Sample Category Title

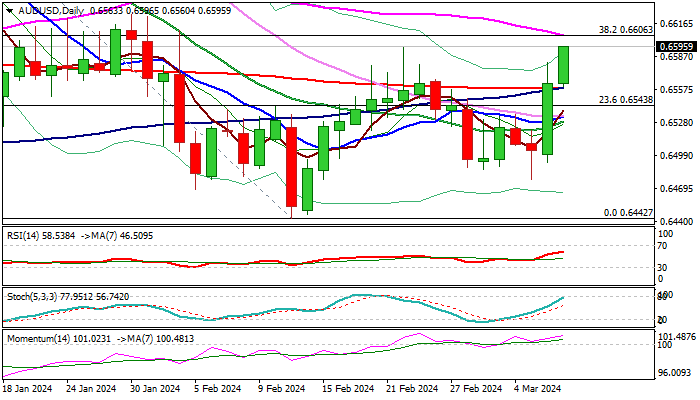

AUD/USD Outlook: Aussie Dollar Rallies for the Second Day and Pressure Pivotal Barriers

AUDUSD advances for the second day, underpinned by weaker US dollar and higher iron ore prices.

The pair hit two-week high and pressure key barriers at 0.6600 zone (near-term range top / Fibo 38.2% of 0.6871/0.6442 descend / 55DMA).

Sustained break here is needed to signal an end of sideways phase and continuation of recovery from 0.6442 (2024 low, posted on Feb 13) and open way for attack at daily cloud (spanned between 0.6642 and 0.6685) and 0.6707 (Fibo 61.8% of 0.6871/0.6442) in extension.

Immediate bullish bias expected to remain in play while broken 200DMA (0.6559) holds

Improving daily studies support the action, as positive momentum strengthens and MA’s turned to bullish setup, with break above converged 100/200 DMA’s (on track to make bull-cross) to additionally boost bulls.

Better than expected economic data from Australia and China are supportive for the Aussie dollar, while the greenback came under increased pressure from relatively dovish remarks from Fed Powell.

Res: 0.6606; 0.6624; 0.6642; 0.6685.

Sup: 0.6559; 0.6543; 0.6526; 0.6492.

