Sample Category Title

Is There a Possibility of No Fed Rate Cuts This Year?

- A summer rate cut by the Fed hangs in the balance amid persistent inflation

- Rate cut bets have been scaled back from more than six to around two

- But limited fallout on Wall Street; can the risk rally survive no rate cuts?

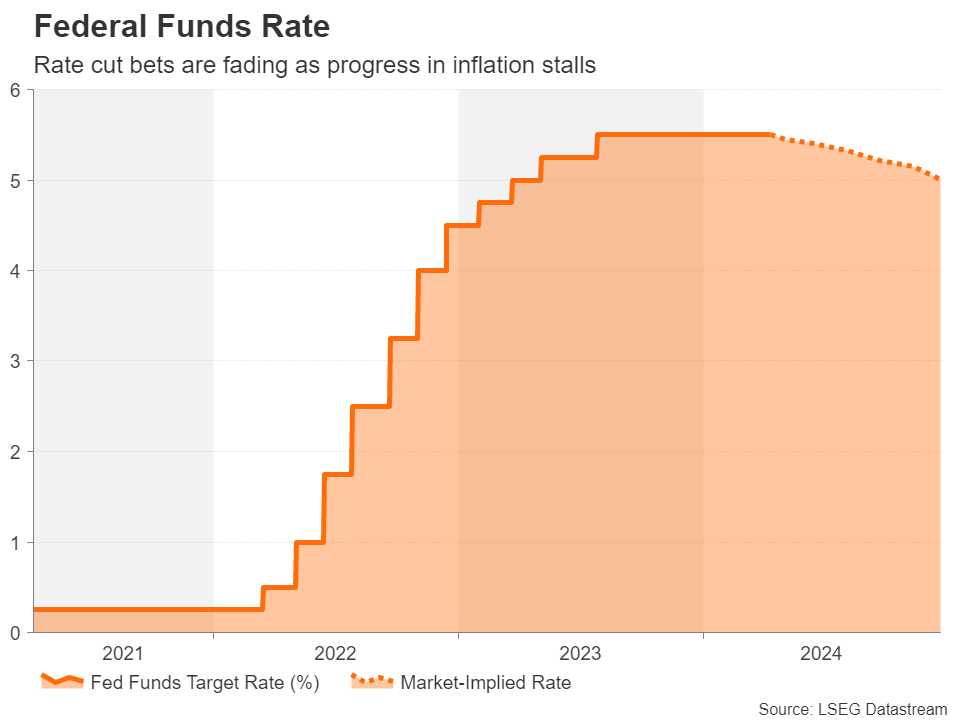

Waiting for the elusive rate cut

Ever since the Fed signalled it was done hiking rates in November last year, the focus swiftly turned to rate cuts, with the timing and scope of policy easing consuming investors’ attention. Subsequently, markets have been abuzz with rate cut speculation all year and that theme looks set to dominate for some time yet as the timing keeps getting pushed back.

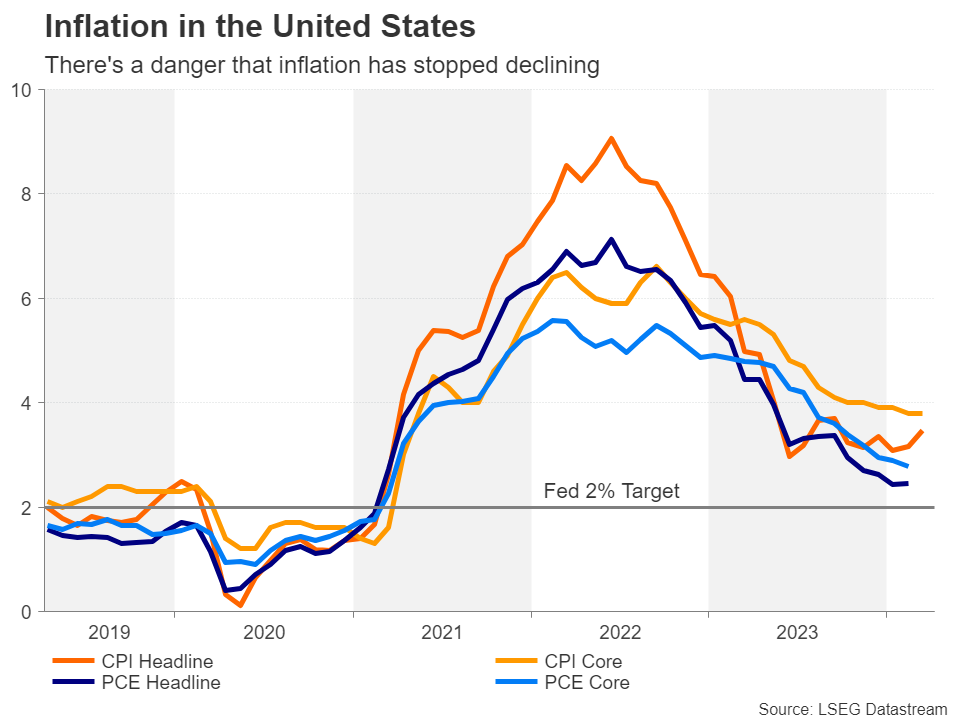

The stalling of the progress to lower inflation to the Fed’s 2% target could soon go from being a minor setback to a major policy headache for Federal Open Market Committee (FOMC) members, which set interest rates. The Fed is still reeling from its policy error in 2021 when it misjudged the surge in inflation to be transitory.

