Sample Category Title

AUDUSD Plummets in the US CPI Aftermath

- AUDUSD drops 1.7% on hotter-than-expected US CPI data

- Violates both 50- and 200-day SMAs before finding its feet

- Momentum indicators deteriorate drastically

AUDUSD had been in a steady advance since the beginning of April, posting a fresh one-month high of 0.6643 on Tuesday. However, the pair experienced a strong decline and erased all its progress following a stronger-than-expected US inflation report on Wednesday.

Should the price extend its recent slide, the recent support of 0.6479, which also held strong in February and March, could act as the first line of defence. A violation of that territory could pave the way for the 2024 bottom of 0.6441. Dropping beneath that floor, the pair may descend towards the August 2023 low of 0.6363.

On the flipside, if the pair finds its footing and jumps back above both the 50- and 200- day simple moving averages (SMAs), the bulls could initially target the February resistance of 0.6594. Further upside attempts could cease at the recent one-month peak of 0.6643. Failing to halt there, the price may advance towards the March high of 0.6666.

In brief, AUDUSD underwent a massive retreat on Wednesday but managed to recoup some losses. Therefore, a test of the congested region that includes both its 50- and 200-day SMAs could decide whether the rebound will resume or falter.

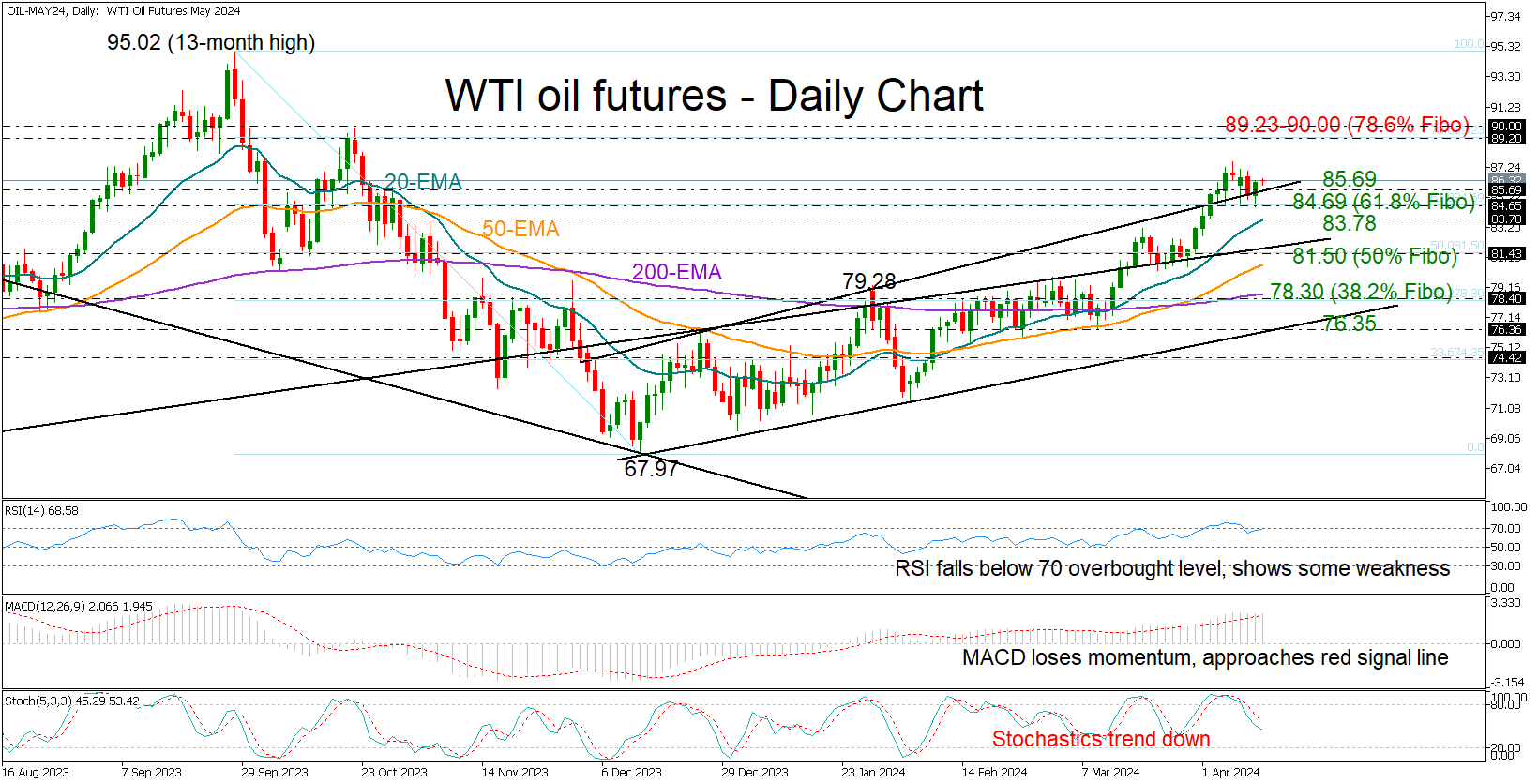

WTI Oil Pauses Rally But Remains Supported

- WTI oil futures step on 84.69 once again, hold near recent highs

- Technical indicators show some weakness, but trend signals are positive

WTI oil futures kept their footing on the 61.8% Fibonacci retracement of the September-December downtrend at 84.69 on Wednesday and closed the day with mild gains at 86.24 after news that Iran may retaliate against Israel’s deadly attack on a diplomatic compound in Damascus.

Although the price has gently bounced back, short-term risks persist as the RSI has left the overbought zone and is leaning to the downside, while the MACD and stochastic oscillator are still trending downwards. On the other hand, the market trend shows a positive trajectory in the 2024 picture and the bullish crosses between the upward-sloping SMAs reaffirm the ongoing upward trend.

