Sample Category Title

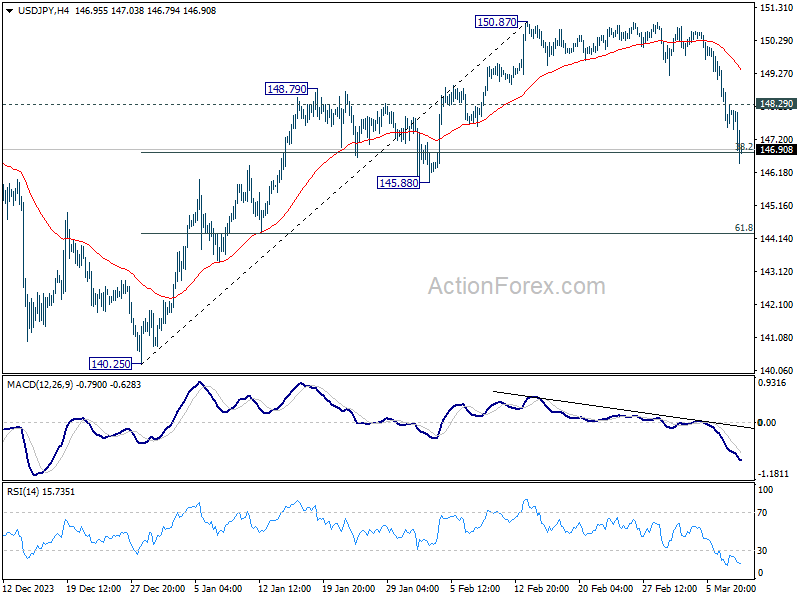

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.28; (P) 148.34; (R1) 149.08; More...

Intraday bias in USD/JPY remains on the downside at this point. Sustained break of 38.2% retracement of 140.25 to 150.87 at 146.81 will argue that fall from 150.87 is reversing the whole rally from 140.25. In this case, deeper decline would be seen to 61.8% retracement at 144.30 and below. Nevertheless, strong support from 146.81, followed by break of 148.29 minor resistance resistance, will argue that fall from 150.87 is merely a correction, which has completed already.

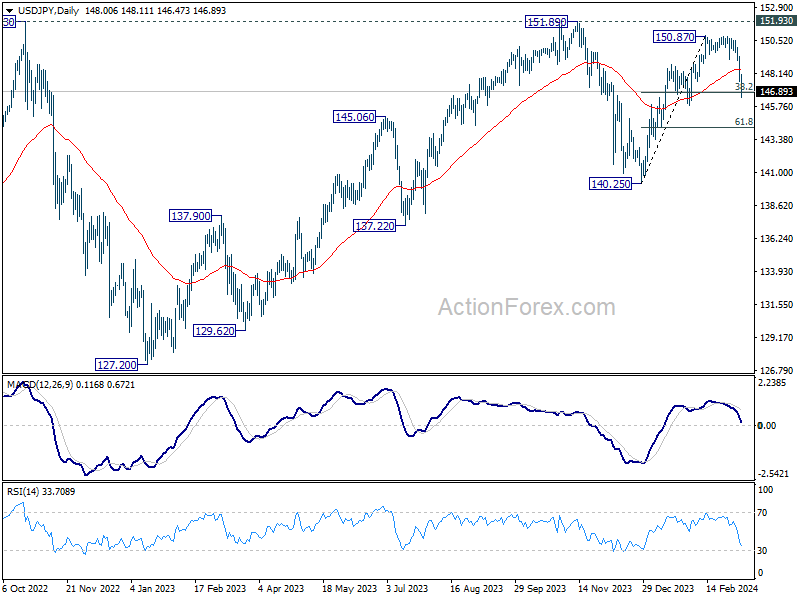

In the bigger picture, outlook is mixed up as fall from 150.87 accelerates lower. Sustained trading below 55 D EMA (now at 148.45) will open up the case that corrective pattern from 151.89 (2023 high) is extending, with fall from 150.87 as the third leg. In this case, deeper decline would be seen to 140.25 support or below. Nevertheless, strong bounce from 55 D EMA will retain near term bullishness for at least another take on 151.89.

