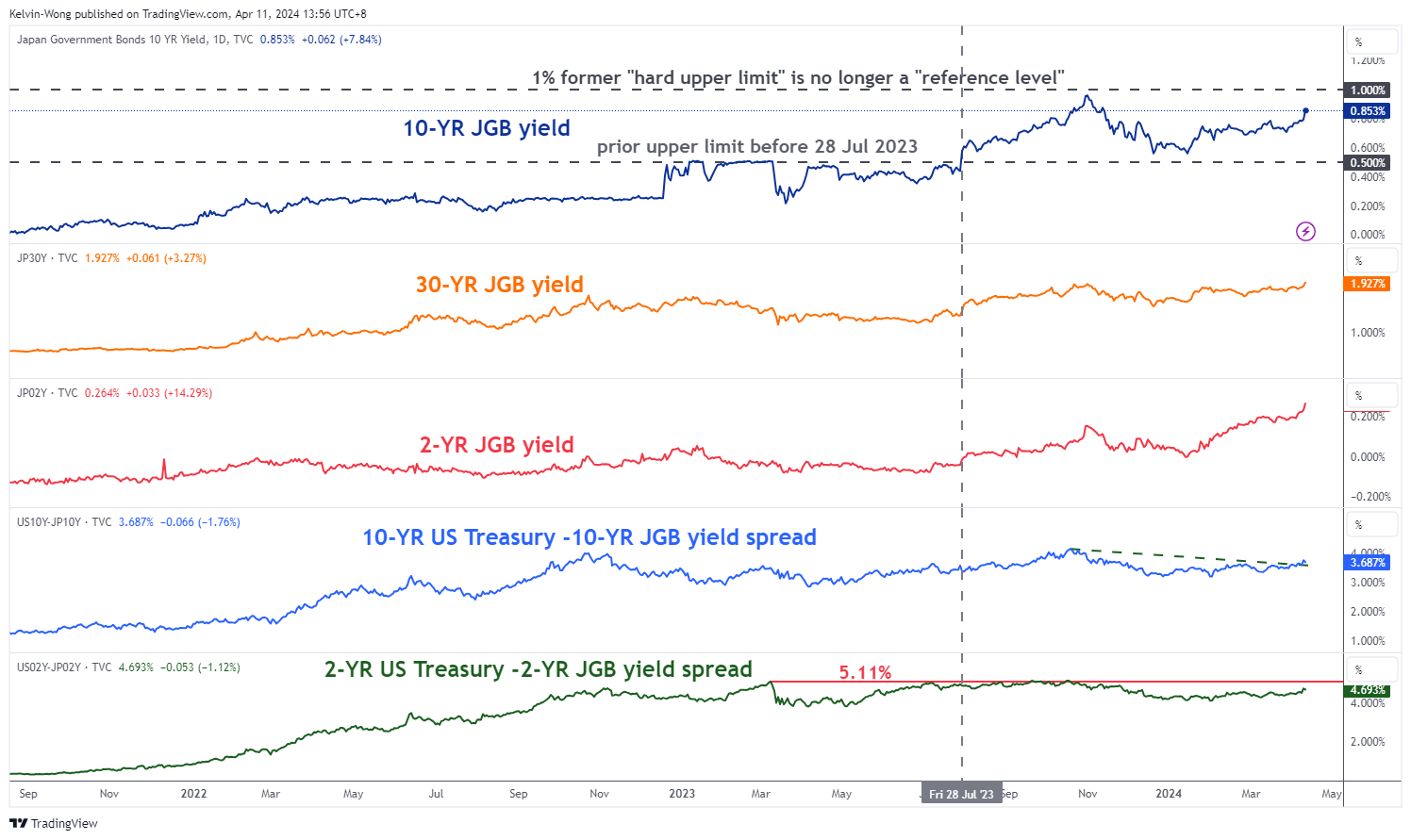

Fig 2: US Treasuries/JGB yield spreads medium-term trends as of 11 Apr 2024 (Source: TradingView, click to enlarge chart)

The impact of the ‘Fed dovish pivot” narrative has been greatly diminished at this juncture where the highly anticipated six Fed funds rate cuts expected at the start of the year has been watered down to only two cuts before 2024 ends as priced by current Fed funds rate futures market according to the CME FedWatch tool.

Also, the first Fed funds rate cut is being pushed further down the calendar to September’s FOMC meeting (69% chance) now from July’s FOMC meeting (reduced to 45% chance now from 68% at the start of this week) (see Fig 1).

Yesterday’s uptick in March’s US CPI has led to rallies in both US Treasury and Japanese Government bond (JGB) yields. However, the pace of increase is more pronounced in the US Treasury yields both in the short and long ends over JGB yields.

