Sample Category Title

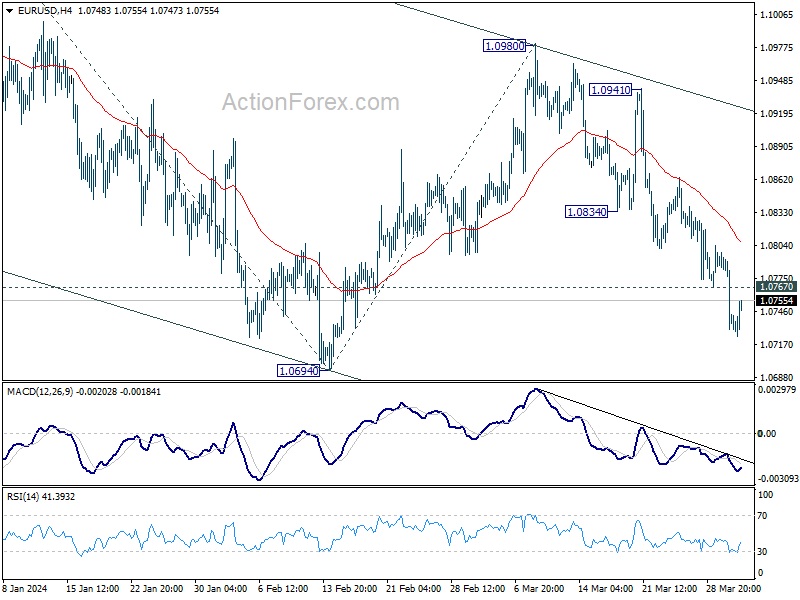

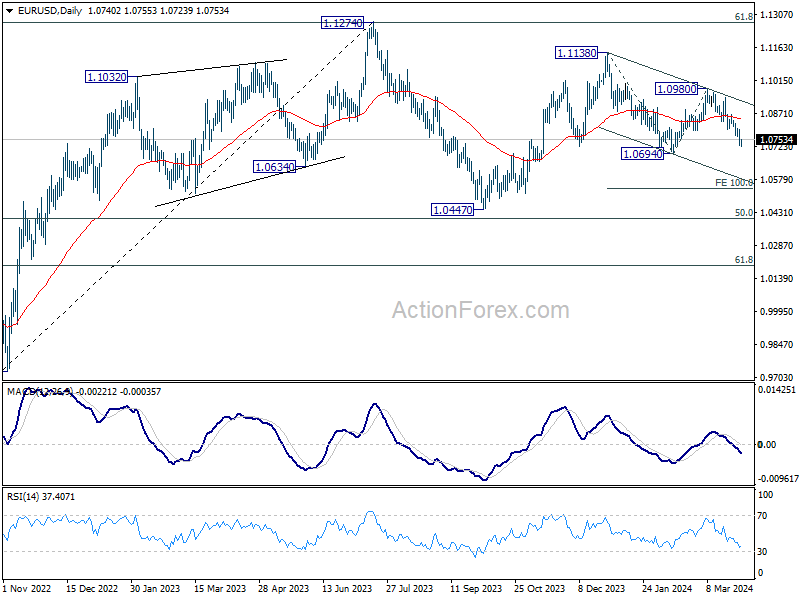

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0716; (P) 1.0758; (R1) 1.0784; More...

EUR/USD's decline is still in progress and intraday bias stays on the downside for 1.0694 support. Decisive break there will resume the whole decline from 1.1138 and target 100% projection of 1.1138 to 1.0694 from 1.0980 at 1.0536. On the upside, above 1.0767 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.0834 support turned resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

