Sample Category Title

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9796; (P) 0.9817; (R1) 0.9830; More...

Intraday bias in EUR/CHF remains neutral as consolidation from 0.9847 is extending. Near term outlook will stay bullish as long as 0.9709 support holds. Break of 0.9847 will resume larger rise from 0.9252. However, considering bearish divergence condition in 4H MACD, break of 0.9709 will confirm short term topping, and turn bias back to the downside for deeper pullback.

In the bigger picture, a medium term bottom should be in place at 0.9252 already, on bullish convergence condition in W MACD. Rise from there would now target 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even as a correction to the down trend from 1.2004. This will remain the favored case as long as 55 D EMA (now at 0.9603) holds.

All Eyes Turn to US March CPI Today

Markets

The payrolls-effect on core bond yields faded ahead of the important US CPI figures scheduled for release today. US Treasuries recovered, pushing yields between 4.7 and 6.2 bps lower. German rates dropped 3.9 (2y) to 7 bps (30y) with the ECB’s Bank Lending Survey strengthening the case for a June rate cut. That said, there’s compelling evidence that the peak impact of the ECB’s hikes is well behind us, possibly aligning the credit and business (e.g. PMIs) cycle. Either way, a Bund rally into the European close tackled the euro on FX markets. EUR/USD retreated from an intraday high around 1.088 back to opening levels of 1.0857. The trade-weighted dollar found support from the 104 big figure and the Japanese yen wasn’t impressed by another series of verbal warnings nor by “people familiar with the matter” suggesting the BoJ would raise the inflation outlook in the April forecasts. USD/JPY isn’t going anywhere just south of 152, a level that’s said to trigger FX interventions if surpassed. Oil prices again eased sub $90/b (Brent) on reports of rising inventories.

All eyes turn to US March CPI today. Fed’s Bostic late yesterday reiterated he expects a slow pace of disinflation for the remainder of 2024. It’s key in his projection of only one rate cut this year. Bostic didn’t rule out the possibility of that one cut being moved out further in time, implying no rate cuts at all in 2024. Bostic is on the same page as his colleague Kashkari and we’re keen to find out who else is, perhaps in tonight’s FOMC meeting minutes. Headline CPI inflation for March is expected to reaccelerate in year-on-year terms due to low base effects from last year and solid current price increases. A “mere” 0.3% m/m rise would push up the y/y from 3.2% to 3.4%. Risks are tilted to the upside. Combined with underlying gauges stalling (core inflation 3.7%) the case for a Fed rate cut is diminishing fast. Not only in June but also in July. US yields across the spectrum after today should already find a bottom after yesterday’s minor decline. The first meaningful resistance in the 2y yield is situated at 5% with the 10y eyeing 4.54%. The US dollar is dealt the best cards against the euro considering tomorrow’s ECB meeting will probably pave the way for a June rate cut. EUR/USD 1.0793 may crack soon.

News & Views

The Reserve Bank of New Zealand kept its policy rate unchanged at 5.5%. The MPC agreed that interest rates need to remain a restrictive level for a sustained period to ensure annual price inflation returns to the 1%-3% target range (expected this calendar year). The Committee noted that most major central banks are cautious about easing monetary policy given the ongoing risk of persistent inflation. The balance of (inflation) risks was little changed. Persistent services inflation, elevated goods price inflation and anticipated increases to local government rates, insurance and utility costs pose upside risks. The ongoing restrictive monetary policy in an environment of weak global growth and structural challenges facing the Chinese economy entail downside risks. New Zealand economic growth is weak, but evolved broadly in line as expected since the February Monetary Policy Report. NZD swap rates follow yesterday’s global move this morning with yields succumbing 2.5 bps (2-yr) to 6 bps (30-yr). The kiwi dollar exploits USD weakness with NZD/USD rising to 0.6070, its highest level since the FOMC meeting.

Rating agency Fitch downgraded the outlook on China’s A+ rating from stable to negative. The revision reflects increasing risks to China’s public finance outlook as the country contends with more uncertain economic prospects amid a transition away from property-reliant growth to what the government views as a more sustainable growth model. Wide fiscal deficits and rising government debt have eroded fiscal buffers from a rating perspective with fiscal policy expected to keep playing an important role in supporting growth. Fitch forecasts the government deficit to rise to 7.1% of GDP in 2024 from 5.8% in 2023 with the debt ratio set to increase from 56.1% to 61.3% this year. GDP growth is likely to slow to 4.5% this year with deflation risks still lingering (0.7% inflation by end-2024 and 1.3% by end-2025). S&P and Moody’s hold similar Chinese credit rating with Moody’s also applying a negative outlook (since December 2023).

