Sample Category Title

ECB Preview – An Intention to Cut

We expect the key takeaway from next week's ECB meeting will be an affirmation of the prevailing ECB narrative, of the ECB on route to deliver a rate cut in June. While this meeting may be considered an interim meeting, and lead to limited market reaction, we expect the ECB to deliver a clear commitment to a June rate cut, in the form of explicit guidance of an 'intention to cut by 25bp in June'. We expect no guidance will be offered beyond that point on the pace of cuts or the end level of the tightening cycle.

Markets are pricing 1bp for next week's meeting and 23bp of cuts in June. Our baseline scenario of three cuts of 25bp this year still holds, but see the risks skewed for ECB to deliver less than that this year, due to the sticky underlying inflation.

Weekly Focus – Decent Data Over Easter Dampen Rate Cut Expectations

Positive data surprises especially in the US have continued to mostly drive interest rates higher and the USD stronger over the last two weeks. Americans increased their consumption by 0.4% in February and reduced their savings rate to its lowest level since December 2022, while the ISM survey showed a clear positive surprise in March for US manufacturers who are now reporting expansion, also for the first time since 2022. While core PCE inflation (the Fed's preferred measure) came out as expected for February, 0.3% m/m price increase is still too much, and the January number was revised up to 0.5% m/m. All in all, the data does not support an early rate cut. Fed Chair Jerome Powell, among others, signalled over Easter that the direction of interest rates is still down, but that the strong data allows for waiting in order to gain more confidence about declining inflation before moving. The market is now pricing almost no chance of a May rate cut, instead looking for June. Key data to watch will be the jobs report later today (Friday) and March CPI on Wednesday next week.

In the euro area, inflation in March was slightly lower than expected, with the core price measure increasing 2.9% y/y. According to the ECB, that corresponds to a bit more than 0.2% m/m, so still to the high side in terms of reaching the 2% annual inflation target, especially as service inflation is 0.4% m/m. In other words, the concern remains that a tight labour market and high wage growth will keep inflation running. The euro area unemployment rate was 6.5% in February, and since earlier data was revised, that still means a record low. Euro area PMIs for March point to economic growth for the first time since May last year.

None of this will likely have changed the quite clearly communicated view from the ECB that there will be no rate change at next week's meeting but that a rate cut in June is to be expected. This means that the meeting on Thursday is unlikely to be a major market mover. We expect the ECB to restate the outlook for a June cut provided that the disinflation process continues, and to clarify that it is a 25bp rate cut and not 50bp, as some market participants have been speculating lately. We do not expect them to give strong guidance as to what will happen after June.

The 2023 budget deficit in France was 5.5% of GDP, significantly higher than expected, drawing negative comments from rating agency Moody's. S&P already has France on negative outlook and there is clearly risk of a downgrade.

Not only US manufacturers reported progress in March. In China, manufacturing PMIs also rose and especially the official version delivered a strong positive surprise. The manufacturing upswing is supporting commodity prices which are generally rising, not least the oil price which is also affected by the conflicts in the Middle East and the war between Russia and Ukraine. However, we are starting to see signs that the manufacturing sector has stopped improving, for example in export data from Asian countries that are usually leading indicators. This includes Japan where the Tankan business survey showed weaker (but still strong) manufacturing - but also the best sentiment among large non-manufacturers since the early 1990s.

Strong NFP Could Deepen Correction in Stocks & Support Dollar

The monthly jobs report has enough potential for the market to set the trend for the coming weeks. However, there is also a risk that the extensive list of indicators, from employment change and unemployment rate to the pace of wage growth, will feed both the dove and hawk camps.

In our view, the slowdown in US job creation is unlikely to be a game changer. Perhaps the only thing that could affect the markets would be a drop in employment. But this would be an unexpected turn of events, as the preliminary figures are more likely to show growth above the expected 200-210k for March.

Much more volatility is likely to come from the wage growth rate. The recent increase in the minimum wage and ADP’s announcement of a 5% acceleration in wage growth make the release cautious.

An acceleration in wage growth could negatively impact risk demand in two ways. Firstly, it will dramatically increase the chances that the Fed will push back even further on plans to start cutting rates and reduce the expected number of cuts this year. That’s good news for the dollar but bad news for the stock market, much of whose rally was based on easing forecasts.

