Sample Category Title

Pound Eyes UK Jobs and GDP Data Eyed After Underwhelming Budget

- UK labour market in the spotlight as wage pressures remain elevated

- GDP data to also be watched as UK in technical recession

- Pound starts March on firmer footing, will the data support further gains?

- Employment report is due Tuesday and GDP figures on Wednesday at 07:00 GMT

Stagnation vs recession

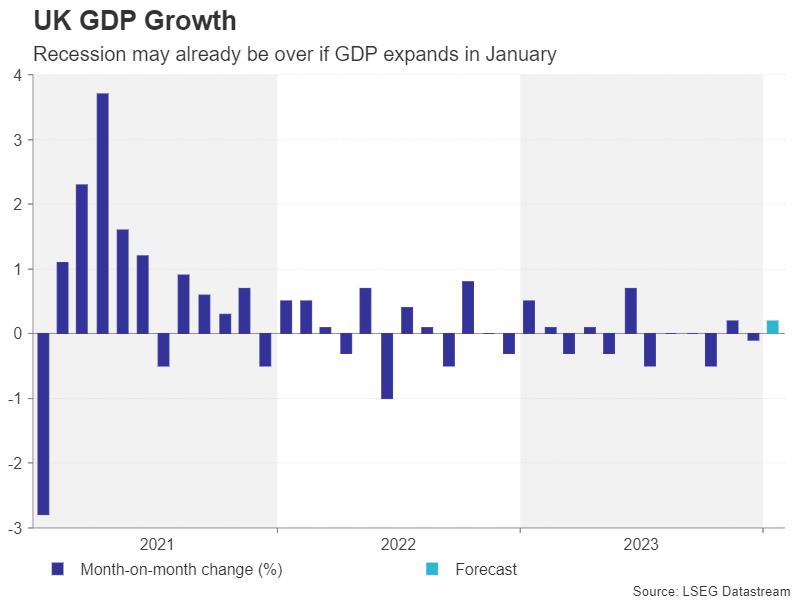

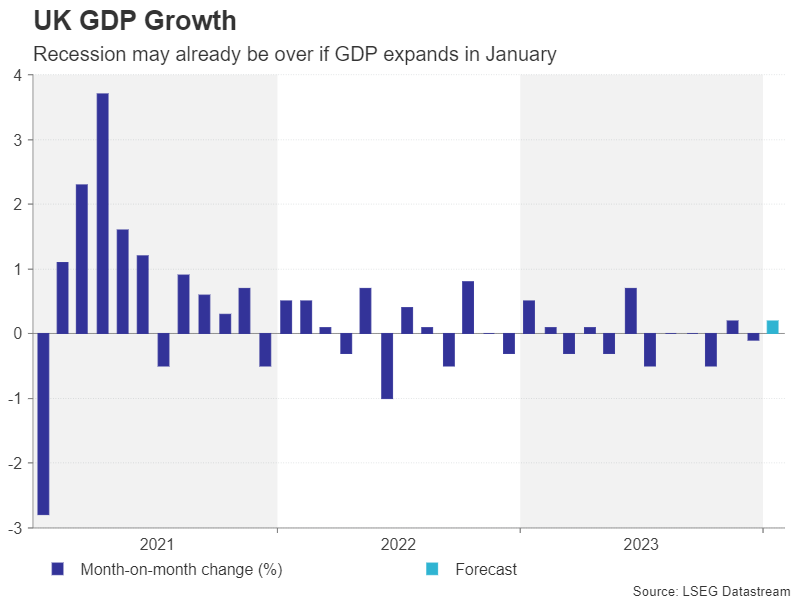

The British economy along with Japan became the first of the major economies in the post-pandemic era to slip into a technical recession in the second half of 2023. Germany narrowly avoided one, while the United States grew at the fastest pace in two years. GDP figures are prone to significant revisions, particularly UK ones, so it’s probably not a good idea to overdo the comparisons.

However, what is clear is that growth in Europe and the UK has stagnated and politicians don’t seem to have a very strong strategy of rectifying that. Such an economic backdrop would normally be bad news for the euro and pound against the mighty US dollar, but the inflation landscape is much more identical on both sides of the Atlantic, hence, there is much less of a divergence when it comes to monetary policy.

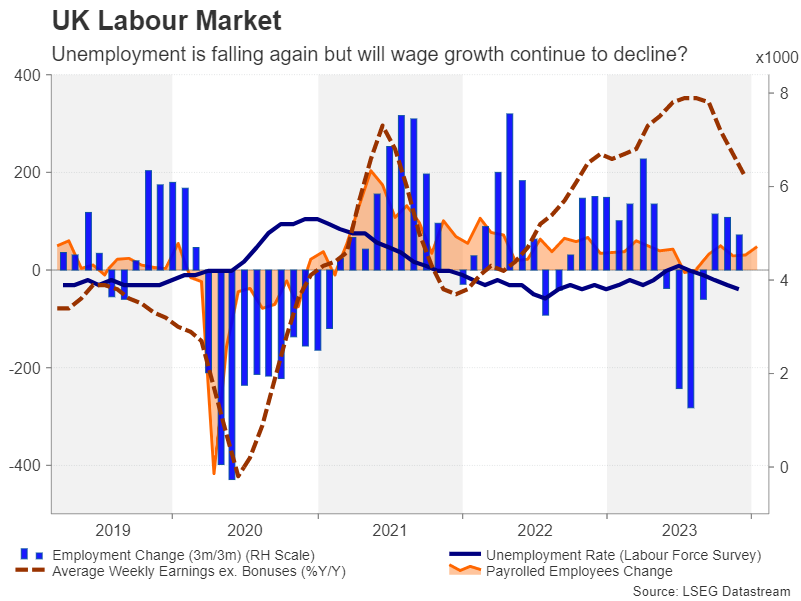

UK labour market may be heating up again

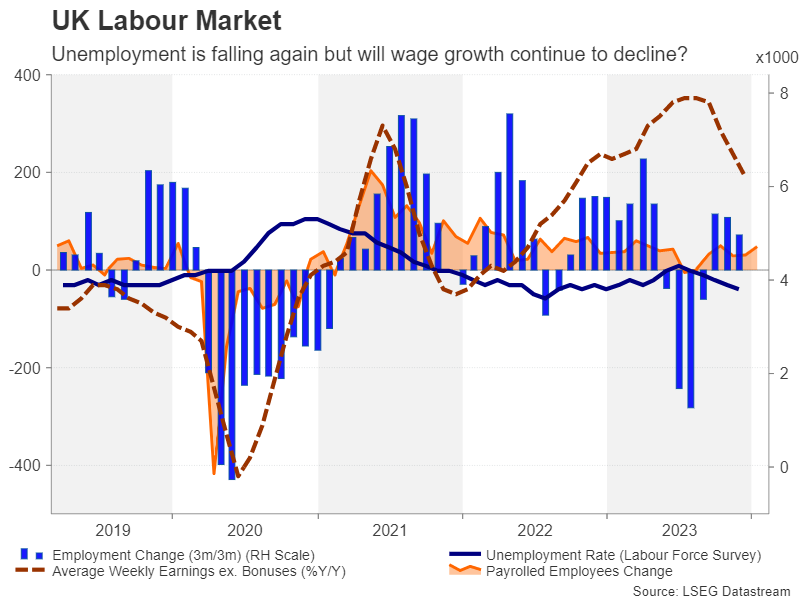

This also solidifies inflation as the primary data driver for sterling. Nevertheless, next week’s employment numbers and GDP readings will be important in setting the mood ahead of the CPI report on March 20 and the Bank of England meeting a day later. Britain’s labour market has bounced back in recent months, with the jobless rate falling to 3.8% in the three months to December.

