Sample Category Title

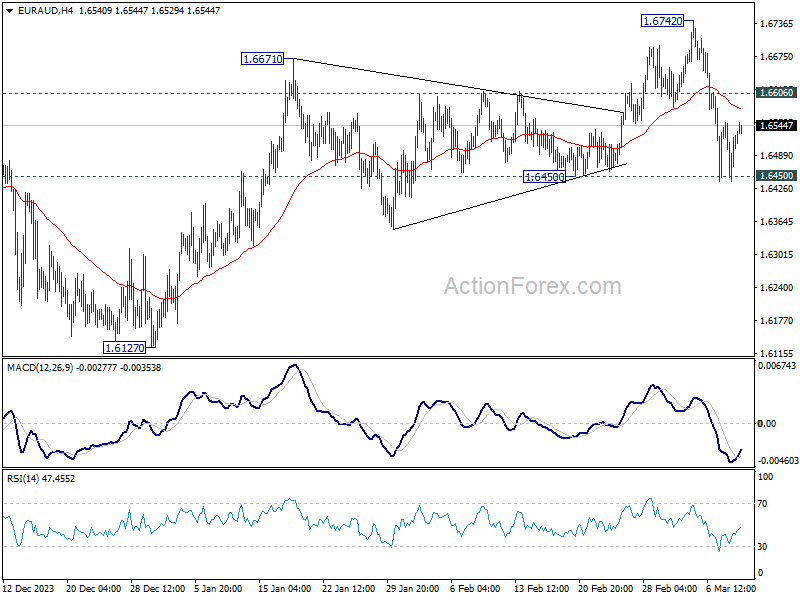

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6451; (P) 1.6502; (R1) 1.6562; More...

Intraday bias in EUR/AUD remains neutral for the moment. On the downside, decisive break of 1.6450 support will argue that whole rebound from 1.6127 has completed with three waves up to 1.6742 already. Near term outlook will be turned bearish for 1.6127 again, to extend the whole corrective pattern from 1.7062. Nevertheless, strong rebound from current level, followed by break of 1.6606 minor resistance, will retain near term bullishness and bring retest of 1.6742.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

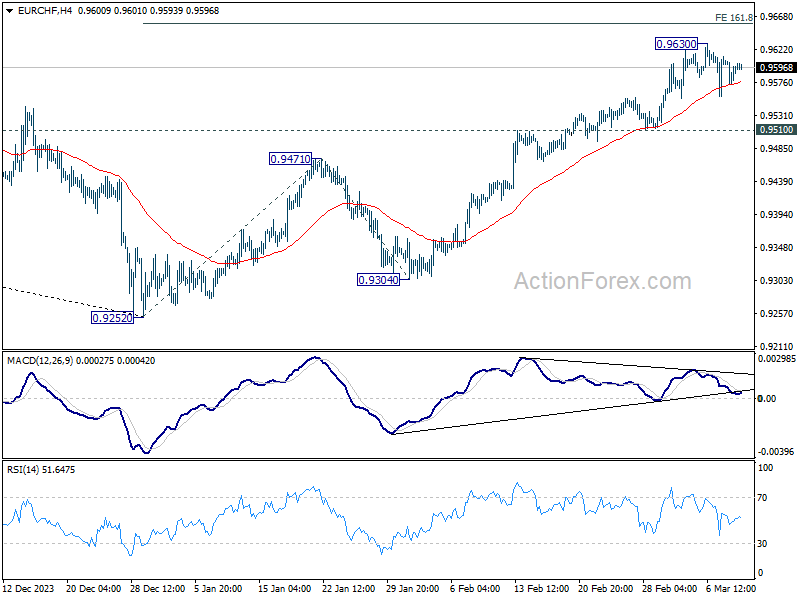

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9581; (P) 0.9596; (R1) 0.9615; More...

Intraday bias in EUR/CHF remains neutral as consolidation from 0.9630 is extending. As long as 0.9510 support holds, further rally is still expected. On the upside, break of 0.9630 will resume the rise from 0.9252 and target 161.8% projection of 0.9252 to 0.9471 from 0.9304 at 0.9658 next. However, considering bearish divergence condition in 4H MACD, firm break of 0.9510 will turn bias back to the downside for deeper fall.

In the bigger picture, as long as 0.9683 resistance holds, rebound from 0.9252 are seen as a corrective move only. Larger down trend is expected to resume through 0.9252 after the correction completes. However, firm break of 0.9683 and sustained trading above 55 W EMA (now at 0.9620) will argue that 0.9252 is already a medium term bottom. Stronger rise would then be seen 61.8% retracement of 1.0095 to 0.9252 at 0.9773 and above.

Big Inflation Week Kicks Off

In focus today

Today is a relatively quiet day on the global data front.

In Denmark, CPI inflation is released for February. We expect that inflation decreased to 1.0% y/y in February from 1.2% y/y in January, largely driven by food prices as the February price surge from last year no longer features in the measure. Additionally, Danish foreign trade and current account data for January is also scheduled for release.

In Norway, February inflation figures are released. We expect Norwegian core inflation to remain unchanged at 5.3%, as import prices are likely to have risen again and will counteract somewhat lower food prices. If proven right, this would be 0.2 pp. lower than Norges Bank expected in the December MPR and in isolation should be an argument for a less hawkish Norges Bank in March, but far from a game changer.

Focus this week will be on inflation releases, with the star of the show being the US CPI inflation release on Tuesday. January's surprisingly strong print dampened rate cut expectations for 2024 in tandem with other strong macro data. Hence, February figures coming in hotter than expected could send rate cut expectations further south. Our call is for the first Fed cut at the May meeting. Furthermore, in China we get credit and money growth between 9 and 15 March but there is no fixed date or time. The credit data is very volatile from month to month, but the trend has been relatively robust in recent months reflecting the stimulus by the government.

