Sample Category Title

BoC to Deliver Another Dovish Hold, Unemployment Rate to Tick Higher

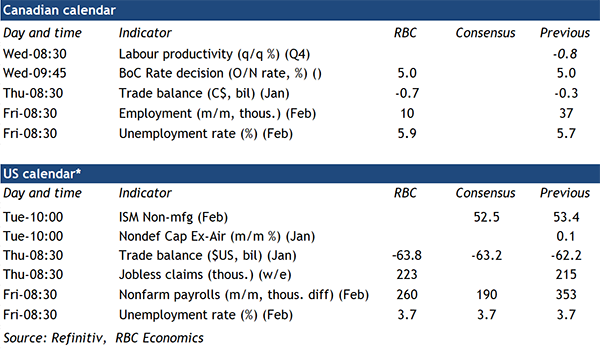

The Bank of Canada is widely expected to maintain the overnight rate steady again at its meeting on Wednesday. An announcement on the ending of quantitative tightening is unlikely but we expect that to follow later in April. Over past meetings, the BoC has been gradually and cautiously moving towards a more dovish stance. Language around the need to hike rates further was already dropped in January and is unlikely to reappear in the statement next week. The central bank will instead continue to highlight softening in aggregate demand while reiterating that inflation pressures, although easing are still a risk.

Economic data since the last monetary policy meeting in January largely confirmed the weakening of the Canadian economy. The 1% annualized increase in gross domestic product in Q4 2023 was above the flat reading that the BoC expected. But details were much softer with growth in Q4 coming almost entirely from net exports. Domestic consumers and businesses on the other hand continued to pull back spending and investment activities. GDP growth was, again, slower on a per capita basis as population growth outpaced output for a sixth consecutive quarter.

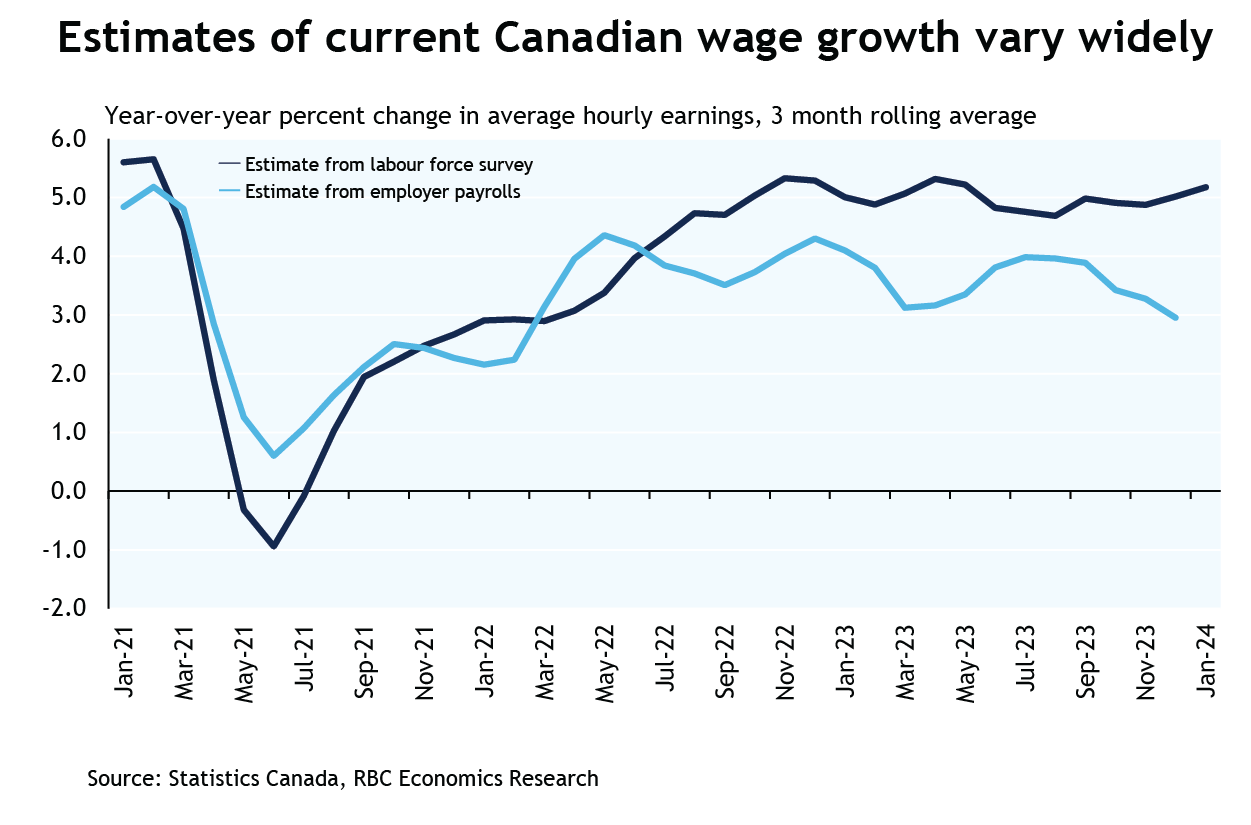

We expect February labour market data released on Friday after the BoC’s decision to show another gain in employment. It will however not be large enough to prevent an increase in the unemployment rate to 5.9% as hiring demand keeps falling short of the rising supply of workers. Labour market numbers for January were firmer than expected with wage growth remaining high. But lower job openings continue to highlight slowing labour demand. Other Statistics Canada estimates of wage growth derived from business payrolls submissions have slowed more significantly. The silver lining of all the softening in the economy is that inflation pressures will likely continue to ease rather than reaccelerate. Our base case continues to assume the BoC will start moving the overnight rate lower in June after more data confirming easing inflation back towards target.

