Sample Category Title

GBP/USD: Remains Constructive Ahead of US Data

Cable is probing above 1.2800 mark in early Thursday, adding to initial signals that shallow correction from new 8-month high (1.2893) might be over.

Two-day pullback was contained by rising 10DMA, with strong downside rejection on Wednesday, pointing to solid bids and signaling that larger bulls remain firmly in play.

Technical picture on daily chart is bullish (positive momentum is strong and Tenkan / Kijun-sen in bullish setup and diverging), with fresh recovery seeing a daily close above 1.2800 (Fibo 38.2% of 1.2893/1.2745 correction) as minimum requirement to keep near-term action biased higher.

Sterling regained traction after markets digested US inflation data and kept growing expectations for June rate cut, which put the dollar under pressure again.

Markets await release of a batch of US economic data today (retail sales, weekly jobless claims, producer price index) for fresh signals.

Res: 1.2820; 1.2837; 1.2858; 1.2893.

Sup: 1.2780; 1.2765; 1.2745; 1.2714.

USD/JPY: Analysts Adjust Forecasts for Strengthening of Yen

Since the beginning of 2024, the USD/JPY price has been in an uptrend (as shown by the blue channel), but when the rate exceeded the psychological level of 150 yen per US dollar, market sentiment changed. This was due to expectations that the Bank of Japan would take interest rates out of negative territory — and statements from officials gave clear indications of this possibility.

Expecting a tightening of monetary policy, the yen sharply strengthened against the dollar, and a bearish A→B impulse formed on the USD/JPY chart. However, having reached the level of 147 yen per US dollar (and dropped slightly below it), the market has stabilized. Moreover, we see some recovery: today, the USD/JPY price is trading around 147.8.

From a fundamental analysis point of view, analysts believe that the strength of the US economy should not be underestimated. And if the Bank of Japan raises rates, it will not be in an aggressive manner. Bloomberg writes that Nomura Securities Co., Mizuho Bank Ltd. and Citigroup Global Markets Japan Inc. have adjusted their forecasts for the yen in recent weeks. On average, they forecast the rate to be around 140 yen per US dollar at the end of this year. HSBC Holdings Plc, in turn, expects the yen to end the year at 136 against the US dollar.

From the point of view of technical analysis of USD/JPY, the current recovery may be due to the influence of support from the lower border of the ascending channel.

Thus, traders can assume that the recovery will end (for example, rising to approximately 148.6 — 50% of the A→B momentum), with the bears attempting to resume the downward trend with a new assault on the lower channel boundary. If it turns out to be successful, this will open the way for the price to reach the levels indicated in analysts' forecasts.

Information from the Bank of Japan will be key. Its interest rate decision is scheduled for Tuesday, March 19.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

