Sample Category Title

GBP/JPY Weekly Outlook

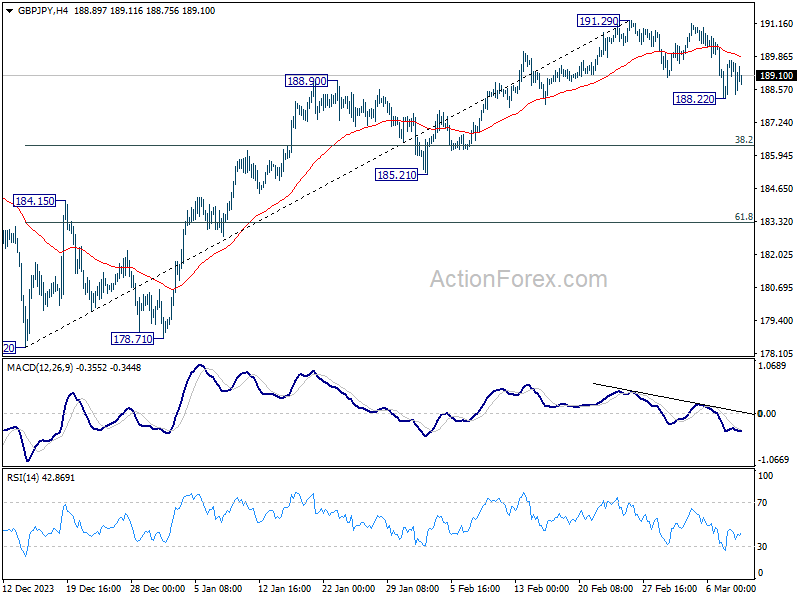

GBP/JPY fell to 188.22 last week but turned sideway since then. Initial bias remains neutral this week first. On the downside, below 188.22 will resume the decline from 191.29 to 38.2% retracement of 178.32 to 191.29 at 186.33. Sustained break there will raise the chance of larger scale correction and target 61.8% retracement at 183.27. On the upside, though, firm break of 55 4H EMA (now at 189.84) will retain near term bullishness and bring retest of 191.29 high.

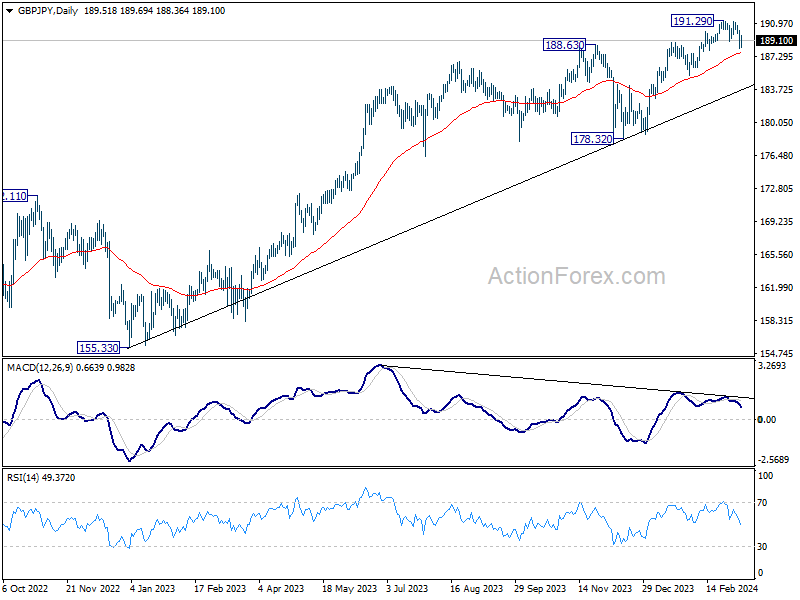

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

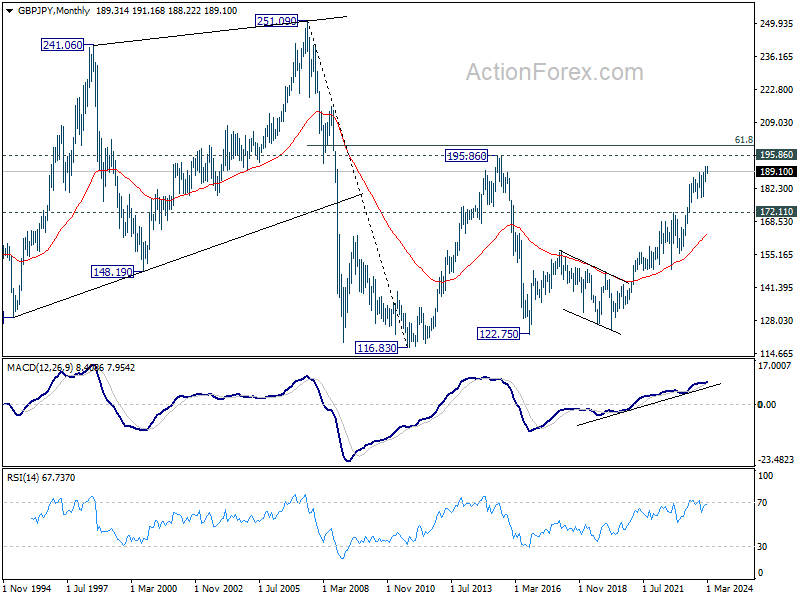

In the longer term picture, rise from 122.75 (2016 low) is seen as the third leg of the pattern from 116.83 (2011 low). Further rally will remain in favor as long as 172.11 resistance turned support holds. Break of 195.86 (2015 high) is possible. But strong resistance could be seen from 61.8% retracement of 251.09 (2007 high) to 116.83 at 199.80 to limit upside, at least on first attempt.

EUR/JPY Weekly Outlook

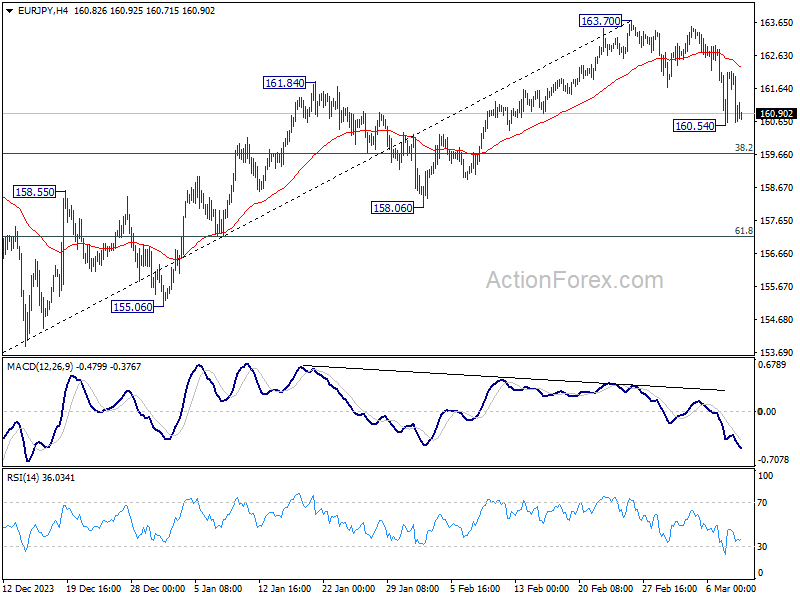

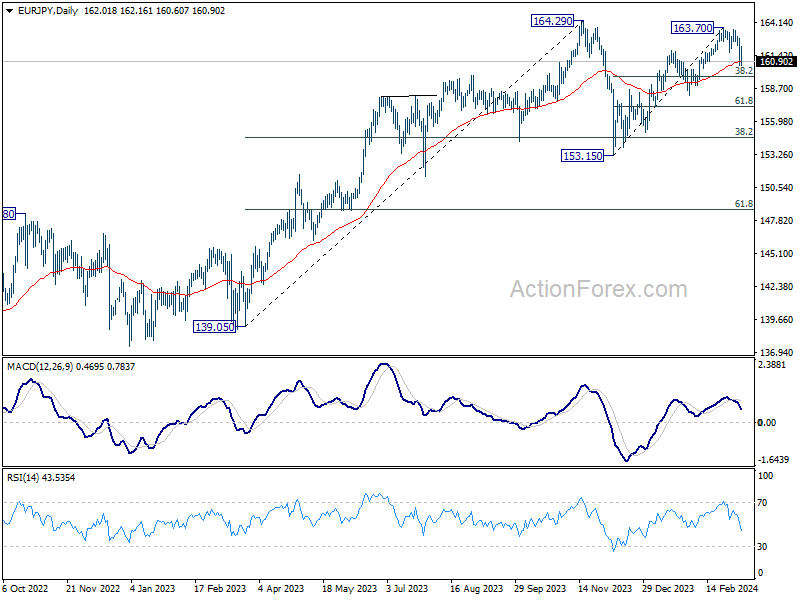

EUR/JPY's fall from 163.70 extended lower to 160.54 last week but turned sideway since then. Initial bias remains neutral this week first. On the downside, break of 160.54 will target 38.2% retracement of 153.15 to 163.70 at 159.66. Sustained break there will indicate that fall from 163.70 is reversing whole rise from 153.13, and target 61.8% retracement at 157.18. On the upside, sustained break of 55 4H MACD (now at 162.27) will retain near term bullishness, and bring retest of 163.70.

