Sample Category Title

EUR/USD Hits 8-Week High

The euro is trading above USD 1.09, hitting its strongest point since mid-January on Friday, helped by news from both the US and Europe.

Friday's news showed that the US labor market is weakening:

→ The change in employment in the non-farm sector showed an increase in jobs = 275k for the month, although last month it was = +353k.

→ The unemployment rate rose to 3.9%, although it was 3.7% for 3 months.

News of a weakening labour market could put pressure on the Fed to ease monetary policy.

Meanwhile in Europe, the ECB kept borrowing costs at a record high, citing significant progress in containing inflation, and revised its inflation expectations downward, forecasting price growth of 2.3% in 2024, and 1.9% in 2025. And during a press conference last Thursday, ECB President Lagarde told reporters that policymakers had not discussed rate cuts at that meeting.

Thus, there is reason to believe that the Fed will start lowering rates earlier (it started raising them earlier than the ECB). And this assumption is shared by many market participants, judging by the bullish dynamics in the EUR/USD market.

Today's chart shows:

→ the price of EUR/USD has been moving within an ascending channel (shown in blue) since mid-February. Moreover, it seems that the median line acts as resistance — Friday’s peak indicates this;

→ the price rose to the important psychological level of 1.1000 – it served as resistance in January;

→ the RSI indicator is in the overbought zone, forming a bearish divergence.

If there is some correction this week after an increase of more than 0.9% last week, then the price of EUR/USD may fall to its lower limit. Failure of the bulls to resume the uptrend from this line could mark the prospect of a decline in price towards the important support of 1.0870.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