Second, wage increases and staff build-ups translate into higher costs and drag down profits. And that’s bad news for stocks.

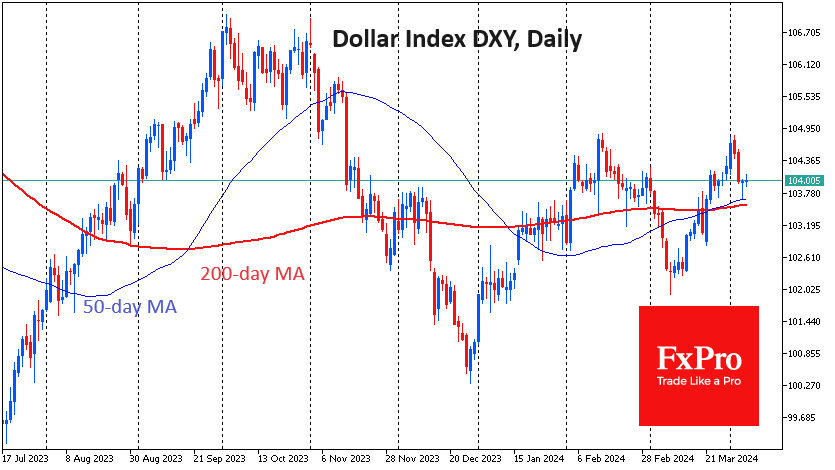

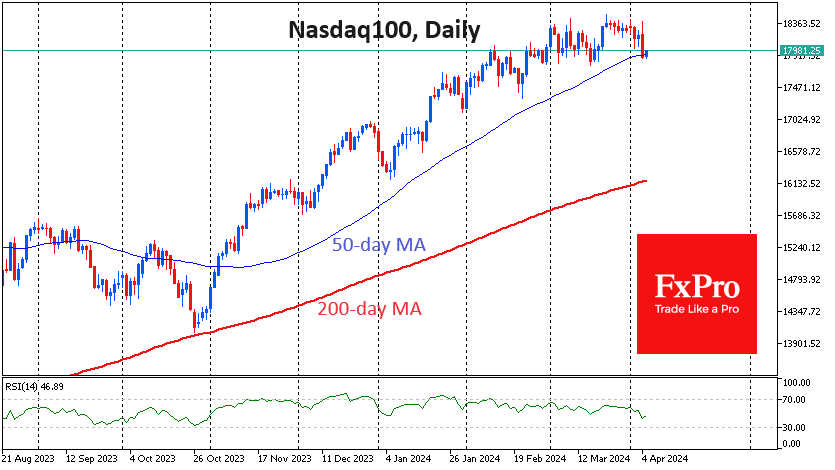

It could be a verdict for key US indices, which have been clinging to the lower boundary of the uptrend of recent months after Thursday’s sell-off. A failure under the 50-day average promises to accelerate the sell-off in equities, putting the 200-day as the bears’ next target. For the Nasdaq100 index, this opens up the potential for a 10% decline, while the Dow Jones 30 could fall 6.7%. News positive for the dollar has a chance to breathe new life into the DXY rally, which started on last month’s NFP but lost momentum at the start of April.

However, it is well worth being prepared for a continuation of the trend towards more moderate wage growth at a rate of job creation just below 200k per month, which is in line with the long-term trend of healthy economic expansion.

We also can’t rule out cooling surprises in wages. In theory, this would be a major relief for the stock market, which would have a chance to cling to established growth trends and return to storming highs in the next couple of weeks. In such an outcome, the Dollar Index may pull back from the current 104 below 103.5 and then head towards 102.3, the area of the lows of the last three months.

