Sample Category Title

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0782; (P) 1.0819; (R1) 1.0842; More...

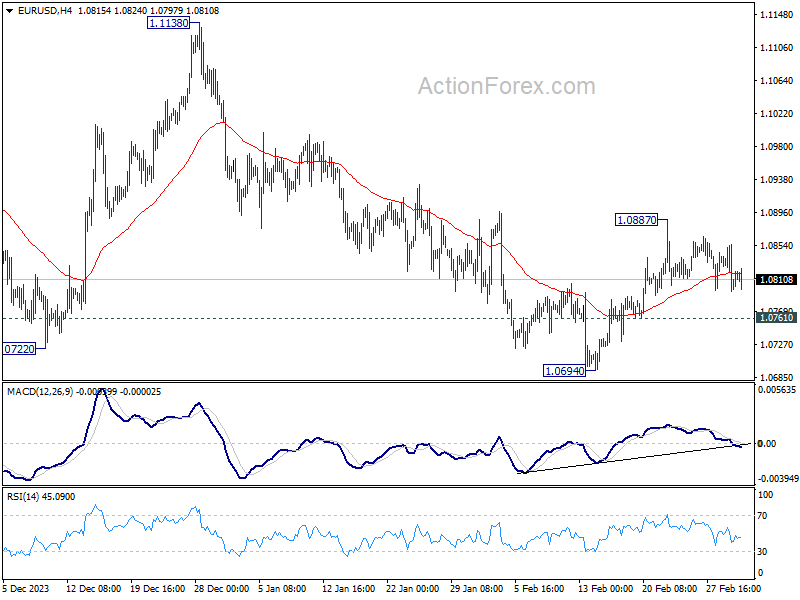

No change in EUR/USD's outlook and intraday bias stays neutral. On the upside, break of 1.0887 and sustained trading above 55 D EMA (now at 1.0832) will affirm the case that fall from 1.1138 has completed. Stronger rally would then be seen back to 1.1138. However, break of 1.0761 will turn bias back to the downside for retesting 1.0694 support.

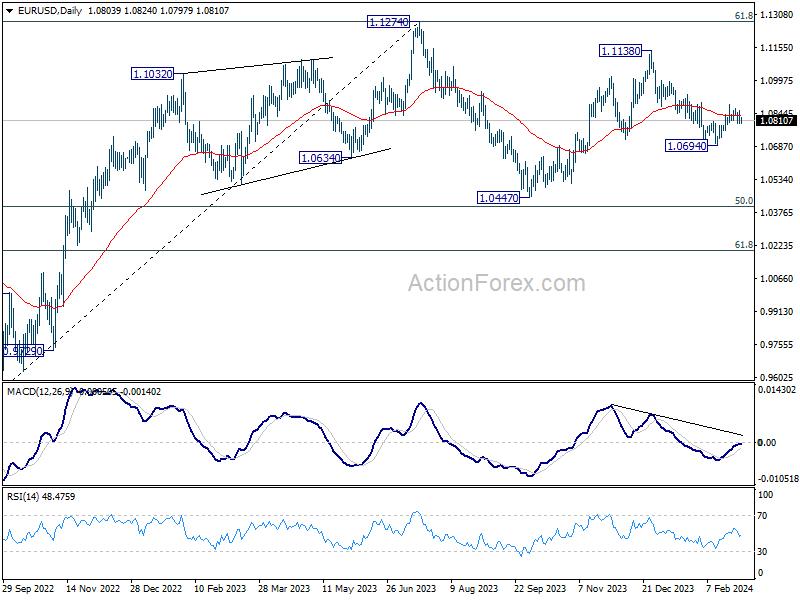

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

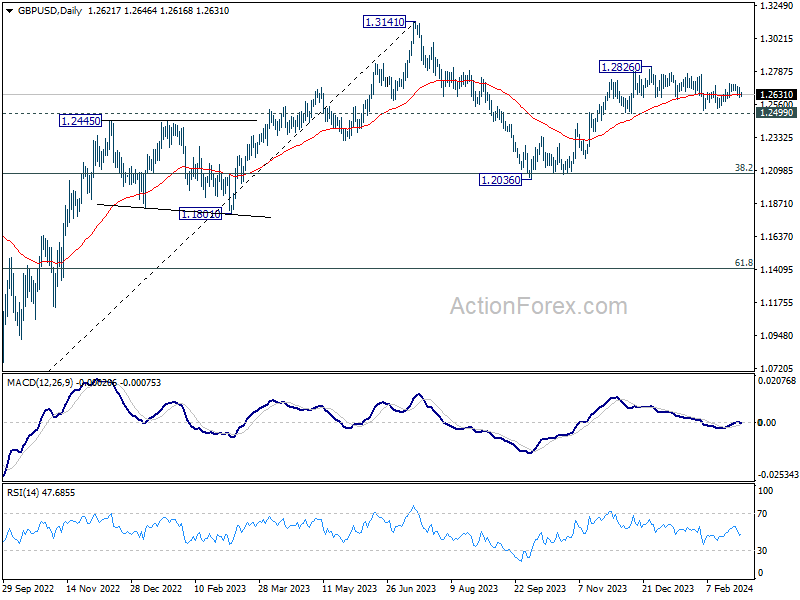

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2598; (P) 1.2640; (R1) 1.2667; More...