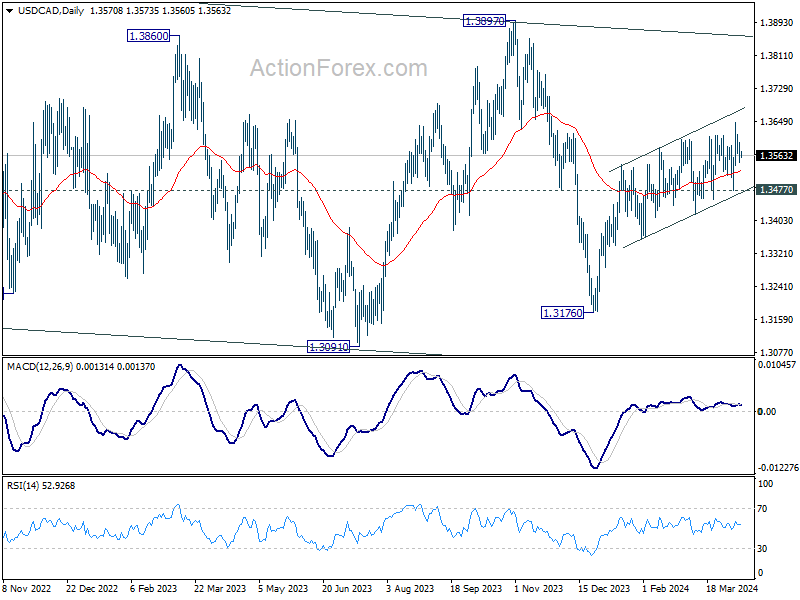

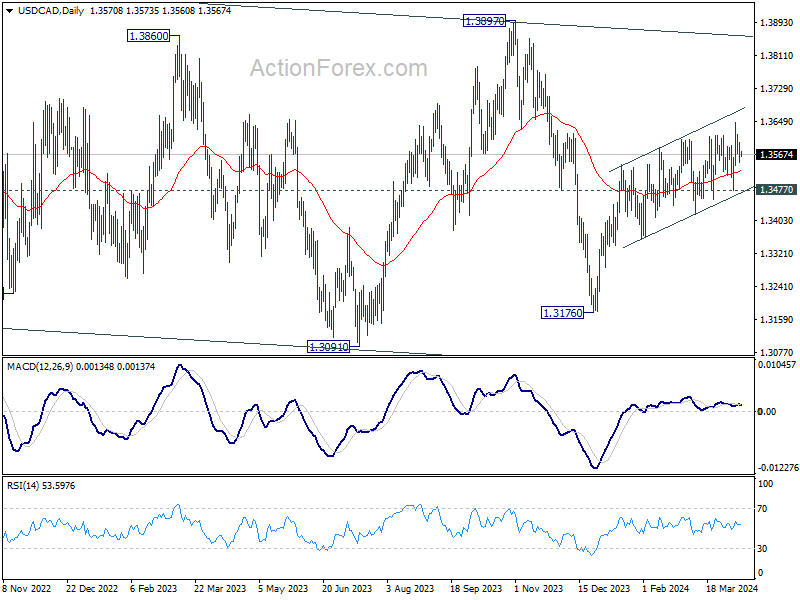

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3546; (P) 1.3572; (R1) 1.3598; More...

Intraday bias in USD/CAD remains neutral for the moment. Some consolidations would be seen but further rally is still expected as long as 1.3477 support holds. Break of 1.3646 will resume the rise from 1.3716. Sustained break of channel resistance would prompt upside acceleration towards 1.3897 resistance next. However, firm break of 1.3477 will argue that rise from 1.3176 has completed and turn outlook bearish.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

