Sample Category Title

Regional Prints Reveal Stickiness in Core Inflation

In focus today

In the euro area we will get the HICP print for February. With the regional data we got yesterday (see more below) we will probably see HICP come in at 2.5% y/y or 2.6% y/y, down from 2.8% in January. That is a little higher than the 2.4% we first expected before yesterday's releases. Core inflation showed signs of stickiness, meaning that taking yesterday's releases into account the core inflation print will probably decrease to 2.9% or 3.0% from 3.3% in February.

In the US, today's main data release will be the ISM Manufacturing index for February. Consensus expects a further increase to 49.5 (from 49.1) following a modest uptick in the flash PMIs. We will also have a range of Fed speakers on the wires today, including a Waller, Logan, Bostic, Daly and Kugler. We also get the University of Michigan consumer sentiment indicator.

February PMIs are released in several countries today, including Sweden. The new order-to-inventory spread in Sweden has seen a clear upward shift over the past six months, which at least historically has been a rather reliable go-ahead signal for production to increase. Whether or not this shows up in today's data remains to be seen, but it should not be far off in any case.

Economic and market news

What happened overnight

In China, PMI numbers were released. We continue to see divergence between the NBS survey and the private Caixin survey. According to the NBS survey, the manufacturing industry slowed marginally from 49.2 in January to 49.1 in February, meaning that according to this figure the Chinese manufacturing sector saw slowing activity for the fifth month straight. However, the Caixin survey showed that the manufacturing sector expanded even more than it did in January, from 50.6 to 50.9 in February. The service PMI got a lift from 50.7 in January to 51.4 in February.

In Japan, BoJ governor Ueda said that he thinks it is too early to declare that the 2% inflation target has been met yet. He said that he would await the results of companies' wage negotiations with unions later in March before being able to be say that the goal has been met. Ueda's statement contradicted the statement from BoJ's Takada yesterday, which was hawkish and fuelled speculations over an impending end to negative rates. We believe that this will happen in April.

What happened yesterday

In the US, we got January PCE inflation data. Core inflation (the Fed's preferred measure for underlying inflation) was in line with expectations (+0.4%) but real consumption volumes were on the weaker side (-0.1% m/m) amid a small uptick in savings rate (3.8%; from 3.7%). Following the release, bond yields turned lower, and the broad USD weakened.

We also got jobless claims. The continued claims unexpectedly rose to the highest level since November which sends a signal of a cooling job market as job seekers take longer to find new employment. Initial jobless claims were still moderate at 215,000, which was a little higher than market expectations.

The Fed's Daly said central bank officials are ready to lower interest rates as needed - but emphasized there is no urgent need given the strength of the economy. Bostic reiterated his view that it will probably be appropriate to begin easing policy this summer. Fed's Mester said that PCE inflation data shows that Fed still has work to do, and three rate cuts in 2024 seems about right.

In the euro area we got local inflation data from the euro countries. French inflation was marginally higher than expected. CPI rose to 2.9% y/y in February (cons: 2.8%, prior: 3.1%). In Spain CPI inflation was as expected, but the HICP inflation was marginally higher than expected due to different weighting in the two methods. The monthly increase in seasonally adjusted core inflation was to the high side at 0.33% m/m s.a. German inflation declined in January, but core was unchanged. The monthly change in core inflation was to the high side due to service inflation that increased 0.37% m/m s.a. Hence, both Spain, Germany, and France signal that the most recent underlying momentum in core inflation is to the high side due to services.

ECB's Panetta sounded dovish by saying that inflation is falling faster than expected.

Equities: Global equities rose to a new all-time high yesterday. Cyclicals outperformed as the storm of macro data boosted the "higher-for-longer" environment. Higher-for-longer can both be a demand and an inflation driver, and yesterday it was a bit of both which also meaning the inflation did come in slightly worrisome. Banks, which are in our opinion the biggest winners from the current mix of incoming data did okay yesterday, but we must admit investors prefer growth stocks on days when risk appetite is improving. In US yesterday, Dow +0.1%, S&P 500 +0.5%, Nasdaq +0.9% and Russell 2000 +0.7%. Asian markets are higher this morning with a sharp lift to Japanese equities. European futures have also seen solid gains while US futures are showing more moderate lifts.

FI: A string of strong core inflation prints from Germany, France and Spain drove European yields higher in the first part of yesterday's trading session. However, this trend was offset in the afternoon following the release of weak US consumption figures for January and the slightly higher US claims figures for the past weeks. The German yield curve bull-flattened with 10Y Bund yields down by 5bp throughout the day, while the US Treasury curve was less changed. This highlights the strong impact of US data on long-end EGB yields at present. The Bund ASW-spread continued drifting lower through the session, reaching the lowest level at 35.3 since the summer 2021.