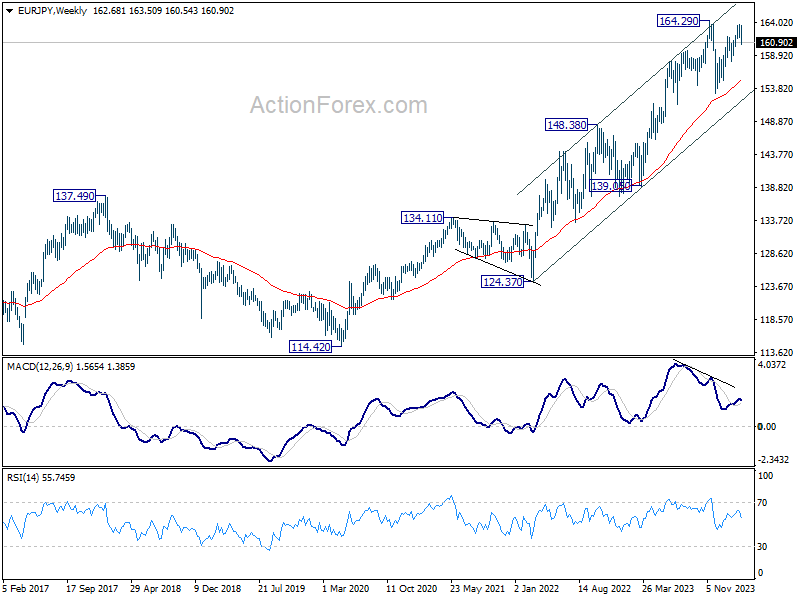

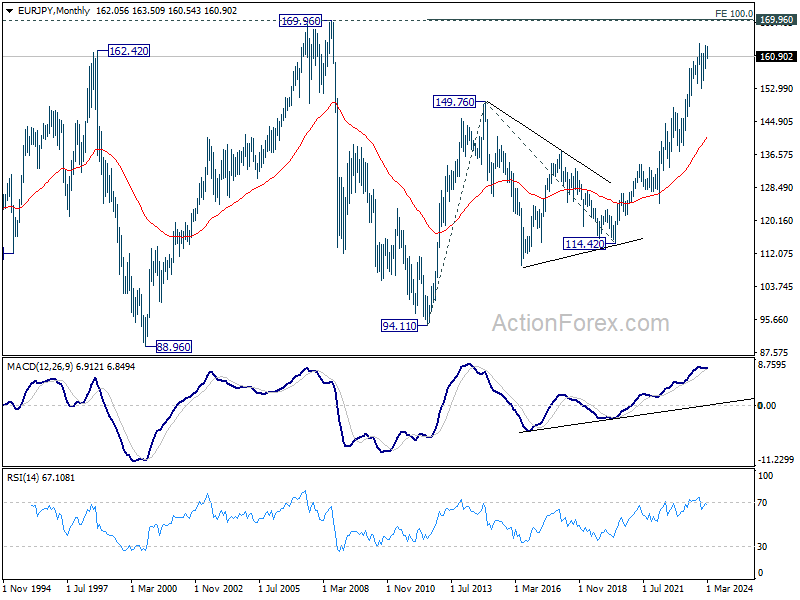

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 which could still be extending. As long as 148.38 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage. Next target would be 169.96 (2008 high).

In the long term picture, rise from 114.42 (2020 low) is seen as the third leg of the whole up trend from 94.11 (2012 low). Next target is 100% projection of 94.11 to 149.76 from 114.42 at 170.07 which is close to 169.96 (2008 high). This will remain the favored case as long as 148.38 resistance turned support holds.

