Sample Category Title

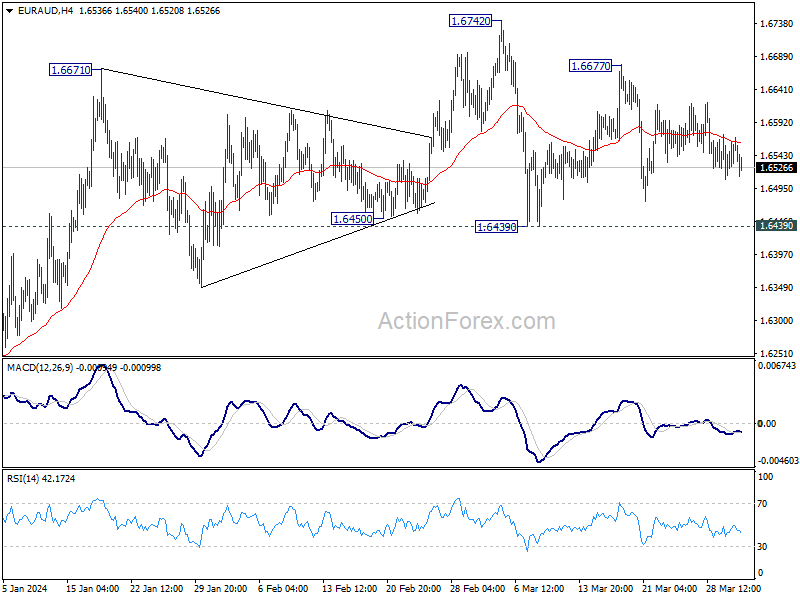

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6518; (P) 1.6545; (R1) 1.6580; More...

Intraday bias in EUR/AUD remains neutral for the moment. Near term outlook will stay cautiously bullish as long as 1.6439 support holds. On the upside, above 1.6677 will target 1.6742 first. Decisive break there will resume whole rise from 1.6127 and target 1.6844 resistance next.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

Fed Unlikely to Lower Policy Rate Ahead of September

Markets

It was all about the March US manufacturing ISM yesterday. The ISM unexpectedly returned above the boom/bust-mark (50) for the first time since September 2022! The increase from 47.8 to 50.3 (vs 48.3 expected) came on account of higher production (54.6 from 48.4), rising new orders (51.4 from 49.2), a smaller contraction in inventories (48.2 from 45.3) and rising input prices (55.8 from 52.5; strongest pace since July 22). Manufacturing jobs were cut for a six straight month though at a lesser pace (47.4 from 45.9). The welcome return to growth in manufacturing and accelerating prices strengthen our view that the Fed is unlikely to lower its policy rate ahead of September. A less robust labour market is the key risk as stressed by Fed Chair Powell at the March press conference and repeated by the Fed Chair last Friday. However, even in that scenario we don’t think that Powell will push through such pivotal decision given the current razor-thin majority in favour of a cumulative 75 bps rate cuts this year. Markets followed the hawkish elements in yesterday’s ISM with US Treasuries selling off. A continued rise in oil prices (Brent crude > $88/b) played a role as well with risk sentiment in the US yesterday caught in the Treasury sell-off. US yields added 8.5 bps (2-yr) to 11 bps (10-yr) in a daily perspective. From a technical point of view, both the US 2-yr yield and the 10-yr yield are in a closing triangle pattern. They bounced off support coming from an upward trend line since February last week and both eye the (already tested) YTD high at respectively 4.75% and 4.35%. The jam-packed US eco calendar this week contains several potential triggers to break resistance with a bearish escape out of the triangle pattern. Chronologically we have JOLTS job openings (today), ADP employment, ISM services and a Powell speech (Wednesday) weekly jobless claims (Thursday) and payrolls (Friday). German Bunds open significantly weaker as well this morning (markets closed yesterday for Easter Monday) in response to the Treasury sell-off. We think that the US underperformance will nevertheless continue as EMU inflation data (Germany today; EMU tomorrow) will likely extend the EMU disinflation process, providing the ECB with momentum to conduct a first rate cut in June, ahead of the Fed. For the same reasoning we see EUR/USD drifting further towards the YTD low at 1.0695. A break lower opens the pat for a return to last year’s low at 1.0494. USD/JPY is again closing on the (potentially intervention triggering) 152 handle.