Further employment growth in the three months to January would suggest that an economic recovery is already underway. However, with the Office for National Statistics admitting that its employment surveys have become less reliable lately and that a fix is months away, wage growth will likely be the main focus for both investors and policymakers.

High wage growth still a problem

Average weekly earnings excluding bonuses stood at 6.2% y/y in the three months to December, having eased substantially from the high of 7.9% over the summer. A further cooldown in wage growth in January would allay concerns about persisting wage pressures.

On Wednesday, GDP data is expected to show that the UK economy grew modestly by about 0.2% in January after contracting by 0.1% m/m in December. Industrial production numbers are also due the same day.

Is $1.30 in sight for the pound?

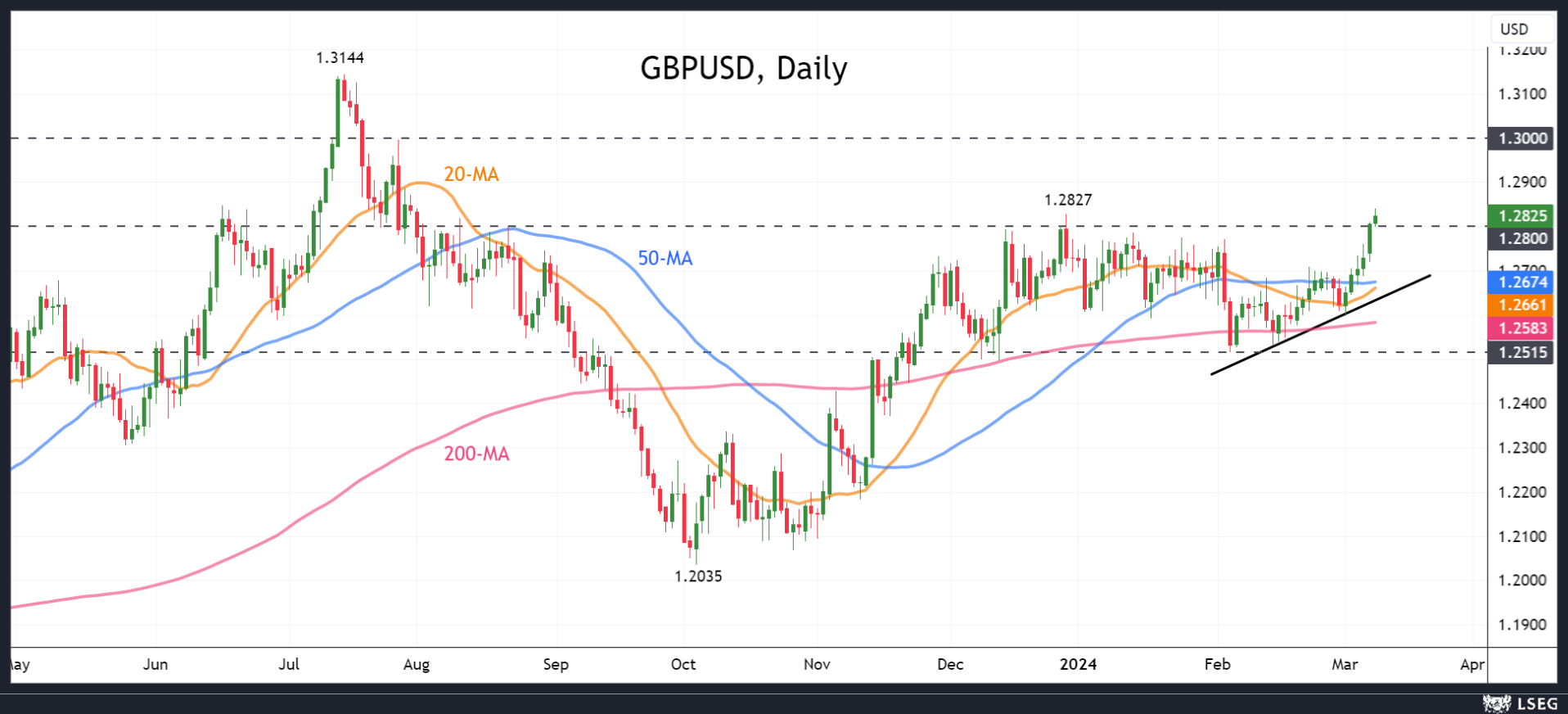

The pound has been consolidating since late December, but the recent break above $1.28 has shifted the short-to-medium-term outlook to bullish. The next key target on the upside is the $1.30 level.

Should sterling come under pressure from weaker-than-expected data, the moving averages stand ready to defend the price from a steep fall. However, the February low of $1.2515 is the more crucial support that if broken, could tip the risks back to the downside.

In the longer term, the outlook for the pound is somewhat muddied. Inflation is likely to fall to the 2% target in the coming months as the energy price cap is lowered again. But the Bank of England expects such a drop to be short-lived and is keeping a closer watch not just on core CPI, but also on services inflation, which has started to tick up again.

Fiscal boost

Complicating matters for policymakers are the latest fiscal measures announced in the spring budget. The government cut the national insurance rate by a further two percentage points to 8%, having announced a similar reduction in the autumn statement.

The tax reductions would support greater spending by consumers, which although would be positive for economic growth, they would limit the scope for interest rate cuts by the Bank of England, and this could effectively put a floor under sterling.

For now, however, markets continue to anticipate a summer rate cut amid ongoing pessimism about the economic outlook. It’s doubtful if next week’s releases alone would significantly alter those views.

Week Ahead – US CPI to Headline Dull Week, May Spoil the Calm

- US inflation and retail sales data to take the spotlight as dollar slips

- UK jobs and GDP numbers coming up too amid recession woes

- Will markets hold their nerve before the looming central bank storm?

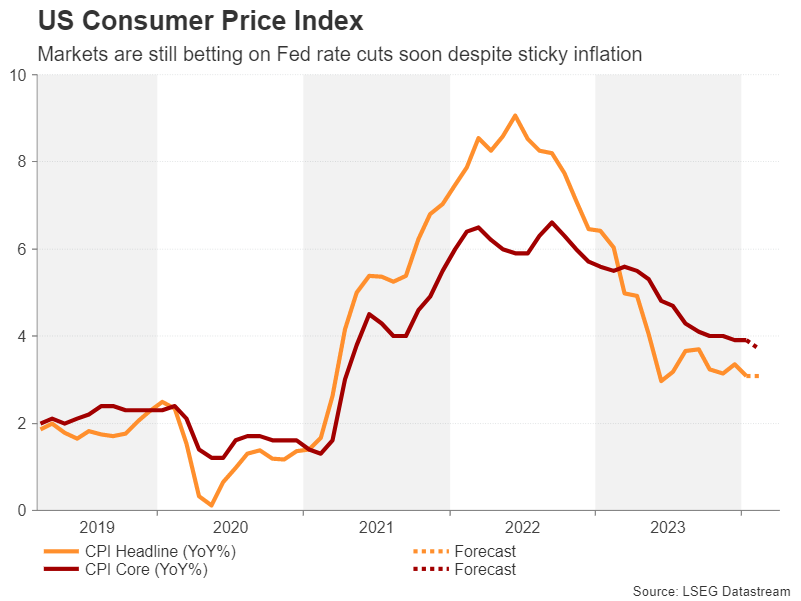

Will CPI report cause a sticky problem for the Fed?