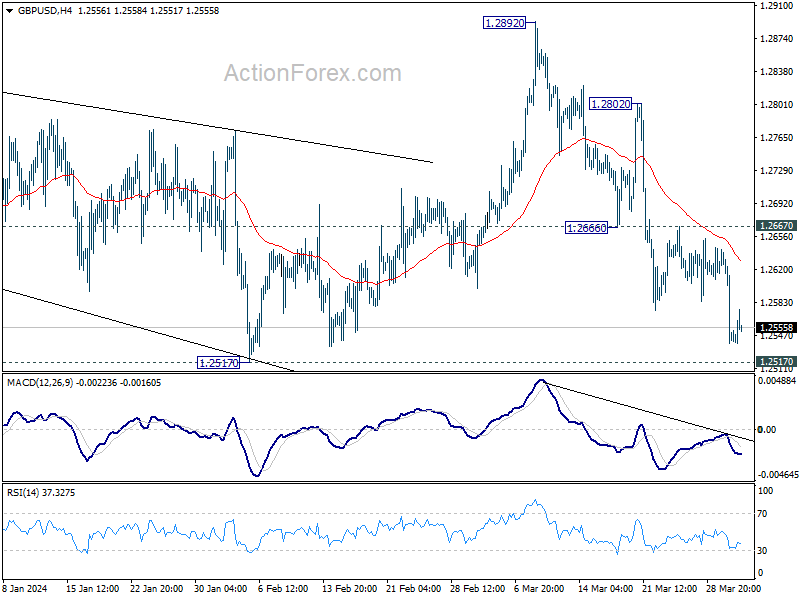

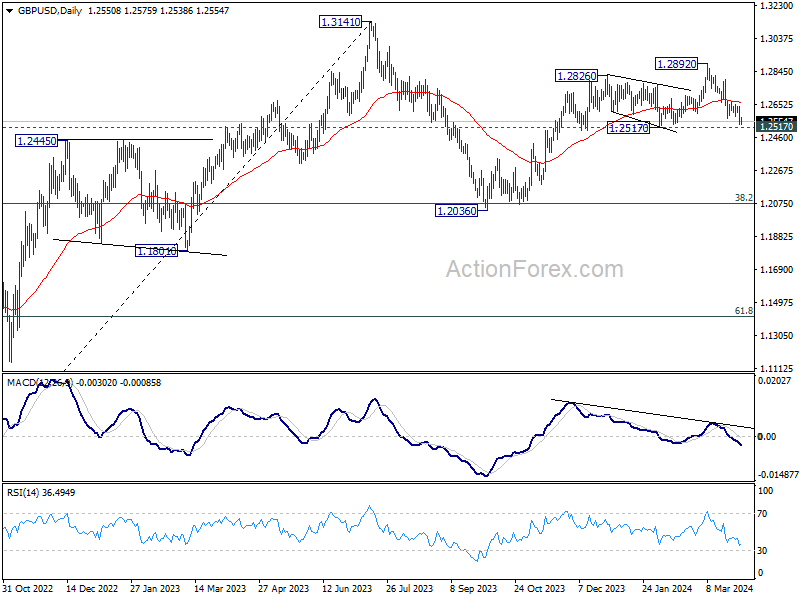

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2513; (P) 1.2578; (R1) 1.2617; More...

GBP/USD's decline is still in progress and intraday bias stays on the downside for 1.2517 structural support. Decisive break there will suggest that rise from 1.2036 has completed at 1.2892 already, and turn near term outlook bearish. For now, risk will stay on the downside as long as 1.2667 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which might still be in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

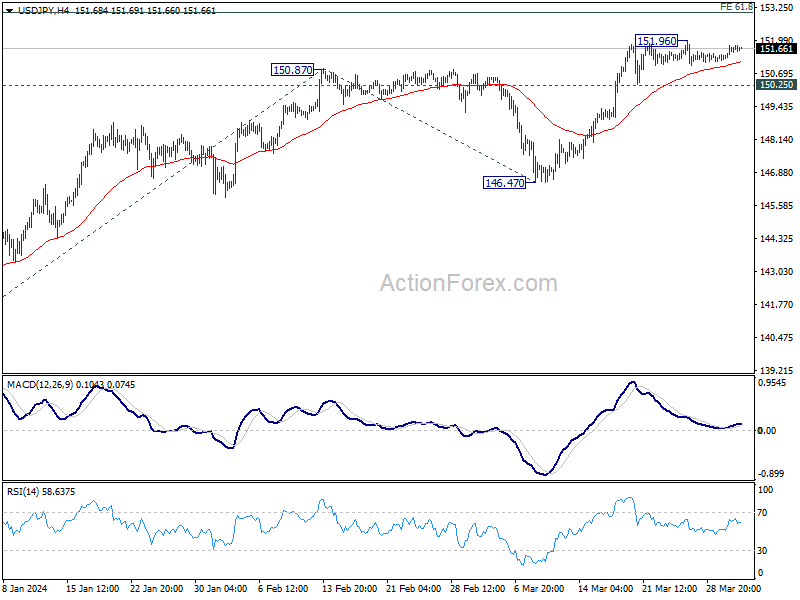

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.33; (P) 151.55; (R1) 151.88; More...

Range trading continues in USD/JPY and intraday bias remains neutral. On the downside, break of 150.25 support should confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 149.35). Nevertheless, sustained break of 151.93 key resistance will confirm long term up trend resumption. Next near term target will be 61.8% projection of 140.25 to 150.87 from 146.47 at 153.03.