FX: Yesterday's session was characterized by broad USD appreciation in the G10 space except against the JPY. EUR/USD drifted lower towards 1.08. The JPY strengthened yesterday on hawkish remarks from BoJ member Hajime Takata, but this morning, BoJ governor Ueda signalled a more dovish stance, saying that the "stable price target is not yet in sight," sending USD/JPY back above 150.

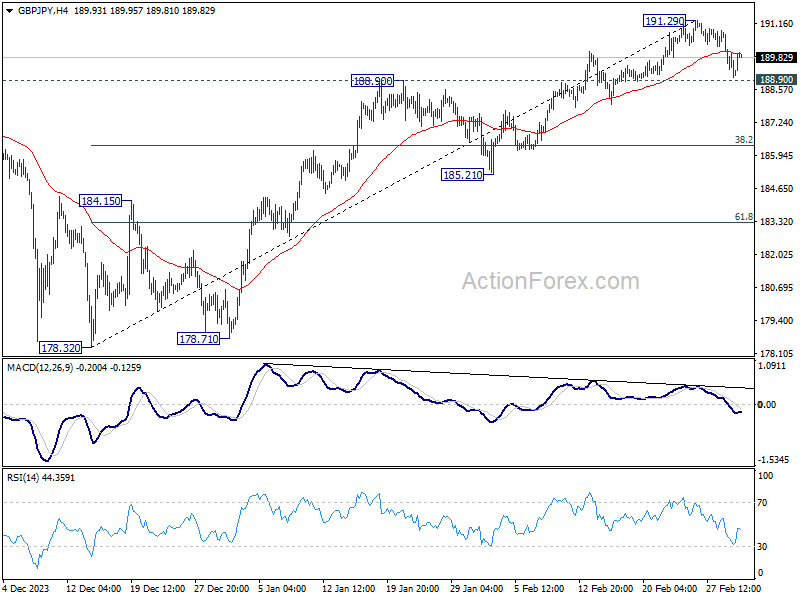

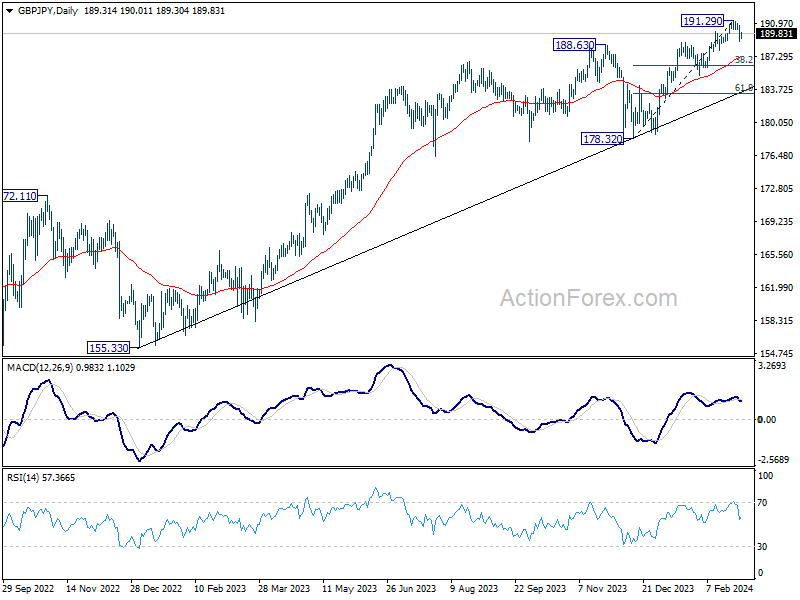

GBP/JPY Daily Outlook

Daily Pivots: (S1) 188.67; (P) 189.75; (R1) 190.44; More....

