Sample Category Title

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0716; (P) 1.0758; (R1) 1.0784; More...

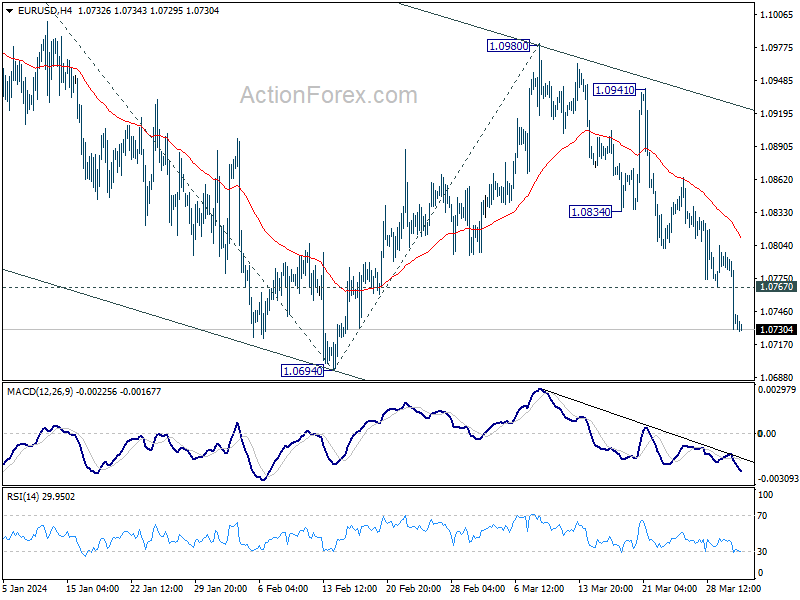

Intraday bias in EUR/USD stays on the downside for 1.0694 support. Decisive break there will resume the whole decline from 1.1138 and target 100% projection of 1.1138 to 1.0694 from 1.0980 at 1.0536. On the upside, above 1.0767 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.0834 support turned resistance holds, in case of recovery.

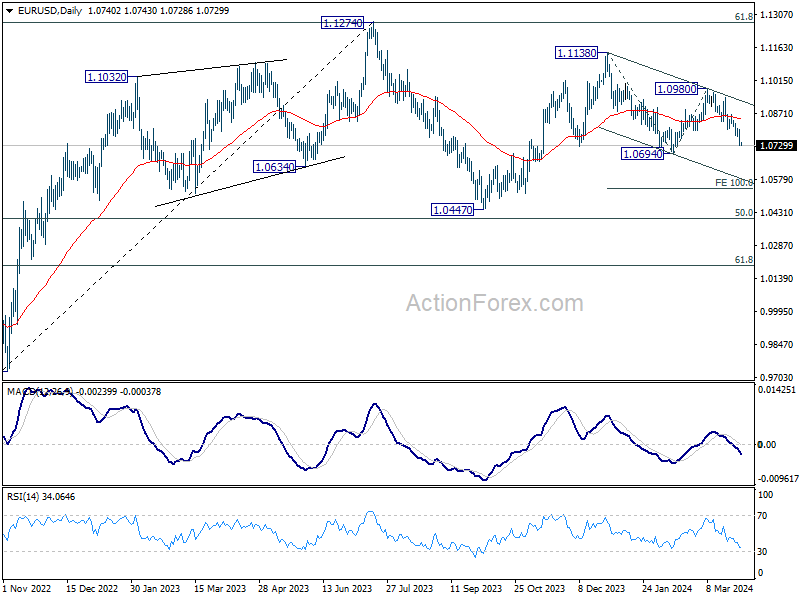

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

Dollar Strength Persists as Markets Await Fed Speakers

Dollar stayed broadly firm in Asian session today, after rallying on robust manufacturing data and significant rebound in treasury yields overnight. The spotlight now shifts to upcoming comments from Fed officials, including Governor Michelle Bowman and New York Fed President John Williams, as markets seek clues about the central bank's monetary easing path.

The burning question for investors and analysts alike revolves around Fed's readiness to initiate interest rate cuts in June, and whether three cuts will be delivered this year. The forthcoming remarks from Fed officials are expected to offer a glimpse into the current hawk-dove dynamic within the central bank, with additional guidance likely to emerge from the ISM services data and Non-Farm Payroll reports slated for later in the week.

In the broader forex market, Sterling is currently the weakest performer so far this week, trailed by Kiwi and Euro. On the other hand, Canadian Dollar and Japanese Yen have shown relative resilience, while Australian Dollar and Swiss Franc are mixed in the middle.