Technically, for the uptrend to continue, the price must stay resilient above the upper boundary of the bullish channel at 85.69. A possible rebound there could take the price towards the 76.8% Fibonacci level of 89.23 and the psychological level of 90.00, where the price peaked in October. Surpassing that area, the bulls could advance towards September’s top of 95.00.

If the latest pullback extends below the 20-day SMA at 83.78, support could initially emerge near the 50% Fibonacci level of 81.50, where the constraining ascending line from the pandemic low is positioned. The 50-day SMA is also converging towards that region, while lower, the 200-day SMA and the 38.2% Fibonacci number of 78.30 could postpone a test near the channel’s lower band at 76.35.

Overall, there is a risk that WTI oil futures exhibit some weakness in the coming sessions, but the absence of concerning signs in the positive market trend suggests any downside correction may be short-lived.

BoE’s Greene cautions inflation persistence more pronounced in UK than in US.

In an opinion piece in FT, BoE MPC member Megan Greene explicitly urges market participants to "stop comparing" the monetary policies of the UK and US.

Greene's commentary comes in the wake of the US March CPI inflation report released yesterday, which surpassed market expectations that "the Bank of England will cut rates earlier and by more than the Federal Reserve this year".

"The markets are moving rate cut bets in the wrong direction," Greene asserts, emphasizing that, contrary to market speculation, "rate cuts in the UK should still be a way off as well."

Highlighting the unique challenges faced by the UK economy, Greene notes the "double whammy" of a tight labor market coupled with a more substantial impact from energy price shocks, which has made "inflation persistence" a more pressing issue for the UK compared to the US and other advanced economies.

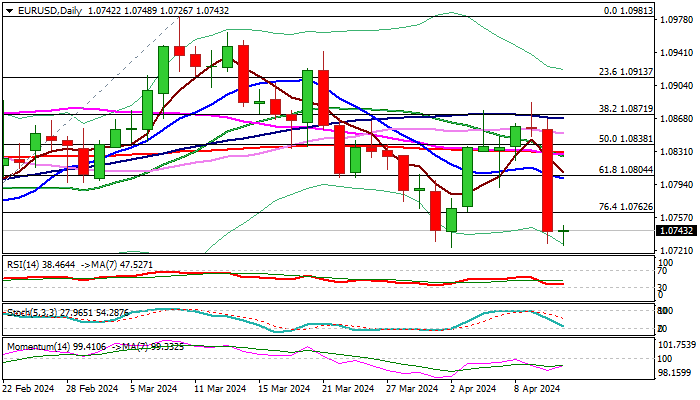

EUR/USD: Bears Taking a Breather Ahead of ECB Policy Decision

The Euro remains firmly in red and holding near last week’s low at 1.0725, following a sharp fall on Wednesday (the pair was down 1%).