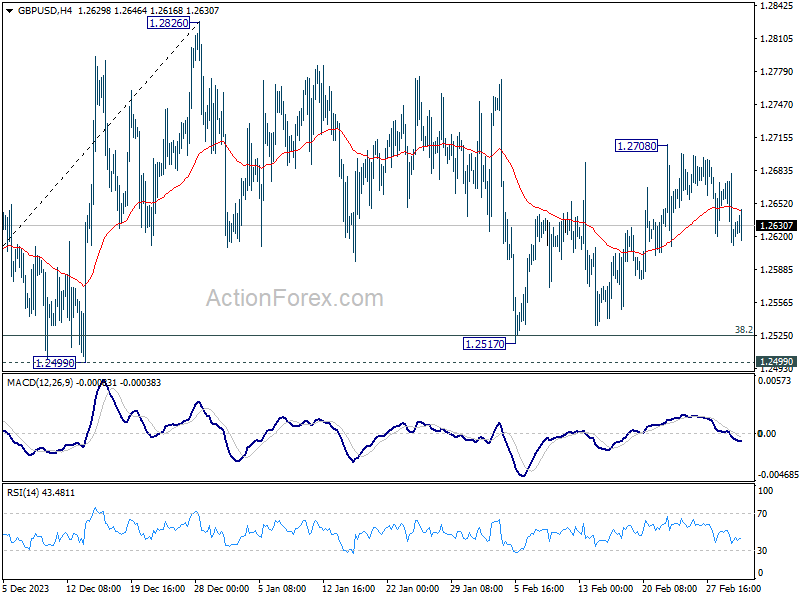

Intraday bias in GBP/USD remains neutral and outlook is unchanged. On the upside, break of 1.2708 resistance will indicate that correction from 1.2826 has completed. Intraday bias will be back on the upside for retesting 1.2826. Nevertheless, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which could be still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

