Sample Category Title

Gold Hits Record High; Silver Peaks on Fed Rate Cut Speculation

Gold prices have soared to an all-time high of 2288.00 USD per troy ounce, while silver reached its highest in two years, driven by speculation surrounding the US Federal Reserve's monetary policy. This surge followed comments from two Fed officials, Mary Daly of the FRB San Francisco and Loretta J. Mester of Cleveland. Both anticipate three rate cuts by the Fed in 2024, although they emphasised there is no immediate need for these adjustments.

The anticipation of a more accommodative monetary policy has been the primary driver behind gold's significant 11% price increase this year, demonstrating substantial gains for what is typically considered a conservative investment. However, this optimism is somewhat tempered by the current US economic data, which presents a complex backdrop for the timing of these expected rate cuts.

Investors and market watchers are now eagerly awaiting remarks from the US Fed Chair Jerome Powell, who is expected to provide further insights into the Federal Reserve's monetary policy outlook soon.

Precious metals traditionally benefit in low-interest-rate environments since they do not offer yields like interest-bearing assets. This dynamic underscores the current rally in gold and silver prices.

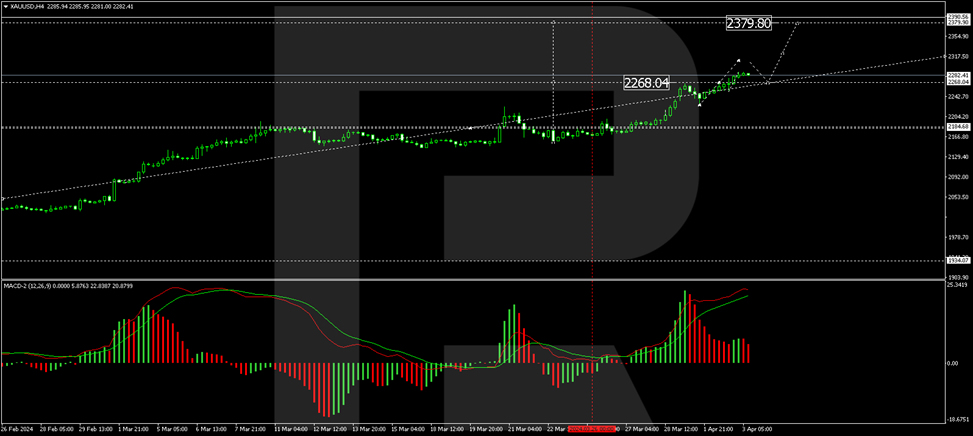

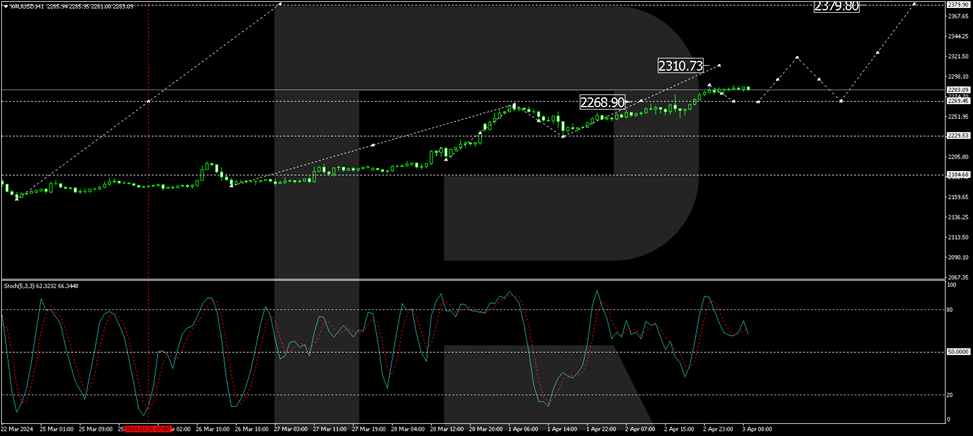