Higher than expected US inflation in March, cooled market expectations for Fed’s first rate cut in June and provided strong boost to US dollar, deflating its major counterparts.

Market focus shifts to the next key event, ECB’s policy decision, due later today.

The central bank is widely expected to keep rates unchanged, and markets will look for ECB’s forward guidance, on hopes to get more details about the timing of the start of monetary policy easing.

Daily studies are in firm bearish mode and maintain negative near-term outlook.

Break of pivotal 1.0725/ 1.0695 support zone (Apr 2 low / Fibo 61.8% of 1.0448/1.1139 / psychological / Feb 14 low) to signal continuation of larger downtrend from 1.1139 (Dec 28 peak).

Broken Fibo 76.4% level (1.0762) reverted to initial resistance, with extended upticks to be capped by 10DMA (1.0800) to keep larger bears in play and offer better selling opportunities.

Res: 1.0762; 1.0800; 1.0829; 1.0867.

Sup: 1.0725; 1.0695; 1.0656; 1.0611.

ECB Meets Today But the Decision Itself (Status Quo) Won’t Be Surprising

Markets

Above-consensus CPI, driven by low 2023 base effects and far more important by (very) strong current price dynamics, sent shockwaves through the bond market yesterday. Ongoing economic resilience and a more than healthy labour market combined with sticky price pressures (January and February were NOT a blip) raise serious questions to the Fed’s ability to cut rates three times this year – or just lower them at all. The market implied probability after March inflation numbers yesterday for a June rate cut dropped to 20%. July is given a 50% chance only and even September is no longer fully priced in. Cumulative easing amounted to less than 2 rate cuts in 2024. US front end yields surged 23-24 bps. The long end joined by adding 12-18 bps in the 10y-30y bucket, supported by a tailing $39bn 10-y auction and unhindered by the FOMC minutes. Policymakers in the March policy meeting discussions “generally favored” slowing the balance sheet roll-off “fairly soon”. The idea was floated to halve the current monthly pace in USTs ($60bn) but stick with the $35bn cap on MBS. With the backing of risk aversion (stocks about 1% lower) and favourable interest rate differentials, there was no stopping the US dollar. DXY surged to a new YtD high of 105.24 – the highest level since mid-November. USD/JPY 152 long acted as a deterrent with markets fearing JPY losses beyond this level would prompt Japanese FX interventions. But the dollar crushed this resistance zone by closing at 153.24. New verbal warnings hit the wires this morning but without money on the table for now. EUR/USD posted the biggest one-day decline since March 2023, dropping more than a full big figure from 1.0857 to 1.0743. The technical charts look dire and pose a great challenge to Lagarde. The ECB meets today but the decision itself (status quo) won’t be surprising. The difficult part lies in the press conference afterwards. Weak (but gradually recovering) economic & credit (e.g. Tuesday’s BLS) indicators and ongoing disinflation back the case for a June rate cut. But because the data about Q1 wage negotiations aren’t available yet, Lagarde will probably just offer hints instead of outright committing to our base case. The key is what happens next. While the ECB in theory moves independently, the maneuvering room in practice remains limited when the Fed has its hands tied. Frankfurt can only lower rates so far before you’ll start seeing the consequences for the euro. A not hawkish enough Lagarde will undoubtedly trigger Bund outperformance and euro weakness against a resurgent US dollar. EUR/USD 1.0695 is less than half a big figure away. A break lower paves the way for a return to the 2023 low of 1.0448.