The yield spread of the 10-year US Treasury over 10-year JGB has risen by 22 basis points from last Thursday, 4 April to print a closing level of 3.75% yesterday which in turn broke above a major resistance at 3.60%.

Secondly, the shorter-term yield spread of the 2-year US Treasury over the 2-year JGB has jumped up by a slightly higher magnitude of 30 bps to hit a closing level of 4.75% yesterday, just a whisker away from its major resistance level of 5.11% (see Fig 2).

In a nutshell, relative movement in sovereign bond yields is one of the key factors that drives the directional basis in FX pairs, and coupled with the current dynamics of inflationary trends in the US that tend to support a stronger US dollar, any intervention attempts by Japanese authorities to significantly reverse the current state of JPY’s weakness at this juncture may be unsuccessful because relative fundaments (yield spread between US Treasuries & JGBs) are not supporting a stronger JPY.

153.50 & 154.25 are the next short-term resistances to watch on USD/JPY

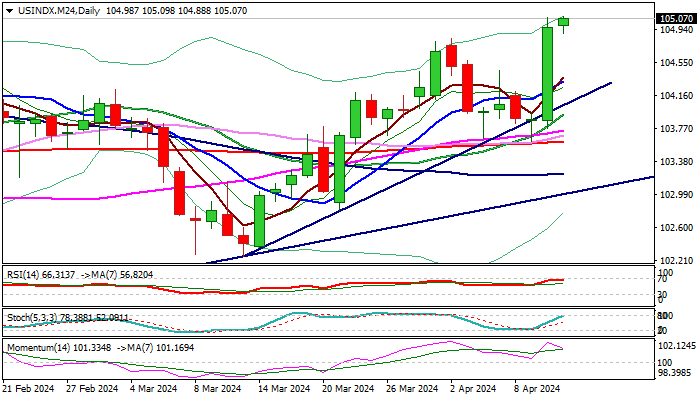

Fig 3: USD/JPY major & medium-term trends as of 11 Apr 2024 (Source: TradingView, click to enlarge chart)

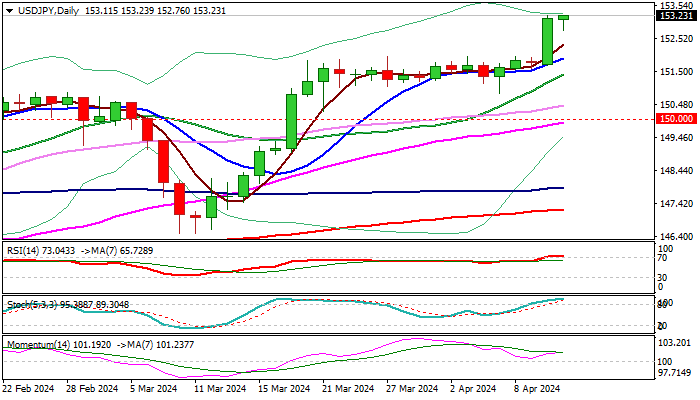

Fig 4: USD/JPY short-term trends as of 11 Apr 2024 (Source: TradingView, click to enlarge chart)

Yesterday’s bullish breakout from its three-week sideways range configuration in place since 20 March 2024 has led the USD/JPY to transform at least into a short-term uptrend phase structure.

The current minor impulsive upmove sequence remains intact as long as the 151.85 short-term pivotal support holds. The next intermediate resistances to watch will be at 153.60 and 154.25/60 (see Fig 4).

However, a reintegration back below 151.95 is considered a bull trap or failure bullish breakout for a potential slide to expose the next intermediate supports at 150.90 and 150.30 (also the upward-slopping 50-day moving average) in the first step.

Euro Stabilizes Ahead of ECB Decision

The euro is steady on Thursday, after sliding over 1% on Wednesday following the hot US inflation report. In the European session, EUR/USD is trading at 1.0745, down 0.03%.

ECB widely expected to hold rates

The European Central Bank meets later today and is widely expected to hold the deposit rate at 4% for a fifth straight time. Investors will be focusing on the rate statement, looking for signals of a rate cut in June. Some ECB policy makers have pointed to June cut and if ECB doesn’t follow suit could hurt the Bank’s credibility. The ECB would prefer to wait for the Fed to cut first, as this would boost the euro and push inflation lower. The most recent US nonfarm payrolls and inflation reports, however, were stronger than expected, which has lowered the probability of a Fed cut in June.

The eurozone economy is showing a bit more strength but a recession is still a possibility. Inflation fell to 2.4% in March, its lowest level since July 2021 and is closing in on the 2% target. Still, there is more work to do – core inflation is at 2.9% and services inflation remains very high at 4%.

