Sample Category Title

All About March US Payrolls Today

Markets

Wednesday’s failed test to sustainably pierce through technical resistance levels (YTD highs) across the US yield curve met with some rebound action during US trading hours yesterday. Upwardly revised EMU PMI’s (composite >50 for first time since May 2023), Minutes of the ECB’s March policy meeting (first rate cut clearly coming into view), weekly jobless claims (still near historically low levels) or rising oil prices (Brent crude > $91/b) had no direct influence on trading. Fed governors clearly lack the ECB’s confidence to ready a June rate cut. Richmond Fed Barkin said that the Fed has time to gain more clarity before lowering rates as he’s looking for the slowdown in inflation to sustain and to broaden. Rightly so, he’s apprehensive on the bumpy road ahead. Next week’s March CPI figures are a point in case. The low comparison base (0.1% M/M in March 2023) suggests that headline inflation will rise again to levels around/above 3.5% Y/Y. This base effect issue will repeat itself in the months of May, June and July irrelevant of the impact of current price pressures (sticky services, lagged impact of rents, energy prices,…), entailing a risk that inflation will settle again around/above 4% Y/Y during summer months. Interestingly, Barkin admitted that he would be open to a target inflation range though he deems it difficult to suddenly back off 2% right now. A higher inflation risk premium because of (implicit) higher inflation targets by central banks is one of the drivers backing our call for substantially higher long-term interest rates over the medium term. Chicago Fed Goolsbee, close ally to Fed chair Powell, focuses more on growth and the labour market. There doesn’t seem to be broad-based overheating of demand while he thinks it’s worth staying attuned to the deterioration in the jobs market. Recent data shouldn’t knock the Fed off the inflation path towards 2% while he stresses developments in housing inflation as the most valuable near-term indicator. Cleveland Fed Mester wants a couple of more months data to assess inflation, but she’s unlikely to get those as she leaves the Fed in June. Finally, Minneapolis Fed Kashkari raised the possibility that the Fed won’t cut policy rates this year if inflation stalls. We stick to the view that the a first 25 bps rate cut will come in September at the earliest. It’s all about March US payrolls today with consensus expecting another decent job growth of 214k in combination with a slightly lower unemployment rate (3.8% from 3.9) and firm wage pressure (0.3% M/M & 4.1% Y/Y). The rather high consensus bar and this week’s failed test push US yields through the roof suggests that those levels will be able to hold into this week’s close. The dollar proved to be vulnerable when the long end of the curve underperformed (rising inflation expectations?!), but found (safe haven) relief after yesterday’s late swoon in US stock markets (up to -1.5%). We expect EUR/USD to gradually return to the low 1.07 area.

News & Views

The National Bank of Poland left its policy rate unchanged yesterday at 5.75%. The NBP sees a gradual recovery developing in Q1 24 after 1% growth in Q4 23. The unemployment rate remains low and annual wage growth continues to rise. The NBP took notice of the CPI declining to 3.9% Y/Y in January, while the further decline in February and March (1.9% Y/Y) was not retained in the NBP assessment (after cut-off date Feb 15). In its new forecast (based on a stable policy rate), the NBP downwardly revised its inflation projections (2024: 2.8%-4.3%, 2025 2.2%-5% and 2026 1.5%-4.3%) but turned more positive on growth (2024 2.7%-4.3%; 2025 3.2%-3.5% and 2026 2%-4.5%). The NBP sticks with its asymmetric upward risk to 2024 inflation. Disinflation is expected to continue in H1, but a rise in VAT and higher energy prices might significantly raise inflation in H2. Public sector wages also suggest upward demand pressures going forward. In this context, the NBP judges that policy is conductive to meeting the target. It still doesn’t give any guidance on (the timing of) further easing. The zloty trades in line with fundamentals and contributes to the disinflation process. EUR/PLN yesterday held stable just below the 4.3 handle.

The Reserve Bank of India left the policy rate this morning unchanged at 6.5% for the seventh consecutive meeting. According to RBI governor Das, strong growth gives the central bank room to keep the focus on inflation as the last mile of disinflation is assessed to be challenging. The RBI sees 7% growth in current fiscal year. Retail inflation is seen staying at 4.5% compared to the RBI target of 4% while food prices remain a risk. The Indian rupee this morning gains modestly against the dollar but at USD/INR 83.41 remains within reach of the all-time (INR) low.

Sour Mood Ahead of US Jobs Data

Risk appetite got a hit yesterday as an army of Federal Reserve (Fed) speakers sounded cautious about the timing of the first rate cut and as the barrel of Brent spiked past the $90pb level on rising tensions between Iran and Israel after Israel bombed the Iranian embassy in Damascus earlier this week. The barrel of US crude spiked to $87.50pb. So far, tensions in the Middle East didn’t impact oil supply significantly. As a result, we saw a sustainable rise in oil prices – not a spike. But Iran’s direct involvement could mark a new milestone in the Middle East conflict and could back a rapid rise in oil prices in the near term. In this context, we can’t rule out the risk of a short-term rally in oil prices to $95/100pb range.

