Sample Category Title

Stars Aligned for Dollar Yesterday, But Greenback Succumbed

Markets

German Bunds opened softer yesterday in a catch-up move with the US Treasury sell-off on (Easter) Monday. Selling pressure remained until the start of US trading despite lower-than-expected German CPI data and a slight fall in short-term (1-yr) inflation expectations in an ECB Survey. Both cement the case for a (discounted) June ECB rate cut. Sluggish growth and disinflation momentum create a window of opportunity for the ECB, but it risks closing rapidly as we believe that the Fed will err on the side of “higher for longer” at least until after the Summer break while European inflation dynamics (Y/Y) will accelerate again in H2. Therefore we think that EMU money markets are still positioned too aggressively when it comes to making monetary policy even less restrictive after June (leaning to a cumulative 100 bps of rate cuts this year). Rising oil prices initially extended the Bund sell-off with Brent crude rising to $89/b for the first time since end October. Dynamics changed in the run-up to the US opening bell with US equity futures sinking after a significant decline in Tesla sales volumes. A few hours earlier, BYD delivered a similar message. The move pulled European equity benchmarks from small gains to closing losses in the direction of 1%. Key US markets opened with similar losses and hovered around opening levels for much of the remaining session. This bout of risk aversion helped core bonds off intraday lows and outweighed US JOLTS job openings (stable at 8.75mn). Daily changes on the German yield curve (compared with Thursday’s close) yesterday ranged between -1 bp (2-yr) and +12.3 bps (30-yr). US yields fluctuated between -1.6 bps (2-yr) and +4.7 bps (30-yr). Stars aligned for the dollar yesterday (stock & bond sell off; higher oil prices), but the greenback succumbed. The dollar failed to cling to Monday’s post-ISM gains. The trade-weighted dollar (DXY) threw the towel after failing to break 105 resistance (YTD high). EUR/USD set a new short term low at 1.0725, without testing the 1.0695 YTD low.

Asian risk sentiment is negative this morning with similar losses to 1% and slightly more. The Taiwan earthquake had only a minor additional effect. The eco calendar contains EMU CPI numbers (risks for lower outcome) and US ADP employment & services ISM. The latter will be pivotal for trading with US rates and USD still close to resistance levels. Fed Chair Powell speaks on the economic outlook after European close in what’s today’s final potential game changer. Will he stick with the balanced approach after the March policy decision (giving equal weight to a weakening labour market & disinflation) in determining the right timing of making policy less restrictive?

News & Views

Minutes of the March CNB meeting confirmed that price stability in the country had been restored, allowing the central bank to continue reducing rates cautiously. To maintain inflation at the target level, it is necessary to keep policy tight until core inflation is fully under control. A cautious approach allows the CNB to interrupt or halt the policy decline in rates at restrictive levels if necessary. Governor Michl assesses that the neutral policy rate is higher than in the past. Risks remain modestly inflationary, including a slower decline in still elevated inflation expectations. Given a tight labour market, this can translate into stronger wage demands. The recent deeper than expected decline in headline inflation was mainly due to lower food prices. Some members see the continuing rise in services prices as a ground for caution. MPC members are mixed on the CZK-weakening of late. Jan Kubicek indicated that the FX rate is fostering monetary policy easing for the first time since quite some time. Eva Zamrazoliva on the other hand didn’t see current FX level as a significant risk to meeting the inflation target longer term. A majority continues to favour 50 bps rate cut steps due to upside inflation risks. Jan Frait and Tomas Holub dissented (75 bps).

The Chinese Caixin services PMI rose from 52.5 to 52.7 in March. The pace of activity accelerated as new business rose at the quickest pace year to date. Business confidence also improved further, but this wasn’t able to avoid an ongoing contraction employment. Input cost inflation in the sector slowed and this also filtered through into selling prices. The above-50 reading marked the 15th consecutive monthly expansion. Still the level of expansion remains below the longer run average. Combined with a further expansion in the manufacturing sector (51.1), the gain in the services sector also raised the composite index from 52.5 to 52.7.

The ‘Two or Three’ Cut Debate Heats Up

Mood was down in Asia today as the strongest earthquake in 25 years led to halted operations in TSM and United Microelectronics.