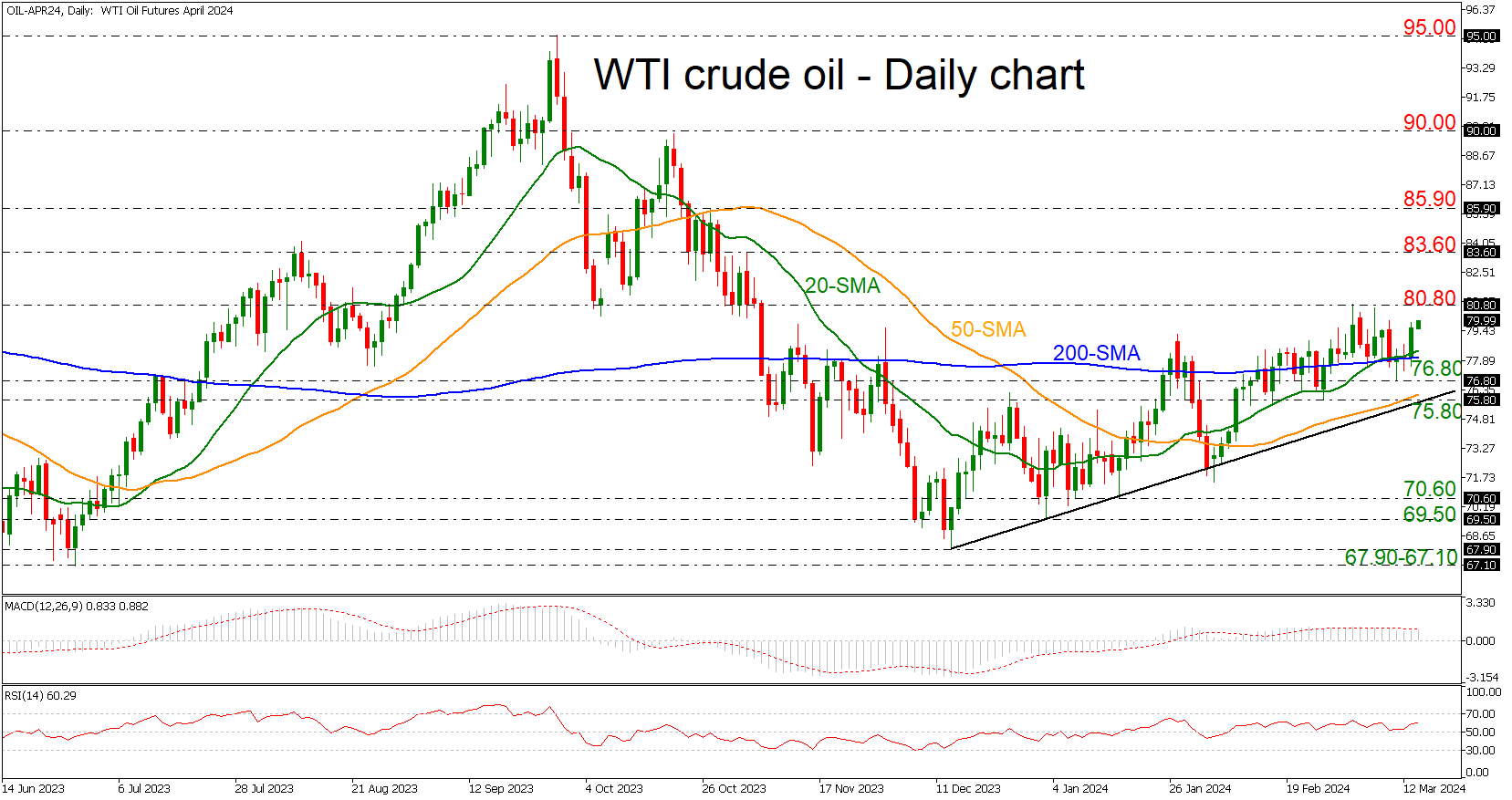

WTI Oil Futures Fight With 80.80 Bar

- WTI crude rebounds off 200-day SMA

- Remains in an uptrend in the short-term

WTI oil futures are finding a strong support level near the 200-day simple moving average (SMA) at 78.00 and are also struggling to jump beyond the 80.80 resistance. The price has been in an uptrend since mid-December with the technical oscillators suggesting a neutral to bullish bias. The RSI is pointing north above the 50 territory, while the MACD is moving sideways below its trigger line and above the zero level.

If the market manages to pick up speed, the 80.80 level could offer nearby resistance ahead of the 83.60 barricade. A significant close above the latter would break the 85.90 hurdle, raising chances for further increases.

Should prices decline, immediate support could be found around the 200-day SMA at 78.00, an area which has provided both resistance and support from January to March. Then a leg below that level, the price could meet the 75.80-76.80 support, which encapsulates the short-term ascending trend line. A drop lower could change the outlook to a neutral one, hitting 70.60.

In a nutshell, WTI crude oil is moving horizontally in the very short-term view, but an increase above 80.80 could endorse the longer-term bullish outlook.