The rate cut debate heats up

The latest spike in oil prices will be reflected in the upcoming inflation reads and may derail the Fed from its ‘three rate cuts’ plan for this year. Indeed, when we listen to the Fed speakers, we sense that there is an increasing caution regarding that expectation. Neel Kashkari for example, who used to be a dovish voice, said yesterday that the January and February inflation readings were ‘a little bit concerning’ and that the Fed may not cut rates at all this year. Happily, he doesn’t vote this year. But earlier this week, Raphael Bostic said that he expects just one cut this year – after the election, and Patrick Harker and Thomas Barkin also backed the idea of a patient approach from the Fed as the uptick in inflation and the rising oil prices don’t necessarily point at further easing in inflation toward the Fed’s 2% target.

Sour mood into US jobs data

The combination of cautious Fed remarks and oil rally spoiled the market mood ahead of today’s US jobs data. The S&P500 fell more than 1%, as Nasdaq 100 retreated 1.55%. The US yields however remained soft on the back of a flight to safety, and the US dollar rebounded in Asia after hitting a two-week low.

Today, all eyes are on the US jobs data, that should distinguish between those expecting that the Fed will cut interest rates three times this year and those who bet that the Fed will barely cut the rates with strong growth and rising inflation. The US economy is expected to have added 212’000 new nonfarm jobs last month, the average earnings may have accelerated on a monthly basis and decelerated on a yearly basis. The unemployment is seen steady at 3.9%. Note that the mention of job cuts in earnings call have been rising since the beginning of the year, yet we haven’t yet seen a material impact on official data. In fact, the past three NFP numbers exceeded market expectations by around 78’000 and the US economy added around 280’000 new nonfarm jobs on average over the past three months. Another higher-than-expected NFP and hotter-than-expected wages growth could lead to a further pullback in dovish Fed expectations, weigh on stock and bond valuations and boost the US dollar. The sweetest combination would be a reasonably strong NFP number and softer wages growth. The latter would cement the expectation of a soft landing and give support to equities.

Diverging Europe

The minutes from the latest European Central Bank (ECB) meeting showed that the Eurozone officials have a clearer opinion on the timing of the first rate hike: a June cut looks like a done deal even though ECB Chief Christine Lagarde warned that the ECB is not willing to commit to further cuts beyond June.

In Switzerland, a further fall in inflation to just 1% on a yearly basis in March (and 0% on a monthly basis) hints that the Swiss National Bank (SNB) is in position to opt for more rate cuts this year to take advantage of a period where they could loosen the franc and boost the Swiss economy – especially for Swiss exporters that have suffered the consequences of a too-strong Swiss franc during the SNB’s fight against inflation. And franc has room to soften, the USDCHF has not yet reached the 38.2% Fibonacci retracement on 2022-2023 selloff, while the EURCHF recovered just a third of the post-pandemic appreciation. Carry traders – which borrow low-yielding currencies to invest in higher yielding ones - are gently leaving the yen – where the Bank of Japan’s (BoJ) next move could only be a hawkish move - and turning to Swiss francs for funding their carry trades. And the latter should help the Swiss franc give back strength, at least until the other central banks decide that it’s time for them to act, as well.

Today’s Focus Will be on March Jobs Report

In focus today

- In the US, today's main event will be the March Jobs Report. We expect non-farm payrolls growth to slow down to 180k and see average hourly earnings growth at +0.2% m/m SA. For more details on today's Jobs Report, please see our latest US Labour Market Monitor - Supply-driven recovery, 4 April.

- In the euro area, we look out for retail sales to see how consumption fared in February. A rebound in consumption is key for the growth outlook in the euro area this year.

- In Germany, we receive data on factory orders for February which will give more information on the state of the German industry that still is very weak.

Economic and market news

What happened overnight

In Japan, Finance Minister Suzuki emphasized the importance of stability in the FX market, highlighting that excessive exchange-rate fluctuations were undesirable and restating the government's readiness to intervene in cases of sharp yen depreciation. Market speculations suggest that if the USD/JPY exceeds the 152 level, the government would react with direct intervention. That happened in 2022, where USD/JPY also flirted with the 152 mark, which made the Japanese government intervene. As of now USD/JPY is trading around 151.25.

What happened yesterday

In the US, jobless claims came in higher than expected at 221k (cons: 214k), reaching the highest level since late January, while continuing claims fell slightly. The release painted a mixed picture, though labour markets remain very strong. However, it should be noted that claims data tend to be noisier around holidays. Prior to the release, the March Challenger Report also showed another uptick in announced layoffs. Tech companies accounted for the largest share of layoffs, with 'cost-cutting' named as the most common reason.

In the euro area, the final PMIs were released, with the composite PMI being revised slightly up in March to 50.3, while the services PMI was revised up to 51.5. Importantly, the composite PMI is now above 50 for the first time since May 2023, indicating some gradual improvement in an economy that had been stagnant.