Week ahead data watch:

January’s Canadian trade data is likely to show monthly declines in both export and exports with rail carloadings (-7.7%)— contracting sharply that month. Oil prices went up 2.8%, and that will impact the value of energy exports and imports. Overall, we expect the trade deficit ($700 million) to widen from the prior month.

The U.S. trade balance (US$-63.8B) likely widened in January given the goods deficits from the advance trade report increased by US$2.3B. Much of that was driven by higher imports of autos, and capital goods.

We expect February U.S. payroll numbers to show another solid employment gain, with growth mainly coming from the leisure and hospitality, health care, and government sectors. We expect the unemployment rate to hold steady at 3.7%.

European Central Bank Gravitating Toward A Mid-Year Rate Cut

Summary

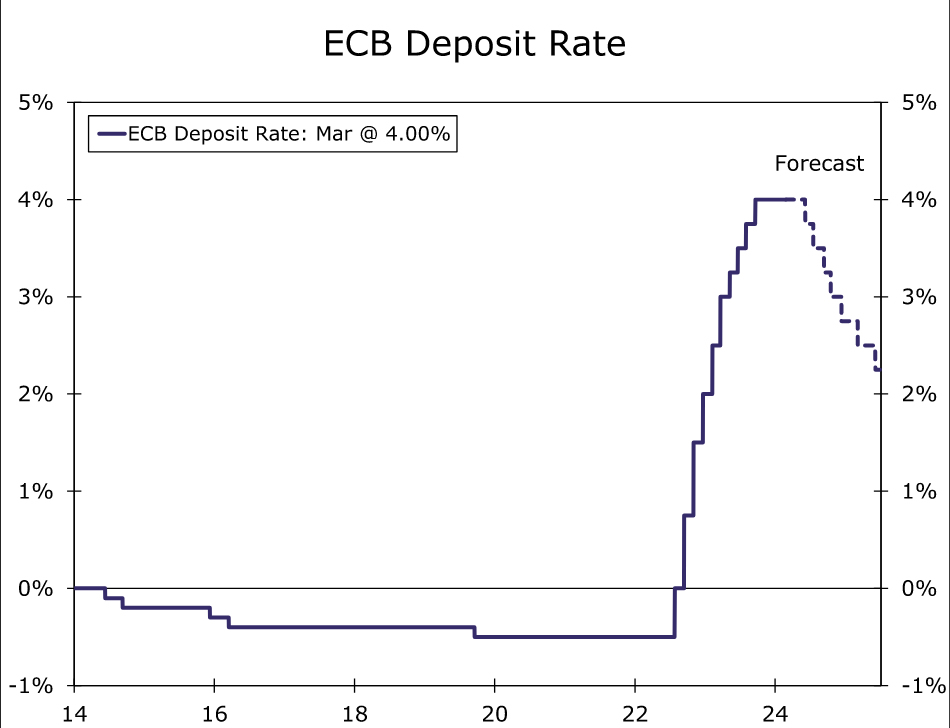

The Eurozone economy faced a particularly challenging period during the second half of 2023, with the region only narrowly avoiding a technical recession. Given the challenging growth environment, the European Central Bank (ECB) ended its tightening cycle with a final 25 bps rate hike in September last year and has, since early 2024, indicated the next move is likely to be a rate cut. The outlook for ECB monetary easing has been fluid, with expectations for an initial ECB rate cut at times fluctuating between April and June. That said, firmer Eurozone PMI surveys, a still-gradual disinflation process, and the weight of ECB policy rhetoric have seen expected rate cut timing shift more solidly towards June. In that context, we now also expect the ECB will begin its easing cycle with a 25 bps Deposit rate cut to 3.75% at its June monetary policy announcement.

