Sample Category Title

Will BoC’s Macklem Pave the Way for June Rate Reduction?

BoC is widely expected to keep interest rate unchanged at 5.00% today and the main focus is whether Governor Tiff Macklem would start to change the tune to lay down the groundwork for a June rate cut. With new economic projections on the table, this meeting presents an opportune moment for such indications.

A recent Reuters poll revealed a consensus among economists, with 27 out of 38 forecasting a 25 bps cut by BoC in June. Meanwhile, 7 expected the cut in July and 4 in September. By the year's end, the expectation is for a 100 bps cumulative reduction, bringing the rate down to 4.00%.

Despite these anticipations, a noteworthy portion of economists — 13 out of 16 — who responded to an additional query, suggested that the timing of the first rate cut is more likely to be delayed than they expected. Moreover, 11 of them believe there's a heightened risk of fewer rate cuts than initially forecasted.

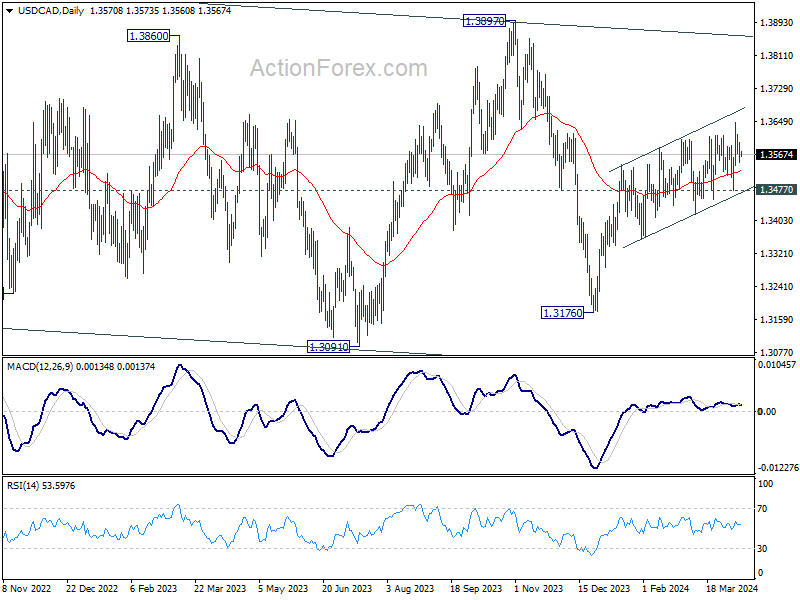

While USD/CAD's rebound from 1.3176 has persisted in the last few months, momentum is clearly lacking as seen in both the structure of the rise, as well as in D MACD. Break of 1.3477 support the first signal that such rebound has completed as a corrective move. Nevertheless, firm break of the upper channel line will likely prompt upside acceleration towards 1.3897 resistance. Today's BoC decision is poised to significantly influence the currency's next move.

RBNZ April 2024 Monetary Policy Review: Staying the Course

Staying the course

- The RBNZ left the OCR at 5.5% as expected.

- The record of the meeting states that the risks to the outlook were viewed as "little changed" since the February Statement.

- The minutes noted the potential for a more flexible approach once inflation returns to the target range and when inflation expectations and pricing intentions are no longer elevated.

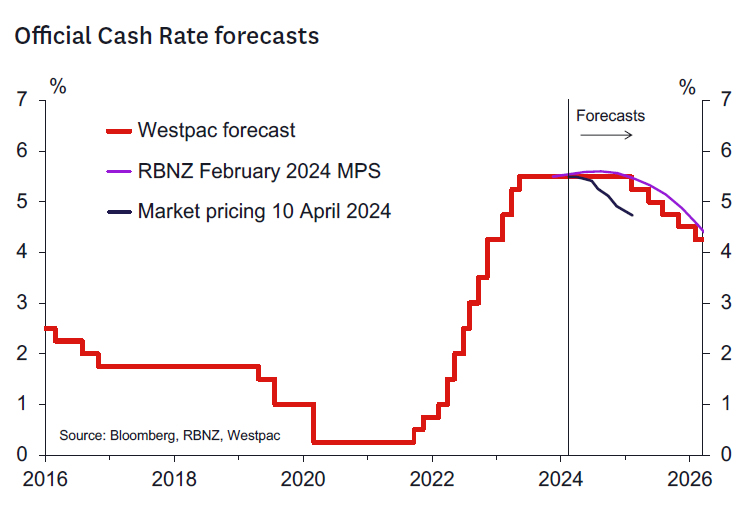

- The RBNZ's monetary policy strategy looks unchanged, implying the OCR will remain at 5.5% until 2025 – in line with Westpac's forecasts. The RBNZ is staying the course.

- We continue to forecast the OCR to remain at 5.5% in 2024 and be reduced from February 2025.