In the bigger picture, correction from 151.87 (2023) high could have completed at 140.25 already. Rise from 127.20 (2023 low), as part of the long term up trend, is probably ready to resume. Decisive break of 151.93 resistance (2022 high) will confirm this bullish case. Next medium term target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. This will remain the favored case as long as 146.47 support holds, in case of another pullback.

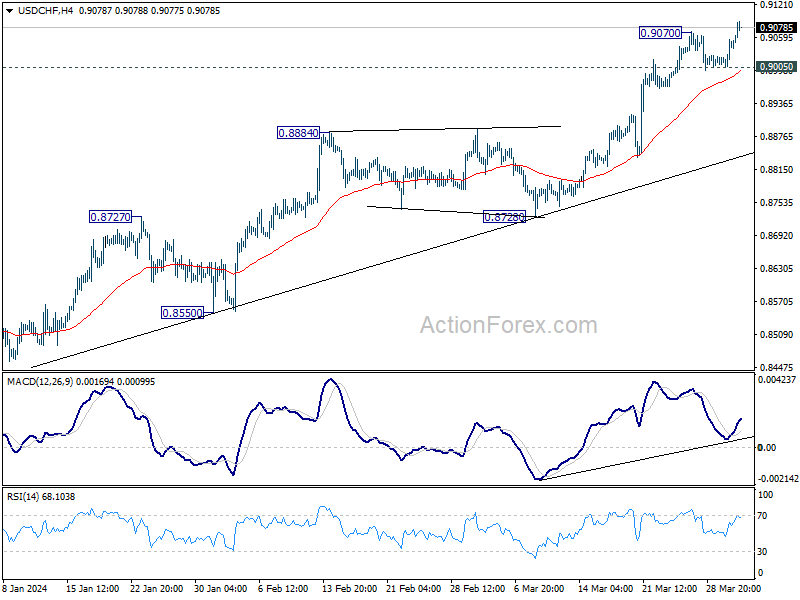

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9014; (P) 0.9036; (R1) 0.9066; More....

USD/CHF's rally resumed by breaking through 0.9070 temporary top and intraday bias is back on the upside. Current rally is in progress for 0.9243 key resistance next. On the downside, break of 0.9005 support is needed to indicate short term topping. Otherwise, outlook will stay bullish in case of retreat.

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.

Swiss Franc Falls Amid Surging Treasury Yields and Manufacturing Optimism

Currency markets shifted their attention towards the sell-off in Swiss Franc today, a reaction to the substantial rally observed in European and US treasury yields. With the 10-year yields in Germany and UK climbing back above 2.4% and towards 4.1% respectively, and US 10-year yield setting sights on 4.4%.

The surge in yields comes on the heels of unexpectedly strong manufacturing data from UK today and US yesterday, suggesting a resurgence in the sector globally. This development may provide some relief for global central banks, easing the imperative for continued rate cuts and offering a more nuanced approach to monetary policy adjustments.

Overall in the forex markets, Yen and Dollar are also under mild scrutiny, shedding gains against European majors and ranking as the next weakest currencies after Swiss Franc so far. In contrast, Australian Dollar is trading as the strongest currency of the day, with Sterling and New Zealand Dollar trailing behind. Euro and Canadian Dollar find themselves positioned in the middle of the pack.