Elsewhere, major stock and bond markets in Europe and the US were painted in the red yesterday as well; rising oil and commodity prices fueled inflation expectations while further strength in the US economic data boosted worries that the Federal Reserve (Fed) may not cut the interest rates as much as wished this year. Yesterday’s data showed faster-than-expected recovery in factory orders, though job openings fell more than expected.

The market now prices less than three rate cuts from the Fed this year, below the three rate cuts plotted by the Fed members at last month’s FOMC meeting. And even though Fed’s Mary Daly and Loretta Mester said that three rate cuts look appropriate this year – God knows why – Mester added that ‘it’s a close call’ on whether fewer rate cuts will be needed. She was certainly referring to robust economic data and up-ticking inflation!

The US 2-year yield extended to 4.73% yesterday, the 10-year yield spiked to 4.40%, the S&P 500 tipped a toe below the 5200 level but managed to close above this psychological mark. Nasdaq closed near 1% lower and volatility rose. The US dollar index however retreated despite the positive pressure on yields.

Today, investors have their eyes set on the ISM non-manufacturing index and the latest ADP data. The US economy is expected to have added nearly 150K new private jobs in March. Friday’s jobs data should split hairs between those anticipating three rate cuts and those banking on just two. A strong set of jobs figures – that would add more spice to strong US growth and picking inflation - should further soften the Fed doves’ hand, weigh on equity and bond valuations and keep the US dollar sustained against most majors, starting with the euro.

The EURUSD rebounded before hitting 1.0740 yesterday as the US dollar fell sharply despite supportive economic data. But the data released in Europe confirmed that inflation in Germany cooled for a third straight month and today’s aggregate Eurozone inflation is expected to show further easing. The headline inflation is expected to ease from 2.6% to 2.5% and core inflation from 3.1% to 3%.

Unlike the strong US growth and rising US inflation since the start of the year, the persistent slowdown in European inflation and gloomy Eurozone economies justify a European Central Bank (ECB) rate cut and should continue to weigh on the EURUSD. Across the Channel, Cable saw support near 1.2550 on a broadly softer US dollar, but the data fueled the Bank of England (BoE) rate cut hopes: inflation in British stores dropped to the lowest level in more than two years.

Overall, the US is isolated on an island with a surprisingly strong economic data and rising inflation. But the dollar inflation could easily spill over to the rest of the world if the US dollar gained strength backed by a significant retreat in dovish Fed expectations.

FTSE 100 in a good place to catch up with the rest of Western indices

The FTSE 100 benefited from rising oil & commodity prices and softer sterling to extend gains past the 8000p psychological mark. The FTSE 100 will likely see more tailwinds if oil and commodity prices pick up momentum and the British blue-chip index could be a good hedge against rising inflation worries.

Across the Atlantic, the moodiness in US stocks since the quarter started is mostly due to a retreat in Fed expectations because of strong data, but note that strong economy per se is not a reason to be sad about. This is why the S&P 500 could temper the significant retreat in Fed cut expectations since the start of the year. If the US earnings continue to satisfy, the US stock markets may avoid a significant meltdown.

Oops

Tesla released the first quarter deliveries report yesterday and the numbers were hard to swallow. Analysts were expecting around 6% drop in deliveries last quarter compared to a year earlier, but the deliveries fell 8.5%. Inventories rose and the inventory build-up will be another major headwind to the cashflow. As such, Tesla closed the session almost 5% lower and will hardly reverse losses when the 50% annual sales growth narrative continues to fade away. Tesla’s PE ratio is still around 63 giving it a large room for extending losses.

Elsewhere, Rivian built and sold more EVs than expected but shares plunged more than 5% on overall gloomy outlook for the EV sector.

All Eyes on Euro Area Inflation

In focus today

In the US, March ADP private sector employment and ISM Services are due for release. Yesterday's labour market data supported the notion of labour markets gradually becoming more balanced. Hence, it will be interesting to see if today's data corroborates this view.