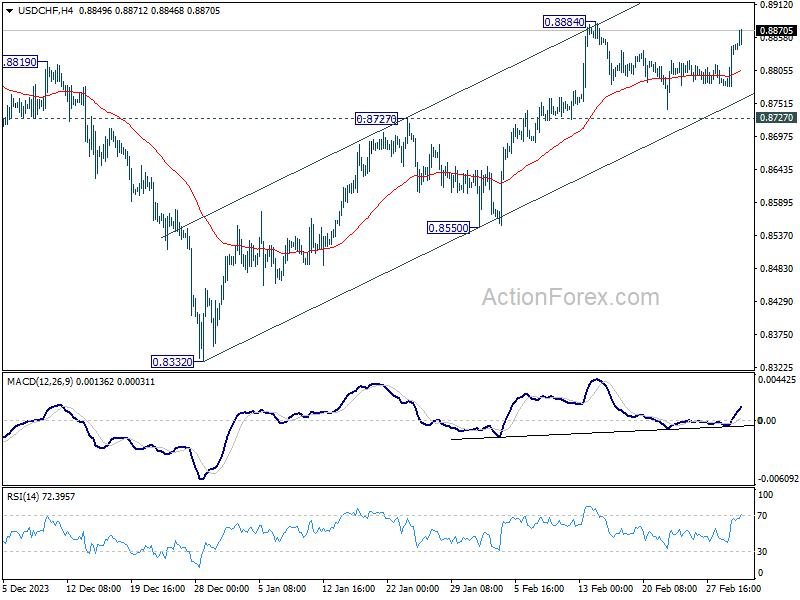

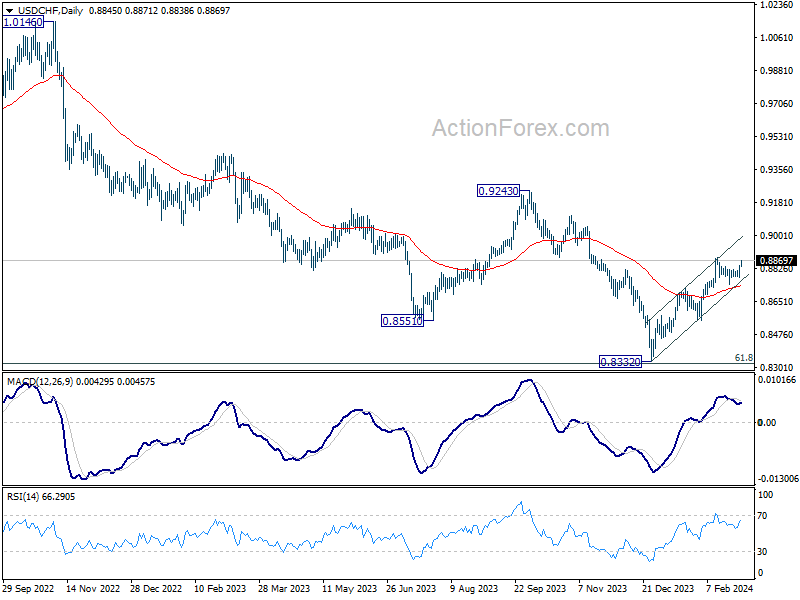

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8802; (P) 0.8825; (R1) 0.8870; More....

Intraday bias in USD/CHF remains neutral at this point. With 0.8727 resistance turned support intact, further rally is expected. On the upside, above 0.8884 will resume the rise from 0.8332 towards 0.9243 resistance. However, sustained break of 0.8727 will dampen this bullish view, and turn bias back to the downside for 0.8550 support instead.

In the bigger picture, a medium term bottom should be formed at 0.8332, on bullish convergence condition in W MACD, just ahead of 0.8317 long term fibonacci support. It's still early to decide if the larger down trend from 1.0146 (2022 high) is reversing. But further rise should be seen to 0.9243 resistance even as a correction.

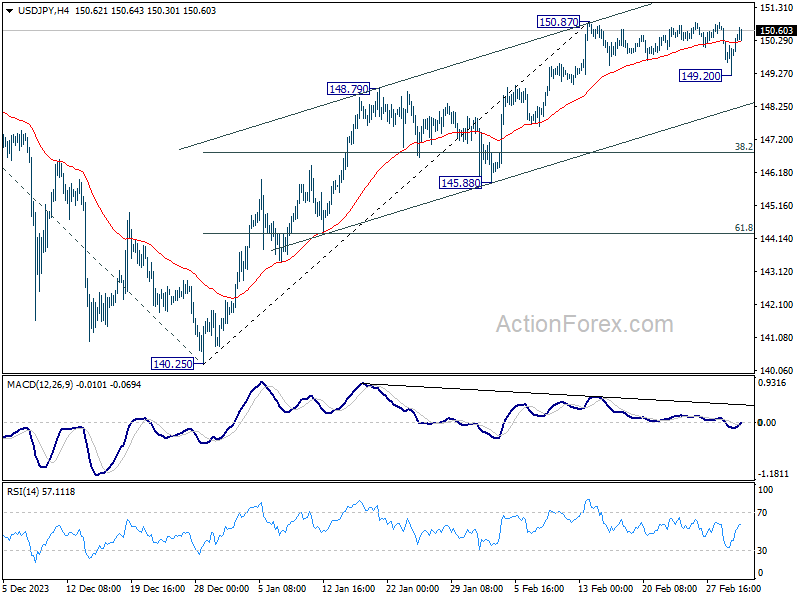

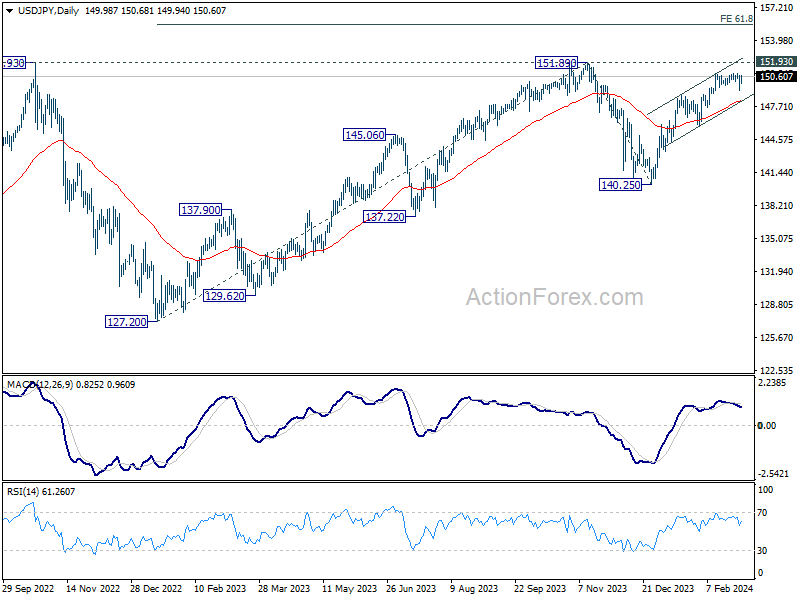

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.24; (P) 149.97; (R1) 150.74; More...