News & Views

The monthly shop price index of the British Retail Consortium showed UK store inflation dropping sharply in March. The Y/Y measure slowed from 2.5% in February to 1.3% in March, the lowest reading since December 2021. Comparted to the previous month, prices declined by 0.4%, with both food (-0.3% M/M ) and non-food prices (-0.4% M/M) contributing to the decline. According to BRC, the decline was driven by fierce competition to bring prices down for costumers. The BRC assesses that while the decline in prices is good news for consumers, “retailers face significant increased cost pressures that could put progress on bringing down inflation at risk”.

The Bank of Canada’s quarterly Business Outlook Survey showed that business sentiment and sales growth expectations have stopped falling. Especially indicators of business conditions, sales outlooks and employment intentions have changed direction after many quarters of decline. Demand remains soft due to high interest rates, but businesses expect interest rates to decline over the next 12 months. Subdued demand allows price pressures and the labour market to ease. Firms are finding it easier to fill job vacancies, but wage growth remains high. Businesses pricing behavior is continuing to normalize. Fewer firms than in the previous survey are planning unusually large or frequent price increases over the next 12months. However, the slow moderation in wage growth and gradual price through of high costs is keeping output price growth elevated. A separate survey on consumers’ inflation expectations shows that inflation has slowed, but their expectations for the near term have barely changed. The share of consumers expecting long-term inflation to be above 5% increased from 37% to 41%.

New Quarter Starts on a Hawkish Note

Hawkish. The new quarter started on a hawkish note. The European markets were closed, but the S&P500 closed the first trading session of the new quarter in the negative after the ISM data unexpectedly jumped into the expansion zone in March, the prices accelerated faster than expected and Atlanta Fed’s GDPNow spiked to 2.8% from 2.3%. Once again, the US data suggests that the Federal Reserve (Fed) should be in no rush to cut the interest rates. The only thing that could pressure the Fed to cut rates sooner rather than later is the end-of-year election, and the popular idea that the Fed may not be able to cut rates this year if it doesn’t starts around summer. But besides the election pressure, the economic data shows no sense of emergency for a June cut. That’s what the market reaction to yesterday’s strong economic data told yesterday. The US 2-year yield jumped 12 basis points to above 4.70%, the 10-year yield spiked to 4.30%. The Fed swaps priced in a 12bp cut for June, meaning that the odds of a June rate cut fell to – and shortly - below 50% yesterday for the first time this year. As such, the US dollar index kicked off the new quarter on a solid footage, the dollar index soared past the 105 level. The strong dollar sent the EURUSD to 1.0732, Cable slipped below its 200-DMA and the USDJPY is preparing to test the 152 level with limited upside potential above this level on threat that the Japanese will intervene to stop the yen depreciation if the USDJPY exceeds the 152 level.

Tesla on the chopping block

The softening Fed rate cut expectations didn’t derail the Big Tech rally in the first quarter, but it didn’t allow the rally to broaden beyond the Big Tech either. On the contrary, we saw a further narrowing of the rally within the so-called Magnificent 7 – where Apple and Tesla fell of the race: Apple for its falling iPhone sales in China and its AI miss and Tesla on its slowing deliveries. Tesla will reveal its latest quarterly deliveries report in the coming hours and analysts predict a large decline in Q1 deliveries. If that’s the case, it would mean that Tesla’s recent price cuts did nothing but to squeeze the profit margins in the latest quarter. Tesla started hiking its EV prices in many locations including China, but investors will likely remain skeptical regarding the impact of the price hikes if the sales growth reverses. If investors sent Tesla’s stock price skyrocketing in the previous years, it was mostly due to the expectation of around 50% annual growth. If the growth narrative falls under a bus, it will be hard to keep Tesla at the current valuation (PE ratio of around 67). In this context, we could only see Tesla’s stock price retreat further. My downside target stands at $150 per share.

What to watch?

Besides the car deliveries, investors will be watching the latest JOLTS data and US factory orders that are due today. Job openings are expected to have further fallen while factory orders are expected to have jumped in February. Any positive surprise on both data should continue to soften the Fed doves’ hands into Friday’s official jobs data and back a further rally in the US dollar across the board.

Elsewhere, the German CPI data and Eurozone final manufacturing data will be closely watched today. Soft figures could further revive the European Central Bank (ECB) doves and increase the downside pressure on the EURUSD.

