Sample Category Title

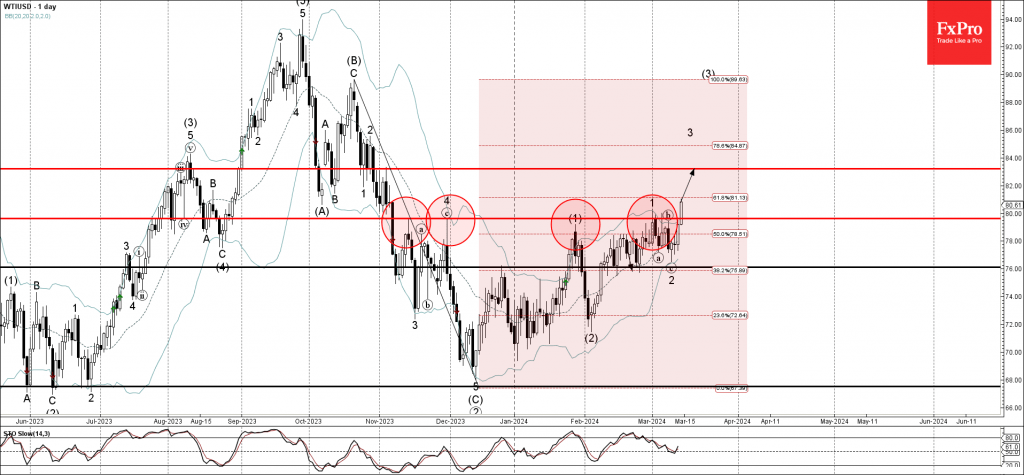

WTI Wave Analysis

- WTI broke resistance level 80.00

- Likely to rise to resistance level 83.20

WTI crude oil recently broke the round resistance level 80.00 (which has been reversing the price from November).

The breakout of the resistance level 80.00 coincided with the breakout of the 50% Fibonacci correction of the previous sharp downward impulse wave (C) from October.

Given the deterioration of the global risk sentiment, WTI crude oil can be expected to rise further toward the next resistance level 83.20.

ETHUSD Trades Flat in Dencun Upgrade Aftermath

- ETHUSD trades sideways in the past few sessions

- Fails to capitalise on completion of Dencun upgrade on Wednesday

- Momentum indicators ease but do not exit overbought zones

ETHUSD (Ethereum) has been in a steep uptrend in 2024, surging to consecutive multi-month highs. However, the leading altcoin seems to be consolidating in the past few sessions despite the successful completion of the Dencun upgrade as it has been repeatedly repelled a tad below the 4,100 mark.

Should bullish pressures fade, the price might reverse towards the recent support of 3,740. Further declines could then cease at the April 2022 resistance of 3,580, which could serve as support in the future. Failing to halt there, the price may challenge the March 2024 support of 3,260.

On the flipside, bullish actions could propel the price to fresh multi-month peaks, where the December 2021 resistance of 4,150 could curb initial upside attempts. Conquering that barrier, the bulls may attack the May 2021 high of 4,385. A violation of that region could pave the way for the November 2021 resistance of 4,670.

Overall, ETHUSD has been struggling to extend its series of multi-month highs despite the recent positive idiosyncratic developments. Is the price headed towards a pullback?

Sunset Market Commentary

Markets

ECB’s Stournaras this morning hijacked the headlines. The Greek governor said rates need to be cut soon: twice before the summer break (in August) and twice before the end of the year. He expects the first one to happen in June. Dutch hawk Knot sided with his Greek colleague insofar he is penciling in June for the kick-off. He refrained from giving guidance for the meetings thereafter though. Chief economist Lane held a more neutral approach, sticking to Lagarde’s message last week that a lot more data (including about wages) will be available at this potentially pivotal June meeting. While calls for ECB cuts in 2024 grow louder and bolder, a different scenario is panning out in front of the Fed. February producer price inflation easily topped forecasts across the board. The headline figure came in at 0.6% m/m, double the 0.3% consensus. The narrowest core gauge (ex. food, energy and trade) rose 0.4%. Year-on-year readings (between 1.6% - 2.8%) added more evidence to a bottoming out process that started somewhere end of last year. Weekly jobless claims meanwhile surprised to the downside. Applications for unemployment benefits last week dropped to a low 209k, from a downwardly revised 210k. Retail sales in February didn’t live up to expectations to more or less overcome the January dip. But with the broader (labour market) picture nicely intact, that didn’t prevent core bond yields from adding between 4.4 and 8.6 bps in the US. The 2-y and 10-y yield are single-digit bps away from their YtD highs. German yields add 2.6 (2-y) to 5.3 (10-y) bps in sympathy though one starts to wonder how much longer the front-end can join the US trend when ECB members continue to talk so openly about cuts. Either way, most tenors in Germany are also closing in on their YtD highs.