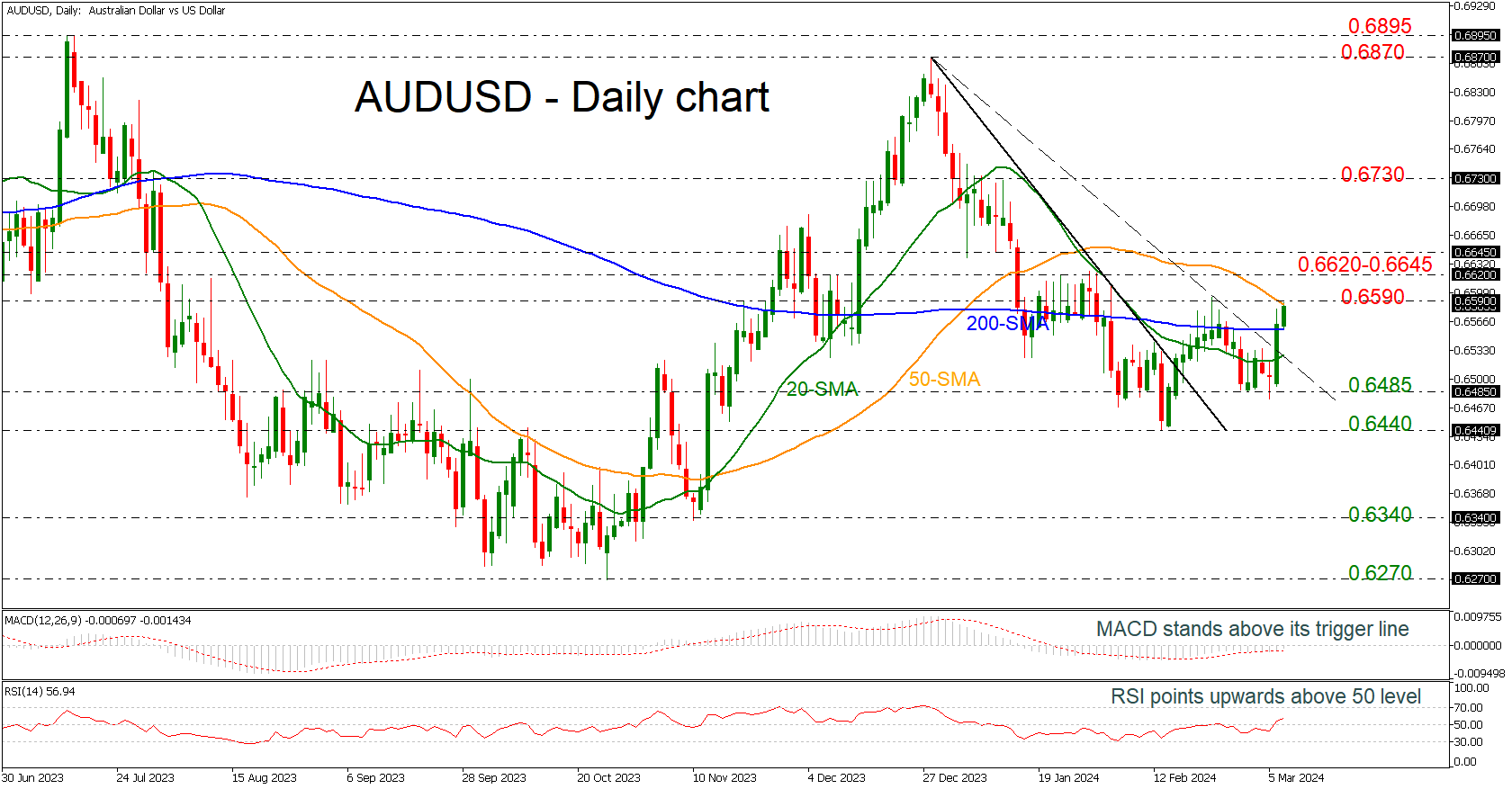

AUDUSD Surges Within Critical Levels

- AUDUSD rebounds off 0.6485 and surpasses downtrend line

- MACD and RSI indicate more upside pressure

AUDUSD has been experiencing a new up leg over the last couple of days, surpassing above the short-term downtrend line and the flat 200-day simple moving average (SMA), meeting the 50-day SMA near the 0.6590 critical resistance.

Technically, the MACD oscillator is standing above its trigger line in the bearish region, while the RSI is pointing upwards above the neutral threshold of 50.

If the market manages to overcome the key region of 0.6590 then it may open the way for more bullish actions towards the 0.6620-0.6645 area ahead of the 0.6790 barricade, taken from the highs on January 9.

On the flip side, a decline beneath the 200- and the 20-day SMAs may increase speculation of a neutral phase, hitting the 0.6485 and 0.6440 support lines. Even lower, the market may switch to a strongly negative one, diving towards the 0.6340 bar.

All in all, AUDUSD is looking neutral in the near-term timeframe, but the break above the downtrend line may add some optimism for traders for some increases.