Gold, Oil rise on Damascus bombing

Copper gained 1% yesterday on strong Chinese PMI data while gold defies the higher US yields and a stronger dollar. The price of an ounce hit a fresh record yesterday on the back of rising uncertainties regarding the actual risk rally and the mounting geopolitical tensions after Israel has reportedly bombed the Iran embassy in Damascus. Also note that the strong EM and central bank demand this year makes gold an investors’ darling. The willingness to diversify the US dollar holdings due to a less than ideal US fiscal discipline will likely remain in play. As such, gold is certainly one of the best hedges against a potential risk meltdown in the foreseeable future.

In energy, US crude flirted with the $85pb level on the Iranian embassy bombing by Israel. On the supply side, OPEC is expected to keep its production cuts in place until the end of the quarter, but the latter has a decreasing impact on the global supply as US producers replace the OPEC supply gap. US crude exports just set their fifth monthly record since Europe imposed sanctions on Russia. As such, Russian sanctions and OPEC cuts are buttering the bread of American exporters. Exxon gained more than 20% since January, Chevron is up by 14% and has just stepped into the bullish consolidation zone – after having cleared the major 38.2% Fibonacci retracement on 2022 to 2024 selloff – hinting at a further extension of gains toward the $165 per share level.

German Inflation as a Bellwether for Euro Area Inflation on Thursday

In focus today

In the US, JOLTs Job Openings are due for release for February. As companies have reported cooling hiring plans and availability of workers has improved, we expect job openings to trend lower over the coming months, which would pave way for the first rate cut from the Fed.

In the euro area, focus is on German inflation data ahead of the important euro area inflation print for March on Thursday. The data released from other countries during Easter indicate that euro area HICP inflation on Thursday will be lower than the consensus forecast of 2.5% y/y as inflation came in lower than expected in France, Italy, and Spain.

Economic and market news

What happened overnight

In Australia, Christopher Kent, Assistant Governor of the Reserve Bank of Australia (RBA), announced a shift in the bank's liquidity provision method. They will replace the current practice of setting a rate floor with excess reserves and an exchange settlement rate with open market repo operations at a price close to the cash rate target. The RBA will soon conduct public and market consultations on this new system before finalizing operational details.

What happened during Easter

In the US, the PCE price index was in line with expectations in February, coming in at 2.5% y/y (0.3% m/m), while the core measure printed 2.8% y/y (0.3% m/m). Overall, final data from the University of Michigan painted a benign picture. Consumer sentiment exceeded expectations at 79.4 (cons: 76.5), while inflation expectations over 1Y and 5Y horizons crept slightly lower to 2.9% and 2.8%, respectively.

Yesterday, the ISM Manufacturing PMI for March came in at 50.3, marking the first reading above 50 since September 2022 and indicating growth in the manufacturing sector.

In the euro area, M3 money supply was higher than expected at 0.4% y/y (cons: 0.3%), while loans to households and loans to non-financial corporations increased by 0.3% and 0.4%, respectively. The upbeat credit data supports the outlook for the recovery in the manufacturing sector this year. Additionally, ECB officials made statements during Easter. Cipollone (dove) emphasized that rate cuts could start in April if inflation and wage data align with ECB expectations of easing price pressures. Villeroy (hawk) stated that the ECB may cut rates independently of the Fed, a sentiment echoed by Holzmann (hawk), who noted the slower growth of the European economy compared to the US. Stournaras (dove) suggested the ECB might cut rates by 100bp in 2024, but there is no consensus within the central bank, with some officials preferring more moderate cuts.

In Japan, key data has been released over Easter. The Bank of Japan's (BoJ) large Tankan business survey showed that the service sector continues on a strong footing supported by booming tourism. Big non-manufacturers reported the best business conditions since the early 90s. The manufacturing sector slowed a bit but largely remains positive. Worth noticing, optimism is driven by big business, which has been able to take advantage of the weak yen. Following the March rate hike, this probably does not change much for the BoJ, which will think twice before moving again. It does however confirm that the economy remains robust, supported by particularly foreign demand, which is a prerequisite for tightening further. Tokyo March inflation (excl. fresh food) declined a bit to 2.4% on the back of core inflation pressures still close to an annualised 2%.