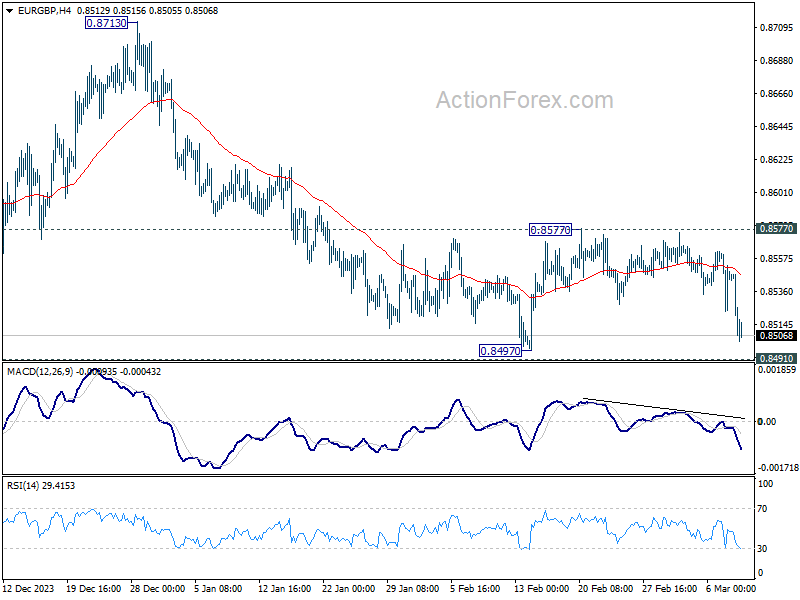

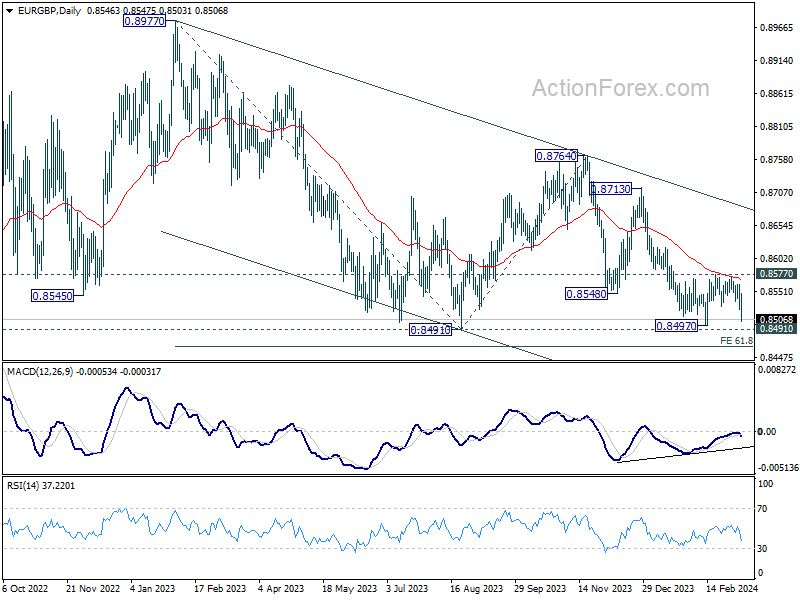

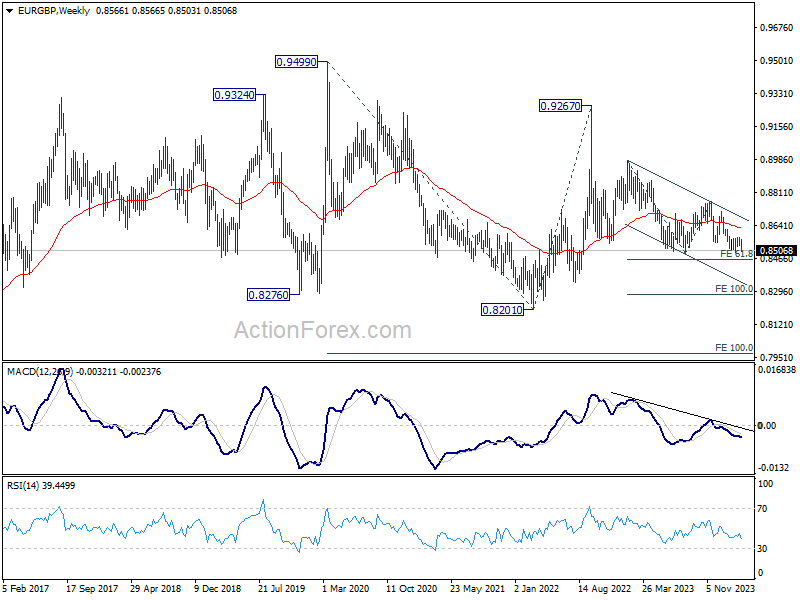

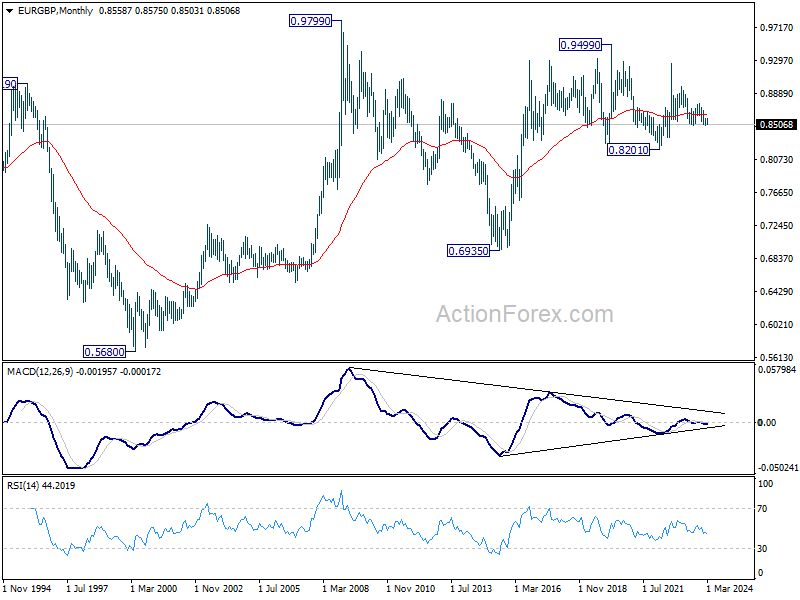

EUR/GBP Weekly Outlook

EUR/GBP stayed in range of 0.8497/8577 last week and outlook is unchanged. Initial bias remains neutral this week first. On the downside decisive break of 0.8491/7 support zone will confirm larger down trend resumption and target 0.8464 projection level first. Nevertheless, firm break of 0.8577 will turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Fall from 0.9267 is the third leg of the pattern from 0.9499. Break of 0.8201 (2022 low) will target 100% projection of 0.9499 to 0.8201 from 0.9267 at 0.7969.

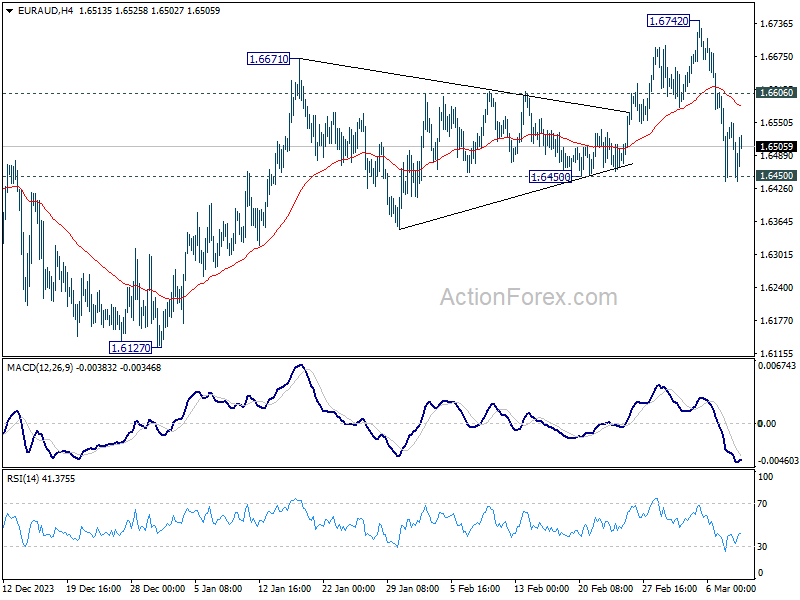

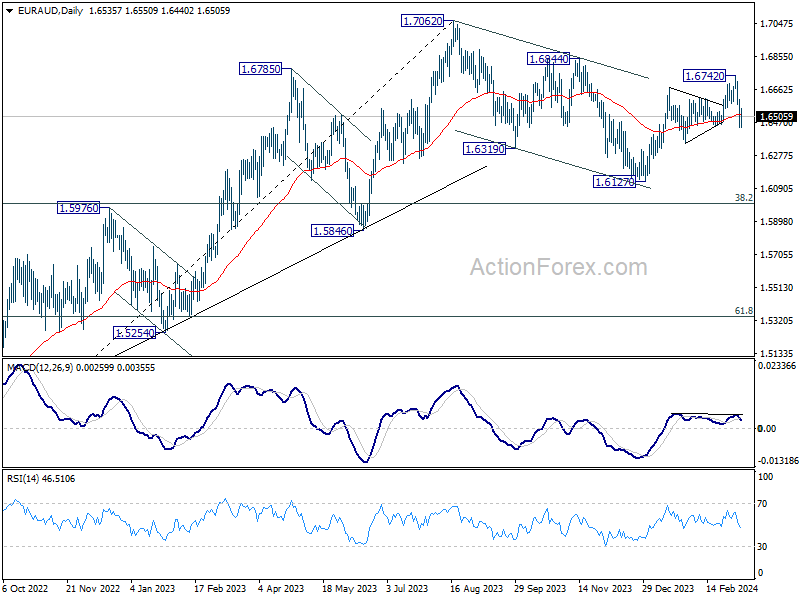

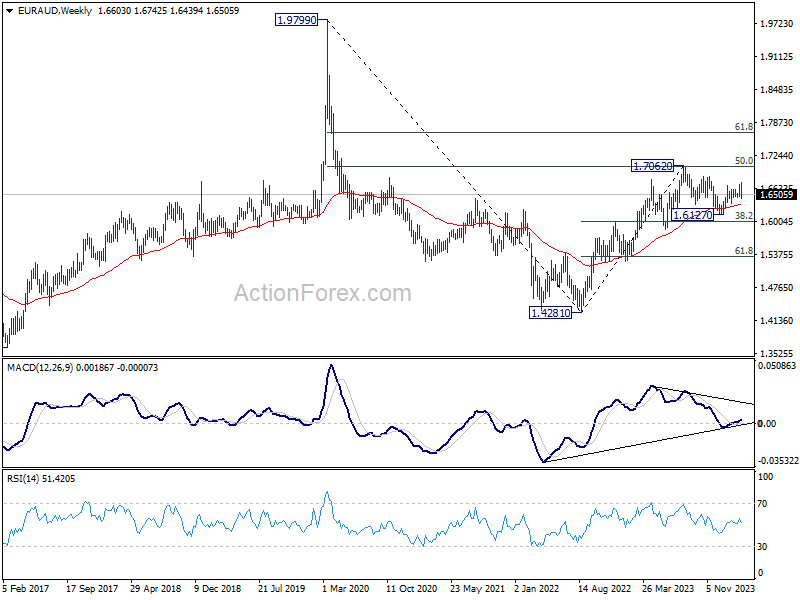

EUR/AUD Weekly Outlook

EUR/AUD edged higher to 1.6742 last week but fell sharply since then. Immediate focus is now on 1.6450 support this week. Decisive break there will argue that whole rebound from 1.6127 has completed with three waves up to 1.6742 already. Near term outlook will be turned bearish for 1.6127 again, to extend the whole corrective pattern from 1.7062. Nevertheless, strong rebound from current level, followed by break o 1.6606 minor resistance, will retain near term bullishness and bring retest of 1.6742.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

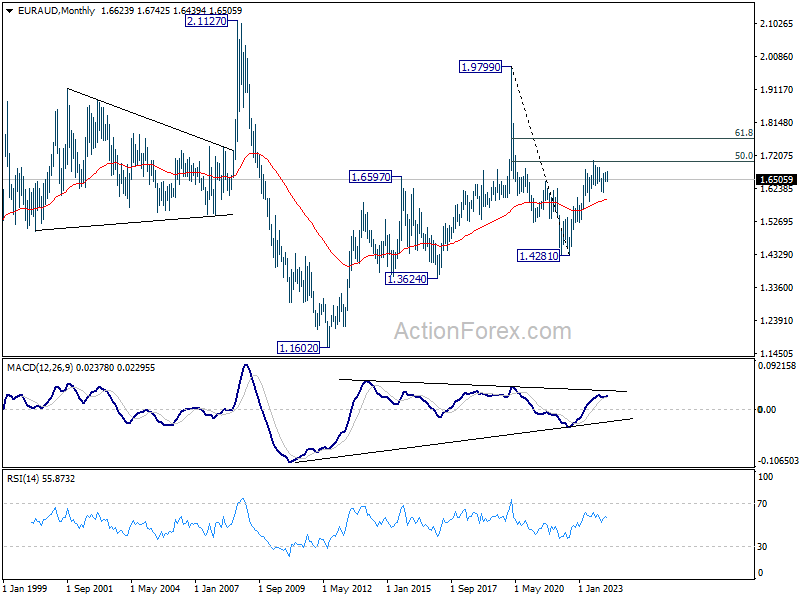

In the longer term picture, price actions from 1.9799 (2020 high) are seen as a long term decline at the same scale as the rise from 1.1602 (2012 low). Rebound from 1.4281 is seen as the second leg. As long as 55 M EMA (now at 1.5928) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