Economic and market news

What happened overnight

In Japan, the final Q4 2023 GDP print was released. The print was revised up to 0.1% q/q from -0.1% q/q, indicating that the Japanese economy averted a technical recession in Q4. Moreover, speculations regarding the Bank of Japan hiking rates in March flared up slightly amid expectations of robust pay increases in this year's annual wage negotiations. This led to the Japanese yen moving somewhat higher.

In China, Chinese regulators engaged in talks with financial institutions and private debt to bolster financing support and extend debt maturity for Vanke, a state-backed developer. Recently, the property developer has faced pressure as investors have sold shares and bonds due to liquidity concerns, prompted by reports of the state-owned entity seeking debt maturity extension with some insurers.

What happened over the weekend and on Friday

In the US, on Friday, the February Jobs Report sent mixed signals. Non-farm payrolls (NFP) came in higher than expected at +275k (cons: 200k). However, at the same time, past months' figures were revised down by a cumulative 167k, offsetting the upside surprise in February. In contrast to the NFP, the household survey (which counts the number of employed workers) was markedly weaker at -184k (Jan: -31k). Coupled with the labour force growing by +150k, the unemployment rate climbed higher to 3.9% from 3.7%, indicating that some slack is slowly building in the labour markets, which is good news for the Fed. On the wage front, average hourly earnings growth declined considerably to 0.1% m/m SA, mainly reflecting a rise in the average hours worked, with wage sum growth continuing its declining trend seen recently.

On the political front, the US government avoided a partial shutdown as six out of 12 individual appropriations bills were signed into law by President Biden. However, with the deadline for the remaining funding bills set for 22 March, a partial shutdown is still possible.

In Europe, euro area wage growth for Q4 2023 was released on Friday. The figure came in at 4.5% y/y down from 5.1% y/y in Q3. Overall wage growth remains too elevated for a 2% inflation target. Hence, we believe that the ECB most likely awaits Q1 2024 data to become confident that wage growth is consistently decreasing, which serves as a key reason why we expect the ECB to start lowering rates at the June meeting.

In China, the February CPI was released on Saturday. The print surprised to the upside, with Chinese consumer prices ticking higher for the first time in six months, coming in at 1.0% m/m and 0.7% y/y (cons: 0.7% m/m, 0.3% y/y). The positive figures are strongly attributed to a spending boom following the Lunar New Year.

In Saudi Arabia, state-owned Saudi Aramco raised its dividend to nearly USD 100bn amid reporting its second-highest annual profit ever despite lower oil prices. The payout stands as the primary revenue source for the Saudi government, which seeks to fund its ambitious modernization plans via the generated profits.

In the geopolitical space, US, French, and British forces retaliated against a Houthi attack on a bulk carrier and destroyer by striking dozens of drones in the Red Sea area. Additionally, the European Commission announced on Friday that a maritime aid corridor could commence operations between Cyprus and Gaza over the weekend, in a project financed by the UAE. However, as of early this morning, the vessel remains docked in Cyprus.

Equities: Global equities were lower Friday, dragged down by US and long duration growth stocks. The pullback in some the best performing names over the last year came despite a day with solid macro figures basically confirming the current investment narrative of a soft landing. Please note both small caps and banks were outperforming and 15 out of 25 industries in the US were higher, highlighting that the sell-off was being macro related. In US on Friday, Dow -0.2%, S&P 500 +0.7%, Nasdaq -1.2% and Russell 2000 -0.10%. Japanese equities are sharply lower this morning as Bank of Japan is increasingly expected to tighten policies soon. US and European futures are lower as well.

FI: US Treasury yields continued to decline last week as 10Y US treasury yields declined some 12-13bp during the week. We have seen a similar move in the 10Y German government bond, where the yield has declined some 13-14bp.

Furthermore, the spread compression in both the German ASW-spreads and the BTPS-Bund spread has been relentless. The Bund ASW-spread is slowly moving towards 30bp and the 10Y BTPS-Bund is gradually tightening towards 125bp. Short-term the momentum seems to be for a tighter as there is plenty of supply from Germany also relative to Italy. This week Germany will tap EUR 9bn in the 2Y and 10Y segments, while Italy will tap EUR 8.5bn in the 7Y to 15Y segments.

FX: The USD had its worst week since December losing out vs the rest of G10, with JPY as the winner with a 2% appreciation. The SEK also had a strong week, with EUR/SEK once more challenging the lower bound of the recent range (11.20). This week brings a lot of interesting macro data, which are bound to influence FX trading.