As we discussed in our Monetary Policy Review preview note, the data flow since the February Statement has not suggested a significant change in the outlook for inflation and the OCR. In general, data suggests:

- A modestly weaker demand picture than expected as the Q4 GDP data were a touch weaker than forecast while confidence indicators show the shine is coming off a bit such that a pickup in growth in H2 might be less certain.

- But the inflation picture looks less favourable than the RBNZ hoped. The near-term CPI outlook seems stronger than the RBNZ expected, as confirmed by the recent monthly price index data. In addition, the exchange rate is weaker, energy prices are a lot stronger, and pricing indicators in sentiment surveys point to lingering cost pressures.

The RBNZ picked up on many of these themes in their relatively short press statement (140 vs 309 words in February) and record of meeting. Key points were:

- Risks to the outlook for inflation were assessed as similar to the February Statement. Upside risks from services prices, local authority rates insurance and utility costs were noted as were downside risks coming from the long period of restrictive policy in a weak global growth environment.

- The global backdrop was assessed as similar to February. Labour markets remain tight but the potential lower policy rates offshore remains.

- The RBNZ still sees a need for the OCR to remain restrictive "for a sustained period".

- The RBNZ's focus remains on returning inflation to the mid-point of the 1-3% target range. However, the minutes noted the potential for more flexibility on this once inflation is back inside the target range and when inflation expectations and pricing intentions are no longer elevated.

We continue to see the OCR as remaining on hold through 2024 with a gradual reduction in the OCR coming from the February Statement. Key data to watch between now and the May Statement include:

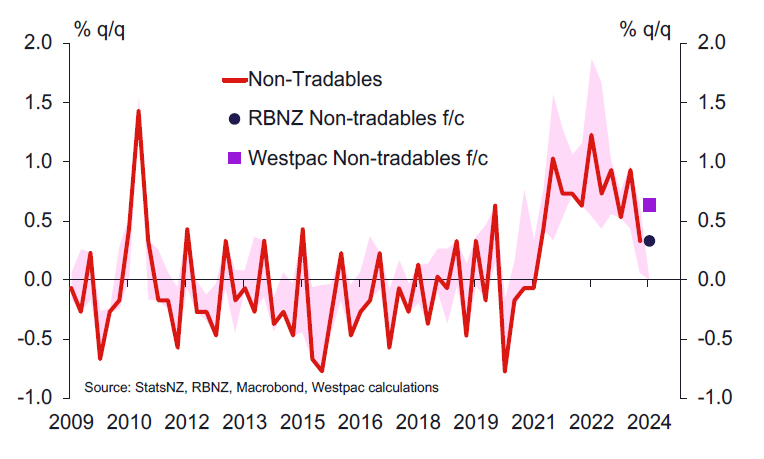

- The March quarter CPI (17 April) where the level of core inflation will be especially key (Headline CPI forecasts: RBNZ February 0.4% q/q, WBC 0.8% q/q, Nontradables CPI forecasts: RBNZ February 1.1% q/q, WBC 1.4% q/q).

- The March quarter labour market reports (1 May) where long awaited signs of labour market adjustment will be sought (Unemployment rate forecasts: RBNZ February 4.2%, WBC 4.3%, Private Sector LCI wages forecasts: RBNZ February 0.8% q/q, WBC 0.8% q/q). Global financial market developments will also be of relevance – especially the exchange rate and oil price developments as these will be crucial for determining the near-term CPI profile.

- As we anticipated, this unchanged outlook probably comes as a disappointment to those market participants looking for signs of an imminent RBNZ dovish pivot. However, there has been only a modest reaction to the statement in interest rate markets, which continue to price about 59bps of policy easing by the end of this year. The revised language around the potential flexibility the RBNZ might have around the timing of the return of inflation to the 2% mid-point is interesting and pragmatic. While inflation is likely to be within the target range by the end of the year, pricing intentions and inflation expectations indicators remain elevated and are only slowly falling. Watching that data as we progress through the year seems appropriate.