The dollar, for the first time since long, finally starts profiting from favourable interest rate differentials and a weakish risk environment (stocks slightly down in the US). EUR/USD slips from an intraday high of 1.0955 to currently test the 1.09 big figure. DXY (trade-weighted) found support at the 50% retracement on the December-February rebound (102.8) before moving beyond 103. USD/JPY and EUR/JPY parted ways with the former rising to 148 but the latter easing a few ticks to 161.5. The Japanese newspaper Jiji reported the BoJ is poised to end negative rates at its meeting next week, though adding that tomorrow’s wage negotiation results play a key role in the final decision. Sterling holds the upper hand against most G10 peers, including the euro (but not the USD). EUR/GBP snapped a three-day winning streak by erasing yesterday’s gains (0.8541).

News & Views

Swedish inflation rose by 0.2% on a monthly basis, both at the top level and the underlying one. Markets anticipated increases by 0.4% and 0.3% respectively. Headline inflation slowed more than expected on an annual level (4.5% from 5.4% vs 4.7% consensus) and for the core gauge using fixed interest rates for household mortgages (CPIF; the Riksbank’s preferred one): 3.5% from 4.4%. That’s less than the Swedish central bank predicted back in November (3.7%). Lower electricity prices contributed to decreased housing costs according to Statistics Sweden. Actual rents for housing still rose though. Furthermore, there were seasonally normal price rises for clothing. There were also price increases in fuel, recreational and cultural services, as well as for restaurant and hotel visits. Today’s data strengthen the Riksbank’s message that they will start cutting their policy rate in the first half of the year. The Swedish krone underperforms today with EUR/SEK rising to 11.23 following an intensive test of 11.14 support at the end of last week.

The International Energy Agency changed its view on this year’s oil availability. They now join OPEC+’s warning of an oil supply deficit throughout the year. The IEA upped its world oil demand growth forecasts by 110k barrels to 1.3mn b/day on a stronger US outlook and increased demand for ship fuel over problems in the Panama canal (climate) and the Suez canal (Houthi attacks). Simultaneously they now believe that OPEC+ could continue output cuts in the second half of the year. Brent crude prices rise for a second straight session, taking out $85/b for the first time since the end of October of last year.

Silver Bulls Return With a Bang

- Silver marks new higher highs in the year to date

- Some caution required as former resistance area is nearby

Silver bulls roared back during Wednesday’s late European trading hours, with the metal soaring to a more-than-three month high of 25.14 before closing marginally below the 25.00 round level.

The completion of a double bottom pattern around the 21.91 floor led to a bullish explosion, as the price advanced above the neckline of 23.51. While the bullish market structure in the short-term picture is still solid, the overbought signals coming from the RSI and the Stochastic oscillators suggest that upside pressures might soon lose steam.

The presence of the descending line, linking the 2021 and 2023 highs, could create downward pressure at 25.45, hindering any potential rise to the crucial 26.00 psychological level. Note that the metal has been attempting to close above the latter without success since the summer of 2021. Hence, if bullish efforts prove fruitful this time, the price might gear up to the 2022 high of 26.90 and then push towards the 28.15 barrier from May 2021.

If the price gets rejected near the 25.00 threshold, it may revisit the 61.8% Fibonacci retracement of the May-October 2023 downleg at 24.00. Failure to pivot there could see a bearish continuation towards the 50% Fibonacci of 23.37 and then an extension to the 38.2% Fibonacci of 22.73. The tentative support trendline, which joins the September 2022 and October 2023 lows, could cause bigger damage to the market if violated around 21.93.

Summing up, silver has experienced strong progress over the past two weeks, though a major resistance area is still overhead, questioning whether the metal will manage to violate its neutral 2023 pattern above 26.00.