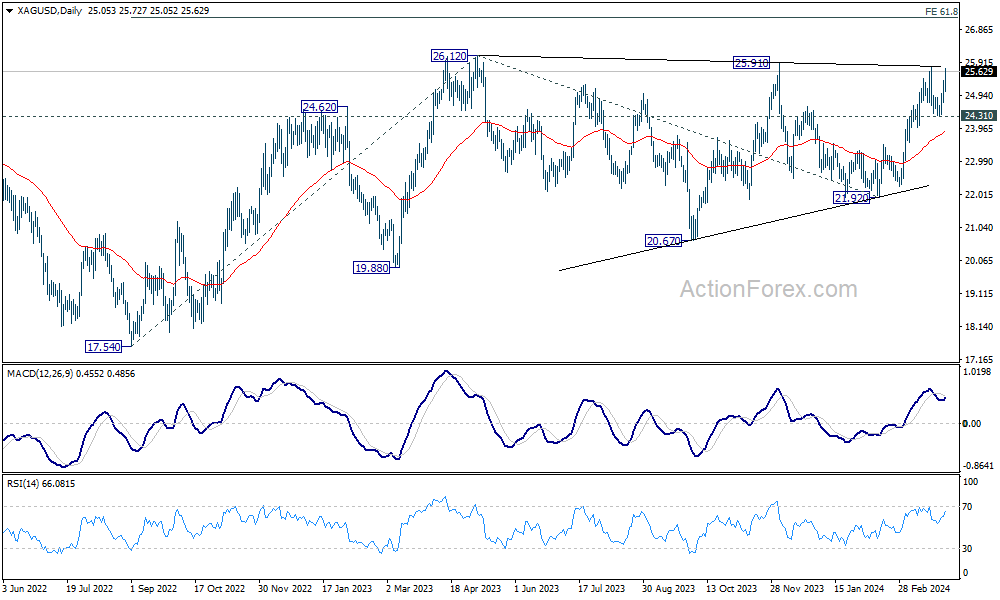

Technically, Silver's near term pull back could have completed at 24.31 already with this week's strong rally. Immediate focus is now on 25.91/26.12 resistance zone. Decisive break there will confirm resumption of whole medium term rebound from 17.54. Next target will be 61.8% projection of 17.54 to 26.12 from 21.92 at 27.22.

In Europe, at the time of writing, FTSE is up 0.30%. DAX is down -0.12%. CAC is down -0.10%. UK 10-eyar yield is up 0.1541 at 4.095. Germany 10-year yield is up 0.121 at 2.425. Earlier in Asia, Nikkei rose 0.09%. Hong Kong HSI rose 2.36%. China Shanghai SSE fell -0.08%. Singapore Strait Times rose 0.40%. Japan 10-year JGB yield rose 0.0104 to 0.752.

ECB consumer survey reveals 1-yr inflation expectations drop to 3.1%, a two-year low

ECB's Consumer Expectations Survey for February indicated continuing decline in consumers' median inflation perceptions over the past 12 months, marking a fifth consecutive month of decrease, settling at 5.5% down from 6.0% in January.

Furthermore, median expectations for inflation over the next 12 months have dipped to 3.1% from 3.3%. This level is the lowest recorded since the onset of Russia's conflict with Ukraine in February 2022.

Expectations for inflation three years ahead remained stable at 2.5%.

Eurozone PMI manufacturing finalized at 46.1, two largest cylinders out of action

Eurozone PMI Manufacturing was finalized at 46.1 in March, down from February's 46.5. Disparities across member countries continued, with Greece achieving a 25-month high at 56.9, Italy at 12-month high at 50.4, and Spain dipped slightly to 5.1.4. Meanwhile, Germany recorded a 5-month low at 41.9, and France fell to 46.2.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, provided a grim outlook based on the latest PMI figures, suggesting that the recession in Eurozone's manufacturing sector is likely to persist.

De la Rubia noted that Eurozone's manufacturing industry, heavily reliant on the collective output of Germany, France, Italy, and Spain—known as the Euro-4 countries—faces significant challenges as Germany and France experience notable downturns. While Italy and Spain showed signs of recovery in March and February, respectively, their improvements have yet to offset the overall sector's decline.

While that the pace of decrease in incoming orders has slowed in the first quarter, yet the industry still records a net loss in orders compared to the previous months. This trend raises concerns that the sector may soon exceed the longest contraction spell for incoming new orders recorded during the euro crisis from 2011 to 2013. Such a scenario underscores the difficulties facing a swift reversal in manufacturing activity across Eurozone.

UK PMI manufacturing finalized at 50.3, signaling first growth since July 2022

UK PMI Manufacturing was finalized at 50.3 in March, climbing from February's 47.5 to mark a 20-month high. This development represents the sector's first move above the critical 50.0 threshold since July 2022, indicating a tentative resurgence in manufacturing activity.

Rob Dobson, Director at S&P Global Market Intelligence, highlighted, "The end of the first quarter saw UK manufacturing recover from its recent doldrums." This recovery is attributed primarily to revival in production and new orders, spurred by strengthening domestic demand. Despite the growth being characterized as hesitant, following year-long downturns, the shift towards expansion signals a turning point for the sector.

The resurgence in demand has also buoyed manufacturers' confidence, with positive sentiment reaching an 11-month peak. Remarkably, 58% of companies surveyed anticipate increase in their output over the coming year.

However, challenges persist, including "weak export performance and supply chain stresses," which continue to hinder the sector's full recovery potential. The EU market, in particular, has been identified as the "main drag" on overseas demand, compounded by ongoing issues in the Red Sea impacting supply chains.

RBA minutes: No rate hike discussed, focus on preserving labor market gains

RBA's minutes from March 18-19 meeting revealed no explicit discussion on rate hikes, marking a departure from previous communications that outlined the board's considered options.

The board assessed that it would require more time to gain "sufficient confidence" in inflation's return to target range within a foreseeable timeframe. At the same time, it emphasized on the priority to "preserve as many of the gains in the labor market as possible."

These considerations led to the characterization of the policy outlook as ambiguous, with the board finding it "difficult to either rule in or out future changes" in the cash rate target.