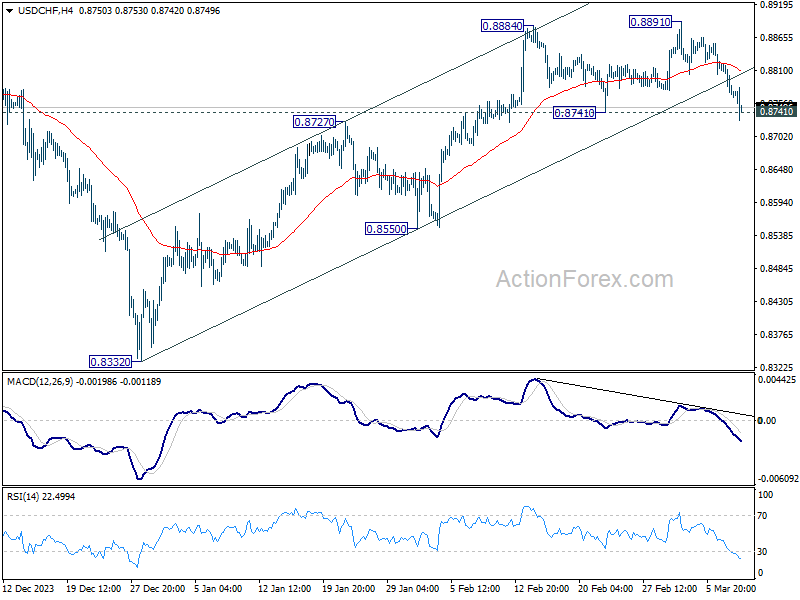

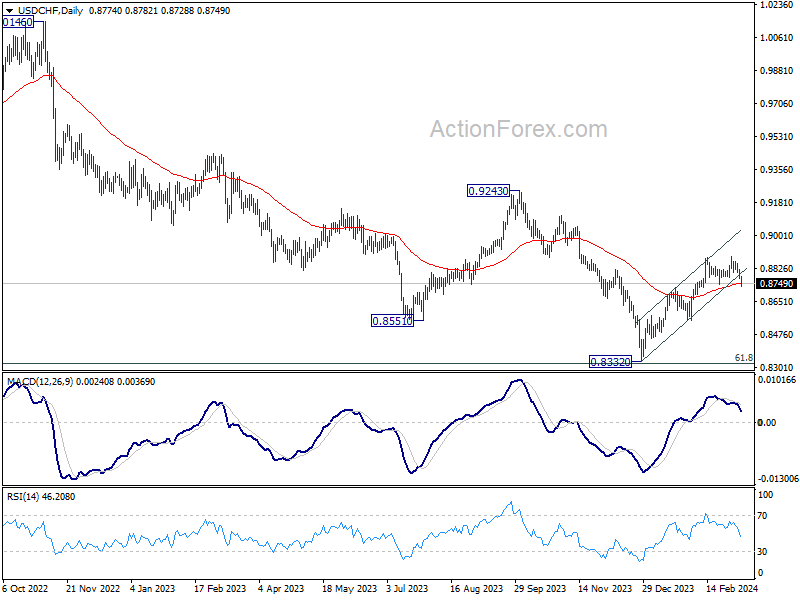

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8757; (P) 0.8793; (R1) 0.8813; More....

Immediate focus is now on 0.8741 support in USD/CHF. Decisive break there will argue that whole rebound from 0.8332 has completed at 0.8891. Deeper fall would then be seen back to 0.8550 support next. Nevertheless, strong bounce from current level will retain near term bullishness for another rise through 0.8891 later.

In the bigger picture, a medium term bottom should be formed at 0.8332, on bullish convergence condition in W MACD, just ahead of 0.8317 long term fibonacci support. It's still early to decide if the larger down trend from 1.0146 (2022 high) is reversing. But further rise should be seen to 0.9243 resistance even as a correction.