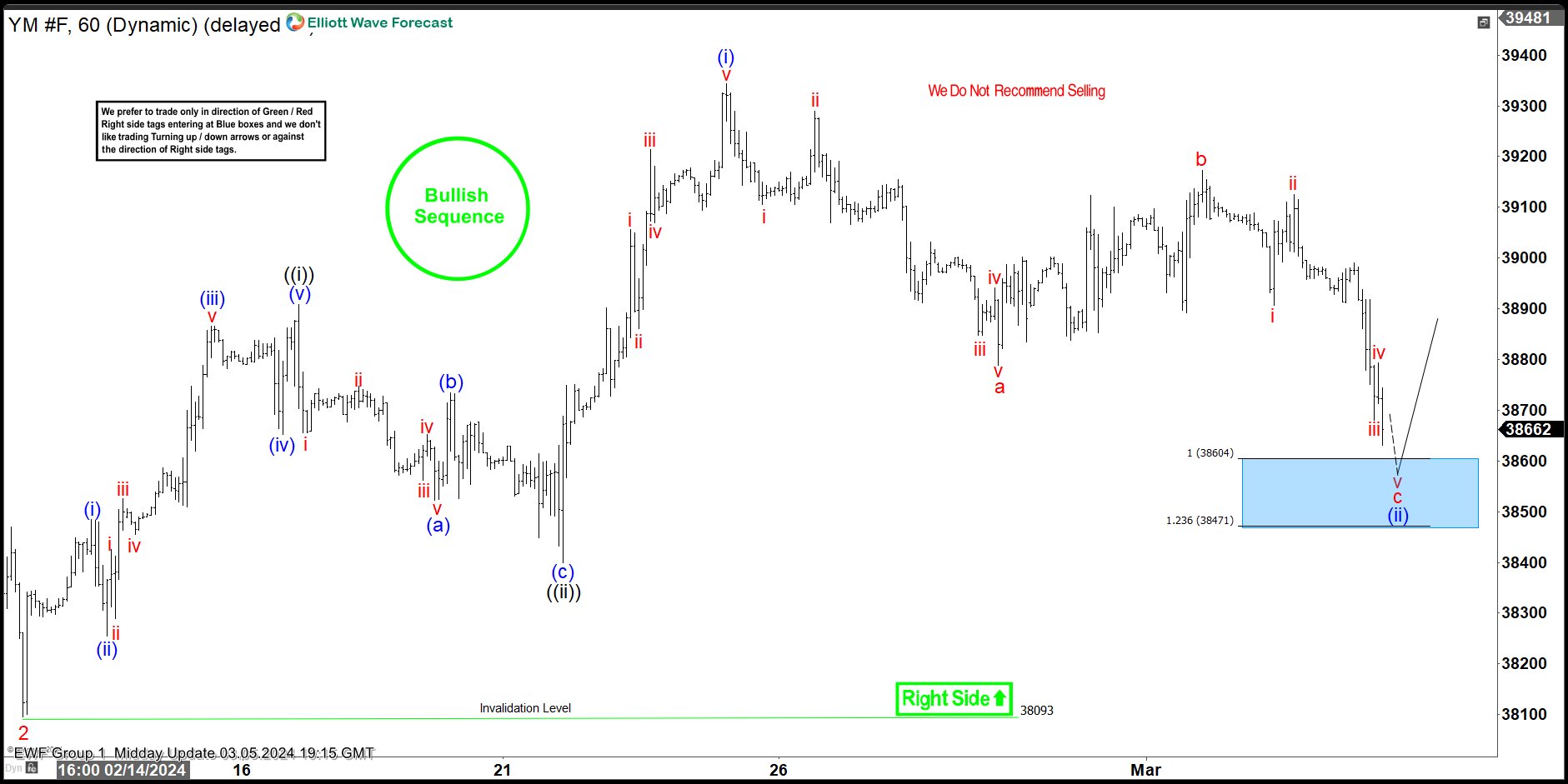

Dow Futures (YM_F) : Buying The Dips At The Blue Box Area

Hello fellow traders. In this technical article we’re going to take a look at the Elliott Wave charts charts of Dow Jones Futures published in members area of the website. As our members know YM_F has recently made pull back that has unfolded as Elliott Wave Zig Zag pattern. It made clear 3 waves down from the February 23rd peak and completed correction right at the Equal Legs zone ( Blue Box -Buying Area) . In further text we’re going to explain the Elliott Wave pattern and trading setup.

YM_F Elliott Wave 1 Hour Chart 03.05.2024

Dow Jones Futures is showing lower low structure from the peak. Correction has a b c labeling, when we can still be in c red leg. The price structure is incomplete at the moment, calling for a more downside in near term toward : 38604-38471 buying zone. We don’t recommend selling YM_F and prefer the long side from the marked Blue Box ( buying zone). Once Dow Jones reaches our buying area, it should ideally make either rally toward new highs or in 3 waves bounce alternatively. Once bounce reaches 50 Fibs against the b red high, we will make long position risk free ( put SL at BE) and take partial profits.

Official trading strategy on How to trade 3, 7, or 11 swing and equal leg is explained in details in Educational Video, available for members viewing inside the membership area.

Quick reminder on how to trade our charts :

