Sample Category Title

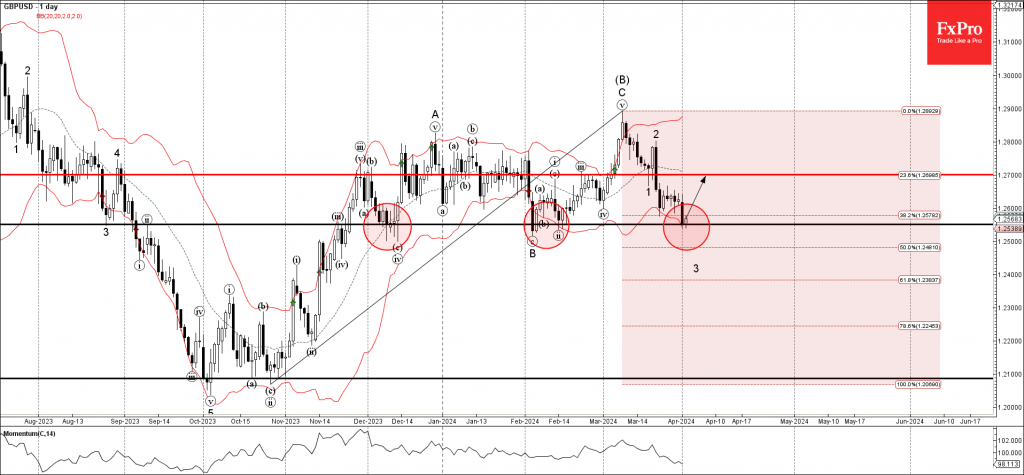

GBPUSD Wave Analysis

- Sterling reversed from pivotal support level 1.2550

- Likely to rise to resistance level 1.2700

Sterling recently reversed up from the pivotal support level 1.2550, which has been reversing the pair from the start of December, as can be seen below.

The support level 1.2550 was strengthened by the lower daily Bollinger Band and by the 38.2% Fibonacci correction of the upward impulse from October.

Given the strength of the support level 1.2550, Sterling can be expected to rise further to the next resistance level 1.2700.

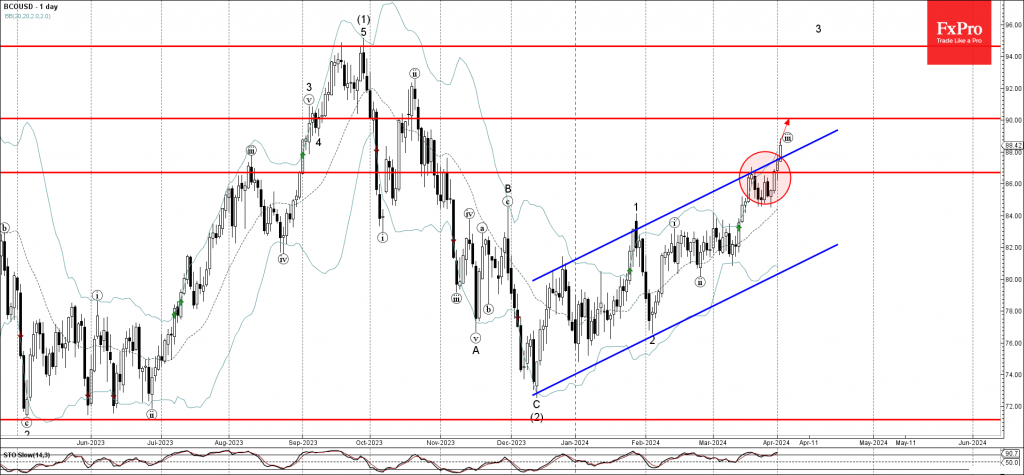

Brent Crude Oil Wave Analysis

- Brent crude oil broke resistance level 86.70

- Likely to rise to resistance level 90.00

Brent crude oil recently broke the resistance level 86.70, which reversed the price with the daily Evening Star in March.

The breakout of the resistance level 86.70 was preceded by the breakout of the resistance trendline of the daily up channel from December.