Risk stays on the downside in GBP/JPY as long as 191.29 short term top holds. Break of 188.90 resistance turned support will extend the decline to 38.2% retracement of 178.32 to 191.29 at 186.33.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

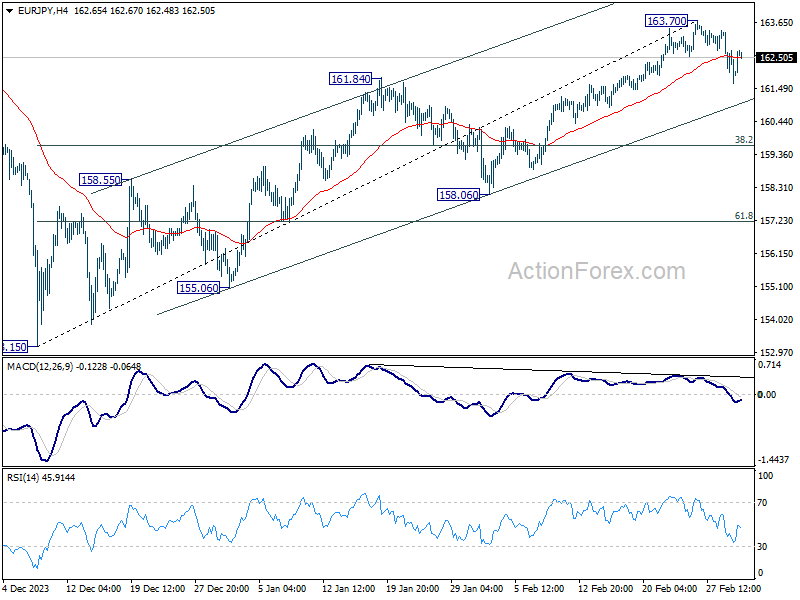

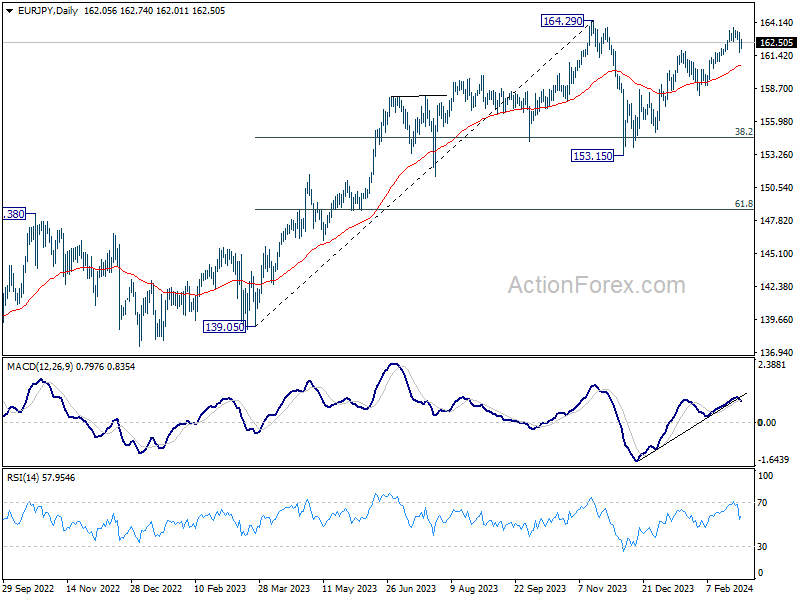

EUR/JPY Daily Outlook

Daily Pivots: (S1) 161.36; (P) 162.40; (R1) 163.11; More...

Risk in EUR/JPY remains on the downside as long as 163.70 short term top holds. Fall from there would extend to channel support (now at 161.06). Firm break there will target 38.2% retracement of 153.15 to 163.70 at 159.66.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 only. As long as 148.38 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage. Next target would be 169.96 (2008 high).

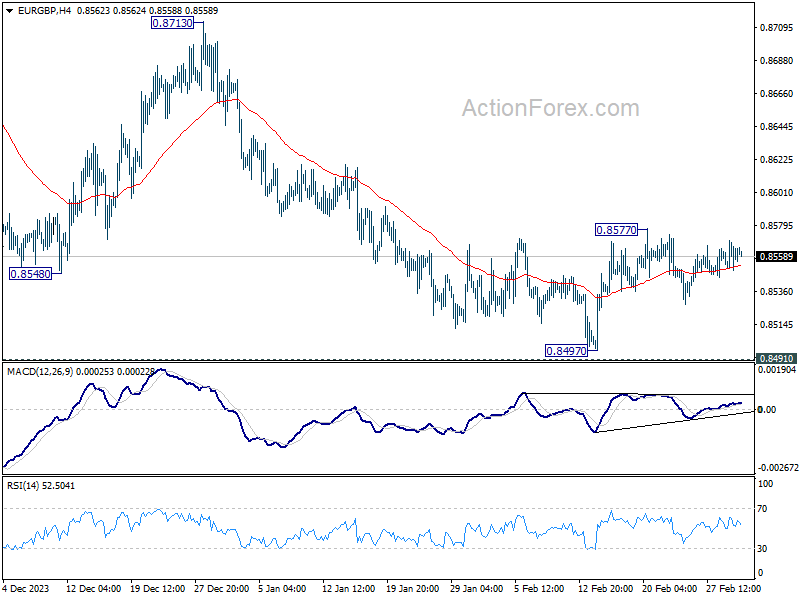

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8550; (P) 0.8560; (R1) 0.8570; More...