Red bearish stamp+ blue box = Selling Setup

Green bullish stamp+ blue box = Buying Setup

Charts with Black stamps are not tradable. 🚫

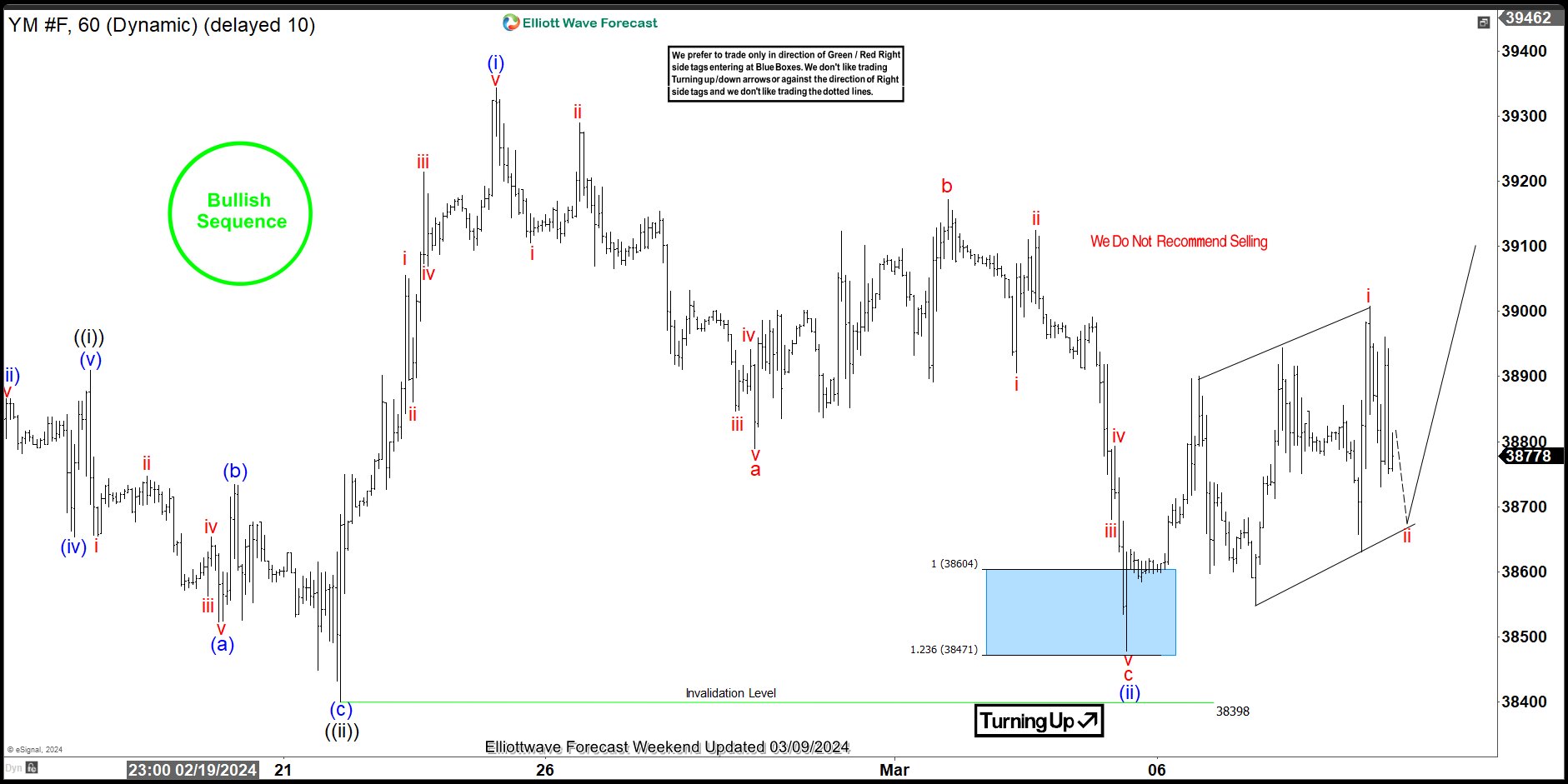

YM_F Elliott Wave 1 Hour Chart 03.09.2024

Dow Jones made extension toward our buying zone at : 38604 – 38471 as we expected. YM_F found buyers at the blue box and we are getting good reaction from there. Consequently, any long positions from the equal legs area should be risk free by now. As far as the price stays above 38473 low, we can see further strength in Dow Jones toward new highs ideally.

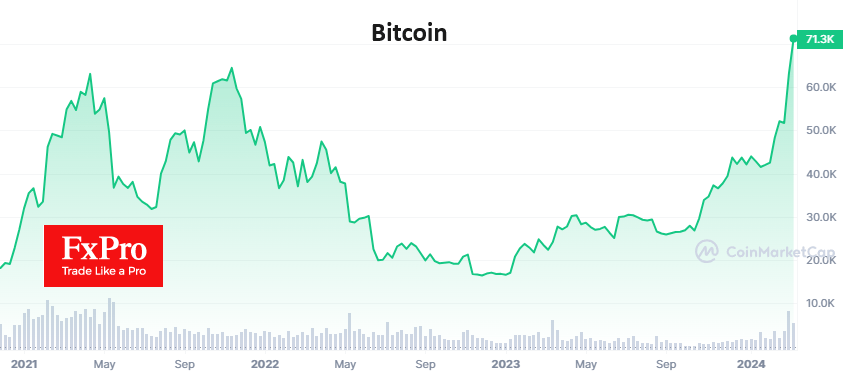

Bitcoin’s New Highs and BNB’s Revival

Market picture

Bitcoin’s record highs support the accelerated recovery of the crypto market. Its capitalisation reached $2.69 trillion (+1.6% in 24 hours), 10% below the record high of $2.97 trillion in November 2021. Extreme greed remains the driver of the crypto market, but major coins are getting the main influx of money.

Bitcoin hit an all-time high of $71.5K early Monday afternoon, adding 2.5% in 24 hours. Ethereum is rising with the market, adding 1.4% in the same time frame and breaking the $4000 price.

The surge in trading activity has helped to revitalise BNB, which is adding over 4% for the day. It has gained 25% in 7 days, twice that of Ethereum and three times ahead of Bitcoin during this interval. However, like Ether, it is about 15% away from the record highs of late 2021.

News background

BlackRock’s spot BTC-ETF iShares Bitcoin Trust (IBIT) managed to accumulate almost 200,000 bitcoins in two months, becoming one of the largest holders of BTC in the world and surpassing MicroStrategy, which has 193,000 BTC on its balance sheet.

According to The Block, investors have built up a substantial volume of open positions with an expiry price of $70K on Bitcoin call options redeemable on 29 March. Bets on BTC rising to $80K over the next three weeks have also increased.

According to Bloomberg data, bitcoin miners set a monthly record for energy consumption. They consumed a record 19.6 GW of electricity in February, up from 12.1 GW in the same period a year earlier. The rise in BTC has prompted mining companies to spend more than $1bn on new equipment over the year.

A US federal appeals court has resumed hearings on a lawsuit filed by a group of investors against Binance. The investors accuse the trading platform of violating US securities laws by selling unregistered tokens.

Billionaire Mark Cuban said he has always invested in Bitcoin because of its limited supply, which could be the driver of the first cryptocurrency’s bull rally. He believes demand for BTC will outstrip supply as more and more people buy bitcoin and fewer sell.