Brent crude oil can be expected to rise further to the next round resistance level 90.00, target price for the completion of the active impulse wave iii.

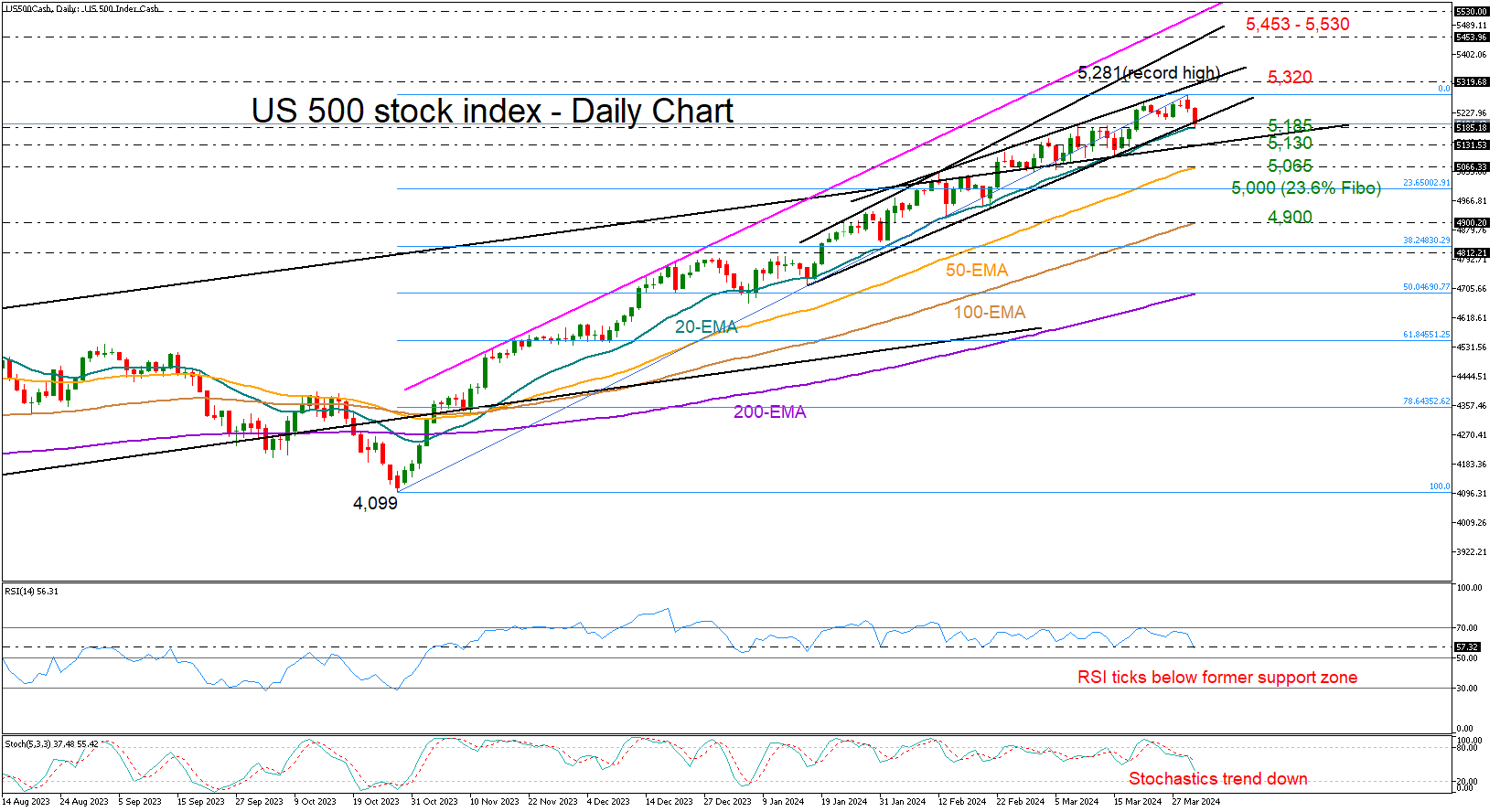

US 500 Index Retreats from Record High

- US 500 faces downside pressures for the second consecutive day

- More weakness possible, but key support levels are nearby

The US 500 stock index (cash) opened negative on Tuesday, strengthening its negative momentum towards its 20-day exponential moving average (EMA), which has been buffering downside movements since the start of the year, around 5,185.