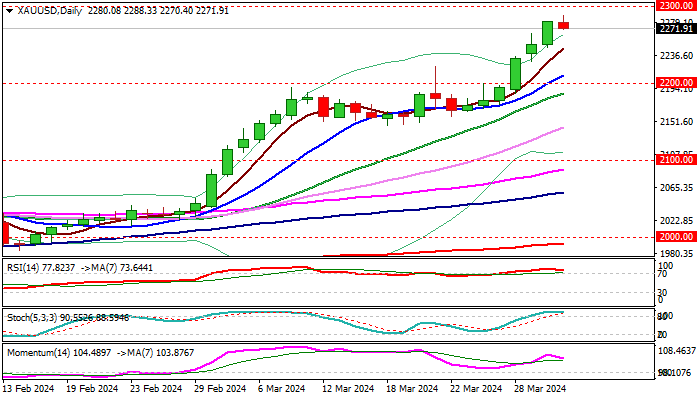

Technical analysis of XAU/USD

H4 chart analysis: the XAU/USD pair has corrected to 2230.00 USD and initiated a new upward wave targeting 2379.80 USD. Following this target, a correction towards 2270.00 USD is anticipated before the price potentially moves towards 2430.00 USD. The MACD indicator, with its signal line well above zero and trending upward, supports this bullish scenario.

H1 chart analysis: on the H1 chart, XAU/USD has experienced a growth wave, reaching 2266.80 USD, with the market updating this peak today. A consolidation phase around this level is expected, with a breakout potentially leading to a further rise to 2310.73 USD and possibly extending towards 2379.80 USD. The Stochastic oscillator, currently below 80 and poised to drop to 50 before rising again, aligns with this forecast.

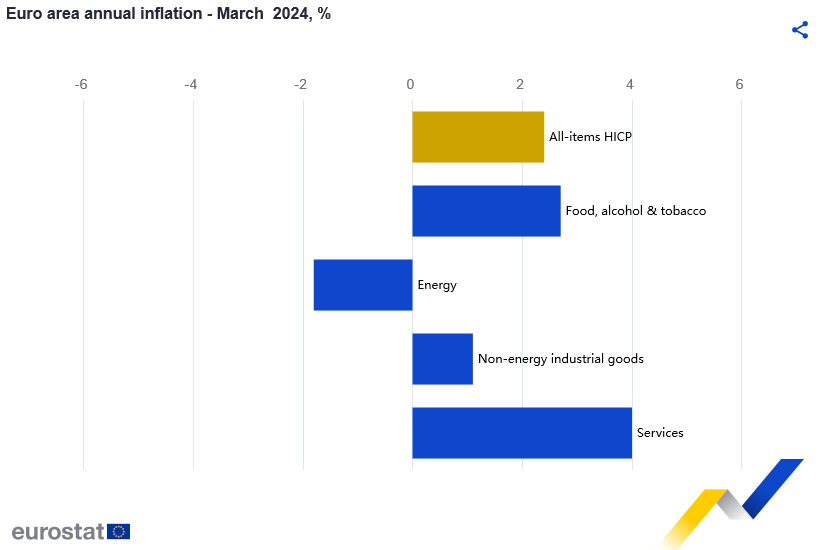

Eurozone CPI slows to 2.4% in Mar, core down to 2.9%, below expectations

Eurozone headline CPI slowed from 2.6% yoy to 2.4% yoy in March, below expectation of 2.5% yoy. CPI core (ex energy, food, alcohol & tobacco) slowed from 3.1% yoy to 2.9% yoy, below expectation of 3.0% yoy.

Looking at the main components services is expected to have the highest annual rate in March (4.0%, stable compared with February), followed by food, alcohol & tobacco (2.7%, down from 3.9%), non-energy industrial goods (1.1%, down from 1.6%) and energy (-1.8%, up from -3.7%).