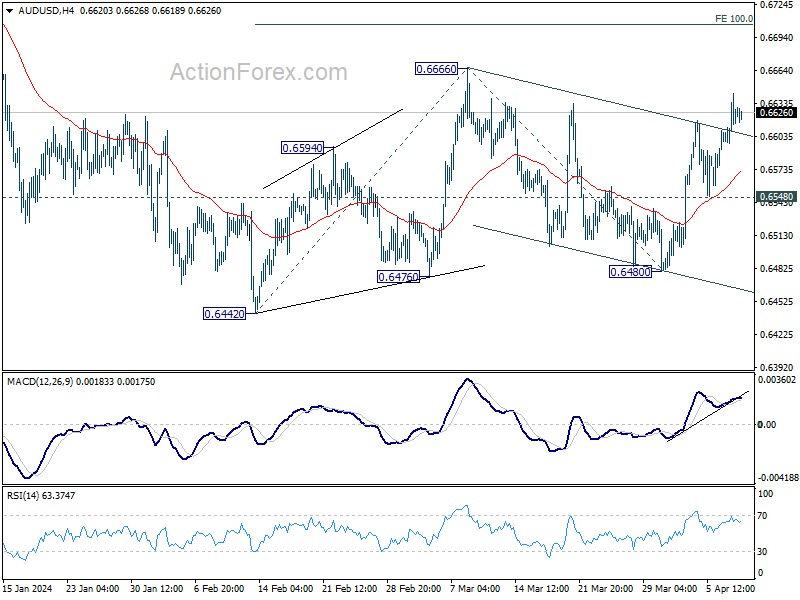

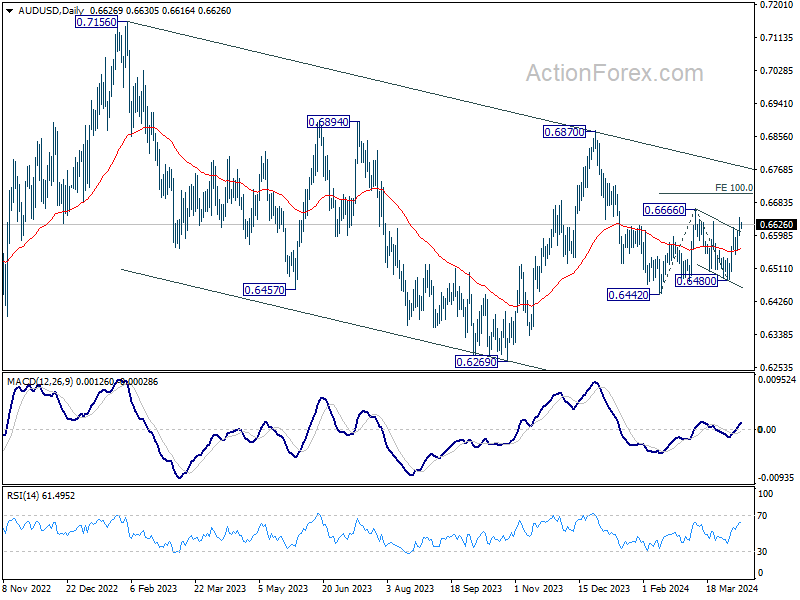

AUD/USD Daily Report

Daily Pivots: (S1) 0.6602; (P) 0.6624; (R1) 0.6649; More...

Intraday bias in AUD/USD remains on the upside at this point. Rise from 0.6480 is seen as the third leg of the pattern from 0.6442. Further rally would be seen to 0.6666 resistance, and then 100% projection of 0.6442 to 0.6666 from 0.6480 at 0.6704. Nevertheless, break of 0.6548 support will turn bias back to the downside instead.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which might still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