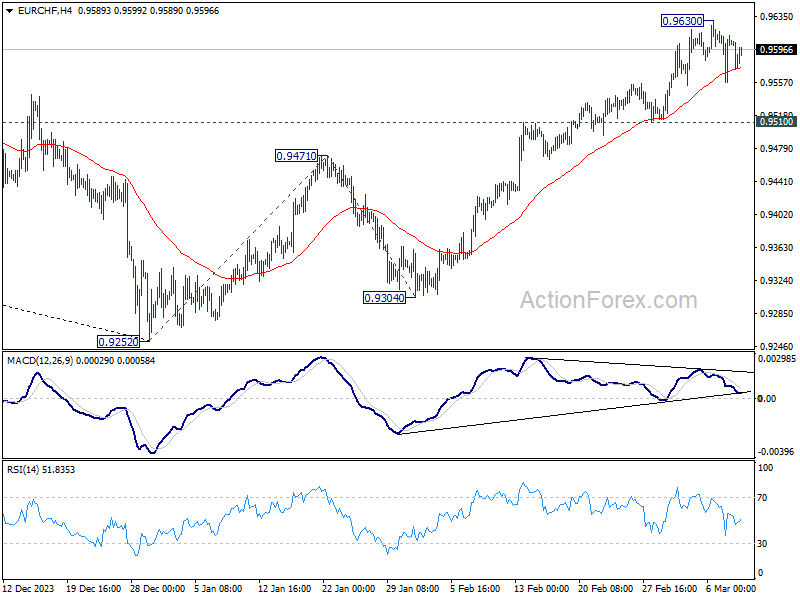

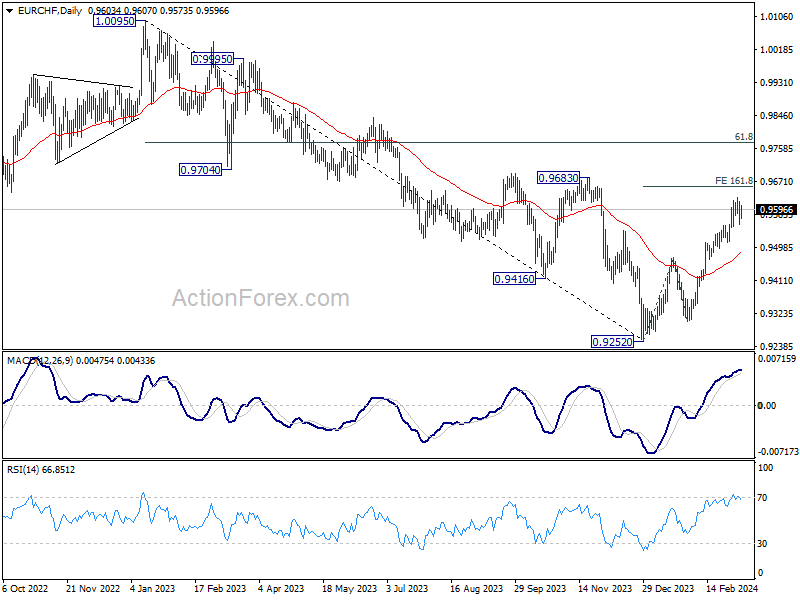

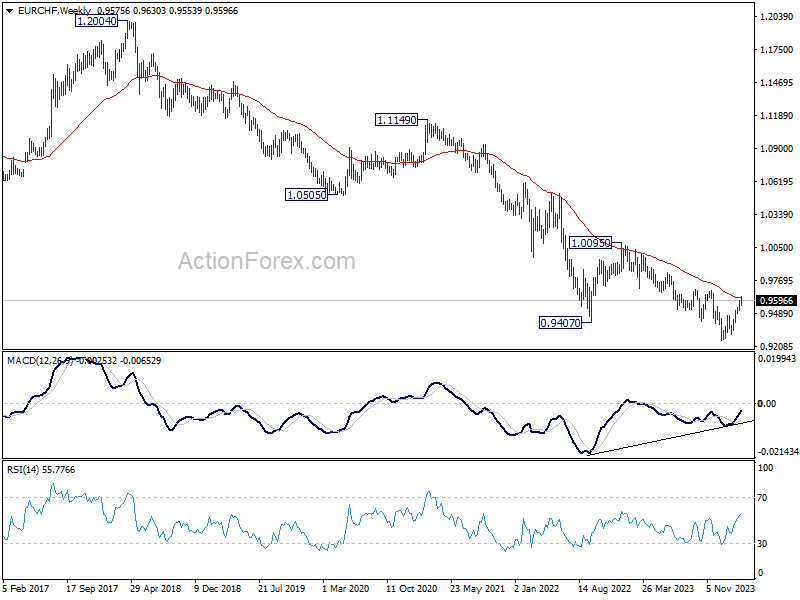

EUR/CHF Weekly Outlook

EUR/CHF edged higher to 0.9630 last week but turned sideway since then. Initial bias remains neutral this week first. As long as 0.9510 support holds, further rally is still expected. On the upside, break of 0.9630 will resume the rise from 0.9252 and target 161.8% projection of 0.9252 to 0.9471 from 0.9304 at 0.9658 next. However, considering bearish divergence condition in 4H MACD, firm break of 0.9510 will turn bias back to the downside for deeper fall.

In the bigger picture, as long as 0.9683 resistance holds, rebound from 0.9252 are seen as a corrective move only. Larger down trend is expected to resume through 0.9252 after the correction completes. However, firm break of 0.9683 and sustained trading above 55 W EMA (now at 0.9620) will argue that 0.9252 is already a medium term bottom. Stronger rise would then be seen 61.8% retracement of 1.0095 to 0.9252 at 0.9773 and above.

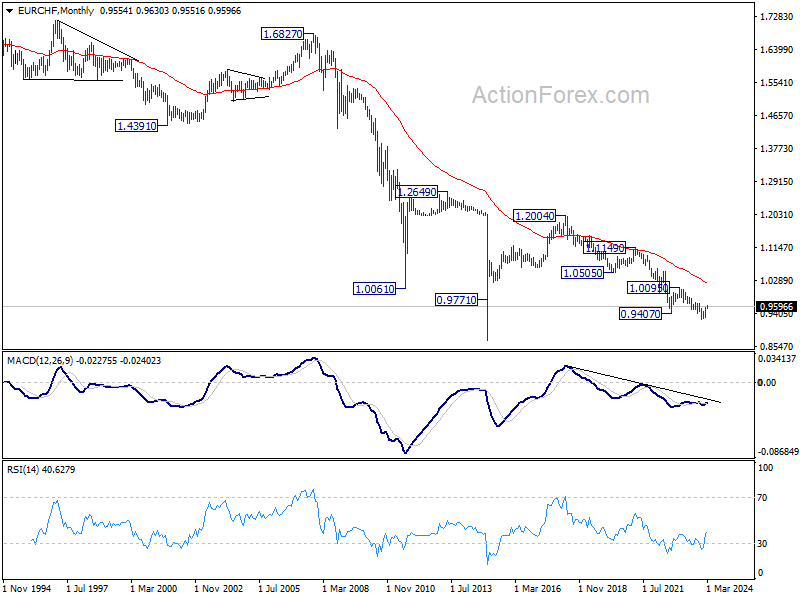

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Firm break of 1.0095 resistance is needed to be the first sign of long term bottoming. Otherwise, outlook will remain bearish.