The ECB minutes yesterday contained limited new information but included some nuances to the discussion within the ECB's governing council, notably the disinflationary process continuing, yet it may be a bumpy road ahead. This morning, we published our ECB preview ahead of next week. While this meeting may be considered an interim meeting and lead to limited market reaction we expect the ECB to deliver a clear commitment to a June rate cut, in the form of explicit guidance of an 'intention to cut by 25bp in June'. For more details, please see ECB Preview - An intention to cut, 5 April.

In Norway, housing prices for March was 0.6% m/m SA, clearly confirming the increasing optimism (or maybe less pessimism) among households at the moment.

In the UK, final PMIs for March were slightly lower than preliminary prints, with the composite PMI at 52.8 (prelim: 52.9), and services at 53.1 (prelim: 53.4). The PMIs indicate a modest rebound in growth following a technical recession at the end of 2023.

In Switzerland, inflation surprised to the downside as headline came in at 1.0% y/y (cons: 1.3%), while core printed 1.0% y/y (cons: 1.2%). Importantly, the m/m SA measures showed broad easing for headline (-0.15%) and core (0.1%).

In Poland, the Polish central bank kept its policy rate unchanged at 5.75%, as widely expected.

In Japan, the largest union group Rengo announced that Japanese firms offered average wage hikes of 5.24% after the third wage tally. Overall, it appears that wage pressures have indeed spread beyond big businesses, putting the Bank of Japan in a comfortable situation. Next is the final wage tally, which will not be published until early July.

In commodities, Brent continued north, settling above USD90/bbl for the first time since October, partly fuelled by escalating geopolitical tensions. This morning, the price has exceeded the USD91/bbl mark.

Equities: Global equities were lower yesterday, dragged down by the US and fear of renewed central bank hawkishness in equity space. S&P 500 made a turnaround halfway through the session with an intraday move above 2% and the biggest loss since February 2013. VIX lifting to 16 with bears getting airtime and uncertainty increased. Please note that energy was still the best performing sector while industrials and materials outperformed the larger part of the defensive space. Hence, this is not about a full risk-off move due to weak growth outlook but rather fear of inflation challenges down the road. Interestingly, this renewed fear in equity space comes with a lag of what we have seen in the bond space, and it comes in a week where macro/price data has been very benign. The trigger is two-sided, with central bank members changing their tones, yesterday it was Kashkari acknowledging the possibility of not cutting this year. Secondly, oil prices are moving higher with the geopolitical tensions rising in the Middle East. In US yesterday, Dow -1.4%, S&P 500 -1.2%, Nasdaq -1.4% and Russell 2000 -1.1%. Asian markets are lower this morning following the weak session in the US. European futures are catching down to the US cash session yesterday while US futures are marginally higher this morning.

FI: The European bond market was quite volatile yesterday. The European PMI and the US jobless claims sent yields lower, yet outside those 'release windows' the yields trended higher amid also Fed speakers downplaying the need for imminent rate cuts. 10y Bund yields ended 3bp lower on the day at 2.35% with Italy being the clear outperformer yesterday in a BTPs-Bund spread tightening of 7bp to end at 137bp.

FX: EUR/USD continued to drift higher in yesterday's session, surpassing 1.0850 with all focus on today's US jobs report. EUR/GBP moved higher during yesterday's session trading close to the 0.86 mark following softer data out from the UK. EUR/CHF continued its upward trajectory during yesterday's session following a sharp downside surprise to Swiss inflation in March. NOK FX performance during yesterday's session was hugely influenced by the report released Wednesday (after close) from the work group on government transactions consisting of employees from Norges Bank and the Ministry of Finance. For spot FX we regard the announcement as a medium- to long-term negative.

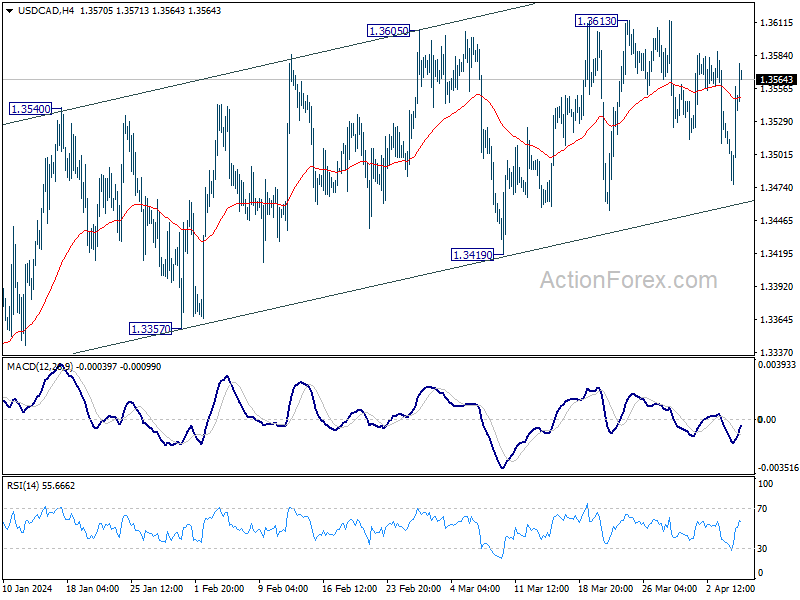

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3495; (P) 1.3527; (R1) 1.3576; More...