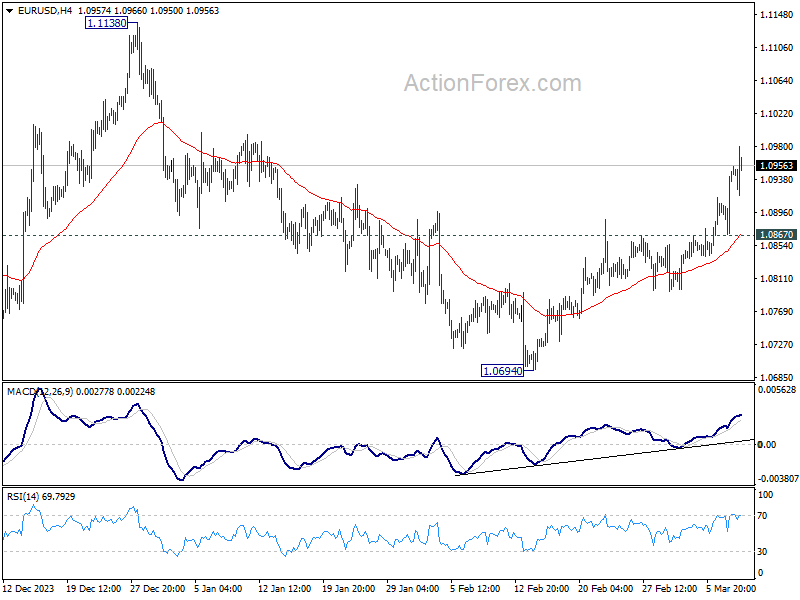

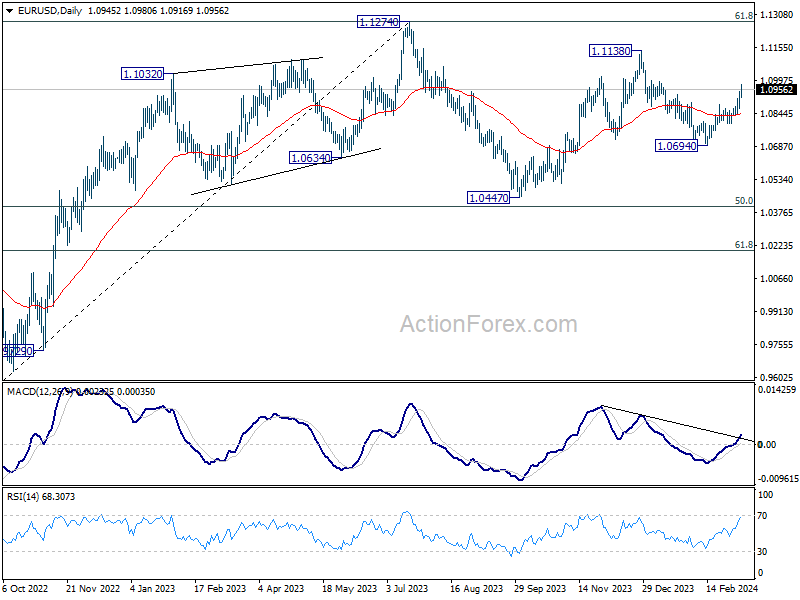

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0894; (P) 1.0922; (R1) 1.0975; More...

EUR/USD's rally continues in early US session and intraday bias stays on the upside. Current rise from 1.0694 should target a retest on 1.1138 resistance next. On the downside, below 1.0867 minor support will turn intraday bias neutral and bring consolidations first.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

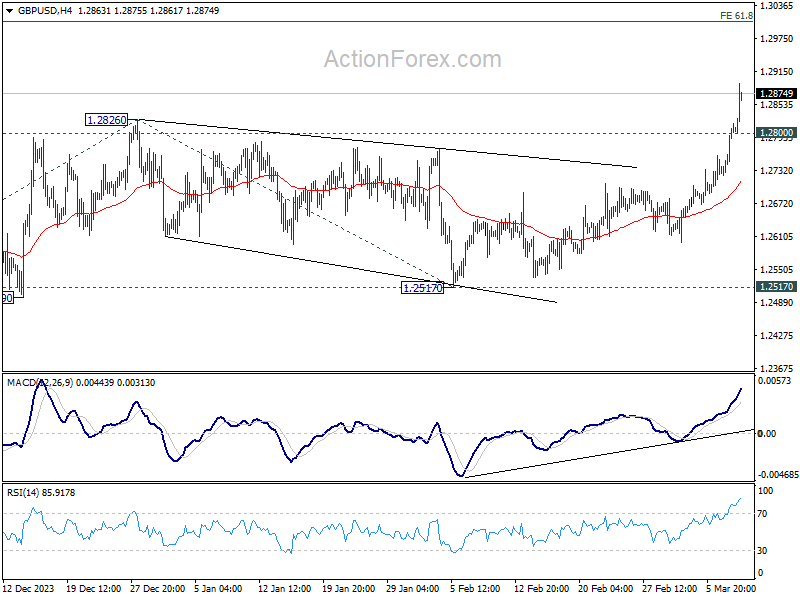

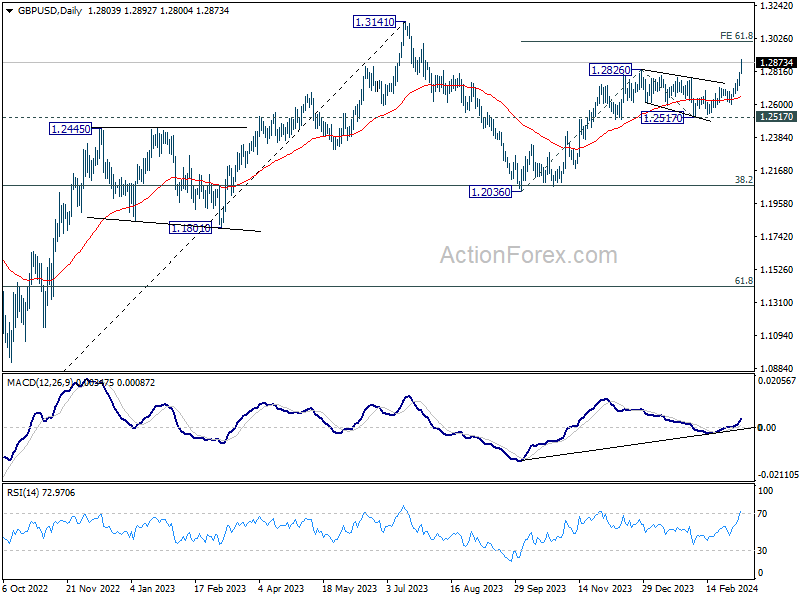

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2750; (P) 1.2781; (R1) 1.2839; More...

GBP/USD accelerates to as high as 1.2892 so far today. The strong break of 1.2826 resistance confirm resumption of whole rally from 1.2036. Intraday bias stays on the upside for 61.8% projection of 1.2036 to 1.2826 from 1.2517 at 1.3005 next. On the downside, below 1.2800 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which could be still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