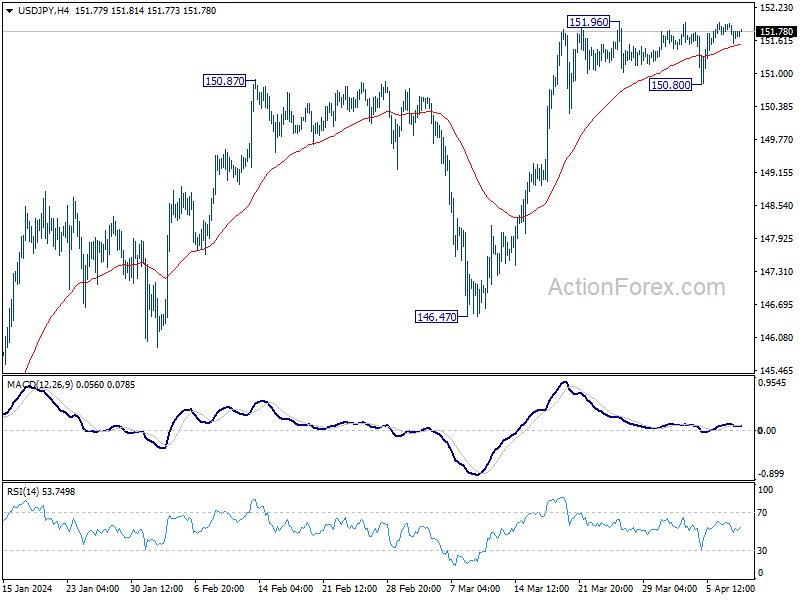

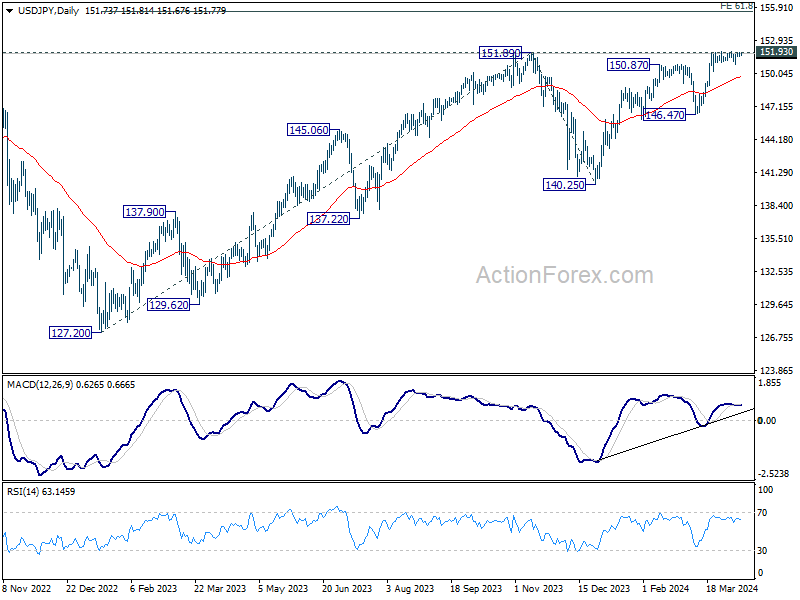

USD/JPY Daily Outlook

Daily Pivots: (S1) 151.59; (P) 151.76; (R1) 151.96; More...

Range trading continues in USD/JPY and intraday bias stays neutral at this point. On the downside, break of 150.80 will turn bias back to the downside for deeper pull back to 55 D EMA (now at 149.73). On the upside, however, sustained break of 151.93 key resistance will confirm long term up trend resumption.

In the bigger picture, correction from 151.87 (2023) high could have completed at 140.25 already. Rise from 127.20 (2023 low), as part of the long term up trend, is probably ready to resume. Decisive break of 151.93 resistance (2022 high) will confirm this bullish case. Next medium term target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. This will remain the favored case as long as 146.47 support holds, in case of another pullback.