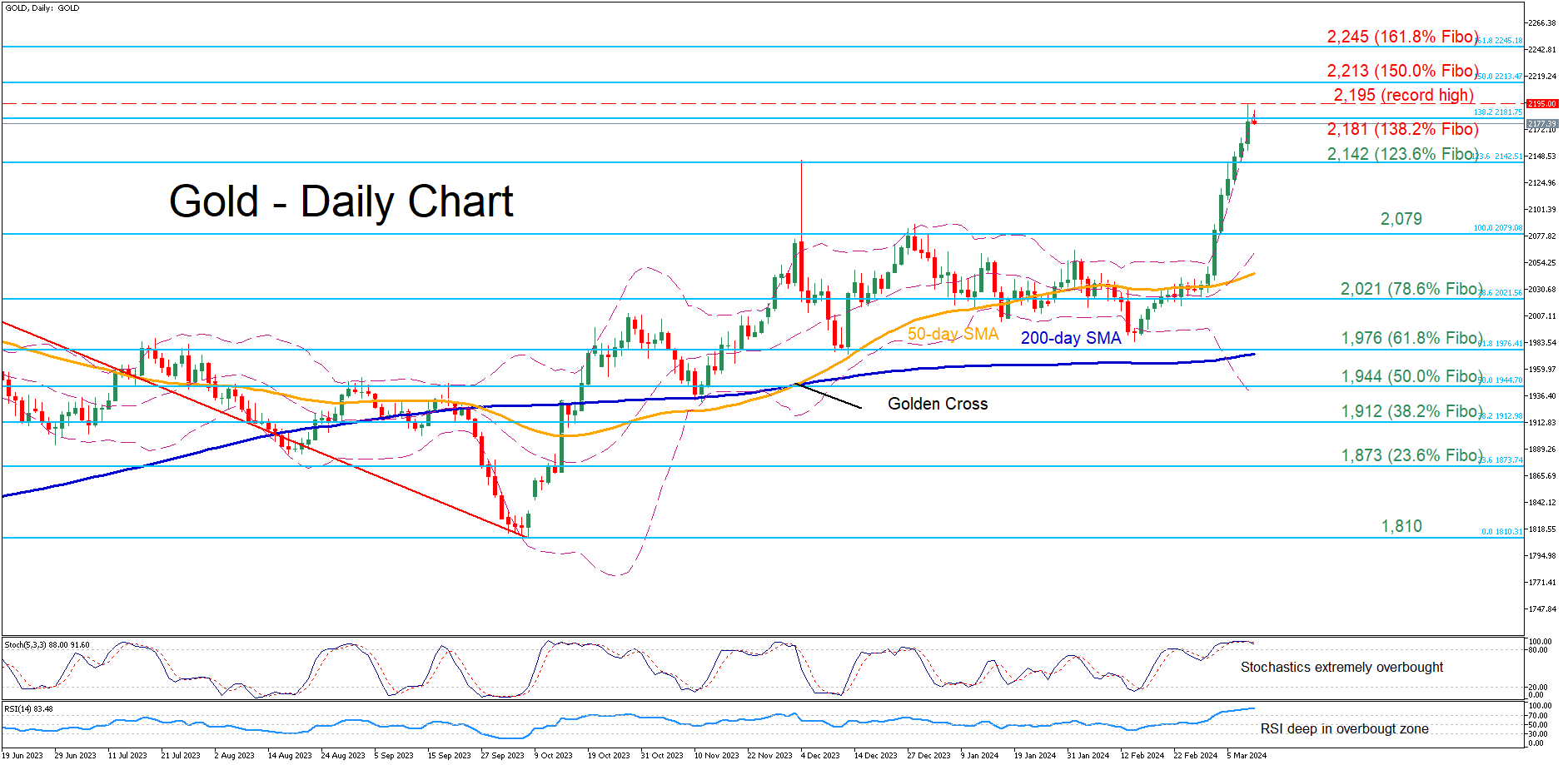

Gold Marches to Consecutive All-Time Highs

- Gold advances sharply after claiming 50-day SMA

- Generates consecutive record highs in recent sessions

- Momentum indicators flag overbought conditions

Gold has been in a steep uptrend following its profound break above the 50-day simple moving average (SMA), posting a barrage of fresh all-time highs in the past few sessions. However, traders should not rule out a pullback as the momentum indicators have been in their overbought zones for more than a week.

Should bullish pressures persist, bullion could initially claim 2,181, which is the 138.2% Fibonacci extension of the 2,079-1,810 downleg. Jumping above that region, the price may revisit its all-time high of 2,195. A violation of that zone could pave the way for the 150.0% Fibo of 2,213.

Alternatively, if gold experiences a mild correction, the 123.6% Fibo of 2,142 could act as the first line of defence. Further declines could then come to a halt at the previous resistance of 2,079, which held strong both in April and December 2023. Even lower, the 78.6% Fibo of 2,021 might provide downside protection.

In brief, gold has exploded in the short-term, surging to consecutive all-time highs amid heightened volatility. Nevertheless, there are emerging signs that the advance could be overdone as the short-term oscillators are deep in their overbought territories.

US 500 Cash Index in the Red Again

- US 500 index trades lower after recording a new all-time high

- The pace of the rally remains aggressive but euphoria dominates

- Bears continue to closely monitor the stochastic oscillator’s movements

The US 500 cash index is edging lower again today after recording a new all-time high of 5,189 last week. Friday’s mixed US labour market data do not appear to have dented the market’s bullish appetite but some profit taking has clearly taken place. Having said that, the pace of the rally since the trough low at 4,100 remains aggressive as made evident by the October 27, 2023 ascending trendline being respected by the US 500 price action.