The euro took a tumble on Wednesday, losing 1.05%, its worst daily performance since March 2023. The US dollar posted sharp gains against the majors, courtesy of a stronger-than-expected inflation report. In March, CPI jumped 3.5%, up from 3.2% in February and above the market estimate of 3.4%. Inflation has accelerated for a second straight month and has lowered expectations of a Fed rate cut to just 23% in June and 54% in July.

EUR/USD Technical

- There is support at 1.0692 and 1.0641

- 1.0779 and 1.0830 are the next resistance lines

Dollar Index Continues to Benefit from Hotter Than Expected US Consumer Prices

The dollar index keeps firm tone and rises further on Thursday after surging over 1% on Wednesday (the biggest one-day gains since 3 Feb 2023), lifted by hotter than expected US inflation data, which dropped bets for the start of Fed’s policy easing cycle in June.

Fresh acceleration higher has fully reversed 104.83/103.61 corrective leg and left the higher base at 103.65 zone (reinforced by 200DMA and top of daily Ichimoku cloud) and signaled bullish continuation.

The dollar broke above 105 mark and hit new five-month high, eyeing next target at 105.44 (Fibo 76.4% of 107.03/100.29 downtrend) with weekly close above former tops at 104.85/83, to confirm fresh bullish signal.

Today’s key economic events -ECB’s policy decision and US PPI / weekly jobless claims, will be in focus for fresh signals.

Res: 105.29; 105.44; 105.75; 106.04.

Sup: 104.83; 104.35; 104.00; 103.61.

USD/JPY: Hit New Multi-Decade High after Strong US CPI Numbers, Intervention Looms

USDJPY is consolidating near new multi-decade high above 153 mark, after surging around 1% on stronger than expected US inflation data.

Eventual break above narrow two-week range generates initial signal of bullish continuation of the latest bull-leg from 146.48 ((Mar 11 low) and exposes targets at 154.66 (Fibo 123.6% projection and 155.75 (1990 peak).

On the other hand, studies on all larger timeframes are strongly overbought and warn that traders may start to collect profits, while markets remain cautious about possible intervention by Japanese authorities to support weakening yen, though it seems that Japan is not in hurry and looking for the best time to intervene.

Former range tops at 152.00 zone, reinforced by rising 10DMA, now mark significant support which should keep the downside protected and maintain firm bullish bias.

Caution on dip below range floor (151.00 zone) which would risk test of psychological 150 support and next pivot.

Res: 153.50; 154.66; 155.00; 155.75.

Sup: 152.76; 152.00; 151.00; 150.00.

USD/JPY Rises to Highest Since 1990

This morning the USD/JPY rate is around 153.20 yen per US dollar, which was facilitated by a sharp strengthening of the dollar against the backdrop of news about inflation in the United States. Thus, the yen weakened to levels last seen in mid-1990.

At the same time, an important event occurred — a bullish breakdown of the level of 152 yen per US dollar. This level is special due to the fact that in 2022, the weakening of the exchange rate to 152 yen per US dollar forced the Bank of Japan and the Ministry of Finance to intervene three times, as Reuters writes, to support the yen.

In 2023, it also acted as a barrier to growth. It also held back the market during March 2024 and early April.

But yesterday the level of 152 yen per US dollar did not survive.

At the same time, technical analysis of the USD/JPY chart today shows that:

→ the price has reached the upper boundary of the ascending channel (shown in blue), now it demonstrates its role as resistance;

→ the RSI indicator indicates that the market is strongly overbought.

At the same time, it can be assumed that the likelihood of interventions has increased, since the Japanese authorities, as stated earlier, do not rule out any steps to combat excessive fluctuations.

Considering what was written above, it is possible to assume that the USD/JPY rate may form a pullback after a strong bullish impulse, and the level of 152 looks like new support.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

US Dollar Strengthens Following High Inflation Data

The EUR/USD pair has experienced a significant decline, stabilising around 1.0745 by Thursday. This movement follows the US releasing inflation data that exceeded expectations, underscoring the ongoing battle against inflation. The March consumer price index (CPI) increased by 0.4% month-on-month, matching February's rise but surpassing the anticipated 0.3%. The annual inflation rate intensified to 3.5% from 3.2%, signalling persistent inflationary pressures.

Core inflation, which excludes volatile food and energy prices, also climbed by 0.4% in March, maintaining a year-on-year core 3.8% core CPI. Such elevated inflation levels suggest that the Federal Reserve might delay interest rate cuts, a sentiment reflected in the CME's FedWatch tool. The likelihood of a rate reduction in June sharply declined to 18% post-CPI announcement, representing a significant drop from the 50% probability seen before the data release. Expectations now lean towards September for potential Federal Reserve actions.