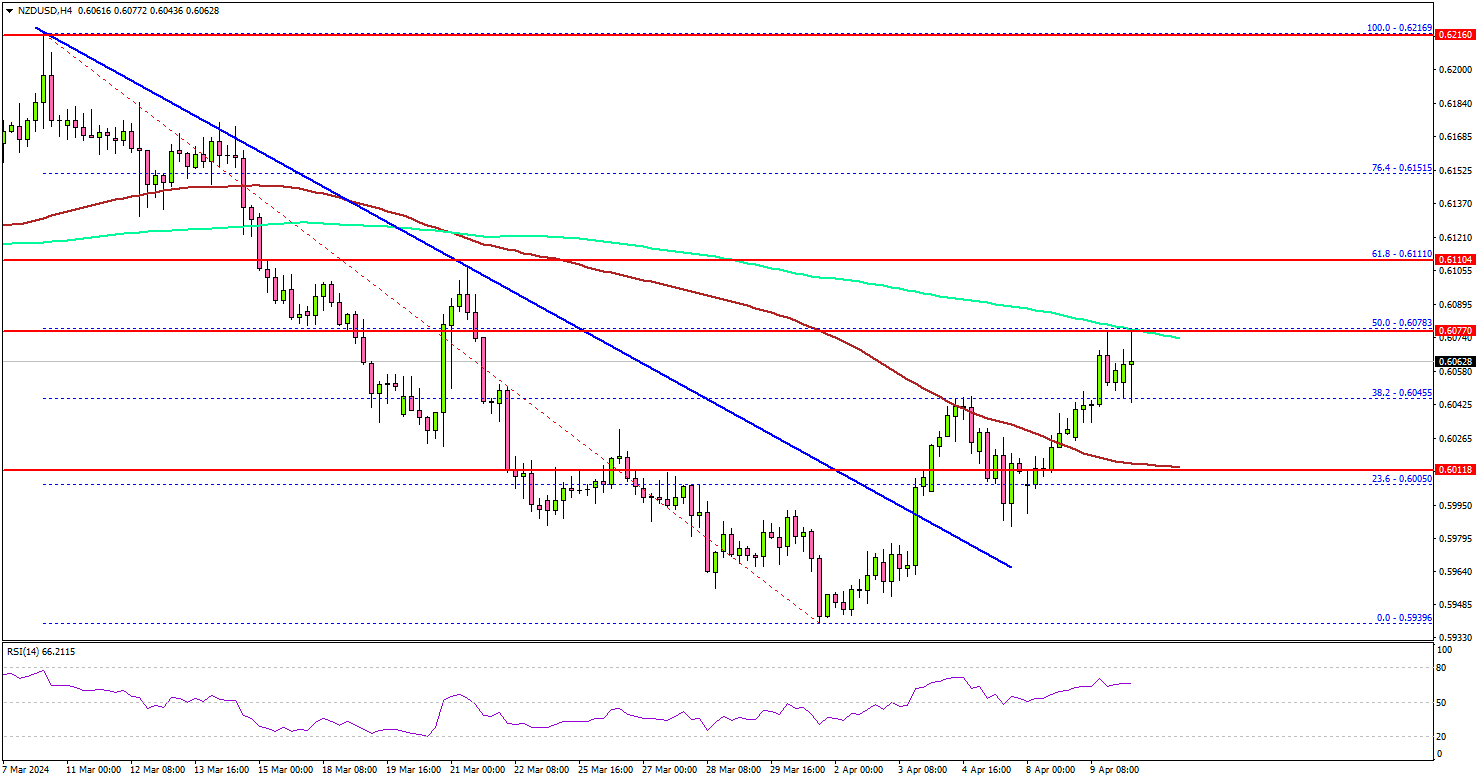

NZD/USD Signals Breakout, US CPI Report Next

Key Highlights

- NZD/USD is attempting a fresh increase above the 0.6000 resistance zone.

- It broke a major bearish trend line with resistance at 0.5990 on the 4-hour chart.

- Gold prices remain elevated ahead of the US CPI release and FOMC meeting minutes.

- The US CPI could increase by 3.4% in March 2024 (YoY).

NZD/USD Technical Analysis

The New Zealand started a recovery wave from the 0.5940 zone against the US Dollar. NZD/USD cleared many hurdles near 0.5990 and 0.6000 to move into a positive zone.

Looking at the 4-hour chart, the pair broke a major bearish trend line with resistance at 0.5990. There was a move above the 38.2% Fib retracement level of the downward move from the 0.6216 swing high to the 0.5939 low.

The pair even settled above the 100 simple moving average (red, 4-hour) and tested the 200 simple moving average (green, 4-hour).

On the upside, the pair is facing hurdles near 0.6080. It is close to the 50% Fib retracement level of the downward move from the 0.6216 swing high to the 0.5939 low. A clear move above the 0.6080 resistance could send the pair further higher. In the stated case, NZD/USD could rise toward the 0.6200 level.

Immediate support is near the 0.6050 level. The next major support is at 0.6020 and the 100 simple moving average (red, 4-hour).

If there is a downside break below the 0.6020 support, the pair could decline toward the 0.5950 support. Any more losses might send the pair toward the 0.5920 level in the near term.

Looking at Gold, the price remained stable near $2,350 and there are still chances of more upsides toward the $2,380 level.

Economic Releases

- US Consumer Price Index for March 2024 (MoM) – Forecast +0.3%, versus +0.4% previous.

- US Consumer Price Index for March 2024 (YoY) – Forecast +3.4%, versus +3.2% previous.

- FOMC Meeting Minutes.