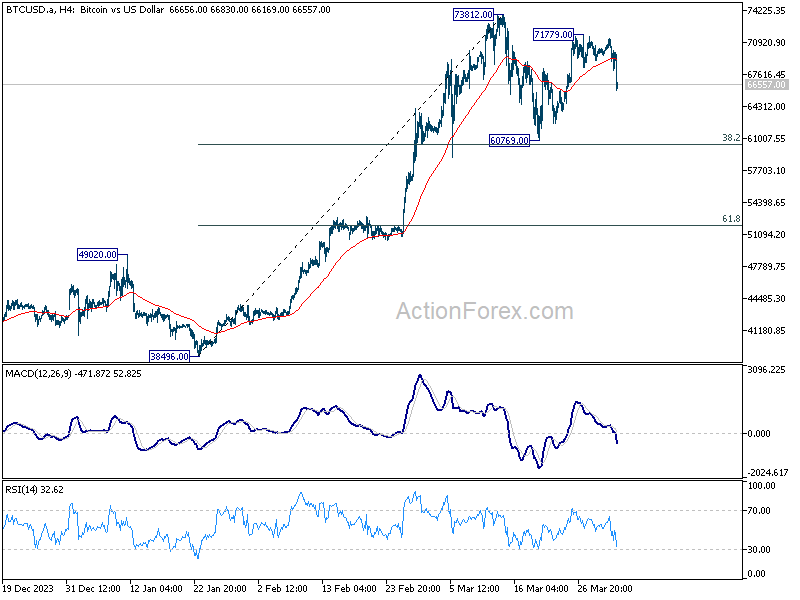

On the technical front, Bitcoin has experienced a sharp decline, indicating that the recent rebound from 60,769 may have reached its peak at 71,779. This suggests that the corrective pattern from 73,812 is entering its third leg, with a deeper fall anticipated back to 60,769. However, significant support is expected around the 38.2% retracement of 38,496 to 73,812 at 60,321, potentially marking the completion of the pattern. Consequently, a firm breach below the 60k threshold appears unlikely at this juncture. In essence, a firm breach of the 60k threshold seems unlikely at this juncture.

In Asia, at the time of writing, Nikkei is up 0.03%. Hong Kong HSI is up 2.25%. China Shanghai SSE is down -0.16%. Singapore Strait Times is up 0.30%. Japan 10-year JGB yield is up 0.0027 at 0.745. Overnight, DOW fell -0.60%. S&P 500 fell -0.20%. NASDAQ rose 0.11%. 10-year yield rose 0.123 to 4.329.

RBA minutes: No rate hike discussed, focus on preserving labor market gains

RBA's minutes from March 18-19 meeting revealed no explicit discussion on rate hikes, marking a departure from previous communications that outlined the board's considered options.

The board assessed that it would require more time to gain "sufficient confidence" in inflation's return to target range within a foreseeable timeframe. At the same time, it emphasized on the priority to "preserve as many of the gains in the labor market as possible."

These considerations led to the characterization of the policy outlook as ambiguous, with the board finding it "difficult to either rule in or out future changes" in the cash rate target.

Inflation remains elevated, albeit on a gradual decline towards the target, while labor market is approaching conditions synonymous with full employment. In light of these observations, maintaining the cash rate target unchanged was deemed the most suitable course of action.

The board also recognized that risks had become little more even", noting that recent data did not suggest "materialisation of upside risks to inflation" and confirmed an anticipated slowdown in economic output.

RBNZ's Orr asserts laser-focused commitment to inflation control

RBNZ Governor Adrian Orr articulated a firm stance today and emphasized that the committee is "laser-focused" on steering inflation back to its target range.

Orr's acknowledged the progress and RBNZ is "on track" getting inflation back to targets. Yet he also tempers expectations by noting that the journey is far from complete with the admission that they are "not there yet."

A critical element highlighted by Orr concerns inflation expectations, which he identifies as a significant challenge in the battle against rising He pointed out the cyclical nature of inflation expectations, stating, "the more people think inflation will rise next year, the more inflation will rise next year."

Looking ahead

Swiss retail sales and PMI manufacturing; Eurozone PMI manufacturing final; UK PMI manufacturing final, and Germany CPI flash will be released in Euroepan session. Later in the day, US will release factory orders.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0716; (P) 1.0758; (R1) 1.0784; More...

Intraday bias in EUR/USD stays on the downside for 1.0694 support. Decisive break there will resume the whole decline from 1.1138 and target 100% projection of 1.1138 to 1.0694 from 1.0980 at 1.0536. On the upside, above 1.0767 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.0834 support turned resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Shop Price Index Y/Y Feb | 1.30% | 2.20% | 2.50% | |

| 23:50 | JPY | Monetary Base Y/Y Mar | 1.60% | 2.50% | 2.40% | |

| 00:00 | AUD | TD Securities Inflation M/M Mar | 0.10% | -0.10% | ||

| 00:30 | AUD | RBA Meeting Minutes | ||||

| 06:30 | CHF | Real Retail Sales Y/Y Feb | 0.40% | 0.30% | ||

| 07:30 | CHF | Manufacturing PMI Mar | 44.9 | 44 | ||

| 07:45 | EUR | Italy Manufacturing PMI Mar | 48.8 | 48.7 | ||

| 07:50 | EUR | France Manufacturing PMI Mar F | 45.8 | 45.8 | ||

| 07:55 | EUR | Germany Manufacturing PMI Mar F | 41.6 | 41.6 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Mar F | 45.7 | 45.7 | ||

| 08:30 | GBP | Mortgage Approvals Feb | 57K | 55K | ||

| 08:30 | GBP | M4 Money Supply M/M Feb | 0.20% | -0.10% | ||

| 08:30 | GBP | Manufacturing PMI Mar F | 49.9 | 49.9 | ||

| 12:00 | EUR | Germany CPI M/M Mar P | 0.40% | 0.40% | ||

| 12:00 | EUR | Germany CPI Y/Y Mar P | 2.40% | 2.70% | ||

| 14:00 | USD | Factory Orders M/M Feb | 1.00% | -3.60% |

Goldilocks at Chifley Square

The current level of the cash rate is assessed as being just right for the time being, but things could change. The Board also picks a happy medium as the future model for implementing policy.

The minutes of the late-March meeting of the RBA Board (the last in the Martin Place building) recorded that the data had turned out broadly as expected, and that this supported keeping the cash rate on hold. Unlike the February minutes, there was no mention of multiple policy options. While the Board endorsed the language of not ruling anything in or out, it seems that policy actions other than keeping rates unchanged were not on the table at this meeting. The current level of the cash rate is assessed as being just right, at least for the time being.