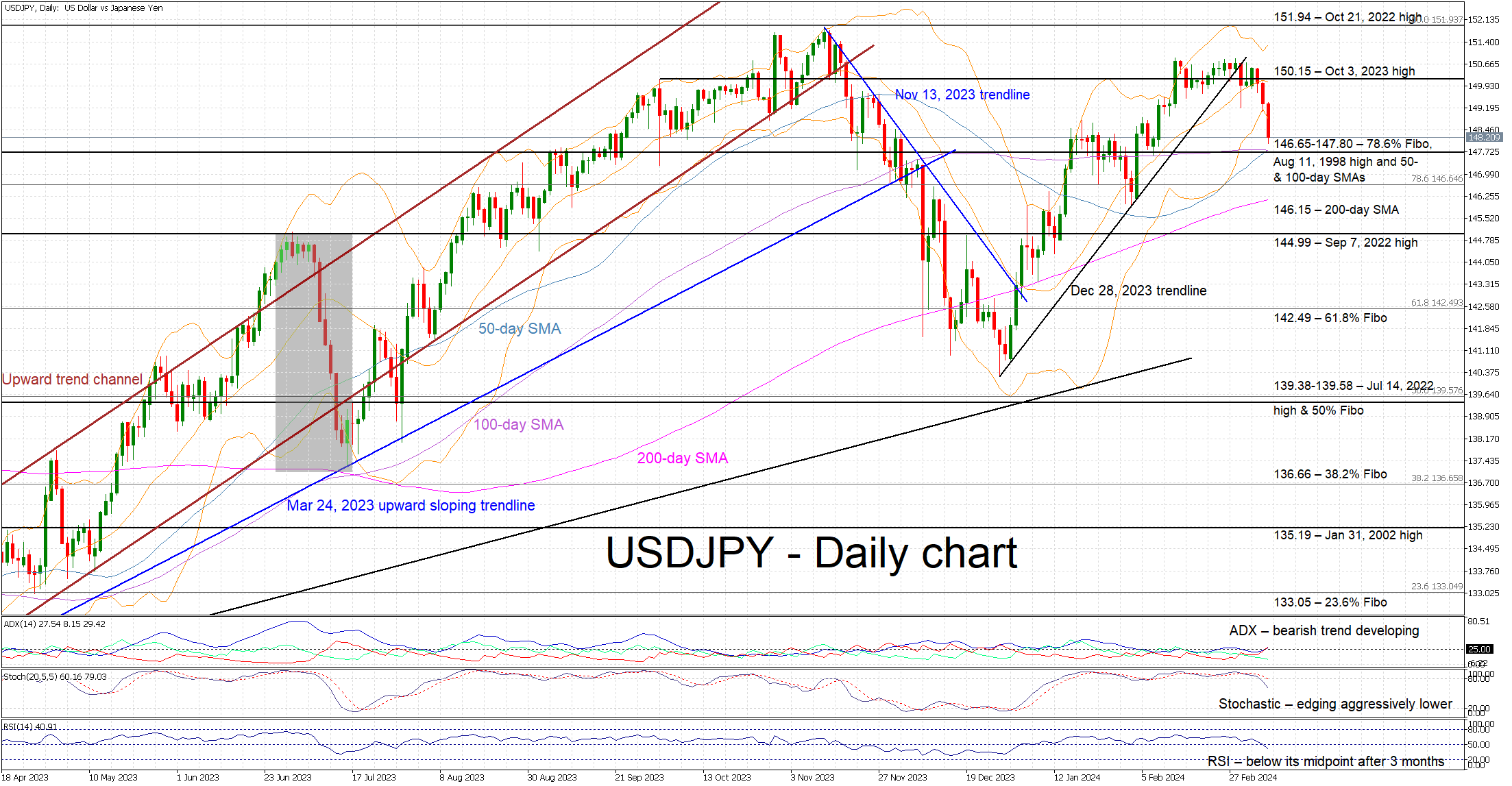

USDJPY Correction Picks up speed

- USDJPY is edging aggressively lower today and closing in on a key support area

- This is the bears' first attempt to push USDJPY significantly below the 150 level

- Momentum indicators support the current correction

USDJPY is recording its third consecutive red candle as recent comments by BoJ members are potentially opening the door to a monetary policy move in the upcoming gathering. USDJPY has managed to drop below the 150 threshold and is getting closer to the busy 146.65-147.80 support area.

In the meantime, the momentum indicators are supportive of the correction. More specifically, the Average Directional Movement Index (ADX) climbed above the 25 threshold and is thus signalling a developing bearish trend in USDJPY. Similarly, the RSI has dropped below its 50-midpoint for the first time in more than 3 months. More importantly, the stochastic oscillator has broken below its overbought (OB) territory and is edging aggressively lower.

Should the bulls remain patient, they could try to regain market control and lead USDJPY again higher towards the October 3, 2023 high at 150.15. If successful, they could then stage a rally towards the October 21, 2022 high at 151.94 and potentially open the door to a new 30-year high.

On the flip side, the bears are keen for the current correction to continue and are possibly preparing to test the support set by the 146.65-147.80 area, which is populated by the 78.6% Fibonacci retracement of the October 21, 2022 - January 16, 2023 downtrend, the August 11, 1998 high, and the 50- and 100-day simple moving averages (SMAs). Even lower, the bears could push USDJPY towards the 144.99 level, provided they overcome the 200-day SMA at 146.15.

To sum up, USDJPY is edging aggressively lower with the bears hoping that the current correction continues with some help from the momentum indicators.