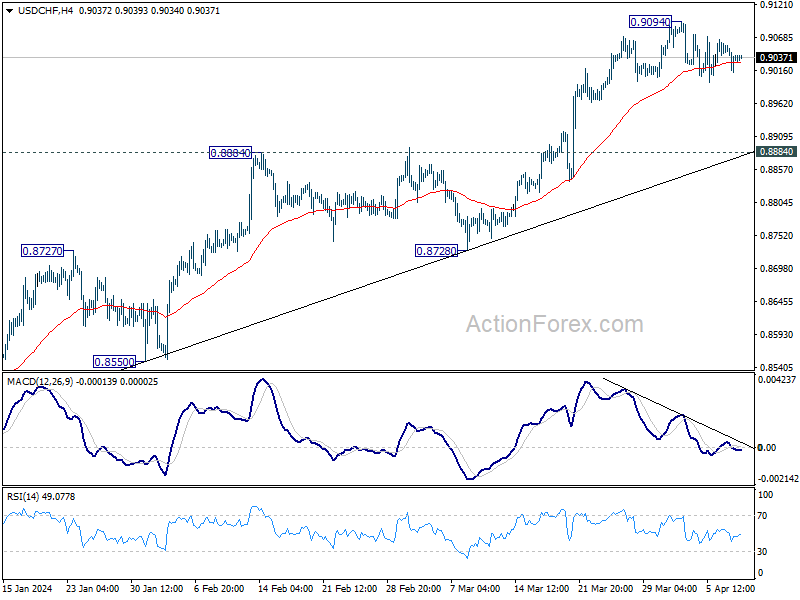

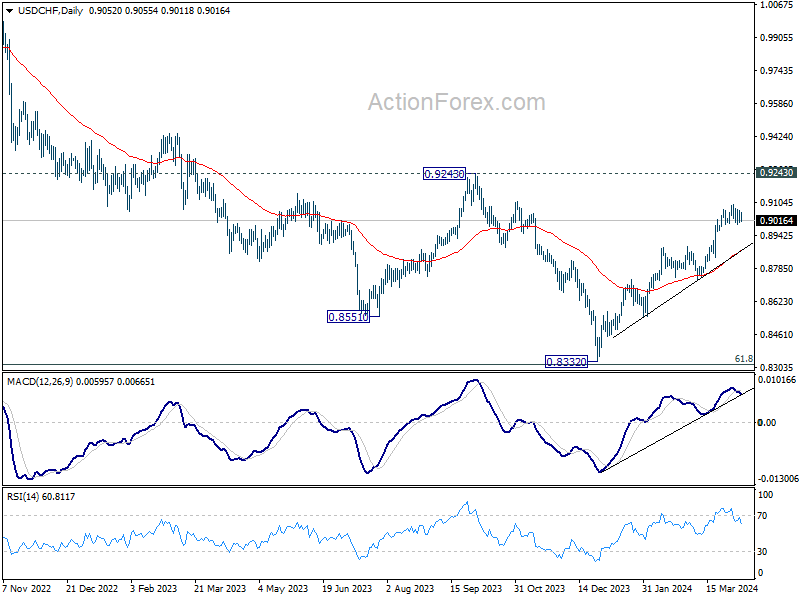

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9011; (P) 0.9038; (R1) 0.9064; More....

Intraday bias in USD/CHF remains neutral and consolidation from 0.9094 is extending. Deeper decline cannot be ruled out, but outlook will stay bullish as long as 0.8884 resistance turned support holds. On the upside, break of 0.9094 will resume larger rise from 0.8332 to 0.9243 key resistance.

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.

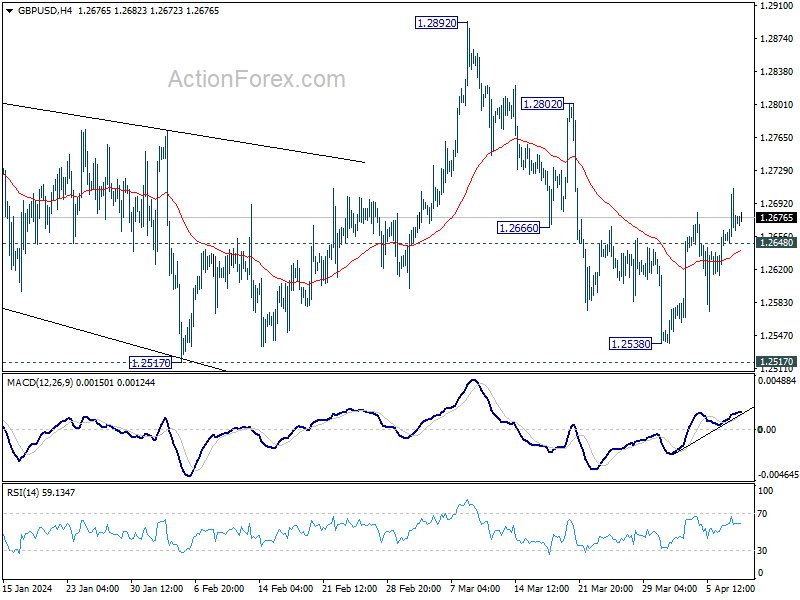

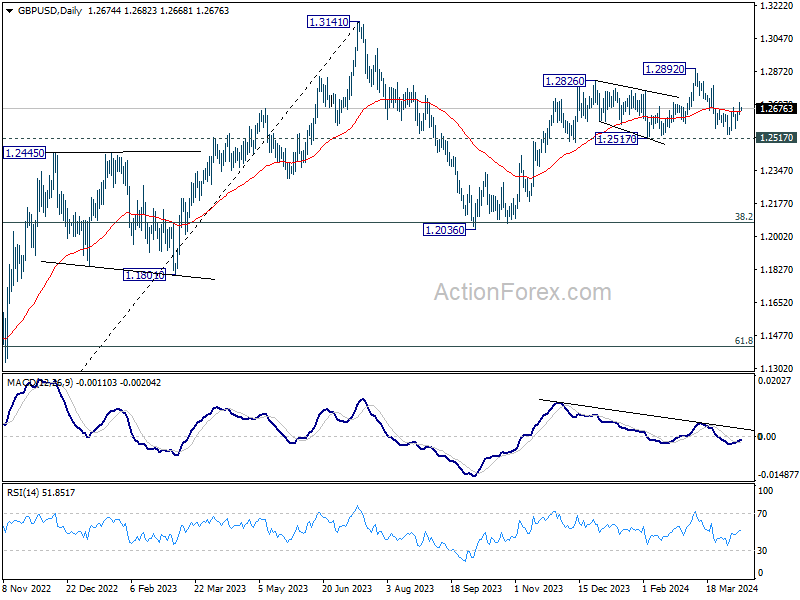

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2645; (P) 1.2677; (R1) 1.2709; More...