The minutes noted that the staff assessed that demand still exceeded supply, but the gap was diminishing quickly. A slowing in labour demand was called out, and growth in labour costs was assessed to have peaked. The Board nonetheless remains concerned that domestic costs could continue to rise quickly. The recent turnaround in productivity was noted, as was the role of the pandemic and economic cycle in driving the recent slump. However, the Board is uncertain whether this turnaround will continue. The possibility of a faster snapback in productivity than expected was not mentioned.

The ongoing decline in inflation was highlighted, with the three-month-ended rate for the monthly indicator used as a timelier metric. Monthly inflation was expected to rebound in coming months as special factors such as electricity rebates unwind. The pace of decline in goods prices was also expected to slow, though the minutes did not elaborate on the reasoning for this view. The minutes highlighted the bumpiness of the decline in inflation in other countries and noted that something similar could happen in Australia.

Policy was still assessed as restrictive, so at some point the policy rate will need to decline to prevent inflation from declining so far that it starts undershooting the target. But unlike its peers overseas, the Board is not ready to talk about this decision yet. The minutes again highlighted that interest rates had peaked at a lower level than in some peer economies, and that this reflected the Board’s intention to preserve the gains on employment made since the pandemic period. A related difference that the minutes did not highlight is the varying squeeze on household sectors across peer economies. Debt-servicing as a share of household income is well above average in Australia at present. By contrast, the financial stability section of the minutes noted that it is below historical averages in many peer economies – despite higher policy rates.

The global outlook was seen as supporting risk sentiment. The chance of a significant downturn had fallen, while interest rates were still expected to decline later in the year. This combination is seen as boosting prices of risk assets and contributing to a more ‘risk on’ tone in markets. This has also been supportive of the Australian dollar exchange rate despite narrower interest differentials and a decline in key commodity prices. Improved risk sentiment also underpins Westpac Economics’ expectation of further upward pressure on the AUD/USD exchange rate later this year; the declines in commodity prices were largely expected and so already priced in.

We expect the RBA to reach the required level of assurance about the path of inflation later in the year, after the full suite of data for the first half of 2024 are released. We continue to expect the first rate cut to occur at the late-September Board meeting.

Ample considerations of a happy medium

The other main decision recorded in the minutes related to the operational arrangements for monetary policy. This decision was further elaborated in a speech this morning by Assistant Governor (Financial Markets) Chris Kent.

The background to this decision is that the policy interest rate that the RBA focuses on is the interest rate that banks (and other deposit-taking institutions) charge each other to borrow unsecured overnight in the cash market. The asset that is being borrowed and repaid is exchange settlement funds – that is, banks’ deposits with the RBA, also known as reserves. These deposits are remunerated at a rate that is set below the policy target rate; currently, the spread is 10 basis points.

Prior to the pandemic, the RBA ran a ‘scarce reserves’ regime. Its balance sheet was small, and the staff needed to forecast daily liquidity flows into and out of the system – for example from tax payments and government spending – to keep the amount of reserves at whatever level would keep the cash rate at target. When the pandemic hit, banks wanted more liquidity, so the RBA switched to a regime of excess reserves. This was also a by-product of the various asset purchase programs introduced during that period. The RBA’s balance sheet expanded, and the actual interest rate banks transacted at in the cash market drifted below the published cash rate target, while remaining above the remuneration rate on exchange settlement balances.

Other central banks, including the Federal Reserve, Bank of Canada and RBNZ, have decided to stick with the excess reserves model even as they wind down their asset purchase programs. Others, including the Bank of England and European Central Bank, have instead settled on a happy medium of ‘ample’, but not excess, reserves. A key distinction between this operating model and its alternatives is that it is managed with full-allotment repo at a pre-specified interest rate, which fixes the price (interest rate) and accepts whatever quantity of reserves is needed to achieve this. By contrast, in both the ‘scarce’ and ‘excess’ reserve regimes, it is up to the central bank to determine the quantity of reserves that it thinks will achieve the desired price. Still to be determined is the composition of assets the RBA will hold under repurchase agreements on the other side of its balance sheet.

As both the speech and minutes emphasise, this is an operational decision with no implications for the stance of monetary policy. Relative to reverting to the pre-pandemic scarce-reserves regime, though, the RBA’s balance sheet will be larger, with implications for the average size of future earnings to be distributed to the government. It will also mean that the RBA continues to hold some fraction of the government bonds on issue. These will not be available to banks and other deposit takers to meet their prudential liquidity requirements (the Liquidity Coverage Ratio).