In China, PMI manufacturing for March surprised strongly to the upside with the official NBS PMI manufacturing jumping higher from 49.1 to 50.8 (cons: 50.1) and the private version from Caixin increasing from 50.9 to 51.1 (cons: 51.0). The NBS PMI manufacturing has hovered at a weaker level than Caixin PMI for some months, but the gap has now closed with the sharp rise in NBS PMI. Especially the export order indices were strong, which fits with our expectation of a moderate recovery in the global manufacturing cycle. The service PMI was also released from NBS showing a rise to 53.0 from 51.4. The Chinese economy seems to have gathered pace during Q1 adding upside risks to our 4.5% GDP growth forecast for this year, which were already in place following the hard data on retail sales and industrial production for January/February.

In Sweden, the Riksbank (RB) left the policy rate unchanged at 4.00%, as widely anticipated. RB maintained its dovish shift and signalled a first rate cut in May or June.

Equities: It has been a fairly quiet Easter for global equities with some gains leading up to Easter before a bit of retracement yesterday. Most interesting was the move in bond markets yesterday (more on this below). Worth noticing on the equity side we still see the inflationary trade continuing with the energy sector outperforming as the oil price is ticking higher. The benign PCE report from US last week did not change that, and near-term risks to equities are still coming from too high inflation prints and a move higher in leading inflation data. In US yesterday, Dow -0.6%, S&P 500 -0.2%, Nasdaq +0.1%, and Russell 2000 -1.0%. Asian markets are mixed this morning with Chinese markets massively outperforming after a broad set of encouraging PMIs. US futures are marginally lower while European futures are marginally higher.

FI: Since our latest EUR FI update on Wednesday, most of the market action played out yesterday. The surprisingly strong US manufacturing ISM figures added to the market's uncertainty about the prospects rate cuts this year: The probability of a June cut of 25bp declined to 50% yesterday, while the UST yield curve rose 10-12bp with the largest increases located in the long end. Market-based inflation rates moved only slightly higher, making real rates the dominant driver of yesterday's move. The Bund curve is close to unchanged since Wednesday (Europe was closed yesterday).

FX: It has been a quiet start to the week with Europe largely out for Easter. Scandies were off to a poor start to the week with EUR/NOK breaching firmly above 11.70 and EUR/SEK close to the 11.60 mark. Conversely, USD and CHF regained ground ahead of a packed calendar in terms of data releases.