In the euro area, today's focus is on euro area inflation for March. We expect inflation to come in at around 2.4% y/y which is slightly below the consensus forecast of 2.5% due to the recent downside surprises in the four biggest economies. Inflation is likely to decline due to falling food inflation and core goods. Service inflation is still sticky which means core inflation will likely tick down only marginally to 3.0% from 3.1% in February. The likely decline in inflation is good news for the ECB but the sticky underlying service inflation and uncertainty regarding high wage growth means we only foresee the first rate cut in June. The euro area unemployment rate for February is also released, which we expect remained stable at 6.4%, highlighting a continued strong labour market.

Economic and market news

What happened overnight

In China, similar to the NBS Services PMI, the Caixin Services PMI edged up to 52.7 in March, propelled by new business increasing at the fastest pace in three months. Coupled with the strong manufacturing PMIs of late, this supports the narrative of the Chinese economy gaining momentum in Q1.

In Taiwan, the island experienced its most powerful earthquake in nearly 25 years, leading to damaged buildings, the suspension of rail traffic, and the necessity to evacuate semiconductor manufacturing plants. Shares of Taiwan Semiconductor Manufacturing Co. were down 1.4% in early trade.

What happened yesterday

In the US, February JOLTS Job Openings came in very close to expectations at 8.76m (cons: 8.75m), while the January print was revised down to 8.75m. Supply of workers ticked higher in February, seeing the ratio of job openings to unemployed job seekers dropping to 1.36 from 1.43. While this is close to the lowest levels seen post-pandemic, it remains above pre-pandemic averages. Other indicators painted a bit of a mixed picture, as involuntary layoffs ticked somewhat higher, though from a low level, while hiring also was slightly higher despite weaker signals from leading surveys such as the NFIB. Bottom line, yesterday's data releases broadly support the narrative of labour markets gradually balancing.

Moreover, Fed's Mester (voting member) was on the wire, stating that she still believes the Fed is on track to cut rates this year but underscored the necessity for more data before confirming such a move is possible. Fed's Daly (voting member) also made public remarks, noting that three rate cuts this year are a "very reasonable" baseline, though nothing is guaranteed.

In the euro area, Banca d'Italia's nowcast model, EuroCOIN, which estimates quarterly growth in the euro area, rose markedly in March, turning positive for the first time since February 2023. This raises questions about the pace of cuts following June.

German HICP inflation declined slightly more than expected in March to 2.32% y/y from 2.74% in February. The decline was driven by lower food, core goods and energy. German core CPI declined to 3.25% in March from 3.37%, while core services inflation rose once again to 3.7%. Hence, service inflation is still sticky in Germany, but this was somewhat expected due to the timing of Easter. The seasonally adjusted series show core inflation at 0.16% m/m s.a. as service inflation was 0.29% m/m s.a.

In commodities, brent crude briefly crossed the USD89/bbl mark as oil supply faced pressure due to Ukrainian attacks on Russian energy facilities, along with escalating tensions in the Middle East, while demand is supported by stronger global growth expectations. Moreover, OPEC+ is scheduled to convene today, though Reuters suggests that any recommendations for oil output policy changes at the meeting are unlikely.

Equities: Global equities were down for the second day in a row as the "overheating" fear took over. With manufacturing outlook improving, oil and commodity prices rising, the higher-for-longer narrative is challenged by a too hot economy that will keep central banks sidelined, and the tight policy will continue. This looks very much like the situation we had in most of Q3 last year. For equities this means energy and materials are the relative winners while long duration growth stocks and small caps are suffering. In US yesterday, Dow -1.0%, S&P 500 -0.7%, Nasdaq -1.0% and Russell 2000 -1.80%. Asian markets are broadly lower this morning and the same goes for European and US futures.

FI: The main event in the European markets today is the release of the European inflation data for February, where we expect to see a decline after a string of national inflation data came in modestly lower than the consensus forecast. The slight decline in the national inflation data including Germany had limited impact on the European yields and rates yesterday, where 10Y German government bond yields ended some 10bp higher relative to the level before Easter. However, much of the impact came from the 10Y Treasury yield that has risen some 15bp relative to level before Easter due to the stronger than expected ISM data released on Monday.