ECB’s Stournaras advocates two rate cuts by summer break, four throughout the year

ECB Governing Council member Yannis Stournara, a known dove, proposed two rate reductions "before the summer break" and a total of four throughout the year. This strategy, he argues, is essential to ensure that ECB's monetary policy "does not become too restrictive" in the face of current economic challenges.

In an interview, Stournaras emphasizes the urgency of beginning these rate cuts soon, but not in April, as there will be "only little new information" available before then.

The rationale behind Stournaras's push for rate cuts stems from his observations on Eurozone's economy is "much weaker than expected," with risks skewed to the downside. Meanwhile, inflation, although significantly reduced, presents a balanced risk profile.

Addressing concerns about risk of "wage-price spiral," Stournaras argued that wages are merely "catching up, not leading inflation." He also highlights the moderating trend in nominal wage growth and the capacity of profits to absorb part of the pay increases, suggesting that fears of a wage-driven inflationary loop may be overstated.

Looking ahead, Stournaras envisions the deposit rate gradually decreasing to 2% by the end of 2025 or the beginning of 2026. However, he draws a line at this level, suggesting that rates should not fall below the pre-pandemic levels of 2%.

Greenback’s Performance Has Been Lackluster Recently

Markets

US Treasuries extended their post-CPI sell-off yesterday in absence of eco data or other news. US yields added 2.8 bps (30-yr) to 5.3 bps (3-yr). The US 2-yr yield is gradually moving back in the direction of the YTD high at 4.74%. Longer tenors show a similar dynamic but there’s some more ground to cover (US 10-yr YTD high at 4.35%). Following upward CPI surprises in January and February, US (CPI) headline and core inflation are now both set to stay above 3% over the course of 2024 with inflation dynamics re-accelerating into Q2. This context suggests significant hawkish risks to next week’s FOMC meeting and to Fed policy this year in general. In absence of additional disinflation evidence in coming inflation reports, we err on the side of delaying a first policy rate cut to September at the earliest. The US eco calendar can today trigger a further hawkish repositioning with February retail sales, producer price inflation and weekly jobless claims on the agenda. The proof of evidence again tipped to the other side. Anything apart from big misses can extend the US Treasury sell-off. Such underperformance should gradually start to support the dollar as well. The greenback’s performance has been lackluster recently, both in case of (minor) risk corrections and in case of rising US yields. We must add that German yields managed to follow the US pace yesterday, rising by 3.5 bps (5-yr) to 5 bps (30-yr). EUR/USD yesterday closed at 1.0948 from an open 1.0927. The ECB’s changes to its operational framework had no direct impact on trading. They will continue to steer policy by adjusting deposit rates and will narrow the spread between the MRO rate and the deposit rate from the current 50 bps to 15 bps from September 18.

Overnight Asian risk sentiment is mixed this morning with China underperforming. Other Asian bourses neglect yesterday evening’s negative WS close (-0.50%). Decent UK housing data (see below) can’t inspire sterling which is back at well-known territory (EUR/GBP 0.8550) after unexpectedly testing the 0.85 support zone at the end of last week. Next week’s UK inflation report and Bank of England meeting can perhaps finally break the deadlock in the currency pair. Our overall bias for today is for higher core bond yields and a firmer dollar.

News & Views

Polish MPC member Janczyk indicated that the Polish central bank (NBP) will resume the debate about a possible interest rate cut in the third quarter when the outlook in inflation becomes clearer. According to Janczyk, the NBP will lookt at at how favourable economic data will be and at which factors that may fan inflation, including government decisions (eg restoring a 5% VAT on food and/or easing measures aimed to cap energy prices). Janczyk estimates the impact to restore to VAT on food may add 0.8 ppt to inflation, but this might be mitigated by competition in the retail sector. The comments from Janczyk bring somewhat of a more moderate message compared to recent guidance from NBP governor Glapinski who said that there might be no case for interest rates cuts further this year. Janczyk’s comments didn’t hurt the zloty. At EUR/PLN 4.28, the Polish currency is trading near the strongest levels against the euro since March 2020.