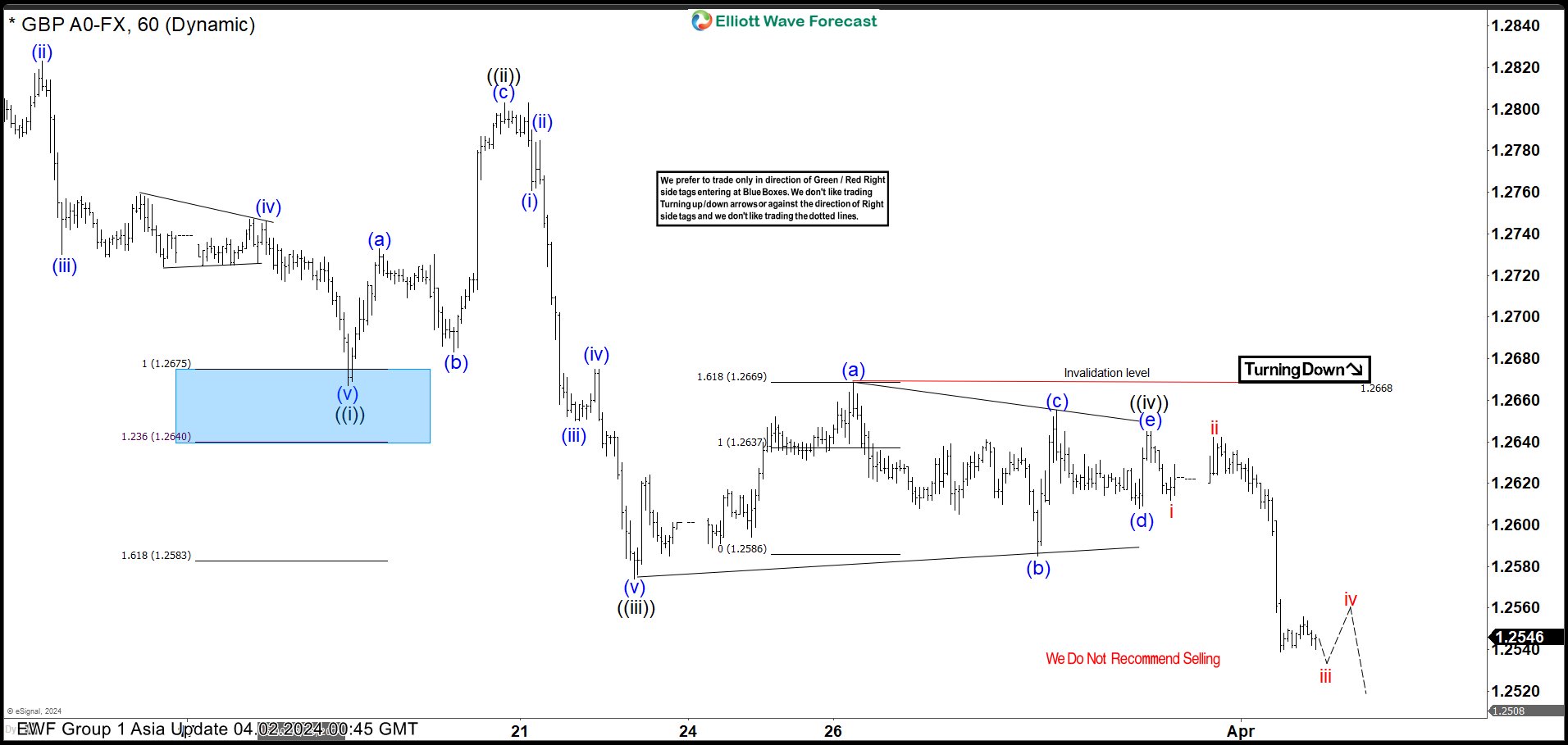

GBPUSD May See Support Soon From Inflection Area

Short Term Elliott Wave view in GBPUSD suggests that decline from 3.8.2024 high is unfolding s an impulse Elliott Wave structure. Down from 3.8.2024 high, wave (i) ended at 1.2745 and wave (ii) rally ended at 1.2823. Wave (iii) lower ended at 1.273 and wave (iv) ended at 1.2747. Final leg wave (v) ended at 1.2667 which completed wave ((i)). From there, pair rallied as a zigzag. Wave (a) ended at 1.2733 and wave (b) ended at 1.268. Wave (c) higher ended at 1.28 which completed wave ((ii)). Pair then resumed lower in wave ((iii)).

Down from wave ((ii)), wave (i) ended at 1.276 and wave (ii) ended at 1.278. Wave (iii) lower ended at 1.265, wave (iv) ended at 1.267 and wave (v) ended at 1.257. This completed wave ((iii)) in higher degree. Wave ((iv)) unfolded as a triangle and ended at 1.2645. Pair resumed lower afterwards. Down from wave ((iv)), wave i ended at 1.261 and wave ii ended at 1.264. Expect pair to extend two more lows to end wave (i) of ((v)). As far as pivot at 1.267 high stays intact, expect rally to fail in 3, 7, 11 swing for further downside.

GBPUSD 60 Minutes Elliott Wave Chart

GBPUSD Elliott Wave Video

https://www.youtube.com/watch?v=rU2choX_x94

RBNZ’s Orr asserts laser-focused commitment to inflation control

RBNZ Governor Adrian Orr articulated a firm stance today and emphasized that the committee is "laser-focused" on steering inflation back to its target range.

Orr's acknowledged the progress and RBNZ is "on track" getting inflation back to targets. Yet he also tempers expectations by noting that the journey is far from complete with the admission that they are "not there yet."

A critical element highlighted by Orr concerns inflation expectations, which he identifies as a significant challenge in the battle against rising He pointed out the cyclical nature of inflation expectations, stating, "the more people think inflation will rise next year, the more inflation will rise next year."

RBA minutes: No rate hike discussed, focus on preserving labor market gains

RBA's minutes from March 18-19 meeting revealed no explicit discussion on rate hikes, marking a departure from previous communications that outlined the board's considered options.

The board assessed that it would require more time to gain "sufficient confidence" in inflation's return to target range within a foreseeable timeframe. At the same time, it emphasized on the priority to "preserve as many of the gains in the labor market as possible."

These considerations led to the characterization of the policy outlook as ambiguous, with the board finding it "difficult to either rule in or out future changes" in the cash rate target.

Inflation remains elevated, albeit on a gradual decline towards the target, while labor market is approaching conditions synonymous with full employment. In light of these observations, maintaining the cash rate target unchanged was deemed the most suitable course of action.

