Sample Category Title

Consolidation Persists Amid Indecision and Anticipation

Consolidative trading continues in the forex markets in general. There is little reaction to the batch of economic data released from there US. Comments from ECB officials were also largely ignored. For now, commodity currencies are the stronger ones for the week, as led by Canadian Dollar, while Euro is also firm. Sterling and Swiss Franc are on the softer side together with Yen. Dollar is mixed in the mixed. Despite these fluctuations, it's noteworthy that all major currency pairs and crosses have remained within last week's range, signaling a market characterized by indecision and anticipation.

This collective pause among traders and investors can be attributed to good reasons. The upcoming week is poised to be a pivotal one for global financial markets, with a slew of central banks, including BoJ, RBA, Fed, SNB, and BoE, all set to announce their monetary policy decisions. This upcoming "central bank bonanza" is expected to inject a significant dose of volatility and directional movement into the forex markets.

Particularly, BoJ's upcoming decision is garnering heightened attention, with speculation that the central bank may finally opt to raise interest rates, a move that could have far-reaching implications for Yen and broader market sentiment. Similarly, Fed's announcement is eagerly awaited, especially given that it will be accompanied by new economic projections and updated dot plots, which could provide fresh insights into the central bank's outlook on the economy and future policy oath.

In Europe, at the time of writing, FTSE is down -0.06%. DAX is up 0.22%. CAC is up 0.77%. UK 10-year yield is up 0.004 at 4.125. Germany 10-year yield is up 0.0181 at 2.385. Earlier in Asia, Nikkei rose 0.29%. Hong Kong HSI fell -0.71%. China Shanghai SSE fell -0.18%. Singapore Strait Times rose 0.81%. Japan 10-year JGB yield rose 0.0147 to 0.776.

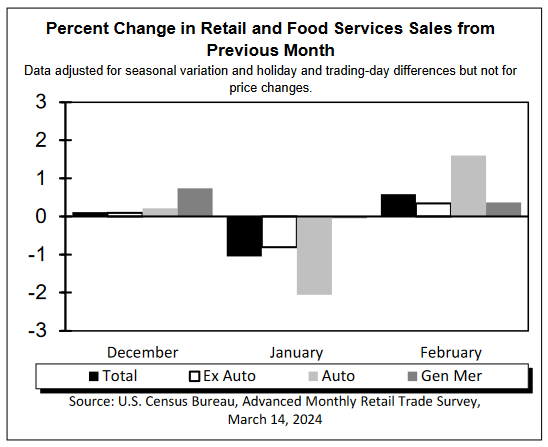

US retail sales rises 0.6% mom in Feb, ex-auto sales up 0.3% mom

US retail sales grew 0.6% mom to USD 700.7B in February, above expectation of 0.5% mom. Ex-auto sales rose 0.3% mom to USD 566.8B, below expectation of 0.4% mom. Ex-gasoline sales rose 0.6% mom to USD 647.7B. Ex-auto & gasoline sales rose 0.3% mom to USD 513.7B.

In the three months to February, sales were up 2.1% from the same period a year ago.

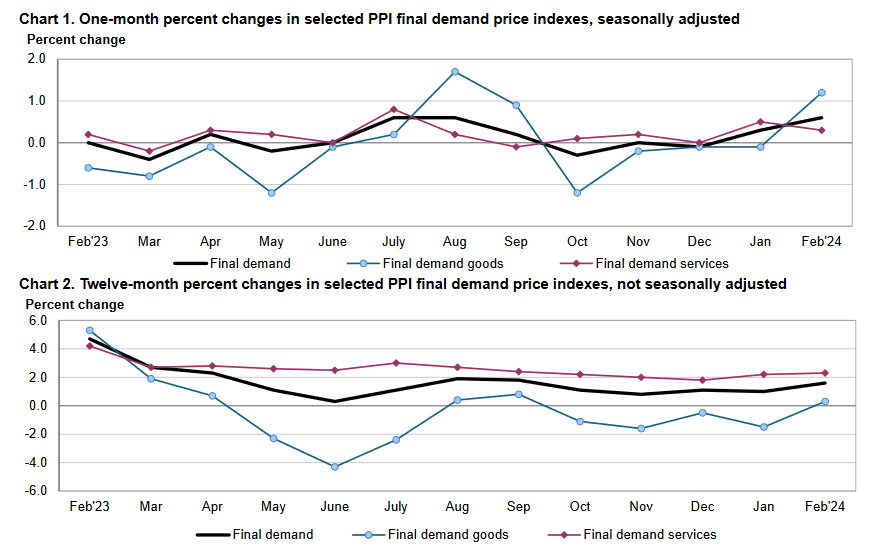

US PPI up 0.6% mom, 1.6% yoy in Feb

US PPI rose 0.6% mom in February above expectation of 0.3% mom. PPI goods rose 1.2% while PPI services rose 0.3% mom. PPI ex-food, energy and trade services rose 0.4% mom.

For the 12-month period, PPI rose 1.6% yoy, above expectation of 1.1% yoy. That's the highest level since September 2023. PPI ex-food, energy and trade services rose 2.8% yoy.