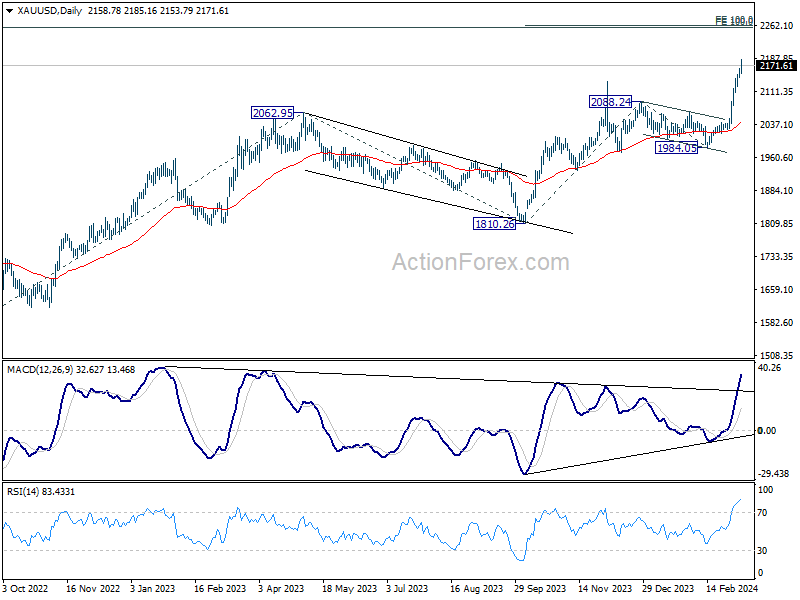

Dollar Slump Intensifies as Jobs Report Underwhelms, Gold at New Record

Dollar's decline accelerated in the early US session, triggered by disappointing non-farm payroll data. Despite a seemingly robust headline job growth figure for February, the substantial downward revision of January's numbers cast a shadow, marking the overall report as a miss. Moreover, the unemployment rate's unexpected jump and the below-forecast earnings growth further dented investor sentiment towards the greenback.

As for the day, Japanese Yen stands out as the strongest currency for now, buoyed by reports from Jiji news suggesting BoJ is contemplating a new quantitative monetary policy framework, which hints at a slowdown in future government bond purchases. Australian and New Zealand Dollars also enjoy notable gains, riding the wave of strong risk-on market sentiment.

Conversely, Euro positions as the day's second weakest currency, albeit maintaining strong gains against Dollar, which languishes as the day's worst performer. Canadian Dollar trails as the third weakest, with the Swiss Franc and Sterling are mixed.

Technically, Gold rides of Dollar's weakness and surges to new record high at 2185. It's now in an upside acceleration phase as seen in D MACD. Next target is the critical cluster projection level at around 2260, 100% projection of 1810.26 to 2088.24 from 1984.05 at 2262.03 and 100% projection of 1614.60 to 2062.95 from 1810.26 at 2259.15.

In Europe, at the time of writing, FTSE is down -0.35%. DAX is up 0.06%. CAC is up 0.28%. UK 10-year yield is down -0.0489 at 4.038. Germany 10-year yield is down -0.059 at 2.250. Earlier in Asia, Nikkei rose 0.23%. Hong Kong HSI rose 0.76%. China Shanghai SSE rose 0.61%. Singapore Strait Times rose 0.42%. Japan 10-year JGB yield rose 0.0009 to 0.735.

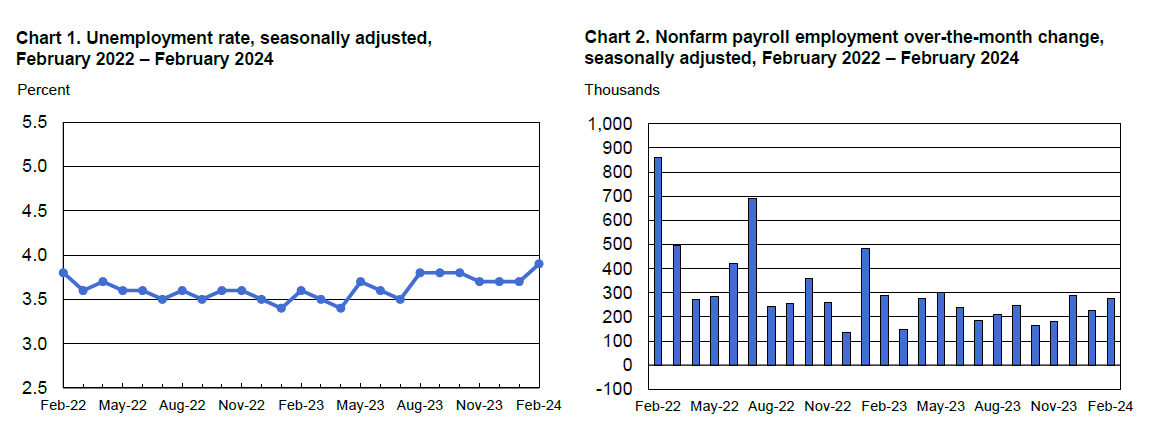

US NFP grows 275k, unemployment rate rises to 3.9%, average hourly earning up just 0.1% mom

US non-farm payroll employment rose 275k in February, above expectation of 200k. However, January's figure was revised sharply lower from 353k to 229k.

Unemployment rate jumped from 3.7% to 3.9%, above expectation of being unchanged at 3.7%. Labor force participation rate was unchanged at 62.5% for the third consecutive month.

Average hourly earnings rose 0.1% mom, below expectation of 0.2% mom. Average workweek edged up by 0.1 hour to 34.3 hours.