Intraday bias in USD/CAD remains neutral for the moment as range trading continues. On the upside, decisive break of 1.3612 resistance will resume whole rise from 1.3176 towards 1.3897 resistance. On the downside, firm break of 1.3419 support will argue that rebound from 1.3176 has completed. Near term outlook will be turned bearish for 1.3357 support first.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

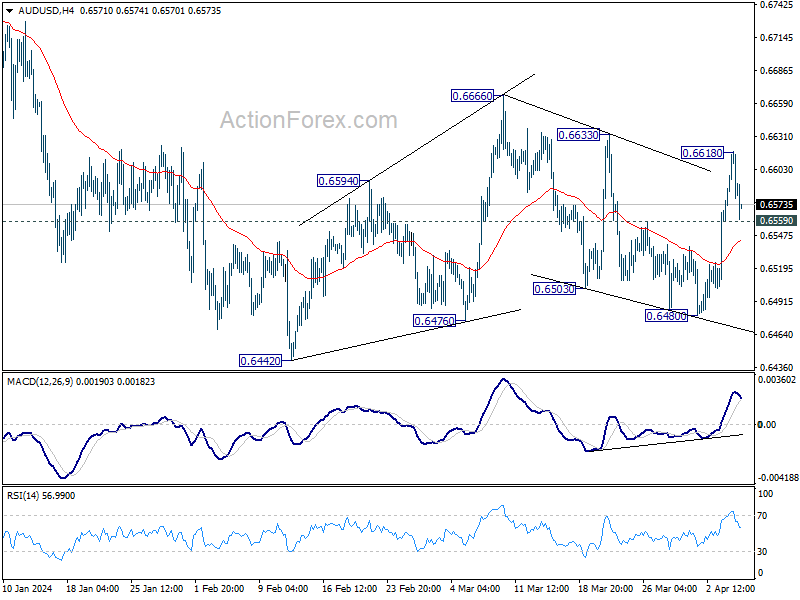

AUD/USD Daily Report

Daily Pivots: (S1) 0.6558; (P) 0.6589; (R1) 0.6618; More....

AUD/USD retreated higher hitting 0.6618 and intraday bias is turned neutral first. Rise from 0.6480 is seen as the third leg of the corrective pattern from 0.6442. Above 0.6618 will target 0.6633 resistance first. Break there will target 0.6666 and above. However, on the downside, sustained break of 55 4H EMA (now at 0.6543) will bring deeper fall back to 0.6442/6480 support zone instead.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which might still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