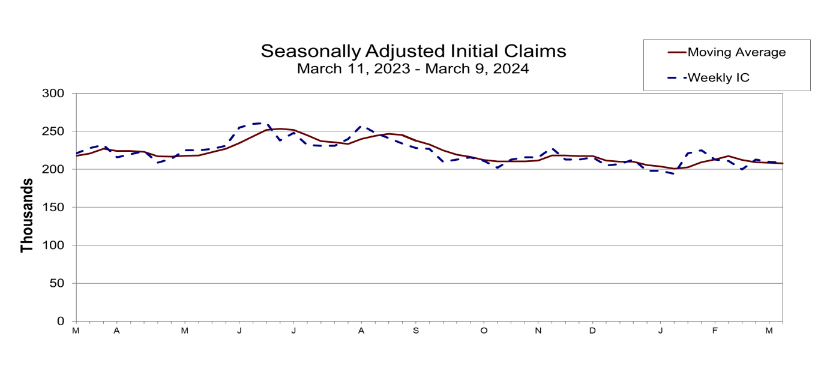

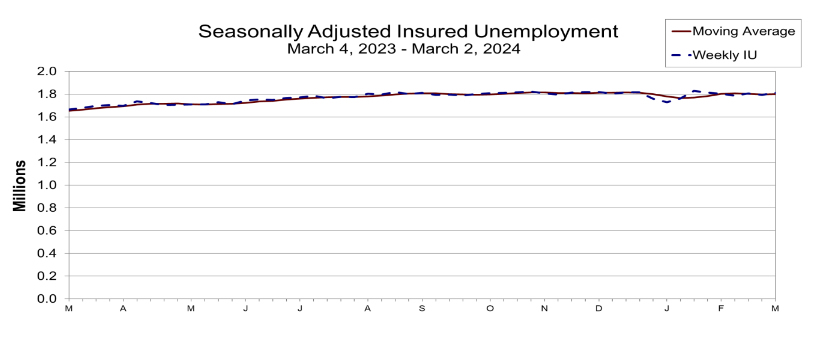

US initial jobless claims falls to 209k vs exp 218k

US initial jobless claims fell -1k to 209k in the week ending March 9, below expectation of 218k. Four-week moving average of initial claims fell -500 to 208k.

Continuing claims rose 17k to 1811k in the week ending March 2. Four-week moving average of continuing claims rose 2k to 1799k.

ECB's Knot pencils in for Jun rate cut, eyes Sep and Dec meetings too

ECB Governing Council member Klaas Knot told reporter today that he has "pencilled in June for a first rate cut". After that, Know said the subsequent path would be "data-dependent".

Highlighting the significance of ECB's meetings in September and December, which will include new economic projections, Knot positions these gatherings as crucial junctures for assessing and adjusting the bank's monetary policy strategy.

Moreover, Knot opens the door for action outside the traditional schedule of projection-inclusive meetings. "But if incoming data tells us we can do more, the interim meetings should also be available," he stated.

ECB's Stournaras advocates two rate cuts by summer break, four throughout the year

ECB Governing Council member Yannis Stournara, a known dove, proposed two rate reductions "before the summer break" and a total of four throughout the year. This strategy, he argues, is essential to ensure that ECB's monetary policy "does not become too restrictive" in the face of current economic challenges.

In an interview, Stournaras emphasizes the urgency of beginning these rate cuts soon, but not in April, as there will be "only little new information" available before then.

The rationale behind Stournaras's push for rate cuts stems from his observations on Eurozone's economy is "much weaker than expected," with risks skewed to the downside. Meanwhile, inflation, although significantly reduced, presents a balanced risk profile.

Addressing concerns about risk of "wage-price spiral," Stournaras argued that wages are merely "catching up, not leading inflation." He also highlights the moderating trend in nominal wage growth and the capacity of profits to absorb part of the pay increases, suggesting that fears of a wage-driven inflationary loop may be overstated.

Looking ahead, Stournaras envisions the deposit rate gradually decreasing to 2% by the end of 2025 or the beginning of 2026. However, he draws a line at this level, suggesting that rates should not fall below the pre-pandemic levels of 2%.