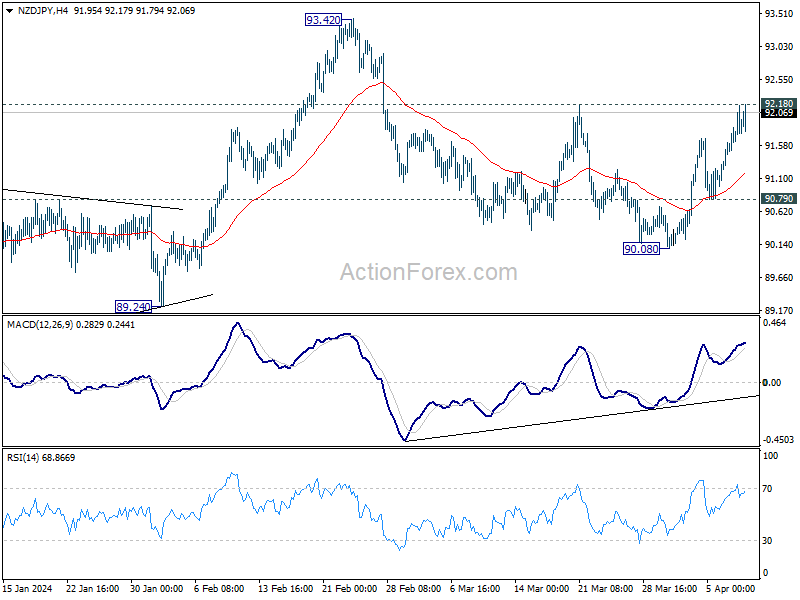

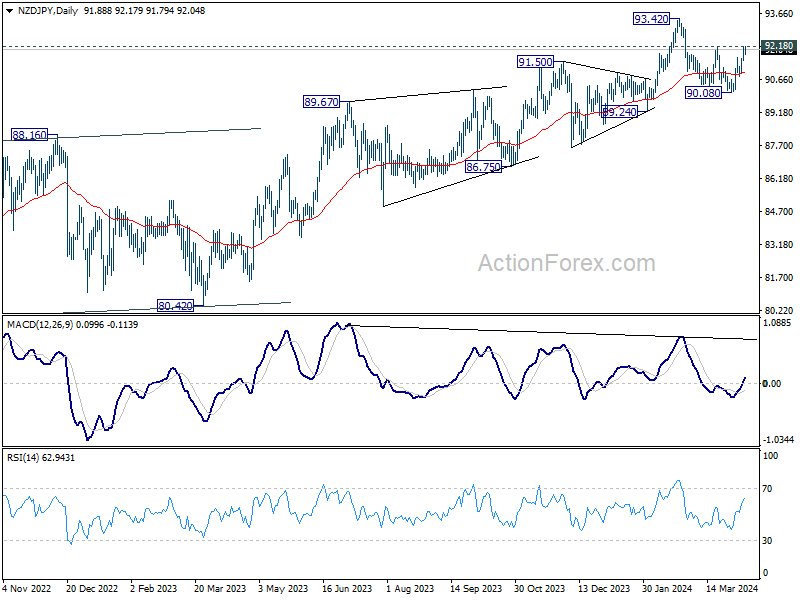

NZD/JPY steady after RBNZ, pressing 92.18 resistance

New Zealand Dollar is steady after RBNZ left interest rate unchanged and drops not clue on the timing of interest rate cuts. NZD/JPY's focus is staying on 92.18 resistance. Decisive break there will argue that corrective pull back from 93.42 has completed with three waves down to 90.08. larger rise from 80.42 would then be ready to resume through 93.42 high.

However, rejection by 92.18, followed by break of 90.79 support, will turn bias back to the downside for 90.08 support. Further break there will argue that NZD/JPY is possibly in larger scale correction.

RBNZ holds OCR steady, no room for delay in bring down inflation to target band

RBNZ maintained Official Cash Rate unchanged at 5.50%, aligning with market expectations. This decision comes with reiterated commitment to "restrictive monetary policy stance," deemed necessary to alleviate capacity pressures and guide inflation back within the target range of 1 to 3 percent within "this calendar year".

During the recent meeting, members concurred that there has been "no material change in economic outlook" since their February Statement. There remains a "limited tolerance" for prolonging the timeframe to meet the inflation target, especially with inflation expectations and pricing intentions continuing to "remain elevated".

The "persistence of services inflation" and "elevated" goods price inflation were identified as continuous risks, with expected near-term increases in local government rates, insurance, and utility costs potentially decelerating the reduction in headline inflation.

On the flip side, RBNZ acknowledges potential downside risks to the inflation outlook, notably the impact of continued restrictive monetary policy amid weak global growth. This environment could precipitate a quicker than anticipated reduction in inflation. Weak business and consumer confidence, coupled with potential increases in unemployment and financial stress, are areas of concern. Additionally, structural economic challenges in China are highlighted as significant, given its critical role in the global economy and as a major trading partner for New Zealand.