With the momentum indicators not sending strong bearish signals, the current bullish trend is assumed to be still in place. In more detail, the RSI is trading sideways, but it has completed four months of comfortably hovering above its 50-midpoint. More importantly, the stochastic oscillator is apparently trying to break below its overbought (OB) area. Should it finally manage to record this move, it would be seen as a strong bearish signal. In the meantime, the Average Directional Movement Index (ADX) is uninterested in the recent moves and remains in range-trading territory.

The bears are desperately trying to retake market control and to push the US 500 index below both the October 27, 2023 ascending trendline and the 5,000 threshold. If successful, they could then have a go at testing the support set by the 4,936-4,976 range, which is populated by the 50-day simple moving average (SMA) and the February 2, 2024 high. Even lower, the January 4, 2022 high at 4,818 could prove stronger to overcome than currently anticipated.

On the flip side, the bulls remain confident and might prepare for new record-high levels. They could first try to keep the US 500 index above the October 27, 2023 trendline and then push the index above 5,189, with the 5,200 level looking like the next easy target.

To conclude, with the US 500 index continuing its advance, the bears are anxiously waiting for a signal from the momentum indicators to, at least, stop the bulls from recording successive record highs.

More Whispers on BoJ Considering Scrapping Yield Curve Control

Markets

Vocal ECB members provided core bonds with some early momentum on Friday. Especially ECB Villeroy gave some support by suggesting that an April rate cut is still in play less than 24 hours after ECB Lagarde actually ruled that scenario out at the ECB’s presser. Fed Chair Powell earlier last week did more or less the same by bringing May back in to play when suggesting that the Fed is not far from being confident enough that inflation is sustainably heading to 2%. Core bonds spiked to intraday highs after February payrolls gave more evidence of a soft landing scenario, enabling the Fed to gradually start lowering rates. Net job growth beat consensus in February (275k vs 200k) but downward revisions to December and January figures (-167k) dwarfed the headline beat. The unemployment rate ticked up to 3.9%, the highest level since January 2022, with wage growth slowing to 0.1% M/M and 4.3% Y/Y. Moves higher didn’t last in the close, suggesting that the March correction higher could be up for a pause. Today’s light eco calendar effectively suggests some kind of truce going into tomorrow’s February US CPI inflation numbers, which together with Thursday’s retail sales are the final key input for the March 20 FOMC meeting.

The US dollar spiked lower on the payrolls, but similarly managed a return to opening levels (DXY 102.75; EUR/USD 1.0940). JPY outperformed after Reuters strengthened expectations that the BoJ at its March policy meeting will lift its policy rate out of negative territory. This morning, there are more BoJ whispers that the central bank is also considering scrapping its yield curve control policy altogether and replacing it by announcing it advance an indication on the amount of bonds it plans to purchase. Japan’s largest union federation on Friday announces results of its annual wage negotiations (shunto) in what is expected to make or break the BoJ’s normalization plans. USD/JPY this morning holds below 147, just above the YTD low (145.90). Sterling was better bid last Friday, perhaps by default as the currency didn’t have to worry about any dovish central bank comments. EUR/GBP closed at 0.8508, near the key 0.85 support zone. The area can be tested this week with the UK labour market report (tomorrow) and production data (Wednesday) on the agenda.

News & Views

The Portuguese center-right coalition Democratic Alliance (DA) narrowly won snap elections. The DA coalition likely secured 79 seats in Parliament. The Socialist Party of outgoing Prime Minister Costa is projected at 77 seats. The far-right Chega Party came out as third and quadrupled its seats to 48. DA leader Luis Montenegro earlier ruled out a coalition between AD and Chega, suggesting that Portugal might be heading for a minority government. Socialist party leader Pedro Nuno Santos, already indicated that his party won’t support DA in parliament.

Chinese CPI inflation rebounded to 0.7% Y/Y in February compared to a 0.8% Y/Y decline in prices in January. On a monthly basis, prices rose 1%. The rebound was more pronounced than the 0.3% Y/Y expected. However, it is far from sure that the up-tick in inflation will mean the end of the deflationary trend in the country. The move for an important part was driven by a deceleration in food price deflation, while seasonal demand related to the Lunar New Year also offers part of the explanation (e.g. a sharp rise in travel prices). However PPI producer prices still remain well in negative territory, easing from -2.5% Y/Y to -2.7% Y/Y.

Rating agency Fitch raised the Turkish long-term foreign currency rating to B+ from B with a positive outlook. The upgrade reflects increased confidence in the durability and the effectiveness of policies implemented since the pivot in June 2023, including greater-than-expected frontloading of monetary policy tightening and reducing macroeconomic and external vulnerabilities. Inflation expectations have eased and external liquidity risks moderated. The positive outlook reflects the expectations that the country’s policy should be consistent with a significant decline in inflation as well as a continued reduction in external vulnerabilities.