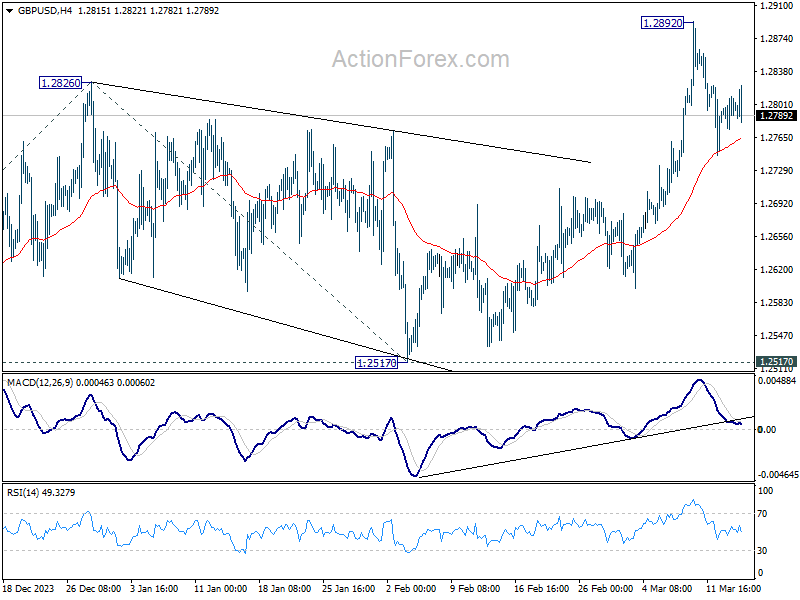

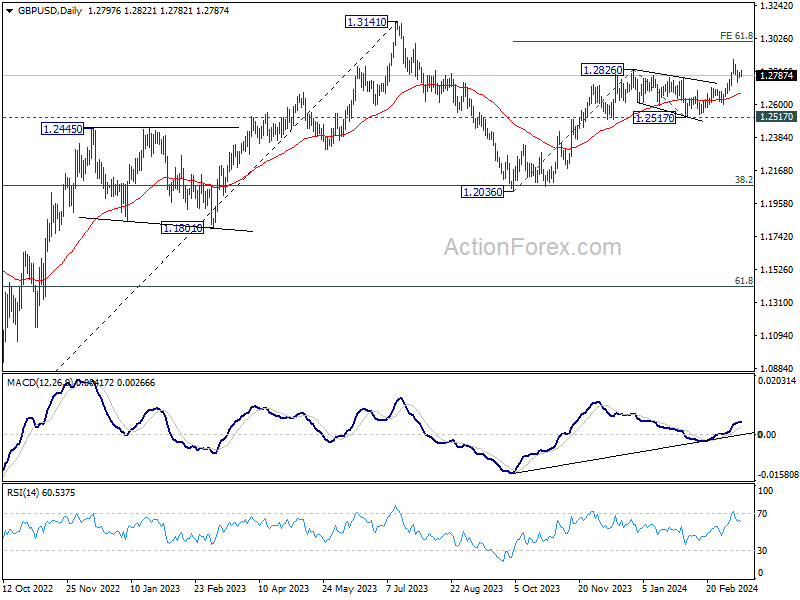

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2778; (P) 1.2794; (R1) 1.2814; More...

Intraday bias in GBP/USD remains neutral and outlook is unchanged. Further rally will remain in favor as long as 55 4H EMA (now at 1.2764) holds. On the upside, above 1.2892 will resume larger rise from 1.2063 and target 61.8% projection of 1.2036 to 1.2826 from 1.2517 at 1.3005. However, sustained break of 55 4H EMA will bring deeper fall back towards 55 D EMA (now at 1.2672), and possibly further to 1.2517 structural support.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which is still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:01 | GBP | RICS Housing Price Balance Feb | -10% | -10% | -18% | |

| 07:30 | CHF | PPI M/M Feb | 0.10% | 0.20% | -0.50% | |

| 07:30 | CHF | PPI Y/Y Feb | -2.00% | -2.30% | ||

| 12:30 | CAD | Manufacturing Sales M/M Jan | 0.20% | 0.30% | -0.70% | |

| 12:30 | USD | Retail Sales M/M Feb | 0.60% | 0.50% | -0.80% | |

| 12:30 | USD | Retail Sales ex Autos M/M Feb | 0.30% | 0.40% | -0.60% | |

| 12:30 | USD | PPI M/M Feb | 0.60% | 0.30% | 0.30% | |

| 12:30 | USD | PPI Y/Y Feb | 1.60% | 1.10% | 0.90% | 1.00% |

| 12:30 | USD | PPI Core M/M Feb | 0.30% | 0.20% | 0.50% | |

| 12:30 | USD | PPI Core Y/Y Feb | 2.00% | 2.00% | 2.00% | |

| 12:30 | USD | Initial Jobless Claims (Mar 8) | 209K | 218K | 217K | 210K |

| 14:00 | USD | Business Inventories Jan | 0.30% | 0.40% | ||

| 14:30 | USD | Natural Gas Storage | -3B | -40B |

US initial jobless claims falls to 209k vs exp 218k

US initial jobless claims fell -1k to 209k in the week ending March 9, below expectation of 218k. Four-week moving average of initial claims fell -500 to 208k.

Continuing claims rose 17k to 1811k in the week ending March 2. Four-week moving average of continuing claims rose 2k to 1799k.

US PPI up 0.6% mom, 1.6% yoy in Feb

US PPI rose 0.6% mom in February above expectation of 0.3% mom. PPI goods rose 1.2% while PPI services rose 0.3% mom. PPI ex-food, energy and trade services rose 0.4% mom.

For the 12-month period, PPI rose 1.6% yoy, above expectation of 1.1% yoy. That's the highest level since September 2023. PPI ex-food, energy and trade services rose 2.8% yoy.

US retail sales rises 0.6% mom in Feb, ex-auto sales up 0.3% mom

US retail sales grew 0.6% mom to USD 700.7B in February, above expectation of 0.5% mom. Ex-auto sales rose 0.3% mom to USD 566.8B, below expecetation of 0.4% mom. Ex-gasoline sales rose 0.6% mom to USD 647.7B. Ex-auto & gasoline sales rose 0.3% mom to USD 513.7B.

In the three months to February, sales were up 2.1% from the same period a year ago.

ECB’s Knot pencils in for Jun rate cut, eyes Sep and Dec meetings too

ECB Governing Council member Klaas Knot told reporter today that he has "pencilled in June for a first rate cut". After that, Know said the subsequent path would be "data-dependent".

Highlighting the significance of ECB's meetings in September and December, which will include new economic projections, Knot positions these gatherings as crucial junctures for assessing and adjusting the bank's monetary policy strategy.