With the RSI marking a new low below an important support area and the stochastic oscillator decelerating, the odds for a bearish impulse have increased.

If the bears stay in charge, the ascending trendline, which connects the December 2022 and July 2023 highs, could add some footing around the 5,130 level ahead of the 50-day EMA at 5,065. The 5,000 round mark, which overlaps with the 23.6% Fibonacci retracement of the ongoing rally, could be the next destination on the downside. Should selling forces breach that floor too, the door will open for the 100-day EMA at 4,900.

On the upside, the price will have to run above the resistance trendline at 5,320 in order to reach the ascending trendline at 5,453. There might be another obstacle around 5,530 before the 5,600 psychological level comes into view.

In a nutshell, the positive trend in the US 500 stock index is still intact, though given the discouraging short-term signals, the current weakness in the price could persist.

Australian Central Bank Meeting Removes Rate Hike Option – Minutes

The Reserve Bank of Australia minutes of the March meeting indicated that there was no mention of raising interest rates. This points to a less hawkish stance but the Australian dollar is unchanged following the release of the minutes.

Reserve Bank drops reference to rate hike

The RBA maintained the cash rate at 4.35% at the March 19th meeting. This marked the third straight time that the RBA paused. This move was expected and what was of more interest to traders was the slight change in language in the rate statement. The February statement said that “a further increase in interest rates cannot be ruled out” and this was changed to the “Board is not ruling anything in or out” at the March meeting.

The markets focused on this slight change in language, viewing it as a signal that the RBA had removed its hiking bias. This sent the Australian dollar sharply lower in the aftermath of the meeting, although it fully recovered by the next day.

The minutes have strengthened the view that the RBA is moving away towards a more neutral stance and is more open to rate cuts sometime this year. The markets had dismissed the possibility of a rate hike and the minutes appear to have laid to rest any lingering concerns that the central bank could continue to raise rates.

The minutes are a clear indication that the Board is becoming more confident that the battle against inflation is on its way to being won, although there is still some way to go before inflation is brought down to the target range of 2 to 3 percent.

Inflation dropped to 4.1% in the fourth quarter of 2023 but that is still high and the RBA is unlikely to lower rates before inflation drops closer to the target range. As we are seeing with the Federal Reserve and other major central banks, inflation is moving in the right direction but the RBA is not in any rush to lower rates. The central bank is widely expected to pause again at the next meeting on May 7.

AUD/USD Technical

- AUD/USD is putting pressure on resistance at 0.6519. Above, there is resistance at 0.6554

- There is support at 0.6480 and 0.6445

EURUSD Gets Set to Go

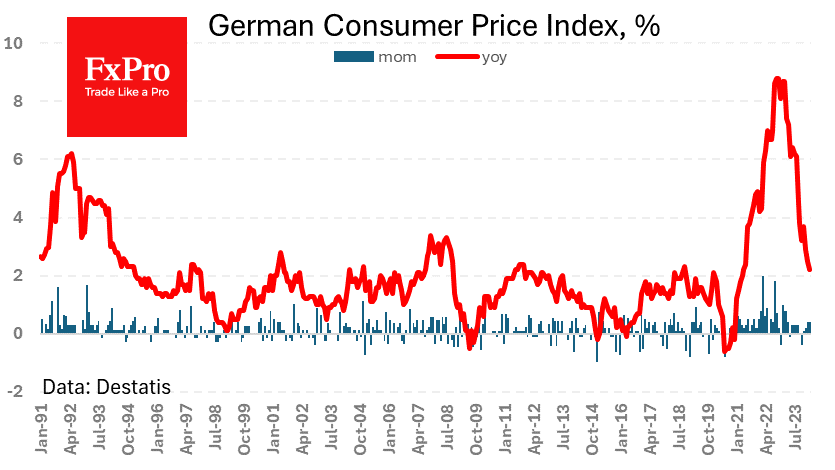

The slowdown in German inflation is fuelling hopes that the ECB will ease policy in the coming months. German CPI rose 0.4% m/m, weaker than the 0.5% expected. Annual inflation slowed from 2.5% in February to 2.2% in March, the lowest since May 2021.