Eurozone Economy Shows Tentative Signs of Stabilization

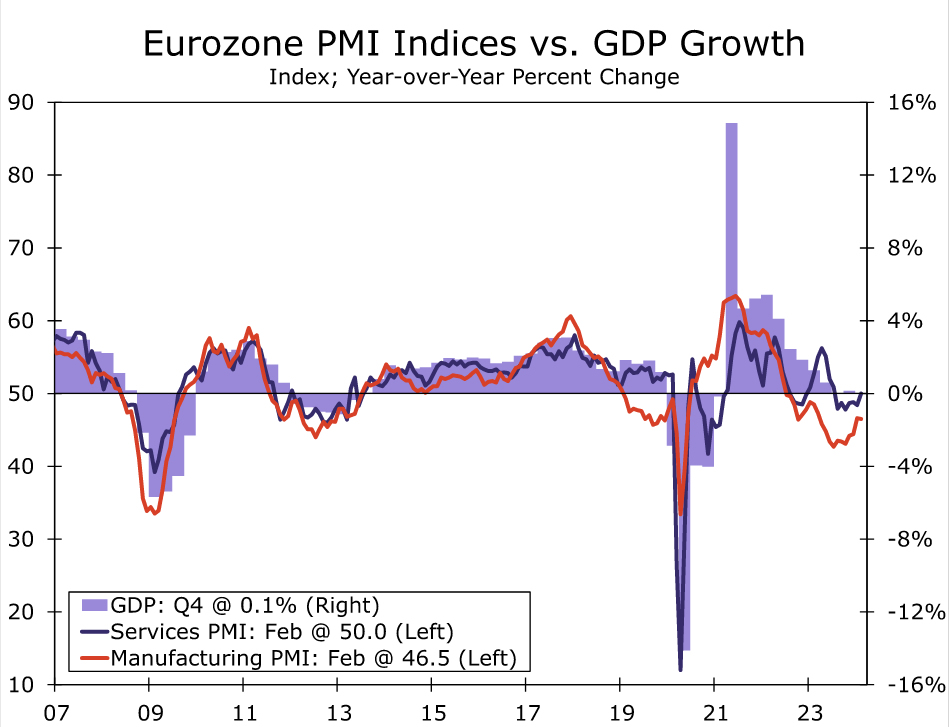

One of the most significant data releases since the European Central Bank's (ECB) most recent policy announcement was the Eurozone PMI surveys for February. Of particular note, the February service sector PMI rose more than expected to 50.0, from 48.4 in January. That saw the services PMI exit contraction territory for the first time since July of last year. Service sector sentiment for the region's largest economies was also favorable, as Germany's services PMI rose to 48.2 and France's services PMI rose to 48.0. The news from the Eurozone manufacturing PMI was not as upbeat, as that index unexpectedly eased to 46.5 in February from 46.6 in January, driven by weakness in German manufacturing. Still, with the service sector a much more sizable portion of the overall economy, the Eurozone composite PMI also rose to 48.9 in February, from 47.9 the prior month. Although not as significant as these headline figures, the details of the February PMI survey also hinted at lingering inflation pressures. The report noted that growth of average input costs across producers of goods and providers of services accelerated for a second successive month to reach the highest level since last May. The report also said that selling price inflation likewise accelerated, up for a fourth month running in February to also hit the highest level since last May.

Other confidence surveys since the ECB's latest announcement are more mixed. At a national level, Germany's February IFO business confidence index rose to 85.5, but French business confidence and Italian economic sentiment both fell in February. Meanwhile, the European Commission's Economic Sentiment Indicator for the Eurozone also fell to 95.4 in February, but that same survey showed the Employment Expectations Indicator edging up to 102.5 in February, a level historically consistent with positive jobs growth. That suggests steady Eurozone labor market trends can continue. In recent weeks, labor market indicators have shown continued employment growth in Q4 of 0.3% quarter-over-quarter and 1.3% year-over-year, and a January unemployment rate that fell to 6.4%, a record low. Taken together, the firming in the PMI indices and mixed readings from other sentiment surveys, along with steady labor market trends, offer early—albeit tentative—signs the Eurozone economy is stabilizing. At the margin, we think tentative economic stability has reduced the urgency for ECB monetary easing, and is a contributing factor to expectations for an initial ECB rate cut getting pushed back to mid-year.

Eurozone Inflation News Still Favorable, But How Long Will It Continue?

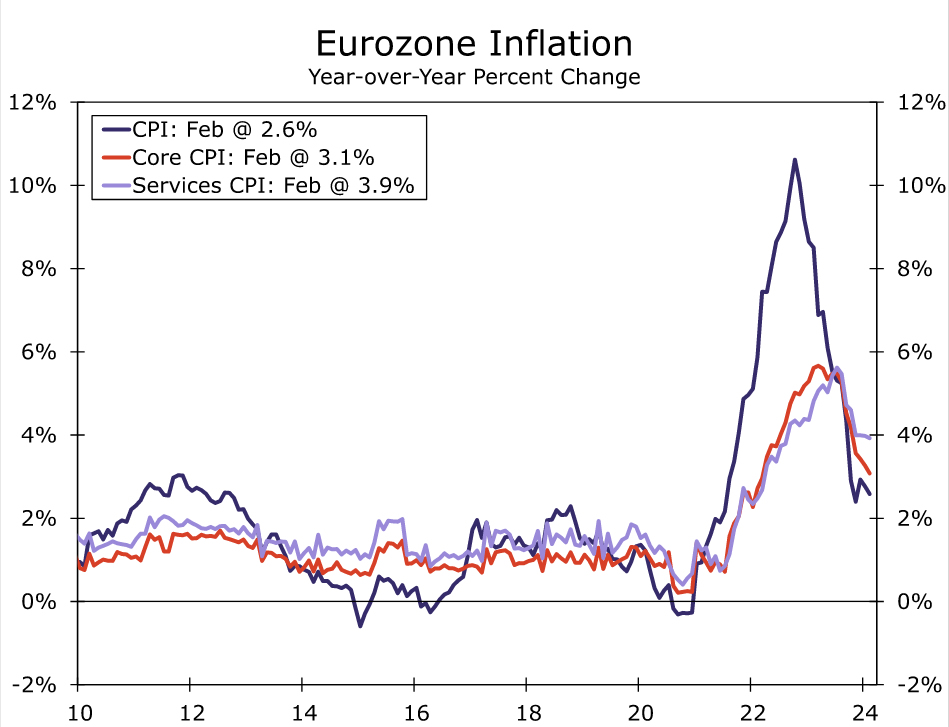

The other key pieces of Eurozone economic news since the ECB's latest policy announcement were inflation data for January and February. Those figures revealed some further progress on the disinflation front, albeit at a gradual pace. For the February CPI, headline inflation slowed to 2.6% year-over-year and core inflation slowed to 3.1% year-over-year. Service sector inflation remained somewhat sticky, easing only slightly to 3.9%. To be sure, the deceleration in annual inflation was flattered by base effects related to the large price increases that were seen in early 2023. Taking a closer and more granular look and price trends over the past six months, we note that the CPI excluding food and energy—which is close to but not identical to the official core CPI measure—has advanced at a 2.3% annualized pace. Thus even over this shorter time period, underlying inflation trends have moved closer to, but not yet converged, to the ECB's 2% inflation target. And likely of concern to ECB policymakers, services inflation has persisted over the past six months, rising at a 3.4% annualized pace during that period.