BoJ’s Ueda: Accommodative monetary policy to continue

In today's parliamentary address, BoJ Governor Kazuo Ueda reaffirmed the Bank of Japan's stance on continuing its accommodative monetary policy, underscoring the short-term interest rate as the "primary policy tool."

A key focus for BoJ, as Ueda noted, is the scrutiny of trend inflation's progress towards 2% target in judging "appropriate degree of monetary support."

Meanwhile, Ueda clarified that BoJ would not alter its monetary policy solely in response to FX fluctuations. However, he acknowledged that significant FX movements, if they lead to an unexpected increase in import prices and thereby risk elevating trend inflation beyond projections, could necessitate a reassessment of monetary policy.

(RBNZ) OCR 5.50% – Official Cash Rate remains unchanged

The Monetary Policy Committee today agreed to leave the Official Cash Rate (OCR) at 5.50 percent.

The New Zealand economy continues to evolve as anticipated by the Monetary Policy Committee. Current consumer price inflation remains above the Committee's 1 to 3 percent target range. A restrictive monetary policy stance remains necessary to further reduce capacity pressures and inflation.

Globally, while there are differences across regions, economic growth remains below trend and is expected to remain subdued. However, most major central banks are cautious about easing monetary policy given the ongoing risk of persistent inflation.

Economic growth in New Zealand remains weak. While some near-term price pressures remain, the Committee is confident that maintaining the OCR at a restrictive level for a sustained period will return consumer price inflation to within the 1 to 3 percent target range this calendar year.

Media contact

James Weir

Senior Adviser External Stakeholders

Phone: +64 4 471 3962 | Mobile: 021 103 1622

Email: James.Weir@rbnz.govt.nz

Summary Record of Meeting – April 2024

The Monetary Policy Committee discussed recent developments in the New Zealand and global economies. The Committee agreed that the New Zealand economy has evolved largely as expected since the February Statement. Restrictive monetary policy is contributing to an easing in capacity pressures to ensure inflation returns to target.

Economic growth in most of New Zealand's major trading partners has been below trend. However, this has varied across regions, with stronger activity in the United States compared with the Euro Area and Australia. Economic growth in most major economies is forecast to slow further over 2024. In China, policymakers have announced a similar growth target for this calendar year, which may be difficult to achieve amid ongoing structural challenges.

The Committee noted that in most major economies the better balance between the demand for, and supply of, labour has been reflected in a decline in job vacancies. However, growth in unit labour costs remains elevated. Inflation will continue to be persistent in regions where higher labour costs have not been accompanied by improved productivity or reduced profit margins.

Most major central banks remain cautious about easing monetary policy given the risks of inflation persistence and elevated inflation expectations. Financial market pricing for most central bank policy rates continues to imply some easing later this year, although this has lessened over recent weeks. Participants in global financial markets continue to exhibit strong confidence in the corporate earnings outlook, as reflected in equity prices and credit spreads.

Aggregate commodity price indices have remained relatively stable despite ongoing geopolitical uncertainties. Oil prices have increased while agricultural commodity prices have generally been weaker. The recent spike in global shipping costs, which has partially receded, has yet to be observed in New Zealand merchandise trade data. This timing is consistent with information from discussions with businesses that suggest shipping contracts in New Zealand are typically renegotiated every three to six months.

The Committee discussed domestic economic data released since the February Statement. Gross Domestic Product for the December 2023 quarter was close to expectations and implies a continued easing in capacity pressure in the economy. Some higher frequency indicators suggest a modest recovery in activity in the first quarter of 2024. However, measures of business confidence have declined and firms' own expectations for activity and investment have weakened. Near-term business pricing intentions have declined but remain elevated, in part reflecting an uptick in both realised and expected costs.

The Committee noted that recent monthly Selected Price Indices (SPI) imply some upside risk to the March 2024 quarter Consumers Price Index (CPI). The Committee agreed that there was large monthly variability in the SPI series and noted that recent relative price changes are due mostly to volatile components including fuel, domestic airfares, and overseas accommodation.

The Committee noted the continued strength in net migration, which is supporting aggregate consumer spending and rising dwelling costs. While the rate of net migration has declined from its recent peak, there have been significant upward revisions to recent historical data. Net migration also adds to labour supply in the economy and has helped to alleviate capacity pressures. Members noted the large decline over recent quarters in the share of firms reporting difficulty in finding labour.

The Committee discussed the outlook for fiscal policy and its implications for monetary policy. Based on the most recent published forecasts in the Half-Year Economic and Fiscal Update, and the commitments outlined in the Budget Policy Statement, the Committee noted that government expenditure is indicated to decline as a share of the economy in coming years.

Domestic financial conditions have eased marginally since the February Statement with declines in wholesale interest rates and the New Zealand dollar. There have been modest reductions in retail interest rates. However, these remain consistent with the Committee's restrictive monetary policy stance, with credit growth remaining subdued. The Committee noted that despite a reduction in wholesale funding costs, term deposit rates were little changed reflecting increasing competition for retail deposits.