Intraday bias in EUR/GBP stays neutral at this point. On the upside, firm break of 0.8577 will resume the rebound from 0.8497. On the downside, decisive break of 0.8491/7 support zone will resume larger down trend.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

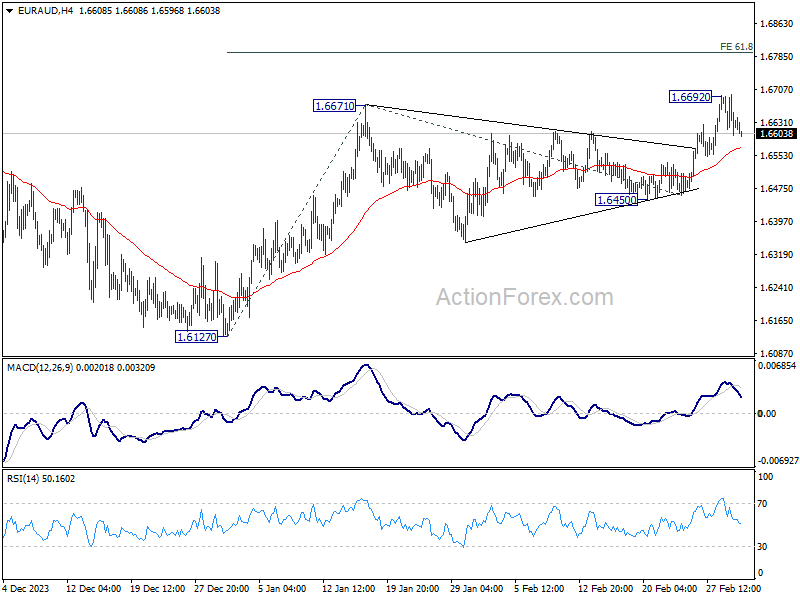

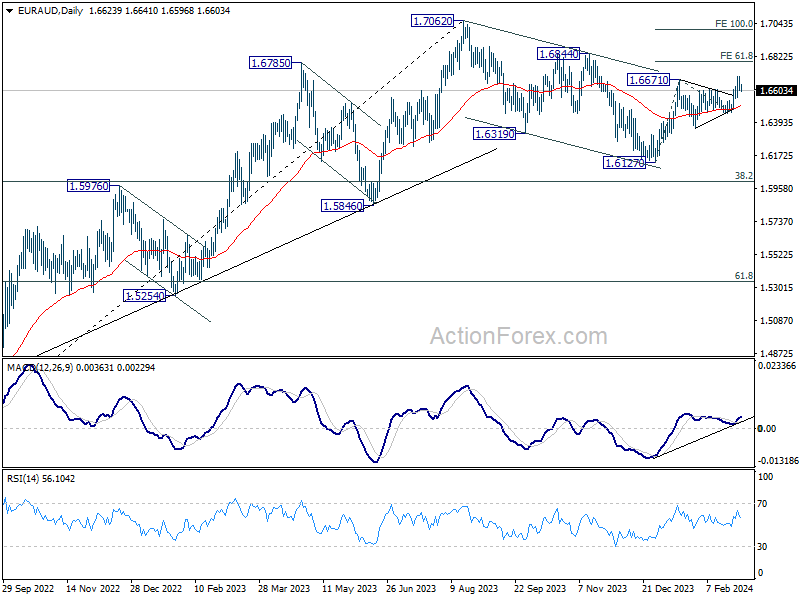

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6589; (P) 1.6644; (R1) 1.6683; More...