Moreover, Knot opens the door for action outside the traditional schedule of projection-inclusive meetings. "But if incoming data tells us we can do more, the interim meetings should also be available," he stated.

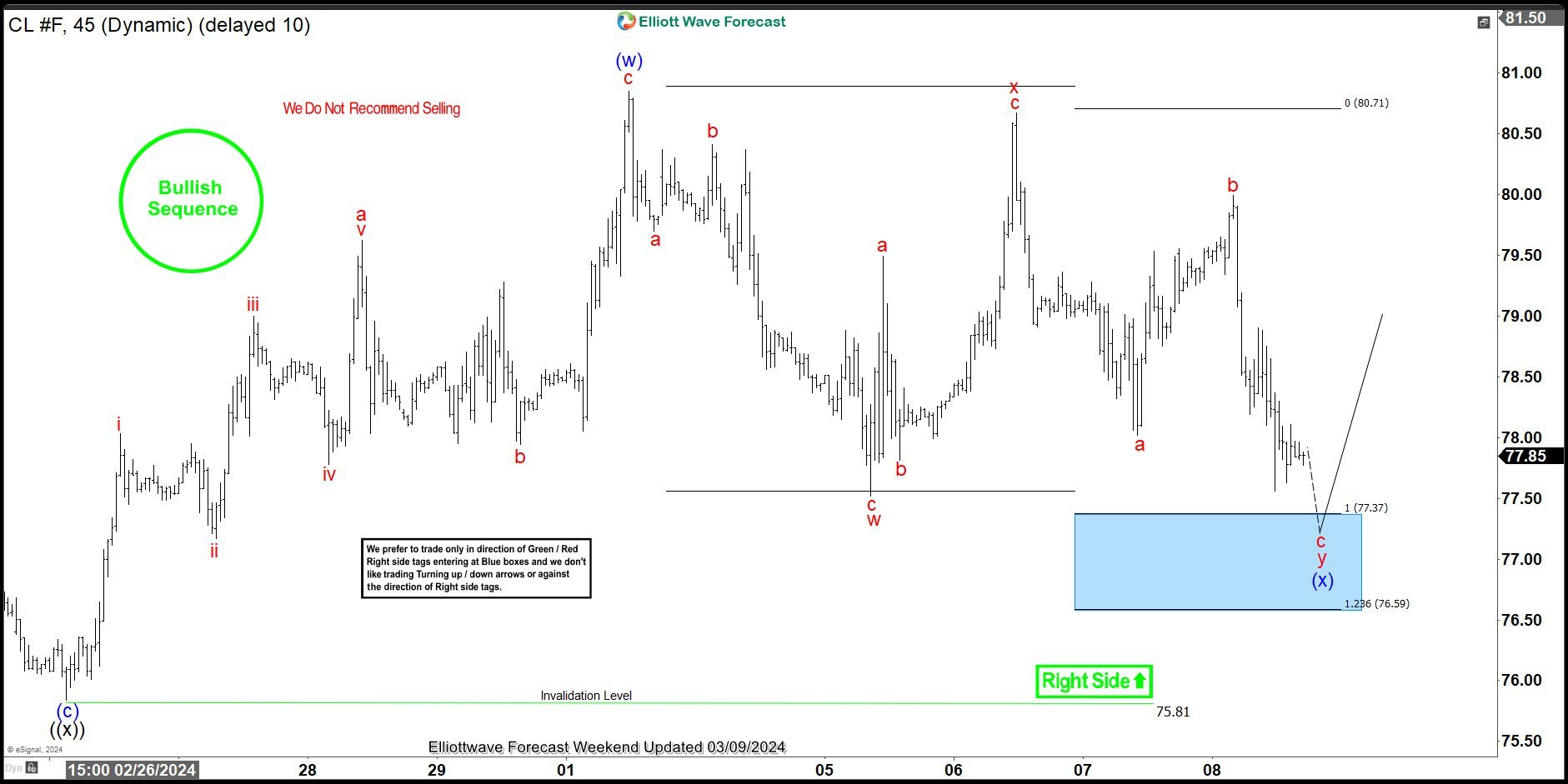

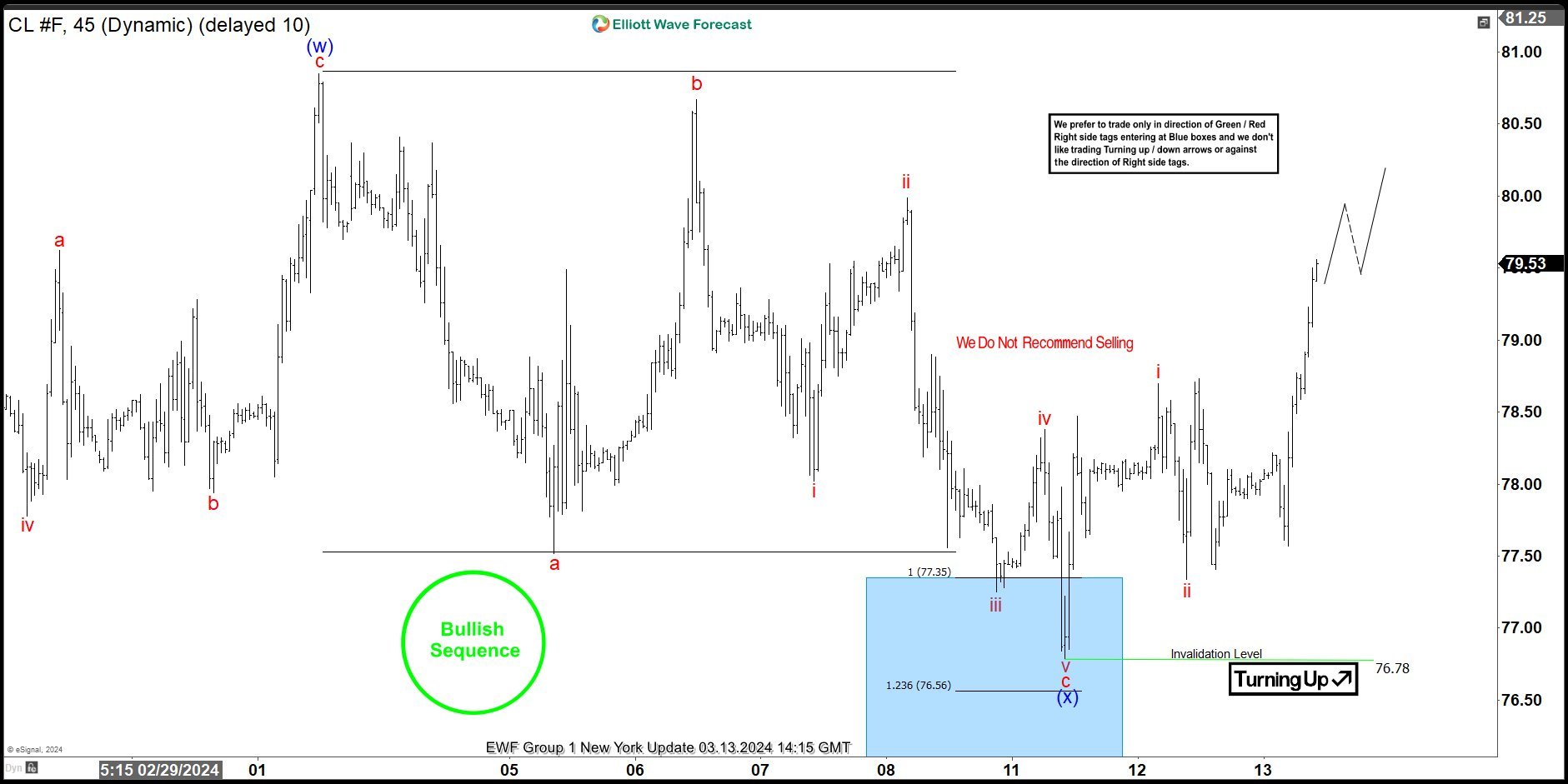

OIL (CL_F) Elliott Wave: Buying The Dips At The Blue Box

Hello fellow traders. As our members know , Oil has recently given us good buying opportunity . In this technical article we’re going to look at the Elliott Wave charts of Oil published in members area of the website. The commodity shows bullish sequences in the cycle from the 67.75 low. Consequently we have been favoring the long side and recommended members to keep buying the dips in 3,7,11 swings. Oil made clear 3 waves down from the March 1st peak and completed correction right at the Equal Legs zone ( Blue Box Area) . In further text we’re going to explain the Elliott Wave pattern and trading setup.

OIL Elliott Wave 1 Hour Chart 03.09.2024

Current view suggests that wave (x) pull back is still in progress , calling for more short term weakness toward 77.37-76.59 area. We don’t recommend selling Oil and prefer the long side from the marked Blue Box ( buying zone). As the main