Summary 3/11 – 3/15

Monday, Mar 11, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | GDP Q/Q Q4 F | 0.30% | -0.10% |

| 23:50 | JPY | GDP Deflator Y/Y Q4 F | 3.80% | 3.80% |

| 23:50 | JPY | Money Supply M2+CD Y/Y Feb | 2.40% | 2.40% |

| 06:00 | JPY | Machine Tool Orders Y/Y Feb P | -14.10% | |

| 23:30 | AUD | Westpac Consumer Confidence (Mar) | 6.20% | |

| 23:50 | JPY | PPI Y/Y Feb | 0.50% | 0.20% |

| 23:50 | JPY | BSI Large Manufacturing Index Q1 | 6.2 | 5.7 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | GDP Q/Q Q4 F | |

| Forecast: 0.30% | Previous: -0.10% | ||

| 23:50 | JPY | GDP Deflator Y/Y Q4 F | |

| Forecast: 3.80% | Previous: 3.80% | ||

| 23:50 | JPY | Money Supply M2+CD Y/Y Feb | |

| Forecast: 2.40% | Previous: 2.40% | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Feb P | |

| Forecast: | Previous: -14.10% | ||

| 23:30 | AUD | Westpac Consumer Confidence (Mar) | |

| Forecast: | Previous: 6.20% | ||

| 23:50 | JPY | PPI Y/Y Feb | |

| Forecast: 0.50% | Previous: 0.20% | ||

| 23:50 | JPY | BSI Large Manufacturing Index Q1 | |

| Forecast: 6.2 | Previous: 5.7 | ||

Tuesday, Mar 12, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Feb | 1 | |

| 00:30 | AUD | NAB Business Conditions Feb | 6 | |

| 07:00 | EUR | Germany CPI M/M Feb F | 0.40% | 0.40% |

| 07:00 | EUR | Germany CPI Y/Y Feb F | 2.50% | 2.50% |

| 07:00 | GBP | Claimant Count Change Feb | 20.3K | 14.1K |

| 07:00 | GBP | ILO Unemployment Rate (3M) Jan | 3.80% | 3.80% |

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Jan | 5.70% | 5.80% |

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jan | 6.20% | 6.20% |

| 10:00 | USD | NFIB Business Optimism Index Feb | 90.7 | 89.9 |

| 12:30 | USD | CPI M/M Feb | 0.40% | 0.30% |

| 12:30 | USD | CPI Y/Y Feb | 3.10% | 3.10% |

| 12:30 | USD | CPI Core M/M Feb | 0.30% | 0.40% |

| 12:30 | USD | CPI Core Y/Y Feb | 3.70% | 3.90% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Feb | |

| Forecast: | Previous: 1 | ||

| 00:30 | AUD | NAB Business Conditions Feb | |

| Forecast: | Previous: 6 | ||

| 07:00 | EUR | Germany CPI M/M Feb F | |

| Forecast: 0.40% | Previous: 0.40% | ||

| 07:00 | EUR | Germany CPI Y/Y Feb F | |

| Forecast: 2.50% | Previous: 2.50% | ||

| 07:00 | GBP | Claimant Count Change Feb | |

| Forecast: 20.3K | Previous: 14.1K | ||

| 07:00 | GBP | ILO Unemployment Rate (3M) Jan | |

| Forecast: 3.80% | Previous: 3.80% | ||

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Jan | |

| Forecast: 5.70% | Previous: 5.80% | ||

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jan | |

| Forecast: 6.20% | Previous: 6.20% | ||

| 10:00 | USD | NFIB Business Optimism Index Feb | |

| Forecast: 90.7 | Previous: 89.9 | ||

| 12:30 | USD | CPI M/M Feb | |

| Forecast: 0.40% | Previous: 0.30% | ||

| 12:30 | USD | CPI Y/Y Feb | |

| Forecast: 3.10% | Previous: 3.10% | ||

| 12:30 | USD | CPI Core M/M Feb | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 12:30 | USD | CPI Core Y/Y Feb | |

| Forecast: 3.70% | Previous: 3.90% | ||

Wednesday, Mar 13, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 07:00 | GBP | GDP M/M Jan | 0.20% | -0.10% |

| 07:00 | GBP | Manufacturing Production M/M Jan | 0.00% | 0.80% |

| 07:00 | GBP | Manufacturing Production Y/Y Jan | 2.00% | 2.30% |

| 07:00 | GBP | Industrial Production M/M Jan | 0.00% | 0.60% |

| 07:00 | GBP | Industrial Production Y/Y Jan | 0.70% | 0.60% |

| 07:00 | GBP | Goods Trade Balance (GBP) Jan | -15.0B | -14.0B |

| 10:00 | EUR | Eurozone Industrial Production M/M Jan | -1.00% | 2.60% |

| 13:00 | GBP | NIESR GDP Estimate (3M) Feb | -0.10% | |

| 14:30 | USD | Crude Oil Inventories | 1.4M |

| GMT | Ccy | Events | |

|---|---|---|---|

| 07:00 | GBP | GDP M/M Jan | |

| Forecast: 0.20% | Previous: -0.10% | ||

| 07:00 | GBP | Manufacturing Production M/M Jan | |

| Forecast: 0.00% | Previous: 0.80% | ||

| 07:00 | GBP | Manufacturing Production Y/Y Jan | |

| Forecast: 2.00% | Previous: 2.30% | ||

| 07:00 | GBP | Industrial Production M/M Jan | |

| Forecast: 0.00% | Previous: 0.60% | ||

| 07:00 | GBP | Industrial Production Y/Y Jan | |

| Forecast: 0.70% | Previous: 0.60% | ||

| 07:00 | GBP | Goods Trade Balance (GBP) Jan | |

| Forecast: -15.0B | Previous: -14.0B | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Jan | |

| Forecast: -1.00% | Previous: 2.60% | ||

| 13:00 | GBP | NIESR GDP Estimate (3M) Feb | |

| Forecast: | Previous: -0.10% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 1.4M | ||

Thursday, Mar 14, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:01 | GBP | RICS Housing Price Balance Feb | -10% | -18% |

| 07:30 | CHF | PPI M/M Feb | 0.20% | -0.50% |

| 07:30 | CHF | PPI Y/Y Feb | -2.30% | |

| 12:30 | CAD | Manufacturing Sales M/M Jan | 0.30% | -0.70% |

| 12:30 | USD | Retail Sales M/M Feb | 0.50% | -0.80% |

| 12:30 | USD | Retail Sales ex Autos M/M Feb | 0.40% | -0.60% |

| 12:30 | USD | PPI M/M Feb | 0.30% | 0.30% |

| 12:30 | USD | PPI Y/Y Feb | 1.10% | 0.90% |

| 12:30 | USD | PPI Core M/M Feb | 0.20% | 0.50% |

| 12:30 | USD | PPI Core Y/Y Feb | 2.00% | 2.00% |

| 12:30 | USD | Initial Jobless Claims (Mar 8) | 218K | 217K |

| 14:00 | USD | Business Inventories Jan | 0.30% | 0.40% |

| 14:30 | USD | Natural Gas Storage | -40B | |

| 21:30 | NZD | Business NZ PMI Feb | 47.3 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:01 | GBP | RICS Housing Price Balance Feb | |

| Forecast: -10% | Previous: -18% | ||

| 07:30 | CHF | PPI M/M Feb | |

| Forecast: 0.20% | Previous: -0.50% | ||

| 07:30 | CHF | PPI Y/Y Feb | |

| Forecast: | Previous: -2.30% | ||

| 12:30 | CAD | Manufacturing Sales M/M Jan | |

| Forecast: 0.30% | Previous: -0.70% | ||

| 12:30 | USD | Retail Sales M/M Feb | |

| Forecast: 0.50% | Previous: -0.80% | ||

| 12:30 | USD | Retail Sales ex Autos M/M Feb | |

| Forecast: 0.40% | Previous: -0.60% | ||

| 12:30 | USD | PPI M/M Feb | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 12:30 | USD | PPI Y/Y Feb | |

| Forecast: 1.10% | Previous: 0.90% | ||

| 12:30 | USD | PPI Core M/M Feb | |

| Forecast: 0.20% | Previous: 0.50% | ||

| 12:30 | USD | PPI Core Y/Y Feb | |

| Forecast: 2.00% | Previous: 2.00% | ||

| 12:30 | USD | Initial Jobless Claims (Mar 8) | |

| Forecast: 218K | Previous: 217K | ||

| 14:00 | USD | Business Inventories Jan | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: -40B | ||

| 21:30 | NZD | Business NZ PMI Feb | |

| Forecast: | Previous: 47.3 | ||

Friday, Mar 15, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 04:30 | JPY | Tertiary Industry Index M/M Jan | 0.10% | 0.70% |

| 09:30 | GBP | Consumer Inflation Expectations | 3.30% | |

| 10:00 | EUR | Italy Retail Sales M/M Jan | 0.20% | -0.10% |

| 12:15 | CAD | Housing Starts Y/Y Feb | 227K | 224K |

| 12:30 | CAD | Wholesale Sales M/M Jan | -0.60% | 0.30% |

| 12:30 | USD | NY Empire State Manufacturing Index Mar | -6.5 | -2.4 |

| 12:30 | USD | Import Price Index M/M Feb | 0.20% | 0.80% |

| 13:15 | USD | Industrial Production M/M Feb | 0.00% | -0.10% |

| 14:00 | USD | Michigan Consumer Sentiment Index Mar P | 77.3 | 76.9 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 04:30 | JPY | Tertiary Industry Index M/M Jan | |