Gold Hits Record as Net Long Positions Jump

The US economy added 275K new nonfarm jobs last month, significantly more than around 200K new job additions penciled in by analysts. But happily, the unemployment rate unexpectedly rose to 3.9% and wages grew slower than expected on a yearly basis and were almost flat on a monthly basis. The fact that another strong NFP read didn’t translate into higher wages gave a peace of mind to investors. US yields fell and the US dollar index tumbled in the immediate aftermath of the US jobs data, the EURUSD spiked to 1.0980.

While I found that the dollar selloff was a bit exaggerated – given that the US economy still added 275K new nonfarm jobs and wages grew 4.3% on yearly basis, more than twice the Fed’s inflation target - Friday’s reaction to the jobs data revealed an important information: investors don’t care about the strength of the US economy and the labour market, they only care about inflation. And because the wages data was lower than expected, Friday’s jobs day wasn’t a disaster for the Federal Reserve (Fed) doves. The market still gives around 74% chance for a 25bp cut from the Fed this June.

This week, attention shifts to the US CPI print, due tomorrow. The headline inflation is expected to steady near 3.1% on a yearly basis, core inflation is expected to have eased from 3.9% to 3.7%. But the monthly figures could print another strong month. If that’s the case, we shall see a softening in dovish Fed expectations. Remember, Fed Chair Powell said last week that the Fed ‘can and will’ start cutting the rates this year, but he also said that they are in no rush.

The US dollar begins the week on a negative note, the EURUSD gave back all post-US jobs data gains as the European Central Bank (ECB) Chief Lagarde gave a strong signal at her press conference last week that the ECB could take the first step as early as in June. Pricing in the market suggests that the ECB will cut the rates by 100bp this year – versus around 80bp cut from the Fed. The ECB’s dovish divergence could limit the euro’s upside potential against the dollar into the 1.10 psychological mark – unless the inflation numbers from the US comes in surprisingly strong.

The euro and sterling recorded their best performance against the US dollar in months on expectation that the first rate cut from the Fed won’t be delayed beyond June, and gold hit another record on Friday. The price of an ounce climbed to $2195 as the market found comfort in the idea that the Fed will cut in June. Released last Friday, the CFTC data showed that money managers boosted their long gold positions in the week through March 5th and the net long positions jumped 35% from a week earlier as they were looking to hedge against a potential post-jobs data market selloff. Also, data shows that China has been increasing its gold purchases since the beginning of last year; the central bank probably wants to diversify its dollar holdings and households certainly want to seek refuge amid the property meltdown. The question is, could the rally extend beyond $2200? Yes, it could. The inflation-adjusted gold price is below the 2020 peak – which would stand at $2323 if the price is adjusted to inflation of today. In 2011, gold traded at $2581 and back in 1980, the price of an ounce went past $3000 in inflation-adjusted terms. There is never an upper limit when people want to buy. But any retreat in Fed expectations could cool down the short term price surges.

In equities, the decline in US yields and the dollar didn’t boost appetite in major US indices. The S&P500 hit another record but closed the session 0.65% down, while Nasdaq 100 fell more than 1.50%. Tech stocks saw their largest weekly outflow on record.

Elsewhere, inflation in China rose for the first time in 6 months thanks to the Lunar New Year holiday boost in spending, but producer prices fell 2.7%. Nearby, the Japanese stocks fell as the USDJPY sank below 147 on rising speculation that the BoJ could exit the negative rates as soon as this month. I still think that there is more chance of a hint regarding the first rate hike than a concrete action on the rates front at this month’s BoJ meeting, but even a good hint could help investors rush into a long yen trade and pull the USDJPY toward the 140 mark. Finally, in energy, US crude slipped below the 200-DMA this Monday following last week’s failure to increase gains above the $80pb psychological level.