Inflation remains elevated, albeit on a gradual decline towards the target, while labor market is approaching conditions synonymous with full employment. In light of these observations, maintaining the cash rate target unchanged was deemed the most suitable course of action.

The board also recognized that risks had become little more even", noting that recent data did not suggest "materialisation of upside risks to inflation" and confirmed an anticipated slowdown in economic output.

RBNZ's Orr asserts laser-focused commitment to inflation control

RBNZ Governor Adrian Orr articulated a firm stance today and emphasized that the committee is "laser-focused" on steering inflation back to its target range.

Orr's acknowledged the progress and RBNZ is "on track" getting inflation back to targets. Yet he also tempers expectations by noting that the journey is far from complete with the admission that they are "not there yet."

A critical element highlighted by Orr concerns inflation expectations, which he identifies as a significant challenge in the battle against rising He pointed out the cyclical nature of inflation expectations, stating, "the more people think inflation will rise next year, the more inflation will rise next year."

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9014; (P) 0.9036; (R1) 0.9066; More....

USD/CHF's rally resumed by breaking through 0.9070 temporary top and intraday bias is back on the upside. Current rally is in progress for 0.9243 key resistance next. On the downside, break of 0.9005 support is needed to indicate short term topping. Otherwise, outlook will stay bullish in case of retreat.

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Shop Price Index Y/Y Feb | 1.30% | 2.20% | 2.50% | |

| 23:50 | JPY | Monetary Base Y/Y Mar | 1.60% | 2.50% | 2.40% | |

| 00:00 | AUD | TD Securities Inflation M/M Mar | 0.10% | -0.10% | ||

| 00:30 | AUD | RBA Meeting Minutes | ||||

| 06:30 | CHF | Real Retail Sales Y/Y Feb | -0.20% | 0.40% | 0.30% | |

| 07:30 | CHF | Manufacturing PMI Mar | 45.2 | 44.9 | 44 | |

| 07:45 | EUR | Italy Manufacturing PMI Mar | 50.4 | 48.8 | 48.7 | |

| 07:50 | EUR | France Manufacturing PMI Mar F | 46.2 | 45.8 | 45.8 | |

| 07:55 | EUR | Germany Manufacturing PMI Mar F | 41.9 | 41.6 | 41.6 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Mar F | 46.1 | 45.7 | 45.7 | |

| 08:30 | GBP | Manufacturing PMI Mar F | 50.3 | 49.9 | 49.9 | |

| 08:30 | GBP | Mortgage Approvals Feb | 60K | 57K | 55K | |

| 08:30 | GBP | M4 Money Supply M/M Feb | 0.50% | 0.20% | -0.10% | |

| 12:00 | EUR | Germany CPI M/M Mar P | 0.40% | 0.40% | 0.40% | |

| 12:00 | EUR | Germany CPI Y/Y Mar P | 2.20% | 2.40% | 2.70% | |

| 14:00 | USD | Factory Orders M/M Feb | 1.00% | -3.60% |

Dollar Strengthens Following Positive Manufacturing Data

The EUR/USD pair has dipped to its lowest since 15 February this year following the release of encouraging data regarding the US manufacturing sector's activity on Monday. This improvement, the first since September 2022, has bolstered the US dollar's position.

The Institute for Supply Management (ISM) reported that the manufacturing business activity index climbed to 50.3 points in March from 47.8 in the preceding month. This rise above the crucial 50.0-point threshold, which distinguishes contraction from expansion, signals a positive development for the sector.

Key insights from the report highlight an increase in new orders, although manufacturing employment figures remained subdued. The surge in raw material prices also influenced the overall index, which might have otherwise recorded a higher reading. Importantly, this data signifies the end of the manufacturing sector's most prolonged downturn in 16 months, a sector that constitutes approximately 10.4% of the US economy.

Further economic data revealed that the US Core Personal Consumption Expenditure (PCE) rose by 0.3% in February, slightly below the anticipated 0.4% increase. This Core PCE index, closely monitored by the Federal Reserve, suggests that the Fed may have room to adjust interest rates downwards in June 2024, given the subdued inflationary pressures.

Market expectations for the Federal Reserve's decision in June have seen slight adjustments. CME FedWatch Tool data indicate a 66% likelihood of policy easing, a slight decrease from the prior 68% and significantly up from 57% the previous week.