Intraday bias in EUR/AUD remains neutral as consolidation continues below 1.6692. Current development suggests that whole correction from 1.7062 should have completed with three waves down to 1.6127. Further rally is expected as long as 1.6450 support holds. Above 1.6692 will target 61.8% projection of 1.6127 to 1.6671 from 1.6450 at 1.6786 next.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

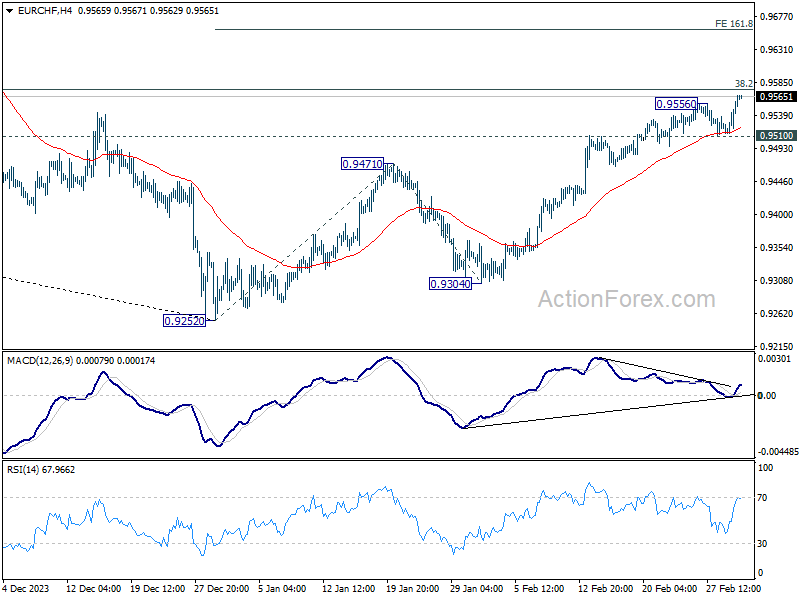

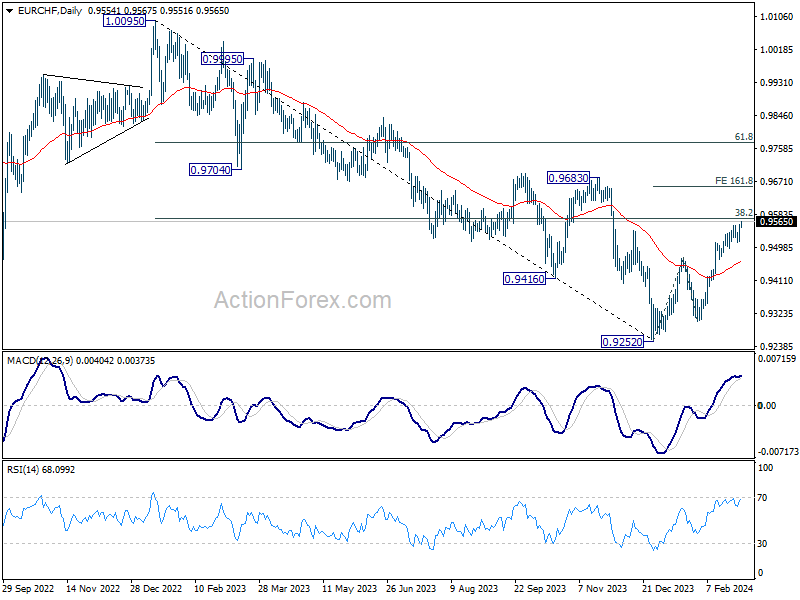

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9529; (P) 0.9545; (R1) 0.9574; More...

EUR/CHF's rally resumed after brief consolidations, and getting support from 4H MACD. Intraday bias is back on the upside for 0.9574 fibonacci resistance. Firm break there will target 161.8% projection of 0.9252 to 0.9471 from 0.9304 at 0.9658 next. On the downside, below 0.9501 support will turn intraday bias neutral first.

In the bigger picture, price actions from 0.9252 are tentatively seen as a correction to the five-wave down trend from 1.0095 (2023 high). Further rise would be seen to 38.2% retracement of 1.0095 to 0.9252 at 0.9574 and possibly above. But overall medium term outlook will remain bearish as long as 0.9683 resistance holds.