The board also recognized that risks had become little more even", noting that recent data did not suggest "materialisation of upside risks to inflation" and confirmed an anticipated slowdown in economic output.

(RBA) Minutes of the Monetary Policy Meeting of the Reserve Bank Board

Sydney – 18 and 19 March 2024

Members present

Michele Bullock (Governor and Chair), Andrew Hauser (Deputy Governor), Ian Harper AO, Carolyn Hewson AO, Steven Kennedy PSM, Iain Ross AO, Elana Rubin AM, Carol Schwartz AO, Alison Watkins AM

Others present

Brad Jones (Assistant Governor, Financial System), Sarah Hunter (Assistant Governor, Economic), Christopher Kent (Assistant Governor, Financial Markets), Carl Schwartz (Acting Head, Domestic Markets Department)

Anthony Dickman (Secretary), David Norman (Deputy Secretary)

Andrea Brischetto (Head, Financial Stability Department), Marion Kohler (Head, Economic Analysis Department), Sally Cray (Chief Communications Officer), Meredith Beechey Osterholm (Future Hub)

Domestic economic conditions

Members commenced their discussion of domestic economic conditions by assessing the recent data on output growth. They noted that growth had slowed further in the December quarter, largely as expected. Aggregate demand had been supported over 2023 by strong growth in business investment and public spending, and members considered how likely it was this would continue in 2024. Members also noted, however, that household consumption growth had been very weak and negative in per capita terms, as high inflation and increases in interest rates and tax payments had weighed on real incomes. They observed that real household disposable income had begun to grow again and was projected to pick up further as the drag from high inflation abated and pre-announced tax cuts took effect. Members discussed a range of factors that could influence the likelihood that consumption growth would pick up in response.

Members observed that growth in underlying demand for housing remained brisk relative to supply, which was contributing to rising prices and rents. On the demand side, population growth remained high and the shift in preferences for more housing space that occurred during the pandemic was yet to unwind, despite worsening affordability. On the supply side, new housing had been constrained by ongoing capacity constraints – particularly for finishing trades and where the required skills were easily transferable to non-residential construction – and rapid increases in construction costs. Advertised rents had continued to grow strongly in most capital cities.

Members noted the staff's overall assessment that aggregate demand had continued to exceed supply in the latter part of 2023, but that the gap between the two was closing relatively quickly, in line with prior forecasts.

Labour market conditions had eased further, as slower output growth had resulted in slowing growth in labour demand. This was evident across a range of labour market indicators, including a further rise in the unemployment rate in January. Members assessed that overall labour market conditions nevertheless remained a little tighter than was consistent with sustained full employment and inflation at target.

Wages growth had been robust in the December quarter. Both the data and liaison signalled that wages growth may have reached a peak, with some jobs and industries already seeing an easing in wage pressures. That said, overall wages growth was not expected to decline quickly.

Growth in labour costs per unit of output remained very high. It had begun to moderate slightly as measured productivity growth had picked up in the second half of 2023, but members noted that it was still uncertain whether this trend would be sustained. They observed that much of the prior weakness in labour productivity had reflected the effects of the pandemic and the economic cycle, which were likely to unwind over coming years. However, it was also possible that the structural factors adversely affecting productivity growth in the years prior to the pandemic would persist. Members noted that the current level of wages growth remained consistent with the inflation target, but only on the assumption that productivity growth increased to around its long-run average. They considered the implications for monetary policy if productivity did not pick up as assumed, recognising that the associated economic adjustment may not be smooth or immediate.

Underlying inflation had continued to moderate, largely in line with the staff's forecasts published in February, but it was still high. The monthly CPI indicator excluding volatile items was around 4 per cent in year-ended terms in January, and had declined below 3 per cent on a three-month-ended annualised basis. However, a rebound was anticipated in coming quarters as recent declines in fuel prices and the pace of decline of some household goods prices were not expected to persist and electricity rebates were legislated to expire. Members noted that the data were consistent with continuing, but diminishing, excess demand and strong domestic cost pressures, for both labour and non-labour inputs.

International economic developments

Turning to economic conditions abroad, members observed that inflation had been moderating in many advanced economies, and recent readings were now closer to central banks' targets. However, inflation remained uneven across components: energy and goods prices inflation had eased, but housing and core services inflation remained high compared with pre-pandemic rates. And some countries, notably the United States, had seen a modest pick-up in inflation in the most recent data. Members noted the risk that non-tradables inflationary pressures could persist in these economies.

Restrictive monetary policy settings had played a part in slowing global output growth, though the risk of significant recession had diminished in major economies over the preceding year. Members observed that activity in the United States had been more resilient than elsewhere. Labour market conditions in major economies had also generally eased a little further but remained tight.

The Chinese authorities had announced a target for growth of 'around 5 per cent' for 2024, despite ongoing headwinds to growth. At the same time, additional fiscal policy support had been announced. Members noted that concerns about the outlook for steel demand had weighed on iron ore prices, which was reducing incomes for Australian exporters.

Financial conditions

Market participants' expectations for the paths of central bank policy rates in advanced economies had risen a little since the previous meeting. This reflected some stronger-than-expected economic data and statements by central bank officials that emphasised the need for further evidence that inflation would sustainably return to targets before central banks started reducing policy rates. Market participants continued to expect that many advanced economy central banks would begin reducing policy rates from around the middle of the year. Members observed that Japan was an exception, with market pricing implying an expectation that the Bank of Japan would end its policy of negative interest rates at an upcoming meeting.