The stronger US data have dampened the rate cut expectations in the US and again the markets are looking towards "higher for longer" regarding monetary policy. Two Fed Officials said yesterday that they still expect three rates cuts in 2024. We have more speeches from Federal Reserve officials today including Fed Chairman Powell as well as the ISM service data ahead of the labour market report on Friday.

FX: Oil prices continue to climb higher and yesterday Brent crude rose to the highest level since October last year, which also contributed to sending NOK FX higher despite the sour risk sentiment. The broadly stronger USD over Easter retreated slightly in yesterday's session, with EUR/USD hovering around 1.0750. Today, focus turns to euro area inflation data with inflation data from Germany out yesterday pointing to a print below the consensus expectation. CHF continues to trade on the backfoot in line with our expectation after the SNB initiated its cutting cycle in March.

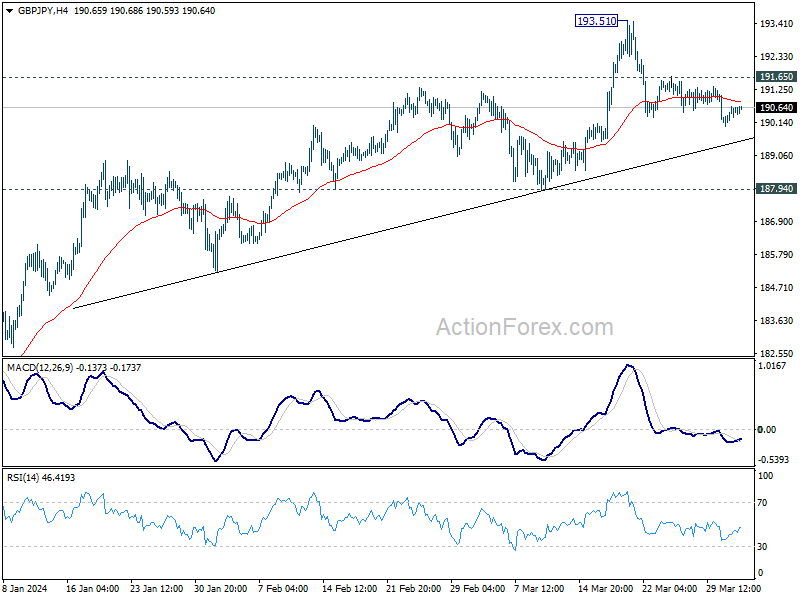

GBP/JPY Daily Outlook

Daily Pivots: (S1) 190.21; (P) 190.46; (R1) 190.88; More.....

Further decline is expected in GBP/JPY with 191.65 minor resistance holds. Fall from 193.51 would target 187.94 structural support. On the upside, break of 191.65 minor resistance will turn bias back to the upside for retesting 193.51.

In the bigger picture, current rally is part of the up trend from 123.94 (2020 low), and is in progress for long term resistance (2015 high). Break of 187.94 support is needed to be the first sign of medium term topping. Otherwise, outlook will remain bullish in case of retreat.