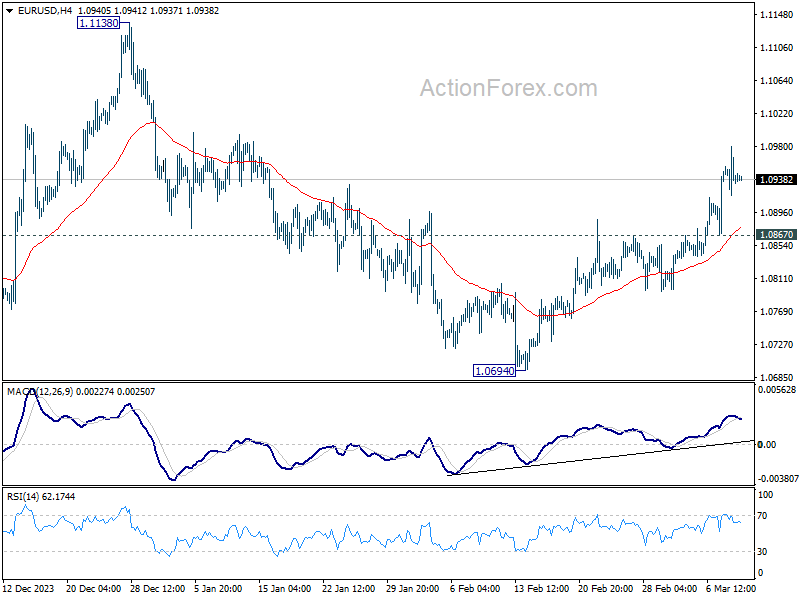

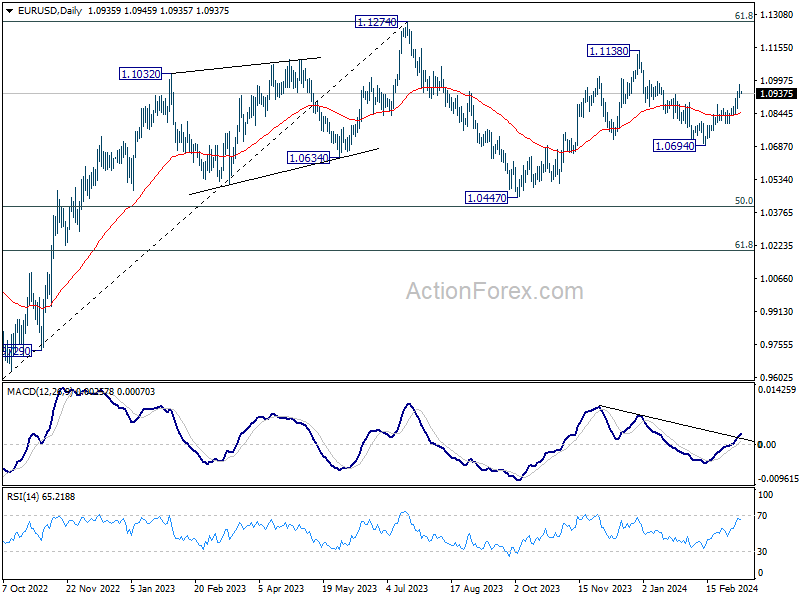

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0911; (P) 1.0946; (R1) 1.0974; More...

Intraday bias is EUR/USD remains on the upside at this point. Fall from 1.1138 could have completed at 1.0694, as a correction to rise from 1.0447. Further rally would be seen to retest 1.1138 next. On the downside, below 1.0867 minor support will turn intraday bias neutral and bring consolidations.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

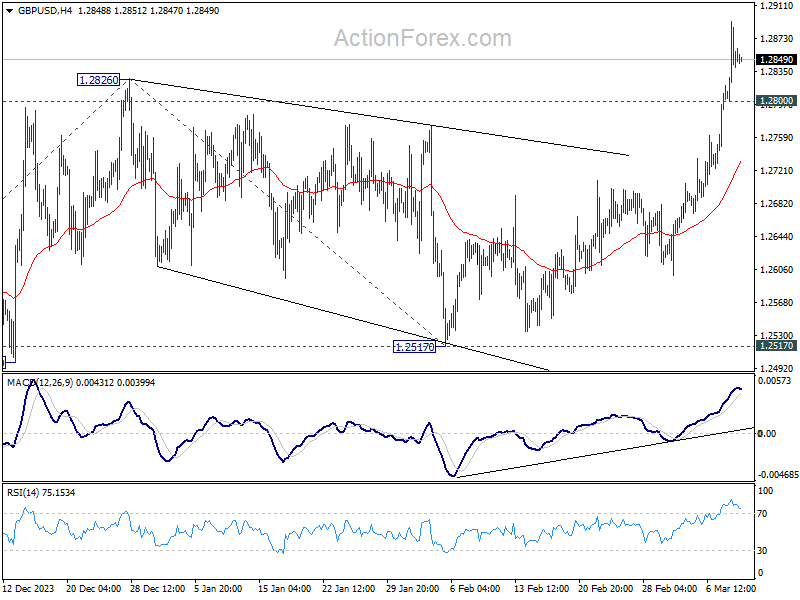

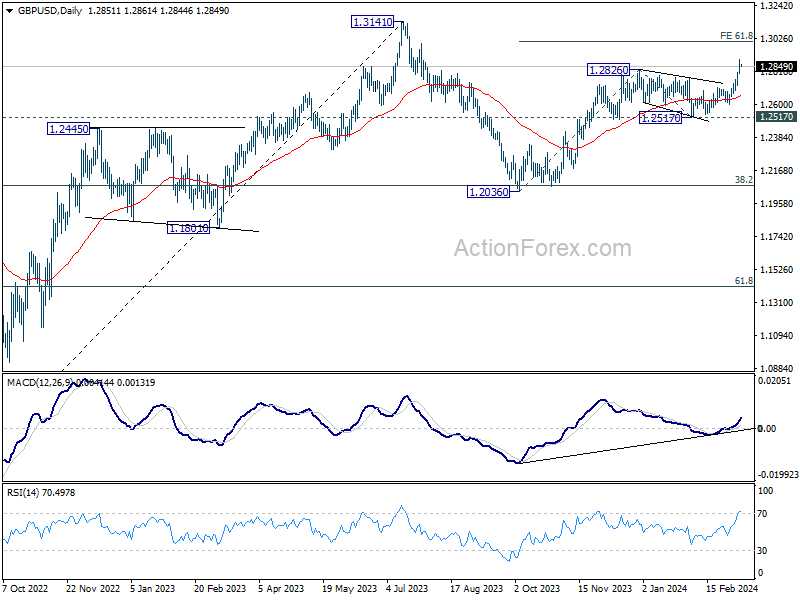

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2809; (P) 1.2852; (R1) 1.2902; More...