Intraday bias in USD/JPY stays neutral for the moment. On the upside, decisive break of 150.87 will resume whole rally from 140.25 to retest 151.89/93 key resistance zone. On the other hand, considering bearish divergence condition in 4H MACD, firm break of 149.20 will confirm short term topping at 150.87. Deeper fall would be seen to channel support (now at 148.33), even as a corrective move.

In the bigger picture, rise from 140.25 is seen as resuming the trend from 127.20 (2023 low). Decisive break of 151.89/.93 resistance zone will confirm this bullish case and target 61.8% projection of 127.20 to 151.89 from 140.25 at 155.50. However, break of 148.79 resistance turned support will delay this bullish case, and extend the corrective pattern from 151.89 with another falling leg.

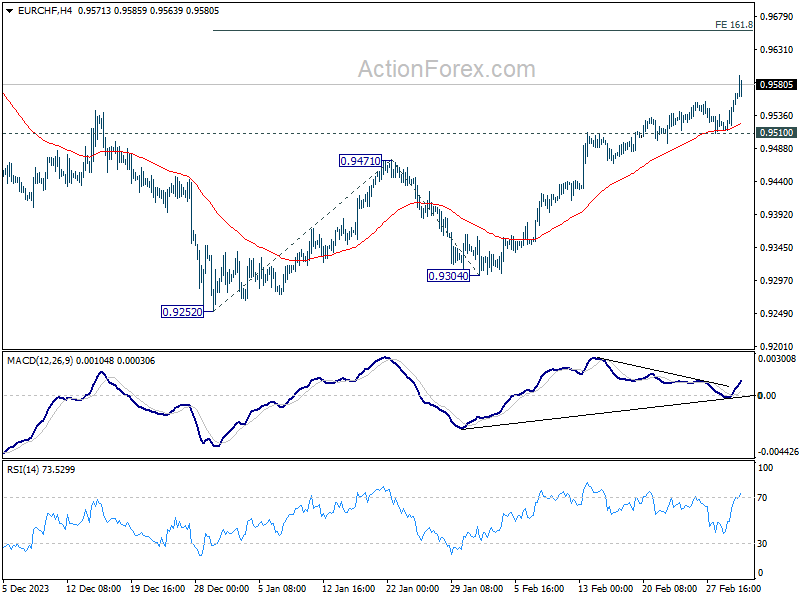

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9529; (P) 0.9545; (R1) 0.9574; More...

EUR/CHF's rally re-accelerates today and breaks through 0.9575 fibonacci resistance. There is no sign of topping yet and intraday bias stays on the upside. Next target will be 161.8% projection of 0.9252 to 0.9471 from 0.9304 at 0.9658 next. For now, further rally is expected as long as 0.9510 support holds, in case of retreat.

In the bigger picture, price actions from 0.9252 are tentatively seen as a correction to the five-wave down trend from 1.0095 (2023 high). 38.2% retracement of 1.0095 to 0.9252 at 0.9574is already met. But overall medium term outlook will remain bearish as long as 0.9683 resistance holds.

Eurozone Inflation Surprises Support Euro, ECB’s Holzmann Urges Patience on Policy

Euro rises broadly today even though gains are so far limited. The common currency is lifted by stronger than anticipated Eurozone inflation figures, which suggests that the path to disinflation may be encountering obstacles. This development could providing ammunition to hawks within the ECB Governing Council, to advocate for a cautious approach towards rate cuts.

Governing Council member Robert Holzmann's remarks underscored this sentiment, emphasizing the need for patience and caution in monetary policy decisions: "we have to wait" and "cannot rush to a decision". Holzmann's timing, however, raises eyebrows as it comes during ECB's quiet period before its upcoming meeting less than a week away.

Overall in the currency markets, Yen and Swiss Franc are trailing as the day's underperformers, with Dollar also softening slightly. Conversely, Australian Dollar the second best just behind Euro, followed by Sterling, while Canadian Dollar is mixed in tandem with the New Zealand Dollar.