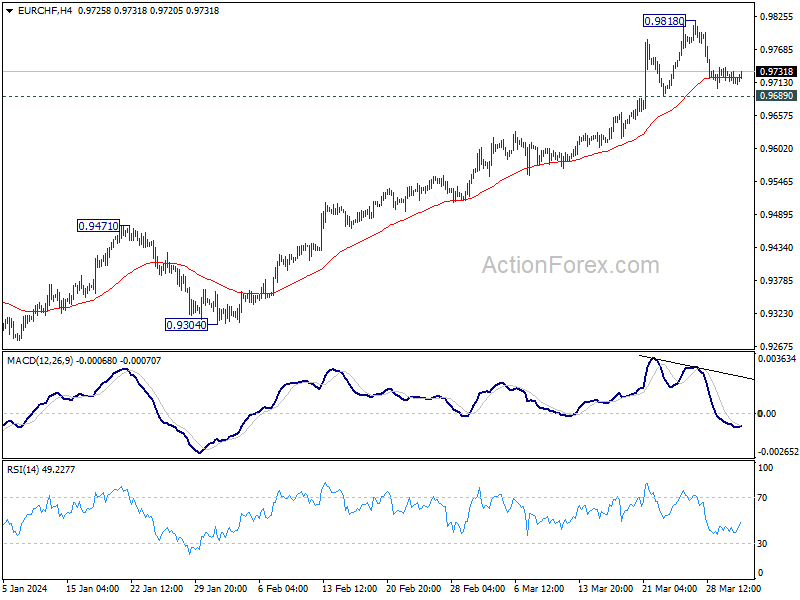

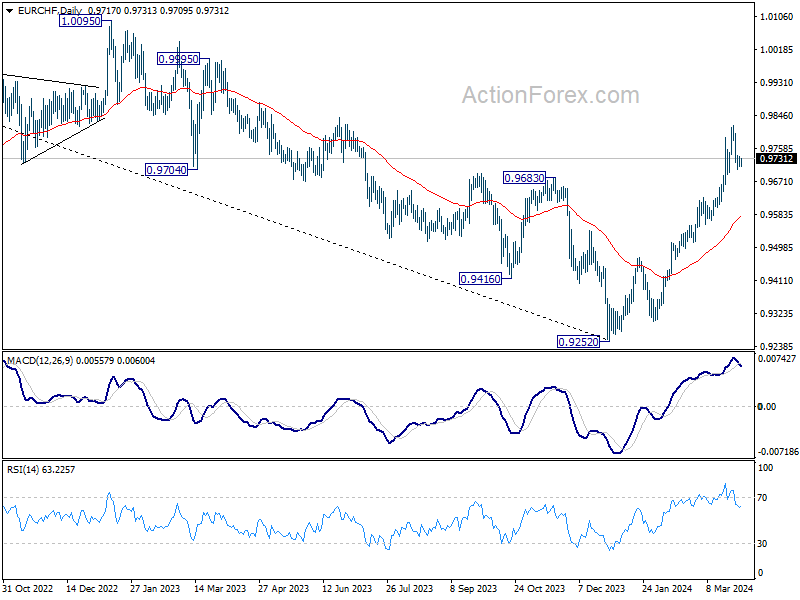

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9705; (P) 0.9721; (R1) 0.9729; More...

Intraday bias in EUR/CHF remains neutral as consolidation continues below 0.9818. Another rally is expected as long 0.9689 support holds. On the upside, above 0.9818 will resume the rise from 0.9252 towards 1.0095 key resistance next. Nevertheless, considering bearish divergence condition in 4H MACD, break of 0.9689 will indicate short term topping, and turn bias back to the downside for 55 D EMA (now at 0.9581) instead.

In the bigger picture, a medium term bottom should be in place at 0.9252 already, on bullish convergence condition in W MACD. Rise from there would now target 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even as a correction to the down trend from 1.2004. This will remain the favored case as long as 55 D EMA (now at 0.9576) holds.