Sunset Market Commentary

Markets

Today’s countdown towards the March payrolls fortunately wasn’t in vain. Job gains printed at a stellar 303k, surging past the 214k consensus, the 232k whisper number and the 290k high-end of analyst estimates. The two-month revision brought an additional 22k jobs. Gains were broad-based but sectors showing the biggest rise include health & social assistance (81k), leisure & hospitality (49k) as well as construction (39k). The government added another 71k. The household survey recently diverged strongly from the afore-mentioned establishment survey job growth - an anomaly some say is related to immigration which isn’t (enough) accounted for in the Census Bureau population estimate. This time around, though, the former caught up with a whopping 498k, confronting those who saw the recent weak readings as early warnings. That same questionnaire also showed the unemployment rate easing back to 3.8% from 3.9%, despite a bigger-than-expected increase in the participation rate from 62.5% to 62.7%. Wage growth picked up as expected from 0.1% m/m to 0.3% to be 4.1% higher compared to March of last year. It’s a strong labour market on all accounts and in any case not the kind that validates quicker rate cuts by the Fed. Powell suggested this could happen if the labour market were to deteriorate suddenly and sharply. Markets react accordingly with US yields spiking 7-8.4 bps higher across the spectrum before paring gains a bit. The short (e.g. 2-y) and the long (e.g. 10-y) end revisit the resistance/YtD (closing) levels they turned away from in recent days, a.o. on a softer services ISM. We don’t expect a break higher just yet ahead of next week’s US CPIs but it looks as if the tiniest upside surprise might just do the trick. Given the low comparison base, especially for the headline number (0.1% m/m in March 2023), inflation is bound to reaccelerate in y/y terms (expected at 3.5%). After today’s data, markets have become less certain on the three rate cuts the dot plot has pencilled in (88% vs near-100% yesterday).

The US labour market report woke the dollar from it’s intraday lull. EUR/USD fell with 1.08 fighting for survival ahead of the weekend. The trade-weighted index bounces to 104.68 but remains south of this week’s high around the 105 big figure. The JPY erased all earlier (and to be honest unconvincing) gains following BoJ governor Ueda’s hint on a second rate hike in 2024H2. USD/JPY trades back into familiar territory at 151.65. Sterling hasn’t drawn any headlines recently but EUR/GBP has been creeping stealth-like higher all week. The pair is currently attacking recent closing highs around 0.8578.

News & Views

After seven months of decline, the UN’s Food and Agriculture Organization’s (FAO) food price index ticked up in March (+1.1% M/M but still -7.7% Y/Y), mostly driven by higher world vegetable oil prices (+8% M/M). Vegetable oil prices reached a one-year high reflecting higher price quotations across palm (seasonally lower outputs and firm demand in Southeast Asia), soy (robust demand from biofuel sector), sunflower and rapeseed oils. Higher crude oil prices also contributed. Dairy prices rose by 2.9% M/M, marking the sixth consecutive monthly increase. Meat prices increased by 1.7%. Cereal prices are down 2.6% M/M and 20% Y/Y. Ample wheat supply and cancelled purchases from China put downward pressure together with favorable crop forecasts. Sugar prices fell 5.4% M/M, mainly because of an upward revision to the 2023/24 sugar production forecast in India and the improved pace of harvest in Thailand. Persisting concerns over the crop in Brazil limit the price decline.

• March Canadian payrolls disappointed. Net job growth fell by 2.2k, while consensus expected an increase by 25k. Details showed marginal job shedding in both full time and part time jobs. The unemployment rate rose from 5.8% to 6.1% with an unchanged participation rate of 65.3%. There were fewer people employed in accommodation and food services (-27k), wholesale and retail trade (-23k) and professional, scientific and technical services (-20k). Employment increased in four industries, led by health care and social assistance (+40k). Total hours worked in March were virtually unchanged but up 0.7% Y/Y. Average hourly wages among employees rose 5.1% Y/Y. USD/CAD rises to a new YTD high (1.3630) on a combination of USD strength and CAD weakness.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0821; (P) 1.0849; (R1) 1.0866; More...