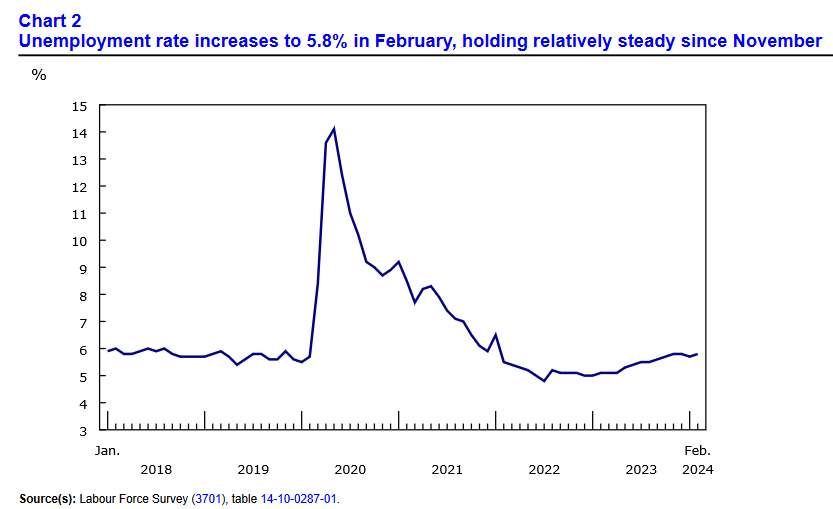

Canada's employment grows 40.7k in Feb, unemployment rate ticks up to 5.8%

Canada's employment rose 40.7k in February, above expectation of 20.0k. Unemployment rate ticked up from 5.7% to 5.8%, matched expectations. Employment rate fell -0.1% to 61.5%. Total hours worked was up 0.3% mom. Average hourly wages rose 5.0% yoy, down from January's 5.3% yoy.

ECB officials signal rate cut prospects, eyeing Spring for initial move

Several ECB policymakers vocalized today their anticipation of impending rate cuts, pinpointing spring—likely June—as the probable period for the first reduction.

Governing Council member Francois Villeroy de Galhau, in an interview with BFM Business television, conveyed a "very probable" outlook for an inaugural rate cut within the spring months. Villeroy indicated there is "large consensus" among officials on the inevitability of rate reductions, albeit with ongoing discussions about the precise timing. He elaborated on the spring timeframe, suggesting it encompasses April to June, thus leaving a window open for an earlier adjustment.

Further adding to the conversation, Governing Council member Gediminas Šimkus acknowledged the prevailing conditions that pave the way for a shift to a less restrictive monetary stance. While not dismissing an April rate cut entirely, Šimkus posited a low likelihood for such an early move, aligning more with expectations for action in the subsequent months.

Compounding these sentiments, another Governing Council member Olli Rehn, expressed his viewpoint through a blog post. Rehn's assessment, grounded in the latest forecasts, indicates that "the risks of too early a decrease in interest rates from the perspective of inflation control have significantly decreased."

Japan's household spending falls -6.3% yoy in Jan, deepening contraction

Japan's household spending fell -6.3% yoy in January well below expectation of -4.3% yoy. That's the 11th consecutive month of contraction, and the biggest annual drop since February 2021. On a seasonally adjusted, spending fell -2.1% mom, versus expectation of 0.4% mom increase.

The Ministry of Internal Affairs and Communications noted that one-off factors such as decreases in new car purchases amid factory suspensions and lower energy bills due to warm weather contributed to the spending drop. Also, the bigger-than-expected fall was also against the backdrop of higher spending in the same month last year from post-pandemic travel subsidies.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2750; (P) 1.2781; (R1) 1.2839; More...

GBP/USD accelerates to as high as 1.2892 so far today. The strong break of 1.2826 resistance confirm resumption of whole rally from 1.2036. Intraday bias stays on the upside for 61.8% projection of 1.2036 to 1.2826 from 1.2517 at 1.3005 next. On the downside, below 1.2800 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which could be still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Overall Household Spending Y/Y Jan | -6.30% | -4.30% | -2.50% | |

| 23:50 | JPY | Bank Lending Y/Y Feb | 3.00% | 3.20% | 3.10% | |

| 23:50 | JPY | Current Account (JPY) Jan | 2.73T | 2.07T | 1.81T | |

| 05:00 | JPY | Leading Economic Index Jan P | 109.9 | 109.7 | 110.2 | |

| 06:00 | JPY | Eco Watchers Survey: Current Feb | 51.3 | 50.6 | 50.2 | |

| 07:00 | EUR | Germany Industrial Production M/M Jan | 1.00% | 0.50% | -1.60% | -2.00% |

| 07:00 | EUR | Germany PPI M/M Jan | 0.20% | -0.10% | -1.20% | |

| 07:00 | EUR | Germany PPI Y/Y Jan | -4.40% | -6.60% | -8.60% | |

| 07:45 | EUR | France Trade Balance (EUR) Jan | -7.4B | -6.5B | -6.8B | -6.4B |

| 10:00 | EUR | Eurozone GDP Q/Q Q4 | 0.00% | 0.00% | 0.00% | |

| 13:30 | USD | Nonfarm Payrolls Feb | 275K | 200K | 353K | 229K |

| 13:30 | USD | Unemployment Rate Feb | 3.90% | 3.70% | 3.70% | |

| 13:30 | USD | Average Hourly Earnings M/M Feb | 0.10% | 0.20% | 0.60% | 0.50% |