U.S. Retail Sales Rebound in February

Retail sales rose 0.6% month-on-month (m/m) in February, reversing most of January's -1.1 % decline (revised from -0.8% previously). This was lower than the consensus forecast calling for slightly stronger growth of 0.8%.

Trade in the auto sector was up 1.6% m/m, reflecting an increase in sales at motor vehicle dealers (1.8%) which was partly offset by a decline in automotive parts and accessory stores (-0.5%).

Sales at gasoline stations broke four consecutive months of decline, rising by 0.9% m/m. This largely reflected an uptick in gas prices. The building materials and equipment category rose by a notable 2.2% m/m.

Sales in the retail sales "control group", which excludes the above volatile components (autos, building materials and gas) and is used to estimate personal consumption expenditures (PCE) was flat on the month after falling by -0.3% m/m in January (revised from -0.4% previously).

- Among the control group, positive contributions came from miscellaneous store retailers (0.6% m/m), department stores (0.4%) and food and beverage stores (0.1% m/m). Sales at sporting goods stores were flat on the month.

- All the remaining categories registered declines. Clothing and accessory stores registered the largest decline of -0.5% m/m.

Food services & drinking places – the only services category in the retail sales report – rose by 0.4% m/m.

Key Implications

Retail spending was back in positive territory in February, after a sizeable decline to start the year. Higher borrowing costs and elevated prices are challenging households but spending is still being fueled by a robust job market and rising wages. However, as the labor market cools and wage gains abate, spending should moderate. With two months of data in for the quarter, consumer spending is currently tracking 2.7% q/q (annualized) for Q1.

The pick-up in retail spending is unlikely to be good news for policymakers at the Federal Reserve. The recent flip in core goods prices from deflation to price growth makes continued buoyant retail sales even more of a challenge to the Fed's inflation targeting objective. The current near-term headwinds, from both inflation and spending, are likely to keep the Fed on the sidelines for a bit longer as they continue to monitor inflation's progress to target.