trend is bullish, we expect the price to make at least bounce in 3 waves from the Blue Box area. Once the bounce reaches 50 fibs against the x red connector we will take partial profits and make position risk free ( put SL at BE) .

Official trading strategy on How to trade 3, 7, or 11 swing and equal leg is explained in details in Educational Video, available for members viewing inside the membership area.

Quick reminder on how to trade our charts :

Red bearish stamp+ blue box = Selling Setup

Green bullish stamp+ blue box = Buying Setup

Charts with Black stamps are not tradable. 🚫

OIL Elliott Wave 1 Hour Chart 03.13.2024

The commodity reached our buying zone at : 77.35-76.56 and found buyers as expected. Oil is giving us very good reaction from the Blue Box Area. We call pull back (x) blue completed at the 76.78 low. As a result, any long positions should be risk free by now. We would like to see break of (w) blue peak (March 1st) to confirm next leg up is in progress.

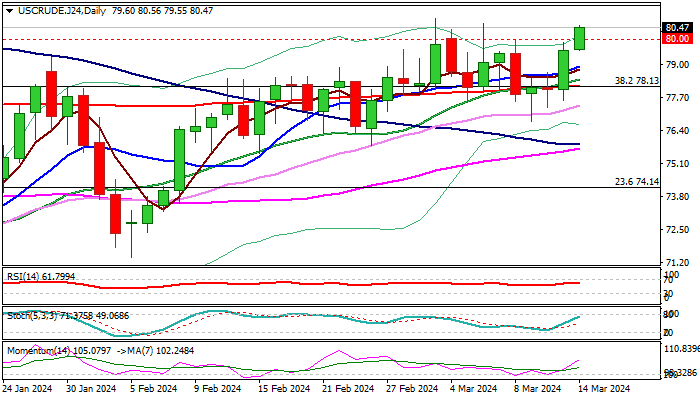

WTI: Oil Prices Continue to Rise on Brighter Demand Outlook

WTI oil price rose further on Thursday, extending gains above psychological $80 barrier and looking for the first daily close above this level since Nov 6.