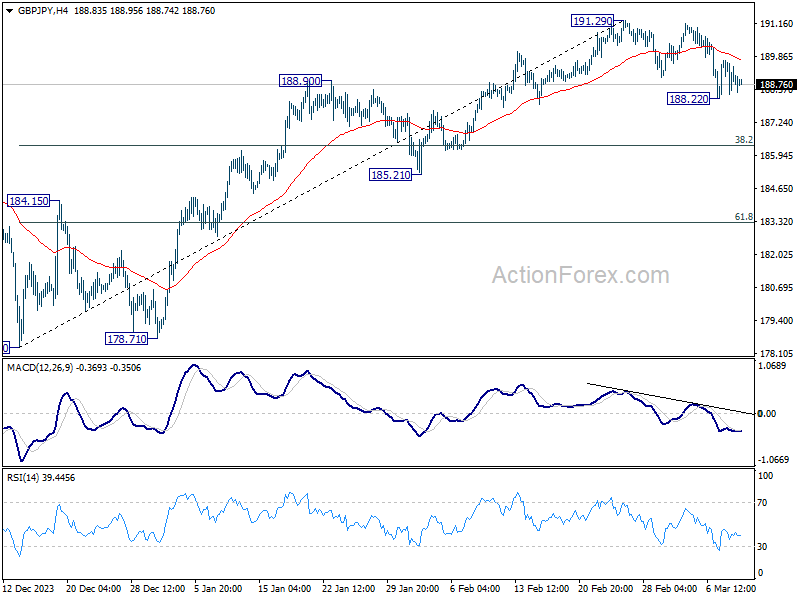

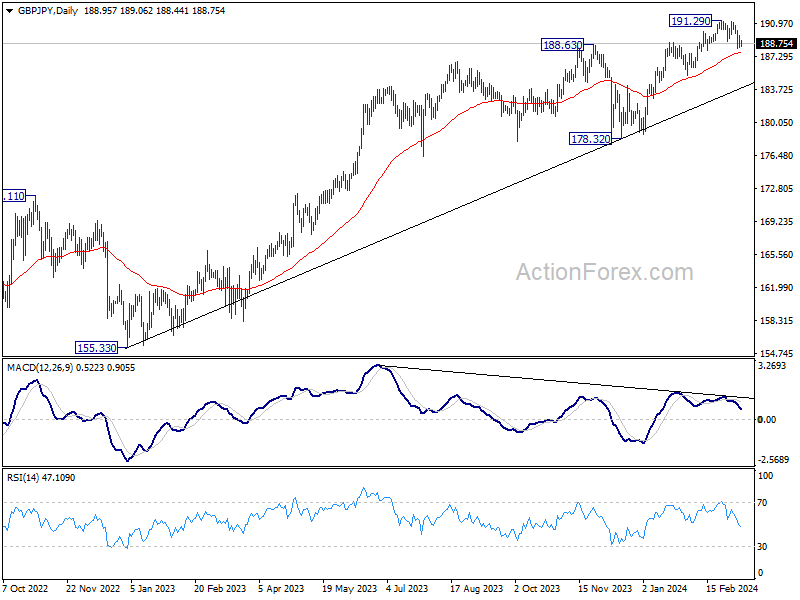

GBP/JPY Daily Outlook

Daily Pivots: (S1) 188.45; (P) 189.08; (R1) 189.78; More.....

Intraday bias in GBP/JPY remains neutral for the moment. On the downside, below 188.22 will resume the decline from 191.29 to 38.2% retracement of 178.32 to 191.29 at 186.33. Sustained break there will raise the chance of larger scale correction and target 61.8% retracement at 183.27. On the upside, though, firm break of 55 4H EMA (now at 189.84) will retain near term bullishness and bring retest of 191.29 high.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