News & Views

The Bank of Canada kept its policy rate unchanged at 5% yesterday and continues its policy of quantitative tightening. In its new Monetary Policy Report, the BoC forecasts GDP growth of 1.5% in 2024, 2.2% in 2025 and 1.9% in 2026. The strengthening economy will gradually absorb excess supply through 2025 and into 2026. Since the January update, oil prices averaged about $5/b more than assumed. Overall financial conditions have eased. Canadian CPI inflation slowed (2.8% Y/Y) with easing in price pressures becoming more broad-based. Sticky shelter price inflation remains an area of concern though. The BoC expects CPI inflation to be close to 3% during the first half of this year, move below 2.5% in the second half, and reach the 2% inflation target in 2025. In coming months, the BoC will look for more evidence that the downward trend in headline and core CPI is sustained. Interestingly, the BoC raised its estimate of the nominal neutral rate from 2%-3% in last year’s assessment to 2.25%-3.25%. USD/CAD yesterday surged to a new YTD high (USD/CAD 1.37) as the loonie succumbed to the mighty USD. CAD did slightly outperform against the euro (EUR/CAD 1.47). The market implied probability of a policy rate cut at the next, June, meeting fell from around 75% to 60%.

Chinese inflation fell again in March (-1% M/M), pulling the Y/Y figure down to 0.1% from 0.7%. The February figure was driven/distorted by stronger demand over the Lunar New Year holiday. The setback was broad-based with services inflation at 0.8% Y/Y from 1.9% and consumer goods prices falling by 0.4% (from -0.1%). Food inflation declined by 2.7% Y/Y (from -0.9%). Core inflation slowed from 1.2% Y/Y to 0.6%. Headline CPI averaged zero in Q1 2024, up from -0.3% in Q4 2023 but insufficient to put deflationary concerns to bed.

Markets Trim Fed Rate Cut Expectations Amid High US CPI

In focus today

Today's focus will be the ECB meeting where we expect no change in the policy rate. We anticipate that the primary insight from the meeting will be a confirmation of the current ECB narrative, thereby indicating that the ECB is on track to deliver a rate cut in June. While this meeting may be considered an interim meeting and lead to limited market reaction, we expect ECB to deliver a clear commitment for a June rate cut, in the form of an explicit guidance of an 'intention to cut by 25bp in June'. No guidance will be offered beyond that point on the pace of rate cuts or the end level of the tightening cycle. We still like our baseline scenario of three cuts of 25bp this year, but see risks skewed for ECB delivering less than that this year, due to the sticky underlying inflation. See more in ECB Preview - an intention to cut, 5 April.

From the US, March PPI is due for release in the afternoon. The March CPI print surprised to the upside yesterday at 0.4% m/m for both headline and core. We will also get jobless claims which could shed some light on the tightness of the labour market.

In Sweden, we get the monthly Prospera at 8.00 CET. The survey should confirm that inflation expectations are anchored close to 2.0% on all horizons and as such welcome input to the Riksbank, whose vice governor Per Jansson gives a speech about the economy and current monetary policy at 13.15 CET.

Economic and market news

What happened overnight

Asian equity markets tumbled overnight following the CPI print from the US, with the Nikkei down 0.8% and the broad MSCI index for Asia-Pacific (excl. Japan) losing 0.7% as of this morning.

March CPI for China showed that inflation slowed more than expected to 0.1% y/y (cons: 0.4%). Part of the decline is driven by base effects as the effects of the Chinese New Year fall out. The PPI showed a 2.8% decline in prices for March, with large manufacturing capacity weighing on prices.

What happened yesterday

Yesterday's big market driver was the US March CPI print which surprised to the upside as headline printed at 0.4% m/m (cons: 0.3%) and core at 0.4% (cons: 0.3%). Especially worrying for the hopes of a Fed rate cut was the fact that broader core services drove the upside surprise (services ex. shelter at 0.8% m/m), which rhymes well with recent signs of continuing strong wage inflation and a tight labour market. Underlying price pressures not only remain too high for comfort, but also show signs of accelerating in early 2024. The market reaction was strong, as markets scaled back expectations of rate cuts to 2 this year, the 10Y yield gained 18bp, while the greenback gained 1% on most G-10 currencies, including the yen where USD/JPY surged past resistance level 152, raising the risk of a Japanese FX intervention. There was also a spill-over to euro area yields with the 10Y bund up 6bp as of last night.