Near-term bullish sentiment improved after the latest International Energy Agency’s report showed an upward revision to demand growth forecasts and cut in 2024 supply forecast.

The data brightened oil’s near-term outlook and provided fresh tailwind to oil’s prices which rally for the second consecutive day and pressure key barriers at $80.83/$81.3 (2024 high od Mar 1 / 50% retracement of $95.00/$67.70 downtrend).

Technical studies on daily chart show strengthening positive momentum and moving averages in full bullish setup, which adds to bullish outlook.

Daily close above $80 to generate initial bullish signal, with sustained break above $80.83/$81.35 to confirm bullish continuation and unmask target at $84.57 (Fibo 61.8%).

Broken $80 level now offers immediate support, with dips to ideally find ground above rising 10DMA ($78.91).

Caution on failure to close above $80 which would signal extended sideways mode.

Res: 80.83; 81.35; 82.00; 82.21.

Sup: 80.00; 79.55; 78.91; 78.20.

Canadian Dollar Seeks Opportunities for Growth

The USDCAD pair remains within a sideways range, with the Canadian dollar occasionally showing a tendency to strengthen.

Recent DES data revealed that Canadian households have become more affluent. In Q4 2023, their "net" worth increased by 1.8%, or 300 billion Canadian dollars, smoothing out the decline seen in the previous quarter.

This increase can be attributed to the recovery in financial market returns, as both stocks and bonds appreciated during the period. This dynamic compensated for the "modest" decline in the country's housing market value. Overall, Canadians became 712.7 billion CAD richer in 2023 than they were the previous year.

Borrowing rates in Q4 of last year increased for the second consecutive quarter, with households attracting 29.5 billion CAD, primarily in mortgage loans, followed by consumer loans. These figures raise concerns, suggesting that some households may become more indebted than others. Canada's economy's loan debt is currently estimated at 2.9 trillion CAD, with three-quarters of these debts being mortgage loans. However, in the economic context, household debt as a percentage of Canadians' disposable income accounts for 178.7% in Q4, slightly lower than in Q3 of last year and the lowest level since the end of 2015. Thus, while debts exist, the overall picture is relatively stable.

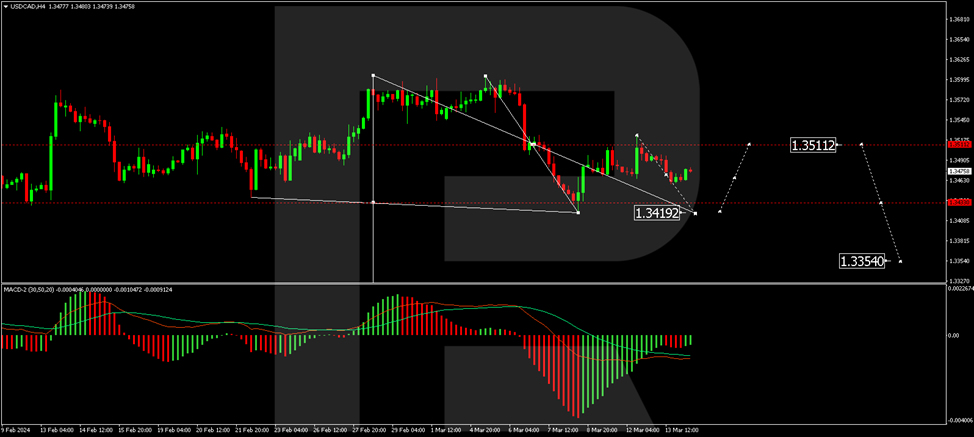

USDCAD technical analysis

On the H4 chart of USDCAD, a declining wave is forming towards 1.3403. Today, we are considering the development of its fifth structure. After reaching the target level, a correction to 1.3511 is possible. Subsequently, we expect the beginning of a new declining structure towards the local target of 1.3354. This scenario is confirmed by the MACD indicator, whose signal line is below the zero mark and heading strictly downward towards new lows.

On the USDCAD H1 chart, the first structure of the fifth declining wave has been completed. Today, we are considering the possibility of a correction to 1.3488. After its completion, we expect a decline to 1.3454, then a rise to 1.3471 (testing from below), and then a decline to 1.3420. This is the first target. The stochastic oscillator, with its signal line above the 80 mark and preparing to drop to 20, also confirms this scenario.

US DJIA Technical: Bullish Breakout Ahoy

- In the past five days, the year-to-date laggard Dow Jones Industrial Average (DJIA) has played a positive catch-up.

- On a rolling 5-day performance basis, the DJIA has outperformed with a gain of +1.10% over the Nasdaq 100’s loss of -0.70% due to recent softness seen in the share price of Nvidia.

- Watch the key short-term support of 38,930.

On a year-to-date performance basis as of 13 March 2024, the Nasdaq 100 has managed to record a gain of 8.3% that surpassed the return of the Dow Jones Industrial Average of +3.50%.

Interestingly, in the past five days (5-day rolling basis as of 13 March), the laggard Dow Jones Industrial Average has started to play a catch-with with a return of +1.10% that overtook the Nasdaq 100’s loss of -0.70%.