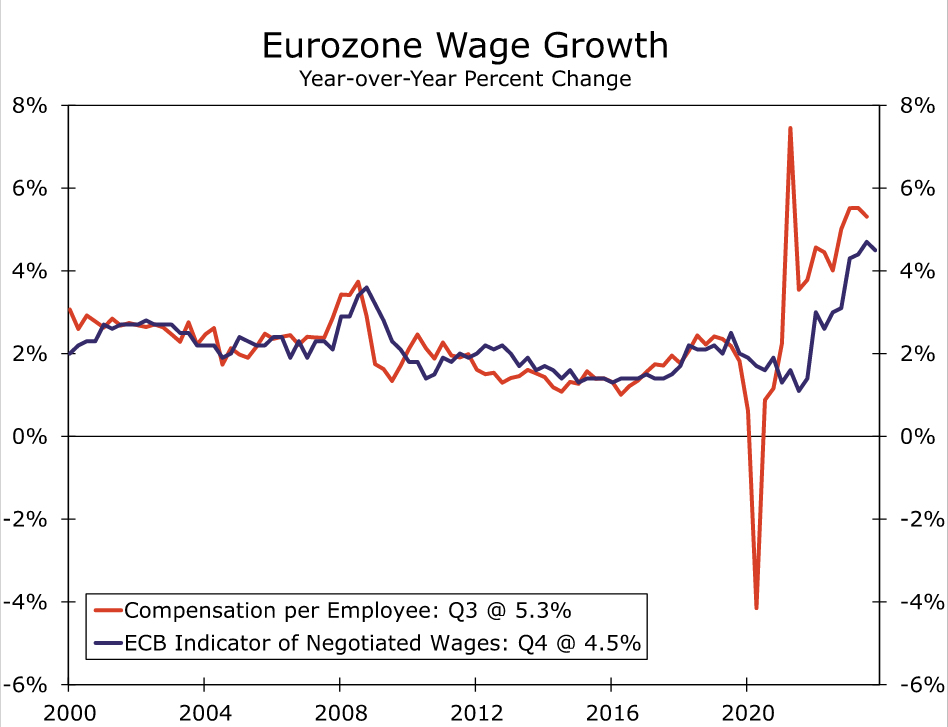

Another reservation regarding the inflation outlook, and one cited by several ECB policymakers, is the still-elevated pace of wage growth. The most up-to-date wage figures available on a Eurozone-wide basis is the ECB's indicator of negotiated wages. The negotiated wage index decelerated slightly to 4.5% year-over-year in Q4 from 4.7% in Q3 but, at least for now, suggests wage growth is at a level that is probably still too high to achieve the 2% inflation target on a sustained basis. The fact that the unemployment rate is at a record low perhaps reinforces concerns that wage growth may decelerate only gradually. It is against this backdrop, and despite the improving inflation trends of the past several months, that ECB policymakers have been wary of moving too aggressively in lowering interest rates, and have indicated an increasingly clear preference to see wage trends from early 2024 before making a decision to adjust interest rates. Those wage data for early 2024 will only be available in time for the ECB's June monetary policy announcement, and not for the ECB's April monetary policy announcement.

Chief among comments from policymakers have been those of ECB President Lagarde. Among her more recent comments, she said the ECB must be convinced that disinflation is sustainable and that Q1 wage data will be important for the ECB's assessment. Some other policymakers (Nagel, Holzmann, Schnabel) have cautioned against early rate cuts, while others have indicated a desire to see more wage data or even cited June as more likely timing for initial ECB easing. In the wake of these comments, market participants are now pricing in just 6 bps of rate cuts for the April meeting, and 24 bps of rate cuts for the June meeting.

Given current market pricing, it would likely take a proactive effort from ECB policymakers to accelerate the market's easing expectations and to allow for an April rate cut to become a more realistic possibility. That proactive guidance from ECB policymakers is something we view as a low probability outcome. Indeed, for those hoping for dovish elements from the ECB monetary policy announcement on 7 March, at best we expect the ECB to repeat it is “not there yet” on inflation, to perhaps caution against premature monetary easing, and to repeat that its preference is to see more wage data before adjusting its policy interest rate. At worst, we would not completely rule out more aggressive guidance in which the ECB takes the possibility of an April rate hike off the table. The other key element of the ECB's March monetary policy announcement to watch will be the central bank's updated economic projections. In the absence of a significant downward revision to its inflation forecast (in December, the ECB projected CPI inflation ex food and energy at 2.3% in 2025 and 2.1% in 2026), there would also be little reason for market participants to pull forward their expected rate cut timing. Since we view dovish policy guidance and/or a sharp downward revision to inflation forecasts as unlikely at the ECB's March announcement, and at the risk of adjusting our own forecasts with 'perfectly imperfect' timing, we now view an initial 25 bps Deposit Rate cut to 3.75% at the ECB June's monetary policy announcement as the most likely outcome.