The Committee discussed whether recent developments in the New Zealand and global economies had implications for when inflation returns to target. Members agreed that there had not been a material change since the February Statement and that monetary policy settings continue to constrain demand broadly as expected. Members agreed that there remains limited tolerance to increase the time to achieve the inflation target while inflation remains outside the target band and while inflation expectations and pricing intentions remain elevated.

The Committee discussed upside risks to the inflation outlook. Members agreed that persistence of services inflation remains a risk and goods price inflation remains elevated. Anticipated near-term increases to local government rates, insurance, and utility costs, could also further slow the decline in headline inflation.

The Committee discussed downside risks to the inflation outlook. Members noted that ongoing restrictive monetary policy in an environment of weak global growth could lead to a more rapid decline in inflation than expected. Business and consumer confidence remain particularly weak which could lead to more unemployment and financial stress than expected. Structural challenges facing the economy in China remain a concern given its importance for the global economy and for New Zealand's trade.

Overall, members agreed that the balance of risks was little changed since the February Statement. Ongoing restrictive monetary policy settings are necessary to reduce inflation, while avoiding unnecessary instability in output, employment, interest rates and the exchange rate.

In discussing the appropriate stance of monetary policy, members agreed they remain confident that monetary policy is restricting demand. A further decline in capacity pressure is expected, supporting an ongoing decline in inflation. The Committee agreed that interest rates need to remain at a restrictive level for a sustained period to ensure annual consumer price inflation returns to the 1 to 3 percent target range. On Wednesday 10 April, the Committee reached a consensus to keep the Official Cash Rate at 5.50 percent.

Attendees

MPC members: Adrian Orr (Chair), Bob Buckle, Carl Hansen, Caroline Saunders, Christian Hawkesby, Karen Silk, Paul Conway

Treasury Observer: Tim Ng

MPC Secretary: David Craigie

Fed’s Bostic: Rate cuts may have to move further out

Atlanta Fed President Raphael Bostic recently highlighted the possibility that rate cuts May have "to move further out" given that the US eocnomy economy has been "so robust, and so strong, and so resilient".

Further elaborating on his perspective in a Yahoo Finance interview, Bostic referred to his previous dot-plot submission, where he initially projected two rate cuts for the year, influenced by the rapid inflation decline in the latter half of 2023.

However, "What happened for me is that it slowed down and the pace went back to the pace that I had expected initially, which had me at one cut," Bostic explained.

SNB’s Schlegel: Interventions contributes to price stability

SNB Vice Chairman Martin Schlegel defended the central bank's use of foreign exchange interventions, highlighting their effectiveness in maintaining price stability within Switzerland.

"Have foreign exchange interventions contributed to achieving price stability? Yes, they have," he said at an event in Geneva overnight.

He further elaborated that without utilizing foreign currency sales, SNB would have faced the necessity to escalate the policy rate significantly higher.

Schlegel also noted a modest average of 0.3% over the last fifteen years. He argued that, in the absence of foreign exchange purchases, inflation rates would have dipped considerably lower, potentially entering deflationary territory.

"Estimates suggest that it would have been significantly below zero without the purchases; we would thus not have fulfilled our mandate," Schlegel pointed out.

Will Friday’s Data Add to Hopes of UK Exit from Recession?