Intraday bias in GBP/USD remains on the upside at tis point. Current rise is part of the rally from 1.2063, and should target 61.8% projection of 1.2036 to 1.2826 from 1.2517 at 1.3005. On the downside, below 1.2800 minor support will turn intraday bias neutral first. But further rise will remain in favor as long as 55 4H EMA (now at 1.2732) holds.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which is still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

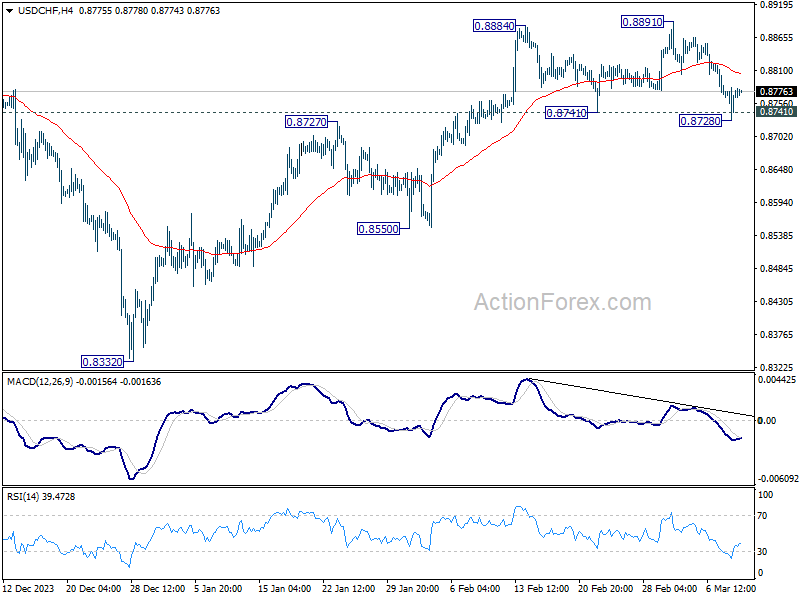

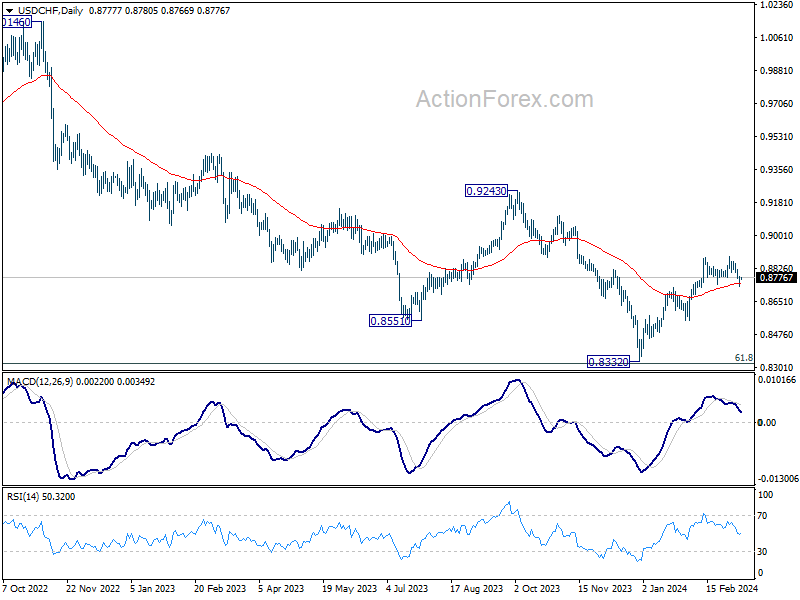

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8743; (P) 0.8764; (R1) 0.8797; More....

Intraday bias in USD/CHF remains neutral for the moment. On the downside, sustained break of 0.8741 will argue that the whole rebound from 0.8332 might have completed, and bring deeper fall to 0.8550 support. Nevertheless, strong bounce from current level will retain near term bullishness. Further break of 0.8891 will resume the rise from 0.8332.

In the bigger picture, price actions from 0.8332 medium term bottom as seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8555 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.

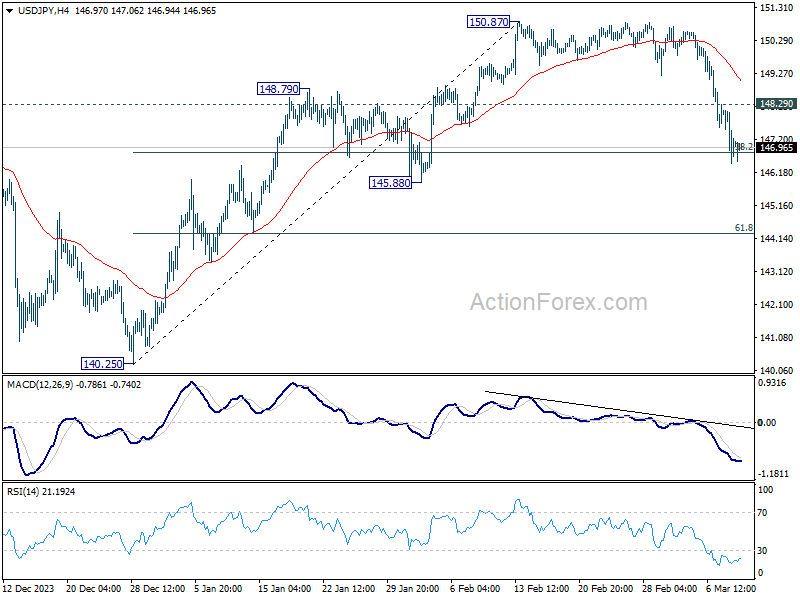

USD/JPY Daily Outlook

Daily Pivots: (S1) 146.33; (P) 147.23; (R1) 147.96; More...