Beyond the initial June move, we expect the ECB will keep lowering interest rates in steady 25 bps rate cut increments at the following meetings. We expect Eurozone economic growth to improve, but remain moderate overall. Meanwhile, we expect wage growth in particular, and price inflation to a lesser extent, to decelerate further as the year progresses. Should those economic trends transpire, we forecast the ECB will follow up with 25 bps rate cuts at the July, September, October and December meetings, which would see the Deposit Rate end 2024 at 2.75%. As the ECB's policy rate moves somewhat closer to a more neutral level and economic activity firms further in 2025, we expect a step down in the pace of ECB rate cuts to once per quarter next year. We forecast 25 bps Deposit Rate cuts in March, June and September 2025, which would see the ECB's policy rate reach a terminal level of 2.00% by late next year.

Week Ahead – ECB Decision and US Payrolls to Steal the Show

- Nonfarm payrolls and Powell’s testimony will be crucial for US dollar

- European Central Bank could set the stage for summer rate cuts

- Bank of Canada decision and UK budget announcement also in focus

Dollar braces for US payrolls

Riding high on a wave of US economic resilience, the dollar is currently the best-performing major currency this year, having gained nearly 3% against a basket of currencies in a couple of months.

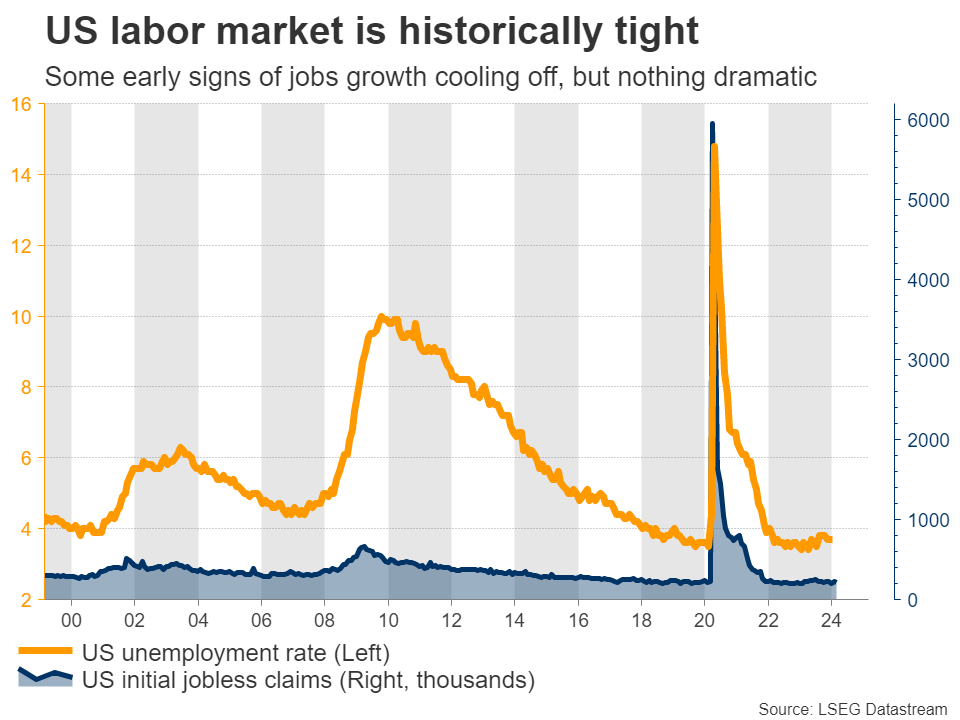

This stellar performance reflects an impressive US economy. Economic growth is running at a solid pace, the labor market remains historically tight, and inflation is not cooling as rapidly as investors had hoped.

With the economy still hot, traders have been forced to unwind bets of imminent Fed rate cuts. Markets are currently pricing just three rate cuts for this year, down from six cuts a few months ago. Hence, investors expect US interest rates to stay at higher levels for a while longer.

Grim economic prospects in the rest of the world have also benefited the dollar. The United Kingdom and Japan have fallen into technical recessions, the Eurozone is haunted by stagnant growth, and China is still dealing with the fallout in its property sector. As such, the alternatives to the dollar are not very attractive at this stage.

Next week’s events will help shape this narrative. The ball will get rolling on Tuesday with the release of the ISM services index for February, ahead of the private ADP employment data on Wednesday.

Meanwhile, Fed Chairman Powell will appear before Congress both on Wednesday and Thursday for his semiannual testimony. Investors usually focus on the Q&A session with lawmakers, where the Fed chief will be grilled on the economic outlook.

Of course, the main event will come on Friday, when the latest US employment report hits the markets. Economists expect another round of solid jobs numbers, which would reaffirm that the labor market remains in good shape. Some early indicators pointed to a slowdown in employment growth in February, but nothing dramatic.

Has the ECB fallen behind the curve?

In the Eurozone, the central bank is widely expected to keep rates steady on Thursday, so the spotlight will fall mostly on the updated economic projections and any signals by President Lagarde on the timing of rate cuts.

The euro area economy hit a wall last year, as high interest rates started to bite demand and governments dialed back their spending. Germany has been hit particularly hard, with a slowdown in global trade crippling its export-heavy business model.