A survey of the Royal Institution of Chartered Surveyors (RICS) showed signs of a gradual improvement in the UK housing market. The index of new buyer inquiries printed at a net balance of +6, unchanged from January but holding at the strongest level since February 2022. The net balance of new instructions to sell rose further from 12 to 20, the best level since autumn 2020. Agreed sales eased slightly from 4 to -3, but sales expectations are still expected to rise (6 from 12). The house price balance of the survey also improved from -19% to -10%, the best level since October 2022. The RICS survey states that “the near-term outlook is still somewhat cautious reflecting, in part, the suspicion that the recent easing in mortgage rates is likely to stall on the back of ongoing uncertainty about the timing and speed of interest rate reductions”

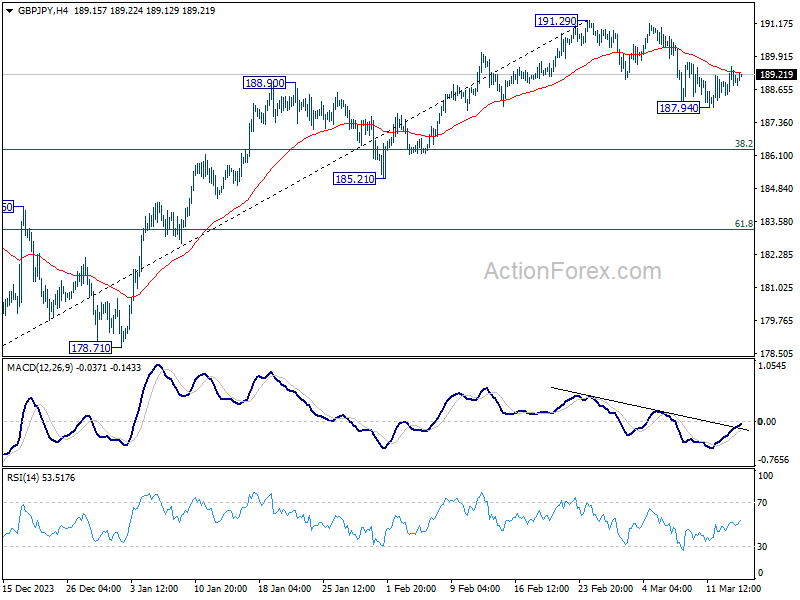

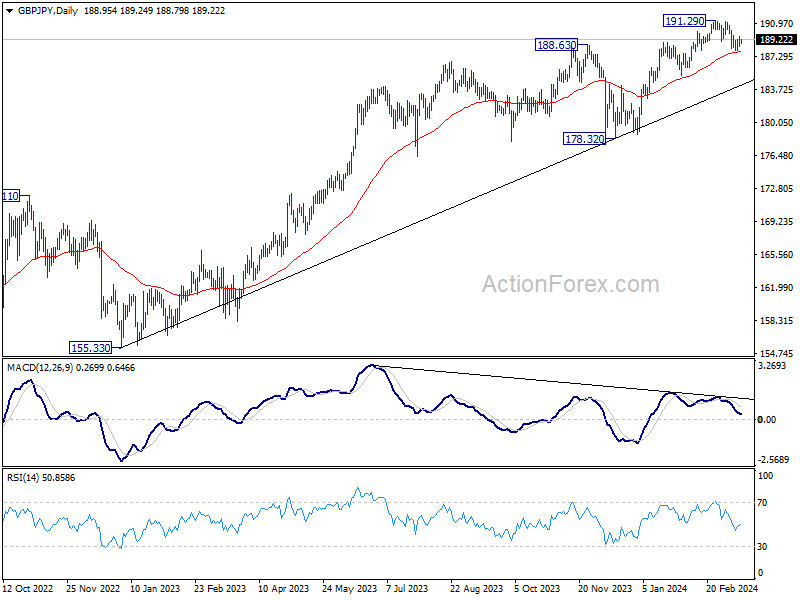

GBP/JPY Daily Outlook

Daily Pivots: (S1) 188.48; (P) 189.02; (R1) 189.61; More.....