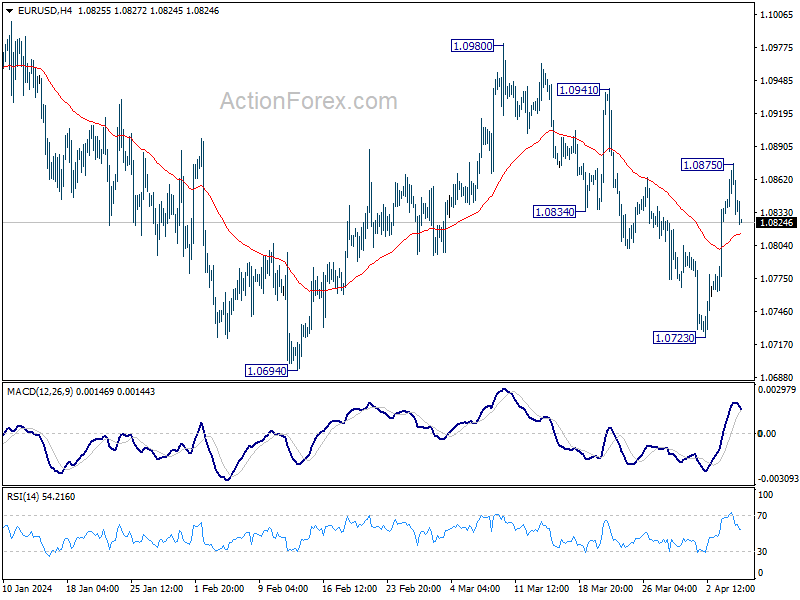

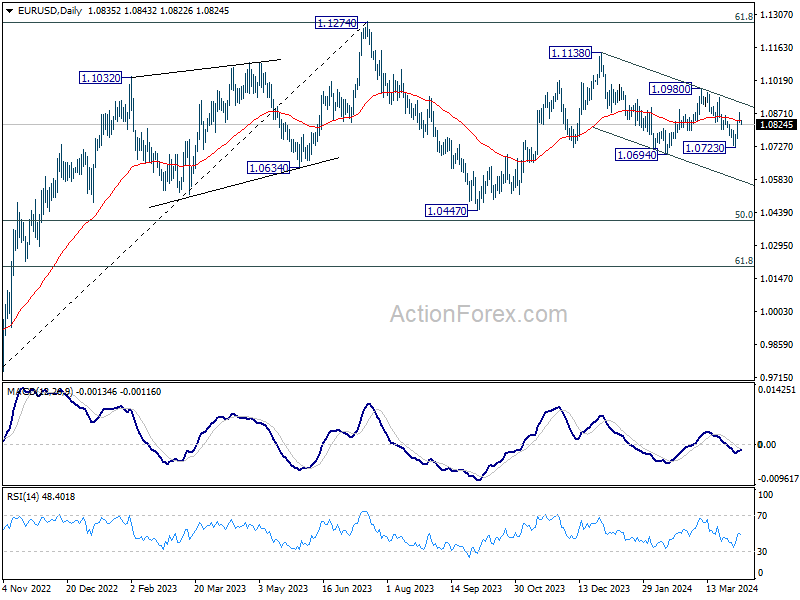

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0821; (P) 1.0849; (R1) 1.0866; More...

Intraday bias in EUR/USD is turned neutral with current retreat. Rise from 1.0723 is seen as the third leg of the corrective pattern from 1.0694. Above 1.0875 will target 1.0941/0980 resistance zone. On the downside, though, sustained trading below 55 4H EMA (now at 1.0814) will bring retest of 1.0694/0723 support zone instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

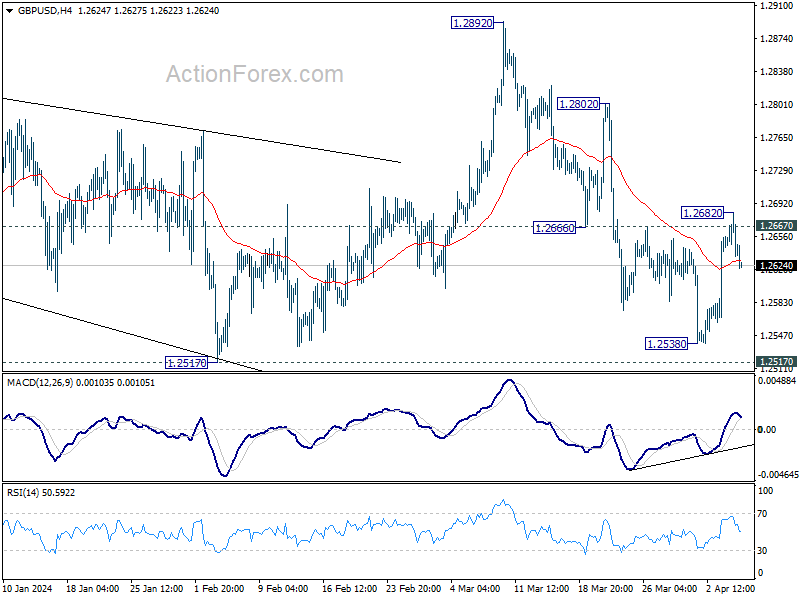

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2624; (P) 1.2654; (R1) 1.2673; More...

GBP/USD retreated after breaching 1.2667 resistance briefly. Intraday bias is back on the downside with break of 55 4H EMA (now at 1.2628). Retest of 1.2517/38 support zone would be seen next. On the upside, however, firm break of 1.2682 will suggest that fall from 1.2892 has completed at 1.2538. Intraday bias will be turned back to the upside for 1.2802 resistance next.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which might still be in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

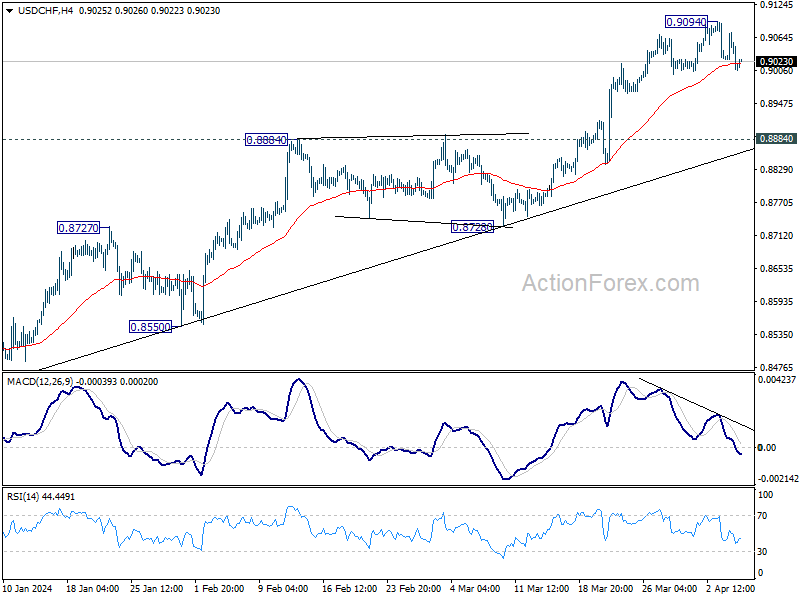

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8989; (P) 0.9033; (R1) 0.9057; More....