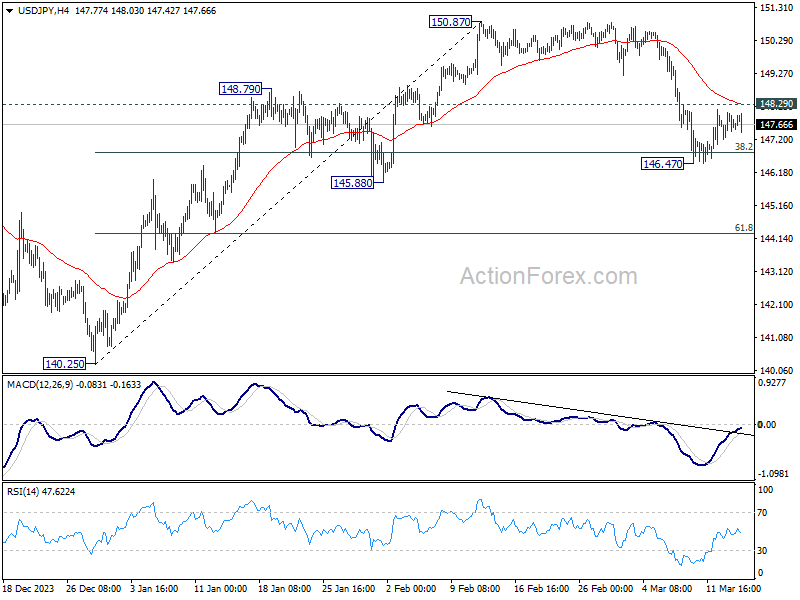

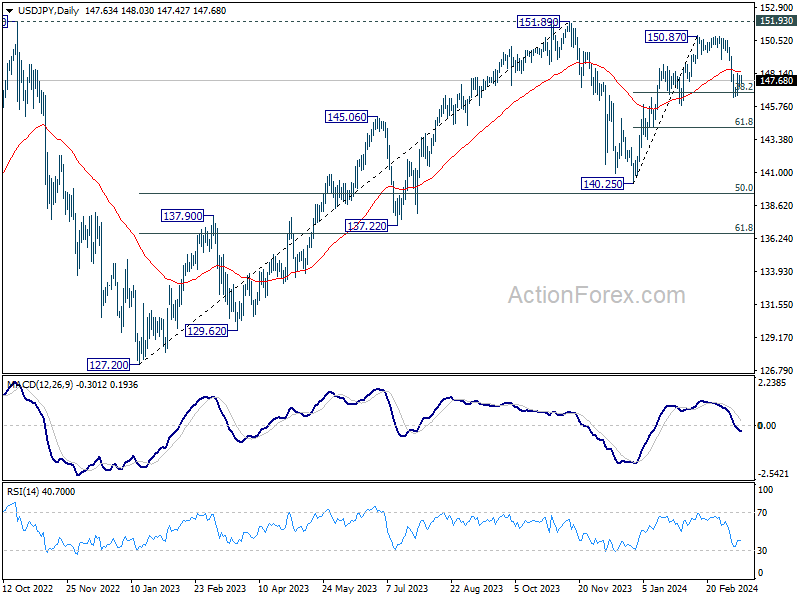

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.31; (P) 147.68; (R1) 148.12; More...

Range trading continues in USD/JPY and intraday bias stays neutral. On the downside, sustained break of 38.2% retracement of 140.25 to 150.87 at 146.81 will argue that fall from 150.87 is reversing the whole rally from 140.25. In this case, deeper decline would be seen to 61.8% retracement at 144.30 and below. Nevertheless, strong support from 146.81, followed by break of 148.29 minor resistance resistance, will argue that fall from 150.87 is merely a correction, which has completed already. Retest of 150.87 should be seen next.

In the bigger picture, no change in the view that price action from 151.89 (2023 high) are correction to up trend from 127.20 (2023 low). The question is whether this correction has completed at 140.25, or extending with fall from 150.87 as the third leg. Sustained break of above mentioned 146.81 fibonacci level will favor the latter case. But even so, downside should be contained by 50% retracement of 127.20 to 151.89 at 139.54.