Gold XAU/USD Sets a Historical Record Exceeding $2160 per Ounce

The previous high was around USD 2,135, but gold rose above USD 2,160 an ounce this morning, reaching its highest level ever, as Treasury yields weakened on hopes that the US Federal Reserve will soon begin cutting interest rates.

In a speech yesterday, the Fed chief offered no clarity, saying it would likely be appropriate to ease policy restrictions "at some point this year."

Traders now see a 70% chance of a Fed rate cut in June.

Technical analysis of the XAU/USD chart shows that:

→ the price of gold is in an ascending channel (shown in blue);

→ after a false breakout of its lower border, the price confidently overcame the downward trend line (shown in red) and resistance 2,090;

→ a strong upward impulse led to the RSI indicator entering the extreme overbought zone.

Although the blue ascending channel leaves room for growth to its upper limit, the rise in the price of gold by more than 5% since the first days of March leaves the market vulnerable to a correction — for instance, to the median line of the ascending channel.

James Steel, chief precious metals analyst at HSBC, also says that gold's upward trajectory may slow down. He believes record high prices could cool physical demand for the metal, especially from central banks.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

USD/CAD Analysis: Canadian Dollar Strengthens after Bank of Canada Decision

The Bank of Canada has decided to keep interest rates at 5.0% for the fifth time in a row, it announced yesterday, as it continues to look for clearer signs that inflation is moving closer to the bank's 2% target before considering rate cuts.

According to Bank of Canada Governor Tiff Macklem:

→ the Bank is concerned that underlying inflationary pressures remain.

→ It is too early to ease restrictive policies. There is a clear consensus within the Board of Governors that the time has not come (for rate cuts).

→ We are now in a difficult phase of the monetary cycle.

These hawkish statements contributed to the Canadian dollar strengthening against other currencies, in particular against the US dollar.

Technical analysis of the USD/CAD chart today shows that:

→ for most of 2024, the price moves within the channel shown in blue;

→ yesterday’s news lowered the price from its upper limit to the median;

→ the psychological level of 1.36 retained its role as resistance, although the bulls repeatedly tried to overcome it.

If the bears maintain the initiative, the price of USD/CAD may fall below:

→ breaking through the median line of the channel;

→ breaking through the local trend line (shown by the orange line);

→ attempting to break through the psychological level of 1.35.

In this scenario, the most obvious target for bears may be the lower boundary of the channel, with news about inflation and interest rates remaining the main drivers in the USD/CAD market. Today, by the way, at 16:15 GMT+3, the decision on interest rates from the ECB will become known — be prepared for surges in volatility.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Japanese Wage Data and BoJ Comments Suggest Policy Change Coming Ever Closer

Markets

Fed’s Powell’s semi-annual appearance before the Financial Services Committee of the House of Representative didn’t bring more specifics on the start of the Fed easing cycle s. The Fed Chair noticed considerable progress toward reaching the 2% goal and the Fed is likely to begin dialing back policy restraint at some point this year, but the MPC needs greater confidence that inflation is moving sustainably to the target. During the hearing, considerations on monetary policy were soon overshadowed by the debate on easing the proposals with respect to capital rules for banks. Earlier in the session, ADP job growth and JOLTS job openings were close to expectations. The US yield curve inverted further with the 2-y easing 0.4 bps while the 30-y declined 5.2 bps. Moves in German Bunds again were very limited with yields changing less than 1 bp across the curve. US equities found their composure after Tuesday’s setback (S&P +0.51%). The decline in the US-EMU interest rate differential finally pushed EUR/USD for a test of the 1.09+area (close 1.0899). USD weakness pushed USD/JPY below the 150 barrier. This morning, the move is extended on yen strength as higher than expected Japanese wage data and BoJ comments suggest a policy change is coming ever closer (USD/JPY 148.1). UK Fin Min Hunt announced in the Spring budget some modest tax cuts (including a 2% reduction in the National insurance tax). However, they were not seen as changing the picture for BoE policy in any profound way. Sterling lost marginally against the euro, holding within well-known territory (close 0.8561).