The US Federal Reserve doesn’t meet until March 20 for its next policy decision and with the jobs report out of the way, all eyes are now on the CPI numbers for February due Tuesday. There’s been good news and bad news on the inflation front in the US lately. The headline CPI rate has been stubbornly stuck above 3.0% with core CPI glued nearer the 4.0% level. There was some comfort from core PCE inflation, which fell to 2.8% y/y in January, although the six-month annualized measure of the same gauge edged up from 1.9% to 2.5% y/y.

Based on the forecasts, February’s readings of the consumer price index will probably be another mixed bag. The 12-month CPI rate is expected to have stayed unchanged at 3.1% on the back of a slight pick up in the month-on-month rate to 0.4%. However, there may be some relief from the core measure that excludes food and energy prices. It’s projected to have eased from 3.9% to 3.7% y/y.

The services component of CPI that excludes shelter costs will also be watched as it had ticked up to 3.6% in January, in a setback for the Fed, which wants to see this number come down. Thursday’s producer price index will be vital too before the March meeting.

Retail sales bounce eyed

Fed Chair Powell maintained caution over the inflation outlook when testifying before lawmakers in Capitol Hill this week. Whilst he signalled that rates will likely be cut later this year, his reluctance to be less vague about the possible timing suggests the Fed has some reservations about how fast inflation is falling.

That did not stop investors, though, from cheering at the prospect of a rate cut soon. The soft landing narrative whereby the US economy is slowing just enough for the Fed to ease policy but can still skirt a recession continues to underpin the risk-on sentiment in the markets.

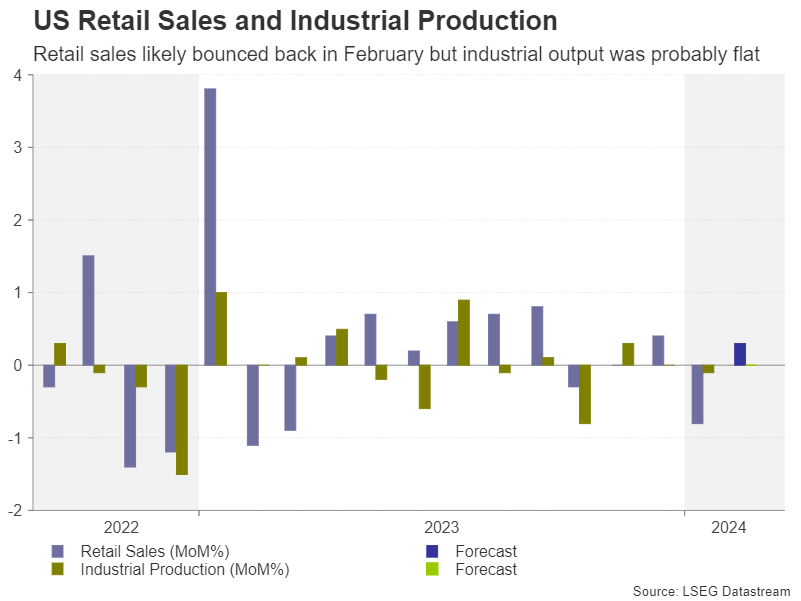

Growth went through a bit of a soft patch in January so some kind of a rebound in February is essential to sustaining this goldilocks scenario. And the latest retail sales figures are expected to do just that on Thursday. After plunging by 0.8% m/m in January, retail sales are forecast to have rebounded by 0.3% in February.

Dollar bulls hoping for hot CPI data

Other indicators on next week’s schedule include the Empire State manufacturing index, industrial production and the University of Michigan’s preliminary estimate of consumer sentiment in March, all due on Friday.

For the US dollar, the main risk is upside surprises in the CPI prints, which have the potential to cast doubt on a June rate hike that investors have pinned their hopes on. A hot CPI report would be damaging for risk assets but positive for the greenback, which badly needs a lift after being on the backfoot since mid-February. Aside from the data, a slew of bond auctions by the Treasury Department could also inject some volatility into bond, FX and equity markets.

Will UK GDP point to a rebound?

The pound will be in the limelight too over the coming week as labour market stats and the monthly GDP reading are on the UK agenda. Employment in the UK slumped last summer as the economy shrunk, but has been rising since October, with the jobless rate falling again to 3.8%. If Tuesday’s report points to a further improvement in the labour market in January, it would ease concerns about a sharp recession.

However, investors will probably not pay too much attention to the jobs numbers amid some reliability issues with the ONS surveys lately and the main focus will be on the wage growth figures. The Bank of England is unlikely to start cutting rates before it sees clear signs that wage pressures are cooling and although there’s been good progress – earnings growth excluding bonuses has declined from 7.9% to 6.2% y/y – there’s a long way to go still.

However, investors will probably not pay too much attention to the jobs numbers amid some reliability issues with the ONS surveys lately and the main focus will be on the wage growth figures. The Bank of England is unlikely to start cutting rates before it sees clear signs that wage pressures are cooling and although there’s been good progress – earnings growth excluding bonuses has declined from 7.9% to 6.2% y/y – there’s a long way to go still.

Sticky wage growth would make it difficult for policymakers to consider lowering rates even if the economy is struggling. The British economy is officially in a technical recession after GDP fell for two consecutive quarters in the second half of 2023. Output data for January are out on Wednesday and are expected to show GDP growing marginally by 0.2% m/m, potentially signalling the end of the recession. Industrial and manufacturing production figures will be released too.

The pound, which has been benefiting from the dollar’s pullback, could extend its recent advances should a stronger-than-expected set of data push up the market implied path for the BoE policy rate.

Drivers for the start of the week

Elsewhere, it will be an extremely quiet week ahead of the crucial central bank decisions from the Fed, Bank of Japan and Bank of England later in the month.

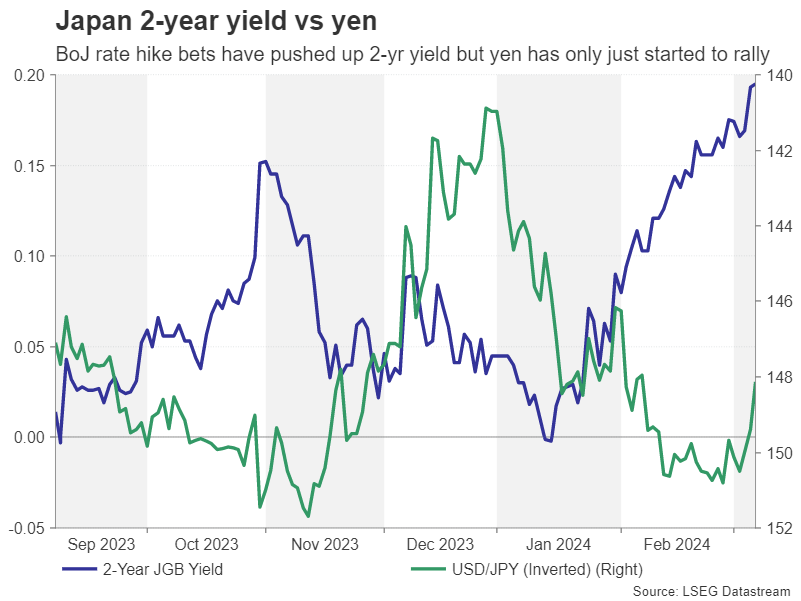

Speculation is mounting that the Bank of Japan could hike interest rates as soon as its March meeting so an upward revision to Japan’s Q4 GDP estimate on Monday could further bolster the yen against the dollar, having already rallied by almost 2% over the past week.