Resilient economy keeping Fed on its toes

Keen on avoiding making the same mistake twice, Chair Jerome Powell has been careful not to pre-commit to any rate cuts before inflation has moved a lot closer to the target. Central banks tend to take their foot off the brake well in advance of inflation reaching their goal, but it’s also usually the case that economic growth has slowed down substantially by then.

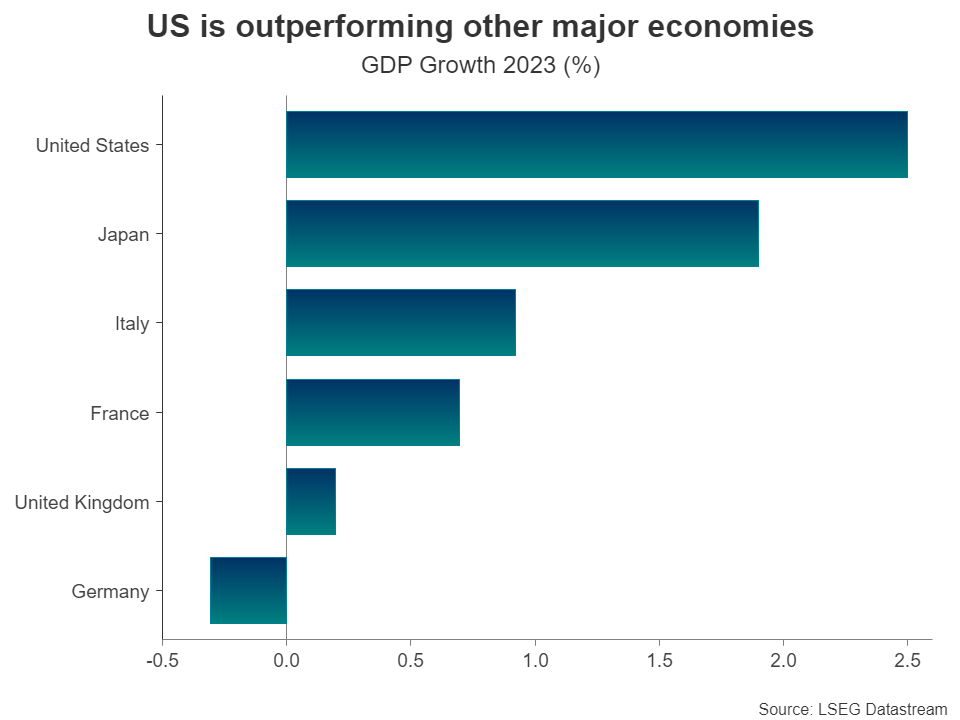

That is certainly not the case with the US economy at the moment, which continues to confound expectations of a slowdown. Full year GDP growth accelerated to 2.5% in 2023 even as borrowing costs hit the highest in two decades, and the economy likely grew by a similar rate in the first quarter of 2024.

Not slowing down

At the heart of the ‘problem’ of an overly strong economy is the tight labour market. Jobs growth has quickened in recent months, with nonfarm payrolls gains exceeding 250k since December, and the unemployment rate has held near decade lows below 4.0%. Fortunately for policymakers, wage growth has been steadily moderating over the past two years, in a sign that the strong demand for workers is being matched by a rise in the supply of labour.

An influx of migrants, as well as previously economically inactive workers being attracted into the labour market by higher wages are the likely causes of the boost in the size of the labour force. The question now is whether this trend is sustainable. Even if the US economy can maintain full employment without adding to wage pressures, consumer spending is unlikely to wane as long as the jobs market remains in such good shape, and that keeps the risks to inflation tilted to the upside.

Inflation picture has become muddied

All this has led some analysts to question whether the Fed has tightened policy enough to prevent a resurgence in inflation let alone bring it down all the way down to 2%. Various price metrics for the American economy indicate that inflation has started to bottom out.