Asian equities trade mixed this morning with China and Japan (stronger yen) underperforming. The dollar remains in the defensive. Later today, markets look out for the ECB meeting, including the Staff’s economic forecast. Especially 2024 growth and headline inflation are expected to be downwardly revised. ECB Lagarde at the press conference will face questions whether this opens the door for ‘earlier’ rate cuts. However, we expect the ECB Chair to avoid any guidance on timing, as the bank looks for more clarity on the outcome of wage negotiations and their impact on core inflation. We don’t expect today’s meeting to be a game-changer for markets. The topside in EMU yields might be capped for now. A further rise in EUR/USD probably will come from USD softness rather than euro strength. EUR/USD 1.0917 (50% retr Dec/Feb decline) is under test. 62% retracement comes in at 1.0969.

News & Views

The Bank of Canada yesterday unsurprisingly kept the policy rate steady at 5%. Economic growth in Q4 was stronger than expected in the January Monetary Policy Report but stayed below potential. The BoC sees signs the labour market is easing, modest hiring and slower wage growth. The data point to an economy in modest supply. Still, inflation’s slow and uneven progress towards the 2% target remains a reason for caution. CPI eased to 2.9% in January but underlying pressures remain a concern. The BoC’s measures of core inflation remain above 3% Y/Y and on a three-month basis and the share of CPI components rising 3%% stays above the historical average. Internal discussions since January shifted from whether the policy rate is restrictive enough to how long it needs to stay at the current level. Before considering to lower the rate, the MPC first wants a further deceleration in core inflation in the coming months. USD/CAD slid yesterday but that was mainly a US dollar move rather than CAD strength. The pair tested but stayed just north of 1.35. Canadian swap yields changed between +1.9 bps (2-y) to -1.2 bps (30-y).

Poland’s central bank left policy rates unchanged as well at 5.75%. New staff forecasts, which assume stable NBP interest rates, show annual CPI at 3.5% (mid-point of the projected range) in 2024, 3.6% in 2025 and 2.9% in 2026. GDP over the same period is seen at 3.5%, 4.2% and 3.2%. Despite inflation is seen falling in coming months to levels consistent with the target, the NBP is particularly worried about the higher core inflation. In addition, the NBP cites substantial uncertainty around the CPI forecast, related to the shielding measures on energy and food prices. They assume a continuation in their current form, creating asymmetric inflation risks (skewed to the upside). Prime minister Tusk on Tuesday already said the cabinet is working on amended protection measures that will probably raise power prices after the current cap ends in June. Given that the NBP also sees medium term demand pressure in the economy coming from wage growth, it stuck to the status quo. The Polish zloty yesterday briefly touched the multi-year highs against the euro below EUR/PLN 4.30. That barrier remains under test this morning.

Keeping Up With the Central Banks

Federal Reserve (Fed) Chair Jerome Powell’s testimony before Congress went smoothly yesterday. He said that the Fed will certainly cut the interest rates this year and that he’s not necessarily looking for inflation to hit the 2% target to start cutting rates. The US 2-year yield eased but remains above the levels that were in play before the Fed’s December dot plot plotted the idea of a 75bp cut plan, and the US 10-year yield fell below 4.10%. News that Steven Mnuchin, the former Treasury Secretary of Trump times, has led a $1 billion cash injection into New York Community Bancorp also soothed investors’ nerves yesterday. The bank rebounded more than 7.5% and the other banks learned, from Powell yesterday, that officials will review their plans to raise banks capital. That’s as good as it gets. And oh, the ADP print came in slightly lower-than-expected and job openings fell, though less-than-expected. Activity on Fed funds futures still gives around 70% chance for the first rate cut in June in the aftermath of Powell’s first day of testimony.

The US dollar index fell sharply below the 50-DMA in the aftermath of a relatively dovish speech from Powell. The index tested a major Fibonacci support, the 38.2% retracement on the ytd rebound. Below this level (103), the dollar index will sink into the medium-term bearish consolidation zone. Gold on the other hand rose to a fresh record and traded at $2161 per ounce on the back of lower yields. But if lower yields are why gold is up, the upside potential should be limited by better appetite in riskier assets that have juicier returns.

But one thing is sure, the broadly softer US dollar will help other central bankers to better cope with inflation at their regions and be able to cut their rates on their turn.