- Dovish BoE encourages more rate cut bets

- UK GDP for February expected to reveal slowdown

- The data comes out on Friday at 06:00 GMT

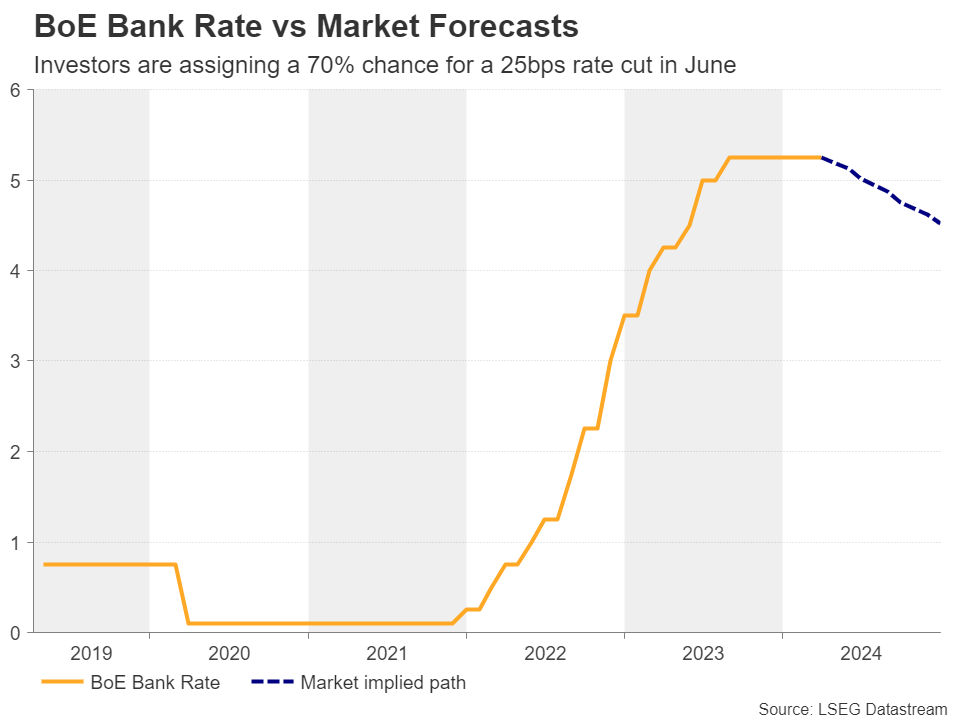

Investors add to June rate cut bets after BoE decision

With inflation in the UK coming down faster than previously expected, the Bank of England (BoE) appeared more dovish than expected at its latest gathering, on March 21. Once again, officials kept interest rates unchanged, but this time, there were no members voting for a hike. There was only one dissenting vote, and that was for a 25bps reduction.

On top of that, Governor Bailey reiterated that they are not yet at the point where they can cut interest rates, but he added that with inflation coming down, things are moving in the right direction.

This has led market participants to bring forward their BoE rate cut bets, with the overnight index swaps (OIS) market suggesting a 25% probability for a quarter point reduction at the Bank’s upcoming gathering in May, and chance for a cut in June rising to around 70%. The quick repricing has been weighing on the pound, with Cable tumbling from 1.2800 to near the 1.2600 area.

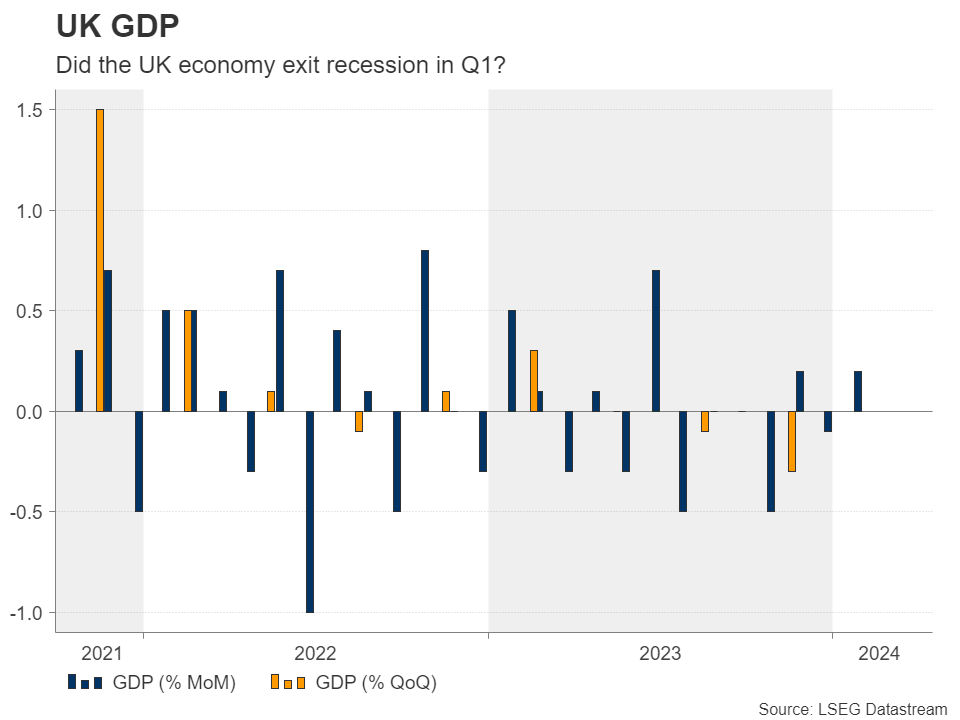

Did the UK economy exit recession in Q1?

For pound traders, this week may not be as busy as for dollar and euro traders, but they will still have the opportunity to reassess their view with regards to the BoE’s future course of action on Friday when the monthly GDP estimate for February is coming out, alongside the industrial and manufacturing production figures for the month.

Given that the UK economy slipped into recession in the second half of 2024, market participants may be eager to find out whether it entered growth mode again during the first quarter of the new year. The monthly GDP rate for January clocked in at 0.2% m/m, while the composite PMIs for both January and February pointed to improvement, although the March print pointed to a mild slowdown.

The aforementioned numbers suggest that the UK economy started the new year on a stronger footing, but that remains to be confirmed by Friday’s numbers. The forecast points to a slowdown to 0.1% m/m, which could revive some concerns regarding the performance of the UK economy, despite not entering contraction territory.