The primary attribution to the current short-term outperformance of the Dow Jones Industrial Average over the Nasdaq 100 has been the lacklustre performance of the Artificial Intelligence (AI) theme play leader, Nvidia (third largest component market cap weightage stock in Nasdaq 100) where its share price has shed -5.6% over the same period.

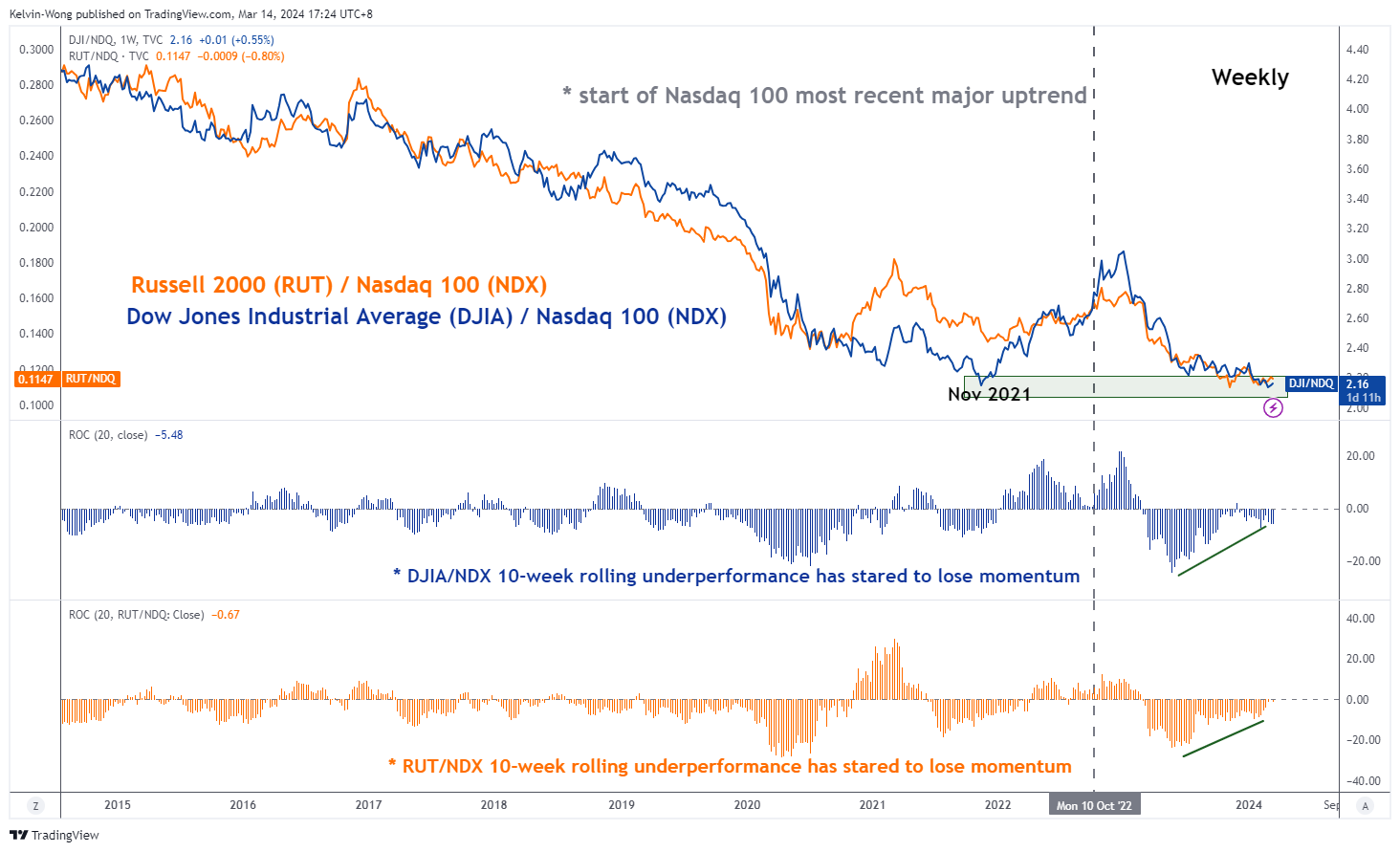

Potential major bullish basing condition in ratio chart of DJIA/NDX

Fig 1: Ratio charts of DJIA & Russell 200 over Nasdaq 100 as of 14 Mar 2024 (Source: TradingView, click to enlarge chart)

The ratio chart of the Dow Jones Industrial Average (DJIA) over the Nasdaq 100 has started to form a potential major basing formation by not breaking below its prior significant November 2021 swing low (see Fig 1).

Also, its 10-week rolling underperformance measured by the ratio’s rate of change has continued to display a bullish divergence condition which suggests a potential looming major outperformance of DJIA over the Nasdaq 100.

Price actions cleared above 20-day moving average

Fig 2: US Wall St 30 short-term trend as of 14 Mar 2024 (Source: TradingView, click to enlarge chart)

Yesterday, 13 March’s price actions movement of the US Wall St 30 Index (a proxy of the Dow Jones Industrial Average futures) staged a bullish breakout from its prior choppy minor range configuration in place since 23 February (see Fig 2).

In addition, the Index has also surpassed the 20-day moving average which suggests the potential revival of bullish momentum at least in the near-term horizon.

If the 38,930 short-term pivotal support holds, the Index may continue to shape “higher highs” for the next intermediate resistances to come in at 39,400 and 39,610 (also the upper boundary of the minor ascending channel from 14 February 2024 low).