The Bank of Canada (BoC) left its rate unchanged at 5% at yesterday’ decision and the European Central Bank (ECB) will announce its latest policy verdict today. The European policymakers will leave rates unchanged but will revise their economic projections. There is a lot of confusion and uncertainty regarding when Europeans could eventually start cutting their rates as many among them came to push back on expectations of a too-early rate cut in Europe – and they were right given that the doves tend to get well ahead of themselves with the slightest smell of lower rates.

The ECB is expected to revise its inflation forecast down and hint that inflation in the euro area could reach the 2% target sooner than in the December projection. If that’s the case, if the Europeans look confident that inflation is trending lower toward their 2% target, there is nothing to prevent them from cutting rates: the economic outlook is soft, growth is stagnating, a sufficiently soft inflation is the only missing thing.

The broad-based dollar depreciation sent the EURUSD above the 1.09 yesterday. A hint of a June rate cut from the ECB could quickly cast shadow on the euro bulls’ excitement to push this rally to 1.10 level. While both central banks are expected to start cutting rates in June, the Fed is expected to cut by around 80bp while the ECB is seen cutting its own rates by 90bp. And the Fed’s Neel Kashkari went a step further and said that the Fed could cut rates two times, or just one time this year. That’s rational given that the US economy performs well, and definitely better than the Eurozone economies thanks to ample fiscal support. But whatever is the reason, the ECB could cut more if inflation is not a problem. All this to say that, the ECB decision could reverse the euro appetite before the EURUSD makes a sustainable attempt above the 50% retracement on ytd decline.

Elsewhere, the UK’s Budget Day went smoothly. The British voters were made happy with tax cuts and other soothing news on alcohol and fuel duty in the expense of some public services but hey… the 10-year gilt yield remained steady near 4% and Cable could benefit from weaker dollar to drill above the top of the ytd negative trend.

In Japan, the USDJPY fell steeply below 149 as the Japanese wage growth accelerated at the fastest pace since June and the latter fueled speculation that the Bank of Japan (BoJ) could hike its rates already at this month’s meeting. Knowing how cautious the BoJ is with its interest rate policy and inflation, we will unlikely see a concrete action at the March 18-19 meeting, but maybe in the first half. Traders don’t take a big risk shorting USDJPY near 150 as the potential of a rise above this level is limited by direct intervention threat. The only possible way is the downside. We just don’t know when the real slide will begin.

All Eyes on the ECB

In focus today

The Governing Council of the ECB is meeting today. Besides the regular rate announcement, we will also get updated staff projections. The new projections are likely to show inflation for 2025 revised down to 2%. Whereas neither the revised projections nor Lagarde are likely to close the door to a rate cut at any specific meeting, we continue to view June as the key meeting for a first rate cut. We thus expect an unchanged deposit facility rate at 4%. Read more in our ECB Preview - Policy normalisation in sight, 1 March.

We also receive data on German factory orders for January which will give a hint of where the industrial production figures scheduled for tomorrow are heading.

In Sweden, the SNDO releases the February borrowing requirement which it forecast to be a SEK52.2bn surplus. At 13.00 CET, Riksbank vice governor Martin Flodén will speak at an event in Stockholm hosted by Danske Bank Markets.

In the US, FOMC chairman Powell speaks in Congress again, this time in the Senate. In his speech yesterday, Powell gave no new signals, and we still expect Fed to initiate its rate cutting cycle in May.

Economic and market news

What happened overnight

In China, imports and exports for January and February rose far more than expected, signalling what may be the beginning of a turn towards greener pastures ahead for global trade. Exports rose 7.1% y/y for the period whereas imports rose 3.5% y/y. A Reuters poll showed consensus expectations amongst economists had stood at 1.9% y/y and 1.5% y/y respectively.

What happened yesterday

In the US, Nikki Haley withdrew from the republican presidential primaries. Albeit winning the state of Vermont she lost heavily overall to former president Donald Trump, whose road to the republican nomination seems to now just be a formality.

The ADP numbers for February came in line with expectations, as they showed an increase of 140k jobs whereas 150k was the consensus. On Friday we get non-farm payroll numbers for February where we expect 180k jobs created, and seasonally adjusted wage growth of 0.2% m/m.

The JOLTS numbers for January were also in line with expectations showing 8.86m job openings whereas consensus expectations according to a Reuters poll were 8.9m. December numbers were revised down from 9m to 8.89m thus indicating a virtually unchanged number since last month.