Intraday bias in USD/CHF remains neutral at this point. On the downside, firm break of 55 4H EMA (now at 0.9018) will bring deeper pullback. But downside should be contained by 0.8884 resistance turned support to bring rebound. On the upside, break of 0.9094 will resume larger rise from 0.8332 to 0.9243 key resistance.

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.

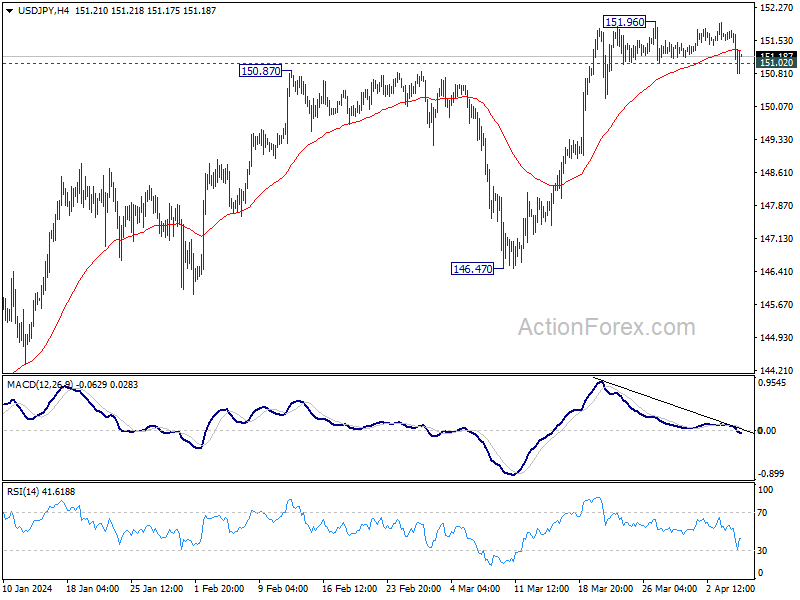

USD/JPY Daily Outlook

Daily Pivots: (S1) 151.06; (P) 151.41; (R1) 151.71; More...

USD/JPY's breach of 151.02 support suggests short term topping at 151.96. Intraday bias is now mildly on the downside for deeper pullback to 55 D EMA (now at 149.56). On the upside, however, sustained break of 151.93 key resistance will confirm long term up trend resumption.

In the bigger picture, correction from 151.87 (2023) high could have completed at 140.25 already. Rise from 127.20 (2023 low), as part of the long term up trend, is probably ready to resume. Decisive break of 151.93 resistance (2022 high) will confirm this bullish case. Next medium term target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. This will remain the favored case as long as 146.47 support holds, in case of another pullback.

BoJ Ueda’s Rate Hike Musings Propel Yen, Dollar Regains Ground on Risk Aversion

Japanese Yen rebounded broadly in Asian session today, shot up by comments from BoJ Governor Kazuo Ueda regarding the conditions for future interest rate hikes. Ueda's discussion, while not immediately setting the stage for rate increases, could be taken as a sign to prepare the markets for such a possibility. Importantly, he underscored that an excessively weak Yen could trigger a monetary policy response, a statement that has provided considerable support to the currency.

This rally in Yen was also supported in the background by risk aversion stemming from the sharp selloff in US stock markets overnight, which extended into the Asian markets. The risk-off mood has not only favored Yen but has also contributed to rebound in Dollar, which managed to regain some of the ground it lost over the past two days.

Besides while there were varying views on the path of monetary easing from the chorus of comments from Fed officials, they have collectively emphasized the need for more data before commencing a cycle of interest rate reductions. The financial markets will now look into today's US non-farm payroll report for guidance for the next move.