Intraday bias in GBP/USD stays mildly on the upside at this point. Rebound from 1.2538 is in progress for 1.2802 resistance first. On the downside, though, below 1.2648 minor support will turn intraday bias neutral again.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which might still be in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Markets in Waiting Position for US March CPI

In focus today

Today's focus will be on the US March CPI, where we forecast both headline and core inflation at +0.3% m/m SA. Higher oil prices continue to lift headline inflation, but the Fed focuses more on the underlying price pressures, not least after concerning upticks in services inflation and strong labour market in early 2024. In the evening, minutes from FOMC's March meeting are also due for release.

This morning, in Sweden we get the GDP Indicator for February as well as PVI and consumption indicators. We expect in the numbers to support our case for improved economic activity and our view of a decent start to the year.

We will get March inflation from Norway this morning. There has been a clear disinflationary trend in Norway in recent months. Although we believe that the declining trend will continue throughout the year, we will probably see a certain correction after the low February figures. Hence, we expect core inflation rose 0.3% m/m, which will pull annual growth down to 4.6% in March. In that case, it will be marginally lower than Norges Bank's estimate from the monetary policy report of 4.7%.

Overnight, Chinese CPI for March is due and is expected to decline from 0.7% y/y to 0.4% y/y as Chinese New Year effects fall out again.

Economic and market news

What happened overnight

As expected, the Reserve Bank of New Zealand kept its policy rate unchanged at 5.50%. Otherwise, things were generally quiet as markets await today's release of the US March CPI.

What happened yesterday

The ECB bank lending survey showed that credit standards remained tight in the euro area while loan demands from firms declined substantially. This suggests a muted growth outlook for the euro area in the next quarters, which supports a June rate cut from the ECB.

The US NFIB's small business optimism index declined to 88.5, which is the lowest level in 11 years. The decline was mainly due to concerns about inflation, and rising input and labour costs.

In the chips space, we got news that TSMC was awarded a USD 6.6bn subsidy for advanced semiconductor manufacturing in the U.S, to support a planned investment of USD 65bn. TSMC supplies the world's most advanced chips and most of their current capacity is in Taiwan, so this is a step in the direction of more diversified semiconductor production capacity and in general an example of major diversification of supply chains.

Equities: Global equities were higher yesterday with European markets going against the trend as especially defence stocks took a heavy beating. The turnaround in defence stocks came as stories about increased likelihood of ceasefire in Gaza got more attention across newswires. Sector rotations revealed a bit of a wait-and-see game ahead of CPI today, ECB tomorrow and the earnings season start on Friday. In US yesterday Dow -0.02%, S&P 500 +0.1%, Nasdaq +0.3%, Russell 2000 +0.3%. Asian markets are higher this morning led by China. US and European futures higher as well.

FI: Long-end rates in the US and Europe gradually drove lower in yesterday's session, reversing some of the sharp rises seen on the back of Friday's NFP report. There was no obvious trigger explaining the move, which happened smoothly through the session. 10Y Bund yields dropped 6bp to 2.37% with the 2s10s curve bull flattening 3bp, while 10Y UST yields are 7bp lower at 4.35%. The 5Y5Y EUR inflation swap rate fell a few bp to 2.31% as energy prices reversed a bit of the recent gains with Brent now trading below USD90/barrel. Long-end BTPs outperformed the core despite the worsening outlook for the deficit presented by the Italian government yesterday.

FX: Yesterday's session did not deliver any major moves in G10 FX. EUR/USD remained around 1.0850. USD/JPY remains slightly below 152. EUR/SEK is hovering around 11.45. EUR/NOK is trading just below 11.60. EUR/GBP declined around 0.8560.

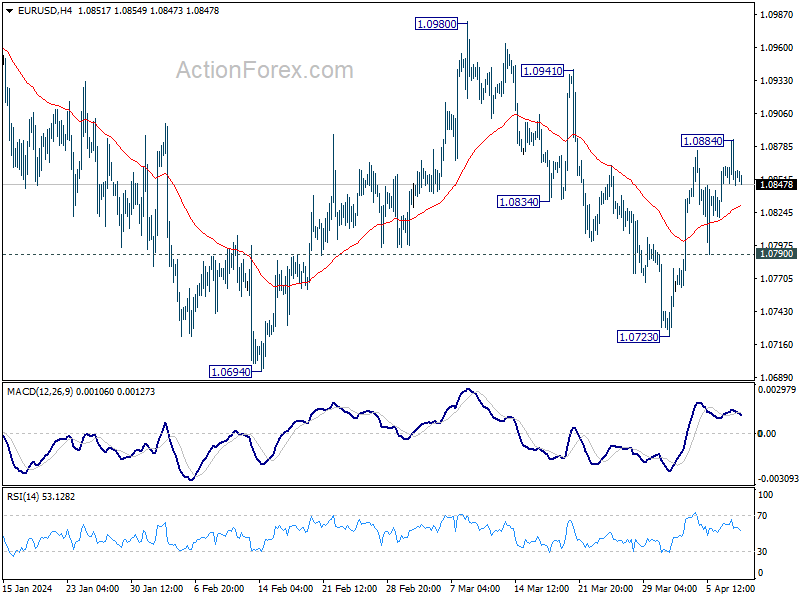

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0842; (P) 1.0863; (R1) 1.0879; More...