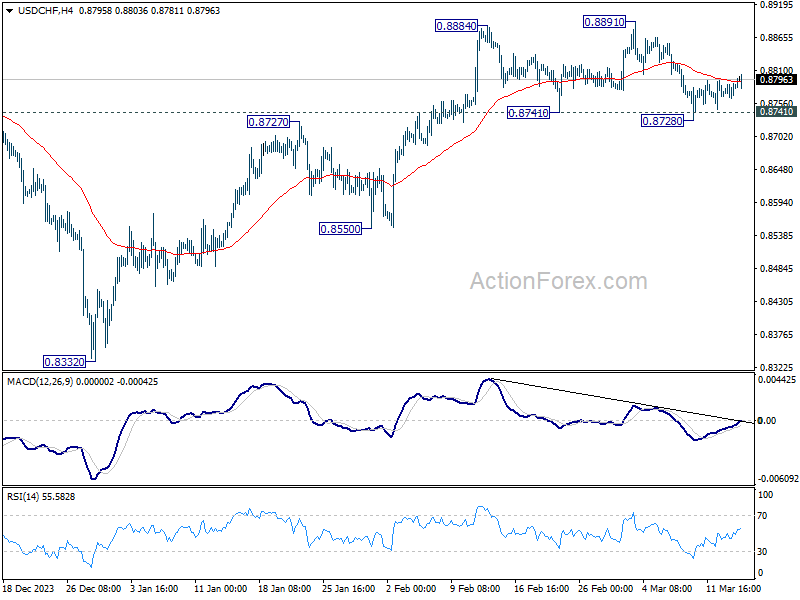

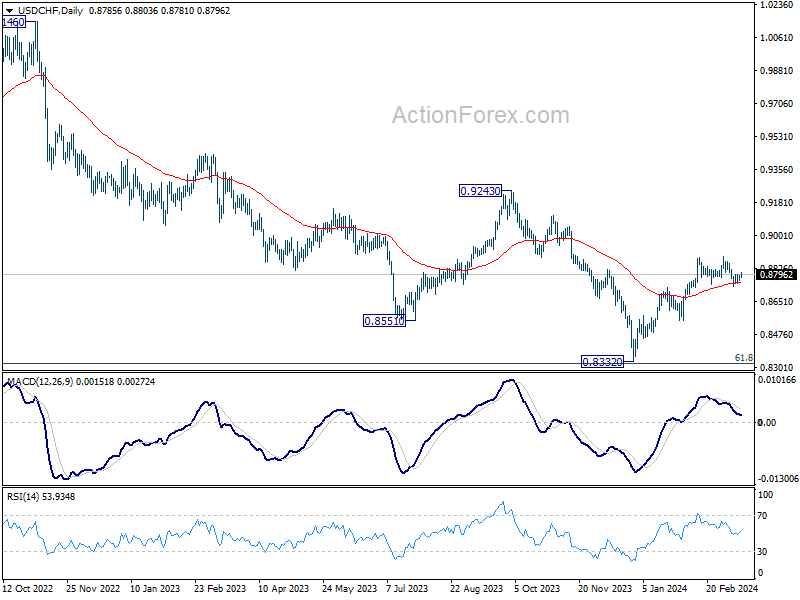

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8773; (P) 0.8782; (R1) 0.8799; More....

Intraday bias in USD/CHF remains neutral at this point. On the downside, sustained break of 0.8741 will argue that the whole rebound from 0.8332 might have completed, and bring deeper fall to 0.8550 support. Nevertheless, strong bounce from current level will retain near term bullishness. Further break of 0.8891 will resume the rise from 0.8332.

In the bigger picture, price actions from 0.8332 medium term bottom as seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8555 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.

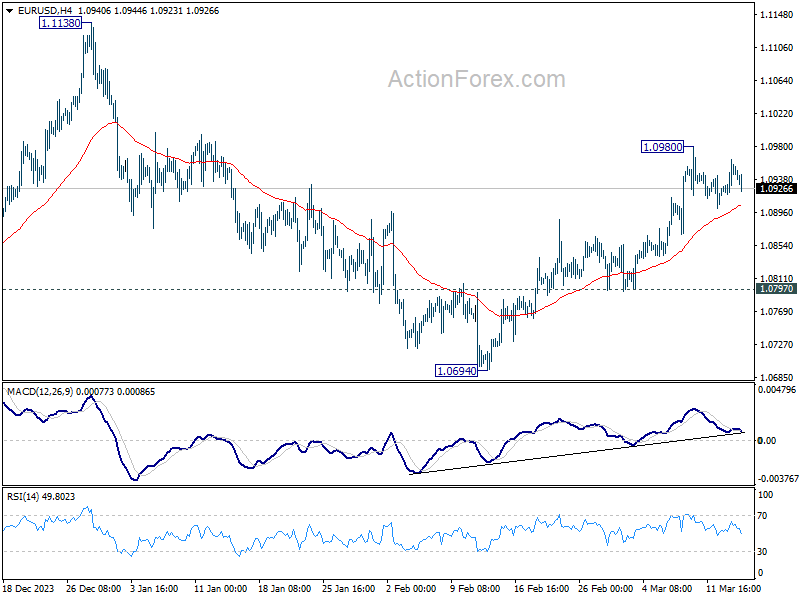

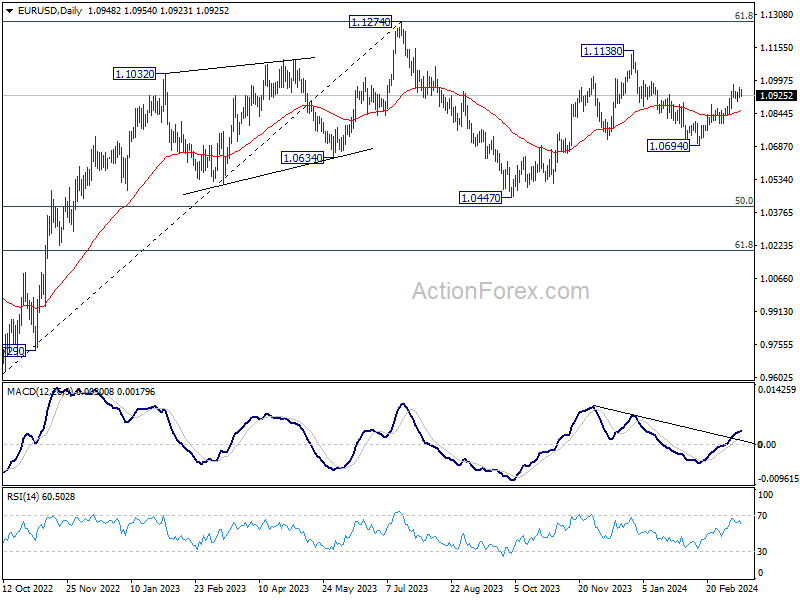

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0924; (P) 1.0944; (R1) 1.0968; More...