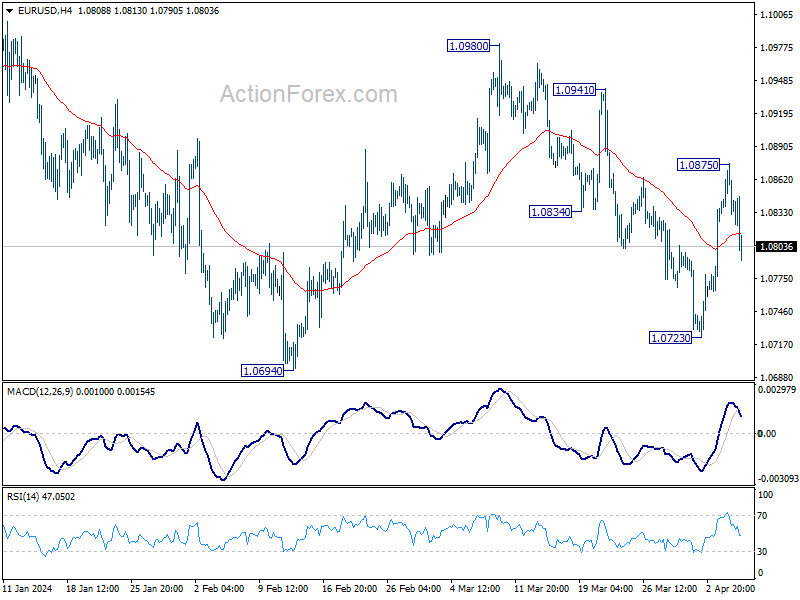

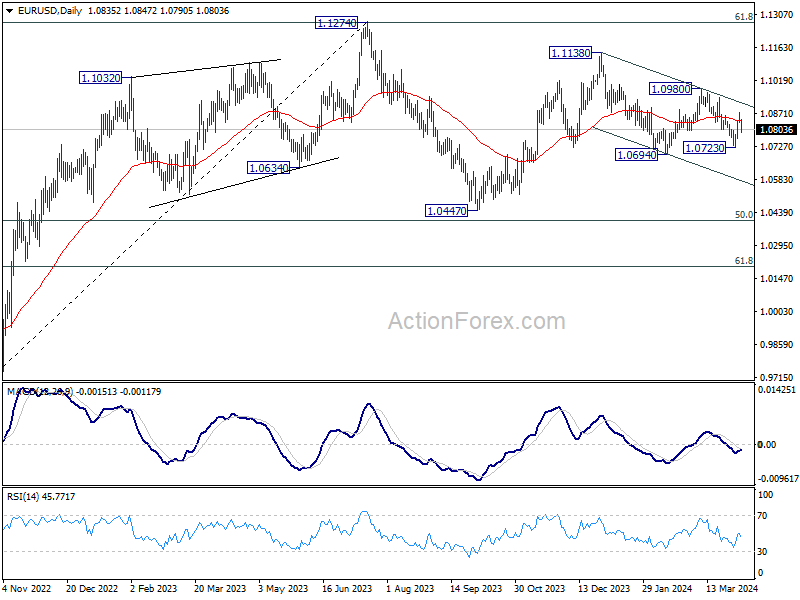

Intraday bias in EUR/USD is back on the downside with break of 55 4H EMA (now at 1.0814). Deeper fall would be seen to retest 1.0694/0723 support zone On the upside, break of 1.0875 will resume the rebound from 1.0723 towards 1.0980 resistance instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