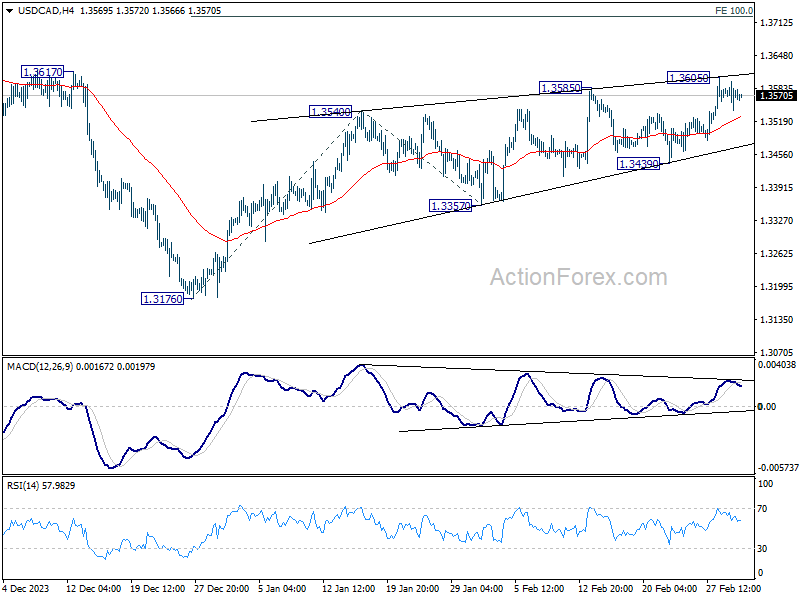

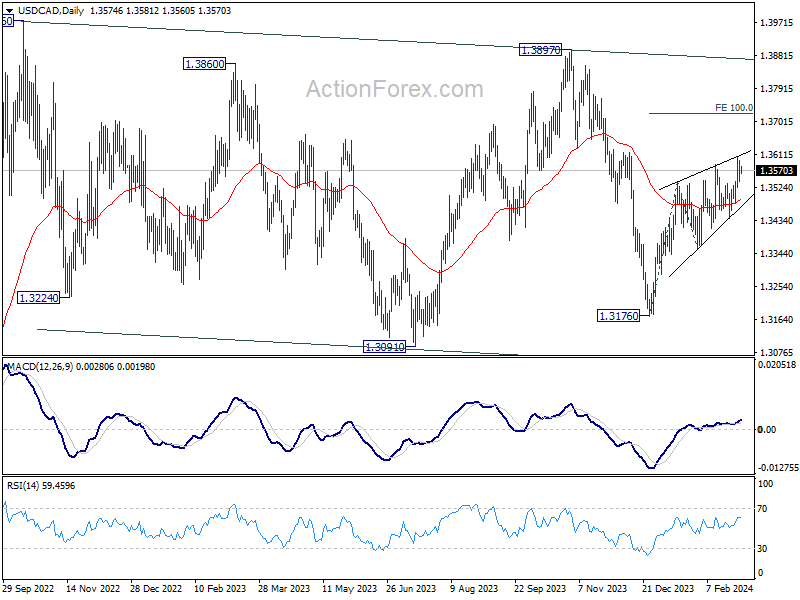

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3548; (P) 1.3573; (R1) 1.3605; More...

Intraday bias in USD/CAD is turned neutral again with current retreat. Near term outlook will stay bullish as long as 1.3439 support holds, and further rally is in favor. Break of 1.3605 will resume the rise from 1.3176 to 100% projection of 1.3176 to 1.3540 from 1.3357 at 1.3721 next.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