Intraday bias in EUR/USD remains neutral for the moment. Further rise is in favor as long as 55 4H EMA (now at 1.0904) holds. Above 1.0980 will resume the rally from 1.0694 to retest 1.1138 high. However, sustained break of the EMA will turn bias to the downside for 1.0797 support instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

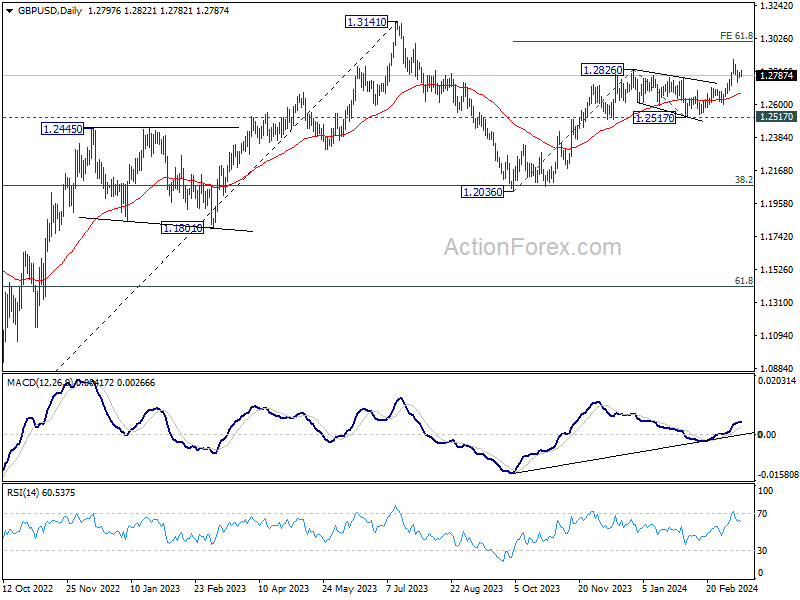

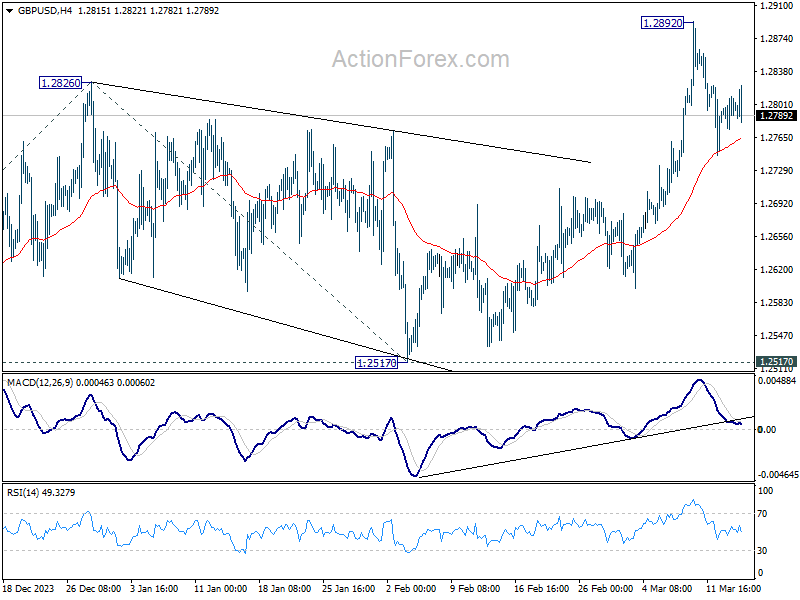

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2778; (P) 1.2794; (R1) 1.2814; More...

Intraday bias in GBP/USD remains neutral and outlook is unchanged. Further rally will remain in favor as long as 55 4H EMA (now at 1.2764) holds. On the upside, above 1.2892 will resume larger rise from 1.2063 and target 61.8% projection of 1.2036 to 1.2826 from 1.2517 at 1.3005. However, sustained break of 55 4H EMA will bring deeper fall back towards 55 D EMA (now at 1.2672), and possibly further to 1.2517 structural support.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which is still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.