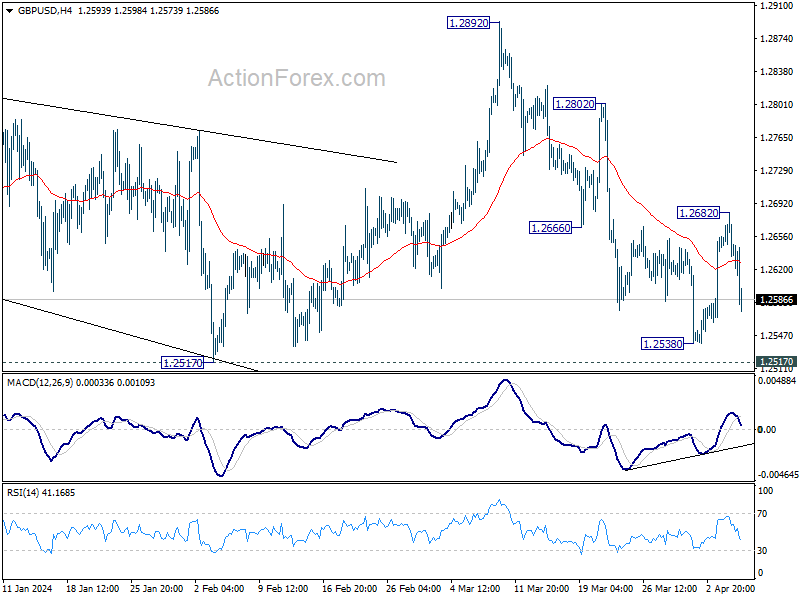

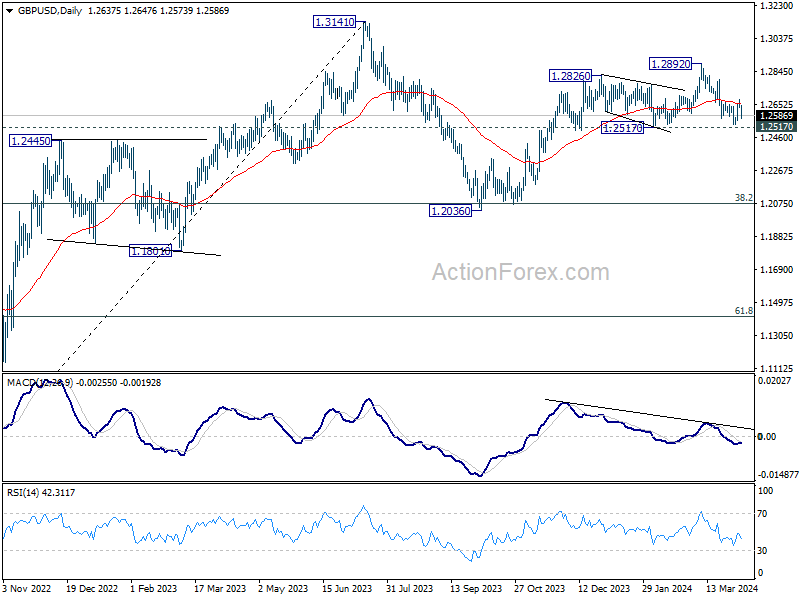

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2624; (P) 1.2654; (R1) 1.2673; More...

Intraday bias in GBP/USD remains mildly on the downside for 1.2517/38 support zone. Decisive break there will suggest that rise from 1.2036 has completed at 1.2892 already, and turn near term outlook bearish. On the upside, however, firm break of 1.2682 will suggest that fall from 1.2892 has completed at 1.2538. Intraday bias will be turned back to the upside for 1.2802 resistance next.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which might still be in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