Equities: Global equities were lower yesterday as US markets was beaten down after a hotter-than-expected CPI report. As we have written extensively about recently, the current situation looks very much like the dynamics and rotation we saw back in Q3 last year when inflation and central bank fear also dominated markets. In US yesterday, Dow -1.1%, S&P 500 -1.0%, Nasdaq -0.8% and Russell 2000 -2.5%. Asian markets are lower this morning following the negative session on Wall Streat. Futures in Europe and US are mixed this morning.

FI: Yesterday's trading session was mostly a waiting game ahead of the US CPI and today's ECB meeting. Yields declined marginally in the morning session, albeit that quickly reversed on the stronger than anticipated US CPI. From 10y Bunds went from being down 2bp on the day to shifting 8bp higher, to end the day at 2.43%. The catalyst was clearly US led with 2y UST rising 22bp on the day to just shy of 5%.

FX: Yesterday's session was characterized by a stronger USD following the higher-than-expected US March CPI print. EUR/USD declined to 1.0750. USD/JPY is hovering around 153, and intervention risk is yet again a market theme. EUR/SEK increased to around 11.50, while EUR/NOK rose above 11.60.

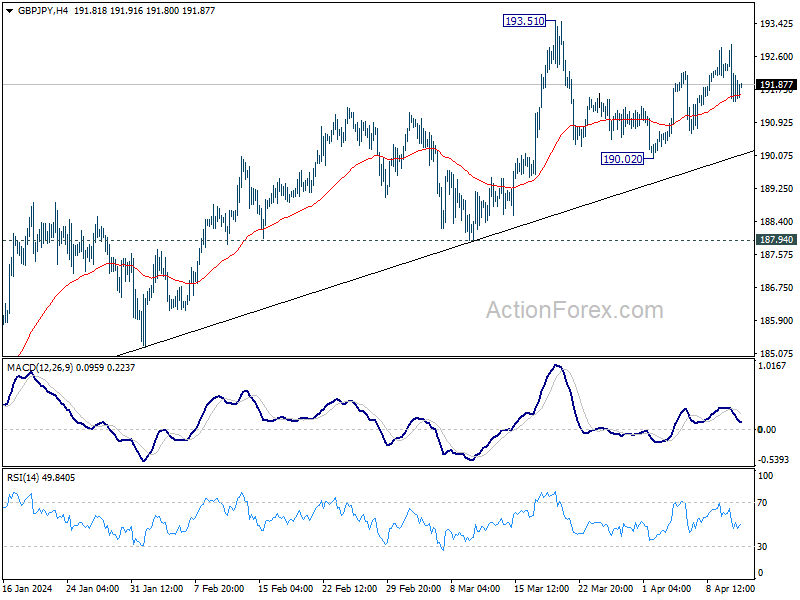

GBP/JPY Daily Outlook

Daily Pivots: (S1) 191.37; (P) 192.16; (R1) 192.85; More.....

Intraday bias in GBP/JPY remains neutral at this point. Consolidation from 193.51 is probably extending with another falling leg. But further rally is expected as long as 190.02 support holds. On the upside, break of 193.51 will resume larger up trend to 195.86 long term resistance. On the downside, though, break of 190.02 will turn bias to the downside for 187.94 support instead.

In the bigger picture, current rally is part of the up trend from 123.94 (2020 low), and is in progress for 195.86 long term resistance (2015 high). Break of 187.94 support is needed to be the first sign of medium term topping. Otherwise, outlook will remain bullish in case of retreat.