Members noted that fewer reductions in the policy rate were expected in Australia than in many other advanced economies. They observed that, in part, this was likely because the cash rate had not risen as high as policy rates in other economies, as the Board had chosen to return inflation to target gradually over time in order to preserve the gains in employment. Members further observed that market expectations were for policy rates to be at broadly similar levels by the end of 2025 across many advanced economies, including Australia.

Sovereign bond yields in advanced economies, including Australia, had been little changed since the previous meeting, while the prices of riskier assets had continued to rise. Equity prices had reached new highs, reflecting stronger-than-expected company earnings and a rise in expected future earnings, as well as declines in risk premia as market participants became more confident that economic growth across a range of countries could be maintained while inflation moderates. Corporate bond spreads had also declined to around their lowest levels since 2022, while corporate bond issuance had picked up in preceding months.

In China, monetary policy had been eased further to support the economy in the face of significant economic headwinds, particularly stresses in the property sector. Members noted that monetary policy easing had been moderate, with more substantive support for the economy having been delivered through fiscal policy. Chinese equity prices had picked up from recent lows following the increased support from authorities.

The Australian dollar had been little changed since the previous meeting, despite a noticeable decline in iron ore prices and a modest decline in the yield differential between Australia and other advanced economies. Members observed that the exchange rate appeared to have been supported by favourable global risk sentiment, noting the historical correlation between the Australian dollar and the price of riskier assets.

Overall financial conditions in Australia were considered to have remained restrictive, particularly for households. The tightening in monetary policy had induced a significant rise in scheduled household debt payments. These were expected to rise a little further in 2024 as additional fixed-rate loans rolled onto higher rates. Housing credit growth remained low and payments into offset accounts had risen since mid-2023. Lower income and less-wealthy households had been most affected. As a result, the average housing deposit had increased at a faster rate than housing prices, and newer borrowers had higher incomes and lower loan-to-income ratios relative to earlier cohorts.

Financial conditions for the business sector, including in wholesale funding markets, had remained more favourable than for households. While interest expenses had increased for businesses, this had been partly buffered by higher nominal earnings. Business credit growth had remained reasonably strong.

Future system for monetary policy implementation

Members discussed a paper on options for the future system that the Bank could use to implement monetary policy. They agreed that it was important to plan for this given the decline in Exchange Settlement (ES) balances ('reserves') as unconventional monetary policies are unwound. Three broad options for the system to control the cash rate were considered: return to a 'corridor system' with scarce reserves (similar to that in operation prior to the pandemic); maintain the current 'floor system' with excess reserves (adopted during the pandemic); or transition to a system where the Bank would provide 'ample reserves' by meeting demand for ES balances from banks at a pre-set price close to the cash rate target, using full-allotment auctions.

Members agreed that each of these options could meet the Bank's primary objective of ensuring that the cash rate and other short-term market interest rates remain close to the Board's cash rate target. However, members assessed that provision of ample reserves through full-allotment auctions was likely to be the best option to move towards. Under this option, the framework would be more resilient to changes affecting the demand and supply of reserves than would be the case in a scarce reserves system, reducing the risk of unexpected liquidity shortages, among other matters. Members also considered that this would help limit the Bank's financial risk and would imply a lower risk of distortions in market prices or impairments in market functioning, compared with an excess reserves system. The Bank's existing operational arrangements are consistent with a transition to ample reserves because current open market operations already include full-allotment auctions. Members discussed the importance of establishing this system in a way that clearly separates liquidity provision for ordinary payments needs or system-wide shifts in liquidity needs from liquidity provision to banks facing idiosyncratic liquidity stress. Members stressed the importance of ES holders – in particular, banks – reflecting on the implications of the prospective framework for their own liquidity management operations as the stock of reserves declines.

Members endorsed a proposal to adopt an ample reserves system with full-allotment auctions. They emphasised that, as this decision was an operational one, it had no implications for the stance of monetary policy, nor did it have a bearing on the Board's current approach to bond holdings acquired during the pandemic. Consistent with these considerations, members agreed that it was appropriate for information on the broad shape of the new framework to be communicated to the public through a speech by the Assistant Governor, Financial Markets. Key details of the ample reserves system would need to be considered later in the year, including the configuration of the full-allotment open market operations and guidelines for the composition of the assets on the Bank's balance sheet. These decisions would be informed by the staff's future engagement with stakeholders, including via public consultation.

Financial stability assessment

Members discussed the Bank's regular half-yearly assessment of financial stability risks. They observed that pressures from high inflation and the sharp tightening in monetary policy had weighed on the financial position of many households and businesses globally. Nonetheless, the global financial system had proved largely resilient to date. Members noted that one reason for this was generally strong household and corporate balance sheets, following sustained deleveraging over the prior decade or so in major advanced economies that had been particularly affected by the global financial crisis. Private sector borrowing at low fixed rates in these economies had also dampened some of the pass-through from higher policy rates and, along with continued strength in labour markets, had contributed to debt-servicing ratios remaining at the lower end of historical ranges. Members noted that stronger lending standards and prudential regulation following the global financial crisis had also led to improvements in large international banks' capital positions, leaving them well placed to weather a decline in asset quality and/or worsening macroeconomic conditions.

Nonetheless, global financial stability risks remained high, and members discussed several that were particularly relevant for Australia:

- Further weakness in the Chinese property sector could interact with longstanding macro-financial vulnerabilities. If stresses in the Chinese economy and financial system intensified or broadened, they could spill over to the rest of the world (including Australia) through trade channels and an increase in global risk aversion.