Germany’s reading is a useful guide to what to expect in the eurozone on Wednesday, which is likely to come in weaker than average market expectations for headline inflation to slow from 2.6% to 2.5% and core inflation to slow from 3.1% to 3.0%. At the same time, it would take a significant deviation from the forecasts to have a material impact on prices.

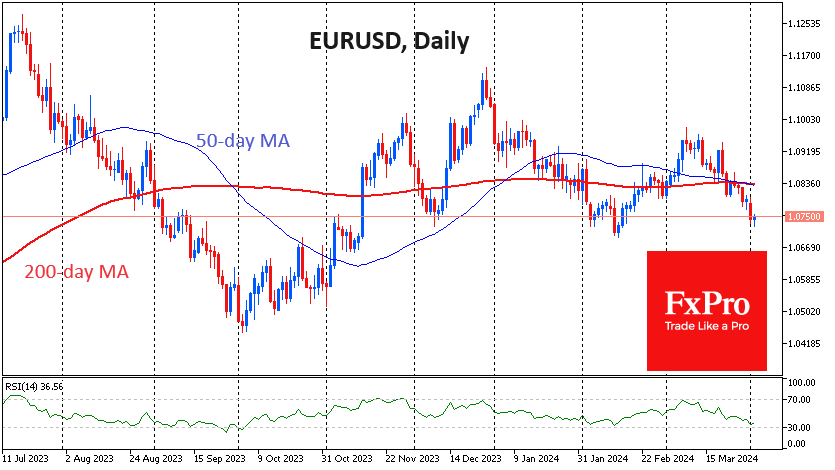

EURUSD slipped to 1.075, the lower boundary of the range since November. This is a good starting position for new momentum on a breakout or bounce. US data released on Monday was supportive of a strong dollar, while German inflation data was in favour of a weaker euro. If the balance of power remains the same, EURUSD may decide to move towards 1.05.

Sunset Market Commentary

Markets

Core bonds dropped with a continued rise in oil prices ($88.5/b) serving as a common factor. German Bunds underperform US Treasuries. That’s partially a catch-up move as European markets missed out on US action yesterday (Easter Monday). German yields add between 1 (2-y) to 14.3 bps (30-y). The curve steepening (less inverse) happens against the background of the ECB survey showing consumer inflation expectations decreasing to 3.1% for the 1-year ahead gauge (but stabilizing at 2.5% longer term (3-y)) as well as German actual inflation figures coming in slightly below consensus. Prices rose 0.6% m/m in March. That’s a lot but given the high bar last year (1.1% m/m), it still caused the yearly figure to ease from 2.7% to 2.3%. After last week’s Spanish and French outcome, the risks for tomorrow’s euro zone reading (0.9% m/m, 2.5% y/y) are marginally tilted to the downside. They are likely to cement expectations for a less restrictive monetary policy stance in the near term at a time when the economy is already bottoming on its own. Money markets in the region fully price in the inaugural June ECB cut. With another (close to) three in the pipeline, we think that’s more than enough for 2024. US rates continue down Monday’s path, adding between 1.7 (2-y) to 8.2 bps (10-y) in a similar curve shift. All maturities but the 2-y are either heavily testing (3-7 year bucket) or pushing through (10 year and longer) to new year-to-date highs, regardless of the fact that there’s still some important data to be published today (JOLTS) and later this week (services ISM, payrolls). US money markets push back the timing for a first Fed rate cut, with not even July fully discounted.