Intraday bias in USD/JPY stays on the downside at this point. Sustained break of 38.2% retracement of 140.25 to 150.87 at 146.81 will argue that fall from 150.87 is reversing the whole rally from 140.25. In this case, deeper decline would be seen to 61.8% retracement at 144.30 and below. Nevertheless, strong support from 146.81, followed by break of 148.29 minor resistance resistance, will argue that fall from 150.87 is merely a correction, which has completed already.

In the bigger picture, no change in the view that price action from 151.89 (2023 high) are correction to up trend from 127.20 (2023 low). The question is whether this correction has completed at 140.25, or extending with fall from 150.87 as the third leg. Sustained break of above mentioned 146.81 fibonacci level will favor the latter case. But even so, downside should be contained by 50% retracement of 127.20 to 151.89 at 139.54.

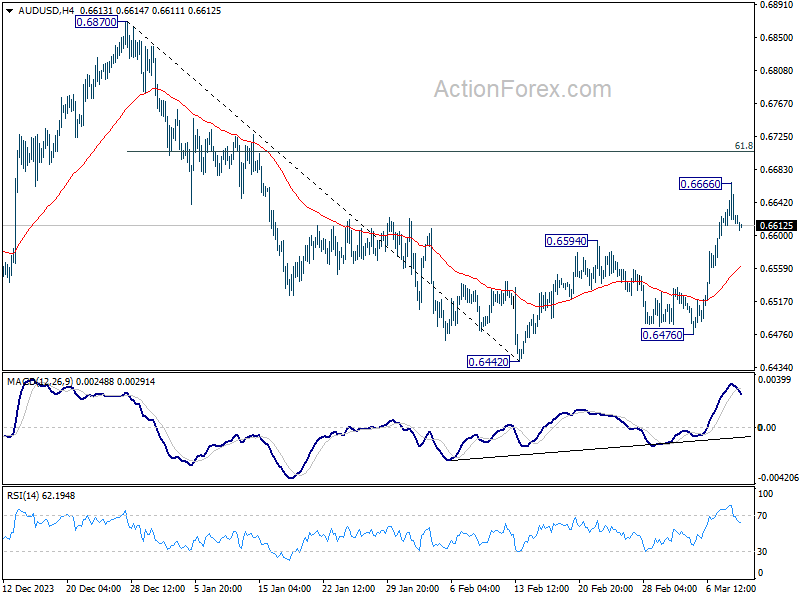

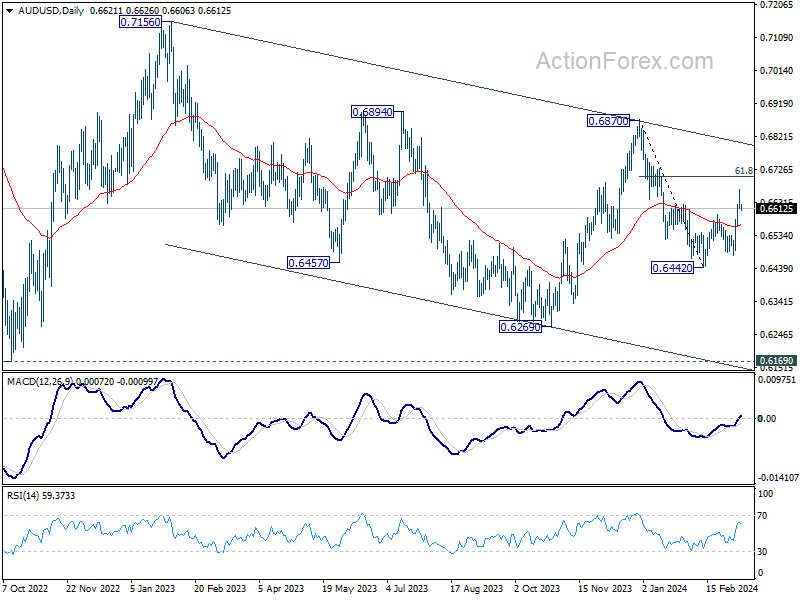

AUD/USD Daily Report

Daily Pivots: (S1) 0.6602; (P) 0.6635; (R1) 0.6657; More...

Intraday bias in AUD/USD is turned neutral first with current retreat. Another rise will be mildly in favor as long as 55 4H EMA (now at 0.6561) holds. Above 0.6666 will resume the rebound from 0.6442 to 61.8% retracement of 0.6877 to 0.6442 at 0.6707 next. Sustained trading above there will argue rise from 0.6442 is probably resuming whole rally from 0.6269. Nevertheless, sustained break of 55 4H EMA will revive near term bearishness and bring retest of 0.6442 low instead.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which might still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

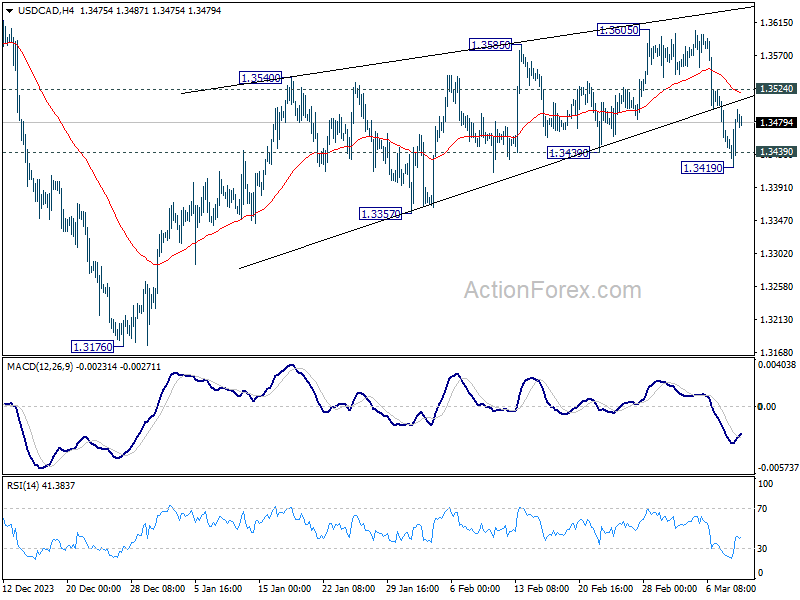

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3439; (P) 1.3469; (R1) 1.3517; More...