EUR/USD retreated after edging higher to 1.0884 and intraday bias is turned neutral again. Further rise would be mildly in favor as long as 1.0790 minor support holds. Above 1.0884 will resume the rebound form 1.0723 to 1.0941 resistance first. However, break of 1.0790 will turn bias back to the downside for 1.0723 instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

Kiwi Rallies on RBNZ’s Hawkish Hold; US CPI and BoC Next

New Zealand Dollar rises broadly in Asian session following RBNZ's decision to keep interest rates steady. The central bank's "limited tolerance" for delaying the achievement of its inflation target conveyed a hawkish tone. Rate cuts are off the table until the central bank is confidence that inflation would sustainably return to the target band. This is clear indication of priority over inflation control, even amidst a slowing economy. However, strength of Kiwi remains measured, with traders likely awaiting next week's Q1 inflation data for a more decisive bet

Now, the financial world turns its attention to three significant events of the day: BoC rate decision, US CPI release, and the minutes from FOMC meeting. The focus for BoC lies in whether Governor Tiff Macklem or the economic projections would start preparing the markets for a June rate cut. Meanwhile, expectations set US headline CPI to increase to 3.4% for March, with core CPI anticipated to decelerate to 3.7%. Any upside surprises in today's data could upend expectations for a June Fed rate cut, sending stocks and bonds lower while pushing Dollar higher.

For the week so far, New Zealand Dollar leads in strength, followed by Australian Dollar and Sterling, while Swiss Franc, Yen, and Dollar lag behind. Euro and Canadian Dollar find themselves in the middle of the performance spectrum.

Technically, NZD/USD's rebound from 0.5938 short term bottom is still in progress, but it's struggling to rises through 55 D EMA (now at 0.6077). While further rally cannot be ruled out, strong resistance should be seen from channel resistance (now at 0.6140) to cap upside. Below 0.5894 minor support will argue that fall from 0.6368 is ready to resume through 0.5938.

In Asian, at the time of writing, Nikkei is down -0.42%. Hong Kong HSI is up 1.87%. China Shanghai SSE is down -0.77%. Singapore Strait Times is up 0.67%. Japan 10-year JGB yield is up 0.0135 at 0.798. Overnight, DOW fell -0.02%. S&P 500 rose 0.14%. NASDAQ rose 0.32%. 10-year yield rose 0.069 to 4.378.

RBNZ holds OCR steady, no room for delay in bring down inflation to target band

RBNZ maintained Official Cash Rate unchanged at 5.50%, aligning with market expectations. This decision comes with reiterated commitment to "restrictive monetary policy stance," deemed necessary to alleviate capacity pressures and guide inflation back within the target range of 1 to 3 percent within "this calendar year".

During the recent meeting, members concurred that there has been "no material change in economic outlook" since their February Statement. There remains a "limited tolerance" for prolonging the timeframe to meet the inflation target, especially with inflation expectations and pricing intentions continuing to "remain elevated".

The "persistence of services inflation" and "elevated" goods price inflation were identified as continuous risks, with expected near-term increases in local government rates, insurance, and utility costs potentially decelerating the reduction in headline inflation.

On the flip side, RBNZ acknowledges potential downside risks to the inflation outlook, notably the impact of continued restrictive monetary policy amid weak global growth. This environment could precipitate a quicker than anticipated reduction in inflation. Weak business and consumer confidence, coupled with potential increases in unemployment and financial stress, are areas of concern. Additionally, structural economic challenges in China are highlighted as significant, given its critical role in the global economy and as a major trading partner for New Zealand.

Will BoC's Macklem Pave the Way for June Rate Reduction?

BoC is widely expected to keep interest rate unchanged at 5.00% today and the main focus is whether Governor Tiff Macklem would start to change the tune to lay down the groundwork for a June rate cut. With new economic projections on the table, this meeting presents an opportune moment for such indications.