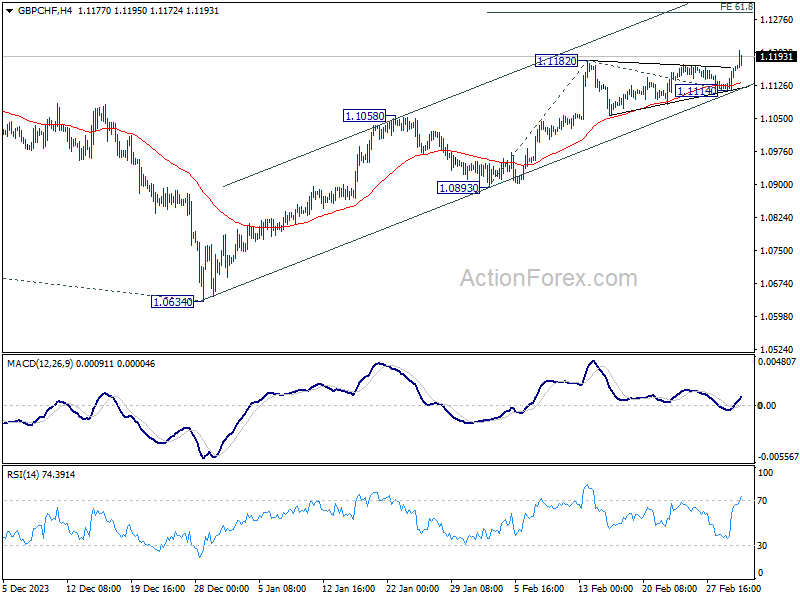

Technically, as a follow up to the Daily Report today, GBP/CHF's break of 1.1182 resistance confirms resumption of whole rise from 1.0634. Next target is 61.8% projection of 1.0893 to 1.1182 from 1.1114 at 1.1293. Now, a focus is on whether USD/CHF could follow by breaking through 0.8884 resistance.

In Europe, at the time of writing, FTSE is up 0.68%. DAX is up 0.51%. CAC is up 0.01%. UK 10-yaer yield is up 0.0285 at 4.250. Germany 10-year yield is up 0.032 at 2.447. Earlier in Asia, Nikkei surged 1.90%. Hong Kong HSI rose 0.47%. China Shanghai SSE rose 0.39%. Singapore Strait Times fell -0.19%. Japan 10-year JGB yield rose 0.0060 to 0.720.

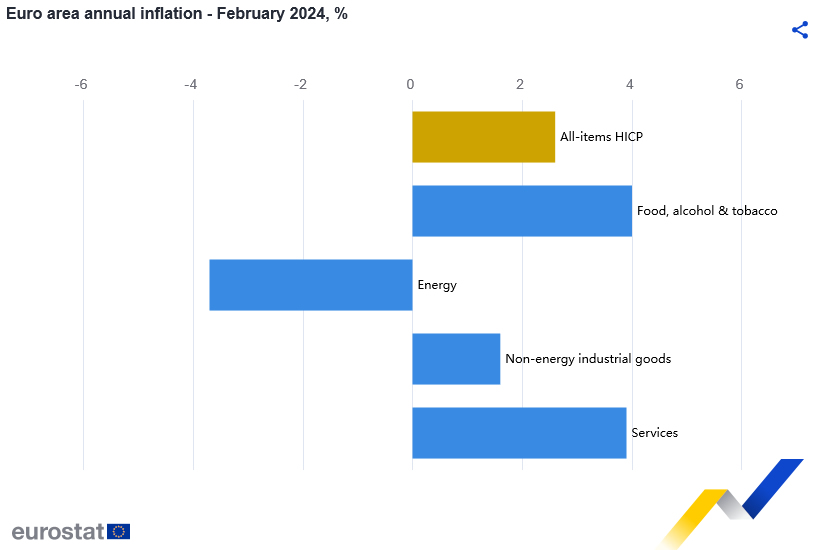

Eurozone CPI slows to 2.6%, core down to 3.1%, both above expectations

Eurozone CPI slowed from 2.8% yoy to 2.6% yoy in February, above expectation of 2.5% yoy. CPI core (ex-energy, food, alcohol & tobacco) slowed from 3.3% yoy to 3.1% yoy, above expectation of 2.9% yoy.

Breaking down the main components, food, alcohol & tobacco is expected to have the highest annual rate in February (4.0%, compared with 5.6% in January), followed by services (3.9%, compared with 4.0% in January), non-energy industrial goods (1.6%, compared with 2.0% in January) and energy (-3.7%, compared with -6.1% in January).

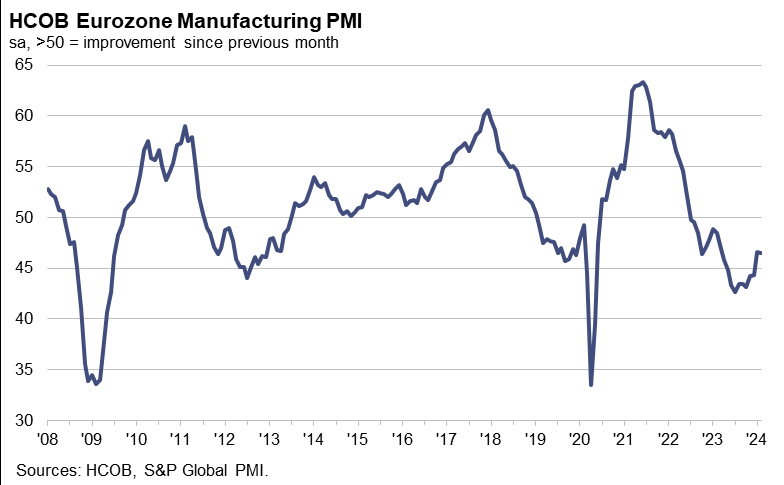

Eurozone PMI manufacturing finalized at 46.5, one-year industrial recession not ending yet

Eurozone PMI Manufacturing was finalized at 46.5 in February, down slightly from January's 46.6.