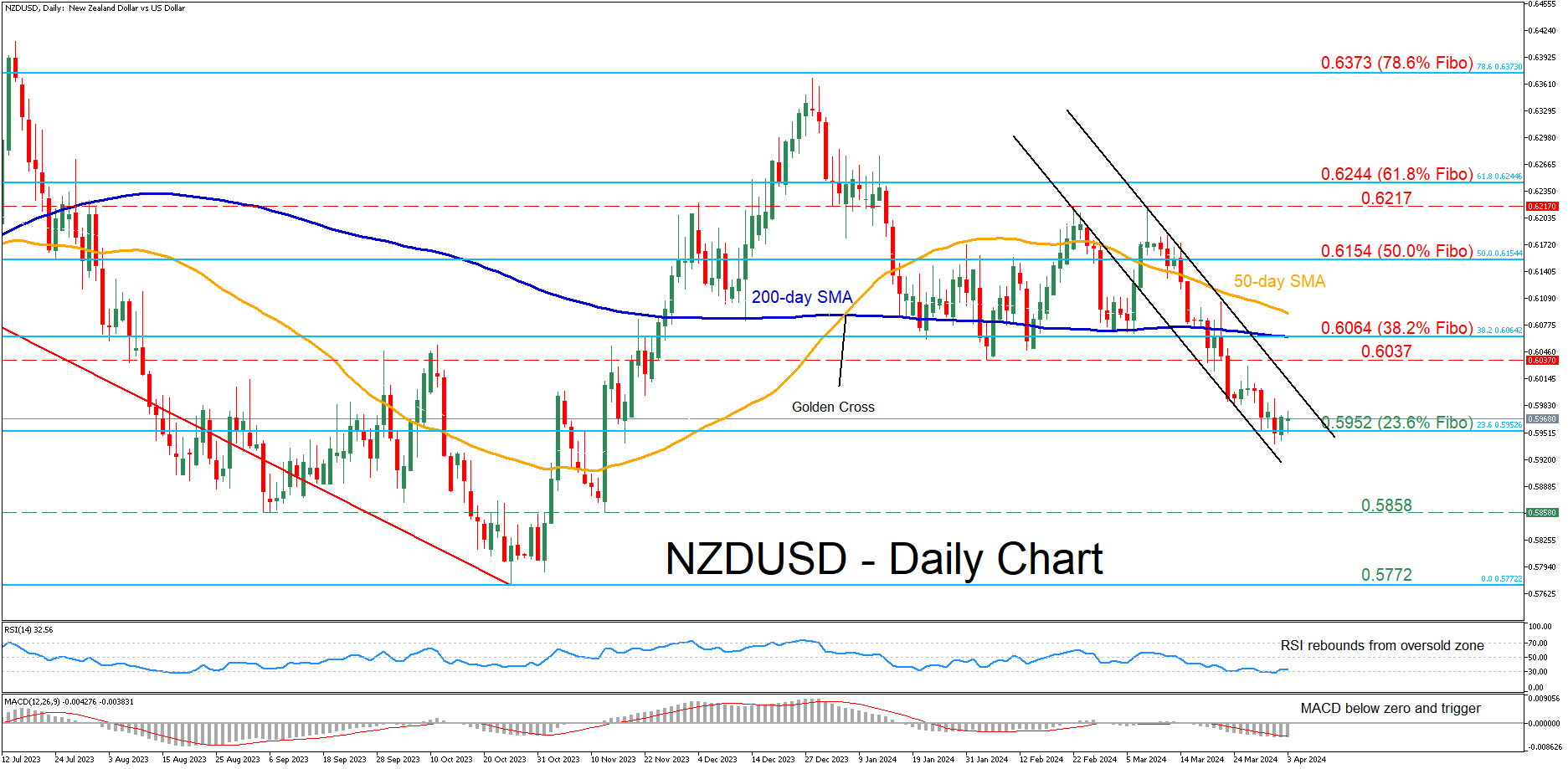

NZDUSD Halts Decline at 23.6% Fibonacci

- NZDUSD declines sharply within descending channel

- Drops below both 50- and 200-day SMAs to a 4-month low

- Oscillators remain deep in their negative territories

NZDUSD has been in an aggressive downtrend since its double rejection at the 0.6217 level in early March. Despite dropping to a fresh four-month bottom this week, the pair seems to be finding its footing around 0.5952, which is the 23.6% Fibonacci retracement of the 0.6536-0.5772 downtrend.