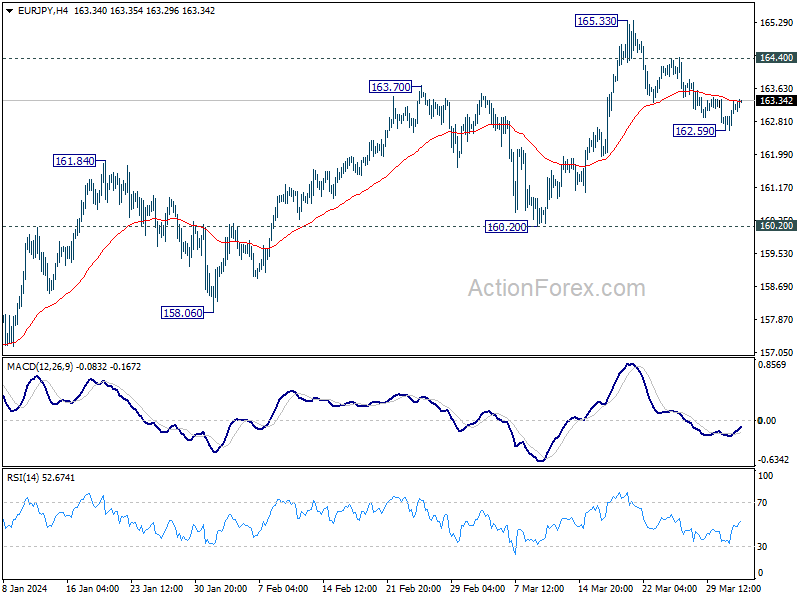

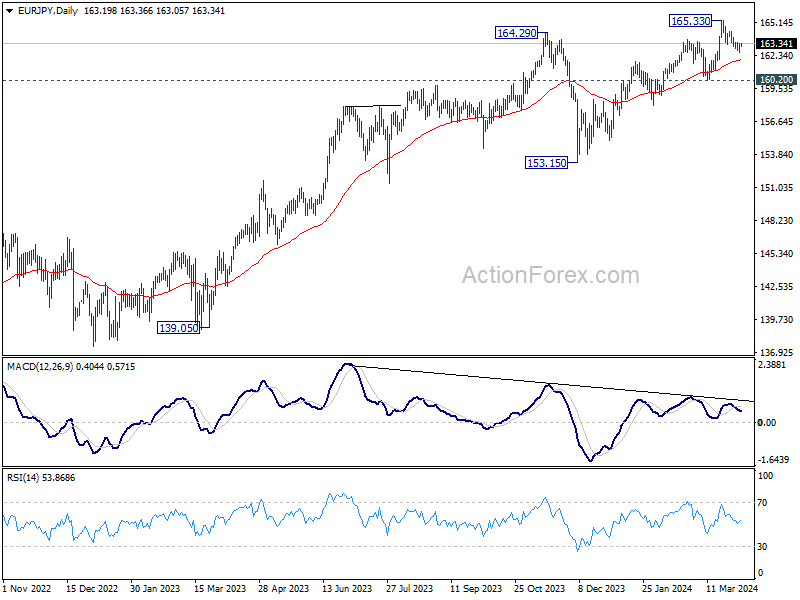

EUR/JPY Daily Outlook

Daily Pivots: (S1) 162.77; (P) 163.06; (R1) 163.49; More...

Intraday bias in EUR/JPY is turned neutral gain with current recovery. On the downside, below 162.59 will resume the fall from 165.33 to 160.20 structural support next. On the upside, however, break of 164.40 minor resistance will bring retest of 165.33 instead.

In the bigger picture, current rally is part of the up trend from 114.42 (2020 low), which is still in progress. Next target is 169.96 (2008 high). Break of 160.20 support is needed to be the first sign of medium term topping. Otherwise, outlook will stay bullish in case of retreat.