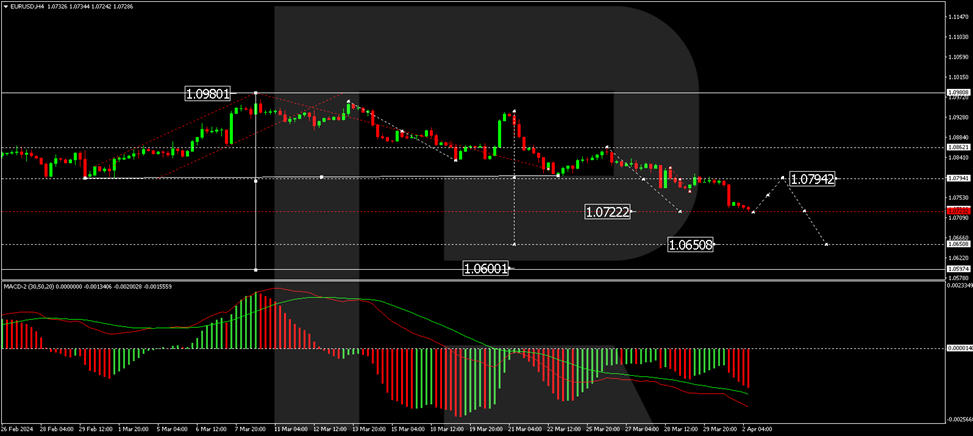

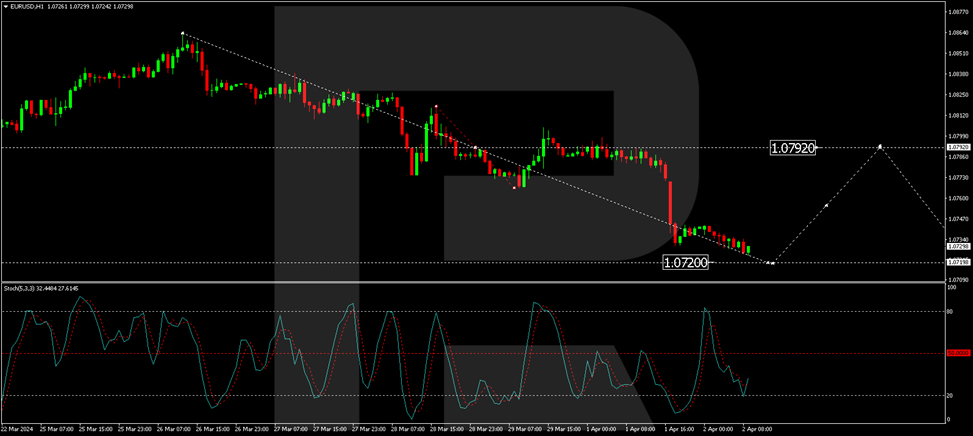

Technical analysis of EUR/USD

H4 Chart Analysis: the EUR/USD pair is currently in a consolidation phase around the 1.0794 level. A downward breakout from this range could lead to a continued decline towards 1.0650. A corrective move back to 1.0794, testing from below, may follow, with potential further descent to 1.0600. This scenario is supported by the MACD indicator, which shows the signal line below zero, indicating a continued downward trend.

H1 Chart Analysis: a corrective structure has been completed at the 1.0804 level on the H1 chart. Following the news release, the market breached the 1.0777 level downwards, continuing the downward trajectory towards 1.0720. Upon completion, a potential uptick to 1.0790 (testing from below) could occur before another drop to the 1.0650 mark. The Stochastic oscillator, currently below 50, anticipates a further decline to the 20 mark, supporting the bearish outlook.