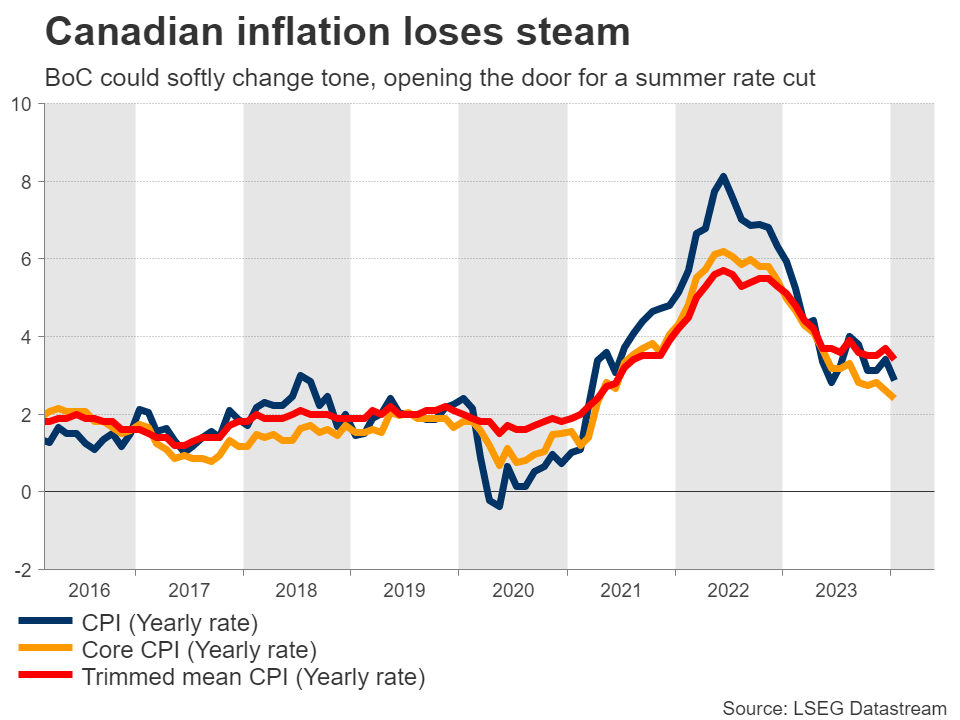

Mirroring this economic slowdown, inflation has lost steam, falling to an annual rate of just 2.6% in February. Wage growth has started to lose speed as well, although it remains at high levels.

Despite this loss of momentum, ECB officials have stressed that it’s still too early to cut rates, as doing so prematurely could fuel a second round of inflation. Most officials have circled June as the most likely month for a rate cut, which would give them access to updated wage numbers.

This meeting will probably be used as a ‘stepping stone’ towards June, with the central bank reaffirming it will be patient with rates until it is certain inflation has been crushed.

Normally, this would be a positive message for the euro. However, this time may be different. The Eurozone economy is already staring down the barrel of a recession and the longer the ECB waits to cut rates, the more painful the downturn might be. In turn, that could force the central bank to cut even deeper later on.

The ECB is laser-focused on wage growth, which unfortunately is one of the most lagging economic indicators. Waiting too long to act could inflict unnecessary damage on the economy and lead to a situation where rates are ultimately slashed with brute force. That paints a gloomy picture for the euro, even if the ECB preaches patience next week.

UK budget and Canadian rate decision coming up

Crossing into the United Kingdom, the government will unveil its latest budget on Wednesday. The Chancellor has made it clear he wants to cut taxes for workers, in a last-ditch attempt to win back voters before a general election that will almost certainly be a disaster for the ruling party.

In the markets, the action will depend on which taxes are cut and how deeply. Meaningful cuts to income tax or national insurance could spell good news for the pound, as that would fuel spending and inflation, adding pressure on the Bank of England to keep rates high for longer. That said, there isn’t much scope for drastic tax changes, so any reaction might be relatively small.

Over in Canada, the central bank will conclude its meeting on Wednesday. Markets are pricing in a 15% probability of an immediate rate cut, but that is highly unlikely considering that the economy is still in decent shape. The housing market in particular is extremely hot, boosted by record levels of migration.

That said, it’s only a matter of time until the Bank of Canada does cut, as inflation has slowed sharply. Markets are pricing in the first rate cut during the summer. Hence, this meeting may bring a soft change in tone, whereby the Bank lays the groundwork for such a move. The nation’s employment data will follow on Friday.

Finally, some data releases from Japan, China, and Australia could attract attention. Starting on Tuesday, the latest inflation stats from Tokyo will give investors a sense of whether the Bank of Japan will raise rates this year. Australia’s GDP data for Q4 will be released on the same day, alongside China’s services PMI for February.

Weekly Focus – Focus Turns to the ECB

Markets were in a waiting mode ahead of the March monetary policy meetings, and the latest round of inflation data did not materially rock the boat. Bond and equity markets remained stable while past weeks' positive sentiment in FX markets took a breather.

Euro Area flash HICP for February came out above expectations at 2.6% y/y (Jan 2.8%) while core inflation was 3.1% (Jan 3.3%). Somewhat worryingly, monthly momentum in services inflation picked up speed, suggesting that underlying price pressures have remained uncomfortably elevated.

In the US, the Fed's preferred measure of underlying inflation, the Core PCE, came in line with expectations at +0.4% m/m SA. Real consumption volumes fell by 0.1%, driven by weaker demand for cars and other big-ticket goods, while services activity remained more upbeat. This was reflected in prices as well, as core goods deflation continued (-0.05% m/m) while core services inflation picked up speed (+0.6% m/m). The Fed's Mester summarized the data by saying it did not 'change the calculus on policy rate decision'.