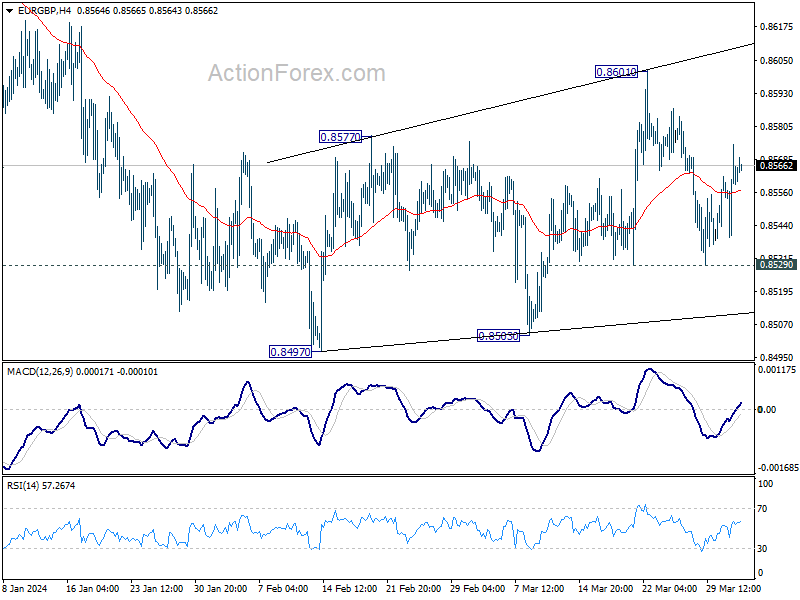

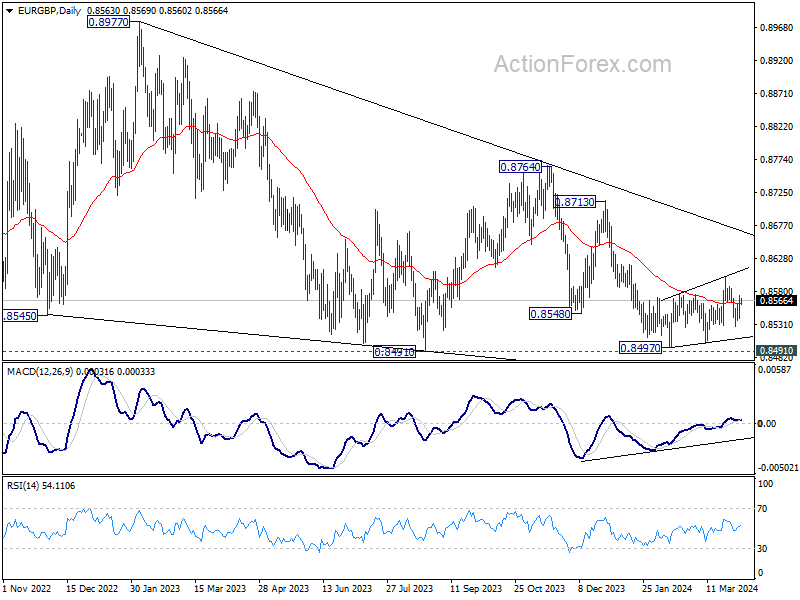

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8544; (P) 0.8559; (R1) 0.8578; More...

No change in EUR/GBP's outlook and intraday bias stays neutral. On the downside, firm break of 0.8529 support will argue that the corrective recovery from 0.8497 has completed at 0.8601. Intraday bias will be back on the downside for retesting 0.8497 low next. On the upside, break of 0.8601 will resume the rebound instead.

In the bigger picture, there is no clear sign that down trend from 0.9267 has completed, despite loss of downside momentum as seen in D MACD. As long as 0.8713 resistance holds, the down trend will remain in favor to resume through 0.8491 low at la later stage.