Bund underperformance helps the euro to hold ground against the dollar, but only barely so. EUR/USD tested the upper bound of the 1.0724 (December correction low)/1.0695 support area. The pair is currently changing hands in the mid 1.07/1.08 area, nothing more than a few ticks higher than yesterday’s close. DXY (trade-weighted dollar index) returned south of 105 in technically insignificant trading. USD/JPY is still eager for a topside break above 152, regardless of the verbal warnings from BoJ/Japanese government officials. USD/CNY meanwhile crept higher to the highest level since mid-November (7.236) in a sign Chinese authorities do allow a further CNY depreciation, provided the process goes gradually.

News & Views

The ECB today published its monthly consumer expectations survey from February. The median rate of perceived inflation over the previous 12 months decreased from 6.0% in January to 5.5%. Median expectations for inflation over the next 12 months also eased from to 3.1% from 3.3%, the lowest level since the start of the start of the war in Ukraine in February 2022. Expectations for inflation 3-years ahead were unchanged at 2.5%. With respect to demand and activity, European consumers saw nominal income growth rising from 1.2% to 1.4%. Perceived nominal spending growth over the previous 12 months eased from 6.6% to 6.4%. Consumers expected spending to grow 3.7% over the next 12 months (unchanged) but still see an contraction of economic activity of -1.1% in the coming year. They also expect unemployment remains unchanged at 10.9% versus 10.5% currently perceived. As a reference, the official EMU unemployment rate (Eurostat figures) was 6.4% in January. Consumers expect the price of their homes to increase by 2.4% in the coming year (2.2% previously). Mortgage rates are seen unchanged at 5.1%.

The Swedish Riksbank today made a submission to the Riksdag with a proposal to restore its equity to the statutory base stipulated in the Sveriges Riksbank Act. The proposal involves a capital injection of SEK 43.7 bln in 2024. The RB is obliged to make such a submission if the reported equity falls below one third of the target level. After the allocation of 2023 profit, equity is expected at SEK -2 bln compared to a statutory base level of SEK 41.7 bln. The Riksbank reported a loss in 2022 caused by a sharp rise in interest rates both in Sweden and abroad due to a rapid increase in inflation. The higher interest rates decimated the market value of the RB’s bonds in Swedish krona and foreign currency. This unrealised loss caused the Riksbank's equity to become negative. RB governor Thedéen assesses that a negative equity does not affect the RB’s ability to conduct monetary policy short-term. However it is necessary that the RB is financially independent to maintain confidence in an independent policy longer term.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0716; (P) 1.0758; (R1) 1.0784; More...