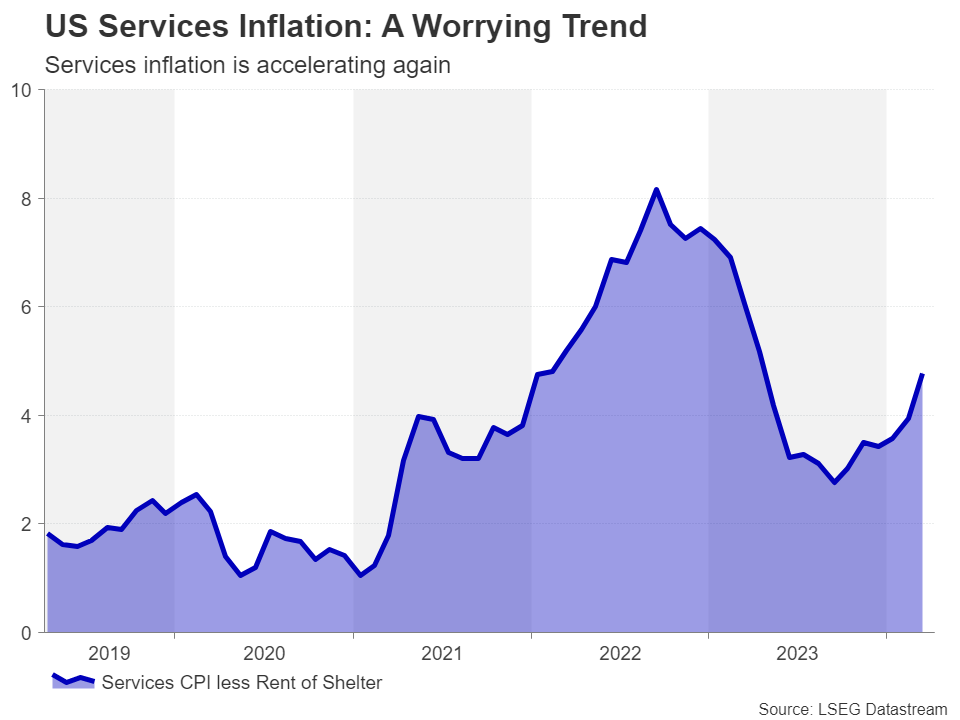

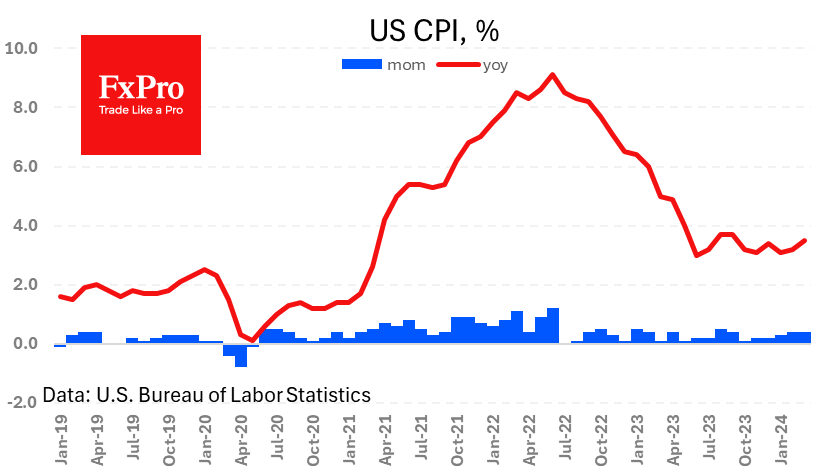

Headline inflation as measured by the consumer price index (CPI) has been moving sideways since June 2023 and so have producer prices. Moreover, a key gauge of services CPI jumped to 4.8% in March, far from abating. Services price pressures have been the stickiest and most problematic for the Fed in its fight against inflation.

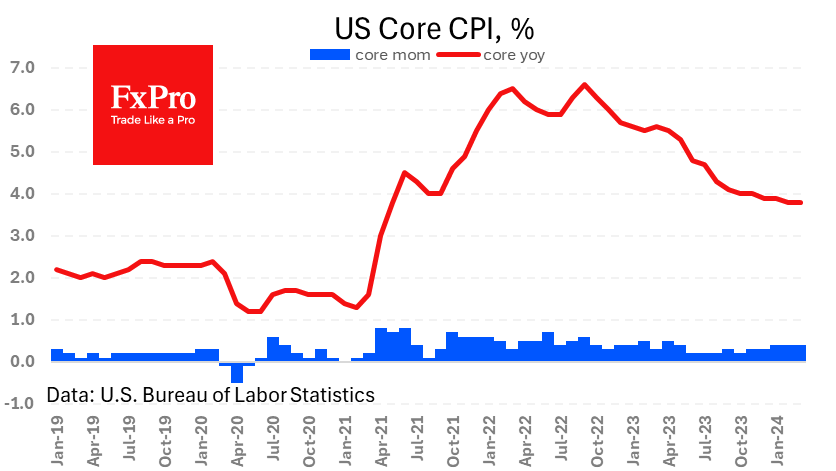

There’s been better progress with the Fed’s preferred PCE measure of inflation. The all-important core PCE price index eased to 2.8% in February – the lowest in nearly three years.

Are price pressures simmering again?

However, there are plenty of risks that could yet scupper central banks’ hopes of reining in inflation once and for all. Energy prices are rising again – WTI oil is up about 19% in the year-to-date – amid heightened geopolitical tensions globally. The fighting between Israel and Hamas in the Middle East threatens to embroil the United States and Iran, while the ongoing war between Ukraine and Russia is showing no sign of de-escalating.

Aside from crude oil, other commodity prices, such as copper and cocoa, have also soared. Meanwhile, the disinflation in goods prices appears to be levelling off.