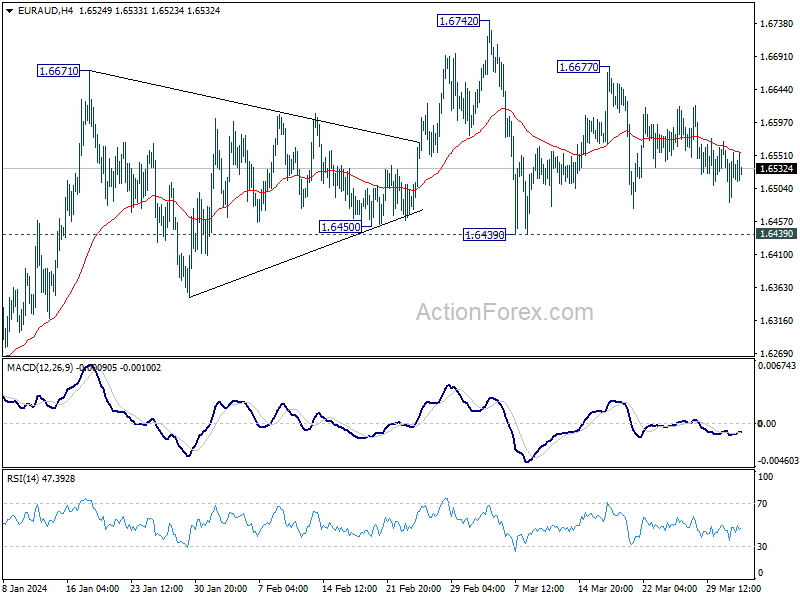

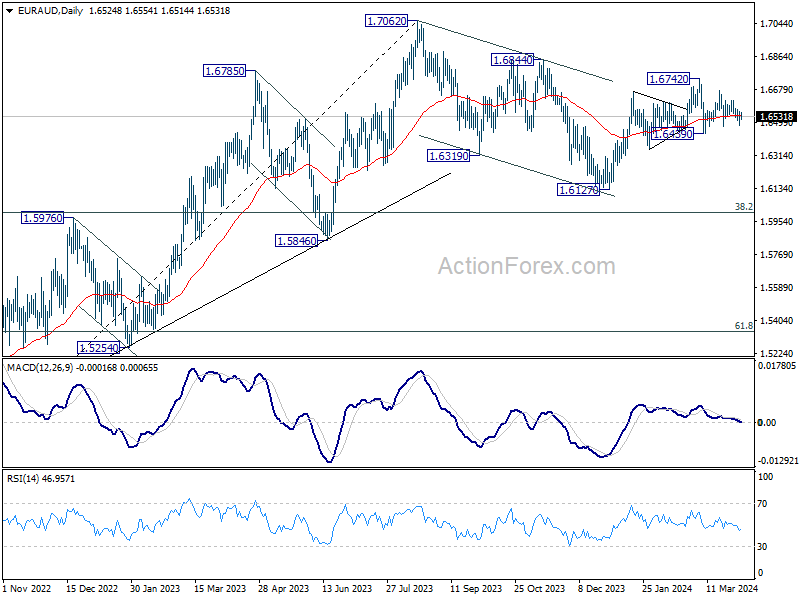

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6484; (P) 1.6525; (R1) 1.6563; More...

Range trading continues in EUR/AUD and intraday bias remains neutral. Near term outlook will stay cautiously bullish as long as 1.6439 support holds. On the upside, above 1.6677 will target 1.6742 first. Decisive break there will resume whole rise from 1.6127 and target 1.6844 resistance next.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

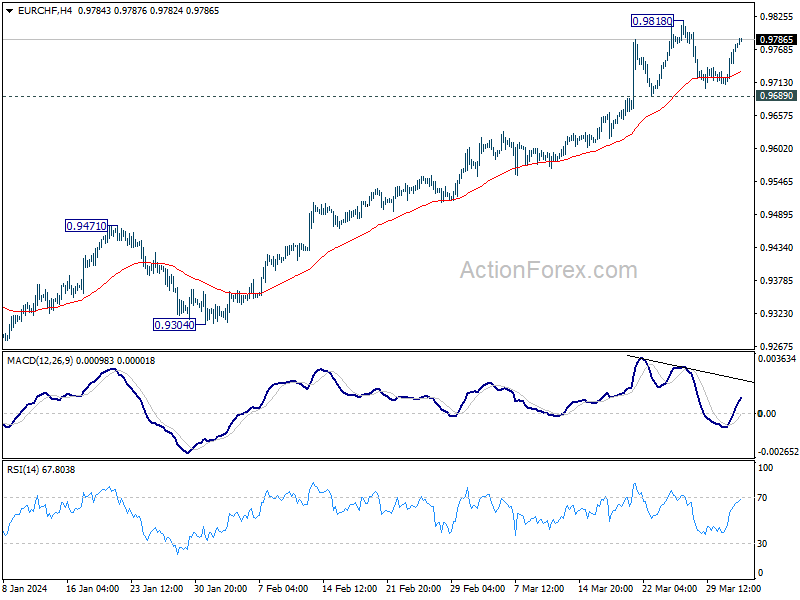

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9731; (P) 0.9755; (R1) 0.9803; More...

EUR/CHF is extending the consolidation from 0.9818 and intraday bias remains neutral. Another rally is expected as long 0.9689 support holds. On the upside, above 0.9818 will resume the rise from 0.9252 towards 1.0095 key resistance next. Nevertheless, considering bearish divergence condition in 4H MACD, break of 0.9689 will indicate short term topping, and turn bias back to the downside for 55 D EMA (now at 0.9590) instead.

In the bigger picture, a medium term bottom should be in place at 0.9252 already, on bullish convergence condition in W MACD. Rise from there would now target 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even as a correction to the down trend from 1.2004. This will remain the favored case as long as 55 D EMA (now at 0.9576) holds.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3554; (P) 1.3569; (R1) 1.3581; More...