Meanwhile, Chinese price indicators released over the weekend could also boost sentiment at the start of the week. Consumer prices in China are expected to have risen by 0.4% y/y in February after plunging by 0.8% in January. However, producer prices are forecast to have remained in deflationary territory, amid a sluggish economic recovery.

Weekly Focus – Rate Cuts on the Horizon

This week, we published our updated economic projections for the major economies and the Nordics, see Nordic Outlook - Return to Nordic growth, 5 March. While political risks remain high, the global economy is performing better than feared. The Nordic economies are currently in stagnation or mild recession, but our forecasts point to gradual return to normal growth over the coming years, supported by lower interest rates, higher purchasing power and lower inflation.

The ECB held interest rates unchanged as was expected. At the press conference President Lagarde was quite clear with guidance for a June rate cut, as she emphasised the need for more data ahead of the decision. Whilst April was not definitively ruled out, she said they will know a little more in April, and a lot more in June. We doubt that the incoming data ahead of the 11 April meeting will be sufficiently weak to change that view, and still expect ECB to deliver its first rate cut in June. The ECB's new staff projections saw a downward revision of the 2024 projections across growth, headline and core inflation. Read more in our Flash: ECB Review - June cut is coming, 7 March.

In the US, the so-called Super Tuesday this week confirmed that the presidential election in November will most likely be a rematch between Biden and Trump after republican Nikki Haley officially dropped out of the race. Fed Chairman Powell did not provide new policy signals in his testimonies to Congress. We still expect Fed to start rate cuts in May.

China announced that its official GDP growth target for this year will be 5%. The announcement was expected but markets were clearly disappointed with the lack of stimulus signals in the 'Work Report'. On a more positive note, trade data on Thursday confirmed a significant rebound in both exports and imports from a year ago. These signals are in line with our view of a 'muddling through' in China and the gradual recovery of the global industrial cycle.

Markets moved largely sideways this week. The biggest mover was gold that recorded a fresh all-time high above USD 2160 per troy ounce. The sudden rush to this traditional inflation hedge and safe-haven fits together with the decline in yields seen this week.

In geopolitics, there has been no breakthrough in ceasefire talks between Hamas and Israel. Israel has threatened to attack the city of Rafah by 10 March if hostages are not released. In our view, if the talks fail and Israel storms Rafah, it marks yet another escalation of the conflict and raises the risk of retaliation by Iran-backed militant groups in the region.

Next week, in euro area, industrial production figures for January are due on Wednesday. Final country-level CPI prints for February are also out during the week. In the US, focus is on February CPI data that is released on Tuesday, retail sales on Thursday and the Michigan survey on Friday. In Japan, the biggest labour union will release the latest tally of pay deals on Friday. This will be the first indication of whether wage growth is creating sustainable inflation pressures that would warrant monetary policy tightening. In China, we get credit and money growth data next week, but the date is not set. On Friday, the PBOC announces medium-term lending facility rates, which we expect to stay unchanged.

US February Employment: The Devil Is in the Details

Summary

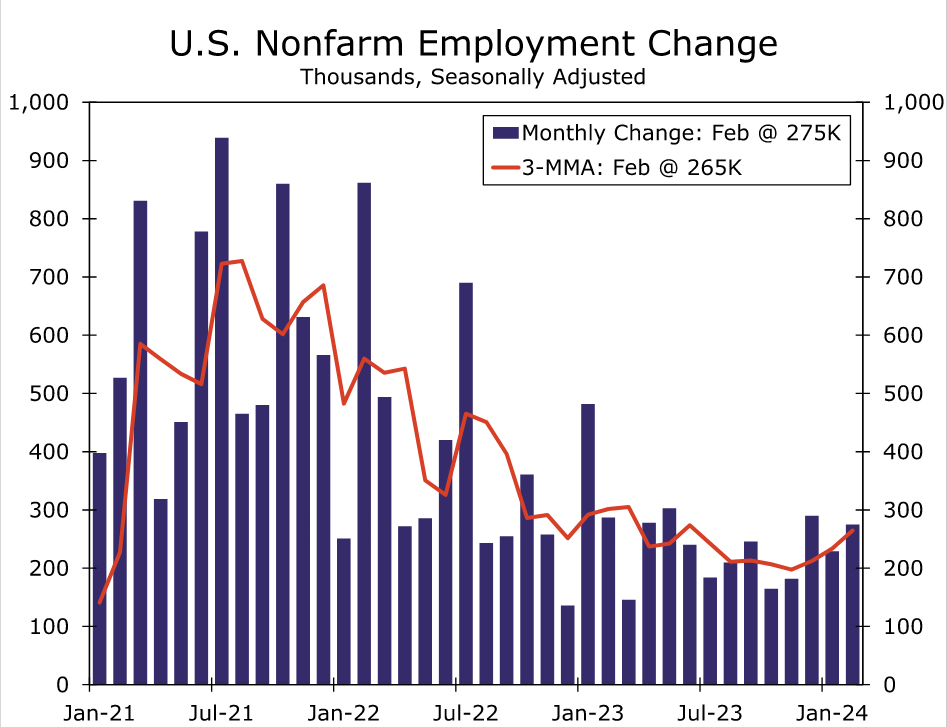

Another strong beat in payroll growth in February masked other signs of softening in the jobs market. Nonfarm payrolls surpassed consensus expectations for a 200K increase by rising 275K last month, with gains broadly-based across industries. Even with some meaningful downward revisions to the prior two months, the three-month average pace of job growth was little changed at a solid 265K. However, the unemployment rate rose to just over a two-year high of 3.9%. The increase was driven by a jump in unemployment and decline in the household measure of employment. While we put more weight on the payroll measure of employment, there were other cautionary signs about the labor markets' strength going forward. Continued declines in temporary help workers, a rise in permanent job losers and a shift toward part-time work all point to deteriorating demand for workers and slower payroll gains ahead. A gradual cooling in the labor market offers additional evidence that inflation also will continue to slow in the months ahead and brings the long-awaited FOMC rate cuts into sharper focus.