In the euro area, retail sales for January grew by 0.1% m/m (consensus 0.2% m/m) thus underlining how consumer spending remains weak. The cautiousness of consumers has also been reflected in recent weak consumer confidence numbers. We believe consumer confidence will pick up this year, which combined with a historically low unemployment should lead to higher spending.

In the U.K., Chancellor of the Exchequer Jeremy Hunt delivered the spring budget. As expected, he confirmed both a lowering of National Insurance by 2pp, as well as freezing both the fuel and alcohol duties.

Geopolitics: As the self-imposed 10 March deadline for Israel to launch an attack into Rafah looms closer, ceasefire talks with Hamas seem deadlocked. If no ceasefire is achieved and Israel launches an invasion into the southern city, it marks another escalation of the conflict, also raising the risk of more severe retaliation by Iran-backed militants in the region.

Equities: Global equities were higher yesterday in a reversal of the moves we saw Tuesday. Macro data was benign without being impressive and like on Tuesday not the driver of equities. One thing that has changed in the last two weeks is the direction of yields with both the short and long end ticking lower. This would normally fuel the appetite for growth stocks, but it has not done so recently as for the moment lower yields are just a positive for both banks and energy and hence a big part of the value space. Another winner in the benign macro, lower yields environment are small caps, and they outperformed large caps again yesterday. In US yesterday, Dow +0.2%, S&P 500 +0.5%, Nasdaq +0.6% and Russell 2000 +0.7%. Asian markets are mostly lower this morning, with Japanese stocks leading the declines for a change. US futures are lower this morning while futures in Europe are more mixed.

FI: US Treasury yields decline as Federal Reserve Chairman Powell "sticks to the script" as he stated that rate cuts will come this year, but the Federal Reserve is on hold for now. Hence, there was no new information in the statement from Powell and this was taken positively by the market.

FX: EUR/USD creeped higher yesterday amid Powell's testimony and trades just above the 1.09-mark ahead of ECB, which we expect will not rock the boat in terms of new policy signals. Meanwhile, monetary policy speculations continue to pull JPY crosses lower with USD/JPY now around 148.50. BOC sent USD/CAD almost a full figure lower to 1.35 and has hovered just above overnight. A recovery day for Scandies yesterday in slight risk on, which broughT EUR/NOK to around 11.43 and EUR/SEK closer to our1M 11.20 target.