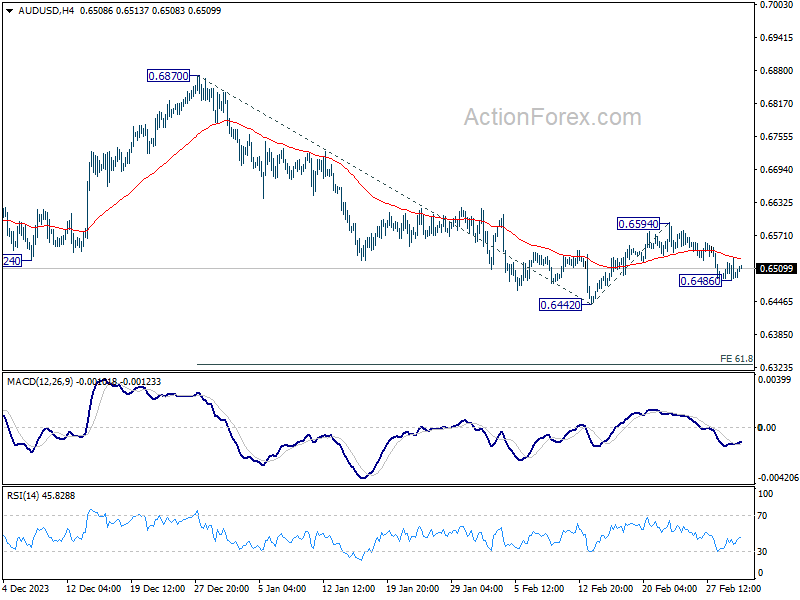

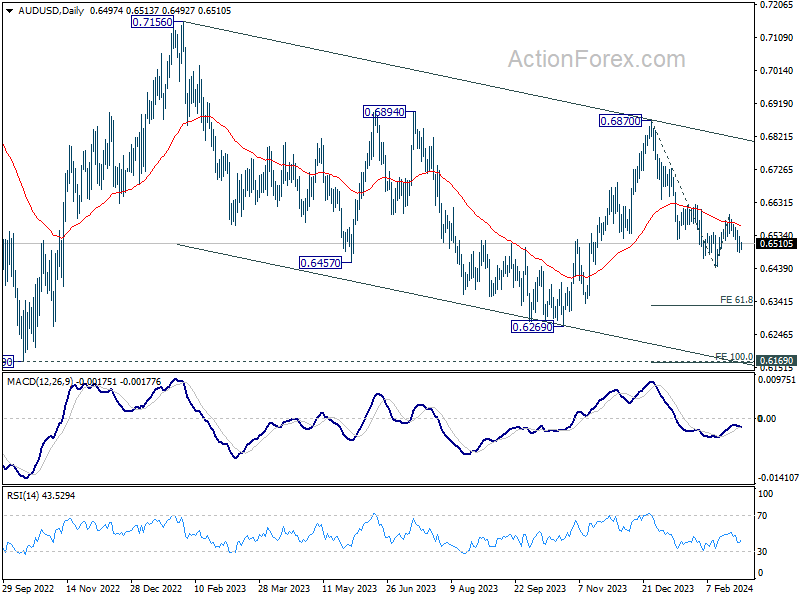

AUD/USD Daily Report

Daily Pivots: (S1) 0.6479; (P) 0.6505; (R1) 0.6523; More...

Intraday bias in AUD/USD is turned neutral with a temporary low formed at 0.6486. Outlook is unchanged that recovery from 0.6442 has completed at 0.6594. Risk will stay on the downside as long as this resistance holds. Below 0.6486 will bring retest of 0.6442 support first. Firm break there will resume whole decline from 0.6870, and target 61.8% projection of 0.6870 to 0.6442 from 0.6594 at 0.6329 next.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which might still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

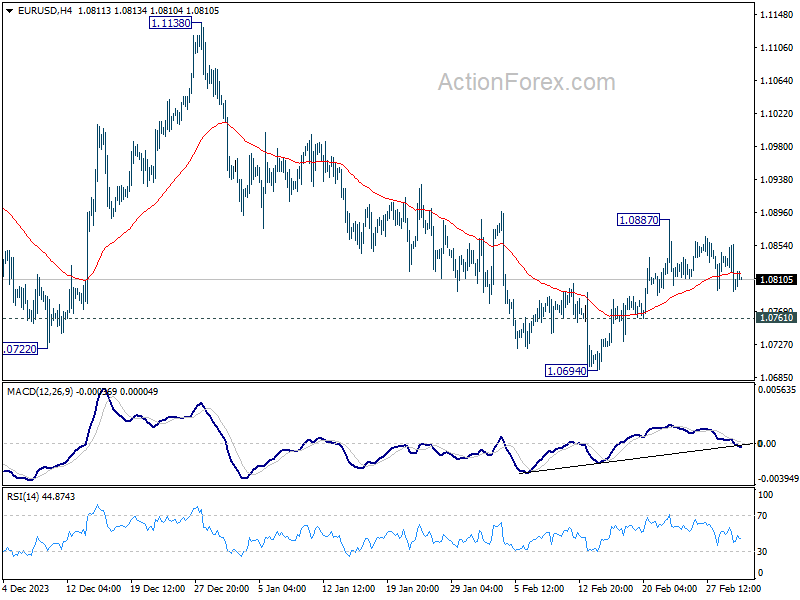

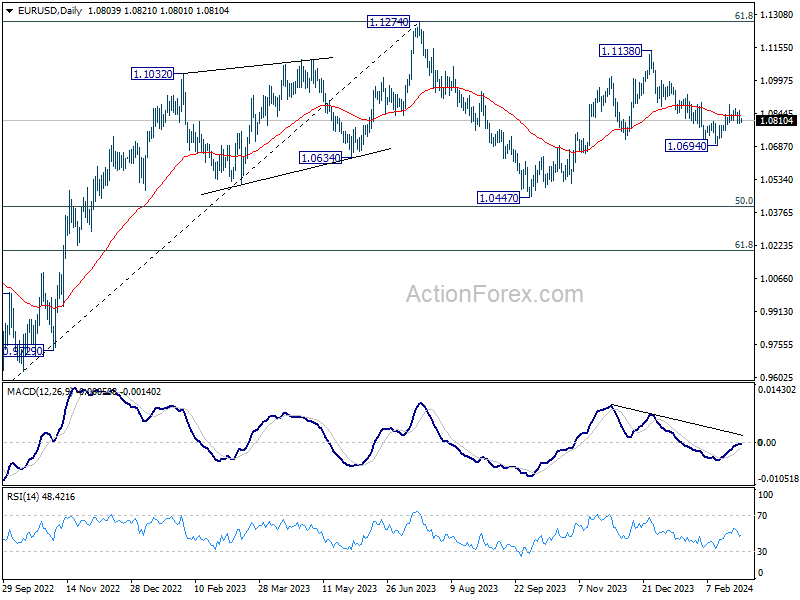

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0782; (P) 1.0819; (R1) 1.0842; More...