Hoping for the best

From the Fed’s perspective, there’s still good reason to believe that inflation will fall further in the coming months, allowing it to begin cutting rates at some point later in the year. But against the current inflation backdrop, the projected three rate cuts in 2024 are looking increasingly optimistic.

Several Fed officials have already hinted that they see scenarios with fewer than three rate cuts and some are also not sure if inflation will have cooled enough by June to proceed with the first 25-basis-point reduction.

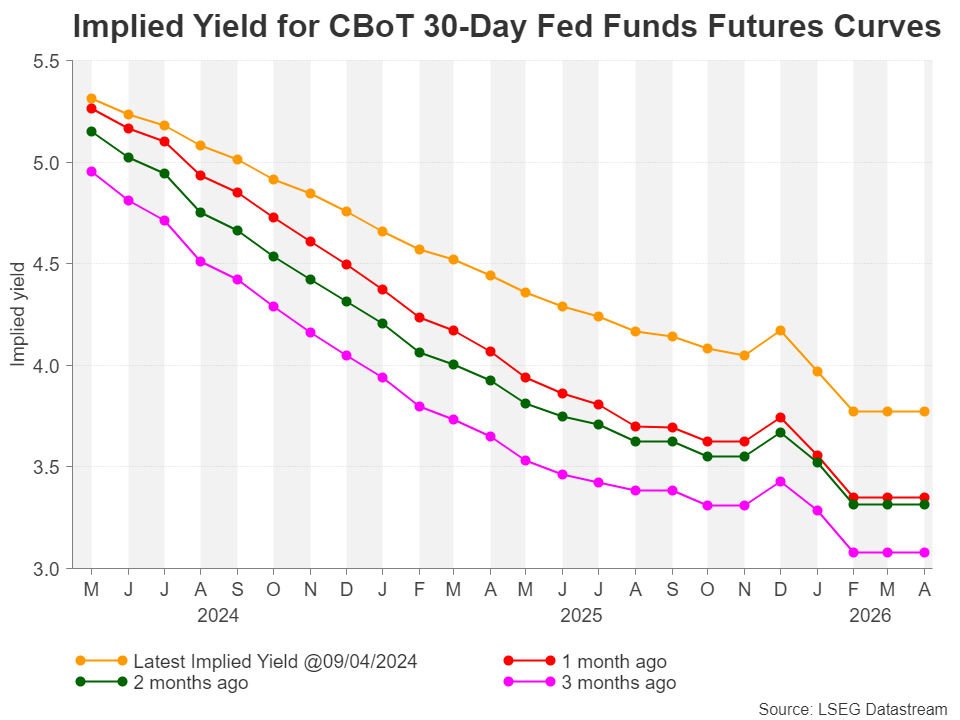

What’s surprising, though, is how well market expectations have aligned with both the data and the Fed’s rhetoric in recent weeks. With expectations for June easing fading and a July move hanging in the balance, a 25-bps cut might be delayed until September. In addition, total rate cut bets for 2024 have been dialled back to fewer than 50 bps.

No panic yet

This suggests that a further hawkish tilt by the Fed in the run up to the May and June policy meetings won’t come as much of a shock for investors. Until recently, equity markets had been taking this steady repricing in their stride. Shares on Wall Street have been scaling all-time highs alongside Treasury yields that have been climbing to fresh yearly highs.

The soft-landing narrative whereby the economy can keep growing as interest rates remain high and inflation falls, has been propping up the risk rally. Even the struggling Eurozone economy may come out of this inflationary episode by evading a recession, while some green shoots of economic stabilization in China are also buoying investor sentiment.

Are markets ready for no rate cuts?

However, markets may now be starting to become more nervous about the prospect of later and fewer rate cuts if there’s a further pricing out of Fed easing in the coming weeks, especially if the 10-year yield continues to edge higher, surpassing 4.50% and pushing up long-term borrowing costs for firms.

At this stage, with US consumers still spending, and the artificial intelligence (AI) mania fuelling a rally in all related stocks, it’s hard to see what the trigger point for a sharp stock market correction would be. Judging by investors’ reaction to the latest paring back of rate cut bets, markets would probably be able to tolerate just two rate cuts in 2024. However, that might change if inflation does not recede further as expected over the next few months and the prospect of just one or even no rate cut becomes real.

Given how inflation has repeatedly surprised to the upside since its upsurge in 2021 and more importantly, how policymakers have again and again underestimated its persistence, the risk of no rate cuts this year and a potentially big market fallout cannot be dismissed.

Strong Inflation Jumpstarts Dollar

US inflation once again beat expectations, causing markets to further discount the chances of an easing cycle starting in June.

The dollar responded with a 1% rise against a basket of major currencies, taking the DXY back to 104.80. The dollar recorded two peaks near these levels in February and late March, and it has not traded steadily higher since November.

The general and core consumer price indexes each added 0.4% versus 0.3% expected. The annual rate of general inflation rose to 3.5%, while the core index maintained its 3.8% y/y pace. In both cases, the monthly rates of increase defy expectations of a return to the targeted 2%.