| Forecast: 0.10% | Previous: 0.70% | ||

| 09:30 | GBP | Consumer Inflation Expectations | |

| Forecast: | Previous: 3.30% | ||

| 10:00 | EUR | Italy Retail Sales M/M Jan | |

| Forecast: 0.20% | Previous: -0.10% | ||

| 12:15 | CAD | Housing Starts Y/Y Feb | |

| Forecast: 227K | Previous: 224K | ||

| 12:30 | CAD | Wholesale Sales M/M Jan | |

| Forecast: -0.60% | Previous: 0.30% | ||

| 12:30 | USD | NY Empire State Manufacturing Index Mar | |

| Forecast: -6.5 | Previous: -2.4 | ||

| 12:30 | USD | Import Price Index M/M Feb | |

| Forecast: 0.20% | Previous: 0.80% | ||

| 13:15 | USD | Industrial Production M/M Feb | |

| Forecast: 0.00% | Previous: -0.10% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Mar P | |

| Forecast: 77.3 | Previous: 76.9 | ||

The Weekly Bottom Line: A Busy Week in Washington

U.S. Highlights

- The U.S. economy added 275k jobs in February, but job gains in the prior two months were revised down significantly and the unemployment rate ticked up to 3.9%.

- In his testimony before Congress this week, Federal Reserve Chair Powell noted that economic resilience gave the FOMC time to assess the sustainability of current disinflation trends.

- Congress is set to pass half of the federal spending bills for the 2024 fiscal year this week, five months and four continuing resolutions after the fiscal year began in October.

Canadian Highlights

- The Bank of Canada (BoC) maintained the overnight rate at 5.00% and stated that it’s still too early to consider lowering the policy rate.

- Markets are leaning towards a first interest rate cut in June, in line with our view.

- Canada’s economy gained a solid 41k new jobs in February, but given continued strength in labour force growth, the unemployment rate ticked higher. Wage growth also moderated, suggesting labour markets are continuing to cool.

U.S. – A Busy Week in Washington

With the first quarter entering its final weeks, we received a host of important economic data this week that will help form expectations for the year ahead. This included a labor market pulse check in addition to Federal Reserve Chair Powell’s semi-annual testimony before Congress. Equity markets continued to notch record highs, with the S&P 500 rising 0.8% on the week, while Treasury yields fell by roughly 10 basis-points as of the time of writing.

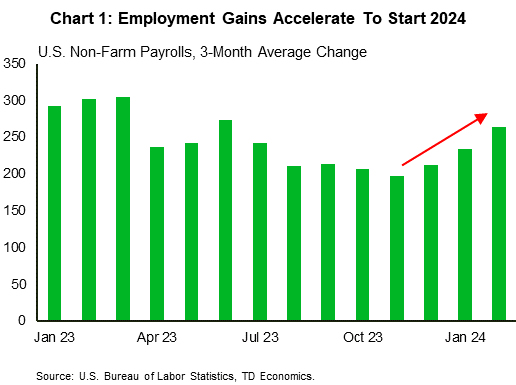

The headline release for this week was Friday’s employment report, which showed that 275k jobs had been added in February. While job gains in the prior two months were revised down by a considerable 167k jobs, the economy still saw solid and accelerating job growth moving into 2024 (Chart 1). However, the unemployment rate ticked up by 0.2 percentage-points to 3.9%, in part due to a return of positive labor force growth. On aggregate, the labor market remains healthy but is continuing to moderate towards a more balanced state. This will be welcome news for the Federal Reserve as they target their dual mandate of maximum sustainable employment and price stability.

The shift towards a more balanced risk outlook was also noted in Chair Powell’s testimony to Congressional committees this week. In his remarks he stated that the resilience of the economy and the labor market gave the FOMC time to assess the sustainability of current disinflation trends. While Powell did note that it would likely be necessary to implement less restrictive policy this year, he cautioned against the risk of easing pre-maturely. Solid job growth and an economy that continues to exhibit above-trend growth support Chair Powell’s assessment and our expectation that the FOMC will hold off until July to begin lowering interest rates.

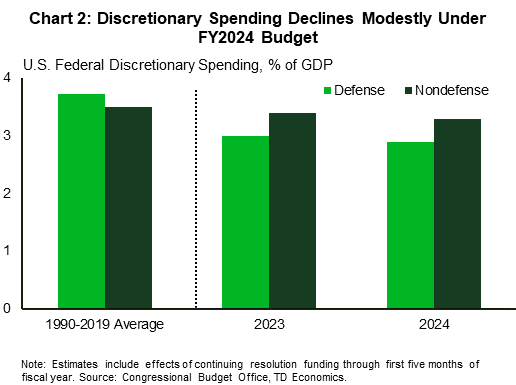

Also on Capitol Hill this week, Congress passed half of the federal spending bills for fiscal year 2024. With funding for six federal departments set to expire on Friday – legislated by the fourth continuing resolution of this cycle passed last week – the House passed a package of appropriation bills on Wednesday for the departments subject to the deadline. Senate approval and the President’s signature is expected ahead of the midnight deadline on Friday. The other six appropriations bills will need to be passed ahead of their March 22nd deadline, but aggregate spending levels are expected to be consistent with the limits previously agreed to by Congress (Chart 2). Removing the near-term risk of a government shutdown is undoubtedly positive, but ongoing structural deficits leave the sustainability of the national debt a long-term risk, which was also noted by Chair Powell in Congress this week.

In the near-term, markets will be closely watching the February CPI inflation data release next week, which is expected to show a deceleration from January’s unexpected uptick. Further progress on disinflation will be required before the Federal Reserve considers shifting its current policy stance.

Canada – Bank of Canada Holds the Line

To no one's surprise, the Bank of Canada (BoC) maintained the overnight policy rate at 5.00% at this week's meeting. When the Bank will start to cut interest rates is still top of mind for market watchers. However, Governor Macklem offered no clues to when this could occur, stating "it's too early to consider lowering the policy rate". January's downside surprise in headline and core inflation was not enough to move the BoC off of their concern that upside risks to the inflation outlook are still present—though they continue to acknowledge progress. As it stands, the narrative remains the same: the BoC is afforded the time to wait to see more evidence that inflation is moving durably back to 2% before lowering interest rates.

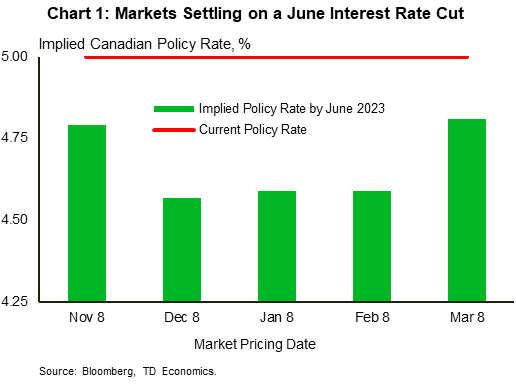

In the wake of the decision, markets moved the probability of a June cut slightly lower, though June still stands as the most likely timing for a first rate cut (~80%). This pricing looks like where it was back in November, despite reactive pricing movements in the interim in the wake of incoming data (Chart 1). We sit in the June-cut camp, taking cues from the fact that economic growth continues to sputter, labour markets are balancing, and core inflation measures, while still a bit elevated, are being driven by shelter prices.

The focus now shifts to the April 10th policy meeting where the BoC will release a fresh set of forecasts in their Monetary Policy Report (MPR). These updates may start to lay the foundation for interest rate cuts. Notably, since the last MPR released in January, inflation for Q4-2023 came in a touch lower than projected (3.2% vs 3.3% y/y), while Q4-2023 growth came in a touch stronger.

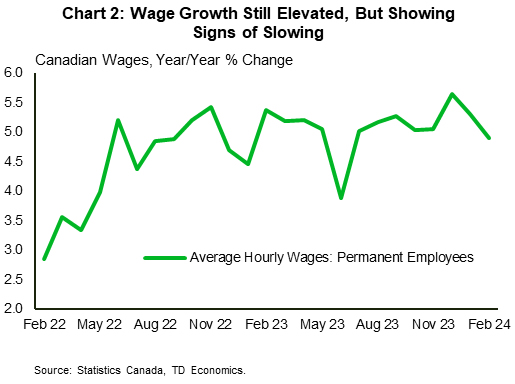

February's jobs data saw a healthy 40.7k net new jobs, driven by full-time employment, but details under the hood were weak. The unemployment rate nudged back up a tenth to 5.8% as labour market gains continue to outpace employment growth. Meanwhile, hours worked tallied a trend-like gain. The pace of wage growth has been a thorn in the side for the BoC, having been stuck above 5% y/y for seven consecutive months. Fortunately, wage growth dipped back into the high 4% y/y range in February, the softest reading since June 2023 (Chart 2). Still, more progress on this front is likely desired by the BoC.