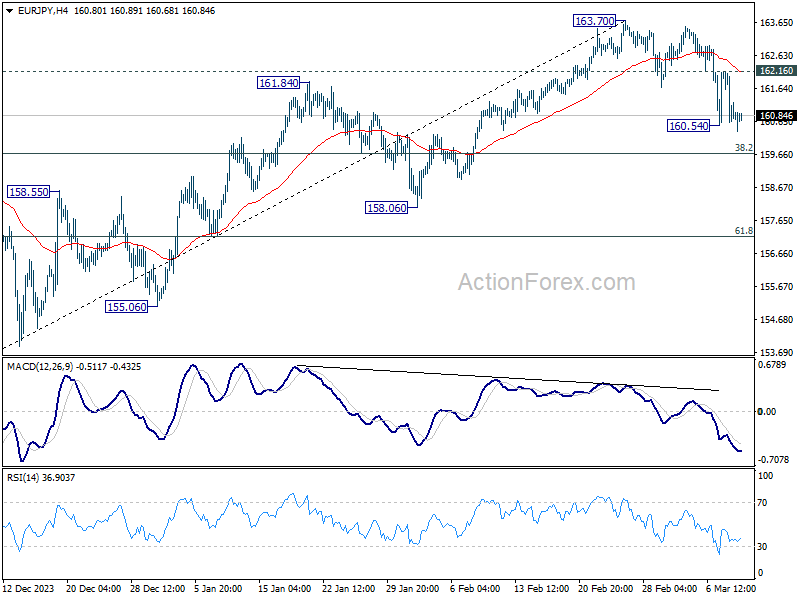

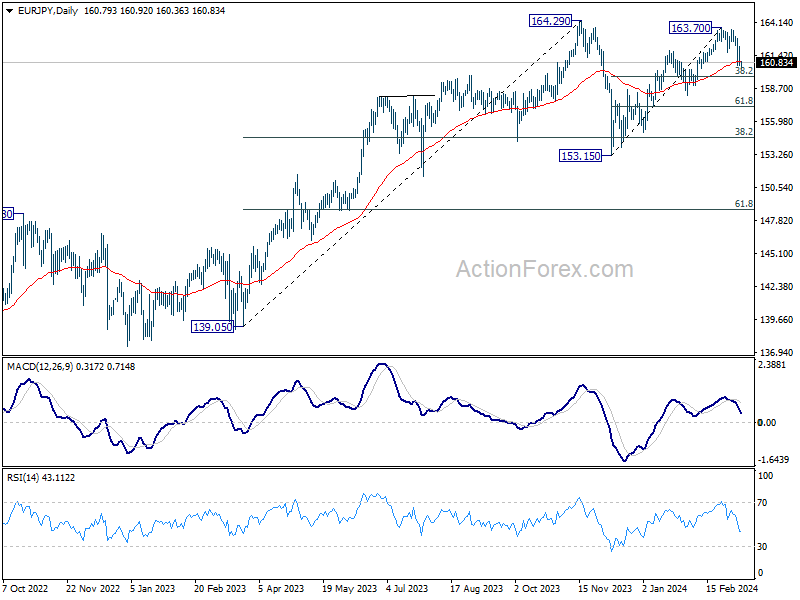

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.26; (P) 161.22; (R1) 161.82; More...

Intraday bias in EUR/JPY is back on the downside with breach of 160.54 temporary low. Fall from 163.70 is resuming to 38.2% retracement of 153.15 to 163.70 at 159.66. Sustained break there will indicate that fall from 163.70 is reversing whole rise from 153.13, and target 61.8% retracement at 157.18. On the upside, though, above 162.16 minor resistance will retain near term bullishness, and bring retest of 163.70.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 which could still be extending. As long as 148.38 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage. Next target would be 169.96 (2008 high).

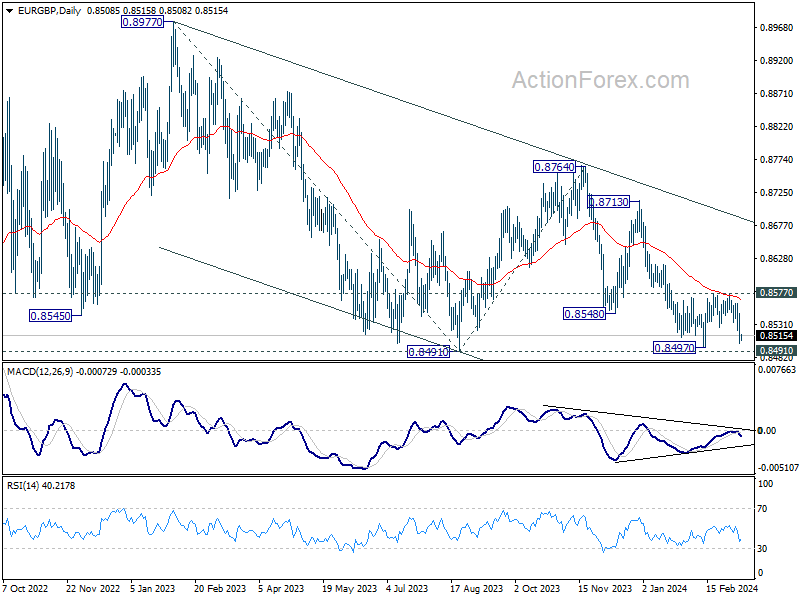

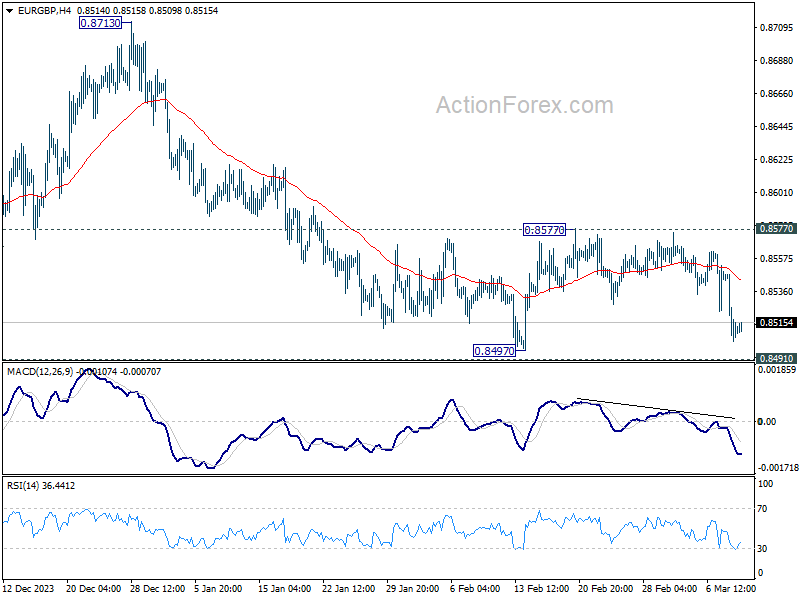

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8491; (P) 0.8520; (R1) 0.8536; More...

Intraday bias in EUR/GBP remains neutral for the moment. On the downside decisive break of 0.8491/7 support zone will confirm larger down trend resumption and target 0.8464 projection level first. Nevertheless, firm break of 0.8577 will turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.