This should be troubling news on top of the strong employment report late last week. The data-linked Fed is unlikely to miss the data set of the past five days and is likely to maintain its wait-and-see stance.

Technically, the current upside momentum looks like an attempt to break away from support in the form of the 50 and 200-day moving average crossover and head higher after a prolonged consolidation. This movement may not meet any significant resistance until the 106.80-107 area, where the downward reversal was formed last October.

Bank of Canada Upgrades Outlook for Economy, Remains Silent on Rate Cuts

The Bank of Canada maintained the overnight rate at 5.0%, while stating that it will continue with Quantitative Tightening (QT).

In its quarterly Monetary Policy Report (MPR), the Bank upgraded its economic growth forecast, stating "this largely reflects both strong population growth and a recovery in spending by households. Residential investment is strengthening, responding to continued robust demand for housing. The contribution to growth from spending by governments has also increased."

On the inflation outlook, the BoC mentioned that inflationary pressures have eased. It highlighted that the "easing in price pressures (are) becoming more broad-based across goods and services". It also stated that it "expects CPI inflation to be close to 3% during the first half of this year, move below 2½% in the second half". While its inflation forecast in the MPR is slightly lower at the end of 2024, the 2025 forecast remained unchanged.

On the future path of policy, the Bank needs more confirmation of the recent inflation trend before it will adjust rates. It said that "while inflation is still too high and risks remain, CPI and core inflation have eased further in recent months. The Council will be looking for evidence that this downward momentum is sustained."

Key Implications

The BoC remains steadfast in its desire to maintain rates at the current 5% level. It can justify this stance based on its upgrade to economic growth, while still expecting inflation to remain somewhat elevated over the coming months. This economic backdrop (alongside an upgrade to the neutral rate) affords the central bank more time to observe how inflation evolves, allowing it to gain greater confidence that price pressures have been tamed before it decides to cut its policy rate.

Market pricing is still holding onto hope for a June cut (~50%), but July (our call) is becoming more likely. Even though inflation has moved within the BoC's 1% to 3% target range over the last few months, markets have become more cautious on the timing of cuts. While some of this is coming from the inflation warning in recent U.S. CPI prints, strong Canadian economic growth to start 2024 has been the main driver. And while spending data have been encouraging, we question how long this will last, especially with the labour market having started to come under pressure in March. Should economic growth weaken further and inflation remain on its current trajectory, we could see the BoC readying markets for the cuts in short order.

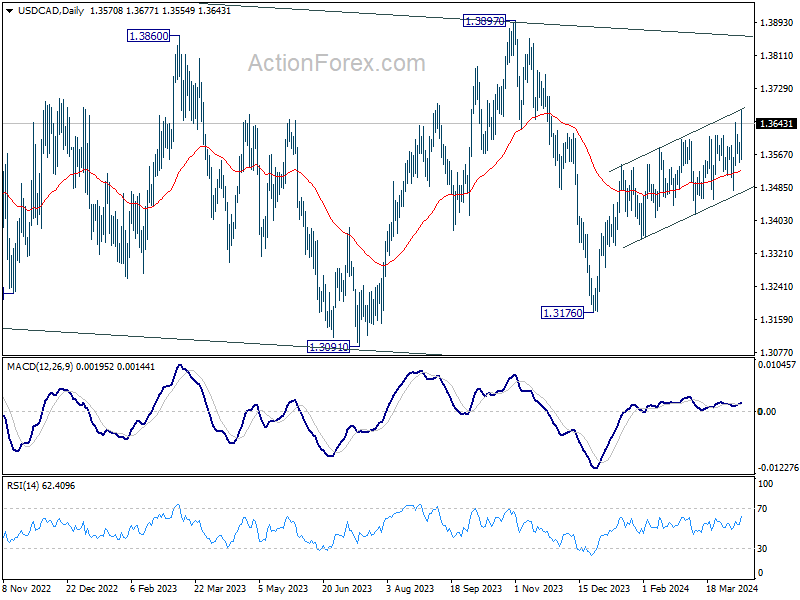

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3546; (P) 1.3572; (R1) 1.3598; More...

Intraday bias in USD/CAD is back on the upside with break of 1.3646 resistance. Firm break of channel resistance would prompt upside acceleration, and extend the rally from 1.3176 to 1.3897 resistance next. On the downside, below 1.3554 minor support will turn intraday bias neutral again. But further rally will remain in favor as long as 1.3477 support holds, in case of retreat.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

BoC stays the course, no explicit hint on rate cut

BoC maintains overnight rate at 5.00% as widely expected. The central bank's statement highlighted that both the CPI and core inflation have "eased further" in recent months, though they remain at elevated levels. BoC emphasized its intention to monitor whether the observed "downward momentum is sustained". But there is no explicit hint on rate cuts.

In its latest economic projections, BoC forecasts GDP growth of 1.5% for 2024, an uptick from previously projected 0.8%. The outlook for the subsequent years also remains optimistic, with growth expected at 2.2% in 2025 (down from previous 2.5%) and 1.9% in 2026.