Outlook in GBP/JPY remains unchanged and intraday bias stays neutral. On the downside, below 187.94 will resume the decline from 191.29 to 38.2% retracement of 178.32 to 191.29 at 186.33. Sustained break there will raise the chance of larger scale correction and target 61.8% retracement at 183.27. On the upside, though, firm break of 55 4H EMA (now at 189.29) will retain near term bullishness and bring retest of 191.29 high.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

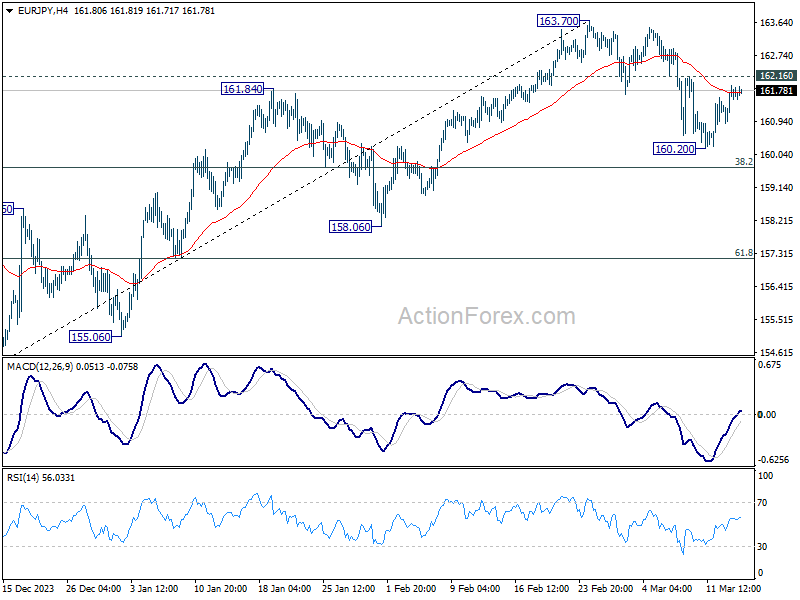

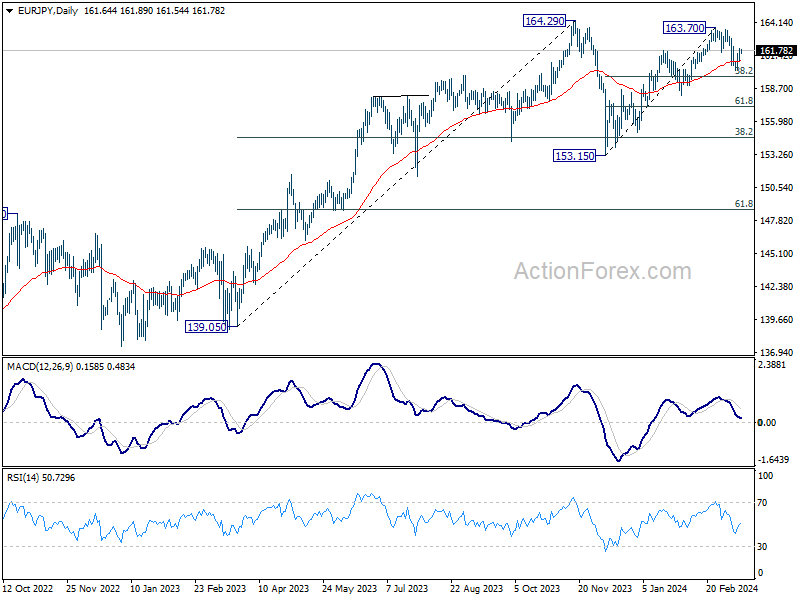

EUR/JPY Daily Outlook

Daily Pivots: (S1) 161.13; (P) 161.54; (R1) 162.18; More...