Greece, Ireland, and Spain notably marked significant highs in their manufacturing PMI, with Greece reaching a 24-month high at 55.7, Ireland a 20-month high at 52.2, and Spain entering growth territory with a 20-month high at 51.5.

These figures contrast starkly with the larger economies within such as Germany and France, where manufacturing activity continued to contract, with Germany hitting a 4-month low at 42.5, and France at 11-month high at 47.1.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, stated the Eurozone's "industrial recession" extends beyond a year without signs of abating. The continued decline in output, particularly in the region's economic powerhouses Germany and France, underscores the persistent challenges facing the manufacturing sector.

Despite the overall contraction, there's a "glimmer of hope" as the pace of decline in new orders across Eurozone has softened. This slight improvement suggests that demand conditions could be stabilizing, potentially laying the groundwork for a gradual recovery in the manufacturing sector.

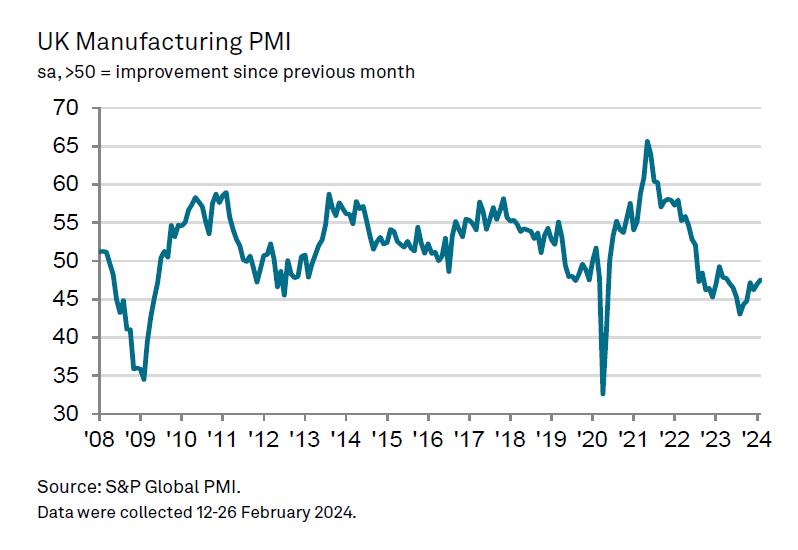

UK PMI manufacturing finalized at 47.5, impacts of Red Sea crisis continue

UK PMI Manufacturing was finalized at 47.5 in February, up from January's 47.0. This marks the highest reading since April 2023, yet the sector has been contracting for 19 consecutive months.

Rob Dobson, Director at S&P Global Market Intelligence, said the impact of the Red Sea crisis was particularly pronounced, causing delays in raw material deliveries, inflating purchase prices, and impairing production capabilities. This crisis also had a knock-on effect on demand, with new export orders suffering due to supply chain disruptions and escalated shipping costs.

The crisis has exerted considerable pressure on both prices and supplies. Input cost inflation reached an 11-month high, necessitating further increases in selling prices, while average supplier lead times extended to the greatest extent since mid-2022.

Dobson suggests that this inflationary pressure may prompt policymakers to reconsider the timing of anticipated interest rate cuts, hinting at the broader economic implications of the manufacturing sector's current challenges.

BoJ's Ueda stays cautious on achieving sustainable inflation

Bank of Japan Governor Kazuo Ueda reiterated that Japan has not yet achieved sustainable 2% inflation. "I don't think we are there yet," he said after G20 finance ministers' meeting.

A significant focus for BoJ in the near term will be the outcome of upcoming annual wage negotiations between companies and unions. Ueda pointed out the importance of these negotiations in determining the potential for a positive wage-inflation cycle in Japan.

"We need to confirm whether a positive wage-inflation cycle would kick off and strengthen," he noted, acknowledging the rising demands from unions for pay increases exceeding last year's and the apparent willingness among many firms to comply.

However, Ueda also stressed the need for a comprehensive review of the collective results of these wage negotiations, alongside other economic data, to gauge whether wages and inflation will sustainably rise in tandem.