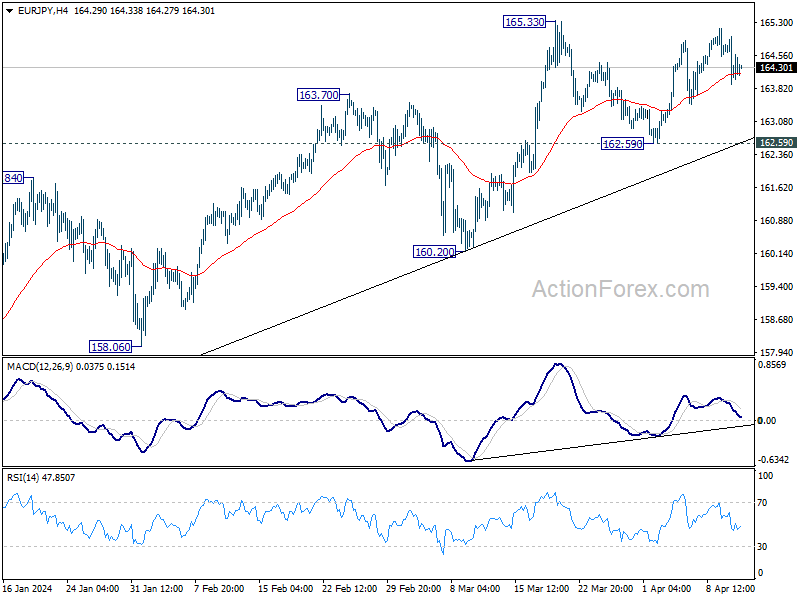

EUR/JPY Daily Outlook

Daily Pivots: (S1) 164.02; (P) 164.51; (R1) 165.01; More...

Intraday bias in EUR/JPY remains neutral at this point. Consolidation from 165.33 is possibly extending with another falling leg, and deeper decline could be seen. But outlook stays bullish as long as 162.59 support holds. On the upside, firm break of 165.33 will resume larger up trend towards 169.96 key resistance next. On the downside, though, break of 162.59 will turn bias to the downside for 160.20 support next.

In the bigger picture, current rally is part of the up trend from 114.42 (2020 low), which is still in progress. Next target is 169.96 (2008 high). Break of 160.20 support is needed to be the first sign of medium term topping. Otherwise, outlook will stay bullish in case of retreat.

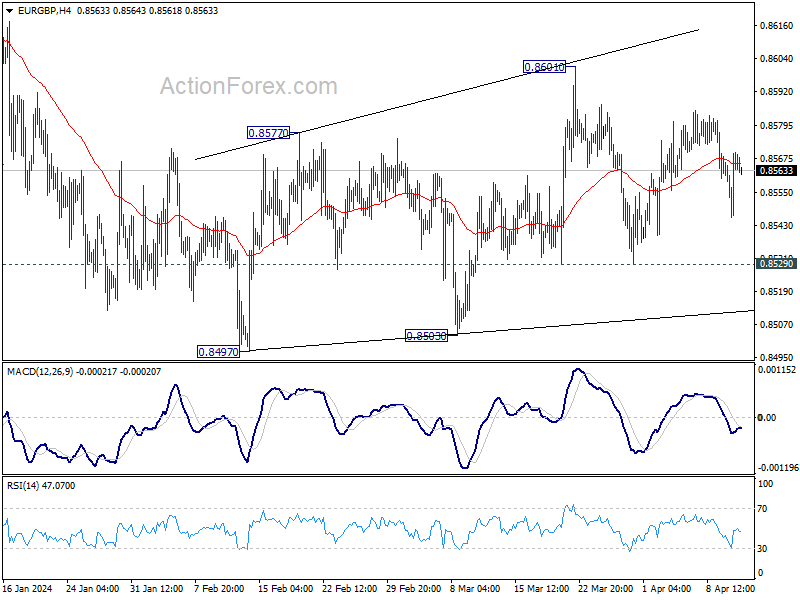

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8552; (P) 0.8562; (R1) 0.8576; More...

Intraday bias in EUR/GBP remains neutral for the moment, as range trading continues. On the downside, firm break of 0.8529 support will argue that the corrective recovery from 0.8497 has completed at 0.8601. Intraday bias will be back on the downside for retesting 0.8497 low next. On the upside, break of 0.8601 will resume the rebound instead.