Intraday bias in USD/CAD remains neutral for the moment. On the downside, break of 1.3419 and sustained trading below 1.3439 support will argue that rebound from 1.3176 has completed as a corrective move to 1.3605. Near term outlook will be turned bearish for 1.3357 support first. On the upside, though, break of 1.3524 minor resistance will revive near term bullishness, and turn bias back to the upside for retesting 1.3605 resistance instead.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

Yen Strengthens on Recession Avoidance, Dollar and Sterling Await Data-Driven Clarity

Yen rises broadly in Asian session today, lifted by economic data indicating Japan's narrow escape from recession last year. This economic turnaround, while not directly influencing BoJ decision on interest rates decision next week, certainly does not obstruct the pathway for a hike. Yen's momentum, though currently modest, could amplify with anticipated positive developments from wage negotiations throughout the week, with prospect of another round of vigorous rally.

In contrast, the Australian Dollar, New Zealand Dollar, and Sterling are showing relative weakness, whereas Canadian Dollar, Euro, and Swiss Franc are having slight gains, and Dollar is mixed. The currency movements today seem more reflective of a consolidation phase, following last week's activities, rather than the formation of new trends.

With today's economic calendar appearing light, trading activity might lean towards the quieter side. However, expectations of volatility loom on the horizon, with significant data releases from the US and UK slated for later in the week.

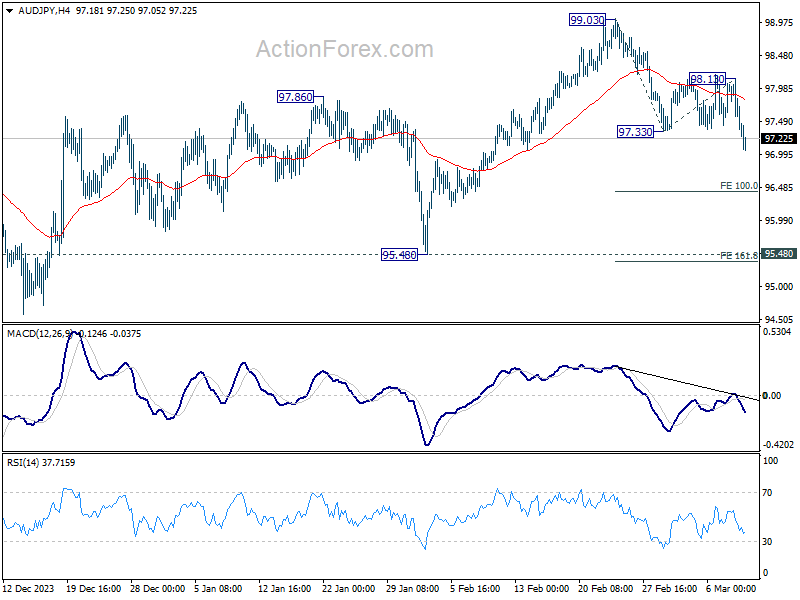

Technically, AUD/JPY's declined from 99.03 short term top resumed by breaking through 97.33 low late last week. Deeper fall is now expected as long as 98.13 resistance holds, to 100% projection of 99.03 to 97.33 from 98.13 first. Firm break there will pave the way to 161.8% projection at 95.37.

In Asia, at the time of writing, Nikkei is down sharply by -2.60%. Hong Kong HSI is up 1.43%. China Shanghai SSE is up 0.14%. Singapore Strait Times is down -0.12%. Japan 10-year JGB yield is up 0.0299 at 0.764.

Japan's Q4 GDP finalized at 0.1% qoq, a narrow escape from recession

Japan's economy has narrowly avoided a recession, as shown in the final GDP figures for Q4. The revised data indicates a modest growth of 0.1% qoq, a positive swing from the preliminary estimate of -0.1% qoq contraction. On annualized basis, GDP expanded by 0.4%, contrasting sharply with initial reports of -0.4% decline.

The main driver behind this upward revision was significant increase in capital expenditure, which surged by 2% qpq, deviating markedly from the initially estimated -0.1% qoq drop. However, private consumption, accounting for approximately 60% of Japan's economy, presented a less optimistic picture, declining by -0.3% qoq, a slight deterioration from the provisional figure of -0.2% qoq.

This latest economic data comes at a crucial time, but it does not seem to deter BoJ from considering an interest rate hike for the first time since 2007, scheduled for March 19. The anticipation builds around the annual Spring wage negotiations, which have so far shown strong momentum. Positive outcomes are also expected from the forthcoming results from Rengo, Japan's largest union group, on March 15.

China's CPI turned positive to 0.8% yoy amid Lunar New Year demands

In February, China's CPI marked its first annual increase after a six-month sequence of declines. CPI rose by 0.7% yoy, surpassing expectation of 0.3% yoy and marking a significant rebound from January's -0.8% yoy, the largest decrease in consumer prices since 2009. On a month-on-month basis, CPI acceleration was evident, jumping from a modest 0.3% mom to 1.0% om, well above the forecasted 0.7% mom.