Given that both the RSI and MACD are heavily tilted to the downside, the price might revisit the 23.6% Fibo of 0.5952. A violation of that region could pave the way for the September 2023 low of 0.5858, which also held its ground in November. Failing to halt there, the pair could challenge the 2023 bottom of 0.5772.

On the flipside, should the pair rotate back higher, immediate resistance could be found at the February support of 0.6037. Further advances could then cease around the 38.2% Fibo of 0.6064, which overlaps with the 200-day simple moving average (SMA). Conquering this barricade, the bulls may attack the 50.0% Fibo of 0.6154.

Overall, NZDUSD has plummeted to a fresh four-month low, but the 23.6% Fibo seems to be curbing the bears’ efforts for further downside. Hence, a clear break below that region could accelerate the decline.

EUR/USD Starts Recovery, USD/CHF Could Extend Gains

EUR/USD is attempting a recovery wave from the 1.0725 zone. USD/CHF climbed higher above 0.9070 and might extend gains in the near term.

Important Takeaways for EUR/USD and USD/CHF Analysis Today

- The Euro declined toward 1.0725 before it started a recovery wave against the US Dollar.

- There was a break above a key bearish trend line with resistance at 1.0765 on the hourly chart of EUR/USD at FXOpen.

- USD/CHF climbed higher above the 0.9035 and 0.9070 resistance levels.

- There was a break above a major bearish trend line with resistance at 0.9035 on the hourly chart at FXOpen.

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair extended the decline below the 1.0785 support zone. The Euro even declined below 1.0750 before the bulls appeared against the US Dollar, as mentioned in the previous analysis.

The pair traded as low as 1.0724 and recently started a recovery wave. There was a move above the 1.0745 resistance zone. Besides, there was a break above a key bearish trend line with resistance at 1.0765.

The bulls pushed the pair above the 50-hour simple moving average and the 50% Fib retracement level of the downward move from the 1.0805 swing high to the 1.0724 low.

Immediate resistance on the EUR/USD chart is near the 1.0785 zone. It is close to the 76.4% Fib retracement level of the downward move from the 1.0805 swing high to the 1.0724 low. The first major resistance is near the 1.0805 level.

An upside break above the 1.0805 level might send the pair toward the 1.0825 resistance. The next major resistance is near the 1.0850 level. Any more gains might open the doors for a move toward the 1.0920 level.

Immediate support on the downside sits at 1.0765. The next major support is the 1.0745 zone. A downside break below the 1.0745 support could send the pair toward the 1.0725 level. Any more losses might send the pair to 1.0650.

USD/CHF Technical Analysis

On the hourly chart of USD/CHF at FXOpen, the pair started a decent increase from the 0.9005 support. The US Dollar climbed above the 0.9035 resistance zone against the Swiss Franc.

There was a break above a major bearish trend line with resistance at 0.9035. The bulls were able to pump the pair above the 50-hour simple moving average and 0.9070. Finally, the pair tested the 0.9090 zone.

A high was formed near 0.9090 before there was a minor pullback. The pair declined below the 23.6% Fib retracement level of the upward move from the 0.9005 swing low to the 0.9090 high.

On the downside, immediate support on the USD/CHF chart is near the 0.9070 zone. The first major support is near the 50-hour simple moving average at 0.9055. A downside break below 0.9055 might spark bearish moves. The next major support is near the 61.8% Fib retracement level of the upward move from the 0.9005 swing low to the 0.9090 high at 0.9035.

Any more losses may possibly open the doors for a move toward the 0.9005 level in the near term. On the upside, the pair is now facing resistance near 0.9090.

The next major resistance is at 0.9120. The main resistance is now near 0.9140. If there is a clear break above the 0.9140 resistance zone and the RSI climbs above 65, the pair could start another increase. In the stated case, it could test 0.9200.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Gold Price XAU/USD Sets Another All-Time High

The XAU/USD gold chart today indicates that the price of the metal has exceeded USD 2,250 per ounce.