| 13:30 | CAD | Net Change in Employment Feb | 40.7K | 20.0K | 37.3K | |

| 13:30 | CAD | Unemployment Rate Feb | 5.80% | 5.80% | 5.70% | |

| 13:30 | CAD | Capacity Utilization Q4 | 78.70% | 79.90% | 79.70% | 78.80% |

Canada’s employment grows 40.7k in Feb, unemployment rate ticks up to 5.8%

Canada's employment rose 40.7k in February, above expectation of 20.0k. Unemployment rate ticked up from 5.7% to 5.8%, matched expectations. Employment rate fell -0.1% to 61.5%. Total hours worked was up 0.3% mom. Average hourly wages rose 5.0% yoy, down from January's 5.3% yoy.

US NFP grows 275k, unemployment rate rises to 3.9%, average hourly earning up just 0.1% mom

US non-farm payroll employment rose 275k in February, above expectation of 200k. However, January's figure was revised sharply lower from 353k to 229k.

Unemployment rate jumped from 3.7% to 3.9%, above expectation of being unchanged at 3.7%. Labor force participation rate was unchanged at 62.5% for the third consecutive month.

Average hourly earnings rose 0.1% mom, below expectation of 0.2% mom. Average workweek edged up by 0.1 hour to 34.3 hours.

EURJPY Has One More Chance Before Bears Take the Lead

- EURJPY flips backwards to retest familiar support zone

- Trend signals lean to the negative side

- More sellers might show up below 160.70

EURJPY could not sustain its recent recovery attempt above the 162.00 round level, drifting lower to seek shelter near the important support trendline, which came to the rescue on Thursday.

The pair eased back below its 200-day simple moving average (SMA) and the technical indicators are not in the oversold area at the moment, increasing the possibility of additional bearish actions in the coming sessions.

If the pair were to extend its downfall below the examined trendline at 160.70, it could initially pause around the 61.8% Fibonacci retracement of the November-December downfall at 160. Additional declines are expected to be more aggressive, likely squeezing the price towards the 50% Fibonacci of 158.73. If the bears claim the 158.00 round level too, then the door will open for the 38.2% Fibonacci of 157.42.

In the positive scenario, where the price overcomes the 200-day SMA at 161.35, traders may not get very excited unless they see a sustainable rebound above the critical resistance zone of 162.00-162.65. In this case, the pair could spike into the crucial resistance area of 163.37-163.70, where it paused its uptrend. The 15-year high of 164.28 from November 2023 could be the next challenge. If the bulls breach the latter too, they may enjoy a fast rally to 165.85, especially if the 165.00 psychological mark gives way.

Summing up, EURJPY’s short-term outlook has taken a bearish turn following the pullback below January’s highs around 162. Sellers might wait for another negative extension below the nearby support trendline before they declare victory.

EUR/USD Technical: At Risk of Minor Mean Reversion Decline as US NFP Looms

- EUR/USD has evolved into a short-term uptrend phase as it traded back above its 20-day and 50-day moving averages in the past two days.

- Yesterday’s swift upmove of +89 pips ex-post ECB increases the risk of a minor mean reversion decline for the EUR/USD.

- The consensus estimate for today’s US NFP is pegged at a relatively low expectation of 200K jobs added for February below 353K added in January.

- Watch the 1.0970 key short-term resistance on the EUR/USD

In the past four days, the trend of the EUR/USD has started to take an abrupt turn from a medium-term corrective downtrend phase from the 28 December 2023 high of 1.1140 to the 4 February 2024 low of 1.0695 (a total of -442 pips/-4% decline) to evolve into a short-term uptrend phase at this juncture.