Japan's PMI manufacturing finalized at 47.2, worst since Aug 2020

Japan's PMI Manufacturing was finalized at 47.2 in February, down from January's 48.0. This marks the ninth consecutive month of contraction, presenting the most significant downturn since August 2020.

According to S&P Global, the decline was characterized by sharper falls in both output and new orders. Additionally, the sector experienced the most substantial decline in employment seen in over three years, indicating that the downturn is having a tangible impact on workforce. Furthermore, rate of increase in output prices slowed to the lowest level since June 2011, suggesting that price pressures are easing amid weakened demand.

China's NBS PMI manufacturing falls slightly to 49.1, Caixin manufacturing rises to 50.9

China's manufacturing sector continued its contraction for the fifth consecutive month in February, with official NBS PMI decreasing slightly from 49.2 to 49.1, matched expectations.

New orders subindex remained steady at 49, indicating stagnant demand. New export orders fell further from 47.2 to 46.3, reflecting ongoing pressures on the export front.

NBS PMI Non-Manufacturing rose from 50.7 to 51.4 , surpassing the anticipated 50.8. PMI Composite remained unchanged at 50.9.

In parallel, Caixin PMI Manufacturing, which focuses more on small and medium-sized enterprises, edged up from 50.8 to 50.9 , slightly above expectations of 50.7.

Caixin noted sustained increase in output and new orders, with firms expressing improved business optimism for the second consecutive month. Additionally, input cost inflation declined to a seven-month low, while selling prices fell.

RBNZ's Orr: Restrictive policy to stay, expects normalization next year

RBNZ Governor Adrian Orr affirmed today that the economy is "evolving as anticipated", with inflation expectations declined. However, he reiterated inflation "is still too high".

The governor emphasized the necessity of maintaining a restrictive monetary policy stance "for some time." He added that he expects to "begin normalizing policy in 2025."

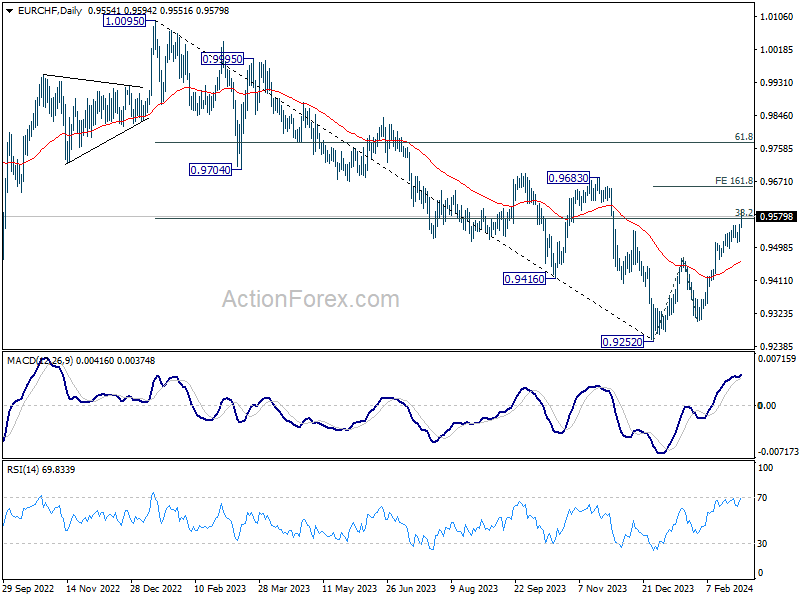

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9529; (P) 0.9545; (R1) 0.9574; More...

EUR/CHF's rally re-accelerates today and breaks through 0.9575 fibonacci resistance. There is no sign of topping yet and intraday bias stays on the upside. Next target will be 161.8% projection of 0.9252 to 0.9471 from 0.9304 at 0.9658 next. For now, further rally is expected as long as 0.9510 support holds, in case of retreat.

In the bigger picture, price actions from 0.9252 are tentatively seen as a correction to the five-wave down trend from 1.0095 (2023 high). 38.2% retracement of 1.0095 to 0.9252 at 0.9574is already met. But overall medium term outlook will remain bearish as long as 0.9683 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Jan | -8.80% | 3.70% | 3.60% | |