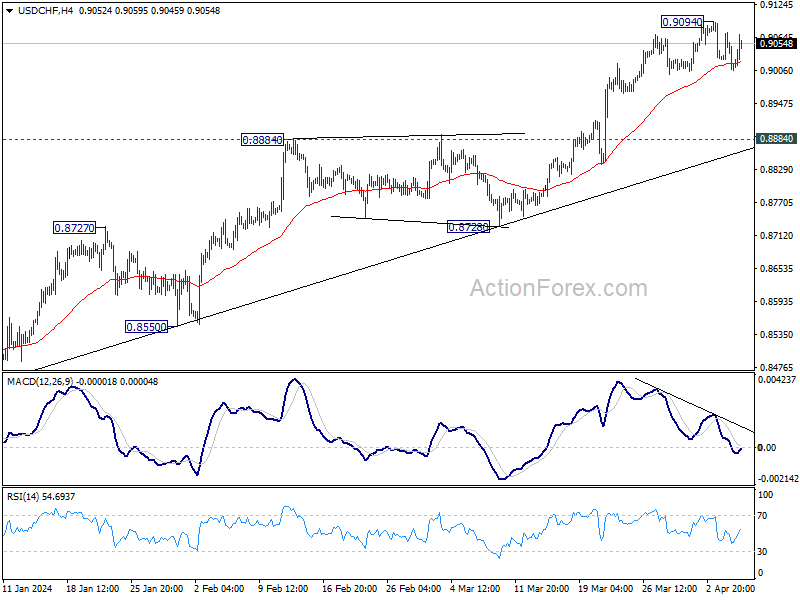

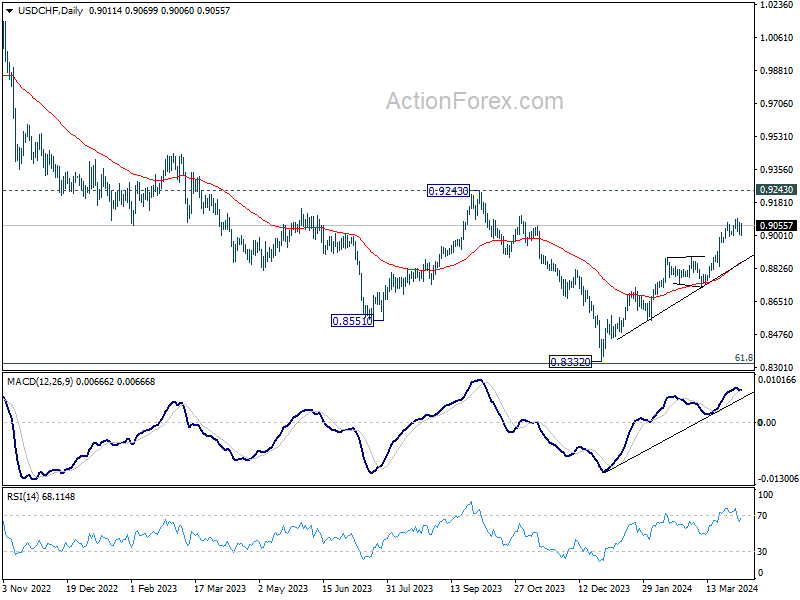

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8989; (P) 0.9033; (R1) 0.9057; More....

Intraday bias in USD/CHF remains neutral and outlook is unchanged. On the downside, firm break of 55 4H EMA (now at 0.9018) will bring deeper pullback. But downside should be contained by 0.8884 resistance turned support to bring rebound. On the upside, break of 0.9094 will resume larger rise from 0.8332 to 0.9243 key resistance.

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.

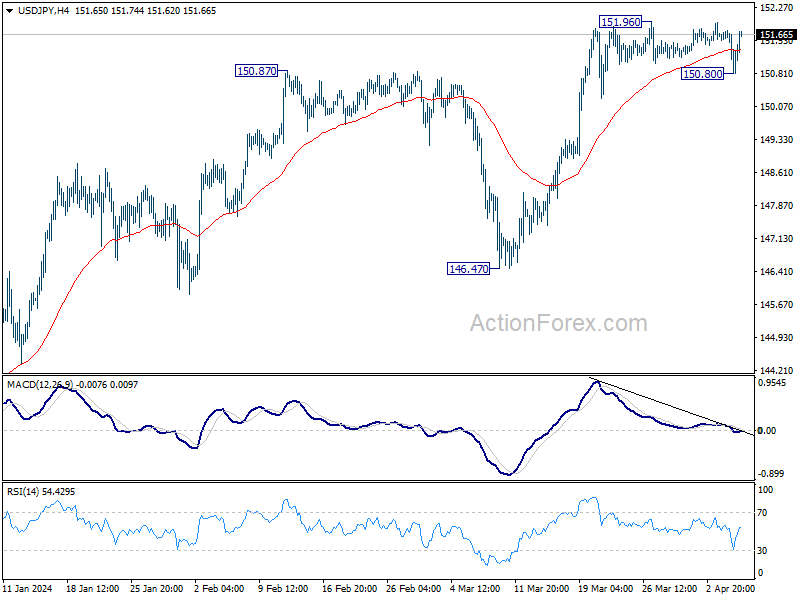

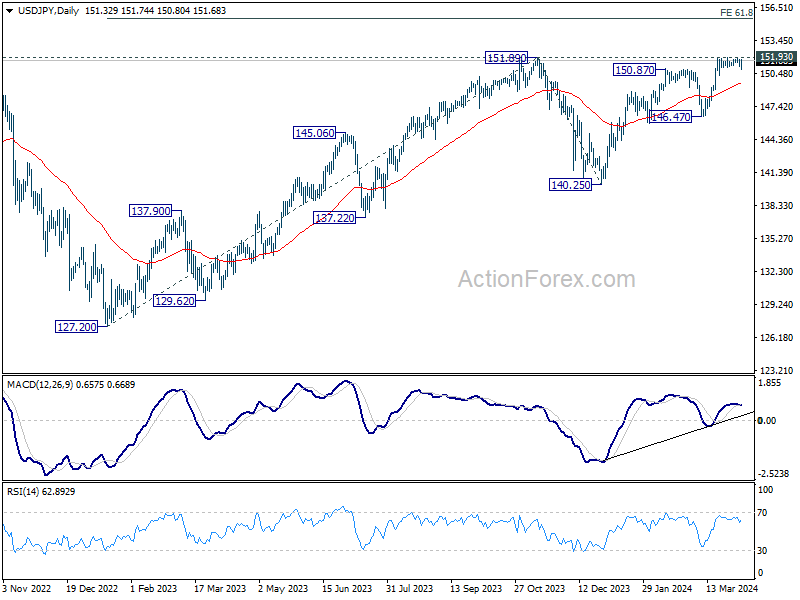

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.06; (P) 151.41; (R1) 151.71; More...