On the political front, US congress once again avoided looming risk of a partial shutdown with fourth short-term 'continuing resolution' funding bill in a row. This time, some signs of more concrete progress are emerging after congressional leaders signalled that they have reached an agreement on six of the 12 individual appropriations bills needed to fund the government. The new deadline for passing the bills is next week's Friday, while the remaining six are still up for negotiations with an extended deadline on 22 March.

Next week's key event will be the ECB meeting on Thursday. We and the markets expect no monetary policy changes, as recent speeches by governing council officials have suggested that ECB has set their sights on the first rate cut in the June meeting, in line with our call. ECB will also publish updated staff economic projections, where inflation will likely be revised to 2% for 2025. Growth forecasts will likely be revised lower for this year and remain broadly unchanged for 2025 and 2026. Read more from our ECB Preview - Policy normalisation in sight, 1 March.

On the data front, focus will be on labour market data from the US, with January JOLTs, ADP and finally the February Jobs Report due for release. We expect NFP growth to cool down to 180k and average hourly earnings to land at +0.2% m/m after the surprisingly strong January report. Leading data has provided mixed signals, but this week's Conference board's consumer sentiment survey showed an unexpected dent to previous months' optimism. We discussed the latest data signals in our US Labour Market Monitor, 1 March.

In China, the annual key policy event, the 'Two Sessions', is up next week starting Monday, where focus will be on the government's work report at the National People's Congress (NPC). The report will include China's new growth target, budget target and other key plans for the year. The growth target is widely expected to be set again at 5.0%, even if it seems like a fairly ambitious target given the less favourable base effects for 2024.

Finally, Danske Bank Research will publish updated economic projections for global and Nordic economies in the Nordic Outlook, due for release on Tuesday morning.

ECB Preview – Policy Normalisation in Sight

Next week, on Thursday 7 March, the ECB is set to take another step in its policy normalisation process, from a restrictive monetary policy stance towards a neutral stance. The new staff projections on growth outlook are expected to be revised lower this year and broadly unchanged in 2025/2026. Inflation is set to be revised to 2% for 2025. While neither the revisions to staff projections nor Lagarde will close the door to a rate cut at a specific meeting, we continue to expect that the key meeting for the first rate cut will be the meeting in June. We do not believe that the incoming data since the January meeting has been sufficiently weak to make April the baseline meeting (see appendix on European data at the end of this report).

Markets significantly repriced policy easing expectations in February from around 150bp worth of rate cuts to 87bp. We continue to expect the first rate cut in June of 25bp and 75bp worth in total for this year.

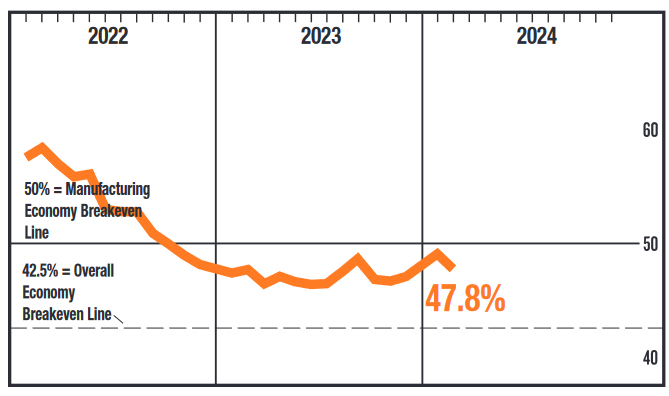

US ISM manufacturing falls to 47.8, 16th month of contraction

US ISM Manufacturing PMI fell from 49.1 to 47.8 in February, below expectation of 49.5. Manufacturing sector continued to contract for the 16th month.

Looking at some details, new orders fell from 52.5 to 49.2. Production fell from 50.4 to 48.4. Employment fell from 47.1 to 45.9. Prices fell from 52.9 to 52.5.

ISM said: "The past relationship between the Manufacturing PMI and the overall economy indicates that the February reading (47.8 percent) corresponds to a change of plus-1.5 percent in real gross domestic product (GDP) on an annualized basis."

BoE’s Pill: Interest rate cuts “some way off” pending inflation evidence

BoE Chief Economist Huw Pill suggested in a speech that interest rate cut is still "some way off" in his baseline scenario.

He emphasized the need for more "compelling evidence" that the persistent component of UK CPI inflation is is being "squeezed down" towards rates that align with 2% inflation target on a lasting and sustainable basis.

"It is that view that led me to vote to keep Bank Rate unchanged in February," he added.

Fed’s Barkin cautious on rate cuts amid lingering inflation pressures

Richmond Fed President Thomas Barkin expressed a cautious stance on the prospect of Fed starting to cut interest rates in the near future, citing ongoing inflation pressures as a primary concern.

In an interview with CNBC, Barkin emphasized the need for inflation to normalize before considering adjustments to the interest rate policy. "I'm still hopeful inflation is going to come down and if inflation normalizes then it makes the case for why you want to normalize rates, but to me it starts with inflation," Barkin stated

Barkin highlighted continued wage and inflation pressures, referencing a recent report indicating high inflation levels. While he noted some stabilization in goods inflation, Barkin pointed out that inflation in the services sector remains a challenge.

"I still see wage pressures, I still see inflation pressures...we just had a high inflation report yesterday... On the goods side inflation is settling. On the services side, not so much," he elaborated.