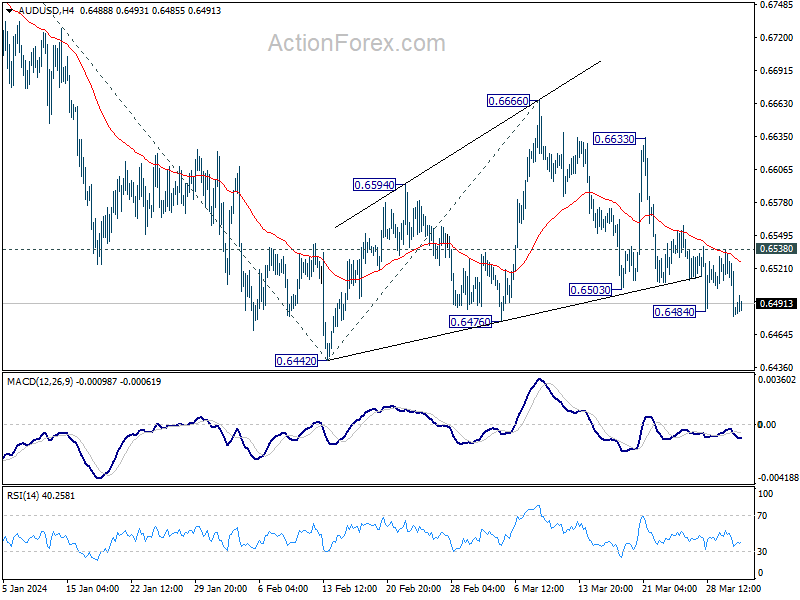

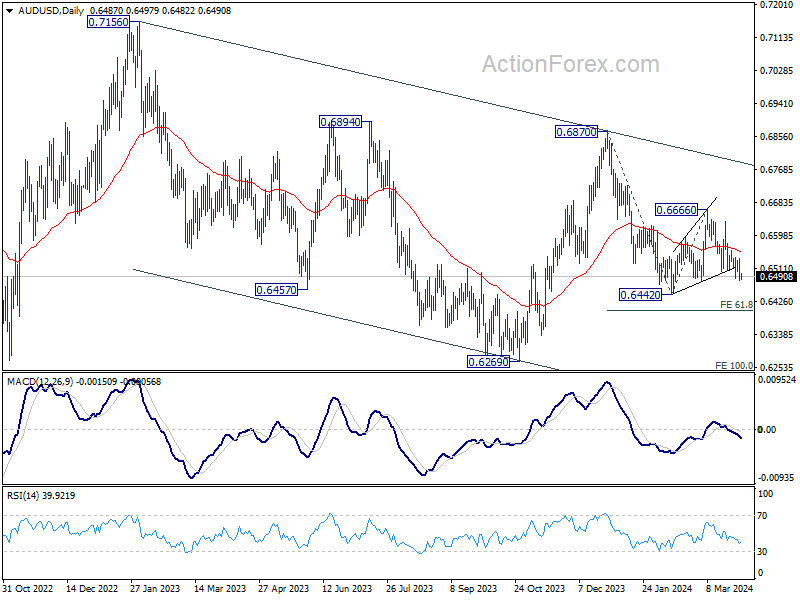

AUD/USD Daily Report

Daily Pivots: (S1) 0.6468; (P) 0.6503; (R1) 0.6526; More....

Intraday bias in back on the downside with breach of 0.6484 support. Retest of 0.6442 should be seen next. Firm break there will resume whole decline from 0.6870 and target 61.8% projection of 0.6870 to 0.6442 from 0.6666 at 0.6401. On the upside, above 0.6538 minor resistance will turn intraday bias neutral again.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which might still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

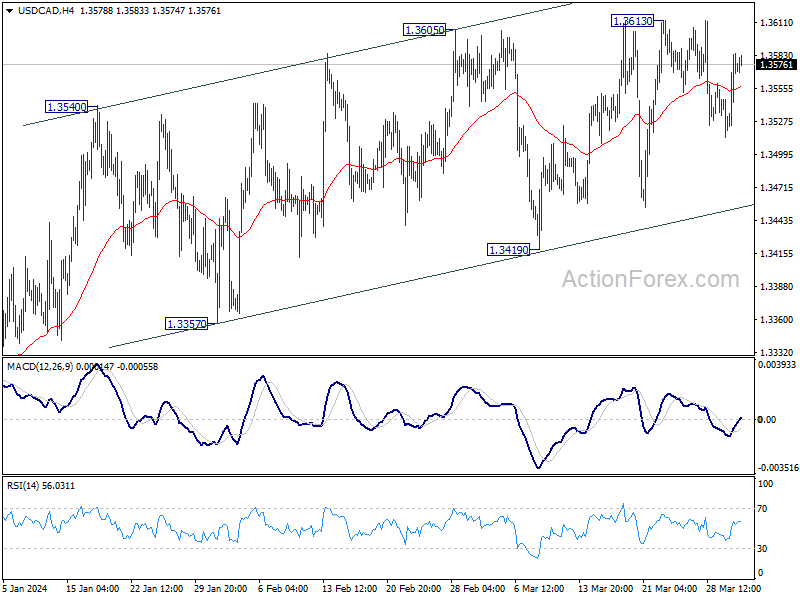

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3528; (P) 1.3558; (R1) 1.3600; More...

Range trading continues in USD/CAD and intraday bias stays neutral. On the upside, decisive break of 1.3612 resistance will resume whole rise from 1.3176 towards 1.3897 resistance. On the downside, firm break of 1.3419 support will argue that rebound from 1.3176 has completed. Near term outlook will be turned bearish for 1.3357 support first.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