Broad-based US dollar weakness

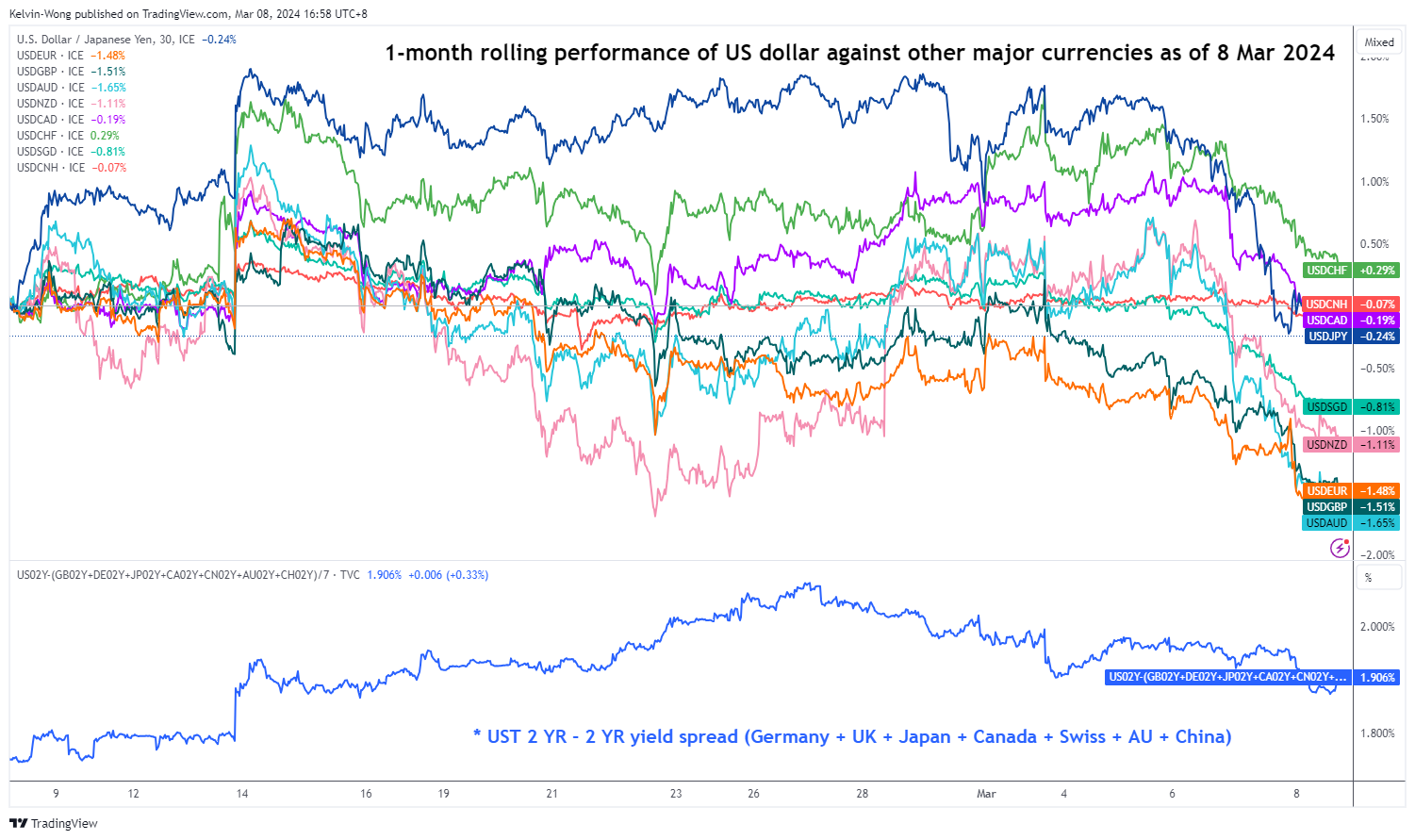

Fig 1: 1-month rolling performances of the US dollar against major currencies as of 8 Mar 2024 (Source: TradingView, click to enlarge chart)

The US dollar has plummeted across the board as measured against the major currencies reinforced by another round of renewed weakness in both the 2-year and 10-year US Treasury yields which in turn reduces the US Treasuries yield premium over other sovereign fixed income.

Based on the current one-month rolling performance, the US dollar has plummeted to a one-month low against the EUR with a loss of -1.5% (see Fig 1) that led the EUR to share the second-best performing major currency ranking together with the GBP when measured against the US dollar.

The US 10-year Treasury yield has declined by 28 basis points in the recent two weeks from its 4.33% key major resistance and broke below a former 4.14% key near-term support which also coincided closely with the 200-day moving average. Right now, the US 10-year Treasury yield is trading at 4.07% at this time of the writing.

US NFP consensus estimate for February is set at a lower print of 200K

One key risk event to take note of today before we wrap off for this week will be the all-important US jobs number, the non-farm payrolls data (NFP) for February. In the prior two months, the US job market has been robust where both data prints (December 2023 and January 2024) have managed to beat expectations that in turn form the current bias of “no in the rush to cut interest rates mantra” among Fed Chair Powell and his colleagues in the US Federal Reserve.

The consensus estimate for today’s US NFP release is pegged at a rather low bar of 200K jobs added for February which is below 353K in January. Therefore, the actual NFP data release later may surprisingly overshoot to the upside (easily) which may spark a potential minor mean reversion rebound scenario for the US dollar.

Watch the 1.0970 key short-term resistance on the EUR/USD

Fig 2: EUR/USD short-term trend as of 8 Mar 2024 (Source: TradingView, click to enlarge chart)

Yesterday’s (7 March) burst up of +89 pips/+0.8% to print an intraday high of 1.0956 on the EUR/USD after a retest on its 50-day moving average ex-post ECB monetary policy decision has led to a bearish divergence condition seen on the hourly RSI momentum indicator at is overbought region.

These observations suggest an increased risk of a potential minor mean reversion decline for the EUR/USD at this juncture within its short-term uptrend phase where price actions have surpassed its 20-day, 50-day as well as 200-day moving averages on the upside.

If the 1.0970 short-term pivotal resistance is not surpassed to the upside, the EUR/USD may see a minor slide to expose the next near-term support zone of 1.0890/0870 (also the 50-day moving average).

However, a clearance above 1.0970 invalidates the minor mean reversion decline scenario for a continuation of the impulsive upmove sequence within its short-term uptrend phase for the next near-term resistances to come in at 1.1000 and 1.1040.