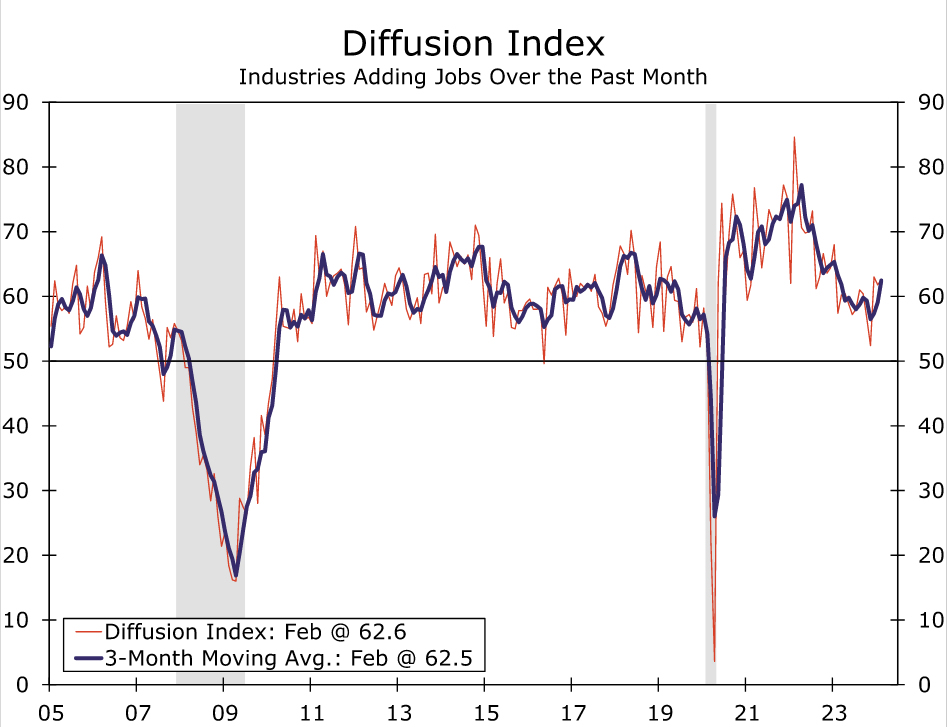

Headline Beat on NFP, but Disappointing Details

Nonfarm payroll growth beat expectations in February, growing by 275K compared to a consensus forecast for a 200K gain. However, downward revisions to job growth in the prior two months lowered past employment gains by 167K, more than offsetting the upside surprise in February. Encouragingly, the breadth of job growth across industries remained solid in the month. The employment diffusion index, a measure of job growth breadth, posted its second highest reading in the past 13 months. Payroll gains were lead by health care (+67K), government (+52K), leisure and hospitality (+58K) and construction (+23K). Average hourly earnings (AHE) posted a benign 0.1% increase in the month, a notable deceleration from the downwardly-revised 0.5% reading in January. That said, annualized AHE growth remains about one percentage point faster than the average pace that prevailed in 2018-2019.

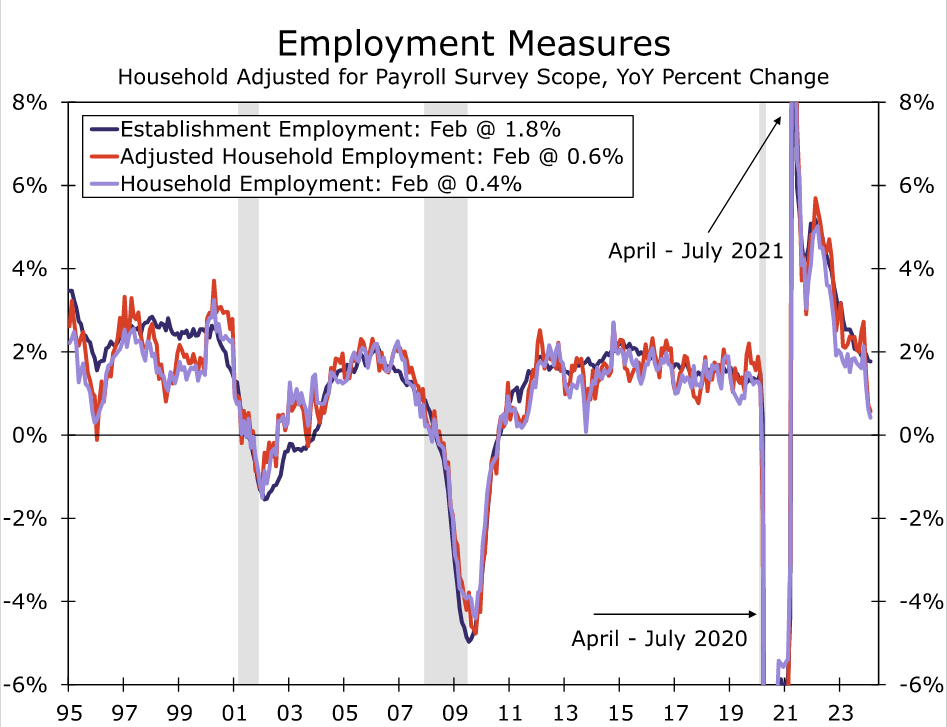

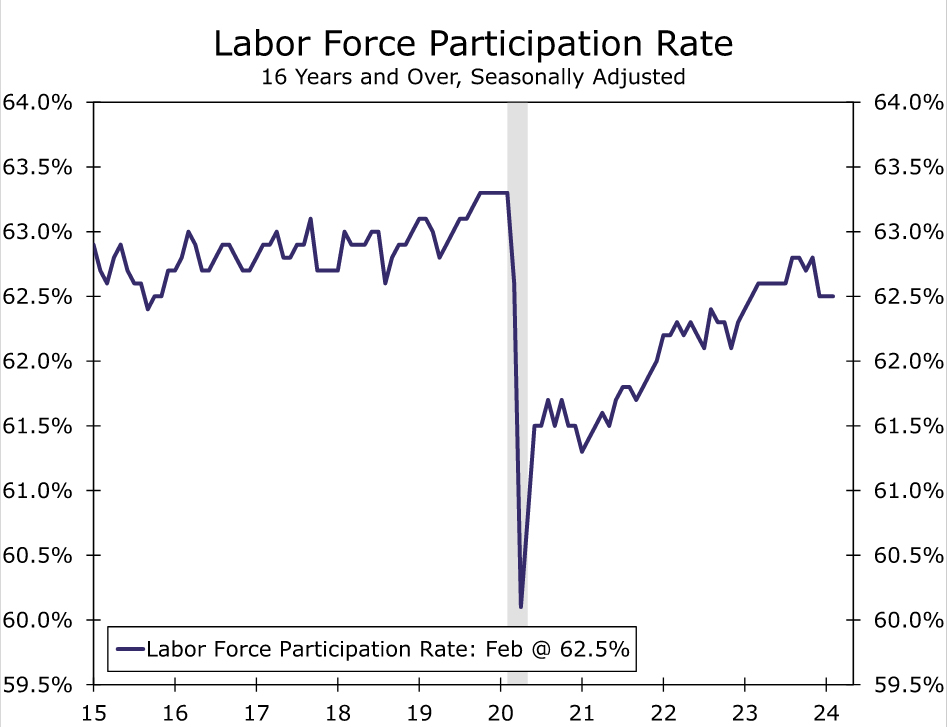

The separate household survey offered additional evidence that the headline beat on nonfarm payrolls masks underlying softening in the labor market. Household measures of employment are more volatile on a month-to-month basis than nonfarm payrolls, but the 184K decline in employment and 343K increase in unemployment helped push the unemployment rate up to 3.9%, the highest reading since January 2022. Solid labor supply growth in 2023 was instrumental in reducing upward pressure on wage growth without a material weakening in job growth. However, the upward trend in labor force participation through much of last year has showed signs of flattening out in recent months. In February, the labor force participation rate held steady at 62.5%, unchanged from both January 2024 and February 2023.