This inflationary uptick, primarily driven by heightened demand during the Lunar New Year celebrations, underscores the seasonal influence on China's economic activities. Notably, food prices witnessed a considerable increase of 3.3% mom, a reflection of the festive period's impact.

Conversely, PPI had a contrary movement, declining by -2.7% yoy, indicating deeper deflationary pressures than the anticipated -2.5%.

EUR/GBP and GBP/CHF await UK data

Sterling would likely be on the move this week as key UK economic indicators, including GDP, employment, and wages data, are set to be released. These figures are eagerly watched, as any deviation from expectations could influence the market's anticipations for the upcoming inflation report and BoE's subsequent meeting next week.

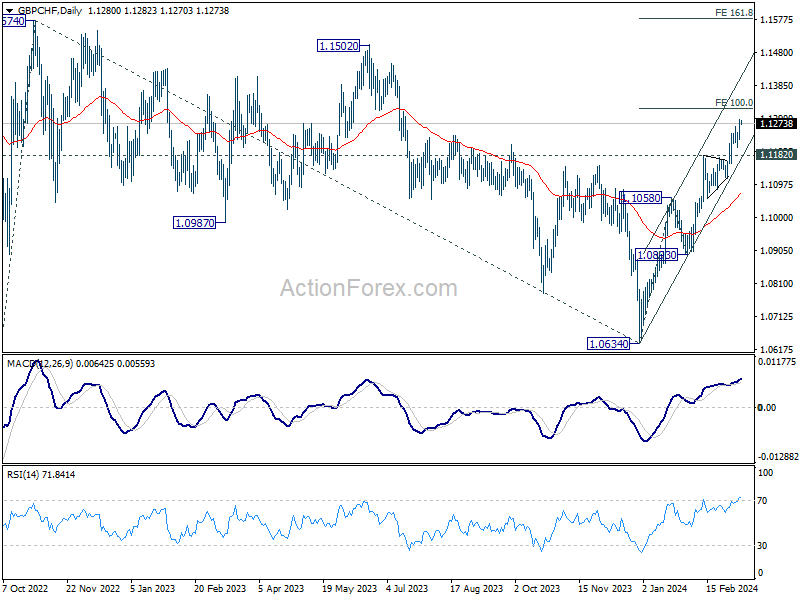

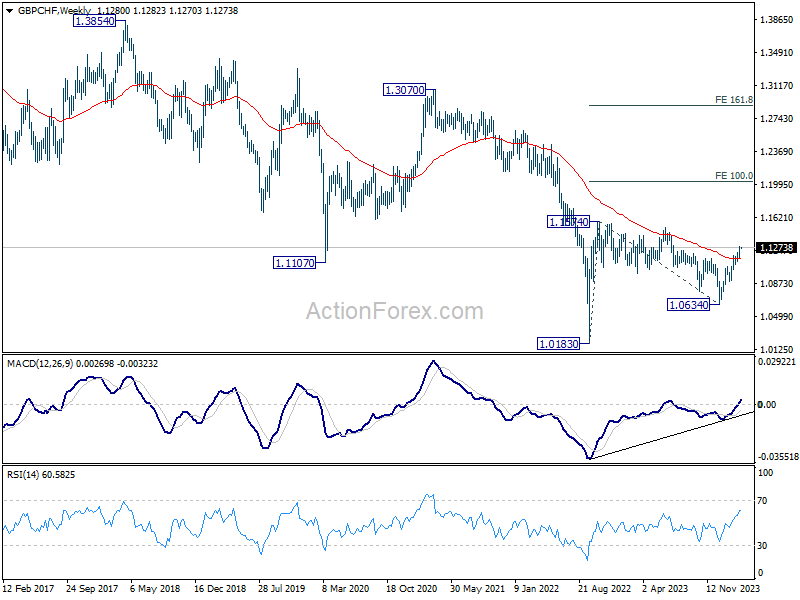

GBP/CHF's rally from 1.0634 continued last week and hit as high as 1.1287. Immediate focus is now on 100% projection of 100% projection of 1.0634 to 1.1058 from 1.0893 at 1.1317. Decisive break there would prompt upside acceleration towards 161.8% projection at 1.1579. While overbought condition, as seen in D RSI, might limit upside at 1.1317 on initial attempt, near term outlook will stay bullish as long as 1.1182 resistance turned support holds.

In the larger picture, the break of 55 E EMA is a medium term bullish sign. This also strengthen the case that correction from 1.1574 has completed at 1.0634 already. Rise from 1.0183 (2022 low) could be ready to resume. Retest of 1.1574 should be seen next, and firm break there will pave the way to 100% projection of 1.0183 to 1.1574 from 1.0634 at 1.2025 in the medium term.