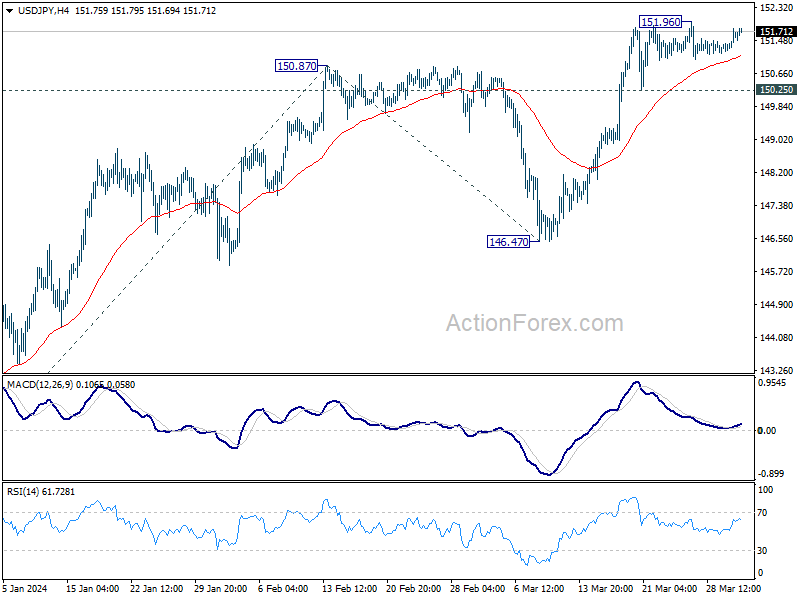

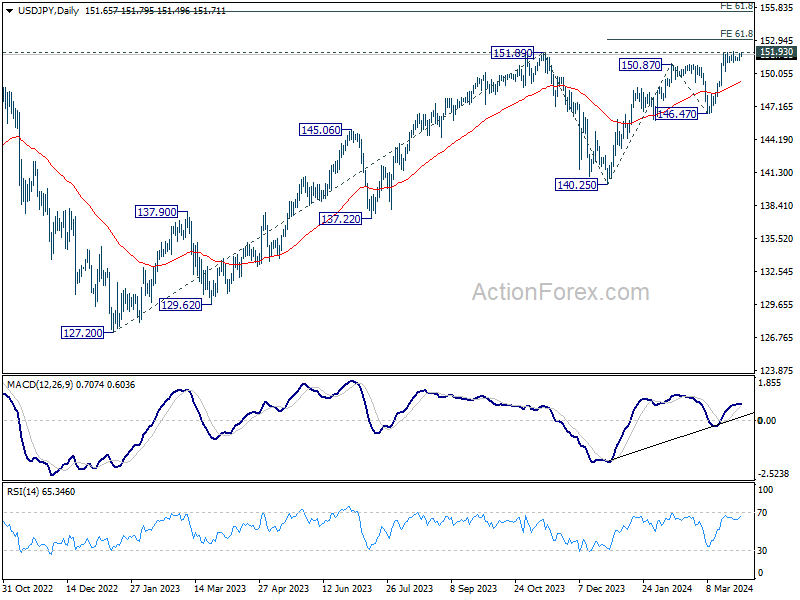

USD/JPY Daily Outlook

Daily Pivots: (S1) 151.33; (P) 151.55; (R1) 151.88; More...

Intraday bias in USD/JPY remains neutral for the moment. On the downside, break of 150.25 support should confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 149.35). Nevertheless, sustained break of 151.93 key resistance will confirm long term up trend resumption. Next near term target will be 61.8% projection of 140.25 to 150.87 from 146.47 at 153.03.

In the bigger picture, correction from 151.87 (2023) high could have completed at 140.25 already. Rise from 127.20 (2023 low), as part of the long term up trend, is probably ready to resume. Decisive break of 151.93 resistance (2022 high) will confirm this bullish case. Next medium term target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. This will remain the favored case as long as 146.47 support holds, in case of another pullback.

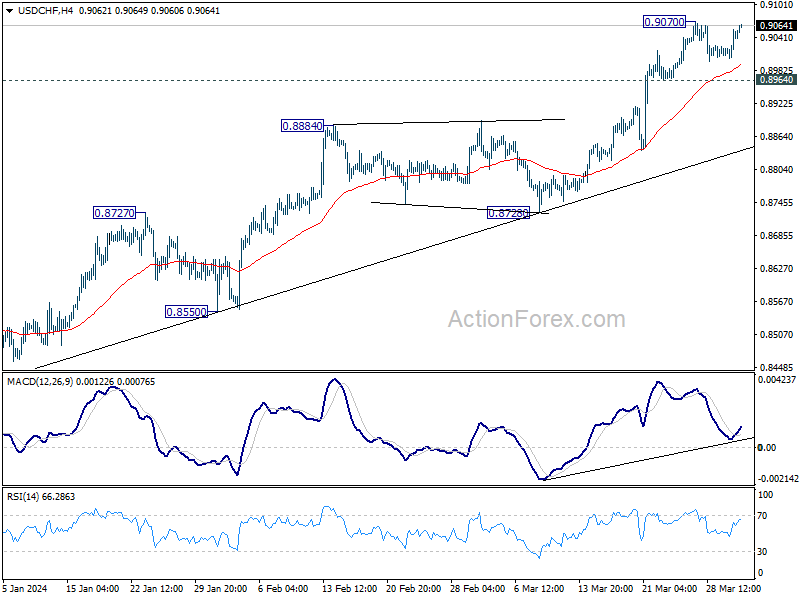

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9014; (P) 0.9036; (R1) 0.9066; More....