Intraday bias in EUR/USD stays neutral as range trading continues. On the upside, break of 1.0887 and sustained trading above 55 D EMA (now at 1.0832) will affirm the case that fall from 1.1138 has completed. Stronger rally would then be seen back to 1.1138. However, break of 1.0761 will turn bias back to the downside for retesting 1.0694 support.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

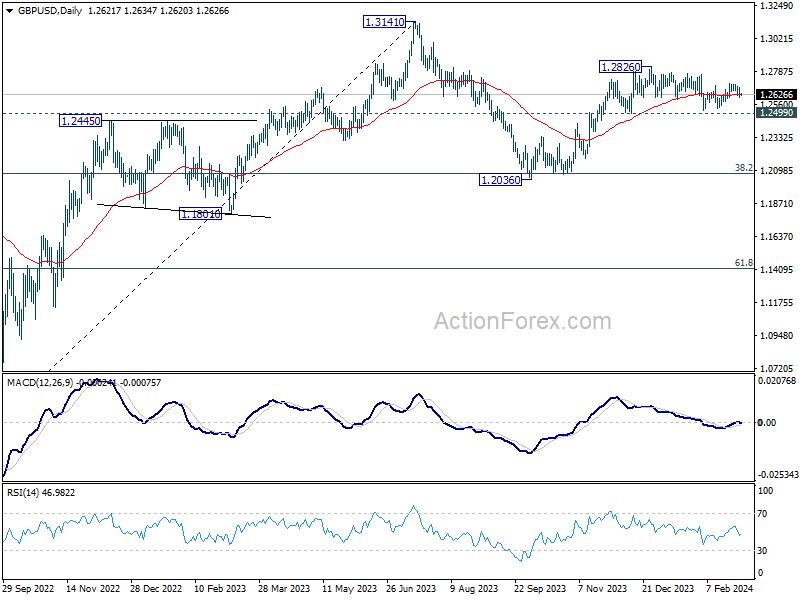

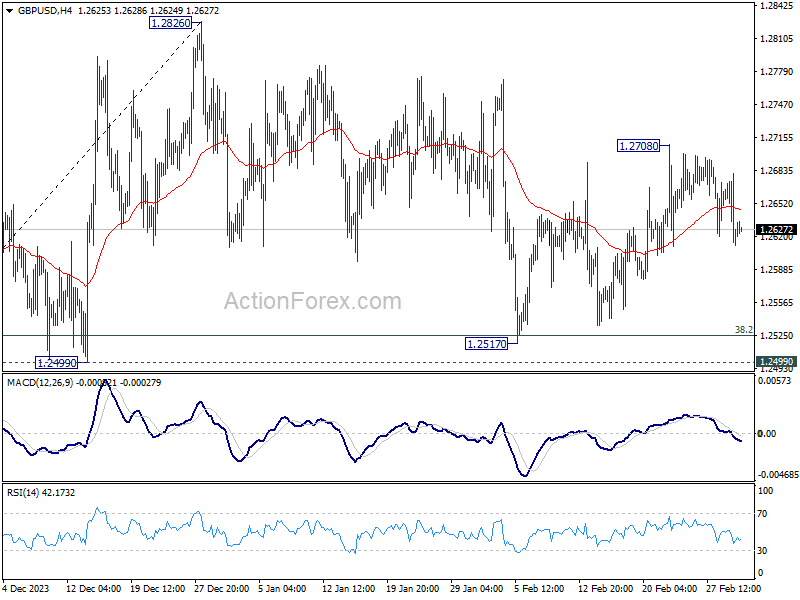

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2598; (P) 1.2640; (R1) 1.2667; More...

Range trading continues in GBP/USD and intraday bias remains neutral. On the upside, break of 1.2708 resistance will indicate that correction from 1.2826 has completed. Intraday bias will be back on the upside for retesting 1.2826. Nevertheless, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which could be still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.