On the inflation front, BoC projects CPI to hover close to 3% during the first half of this year, with a downward trend anticipated in the latter half to below 2.5%, and reach 2% inflation target in 2025.

(BOC) Bank of Canada maintains policy rate, continues quantitative tightening

The Bank of Canada today held its target for the overnight rate at 5%, with the Bank Rate at 5¼% and the deposit rate at 5%. The Bank is continuing its policy of quantitative tightening.

The Bank expects the global economy to continue growing at a rate of about 3%, with inflation in most advanced economies easing gradually. The US economy has again proven stronger than anticipated, buoyed by resilient consumption and robust business and government spending. US GDP growth is expected to slow in the second half of this year, but remain stronger than forecast in January. The euro area is projected to gradually recover from current weak growth. Global oil prices have moved up, averaging about $5 higher than assumed in the January Monetary Policy Report (MPR). Since January, bond yields have increased but, with narrower corporate credit spreads and sharply higher equity markets, overall financial conditions have eased.

The Bank has revised up its forecast for global GDP growth to 2¾% in 2024 and about 3% in 2025 and 2026. Inflation continues to slow across most advanced economies, although progress will likely be bumpy. Inflation rates are projected to reach central bank targets in 2025.

In Canada, economic growth stalled in the second half of last year and the economy moved into excess supply. A broad range of indicators suggest that labour market conditions continue to ease. Employment has been growing more slowly than the working-age population and the unemployment rate has risen gradually, reaching 6.1% in March. There are some recent signs that wage pressures are moderating.

Economic growth is forecast to pick up in 2024. This largely reflects both strong population growth and a recovery in spending by households. Residential investment is strengthening, responding to continued robust demand for housing. The contribution to growth from spending by governments has also increased. Business investment is projected to recover gradually after considerable weakness in the second half of last year. The Bank expects exports to continue to grow solidly through 2024.

Overall, the Bank forecasts GDP growth of 1.5% in 2024, 2.2% in 2025, and 1.9% in 2026. The strengthening economy will gradually absorb excess supply through 2025 and into 2026.

CPI inflation slowed to 2.8% in February, with easing in price pressures becoming more broad-based across goods and services. However, shelter price inflation is still very elevated, driven by growth in rent and mortgage interest costs. Core measures of inflation, which had been running around 3½%, slowed to just over 3% in February, and 3-month annualized rates are suggesting downward momentum. The Bank expects CPI inflation to be close to 3% during the first half of this year, move below 2½% in the second half, and reach the 2% inflation target in 2025.

Based on the outlook, Governing Council decided to hold the policy rate at 5% and to continue to normalize the Bank's balance sheet. While inflation is still too high and risks remain, CPI and core inflation have eased further in recent months. The Council will be looking for evidence that this downward momentum is sustained. Governing Council is particularly watching the evolution of core inflation, and continues to focus on the balance between demand and supply in the economy, inflation expectations, wage growth, and corporate pricing behaviour. The Bank remains resolute in its commitment to restoring price stability for Canadians.

Information note

The next scheduled date for announcing the overnight rate target is June 5, 2024. The Bank will publish its next full outlook for the economy and inflation, including risks to the projection, in the MPR on July 24, 2024.

Sunset Market Commentary

Markets

Strike three. Some dismissed the hotter-than-expected inflation prints in January and February as statistical flukes that would soon be reversed. March delivered another nasty upside surprise. Headline CPI rose from 3.2% to 3.5% vs 3.4% expected while the underlying gauge defied hopes for the tiniest of declines by stabilizing at 3.8%. Low base effects have helped but that’s only part of the story. Current price dynamics remain (very) strong with 0.4% m/m readings for both indicators topping the 0.3% estimate. For core CPI specifically, the Q1 m/m readings result in an annualized 4.5%, the most since May last year. Housing has been a major boost to (services) inflation for quite some time because of the slow roll-over of rents in the CPI calculations. But even when filtering for this component (as well as energy), the so-called supercore services gauge came in at a sharp 0.65% m/m, pushing the y/y to 4.77% - the fastest pace since April last year. Today’s numbers are a similarly nasty surprise for Powell too. The Fed chair put aside the January and February editions with surprising ease at the March policy meeting, labelling them as the bumps one can expect to occur in the road toward 2% inflation. Let’s see how many agreed with that in tonight’s FOMC meeting minutes release. Anyway, we flagged the idea of a first Fed rate cut in September at the very earliest for some time now. Markets are aligning. June was already off the table, July is given a less than 50% chance and even September currently is no longer fully priced in. There’s <50 bps (or two cuts) priced in for all of 2024. That’s less than the three cuts the March dot plot projected. Back then, this was backed by the smallest majority possible. That balance now probably shifted to the hawkish side. The front end of the yield curve underperforms hugely. The 2-y yield surges 18.4 bps and has set its sights on the symbolical 5%. Longer maturities add between 6.6 (30-y) and 11.9 bps (10-y). We’re wary to draw firm conclusions from intraday moves in the 10-y real yield, but a 10 bps daily increase sure is worth mentioning. Tonight’s $39 bn 10-y auction just got even more interesting. Any sign of weakness won’t go unnoticed and will prompt a test of the 4.54% resistance level (62% recovery on the 2023Q4 decline). The US dollar spares no one, not least JPY. USD/JPY surpasses the 152 mark with ease to a new 34-year high. At this point, verbal interventions by Japanese officials have officially turned useless. EUR/USD loses a big figure to 1.0767 currently with technically little in the way for a return to the current 1.0695 YtD low. It’s up to ECB’s Lagarde tomorrow to prevent the euro from succumbing to pressure.