- Higher interest rates and ongoing weak demand, particularly for older or lower quality offices, continued to weigh on conditions in global commercial real estate (CRE) markets. Risks were greater among regional banks in the United States and parts of Europe, including in Germany, where CRE exposures were largest and lending standards had eased over prior years. While distressed CRE sales and non-performing loans in international markets had been limited, they could increase in the period ahead as CRE loans had to be refinanced at higher rates in a weaker demand environment.

- Declining risk premia in debt and equity markets in part reflected market participants' current optimism about the prospects for a soft landing in the global economy. Worse-than-expected macroeconomic outcomes – for example, arising from global inflation proving more persistent than expected or a geopolitical shock – could result in a disorderly adjustment in financial asset prices. Events in recent years had demonstrated the potential for this adjustment to be amplified by vulnerabilities in non-bank financial intermediaries in key global financial centres. Tight market spreads, if they persisted over an extended period, could contribute to a build-up of leverage and future risks to financial stability.

Turning to domestic financial stability considerations, members noted that most Australian households remained able to service their debts and meet essential expenses, and this was expected to remain true even if inflation were to prove more persistent than anticipated. Strong conditions in the labour market and the large savings buffers accumulated during the pandemic were helping households adapt to challenging economic conditions and restrictive monetary policy. Many borrowers, including those on lower incomes, had also increased the savings they held in offset and redraw facilities over the preceding year; some were likely to have reduced consumption in order to facilitate this. Members recognised that a small group of borrowers, typically those with modest savings or income buffers, remained under acute financial pressure owing to the effects of high inflation and higher interest rates. However, members observed these developments were more relevant to the near-term outlook for consumption than financial stability.

Members discussed the uneven conditions experienced across the business sector. They observed that the strong financial starting position of many businesses was supporting their resilience in the face of a slowing economy. Profit margins of many businesses were around pre-pandemic levels, balance sheets remained strong and arrears on bank loans to businesses were low. Company insolvencies had risen to pre-pandemic levels, although this had been driven largely by smaller businesses, particularly in construction as well as discretionary sectors, which tended to have only modest bank debt. This limited the direct risks to financial stability in Australia.

Members noted that banks expected overall loan arrears to pick up further in the period ahead, but to remain low relative to history. This reflected most Australian households' and businesses' strong financial starting positions, resilient labour market conditions and sound lending standards in recent years. Banks' high capital levels, profitability and provisions left them well placed to absorb a deterioration in credit quality in the event of worse-than-expected macroeconomic conditions.

Lending by Australian non-banks had picked up recently as funding conditions had improved in the securitisation market, and there had been some loosening of lending standards. However, members agreed that risks to financial stability posed by Australian non-bank lenders remained relatively contained, given their small share of overall credit.

Despite challenging conditions in the domestic CRE market, there was little evidence to date of financial stress among owners of Australian CRE. Members noted that the limited size and more conservative nature of CRE bank lending in Australia, compared with past cycles, meant the risks to the banking system were lower than in previous downturns. However, the risk of CRE stresses overseas affecting the Australian market had risen over the prior decade with the increase in foreign participation in Australia's CRE market.

Finally, members noted the importance of strengthening financial institutions' operational resilience to threats emanating from outside the financial system. If realised, such threats could have material economic and financial stability consequences. Cyber-attacks and the potential for a further escalation in geopolitical tensions were particularly relevant in this context. Strengthening financial institutions' operational resilience to these threats is therefore an ongoing area of focus for the Bank and other member agencies of the Council of Financial Regulators.

Considerations for monetary policy

Turning to the policy decision, members noted that the economic data over preceding weeks had been broadly as expected. GDP growth had been below both its historical trend and growth in the population. Consumption had been persistently weak, but this had been partly offset by considerable strength in business investment and above-average growth in public demand. While these outcomes implied the output gap was closing relatively quickly, as anticipated, members noted the staff's assessment that aggregate demand still exceeded supply and would be likely to continue to do so for a time. Consistent with this, labour market tightness had abated somewhat, though the pace at which this was occurring had been clouded by shifting seasonal patterns.

Members observed that inflation had continued to moderate over prior months, broadly as expected. That said, services inflation remained high and the recent slowing in the pace of monthly inflation had been influenced by several temporary factors. Members observed that the path of disinflation in other countries had not been smooth, which could hold lessons for Australia. Furthermore, while recent data suggested wages growth had peaked, growth in labour costs per unit of output remained strong, even as productivity growth had begun to recover.

Members observed that financial conditions in Australia had been little changed overall since the previous meeting. Financial conditions for households remained restrictive, though financial conditions for businesses had eased a little over prior months. Some households were finding it difficult to service their debts and meet essential expenses. However, rates of arrears on housing loans were still low and banks had recently reduced their forecasts of potential loan losses. Risks to the financial system from lending to households and businesses remained contained.

In light of these assessments, members agreed that it was appropriate to leave the cash rate target unchanged at this meeting. They agreed that the data received since the previous meeting had been broadly as expected and did not materially alter the outlook for output growth and inflation. In particular, members noted that the data had continued to indicate that inflation was high but gradually returning to target, and that the labour market was moving towards conditions consistent with full employment. Members agreed that leaving the cash rate target unchanged at this meeting was the best way to achieve the Board's strategy of supporting a gradual return of inflation to target and the labour market to full employment.