The NIESR GDP tracker points to a 0.3% q/q for the first quarter of 2024, but a soft monthly rate for February could bring that forecast into question, especially after the March PMIs pointed to a slowdown in business activity during the last month of the quarter.

Too early for conclusions as CPI data loom next week

Therefore, investors may remain convinced that there is a strong chance for the BoE to begin cutting interest rates in June, which could weigh somewhat on the pound. However, calling for a bearish outlook may still be premature, especially ahead of next week’s CPI data for March.

Despite the slowdown, the March PMIs also revealed that output prices across the UK private sector rose at the fastest pace in eight months, which tilts the risks surrounding next week’s inflation data to the upside. Therefore, even if the pound slips somewhat this week, it could bounce back up next week.

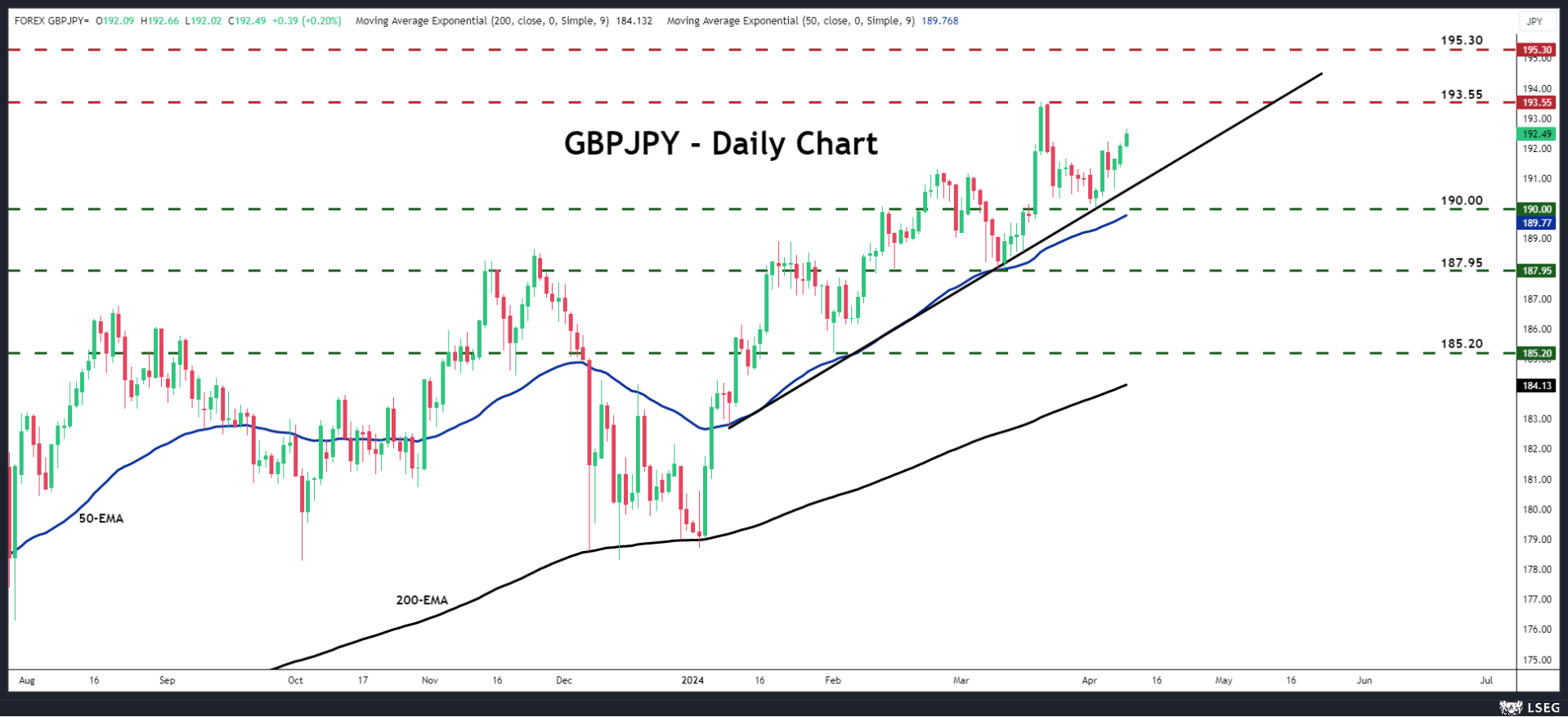

Pound/yen remains in uptrend mode

Pound/yen has been marching north since April 2, when it hit support at the crossroads of the 190.00 barrier and the short-term upward sloping support line drawn from the low of January 9. Even if the pair pulls back this week, as long as the retreat stays in check above 190.00, the bulls could remain willing to jump back into the action and aim for the high of March 20 at around 193.55.

On the downside, a slide below 190.00 could signal a larger bearish correction, but for a major trend reversal to start being examined, the pair may need to fall all the way below the 187.95 zone.