News & Views

Czech inflation rose by 0.1% M/M in March with the Y/Y-figure stabilizing at 2%. Food prices continue to drive the relatively strong disinflation this year, down 5.9% Y/Y. We expect headline inflation to remain relatively stable in the coming months, falling back to close to 1.5% Y/Y in the summer (base effects). Towards the end of the year, it should again be slightly above the CNB's 2% target. Annual inflation was 0.9 percentage point lower in March than the CNB’s winter forecast. There was a greater-than-expected slowdown in administered price inflation (6.6% Y/Y vs 9.5% expected by the CNB). Core inflation was also somewhat lower than forecasted (3.3% Y/Y vs 2.7%), reflecting low growth in prices of foreign inputs and a cooling of domestic demand due to a restrictive CNB monetary policy stance. Fuel prices unexpectedly increased year on year in March (3.8% vs -1.6%). We don’t expect today’s inflation print to alter the CNB’s current 50 bps rate cut pace at the next couple of meetings. Only by September, they could return to slower steps (25 bps), resulting in an end of year policy rate of 3.5%. Czech swap yields add 2.5 to 3.5 bps across the curve today with CZK reversing yesterday’s losses at EUR/CZK 25.36.

Norwegian headline and core inflation both rose by 0.2% M/M in March, compared with consensus estimates of 0.5% and 0.4% respectively. Especially food and non-alcoholic beverages (1.9% M/M) and recreation and culture (-0.4% M/M) contributed to this lower outcome. As a result, annual inflation fell more than hoped, from 4.5% Y/Y to 3.9% Y/Y at the top level and from 4.9% to 4.5% for the core gauge (lowest level in 20 months). Today’s data back the case of a first rate cut by the Norges bank in autumn (September 16). The market implied probability of this scenario rose from 50% to 65% after the CPI release. The Norwegian krone trades volatile near 11.60.