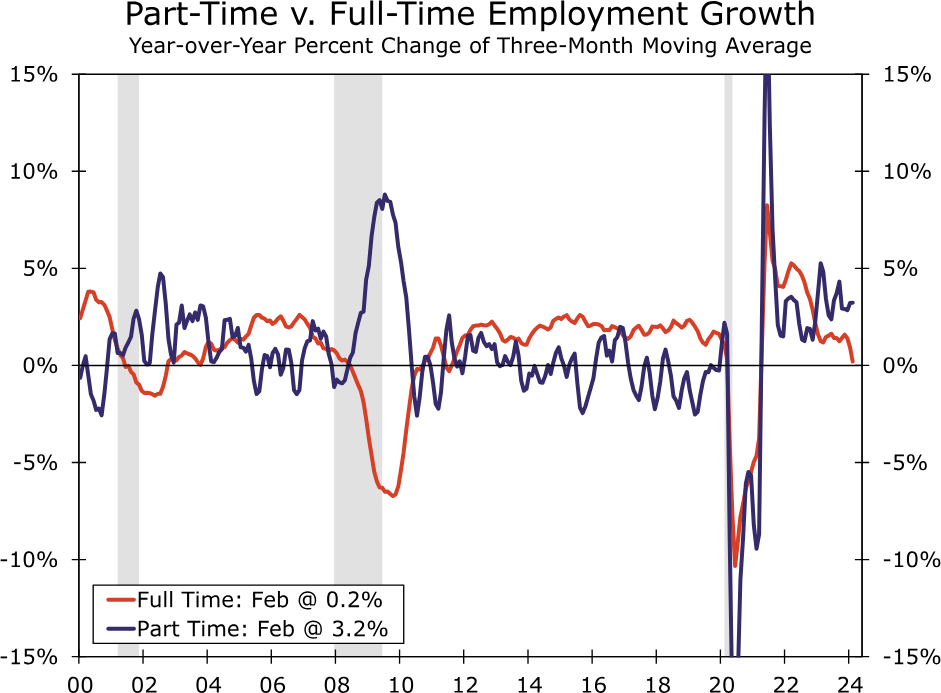

While hiring has remained robust to the start the year, we continue to see a moderation ahead. Underneath the still decent pace of payroll growth are cautionary signs. Demand for workers around the margin continues to weaken with temporary help services falling for a 23rd consecutive month. Average weekly hours rebounded after January's odd plunge but remain below the 2019 average in a sign businesses are using workers less intensely. The drop in household employment was entirely accounted for by a drop in full time employment, continuing the trend of part-time employment comfortably outpacing full-time employment growth over the past year. Furthermore, the ranks of permanent job losers moved up again—a signal it is taking longer for laid off workers to find reemployment. These downbeat elements of today's report come amid other signs of jobs market softening, such as small business hiring plans falling back to the lowest levels since 2016 and a rising number of layoff announcements according to the Challenger data. We expect to see payroll growth downshift in the months ahead as a result, which is likely to put further downward pressure on wages and weigh on household income and spending.

The upshot is that these signs point to a further moderation in inflation as 2024 progresses. The results may not be instantaneous as we noted in a recent report previewing next week's CPI report, but there should be enough progress in the months ahead that the FOMC feels comfortable beginning the process of cutting the fed funds rate at some point in the May-July window. Next week's inflation data will be key to how the FOMC views the outlook at its upcoming meeting on March 19-20, and we will be revising our economic and rates forecast post-CPI.

Sunset Market Commentary

Markets

It’s as if some ECB members were inspired by yesterday’s comment by Fed Chair Powell that the US central bank is not far from being confident that the time is right to start dialing back the level of policy restriction. After Fed members recently closed ranks on a first rate cut in June, he suddenly opened the door for action as soon as May. ECB President Lagarde similarly almost completely ruled out an April rate cut at yesterday’s press conference, only for French ECB member Villeroy to open the door. He thinks that it is very probable that the ECB will cut rats in spring, defining the season from April until June 21. He argues that there’s more and more confidence of getting inflation back to 2% between now and next year. German Bundesbank Nagel welcomed that markets are now on the June rate cut path stressing the increased possibility of a move ahead of the summer break. The rather soft comments from the traditionally hawkish Bundesbank come as Germany is currently “the tired man” in Europe. The economy can use the boost from a less restrictive policy. ECB Rehn stressed the independence from the US central bank and argues that the risks of premature interest rate cuts in terms of inflation control have substantially decreased. EstonianECB Muller gave more details on Q1 wage deliberations, saying that pay increases close to 5% would make it more difficult for inflation to slow. Latvian ECB Kazaks suggested that the central bank isn’t obliged to cut at each and every meeting in comments similar to the ones from Atlanta Fed Bostic. A synchronic June-September-December could be in the making with Lithuanian Simkus happy with 25 bps steps. Despite an outperformance of German Bunds on those early ECB comments, the euro held his ground above EUR/USD 1.09.

US payrolls amplified the goldilocks soft landing scenario. February job growth beat consensus (275k vs 200k) but a cumulative 167k (!) downward revisions for December/January overshadowed the headline numbers. Average hourly earnings only rose by 0.1% M/M (vs 0.2% forecast) to be up 4.3% Y/Y. The unemployment rate ticked up from 3.7% to 3.9% (highest since January 2022) with a stable participation rate (62.5%). US Treasury yields currently lose up to 5.5 bps at the front end of the curve (2-yr) compared with 7.7 bps for Germany. EUR/USD sets a new short term high at 1.0981. US stock markets barely profit, opening up to 0.3% higher (albeit at record levels).

News & Views

The Food and Agriculture Organization of the United Nations (FAO) price index showed that food prices eased further in February, by 0.7% M/M and 10.5% Y/Y. Decreases for cereals and to a lesser extent vegetable oils more than offset increases for sugar, meat and dairy products. Cereal prices declined 5% M/M and 22.4% Y/Y. Maize prices dropped the most on expectations of large harvests in Argentina and Brazil along with competitive prices offered by Ukraine eager to take advantage of the smooth running of the maritime trade route. Vegetable oil prices eased 1.6% M/M and 11.0% Y/Y. Dairy prices rose modestly (1.3% M/M) but still were 13.4% lower Y/Y. Meat prices (+ 1.8% M/M) reversed seven months of consecutive drops to stand 0.9% below last year’s value. Sugar prices showed a second monthly increase (3.2%), rising 12.5% Y/Y mainly on concerns for the upcoming season in Brazil following a prolonged period of below-average rainfall.