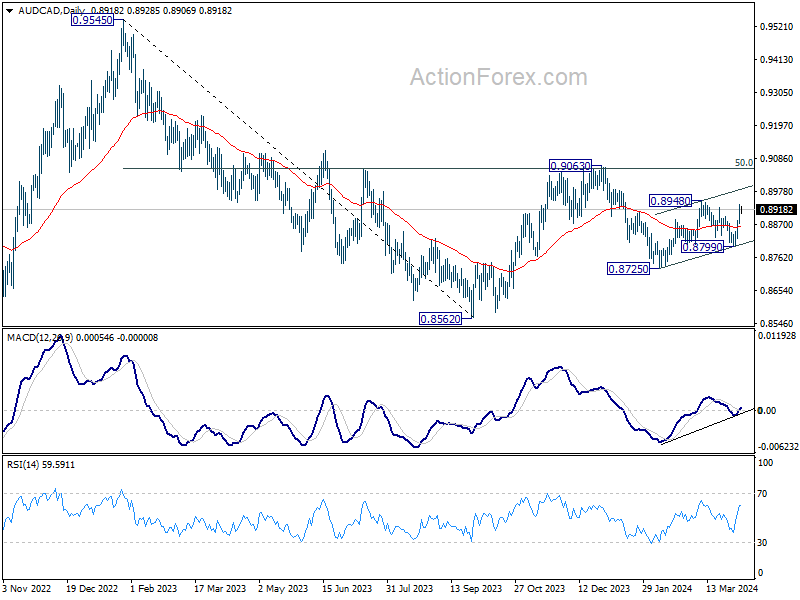

Overall for the week so far, Aussie is staying as the strongest one with help from surges in precious and industrial metal prices. Kiwi is in the second place, followed by Euro. Canadian Dollar is the worst performer, followed by Swiss Franc and Dollar. Yen and Sterling are positioned in the middle.

Technically, AUD/CAD is currently the top mover of the week with strong rebound from 0.8799. Further rise is mildly in favor for 0.8948 resistance and possibly above. Nevertheless, price actions from 0.8725 are currently seen as a corrective move only. Thus, AUD/CAD should start to lose momentum above 0.8948, and strong resistance should emerge below 0.9063 to limit upside. Break of 0.8799 support will argue that the fall from 0.9063 is ready to resume through 0.8725 to retest 0.8562 low.

In Asia, at the time of writing, Nikkei is down -2.03%. Hong Kong HSI is down -0.71%. China Shanghai SSE is on holiday. Singapore Strait Times is down -0.69%. Japan 10-year JGB yield is down -0.0006 at 0.777. Overnight, DOW fell -1.35%. S&P 500 fell -1.23%. NASDAQ fell -1.40%. 10-year yield fell -0.046 to 4.309.

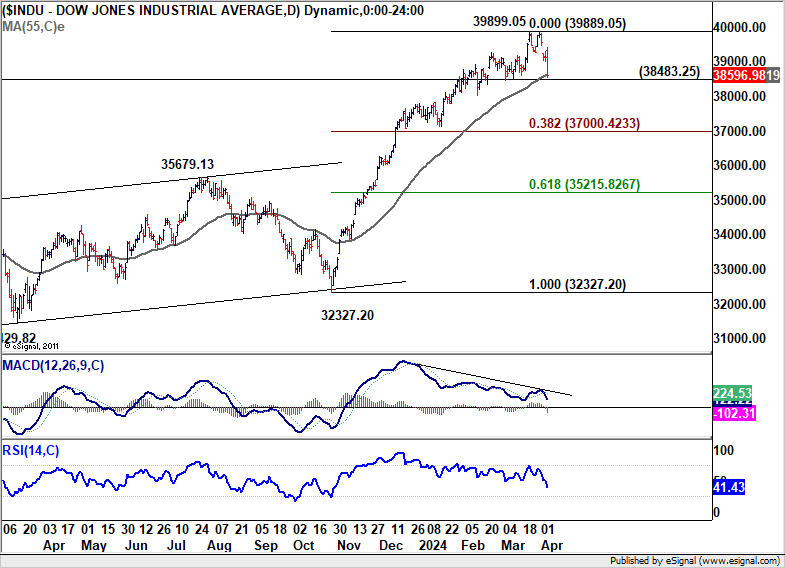

Dow registers steepest decline in a year pre-NFP, a medium-term top established already?

DOW tumbled sharply overnight, shedding -530 points or -1.35%, marking its most pronounced session drop since March 2023 and its fourth consecutive day of losses. This sharp decline seems a natural reaction after the index's robust bullish run since last November, which propelled it to new record highs, lost steam. It's also a logical area for some profit-taking and consolidations, just ahead of 40k psychological level.

The strong rally was largely fueled by anticipations of forthcoming interest rate cuts, even with delays. Nevertheless, there is little, but growing skepticism among investors on whether the policy easing cycle would really start this year. The recent surge in commodity prices has also served as a stark reminder of the challenges in curbing inflation.

The selloff also come just ahead of the crucial non-farm payroll report from the US today. Markets are expecting 205k job growth in March. Unemployment rate is expected to be unchanged at 3.9% while average hourly earnings are expected to rise 0.3% mom. Any upside surprises in today's report, in particular wages growth, could prompt further shift in Fed expectations, and hut overall risk sentiment in the stock markets.

Technically, considering bearish divergence condition in D MACD, 39899.05 could be a medium term top in DOW already, just ahead of 40k psychological level, and 61.8% projection of 18213.65 to 35962.65 from 28660.94 at 40241.64.

Decisive break of 38483.23 support should confirm this bearish case, and bring deeper correction back to 38.2% retracement of 32327.20 to 39889.05 at 37000.42.

Nevertheless, strong rebound from the current level would push DOW for another take on 40k before topping.