In the bigger picture, there is no clear sign that down trend from 0.9267 has completed, despite loss of downside momentum as seen in D MACD. As long as 0.8713 resistance holds, the down trend will remain in favor to resume through 0.8491 low at la later stage.

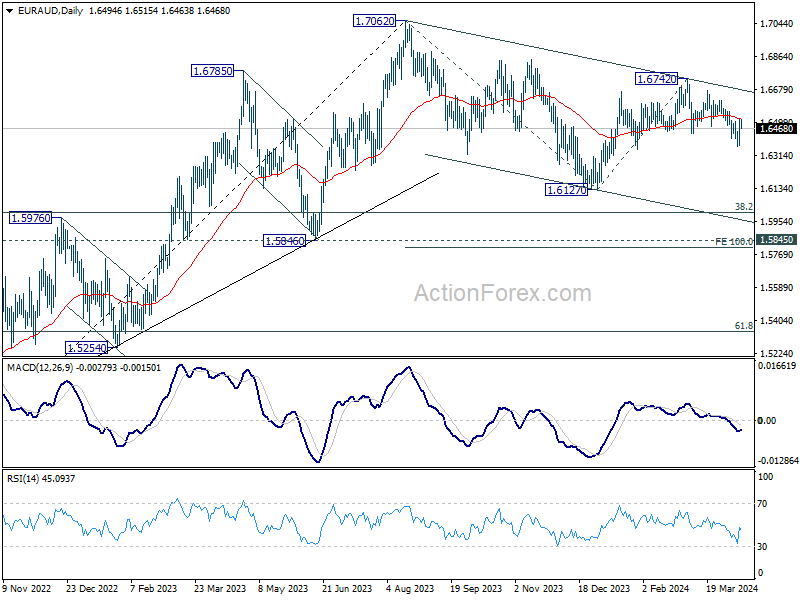

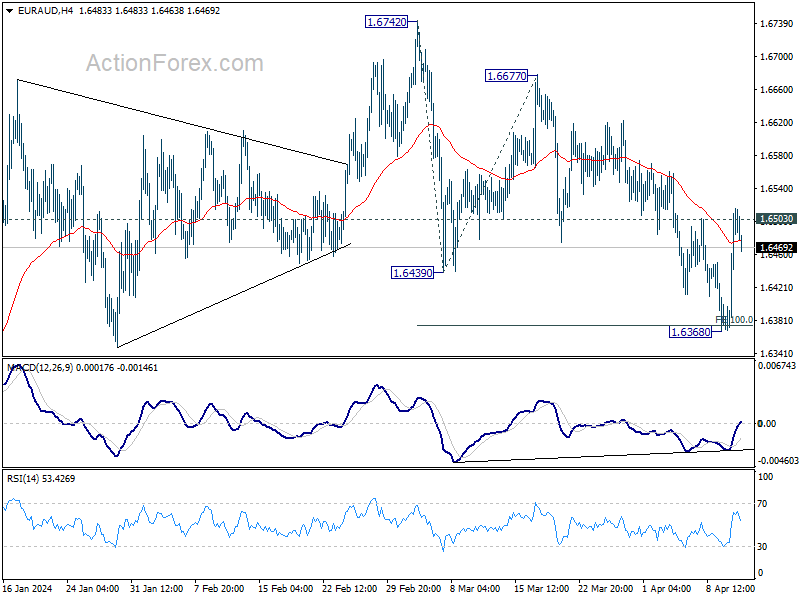

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6398; (P) 1.6458; (R1) 1.6556; More...

Intraday bias in EUR/AUD is turned neutral first as it recovered after hitting 100% projection of 1.6742 to 1.6439 from 1.6677 at 1.6374. On the downside, below 1.6368 will resume the fall from 1.6742 towards 1.6127 low. Nevertheless, sustained trading above 55 D EMA (now at 1.6519) will turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). The correction is still in progress with fall from 1.6742 as the third leg. Strong support is expected around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.