Intraday bias in USD/CHF remains neutral at this point. Further rally is expected as long as 0.8964 support holds. Firm break of 0.9070 will resume larger rise from 0.8332 towards 0.9243 key resistance next.

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.

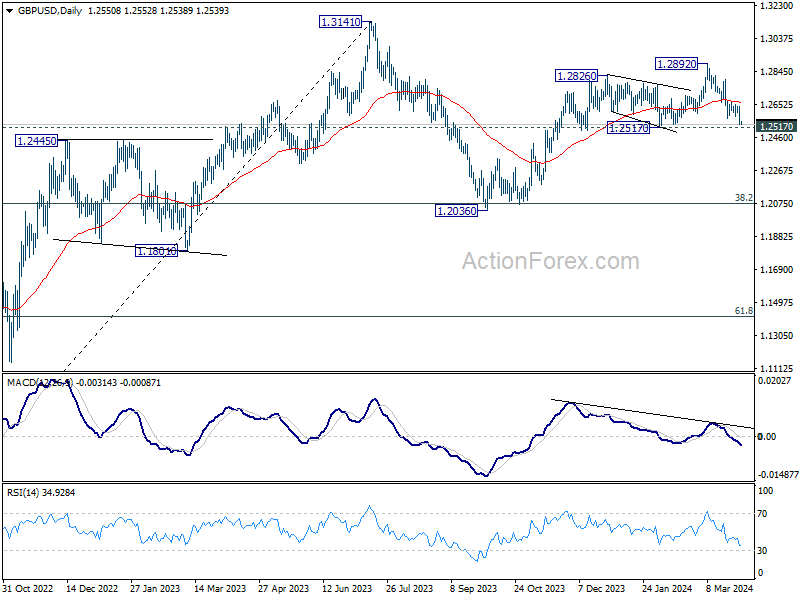

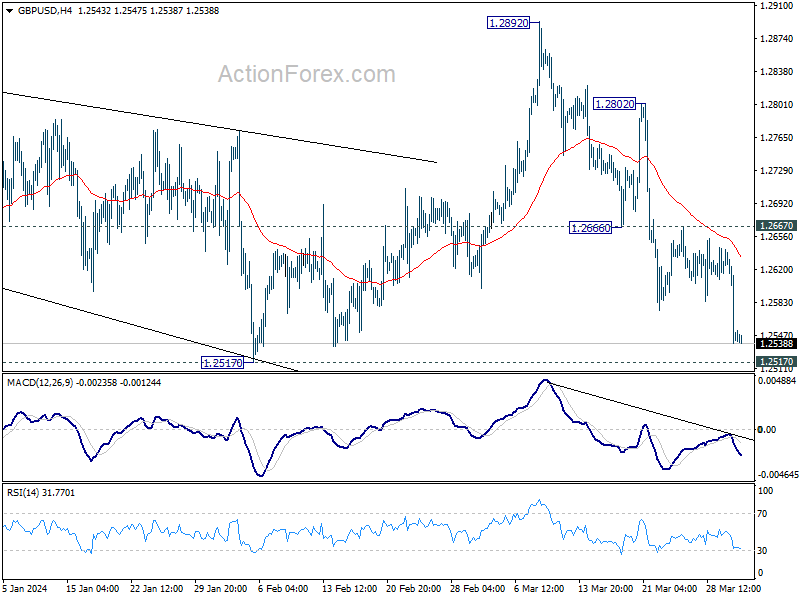

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2513; (P) 1.2578; (R1) 1.2617; More...

Intraday bias in GBP/USD remain son the downside for 1.2517 structural support. Decisive break there will suggest that rise from 1.2036 has completed at 1.2892 already, and turn near term outlook bearish. For now, risk will stay on the downside as long as 1.2667 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which might still be in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.