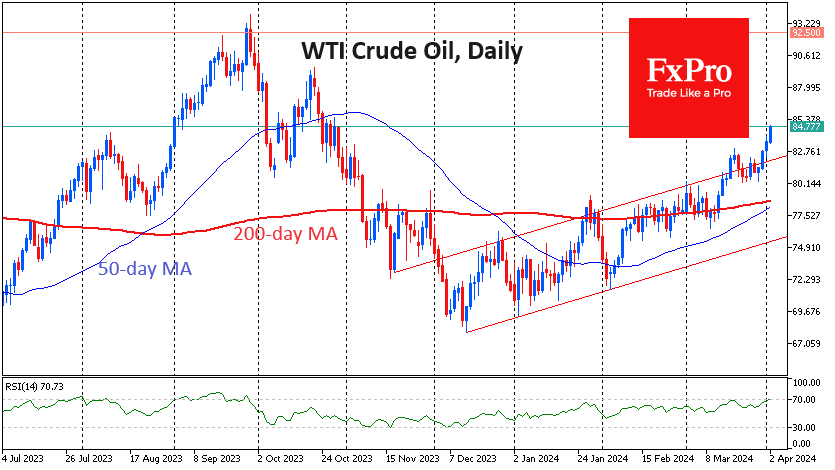

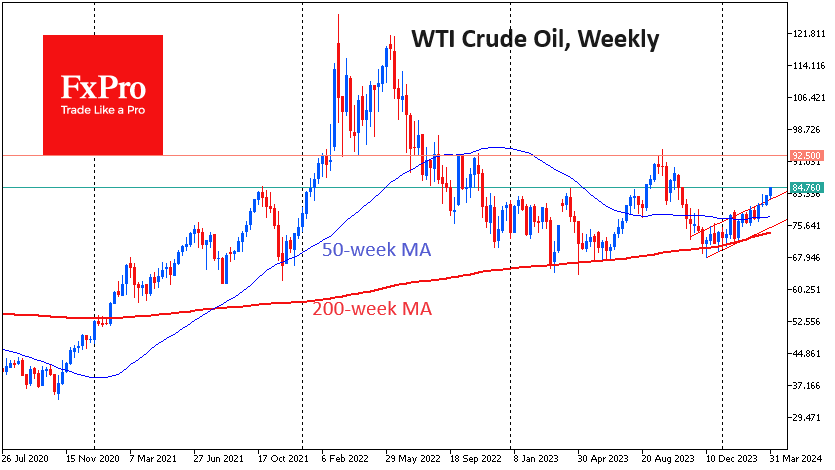

Oil Clears Way for Growth Above $90

Oil prices have been hitting five-month highs, and every trading session has been rising since 27 March. The price of a barrel of WTI reached $84.6 at the start of the day on Tuesday before retreating slightly by midday in Europe.

To some extent, oil is managing to copy gold, which has also seen a steady increase in buying since the beginning of last week. The latest rally can also be attributed to signs of acceleration in China and continued strong manufacturing data from the US, which promises energy demand.

Contrary to common logic, oil prices are rising simultaneously with the dollar despite historically having a negative correlation. But America has commonly been the largest energy importer, consuming a quarter of all Crude in the early 2000s. In recent years, however, the US has become a net Crude exporter. Last year, it reclaimed the title of largest oil producer. Recently, it became the largest exporter of LNG, a formidable competitor to the OPEC+ countries.

Meanwhile, the states have maintained production at 13.1 million bpd since October last year. Drilling activity has also stagnated for all these months, barring any supply spikes in the coming quarters.

All of this argues for further price growth and methodical, albeit small, additions to the strategic reserve.

The price chart clearly shows the acceleration in growth since the second half of March, when the previous upper boundary of the rising channel turned into support last week. We are also watching for the formation of a “golden cross”, which could attract additional speculative buying in the coming days.

From a technical point of view, the only barrier for oil is the area of previous highs at $92.5. Approaching this area may require significant profit-taking and prolonged consolidation before the next breakout, but success is by no means guaranteed.

ECB consumer survey reveals 1-yr inflation expectations drop to 3.1%, a two-year low

ECB's Consumer Expectations Survey for February indicated continuing decline in consumers' median inflation perceptions over the past 12 months, marking a fifth consecutive month of decrease, settling at 5.5% down from 6.0% in January.

Furthermore, median expectations for inflation over the next 12 months have dipped to 3.1% from 3.3%. This level is the lowest recorded since the onset of Russia's conflict with Ukraine in February 2022.

Expectations for inflation three years ahead remained stable at 2.5%.