Intraday bias in EUR/JPY remains neutral and outlook is unchanged. On the downside, below 160.20 will resume the fall from 163.70 to 38.2% retracement of 153.15 to 163.70 at 159.66. Sustained break there will indicate that fall from 163.70 is reversing whole rise from 153.13, and target 61.8% retracement at 157.18. On the upside, though, above 162.16 minor resistance will retain near term bullishness, and bring retest of 163.70.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 which could still be extending. As long as 148.38 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage. Next target would be 169.96 (2008 high).

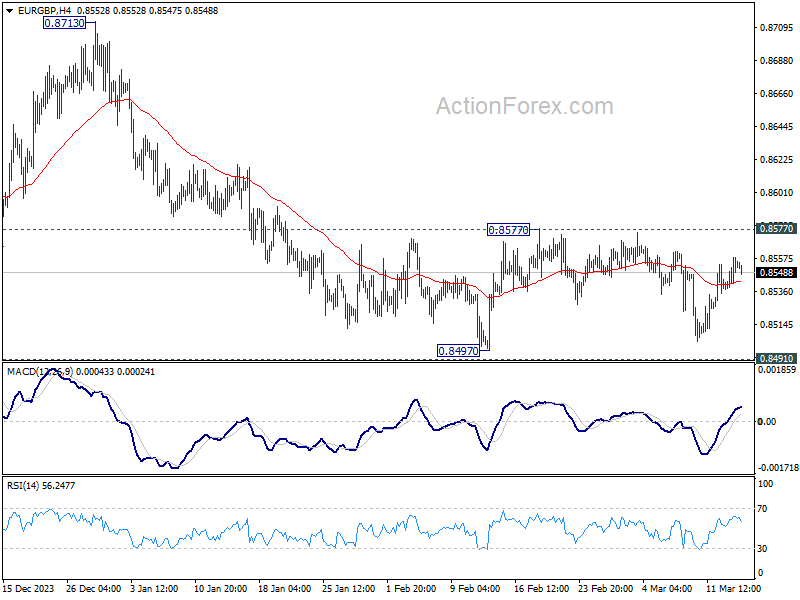

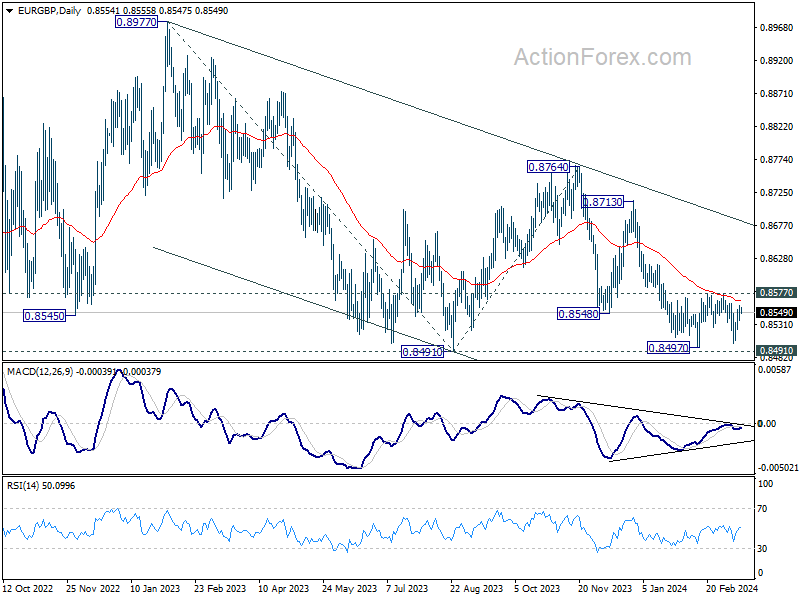

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8540; (P) 0.8550; (R1) 0.8565; More...