EUR/USD Steady After Eurozone Inflation Dips

- Eurozone inflation falls to 2.6%

- Eurozone unemployment rate drops to record low of 6.4%

The euro is calm on Friday. In the European session, EUR/USD is trading at 1.0818, up 0.13%.

Eurozone inflation eases to 2.6%

Inflation continues its downward trend in the eurozone. On Thursday, Germany and France saw inflation fall in February. The eurozone followed suit on Friday, as headline inflation dropped to 2.6% y/y in February, down from 2.8% in January.

This was the lowest rate in three months but was above the market estimate of 2.5%. A sharp drop in energy prices was the main reason for the drop in inflation. However, February inflation rose 0.6% m/m, higher than expected and above the January reading of -0.4%. This upswing was mainly due to services inflation which remains sticky and this will be a concern for the European Central Bank.

The core inflation rate, which excludes food and energy, fell to 3.1% in February, down from 3.3% in January but higher than the market estimate of 2.9%.

The slight decline in inflation is welcome news but is unlikely to have much sway on policy makers at the ECB, as the drop was mainly due to base effects. The ECB remains concerned about cutting rates too early and then having to deal with inflation reversing directions and accelerating. The next meeting is on March 7th and the central bank is expected to maintain the deposit rate at 4.0%.

Overshadowed by the inflation release was the eurozone unemployment rate, which ticked lower to 6.4% in January, down from a revised 6.5% in December and matching the market estimate. This was the lowest level since the formation of the eurozone in 1999. (The initial December release came in at 6.4% but was revised upwards to 6.5%.)

The impressive unemployment rate points to a robust labour market, which is surprising given that the economy has been in poor shape. The solid labour market and strong wage growth means there is less pressure on the ECB to lower interest rates.

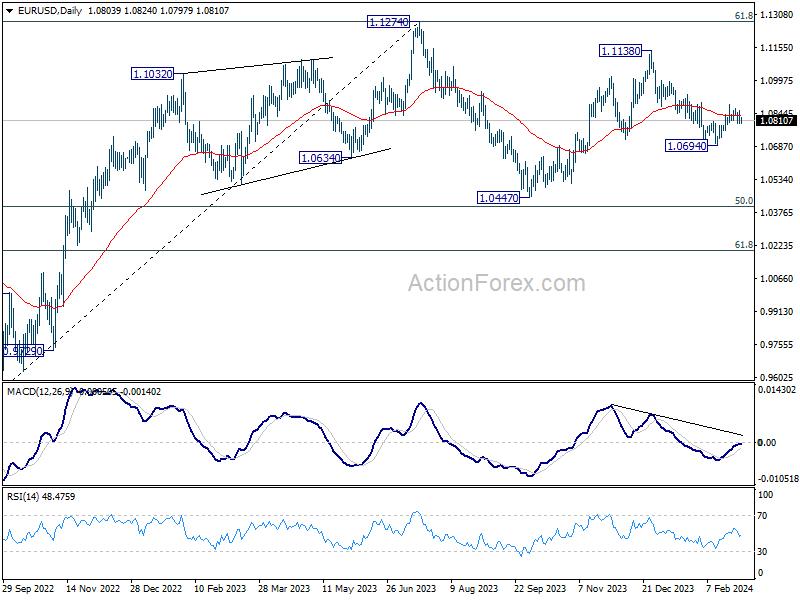

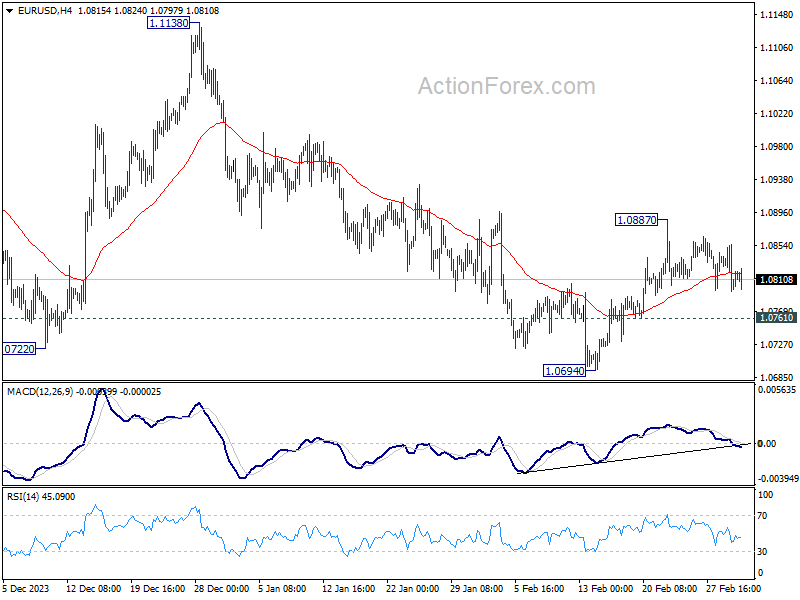

EUR/USD Technical

- EUR/USD is testing resistance at 1.0819. Above, there is resistance at 1.0842

- 1.0782 and 1.0759 are providing support

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0782; (P) 1.0819; (R1) 1.0842; More...

No change in EUR/USD's outlook and intraday bias stays neutral. On the upside, break of 1.0887 and sustained trading above 55 D EMA (now at 1.0832) will affirm the case that fall from 1.1138 has completed. Stronger rally would then be seen back to 1.1138. However, break of 1.0761 will turn bias back to the downside for retesting 1.0694 support.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.