Finally, international trade data for the month of January showed that both import and export activity are slowing. The sharp drop in import volumes reflects weakness in the Canadian consumer. This is consistent with Statistics Canada's guidance for January's retail sales and our own view of weaker spending over the first half of the year. Recall that last quarter, strong export activity contributed most to Canada's GDP growth. Early tracking is showing trade may not be as much of a tailwind to Q1-2024 growth.

Now we sit and wait. One more inflation and labour market reading, as well as the release of the Bank of Canada's Business Outlook Survey in early-April, are due before the BoC's next meeting. These developments could set the tone for a potential communication shift from the BoC as rate cuts come closer to fruition.

Weekly Economic & Financial Commentary: G10 Central Banks Sitting Tight

Summary

United States: Labor Market Cooling but Far from Cold

- With fresh updates on a variety of indicators, particularly those associated with the labor market, the past week's performance continued to help shape the narrative heading into the March FOMC meeting. Beating expectations, total nonfarm payrolls increased 275K in February.

- Next week: CPI (Tue.), Retail Sales (Thu.), Industrial Production (Fri.)

International: G10 Central Banks Sitting Tight

This week, both the Bank of Canada and European Central Bank held policy rates steady. Inflation concerns in Canada and the Eurozone will, in our view, see the respective central banks waiting until June to initiate rate cuts. Japan also made headlines this week, but despite buzz growing around the idea of a March rate hike, we maintain our forecast for an April BoJ move.

- Next week: Brazil CPI (Tue.), U.K. Monthly GDP (Wed.), Sweden CPI (Thu.)

Interest Rate Watch: Markets Come Around to the Dot Plot

- Financial markets entered 2024 anticipating more monetary policy easing than the FOMC's December dot plot signaled. Fast-forward to today and the market's pricing of rate cuts this year seems more in line with the Fed's.

Credit Market Insights: Locked and Loaded: NFC Sector Looks Solid

- Relative to Q1-2022, when interest rates began their ascent, total non-financial corporate debt has expanded 5%. The muted rise has coincided with corporate bond yields that are hovering well above their norms a few years ago. With borrowing costs elevated, why hasn't business debt shot meaningfully higher?

Topic of the Week: Can't Grow Old Without Her: Women's Central Role in a Growing Eldercare Economy

- To celebrate International Women's Day, we explore how the aging of the U.S. population stands to affect women as they shoulder a disproportionate share of unpaid care responsibilities but also play an outsized role in providing paid care. As the population rapidly ages, it won't be able to do so gracefully without her.

U.S. Inflation, Spending Data Will Help Set Fed Rate Cut Expectations

U.S. inflation numbers will be in the spotlight on Tuesday as U.S. Federal Reserve officials consider when it might be appropriate to begin lowering interest rates.

Inflation pressures eased significantly last year largely without the economic pain that was feared when the Fed began aggressively hiking interest rates. But a resilient economic backdrop and strong consumer spending also means there is a risk that price growth could reaccelerate—and those fears grew after a broad-based upward surprise in January’s inflation numbers.

We look for a softer price report for February with consumer price index growth holding at 3.1% on higher energy prices, but slower “core” (excluding food and energy) price growth. Gasoline prices jumped 4.4% by our count in February and food prices should continue to edge higher from last month, albeit at a slower rate. Core inflation is expected to slow to 3.7% from a year ago on a 0.3% increase from January. Shelter costs still account for a disproportionate share of the price growth and that is expected to continue slowing as moderation in home rent growth passes through to lease renewals. Consumer demand is still strong, but we expect a 0.7% increase in U.S. retail sales on Thursday after the CPI report. This will largely be a result of higher gasoline prices and will not fully recover from the 0.8% drop in January.

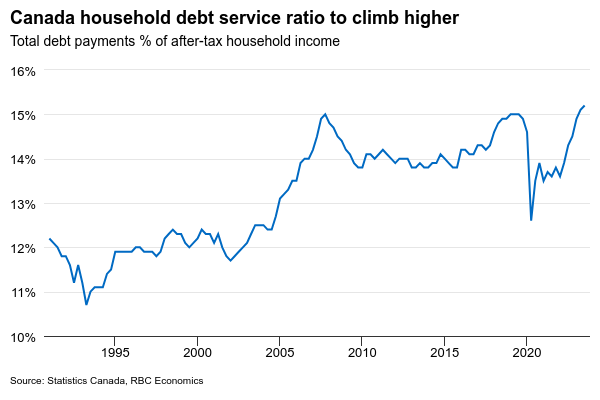

In Canada, fourth quarter national balance sheet numbers should show the household debt service ratio rising to another new record as higher interest rates pass through to debt payments. We expect household net worth was little changed with strong equity markets boosting the value of financial asset holdings and offsetting a pullback in house prices. The household credit market debt-to-income ratio likely edged lower with household income growth outpacing debt growth.

Week ahead data watch

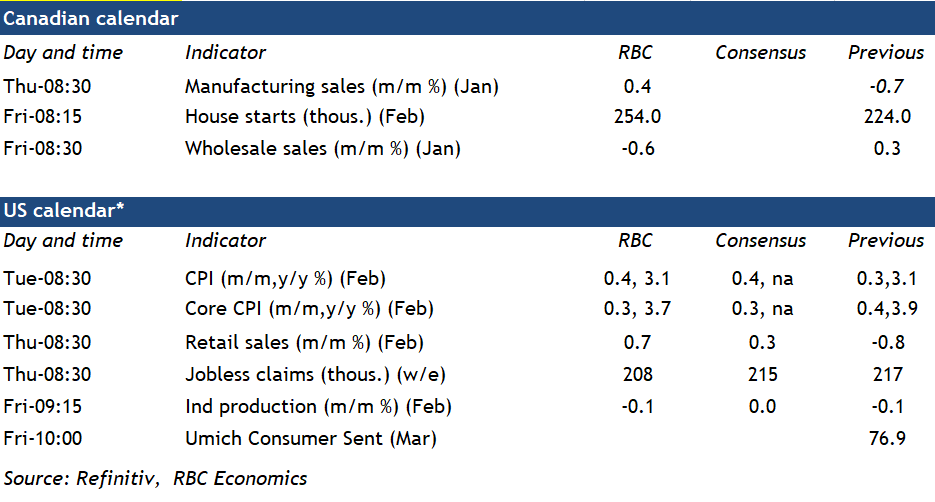

Manufacturing sales likely inched up 0.4% in January, according to Statistics Canada’s advance indicator. Sales in transportation equipment and machinery subsectors led the growth. The Industrial Product Price Index fell about 0.8% from December on a seasonally adjusted basis, indicating an upswing in sales volume.

Statscan’s early indicator showed a dip (-0.6%) in January “core” wholesale sales (excluding petroleum products, other hydrocarbons, oilseed and grain) with sector-wide declines, especially in building materials and the supplies subsector.

Housing starts are expected to rise to 254,000 in February, consistent with the bouncing back of building permits in January.

Will US CPI Data Come to Dollar’s Rescue?