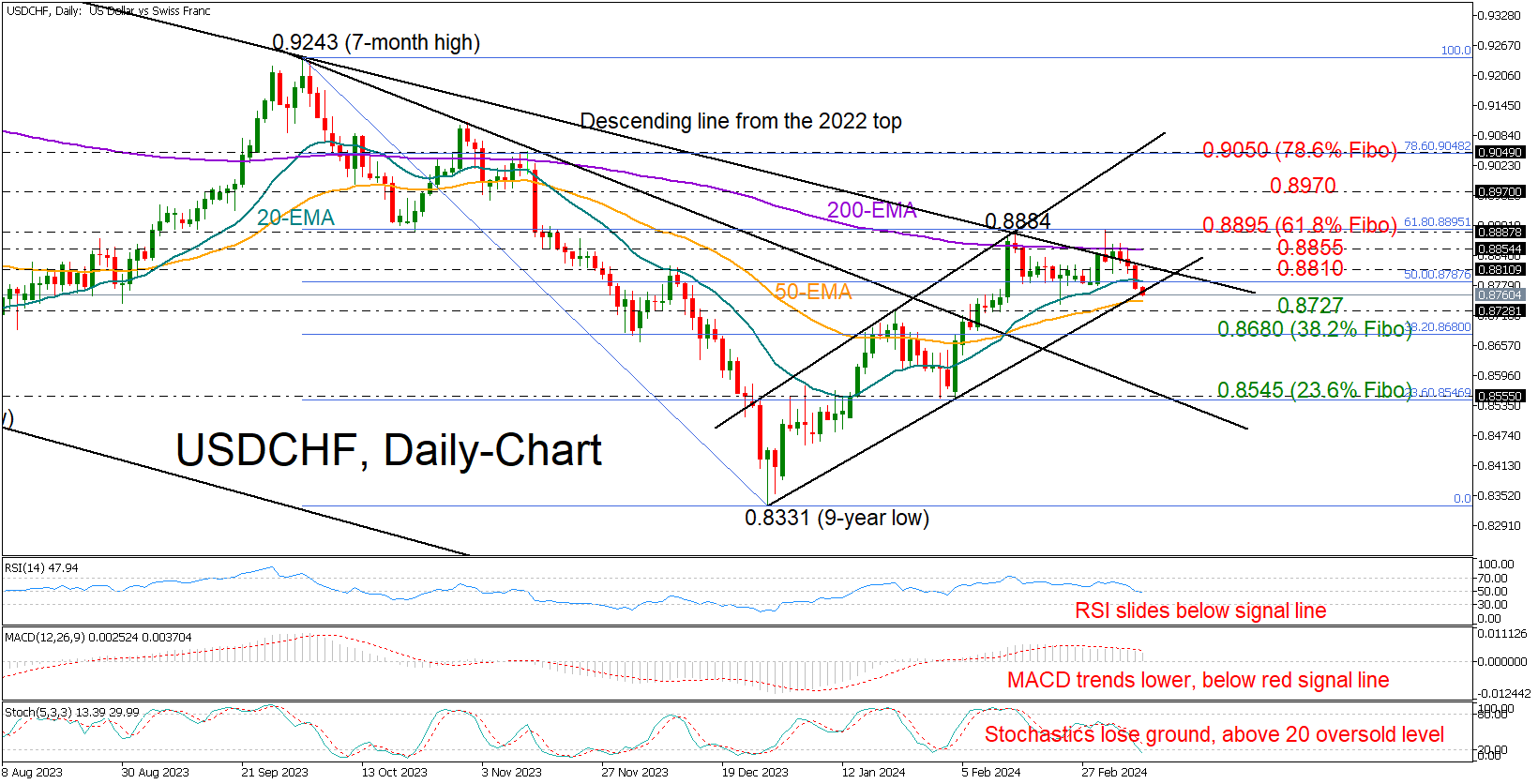

USDCHF Puts 2024 Uptrend in Test

- USDCHF consolidates its 2024 uptrend

- Short-term bias weakens, but a rebound is still possible

USDCHF topped twice around February’s high of 0.8884 and the 200-day exponential moving average (EMA), increasing fears that the 2024 upleg might have peaked, especially after the tick below the nearby 0.8780 support region on Thursday.

However, the ascending trendline from December's low is still intact and is currently being examined at 0.8765, with the possibility that January's high at 0.8727 could also mitigate pressures. The bearish wave could gain momentum if the latter is breached, causing the price to approach the 0.8680 constraining zone. This zone represents the 38.2% Fibonacci retracement of the October-December downleg. A steeper decline could head for the 23.6% Fibonacci level of 0.8545.

The above bearish scenario is backed by the technical indicators, as the RSI is poised to fall below 50 and the MACD is consistently below its signal line. The stochastic oscillator is also maintaining its negative trajectory above its 20 oversold level.

On the upside, the pair will have to pierce through the 0.8810-0.8855 region, which includes the long-term resistance trendline from November 2011, in order to re-challenge the double-top region and the 61.8% Fibonacci of 0.8895. A successful penetration higher could bolster buying appetite towards the 0.8970 barrier and then up to the 78.6% Fibonacci bar of 0.9050.

In short, the uptrend of USDCHF in 2024 has plateaued, but the downside risks may remain balanced as long as the price stays above 0.8730.