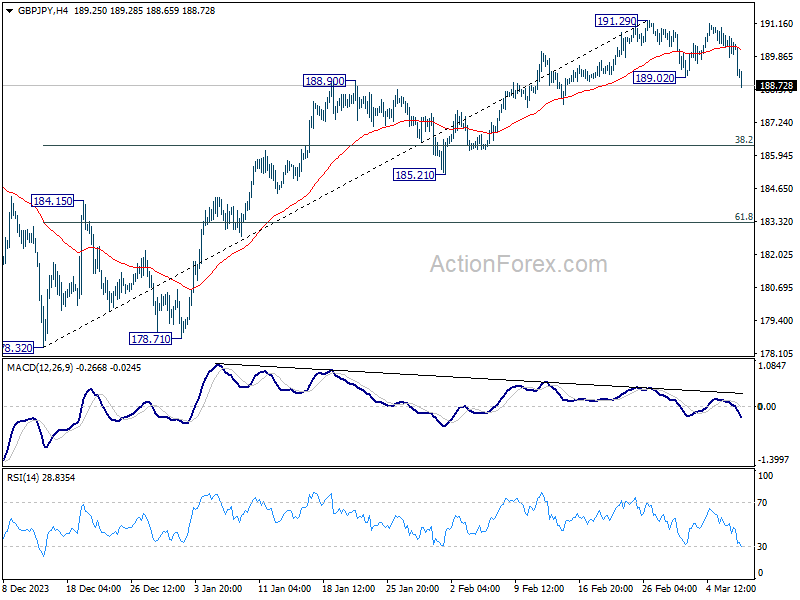

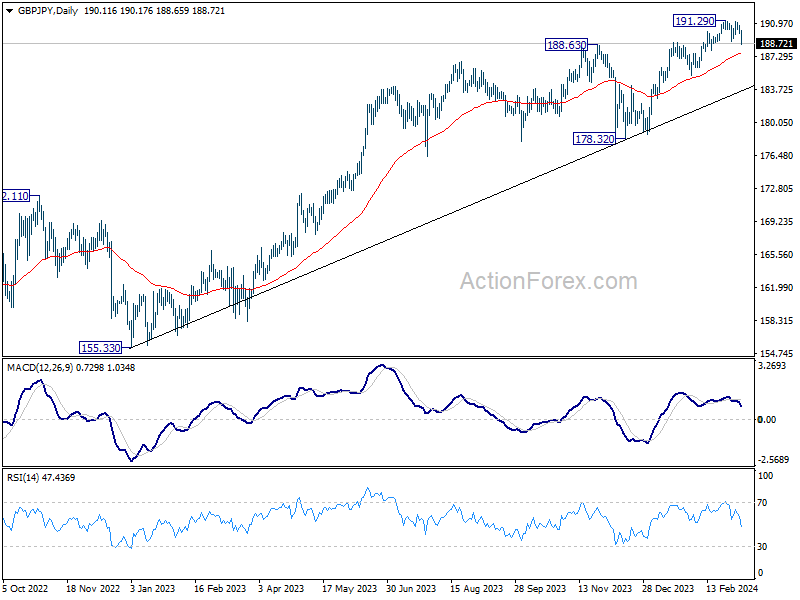

GBP/JPY Daily Outlook

Daily Pivots: (S1) 189.82; (P) 190.26; (R1) 190.67; More.....

Intraday bias in GBP/JPY is back on the downside with break of 189.02 support. Price actions from 191.29 are seen as a correction to rise from 178.32 for now. Deeper fall would be seen to 38.2% retracement of 178.32 to 191.29 at 186.33. Sustained break there will raise the chance of larger reversal and target 61.8% retracement at 183.27. Risk will now stay on the downside as long as 191.29 resistance holds, in case of recovery.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

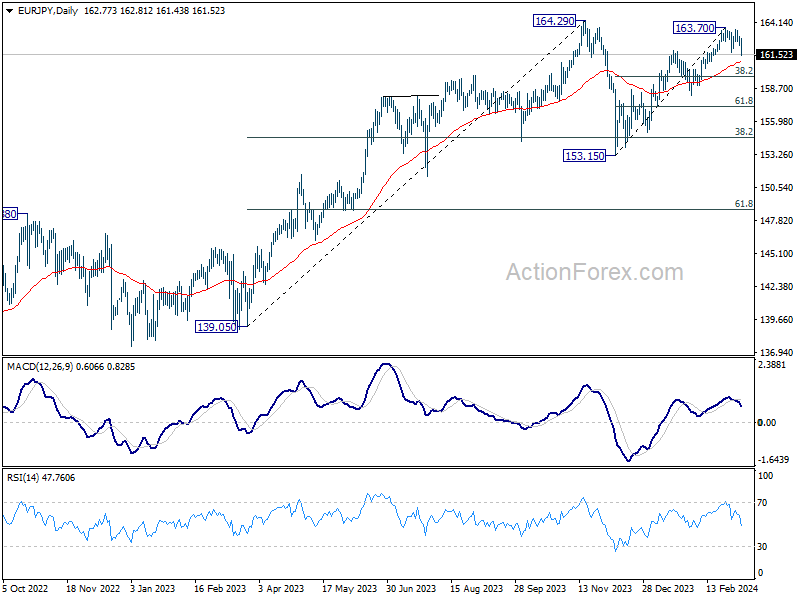

EUR/JPY Daily Outlook

Daily Pivots: (S1) 162.38; (P) 162.67; (R1) 163.14; More...

Intraday bias in EUR/JPY is back on the downside with break of 161.67 support. Price actions from 163.70 could be a correction to the rally from 153.15, or reversing the whole move. In either case, deeper fall would be seen to 38.2% retracement of 153.15 to 163.70 at 159.66. Sustained break of 159.66 will affirm the latter case and target 61.8% retracement at 157.18. For now, risk will stay on the downside as long as 163.70 resistance holds, in case of recovery.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 which could still be extending. As long as 148.38 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage. Next target would be 169.96 (2008 high).