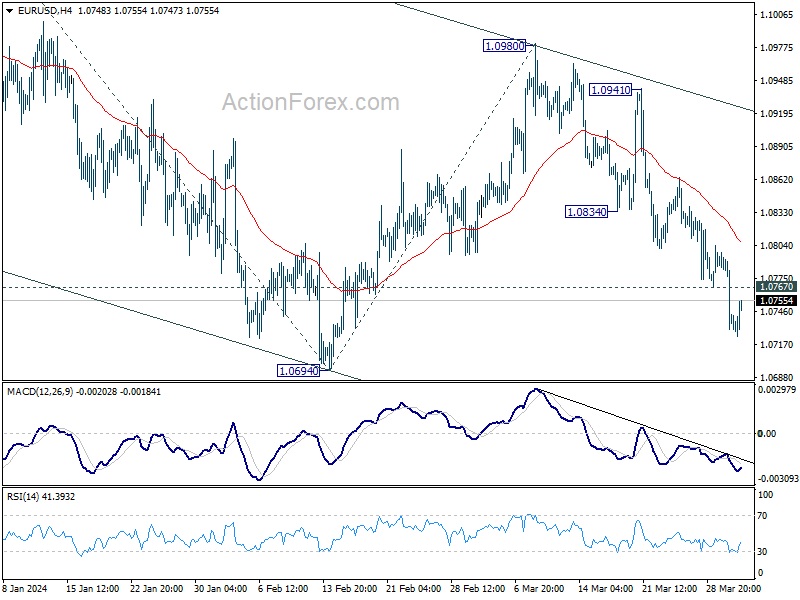

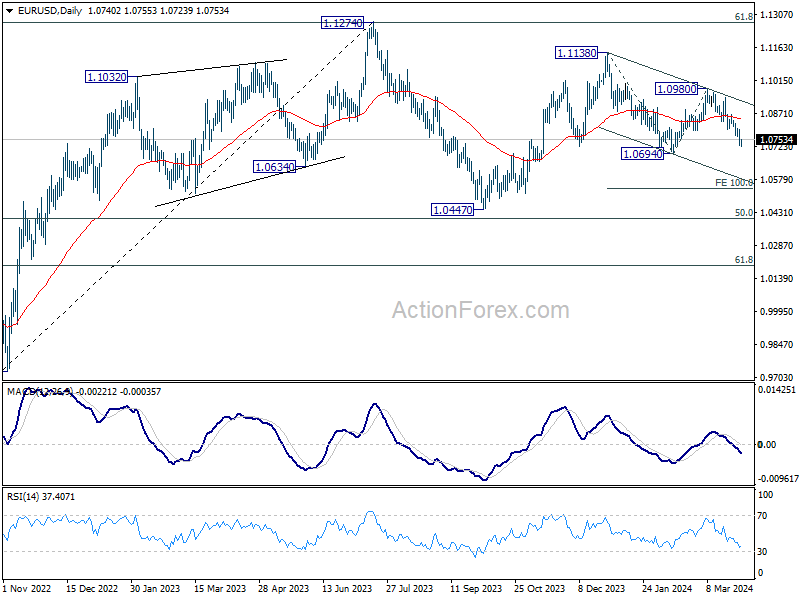

EUR/USD's decline is still in progress and intraday bias stays on the downside for 1.0694 support. Decisive break there will resume the whole decline from 1.1138 and target 100% projection of 1.1138 to 1.0694 from 1.0980 at 1.0536. On the upside, above 1.0767 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.0834 support turned resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

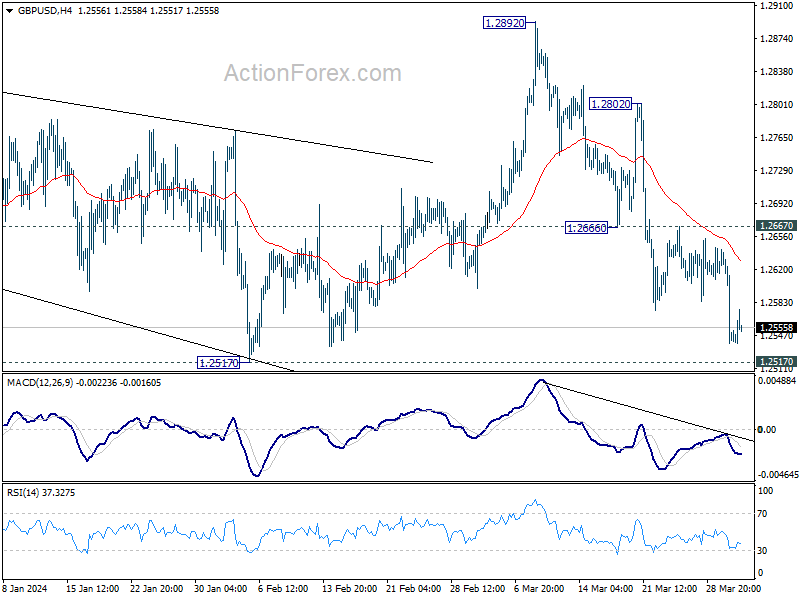

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2513; (P) 1.2578; (R1) 1.2617; More...