Causes:

→ Geopolitical tensions. Military conflicts in Ukraine and the Middle East do not subside, the threat of terrorist attacks is growing, and new hot spots may appear on the world map.

→ Concerns about a new round of inflation due to rising commodity prices.

In both cases, gold acts as a safe-haven asset.

Since the beginning of 2024, the price of XAU/USD has risen by 12%. How much longer can the rally last?

In terms of technical analysis of the gold price, there are two tools to take into account:

→ ascending channel (shown in blue). Today XAU/USD is in its upper half, the price has tested (shown by the arrow) the support of the median line. And from the first days of April it has been demonstrating dynamics that direct it towards the upper border of the channel.

→ Fibonacci proportions. If we take the A→B impulse as 100%, then the decrease in B→C finds support in the zone of levels 0.5-0.618, which confirms the relevance of using proportions. Then the target for impulse price growth from point C may be the level of 1.618.

Thus, these technical analysis tools for the XAU/USD chart indicate that the price of gold may rise to the 2,333-2,380 zone if the current bullish sentiment continues.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

XAU/USD: Healthy Correction Likely to Precede Fresh Push Higher

Gold edges lower from new record high ($2288) in early Wednesday, as bulls show signs of fatigue after advancing over 5% in a steep acceleration in past six days.

Although the metal resumed the uptrend in early April, after an impressive 9.3% rally in March, remaining strongly underpinned by growing signals of Fed’s first rate cut in June and geopolitical tensions, corrective action in the near term cannot be ruled out.

Profit taking after latest rally may spark fresh dips, as stretched technical studies on all larger timeframes (day / week / month) have already sent initial warnings that bulls may face increased headwinds on approach to psychological $2300 resistance.

Larger picture remains firmly bullish, adding to scenario of a healthy correction, which will give bulls space to consolidate before broader uptrend resumes.

Initial supports lay at 2222 (former top/daily Tenkan-sen)) and $2211 (rising 10DMA) with extended pullback expected to find firmer ground at $2200/$2180 zone (psychological/20DMA) to keep bulls intact.

Res: 2288; 2300; 2359; 2400.

Sup: 2222; 2211; 2200; 2187.

ECB’s Holzmann: No fundamental objection to rate cut in Jun

In an interview with Reuters, ECB Governing Council member Robert Holzmann said that an interest rate cut in April is "not on my radar". Instead, he highlighted June as a critical time for evaluating the bank's next steps, emphasizing a commitment to data-driven decision-making regarding monetary easing.

"If the data allows it, a decision will be made," he noted. "I don't have an in-principle objection to easing in June, but I'd like to see the data first and I want to stay data-dependent."

An intriguing aspect of Holzmann's perspective is his consideration of Fed's actions in relation to ECB's. He mentioned, "If by June the data supports a strong case for a cut, and we're a week before the Fed makes its decision, then it's quite likely we'll proceed, hoping the Fed follows suit." However, if Fed doesn't come along, "then it may reduce the economic impact of our move."

Notably, Holzmann's remarks signal a significant shift, especially considering his reputation as one of the more conservative voices within ECB, typically resistant to premature discussions of rate reductions. For him, the shift appears to be influenced by an increasingly benign inflation outlook. Also there were signs of economic fragility within Eurozone, which has been hovering on the brink of recession for multiple quarters.