EUR/GBP is still bounded in range of 0.8497/8557 and intraday bias remains neutral. On the downside decisive break of 0.8491/7 support zone will confirm larger down trend resumption and target 0.8464 projection level first. Nevertheless, firm break of 0.8577 will turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

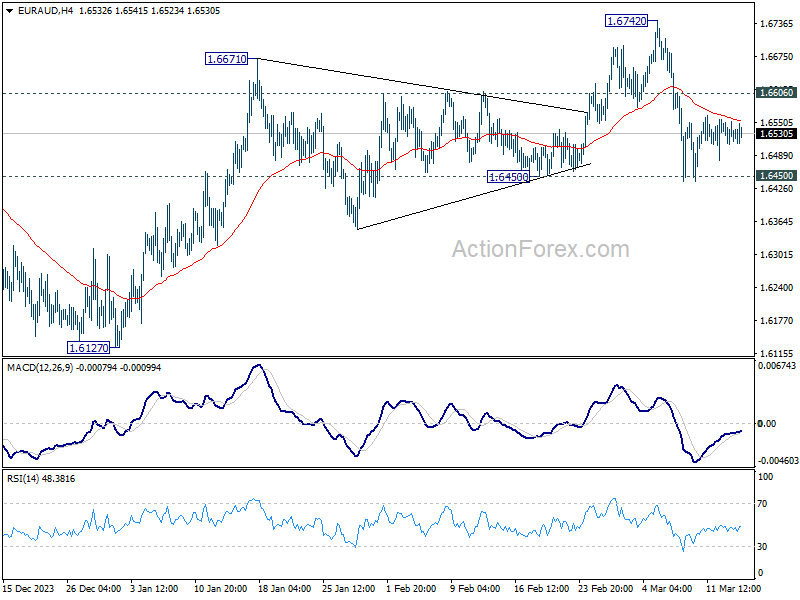

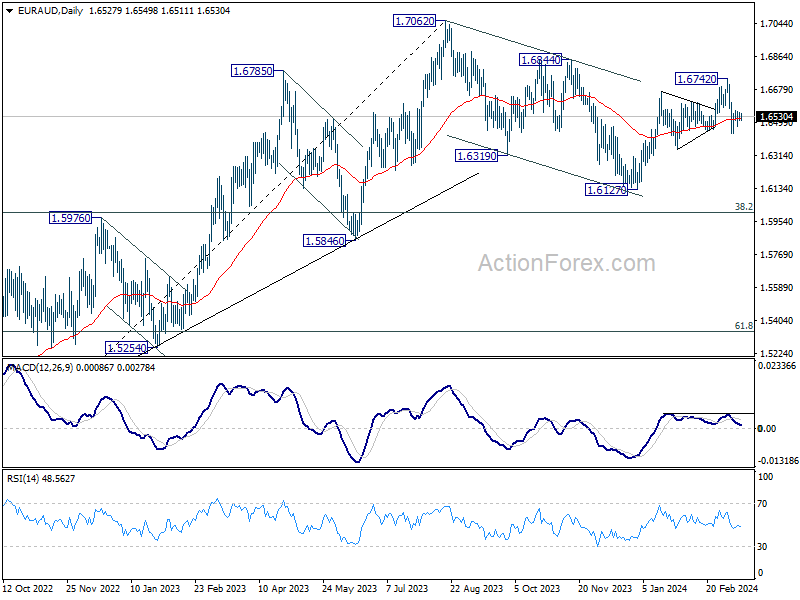

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6511; (P) 1.6536; (R1) 1.6559; More...

Range trading continues in EUR/AUD and intraday bias stays neutral at this point. On the downside, decisive break of 1.6450 support will argue that whole rebound from 1.6127 has completed with three waves up to 1.6742 already. Near term outlook will be turned bearish for 1.6127 again, to extend the whole corrective pattern from 1.7062. Nevertheless, strong rebound from current level, followed by break of 1.6606 minor resistance, will retain near term bullishness and bring retest of 1.6742.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