GBP/USD's decline is still in progress and intraday bias stays on the downside for 1.2517 structural support. Decisive break there will suggest that rise from 1.2036 has completed at 1.2892 already, and turn near term outlook bearish. For now, risk will stay on the downside as long as 1.2667 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which might still be in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

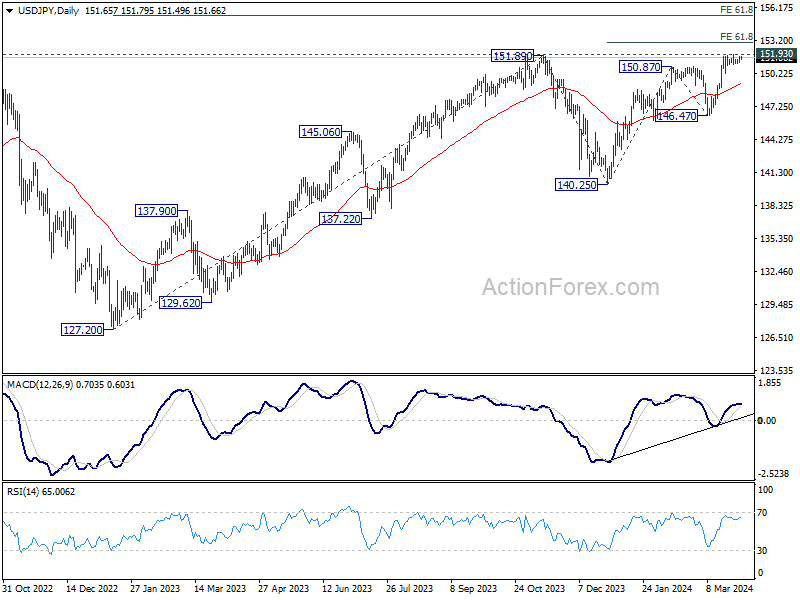

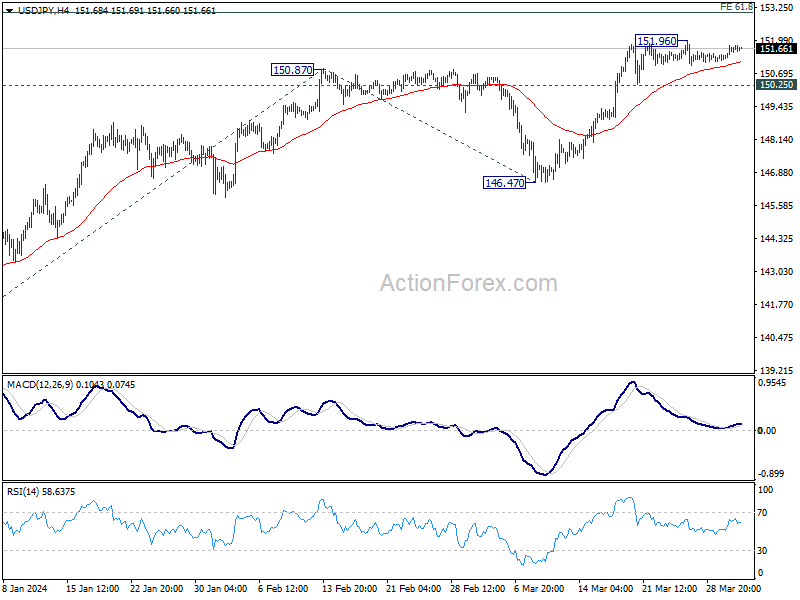

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.33; (P) 151.55; (R1) 151.88; More...

Range trading continues in USD/JPY and intraday bias remains neutral. On the downside, break of 150.25 support should confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 149.35). Nevertheless, sustained break of 151.93 key resistance will confirm long term up trend resumption. Next near term target will be 61.8% projection of 140.25 to 150.87 from 146.47 at 153.03.

In the bigger picture, correction from 151.87 (2023) high could have completed at 140.25 already. Rise from 127.20 (2023 low), as part of the long term up trend, is probably ready to resume. Decisive break of 151.93 resistance (2022 high) will confirm this bullish case. Next medium term target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. This will remain the favored case as long as 146.47 support holds, in case of another pullback.