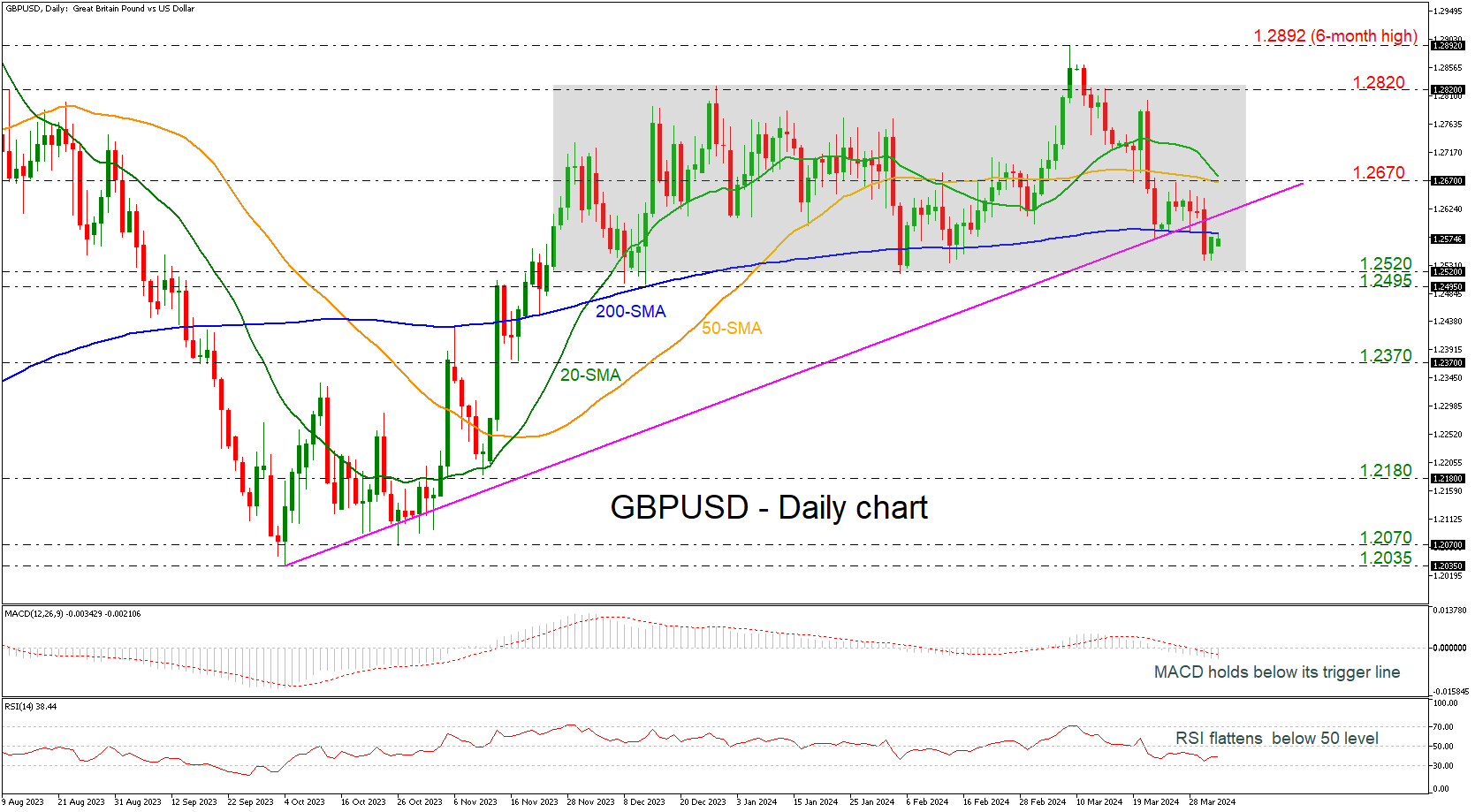

GBPUSD Battles With 200-Day SMA

- GBPUSD drops below uptrend line

- Price remains within sideways channel

- MACD and RSI indicate neutral-to-bearish bias

GBPUSD dropped beneath the long-term ascending trend line and the 200-day simple moving average (SMA. Nevertheless, it has not escaped the consolidation area of 1.2520-1.2820, which has confined the price action since November 24. Currently, the pair is trying to recoup some of the previous days’ losses, but the momentum is still weak.

In case of a sell-off beneath the lower boundary of the range and the 1.2495 support line, the market outlook will switch to a more negative one, challenging the 1.2370 barricade.

The technical oscillators are confirming the neutral-to-bearish outlook as the MACD is extending its negative movement beneath its trigger and zero lines, while the RSI is moving horizontally beneath the neutral threshold of 50.

In the positive scenario, a successful jump above the 200-day SMA could open the way for a retest of the mid-level of the channel at 1.2670, which overlaps with the upcoming bearish crossover within the 20- and the 50-day SMAs. Even higher, the upper boundary of the range at 1.2820 may halt upside pressure.