Consolidation Not Going According to Plan

Market picture

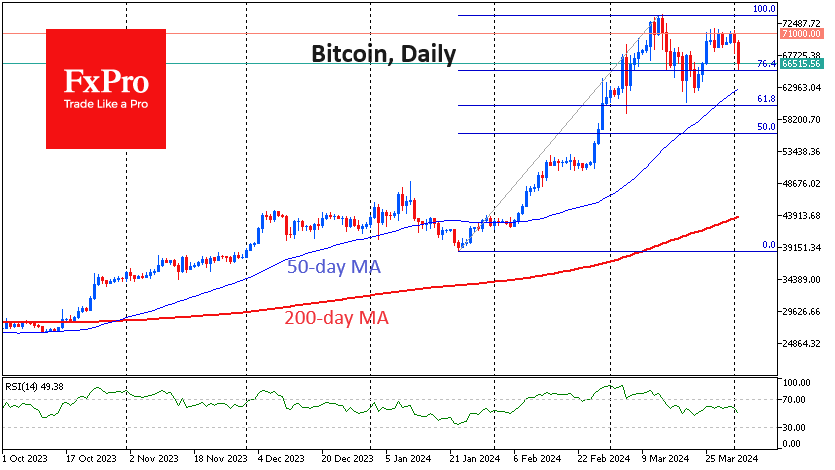

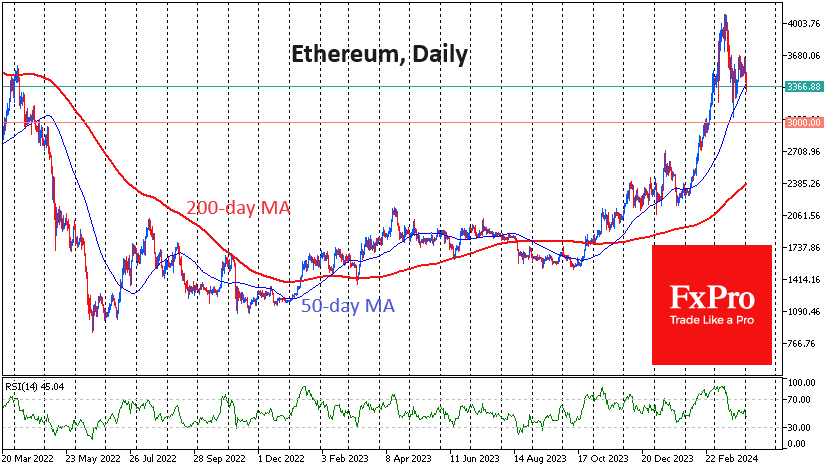

The crypto market lost 4% in 24 hours, falling to a capitalisation of $2.53 trillion. Bitcoin (-3.7%), Ethereum (-4.5%) and BNB (-3.5%) are all down by the same amount. Solana (-6.4%) and Doge (-7.9%) are lagging the market, not to mention the systematically weak Avalanche (-7% for the day and -17% for 7 days) and Cardano (-4.5% for the day and -19% for 30 days).

A promising consolidation has yet to bear fruit. For Bitcoin, the bullish chart picture has not changed: we see only an extension of the consolidation after the rally from the January lows to mid-March. The next key support area is $62.8-63.0K, where the 50-day moving average and the lows of the corrective pullback in March are centred.

Ethereum has been testing the 50-day MA since the beginning of the day, which actively played the role of support in March. It has been rising steadily since the end of last year, but too much distance from it has caused corrections on more than one occasion.

News background

According to CoinShares, investments in crypto funds rose by $862 million last week, following a record outflow of $942 million the week before. Investments in Bitcoin rose by $865 million, while those in Solana rose by $6 million, and those in Ethereum fell by $19 million. Against the backdrop of bitcoin’s recovery to $70,000, assets under management (AuM) increased from $88.2 billion to $97.9 billion, CoinShares noted.

According to Arkham Intelligence, Tether increased its bitcoin reserves by 8,888 BTC ($618 million) to 75,354 BTC ($5.23 billion), making it the seventh largest Bitcoin holder.

The Tron Foundation has filed a motion in a New York federal court to dismiss a lawsuit brought by the US SEC alleging that Tron’s crypto assets and BitTorrent are unregistered securities. Tron’s lawyers argue that the SEC’s jurisdiction does not extend to transactions that take place on global platforms outside the US.

Telegram released an update that allows owners of channels with more than 1,000 subscribers to receive 50% of ad revenue in the Toncoin (TON).

Pound Stabilizes as Shop Inflation Drops

The British pound is steady on Tuesday after starting the week with losses. In the European session, GBP/USD is trading at 1.2563, up 0.09%. On Monday, the pound fell 0.57% and dropped as low as 1.2539, its lowest level since February 14.

UK shop inflation eases to 1.3%

Inflation in UK stores fell to 1.3% y/y in March, according the British Retail Consortium (BRC). This was below the 2.5% rise in February and the market estimate of 2.2% and was the lowest level since December 2021. The BRC also reported that food price inflation fell to 3.7% y/y in March, its lowest level since April 2022. This was the 10th straight month that food prices inflation has decelerated.

The data points to headline inflation continuing to fall and has raised expectations for a rate cut from the Bank of England. The markets have priced in a quarter-point cut in June at 62%, with an outside chance of an initial quarter-point cut in May. The BoE has stuck to its script of “higher for longer”, maintaining rates at 5.25% for five straight times, but the March meeting signaled a possible shift in policy.

Governor Bailey said at the March meeting that the UK was “on the way” to winning the battle against inflation but signaled that rate cuts could be on the way. As well, eight MPC members voted to pause and one voted to lower rates at the March meeting, while at the previous meeting, two members voted in favor of a rate hike. The UK releases the March inflation report on April 16th and this release will likely have a significant impact on the BoE’s rate path.

GBP/USD Technical

- GBP/USD is testing support at 1.2605. Below, there is support at 1.2552

- There is resistance at 1.2704 and 1.2757