Hungarian inflation rose by 0.7% M/M in February, but this rather high monthly pace still allowed the Y/Y measure to ease from 3.8% to 3.7%. Food prices rose 0.2% M/M, electricity gas and other fuels became 0.6% more expensive. Services added 0.6% M/M bringing the Y/Y figure at 10.7%. Core inflation measures as calculated by the Hungarian central bank (MNB) all eased Y/Y (core ex indirect taxes 5.1% from 6.1%; CPI ex processed food 7.1% from 8.1%; sticky price CPI 7.7% from 6.8%). The slowdown in (core) inflation probably will continue to fuel the debate on the appropriate pace of MNB rate cuts. At the February meeting, lower than expected inflation caused the MNB to step up the pace of rate cuts from 75 bps to 100 bps, but this triggered a substantial loss of the forint. A similar 100 bps move end March probably risks a similar reaction. EUR/HUF eased to 394 today, but these levels still suggests vulnerability to a too fast pace of MNB easing, especially if disinflation slows down toward the summer (Q2).

CAD Set to End the Week Higher After a Long Slide

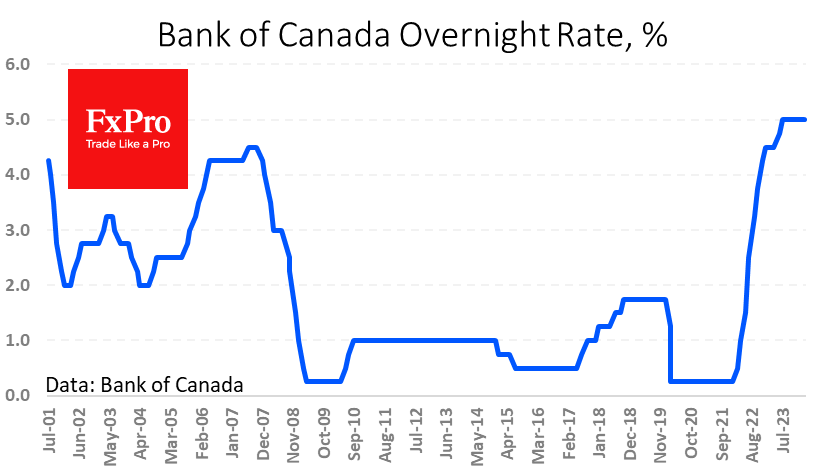

The Canadian dollar gained 0.5% following comments from the Bank of Canada on Wednesday night. The central bank kept its benchmark interest rate at 5% at its regular meeting and continued its quantitative tightening policy.

The Bank of Canada remains concerned about keeping inflation stable and wants to see more evidence that it is returning to target from current levels that are above historical averages.

CAD buying was supported by the fact that the commentary did not hint at an imminent rate hike – Canada is clearly preparing for a long pause.

USDCAD’s move lower also added to the pressure on the U.S. dollar from Powell’s speech and signs of deteriorating economic data in recent days.

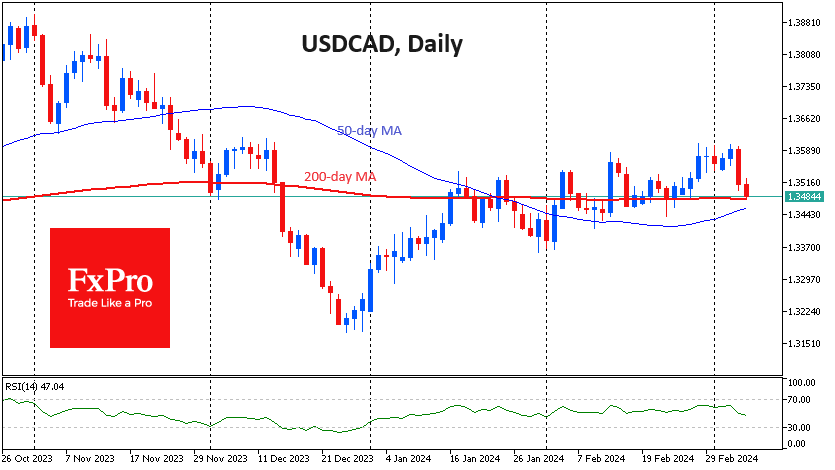

Technically, the USDCAD has returned to the 1.3500 level, which is the consolidation level from late March. A critical test for the USDCAD will be the support at 1.3480, the 200-day moving average. It is about to be crossed from below by the 50-day MA, forming a “golden cross”. This signal, which is usually followed by increased buying, will be an essential test of the strength of the recent bearish momentum.

Given that the pair’s most recent decline was also due to the weakening of the US currency, the bearish momentum could continue, marking the first weekly decline after nine consecutive weeks of gains.

At the same time, the USDCAD may not find significant support until the 1.3200-1.3250 area, where the pair was pushed several times last year.

Canada’s Labour Market Adds Jobs in February, Weak Underlying Details

The Canadian labour market added 40.7k positions in February, with full-time employment up 70.6k and part-time employment down 29.9k.

The unemployment rate increased 0.1 percentage point to 5.8% and the participation rate was flat at 65.3%.

Employment by industry showed gains in the service sector, with accommodation and food services (+26k) and professional, scientific, and technical services (+18k). Losses were seen in educational services (-17k) and manufacturing (-14k).

Lastly, total hours worked rose a trend-like 0.3% month-on-month and wages were down to 5.0% year-on-year (from 5.3% in January and 5.7% in December).

Key Implications

Nothing new from the Canadian labour market. Another decent gain in jobs, with weakness in the details. The boost to full-time jobs was nice to see, but this was all in public sector jobs and the notoriously volatile self-employment category. And as has been the case for 13 straight months, population growth (+83k) massively outstripped any gain in employment. As a result, the total number of unemployed people continues to rise (+220k since late 2022), causing the unemployment rate to rise again. Additionally, wage growth eased again, a trend that should continue now that the broad labour market has found greater balance.

The Bank of Canada has made it clear that it is not ready to cut rates yet. Today's labour market report won't sway this stance. While the job market has held in okay in spite of Canada's meager pace of growth over the last year, the path of inflation is the deciding factor. And to date, the central bank believes it hasn't seen enough evidence to move off the sidelines, although the slight easing in wage pressures may help. Looking at market pricing in the wake of today's report, it is clear that markets aren't swayed either, with odds of a June rate cut holding firm.

US: Job Growth Remained Strong in February, But Unemployment Rate Rises to Two-Year High

Non-farm employment rose by 275k in February, well ahead of the consensus forecast calling for a smaller gain of 200k. However, revisions to the two-prior months were meaningfully lower, subtracting 167k jobs from the previously reported figures.

- Hiring over the last three-months (December-February) averaged 265k jobs per-month, only slightly lower than the pace of job creation measured over the same time last year (302k).

Private payrolls rose by 223k – an uptick from January's 177k. The service sector added 204k jobs, with gains concentrated in health care & social assistance (+90.7k) and leisure & hospitality (+58k). Job gains across goods producing industries (+19k) were almost entirely concentrated in construction (+23k), while manufacturing (-4k) shed jobs. Government hiring remained robust, adding 52k jobs last month.

In the household survey, civilian employment declined by 184k while the labor force rose by 150k. As a result, the unemployment rate increased by 0.2 percentage points to 3.9% – the highest level in just over two years. The participation rate held steady at 62.5% for the third consecutive month.

Average hourly earnings (AHE) rose by just 0.1% month-on-month – a sharp deceleration from January's downwardly revised reading of 0.5% m/m (previously 0.6%). The deceleration in wage growth was largely attributed to a rebound in average weekly hours, after falling sharply last month – likely due to weather impacts. On a twelve-month basis, AHE slipped to 4.3%, while the three-month annualized rate of change fell to 4.0% (from 5.0% in January).