- Weak ISM PMIs and dovish Powell hurt the dollar

- Investors add to their June rate cut bets

- US CPI data the next test for the greenback

- The data is scheduled for Tuesday at 12:30 GMT

After Powell’s testimony, investors see June cut a done deal

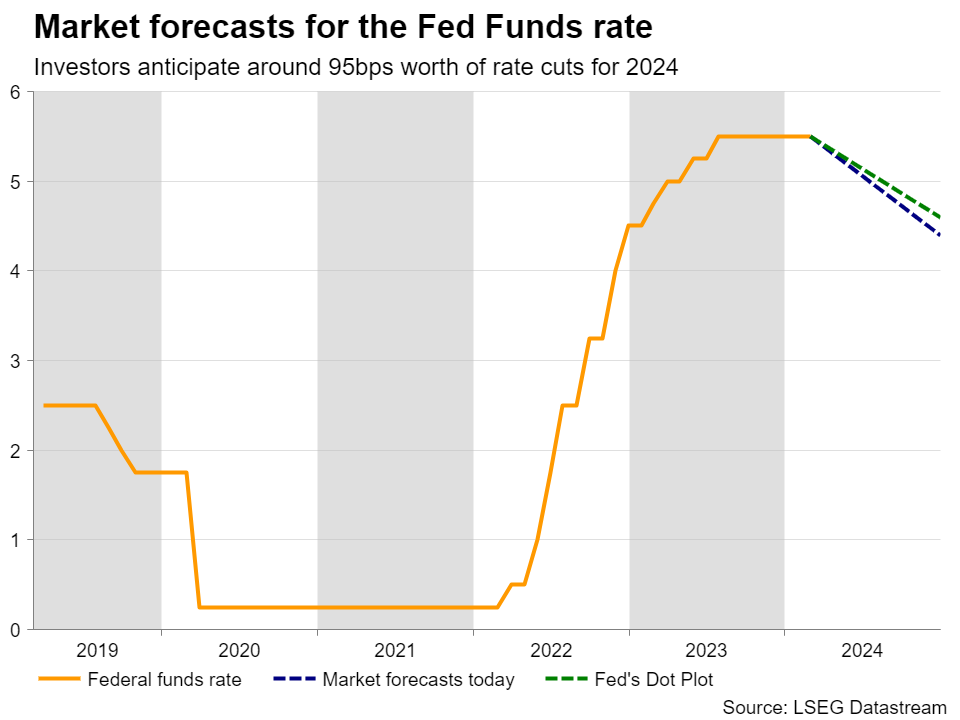

There has been a notable repricing in market expectations with regards to the Fed’s future course of action since the start of the year. From penciling in around 160bps worth of rate cuts by December, at some point the market got confident that the Fed will reduce interest rates by only 80bps, just five points more than the Fed’s December projections of 75bps. What has led to this repricing was data pointing to a US economy firing on all cylinders, a still-tight labor market, stickier than expected inflation, and a less-dovish-than-expected Fed.

However, after the disappointing ISM PMIs and the Congressional testimony by Fed Chair Powell, investors have added back some basis points worth of cuts, now expecting interest rates to end the year 95bps below current levels.

During his second Congressional testimony, before the Senate Banking Committee, the Fed Chief said that the central bank was “not far” from gaining the confidence it needs to begin cutting interest rates, although he was reluctant to declare the inflation battle had been won. His comments refueled bets that a first quarter-point cut will be delivered in June, with the probability of such an action rising to around 95%.

Will US inflation get closer to the Fed’s 2% objective?

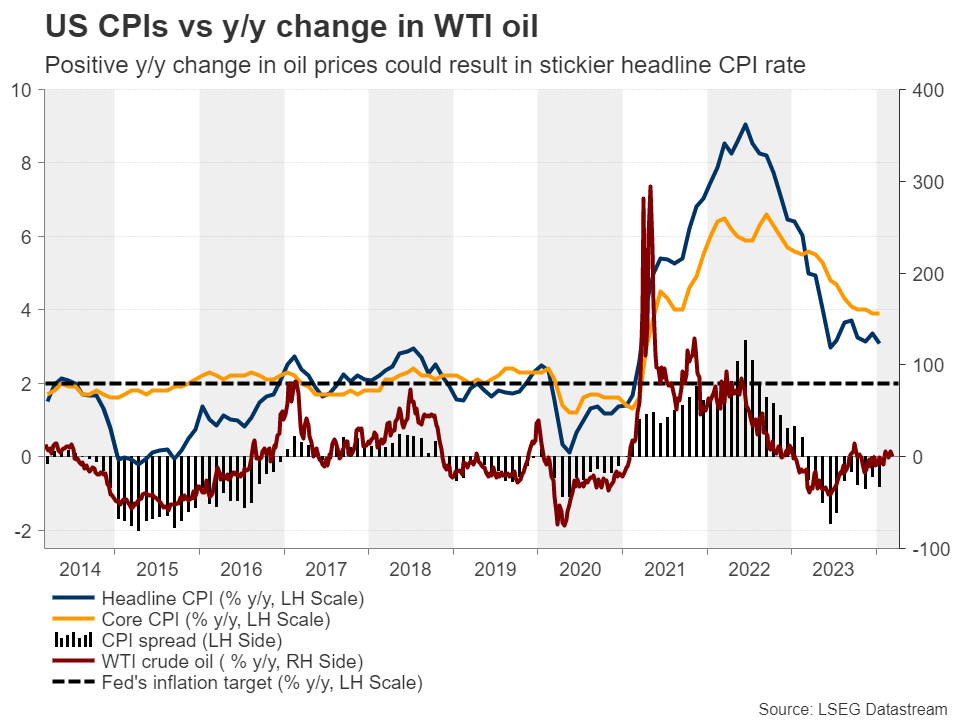

With all that in mind, the spotlight next week is likely to turn to Tuesday’s CPI data for February. The forecasts suggest that the headline rate remained unchanged at 3.1% y/y, while the core one is expected to have slid to 3.7% y/y from 3.9%. According to both the ISM manufacturing and non-manufacturing PMIs, prices continued to increase in February, but at a slower pace than in January, corroborating the forecast for the core CPI rate, while the fact that the year-on-year change in oil prices turned somewhat positive lately, supports the notion for a sticky headline rate.

Therefore, with headline inflation not cooling, the US dollar may initially receive some support, but a further slowdown in underlying price pressures is unlikely to tempt investors to reduce their June cut bets as it may add to Fed officials’ confidence that inflation is moving sustainably towards their objective.

The dollar could soon give back any headline-related gains and resume its recent short-term downtrend, while equities are likely to continue marching north, as expectations of lower interest rates are a positive for present values of high-growth tech firms, which are usually valued by discounting expected free cash flows for the quarters and years ahead.

Is an upward revision in the dot plot possible?

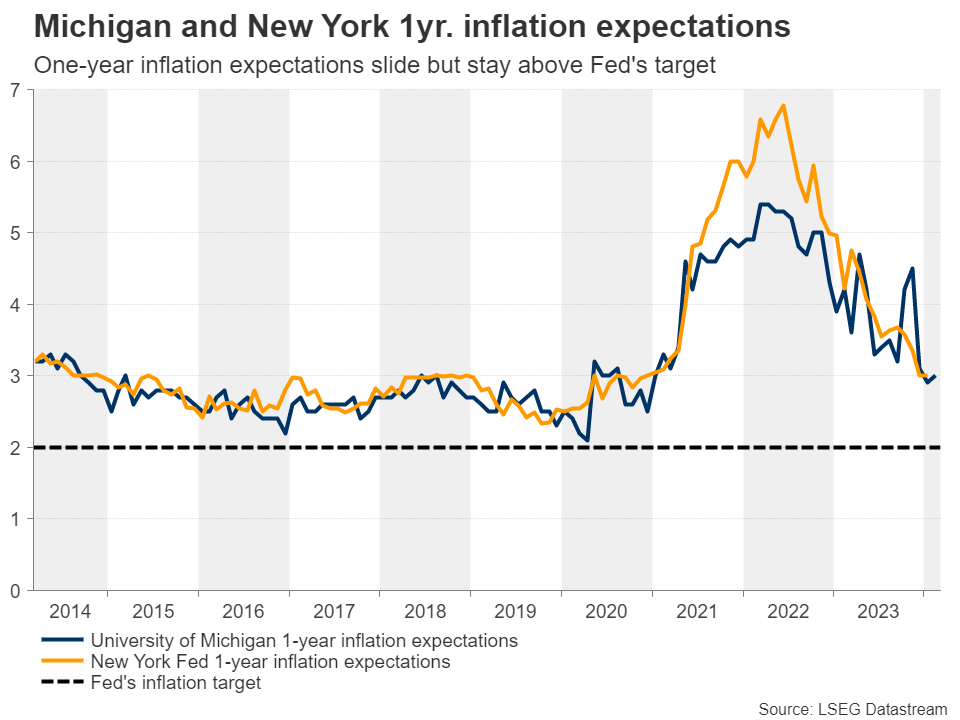

For the dollar to stage a strong comeback, the Fed may need to revise up its dot plot when it meets on March 20. Although Powell sounded more dovish than expected when testifying before Congress, other policymakers have been vocal about their preference of fewer rate cuts than the December dot plot pointed to. Atlanta Fed President Bostic said recently that only two rate cuts may be appropriate by the end of his year, while Minneapolis Fed President Kashkari talked about the possibility of even only one reduction. What’s more, both the University of Michigan and the New York Fed 1-year inflation expectations are both resting at 3.0%, suggesting no material progress in lowering the inflation consumer expect.

Having said all that though, Kashkari is not a voting member this year, and Bostic is the only member who clearly favored less than three cuts, at least until now. So, although an upside revision in the Fed’s interest rate projections is not totally off the cards, especially with the US economy still performing better than its major peers, it currently appears to be a less likely case.

Dollar index completes a failure swing top

From a technical standpoint, the dollar index accelerated its slide in the last couple of days, breaking below the key zone of 103.65 and completing a failure swing top formation. The index is now ready to challenge the 102.65 zone, where a dip could aim for the 102.00 zone. For the outlook to change to bullish, the index may need to climb all the way above the psychological number of 105.00, which was last tested on February 14.