Members debated the balance of risks around the outlook. On the upside, there remained a risk that inflation would take longer to return to target than currently expected, resulting in an upward shift in inflation expectations. Members observed that this could occur if aggregate demand continued to exceed supply for longer than anticipated, productivity growth did not increase sustainably or if services price inflation proved stickier than assumed in the forecasts. On the other hand, members noted the risk that weakness in consumption could continue for longer than expected. In particular, the recovery in real household disposable income growth may not lift consumption growth if households do not respond as expected, perhaps because of a weakening in the labour market. If that occurred, growth in output would be slower than expected and inflation would be likely to decline more quickly. On balance, members considered that the relative probability of these two sets of risks had become a little more even, as the incoming data had not indicated a materialisation of upside risks to inflation and as growth in output had slowed as expected.

Members agreed that returning inflation to target remained the Board's highest priority and that it would take some time before they could have sufficient confidence that this would occur within a reasonable timeframe. At the same time, members noted the importance of preserving as many of the gains in the labour market as possible. In light of this and their assessment of the economy, members agreed that it was appropriate to characterise the policy outlook as one in which it was difficult to either rule in or out future changes in the cash rate target. Members remain committed to paying close attention to developments in the global economy, trends in domestic demand, and the outlook for inflation and the labour market.

In finalising the Board's statement, members agreed that it was important to convey that recent data and information had not materially changed their views on the outlook. They decided to emphasise that the data indicated the economy was tracking broadly as expected and that while there were significant uncertainties, the risks seemed broadly balanced. Members agreed that it was therefore not possible to either rule in or out future changes in the cash rate target. They agreed to reiterate their resolve to do what is necessary to return inflation to target.

The decision

The Board decided to leave the cash rate target unchanged at 4.35 per cent, and the interest rate on Exchange Settlement balances unchanged at 4.25 per cent.

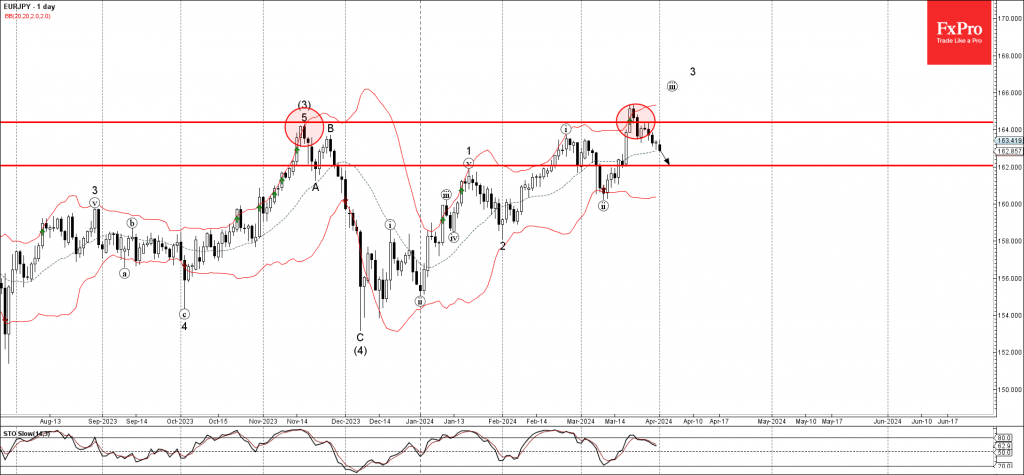

EURJPY Wave Analysis

- EURJPY reversed from resistance level 164.30

- Likely to fall to support level 162.00

EURJPY currency pair recently reversed down from the resistance level 164.30, former multi month high from the middle of November.

The resistance level 164.30 was strengthened by the upper daily Bollinger Band.

EURJPY currency pair can be expected to fall further to the next support level 162.00, former minor support from March.

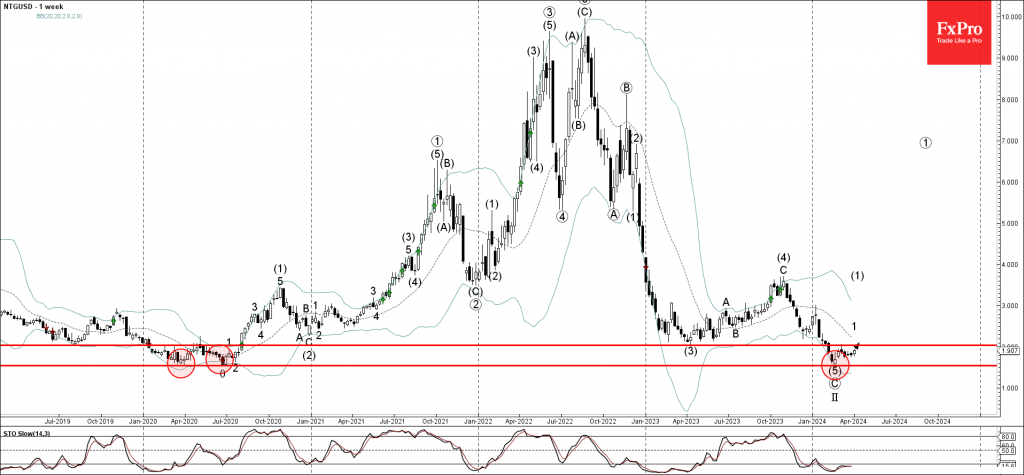

Natural Gas Wave Analysis

- Natural gas reversed from multi-month support level 1.541

- Likely to rise to resistance level 2.030

Natural gas recently reversed up from the multi-month support level 1.541, which reversed the price twice in the middle of 2020.

The support level 1.541 was strengthened by the lower weekly and the daily Bollinger Bands.

Given the strength of the support level 1.541 and the oversold weekly Stochastic, Natural gas can be expected to rise further to the next resistance level 2.030, former yearly low from last year.