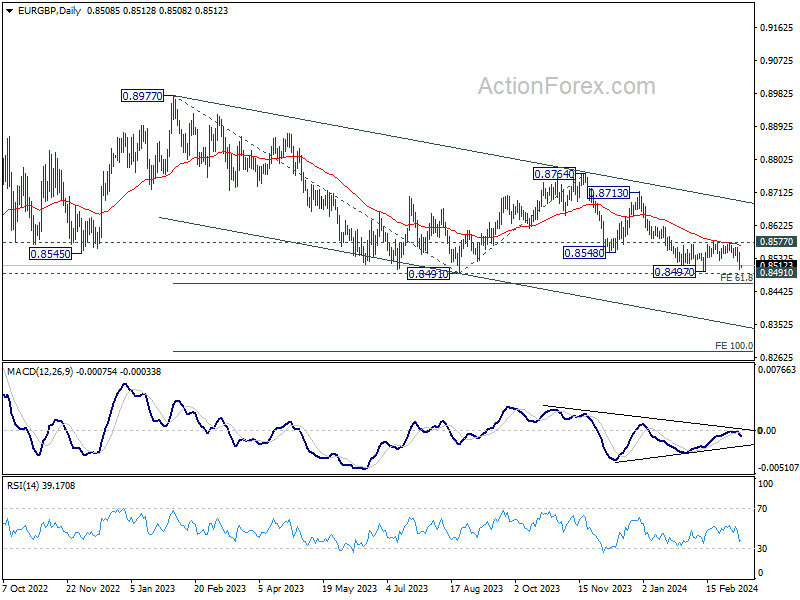

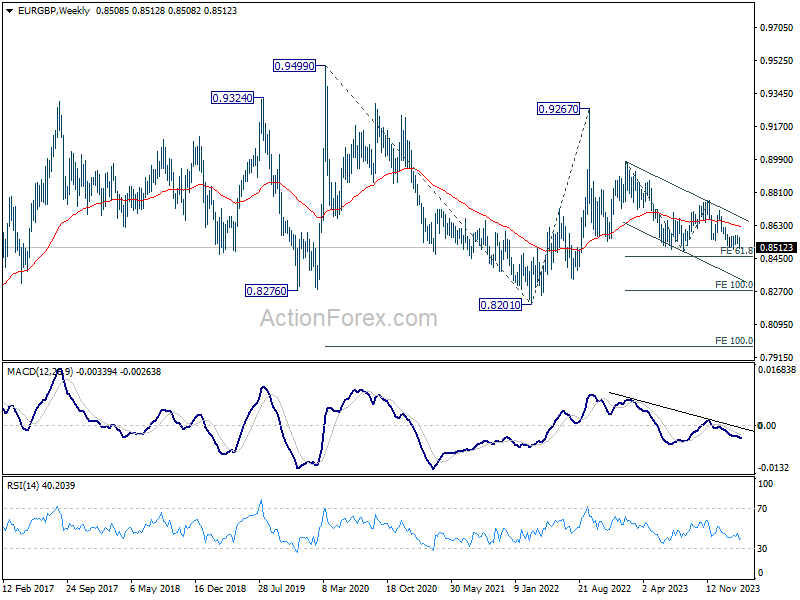

EUR/GBP's rejection by 55 D EMA is a near term bearish sign, which suggests that fall from 0.8764 is still in progress. Break of 0.8497 support will resume this decline to 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464. Firm break there could trigger downside acceleration to 100% projection at 0.8278.

Any downside acceleration ahead would also strengthen the case that fall from 0.9267 is going to extend through 0.8201 (2022 low) in the medium term, as the third leg of the pattern from 0.9499 (2020 high).

US CPI to test Fed's rate cut timeline, UK GDP and wages growth crucial too

Spotlight turns to the US and the UK in this relatively light week, as both nations prepare to release crucial economic data.

In the US, all eyes are on the upcoming consumer inflation figures, positioned as the centerpiece. February's CPI is anticipated to show 0.4% mom increase, primarily driven by a surge in gasoline prices. This expected rise would keep the annual inflation rate steady at 3.1% yoy, signaling a pause in the disinflation progress again. Core CPI, stripping out volatile food and energy prices, is forecasted to climb by 0.3% mom, with the yoy rate decelerating from 3.9% to 3.7%.

Should these expectations hold true, they would underscore Fed Chair Jerome Powell's recent cautionary remarks, emphasizing the need for more data and confidence before contemplating rate reductions. Presently, futures markets assign roughly 75% probability to a June rate cut by Fed. A modest undershoot in CPI might not expedite this timeline to May, whereas a surprise on the upside could prompt a reassessment of the cut's timing.

Other notable data from the US include PPI, retail sales, and the University of Michigan consumer sentiment index.

Across the Atlantic, the UK is poised to unveil GDP and employment statistics for January. GDP growth is forecasted at 0.2% mom, signaling a move towards stabilization from last year's recessionary. This development would be greeted positively by BoE policymakers, allowing them a longer leash before reducing interest rates. Additionally, the wages growth data will offer insights into persistence of domestic inflationary pressures.

Amid diverging views among economists and even members of MPC regarding BoE's rate cut timeline, August emerges as the more likely month for commencing policy easing.

Here are some highlights for the week:

- Monday: Japan GDP final, machine tool orders;.

- Tuesday: Japan BSI manufacturing, PPI; Australia NAB business confidence; Germany CPI final; UK employment; US CPI.

- Wednesday: UK GDP, production, trade balance; Eurozone industrial production.

- Thursday: UK RICS house price balance; Swiss PPI; Canada manufacturing sales; US PPI, retail sales, jobless claims, business inventories.

- Friday: New Zealand BNZ manufacturing; Japan tertiary industry index; UK consumer inflation expectations; Canada housing starts; US Empire state manufacturing, import prices, industrial production, U of Michigan consumer sentiment.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3439; (P) 1.3469; (R1) 1.3517; More...

Intraday bias in USD/CAD remains neutral for the moment. On the downside, break of 1.3419 and sustained trading below 1.3439 support will argue that rebound from 1.3176 has completed as a corrective move to 1.3605. Near term outlook will be turned bearish for 1.3357 support first. On the upside, though, break of 1.3524 minor resistance will revive near term bullishness, and turn bias back to the upside for retesting 1.3605 resistance instead.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | GDP Q/Q Q4 F | 0.10% | 0.30% | -0.10% | |

| 23:50 | JPY | GDP Deflator Y/Y Q4 F | 3.90% | 3.80% | 3.80% | |

| 23:50 | JPY | Money Supply M2+CD Y/Y Feb | 2.50% | 2.40% | 2.40% | |

| 06:00 | JPY | Machine Tool Orders Y/Y Feb P | -8.0% | -14.10% | -14.0% |