To sum up, GBPUSD lacks a clear direction in the medium-term timeframe and a bearish tendency in the longer timeframe cannot be not excluded.

Stars Aligned for Dollar Yesterday, But Greenback Succumbed

Markets

German Bunds opened softer yesterday in a catch-up move with the US Treasury sell-off on (Easter) Monday. Selling pressure remained until the start of US trading despite lower-than-expected German CPI data and a slight fall in short-term (1-yr) inflation expectations in an ECB Survey. Both cement the case for a (discounted) June ECB rate cut. Sluggish growth and disinflation momentum create a window of opportunity for the ECB, but it risks closing rapidly as we believe that the Fed will err on the side of “higher for longer” at least until after the Summer break while European inflation dynamics (Y/Y) will accelerate again in H2. Therefore we think that EMU money markets are still positioned too aggressively when it comes to making monetary policy even less restrictive after June (leaning to a cumulative 100 bps of rate cuts this year). Rising oil prices initially extended the Bund sell-off with Brent crude rising to $89/b for the first time since end October. Dynamics changed in the run-up to the US opening bell with US equity futures sinking after a significant decline in Tesla sales volumes. A few hours earlier, BYD delivered a similar message. The move pulled European equity benchmarks from small gains to closing losses in the direction of 1%. Key US markets opened with similar losses and hovered around opening levels for much of the remaining session. This bout of risk aversion helped core bonds off intraday lows and outweighed US JOLTS job openings (stable at 8.75mn). Daily changes on the German yield curve (compared with Thursday’s close) yesterday ranged between -1 bp (2-yr) and +12.3 bps (30-yr). US yields fluctuated between -1.6 bps (2-yr) and +4.7 bps (30-yr). Stars aligned for the dollar yesterday (stock & bond sell off; higher oil prices), but the greenback succumbed. The dollar failed to cling to Monday’s post-ISM gains. The trade-weighted dollar (DXY) threw the towel after failing to break 105 resistance (YTD high). EUR/USD set a new short term low at 1.0725, without testing the 1.0695 YTD low.

Asian risk sentiment is negative this morning with similar losses to 1% and slightly more. The Taiwan earthquake had only a minor additional effect. The eco calendar contains EMU CPI numbers (risks for lower outcome) and US ADP employment & services ISM. The latter will be pivotal for trading with US rates and USD still close to resistance levels. Fed Chair Powell speaks on the economic outlook after European close in what’s today’s final potential game changer. Will he stick with the balanced approach after the March policy decision (giving equal weight to a weakening labour market & disinflation) in determining the right timing of making policy less restrictive?

News & Views

Minutes of the March CNB meeting confirmed that price stability in the country had been restored, allowing the central bank to continue reducing rates cautiously. To maintain inflation at the target level, it is necessary to keep policy tight until core inflation is fully under control. A cautious approach allows the CNB to interrupt or halt the policy decline in rates at restrictive levels if necessary. Governor Michl assesses that the neutral policy rate is higher than in the past. Risks remain modestly inflationary, including a slower decline in still elevated inflation expectations. Given a tight labour market, this can translate into stronger wage demands. The recent deeper than expected decline in headline inflation was mainly due to lower food prices. Some members see the continuing rise in services prices as a ground for caution. MPC members are mixed on the CZK-weakening of late. Jan Kubicek indicated that the FX rate is fostering monetary policy easing for the first time since quite some time. Eva Zamrazoliva on the other hand didn’t see current FX level as a significant risk to meeting the inflation target longer term. A majority continues to favour 50 bps rate cut steps due to upside inflation risks. Jan Frait and Tomas Holub dissented (75 bps).

The Chinese Caixin services PMI rose from 52.5 to 52.7 in March. The pace of activity accelerated as new business rose at the quickest pace year to date. Business confidence also improved further, but this wasn’t able to avoid an ongoing contraction employment. Input cost inflation in the sector slowed and this also filtered through into selling prices. The above-50 reading marked the 15th consecutive monthly expansion. Still the level of expansion remains below the longer run average. Combined with a further expansion in the manufacturing sector (51.1), the gain in the services sector also raised the composite index from 52.5 to 52.7.