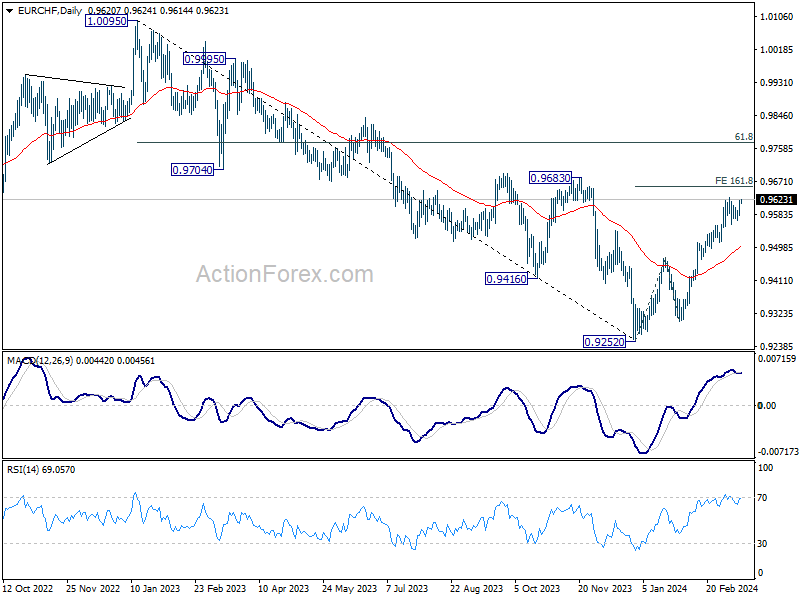

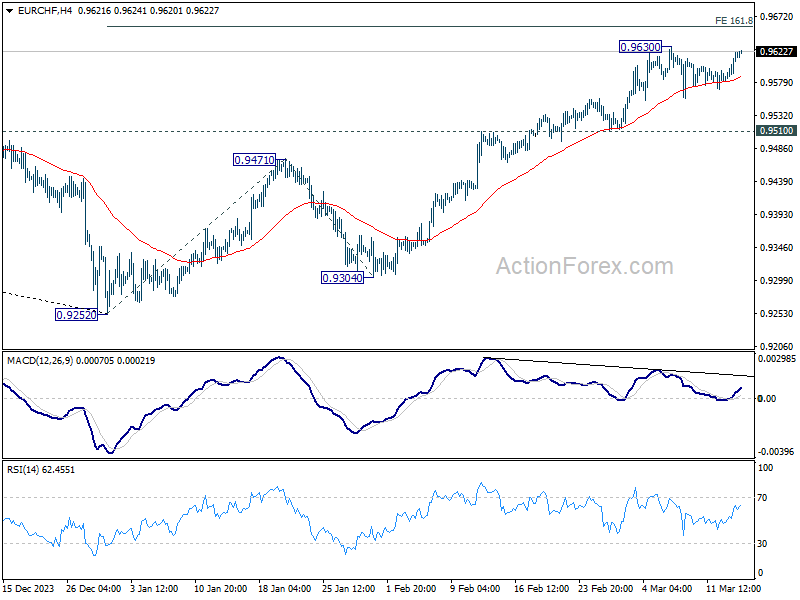

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9596; (P) 0.9610; (R1) 0.9635; More...

EUR/CHF is staying below 0.9630 despite today's recovery. Intraday bias remains neutral first. As long as 0.9510 support holds, further rally is still expected. On the upside, break of 0.9630 will resume the rise from 0.9252 and target 161.8% projection of 0.9252 to 0.9471 from 0.9304 at 0.9658 next. However, considering bearish divergence condition in 4H MACD, firm break of 0.9510 will turn bias back to the downside for deeper fall.

In the bigger picture, as long as 0.9683 resistance holds, rebound from 0.9252 are seen as a corrective move only. Larger down trend is expected to resume through 0.9252 after the correction completes. However, firm break of 0.9683 and sustained trading above 55 W EMA (now at 0.9620) will argue that 0.9252 is already a medium term bottom. Stronger rise would then be seen 61.8% retracement of 1.0095 to 0.9252 at 0.9773 and above.