Market predictions have adjusted to foresee a 43-45 basis point rate cut by the Fed within this year, a sharp decline from the 75 basis points expected at the week's start and the 150 basis points anticipated at the year's beginning. The minutes from the Federal Reserve's recent meeting further solidified concerns, revealing policymakers' dissatisfaction with inflation trends even before the latest price statistics.

This series of developments has bolstered the US dollar's strength in the currency market.

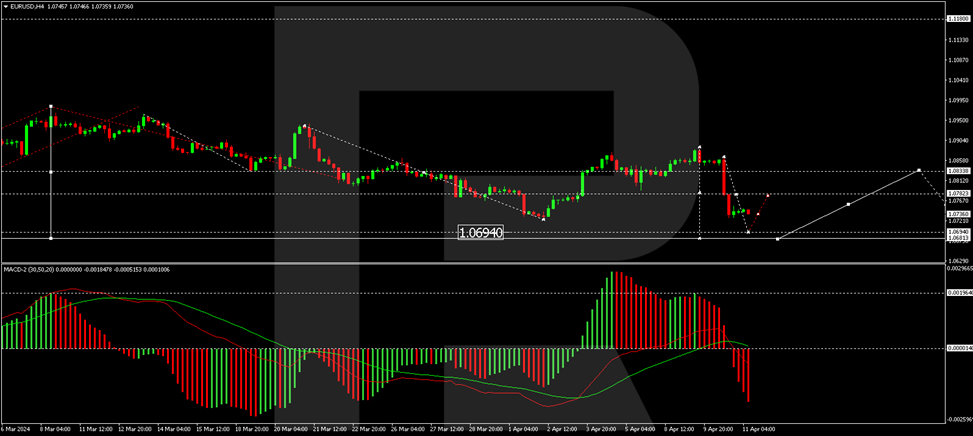

EUR/USD technical analysis

The H4 chart analysis for EUR/USD shows a correction to 1.0883, followed by a downturn to 1.0728 on the back of the recent news. A consolidation range has currently formed around this level, with a potential rise to 1.0784. A downward breakout from this range could lead to a decrease towards 1.0700. The MACD indicator, positioned below zero and trending downward, supports this potential scenario.

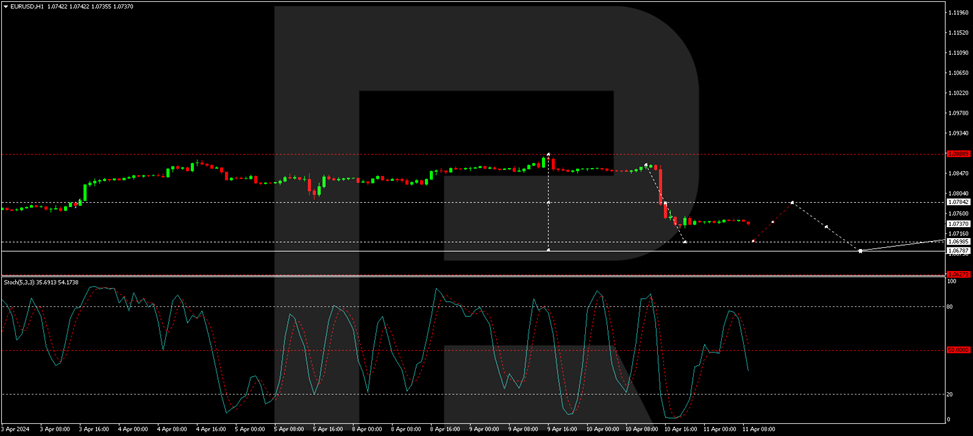

On the H1 chart, the downward trend towards 1.0700 continues, with a possible correction to 1.0780 expected. This may be followed by a further drop to 1.0680, representing an initial phase of a broader downtrend. The Stochastic oscillator, currently below 80, anticipates a continued decline towards 20, reinforcing the bearish outlook for the EUR/USD pair.

Cable’s Sharp Decline after Higher Inflation in the US

In a significant turn of events, the GBP/USD pair, often referred to as 'Cable', reversed sharply to the downside in the last 24 hours. This movement was characterized by the price decisively breaking through the corrective channel's support line, signaling a strong bearish momentum among traders. The current landscape suggests a bearish impulse in progress, likely to extend as market conditions mature.

As of now, the minor rally that we're witnessing is classified as Red Wave 4, based on Elliott Wave analysis. It's essential to consider this as a corrective phase within a larger downtrend. Analysts are pinpointing potential resistance levels, notably at 1.2560 up to 1.2580. Traders should be cautious around these levels, as they may herald the next leg down if the bearish thesis holds true.

Adding to the complexity of Cable's movements, the market has factored in the shifting sands of monetary policy. The Bank of England's rate cut bets have plunged below 50 basis points for the current year. This adjustment follows the release of U.S. inflation data, which came in hotter than anticipated.