Key Implications

On the surface, this was a very strong employment report with payrolls coming in well above the consensus forecast. But February's upward surprise needs to be weighed against the 167k in downward revisions to the prior two months, and the fact that the unemployment rate ticked up to a two-year high. Overall, the labor market remains incredibly tight and will likely need to show further signs of cooling before inflation can return to 2%.

With the Fed recently downplaying growth and focusing more on inflation dynamics, this morning's report will ultimately play second fiddle to next week's inflation data. That said, the fact that the labor market is showing little sign of deteriorating supports the case that Fed officials can be patient and continue to monitor the inflation data over the coming months. We suspect that by July, policymakers will have gained enough conviction that inflation is on a sustainable path back to 2 percent to warrant some easing in the policy rate.

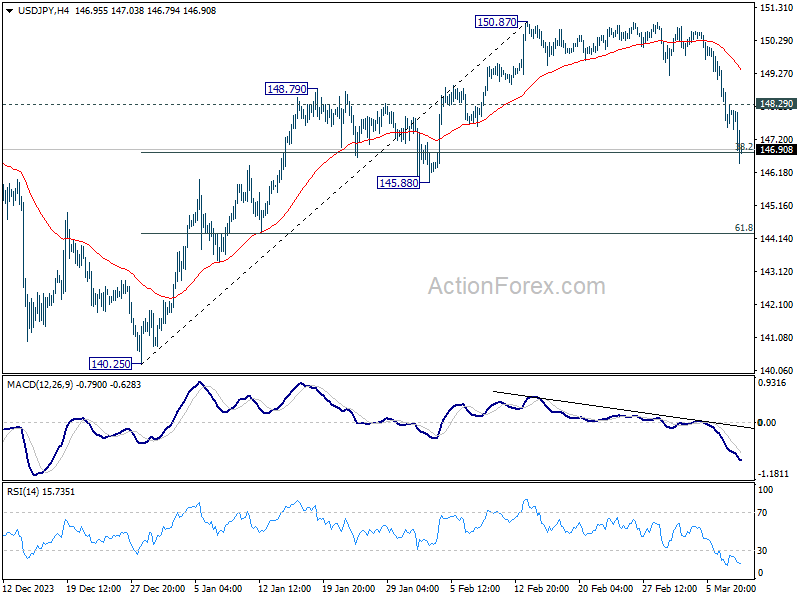

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.28; (P) 148.34; (R1) 149.08; More...

Intraday bias in USD/JPY remains on the downside at this point. Sustained break of 38.2% retracement of 140.25 to 150.87 at 146.81 will argue that fall from 150.87 is reversing the whole rally from 140.25. In this case, deeper decline would be seen to 61.8% retracement at 144.30 and below. Nevertheless, strong support from 146.81, followed by break of 148.29 minor resistance resistance, will argue that fall from 150.87 is merely a correction, which has completed already.

In the bigger picture, outlook is mixed up as fall from 150.87 accelerates lower. Sustained trading below 55 D EMA (now at 148.45) will open up the case that corrective pattern from 151.89 (2023 high) is extending, with fall from 150.87 as the third leg. In this case, deeper decline would be seen to 140.25 support or below. Nevertheless, strong bounce from 55 D EMA will retain near term bullishness for at least another take on 151.89.

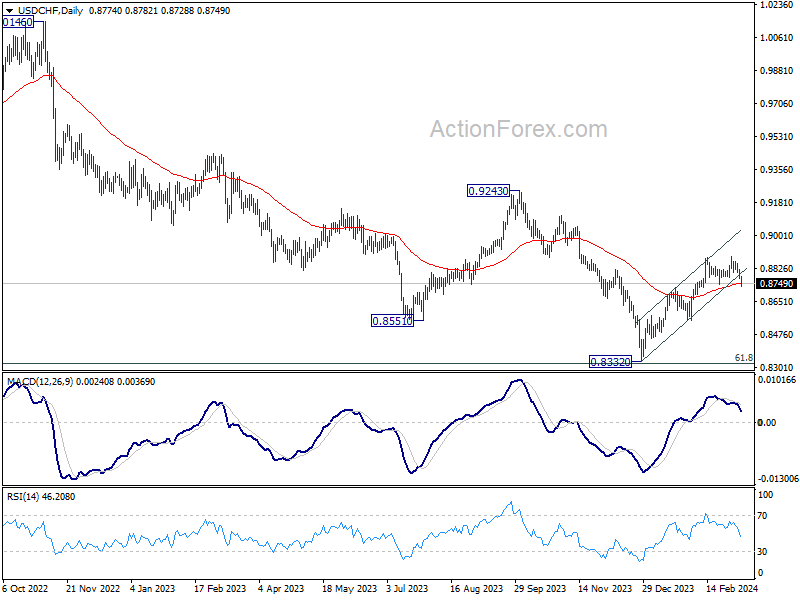

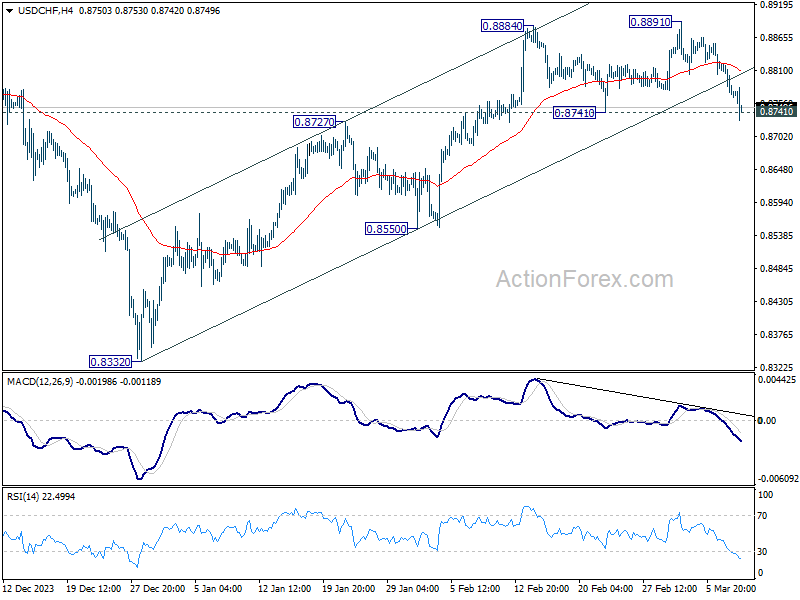

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8757; (P) 0.8793; (R1) 0.8813; More....

Immediate focus is now on 0.8741 support in USD/CHF. Decisive break there will argue that whole rebound from 0.8332 has completed at 0.8891. Deeper fall would then be seen back to 0.8550 support next. Nevertheless, strong bounce from current level will retain near term bullishness for another rise through 0.8891 later.

In the bigger picture, a medium term bottom should be formed at 0.8332, on bullish convergence condition in W MACD, just ahead of 0.8317 long term fibonacci support. It's still early to decide if the larger down trend from 1.0146 (2022 high) is reversing. But further rise should be seen to 0.9243 resistance even as a correction.