A recent Reuters poll revealed a consensus among economists, with 27 out of 38 forecasting a 25 bps cut by BoC in June. Meanwhile, 7 expected the cut in July and 4 in September. By the year's end, the expectation is for a 100 bps cumulative reduction, bringing the rate down to 4.00%.

Despite these anticipations, a noteworthy portion of economists — 13 out of 16 — who responded to an additional query, suggested that the timing of the first rate cut is more likely to be delayed than they expected. Moreover, 11 of them believe there's a heightened risk of fewer rate cuts than initially forecasted.

While USD/CAD's rebound from 1.3176 has persisted in the last few months, momentum is clearly lacking as seen in both the structure of the rise, as well as in D MACD. Break of 1.3477 support the first signal that such rebound has completed as a corrective move. Nevertheless, firm break of the upper channel line will likely prompt upside acceleration towards 1.3897 resistance. Today's BoC decision is poised to significantly influence the currency's next move.

BoJ's Ueda: Accommodative monetary policy to continue

In today's parliamentary address, BoJ Governor Kazuo Ueda reaffirmed the Bank of Japan's stance on continuing its accommodative monetary policy, underscoring the short-term interest rate as the "primary policy tool."

A key focus for BoJ, as Ueda noted, is the scrutiny of trend inflation's progress towards 2% target in judging "appropriate degree of monetary support."

Meanwhile, Ueda clarified that BoJ would not alter its monetary policy solely in response to FX fluctuations. However, he acknowledged that significant FX movements, if they lead to an unexpected increase in import prices and thereby risk elevating trend inflation beyond projections, could necessitate a reassessment of monetary policy.

Fed's Bostic: Rate cuts may have to move further out

Atlanta Fed President Raphael Bostic recently highlighted the possibility that rate cuts May have "to move further out" given that the US economy economy has been "so robust, and so strong, and so resilient".

Further elaborating on his perspective in a Yahoo Finance interview, Bostic referred to his previous dot-plot submission, where he initially projected two rate cuts for the year, influenced by the rapid inflation decline in the latter half of 2023.

However, "What happened for me is that it slowed down and the pace went back to the pace that I had expected initially, which had me at one cut," Bostic explained.

SNB's Schlegel: Interventions contributes to price stability

SNB Vice Chairman Martin Schlegel defended the central bank's use of foreign exchange interventions, highlighting their effectiveness in maintaining price stability within Switzerland.

"Have foreign exchange interventions contributed to achieving price stability? Yes, they have," he said at an event in Geneva overnight.

He further elaborated that without utilizing foreign currency sales, SNB would have faced the necessity to escalate the policy rate significantly higher.

Schlegel also noted a modest average of 0.3% over the last fifteen years. He argued that, in the absence of foreign exchange purchases, inflation rates would have dipped considerably lower, potentially entering deflationary territory.

"Estimates suggest that it would have been significantly below zero without the purchases; we would thus not have fulfilled our mandate," Schlegel pointed out.

Looking ahead

Italy retail sales will be released in European session. Later in the day, US CPI and BoC rate decisions are the main feature.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0842; (P) 1.0863; (R1) 1.0879; More...

EUR/USD retreated after edging higher to 1.0884 and intraday bias is turned neutral again. Further rise would be mildly in favor as long as 1.0790 minor support holds. Above 1.0884 will resume the rebound form 1.0723 to 1.0941 resistance first. However, break of 1.0790 will turn bias back to the downside for 1.0723 instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Mar | 3.20% | 3.10% | 3.00% | |

| 23:50 | JPY | PPI Y/Y Mar | 0.80% | 0.80% | 0.60% | 0.70% |

| 02:00 | NZD | RBNZ Rate Decision | 5.50% | 5.50% | 5.50% | |

| 08:00 | EUR | Italy Retail Sales M/M Feb | 0.20% | -0.10% | ||

| 12:30 | CAD | Building Permits M/M Feb | -3.50% | 13.50% | ||

| 12:30 | USD | CPI M/M Mar | 0.30% | 0.40% | ||

| 12:30 | USD | CPI Y/Y Mar | 3.40% | 3.20% | ||

| 12:30 | USD | CPI Core M/M Mar | 0.30% | 0.40% | ||

| 12:30 | USD | CPI Core Y/Y Mar | 3.70% | 3.80% | ||

| 13:45 | CAD | BoC Rate Decision | 5.00% | 5.00% | ||

| 14:00 | USD | Wholesale Inventories Feb F | 0.50% | 0.50% | ||

| 14:30 | USD | Crude Oil Inventories | 0.9M | 3.2M | ||

| 15:30 | CAD | BoC Press Conference | ||||

| 18:00 | USD | FOMC Minutes |