Intraday bias in USD/CAD remains neutral as range trading continues. On the upside, decisive break of 1.3612 resistance will resume whole rise from 1.3176 towards 1.3897 resistance. On the downside, firm break of 1.3419 support will argue that rebound from 1.3176 has completed. Near term outlook will be turned bearish for 1.3357 support first.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

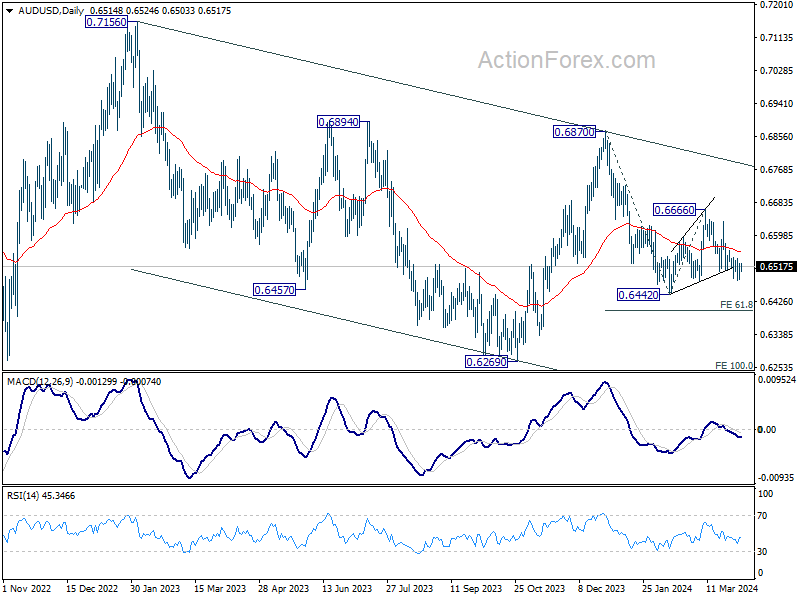

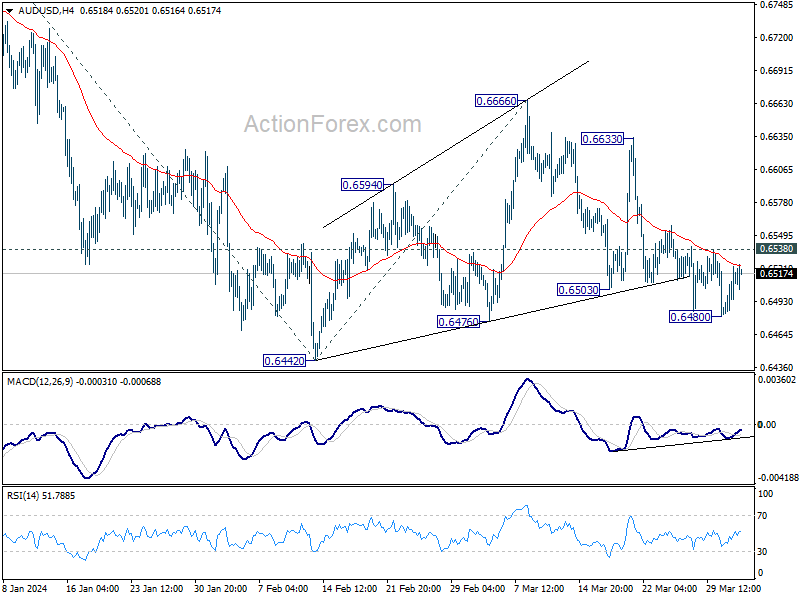

AUD/USD Daily Report

Daily Pivots: (S1) 0.6492; (P) 0.6508; (R1) 0.6534; More....

Intraday bias in AUD/USD is turned neutral again with current recovery. For now, risk will stay on the downside as long as 0.6538 minor resistance holds. Below 0.6480 will target 0.6442 support. Firm break there will resume whole decline from 0.6870 and target 61.8% projection of 0.6870 to 0.6442 from 0.6666 at 0.6401. Nevertheless, break of 0.6538 will delay the bearish case, and turn bias to the upside for stronger rebound.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which might still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.