On the flip side, a break below 38,930 negates the bullish tone for another round of choppy minor corrective decline that may expose the next intermediate supports at 38,660 and 38,380 (also the upward-sloping 50-day moving average).

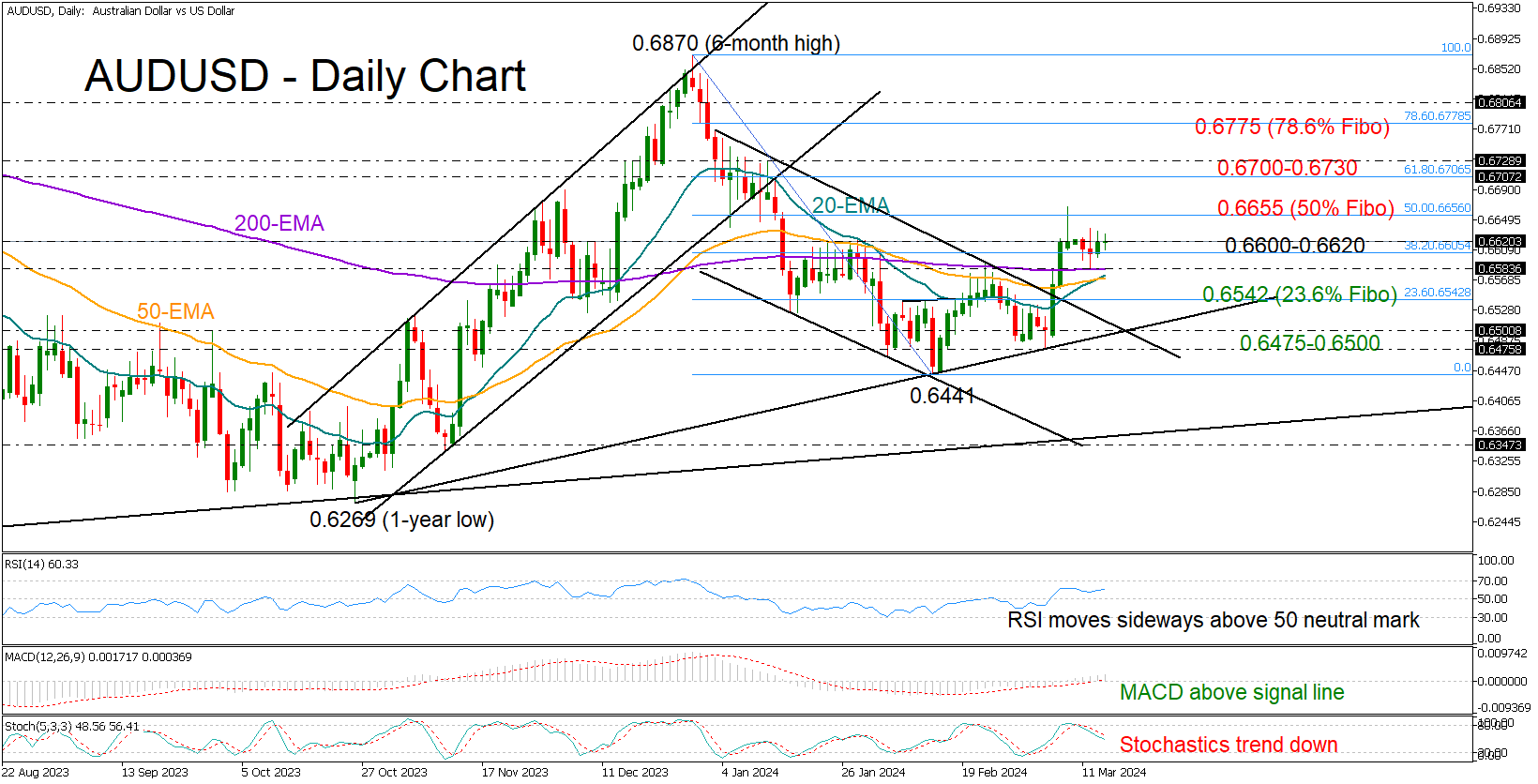

AUDUSD Waits for Direction After Bullish Break

- AUDUSD squeezed between key levels

- Traders indecisive ahead of US retail sales

AUDUSD regained positive momentum and climbed above its exponential moving averages (EMAs) after breaking out of its 2024 bearich channel. But the 0.6620 region, which was a tough barrier in January, dented the upside forces following the flash spike to 0.6666.

The technical indicators are sending mixed signals, though the nearby support area of 0.6600, which has been limiting downside movements, is preserving a ray of hope that the ongoing tight consolidation phase might develop to the upside.

A close above 0.6620 could help the price to reach the 50% Fibonacci mark of 0.6655 and then stretch towards the 61.8% Fibonacci of 0.6706 and the 0.6730 resistance. Additional gains from there are expected to pick up steam towards the 0.6770 barrier.

Should the price dip below the 38.2% Fibonacci level of 0.6600 and the EMAs, it may find immediate support at the 23.6% Fibonacci mark of 0.6542, thus preventing a decline towards the ascending trendline from October at 0.6500. If the bears claim the March low of 0.6476 too, the door will open for the February trough of 0.6441.

All in all, AUDUSD is within a tight neutral territory, waiting for a clear close above 0.6620 or below 0.6583 to get a new direction.