The ‘Two or Three’ Cut Debate Heats Up

Mood was down in Asia today as the strongest earthquake in 25 years led to halted operations in TSM and United Microelectronics.

Elsewhere, major stock and bond markets in Europe and the US were painted in the red yesterday as well; rising oil and commodity prices fueled inflation expectations while further strength in the US economic data boosted worries that the Federal Reserve (Fed) may not cut the interest rates as much as wished this year. Yesterday’s data showed faster-than-expected recovery in factory orders, though job openings fell more than expected.

The market now prices less than three rate cuts from the Fed this year, below the three rate cuts plotted by the Fed members at last month’s FOMC meeting. And even though Fed’s Mary Daly and Loretta Mester said that three rate cuts look appropriate this year – God knows why – Mester added that ‘it’s a close call’ on whether fewer rate cuts will be needed. She was certainly referring to robust economic data and up-ticking inflation!

The US 2-year yield extended to 4.73% yesterday, the 10-year yield spiked to 4.40%, the S&P 500 tipped a toe below the 5200 level but managed to close above this psychological mark. Nasdaq closed near 1% lower and volatility rose. The US dollar index however retreated despite the positive pressure on yields.

Today, investors have their eyes set on the ISM non-manufacturing index and the latest ADP data. The US economy is expected to have added nearly 150K new private jobs in March. Friday’s jobs data should split hairs between those anticipating three rate cuts and those banking on just two. A strong set of jobs figures – that would add more spice to strong US growth and picking inflation - should further soften the Fed doves’ hand, weigh on equity and bond valuations and keep the US dollar sustained against most majors, starting with the euro.

The EURUSD rebounded before hitting 1.0740 yesterday as the US dollar fell sharply despite supportive economic data. But the data released in Europe confirmed that inflation in Germany cooled for a third straight month and today’s aggregate Eurozone inflation is expected to show further easing. The headline inflation is expected to ease from 2.6% to 2.5% and core inflation from 3.1% to 3%.

Unlike the strong US growth and rising US inflation since the start of the year, the persistent slowdown in European inflation and gloomy Eurozone economies justify a European Central Bank (ECB) rate cut and should continue to weigh on the EURUSD. Across the Channel, Cable saw support near 1.2550 on a broadly softer US dollar, but the data fueled the Bank of England (BoE) rate cut hopes: inflation in British stores dropped to the lowest level in more than two years.

Overall, the US is isolated on an island with a surprisingly strong economic data and rising inflation. But the dollar inflation could easily spill over to the rest of the world if the US dollar gained strength backed by a significant retreat in dovish Fed expectations.

FTSE 100 in a good place to catch up with the rest of Western indices

The FTSE 100 benefited from rising oil & commodity prices and softer sterling to extend gains past the 8000p psychological mark. The FTSE 100 will likely see more tailwinds if oil and commodity prices pick up momentum and the British blue-chip index could be a good hedge against rising inflation worries.

Across the Atlantic, the moodiness in US stocks since the quarter started is mostly due to a retreat in Fed expectations because of strong data, but note that strong economy per se is not a reason to be sad about. This is why the S&P 500 could temper the significant retreat in Fed cut expectations since the start of the year. If the US earnings continue to satisfy, the US stock markets may avoid a significant meltdown.

Oops

Tesla released the first quarter deliveries report yesterday and the numbers were hard to swallow. Analysts were expecting around 6% drop in deliveries last quarter compared to a year earlier, but the deliveries fell 8.5%. Inventories rose and the inventory build-up will be another major headwind to the cashflow. As such, Tesla closed the session almost 5% lower and will hardly reverse losses when the 50% annual sales growth narrative continues to fade away. Tesla’s PE ratio is still around 63 giving it a large room for extending losses.

Elsewhere, Rivian built and sold more EVs than expected but shares plunged more than 5% on overall gloomy outlook for the EV sector.