Fed officials want more evidence before considering rate cuts

A wave of comments from several Fed officials overnight highlighted a consensus on the need for patience before initiating interest rate reductions. While the higher than expected inflation readings in January and February were "concerning", they're not seen as derailing the broader disinflation process yet. Nevertheless, the sentiment is clear: more evidence is required to confirm inflation's downward path towards 2% target before any policy easing is initiated.

Cleveland Fed President Loretta Mester emphasized the necessity of observing "a couple more months of data" to verify if the recent inflationary trends are indeed reversing. Mester pointed out the need for "more evidence" that supports the continuation of inflation's decline. Meanwhile, Fed is in a "policy position" to adjust policy "more swiftly and sooner" if labor markets were to "deteriorate significantly"

Minneapolis Fed President Neel Kashkari on penciled in two "rate cuts" this year back in March, predicated on inflation's decline towards target." Yet, if inflation is "moving sideways", he would question "whether we needed to do those rate cuts at all."

Chicago Fed President Austan Goolsbee said the inflation in the first two months of the year "should not knock us off the path back to target". He views housing inflation as the "most valuable indicator" now. "If it does not come down, we will have a very difficult time getting overall inflation back to the 2% target."

Richmond Fed President Thomas Barkin emphasized the strategic patience afforded by a "strong labor market," suggesting that Fed has the time needed for the economic "clouds to clear" before commencing with rate adjustments.

BoJ's Ueda: Excessive Yen weakness could prompt monetary policy response

In an interview with The Asahi Shimbun newspaper, BoJ Governor Kazuo Ueda highlighted extended Yen weakness could prompt further rate hikes by the central bank.

"If exchange rate trends have an effect on the cycle between wages and prices that cannot be ignored, that would become a reason for responding to the situation through monetary policy," he explained.

Ueda also outlined other conditions under which BoJ might consider additional rate hikes, after the landmark shift in March which exited negative interest rates.

The decision to end negative interest rates was made with a certain level of confidence, quantified by Ueda as "75 percent." He indicated that an increase in this confidence level to "80 percent or 85 percent" could prompt further adjustments

Governor also touched on factors likely to boost personal consumption, including the government's planned income tax cut in June, expected wage increases, and a slowdown in consumer price inflation. These developments, if they materialize as anticipated, could pave the way for a higher interest rate as early as between summer to autumn.

Moreover, Ueda acknowledged the impact of a "excessively weak yen" on Japan's economy and consumer prices, suggesting that significant currency weakness could influence future decisions regarding interest rate hikes.

Looking ahead

Germany factory orders and import prices, France industrial production, Swiss foreign currency reserves and SECO consumer climate, UK PMI construction, Eurozone retail sales will be released in European session.

Later in the day, Canada will also release employment report, together with US non-farm payrolls.

USD/JPY Daily Outlook

Daily Pivots: (S1) 151.06; (P) 151.41; (R1) 151.71; More...

USD/JPY's breach of 151.02 support suggests short term topping at 151.96. Intraday bias is now mildly on the downside for deeper pullback to 55 D EMA (now at 149.56). On the upside, however, sustained break of 151.93 key resistance will confirm long term up trend resumption.

In the bigger picture, correction from 151.87 (2023) high could have completed at 140.25 already. Rise from 127.20 (2023 low), as part of the long term up trend, is probably ready to resume. Decisive break of 151.93 resistance (2022 high) will confirm this bullish case. Next medium term target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. This will remain the favored case as long as 146.47 support holds, in case of another pullback.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Household Spending Y/Y Feb | -0.50% | -2.80% | -6.30% | |

| 00:30 | AUD | Trade Balance (AUD) Mar | 7.28B | 10.50B | 11.03B | 10.06B |

| 05:00 | JPY | Leading Economic Index Feb P | 111.8 | 111.6 | 109.9 | 109.5 |

| 06:00 | EUR | Germany Factory Orders M/M Feb | 0.60% | -11.30% | ||

| 07:00 | EUR | Germany Import Price Index M/M Feb | -0.10% | 0.00% | ||

| 06:45 | EUR | France Industrial Output M/M Feb | 0.50% | -1.10% | ||

| 07:00 | CHF | Foreign Currency Reserves (CHF) Mar | 678B | |||

| 08:30 | GBP | Construction PMI Mar | 49.8 | 49.7 | ||

| 09:00 | EUR | Eurozone Retail Sales M/M Feb | -0.30% | 0.10% | ||

| 12:30 | CAD | Net Change in Employment Mar | 34.5K | 40.7K | ||

| 12:30 | CAD | Unemployment Rate Mar | 5.90% | 5.80% | ||

| 12:30 | USD | Nonfarm Payrolls Mar | 205K | 275K | ||

| 12:30 | USD | Unemployment Rate Mar | 3.90% | 3.90% | ||

| 12:30 | USD | Average Hourly Earnings M/M Mar | 0.30% | 0.10% | ||

| 14:00 | CAD | Ivey PMI Mar | 54.2 | 53.9 |