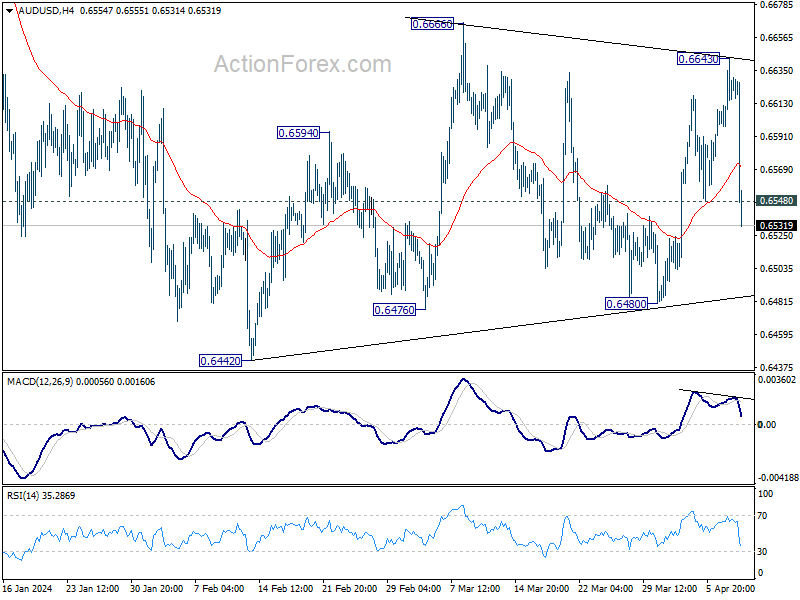

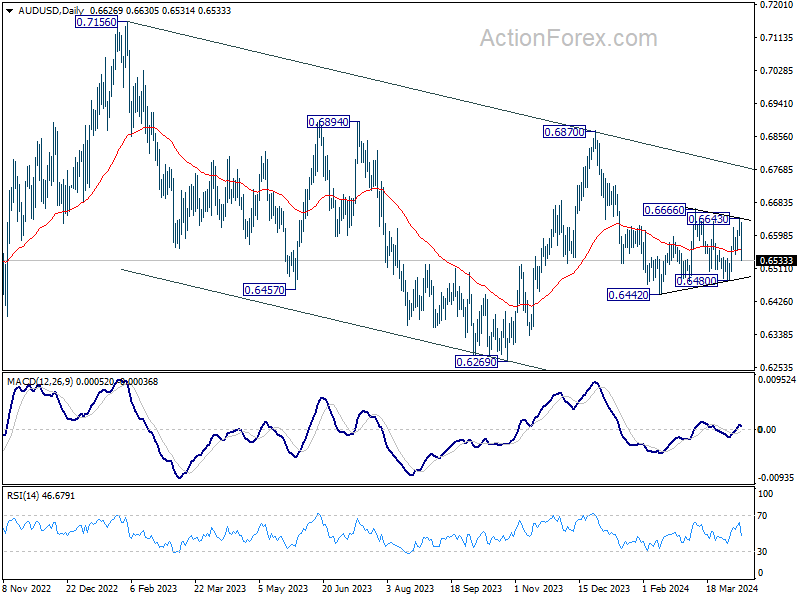

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6602; (P) 0.6624; (R1) 0.6649; More...

AUD/USD's break of 0.6548 suggests that rebound from 0.6480 has completed at 0.6643. Intraday bias is back on the downside for 0.6480 support. Firm break there will argue that whole fall from 0.6870 is ready to resume through 0.6442 support. For now, risk will stay mildly on the downside as long as 0.6643 resistance holds, in case of recovery.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which might still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

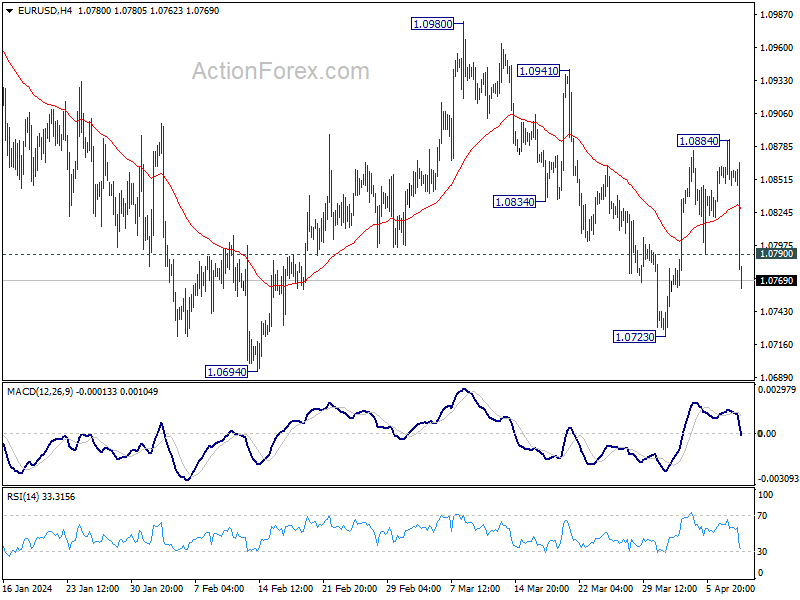

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0842; (P) 1.0863; (R1) 1.0879; More...

EUR/USD's break of 1.0790 support argues that rebound from 1.0723 has completed at 1.0884 already. Intraday bias is back on the downside of 1.0723 support. Break there will target 1.0694 support next. For now, risk will stay mildly on the downside as long as 1.0884 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

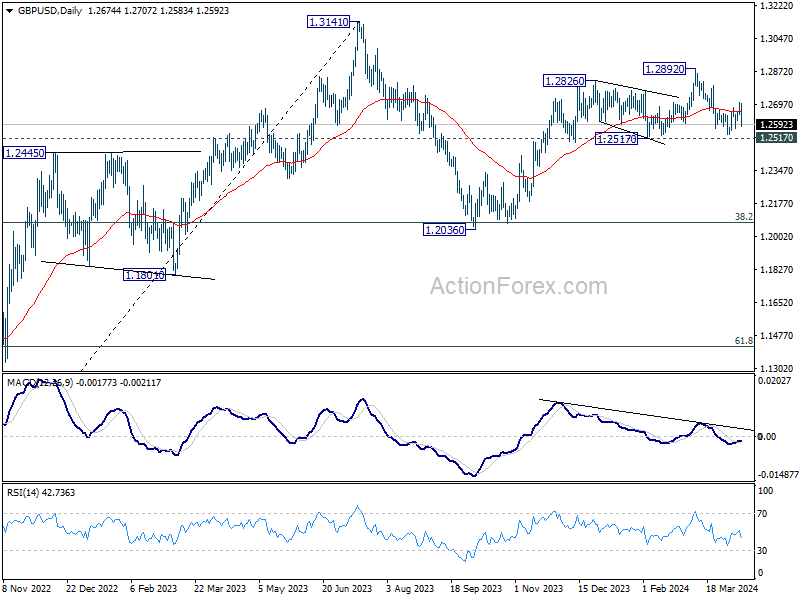

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2645; (P) 1.2677; (R1) 1.2709; More...

GBP/USD's sharp decline argues that rebound from 1.2538 has completed at 1.2708 already. Intraday bias is back on the downside for retesting 1.2517 key support. Sustained break there will turn near term outlook bearish. For now, risk will stay mildly on the downside as long as 1.2708 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which might still be in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.