Intraday bias in USD/JPY is turned neutral as it recovered after dipping to 150.80. On the downside, break of 150.80 will resume the fall to 55 D EMA (now at 149.56). On the upside, however, sustained break of 151.93 key resistance will confirm long term up trend resumption.

In the bigger picture, correction from 151.87 (2023) high could have completed at 140.25 already. Rise from 127.20 (2023 low), as part of the long term up trend, is probably ready to resume. Decisive break of 151.93 resistance (2022 high) will confirm this bullish case. Next medium term target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. This will remain the favored case as long as 146.47 support holds, in case of another pullback.

US: Payrolls Surprise to the Upside (Again), Unemployment Rate Ticks Down to 3.8%

Non-farm employment rose by 303k in March, considerably above the consensus forecast of 213k. Job gains in the two prior months were also revised higher by a combined 22k.

Private payrolls rose 232k, with the bulk of service sector gains (212k) concentrated in health care & social assistance (81.3k) and leisure & hospitality (49k). Hiring across the construction sector (+39k) rose by the fastest pace in nearly two-years. Government hiring remained robust in March, adding 71k jobs.

In the household survey, both the labor force (+469k) and civilian employment (+498k) recorded strong gains, with the latter more than offsetting February's pullback. The unemployment ticked down 0.1 percentage points to 3.8%, while the labor force participation rate rose 0.2 percentage points to 62.7%

Average hourly earnings (AHE) were up 0.3% month-on-month (m/m) – an acceleration from February's soft 0.1% m/m gain. On a twelve-month basis, AHE rose 4.1% – the slowest pace of wage growth since June 2021.

Key Implications

Another solid employment report, with payroll gains coming in well above consensus and revisions showing a bit stronger pace of job creation in months prior. Through the first quarter, the U.S. economy added an impressive 829k new jobs – nearly a 200k more than in the fourth quarter of last year. With job openings still elevated and stronger immigration flows helping to alleviate some of the constraints on labor supply, job growth has the potential to run in the 150k-200k range through the remainder of the year.

We heard from several voting FOMC members this week and the messaging was consistent: policymakers are in no rush to cut rates. With the labor market still strong and the economy humming, the FOMC can afford to be patient and wait for clearer signs that inflation is on a sustainable path back to 2% before dialing back the policy rate. Post-payrolls release, market pricing for a June cut has narrowed and bets are now more evenly split between June and July. Any upward surprise in next week's CPI release could fully push market expectations of the first rate cut to July, which would align to our forecast.

Canada’s Labour Market Sheds Jobs, Unemployment Rate Jumps

The Canadian labour market shed 2.2k positions in March, with full-time employment down -0.7k and part-time employment down -1.6k.

The unemployment rate rose 0.3 percentage points to 6.1%, the highest level in more than two years, and the participation rate was unchanged at 65.3%.

Employment by sector showed losses in accommodation and food services (-27k), wholesale and retail trade (-23k) and professional, scientific and technical services (-20k). A positive offset was seen in health care and social assistance (+40k).

Lastly, total hours worked fell 0.3% month-on-month, while wages were up 5.1% year-on-year (from 5.0% in February).

Key Implications

The Canadian labour market lost steam in March, with the unemployment rate rising significantly. This continues the trend over the last year, where Canadian firms have been unable to absorb strong population-driven labour force growth. While this has brought the labour market into balance, it also means that more Canadian workers are unemployed (280k more since the beginning of 2023). To make matters worse, hours worked fell for the first time in four months. This throws some cold water on expectations that the recent string of hot economic data prints to start 2024 will be sustained.

Today's report casts a cloud over the Canadian economy, but it is unlikely to change the Bank of Canada's (BoC's) thinking when it meets next week. As mentioned above, recent data outside of this weak employment report has been quite strong. This validated the Bank's decision to remain patient with the start of rate cuts. While it has afforded the central bank some extra time to wait to ensure inflation remains on its downward trajectory 2%, markets are increasingly betting that the BoC will pull the trigger on its first rate cut in June.