| 23:30 | JPY | Unemployment Rate Jan | 2.40% | 2.40% | 2.40% | |

| 00:30 | JPY | Manufacturing PMI Feb F | 47.2 | 47.2 | 47.2 | |

| 01:00 | CNY | NBS Manufacturing PMI Feb | 49.1 | 49.1 | 49.2 | |

| 01:00 | CNY | NBS Non-Manufacturing PMI Feb | 51.4 | 50.8 | 50.7 | |

| 01:45 | CNY | Caixin Manufacturing PMI Feb | 50.9 | 50.7 | 50.8 | |

| 05:00 | JPY | Consumer Confidence Index Feb | 39.1 | 38.4 | 38 | |

| 07:30 | CHF | Real Retail Sales Y/Y Jan | 0.30% | 0.40% | -0.80% | -0.10% |

| 08:30 | CHF | Manufacturing PMI Feb | 44 | 44.6 | 43.1 | |

| 08:45 | EUR | Italy Manufacturing PMI Feb | 48.7 | 49.5 | 48.5 | |

| 08:50 | EUR | France Manufacturing PMI Feb F | 47.1 | 46.8 | 46.8 | |

| 08:55 | EUR | Germany Manufacturing PMI Feb F | 42.5 | 42.3 | 42.3 | |

| 09:00 | EUR | Italy Unemployment Jan | 7.20% | 7.20% | 7.20% | |

| 09:00 | EUR | Eurozone Manufacturing PMI Feb F | 46.5 | 46.1 | 46.1 | |

| 09:30 | GBP | Manufacturing PMI Feb F | 47.5 | 47.1 | 47.1 | |

| 10:00 | EUR | Eurozone Unemployment Rate Jan | 6.40% | 6.40% | 6.40% | |

| 10:00 | EUR | CPI Y/Y Feb P | 2.60% | 2.50% | 2.80% | |

| 10:00 | EUR | CPI Core Y/Y Feb P | 3.10% | 2.90% | 3.30% | |

| 14:30 | CAD | Manufacturing PMI Feb | 48.3 | |||

| 14:45 | USD | Manufacturing PMI Feb F | 51.5 | 51.5 | ||

| 15:00 | USD | ISM Manufacturing PMI Feb | 49.5 | 49.1 | ||

| 15:00 | USD | ISM Manufacturing Prices Paid Feb | 52 | 52.9 | ||

| 15:00 | USD | ISM Manufacturing Employment Index Feb | 47.1 | |||

| 15:00 | USD | Construction Spending M/M Jan | 0.10% | 0.90% | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Feb F | 79.6 | 79.6 |

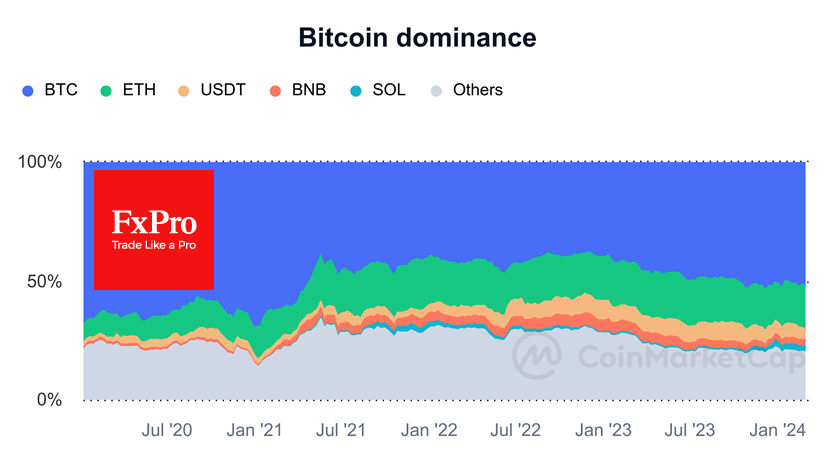

Time to Take a Closer Look at Altcoins?

Market picture

The cryptocurrency market has corrected by 2%, dropping below $2.3 trillion in market capitalisation. Now, this looks like a technical correction, with the biggest coins pulling back from Thursday night’s highs and holding their positions at the start of Friday’s trading. Bitcoin and Ether are drawing their seventh consecutive daily growth candle, albeit at a distance from the previous two days’ highs.

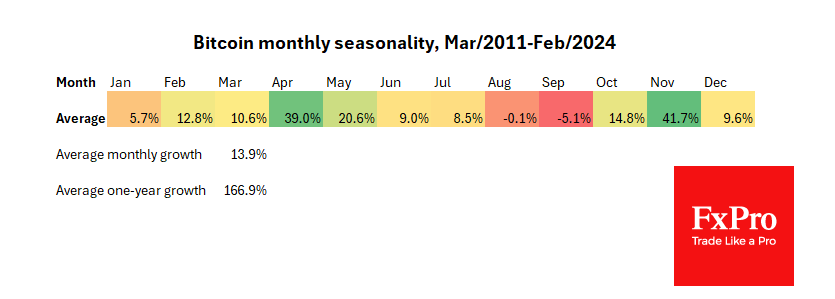

Bitcoin rose 44.7% in February, the strongest monthly gain since December 2020. This coming March is not considered favourable from a seasonal perspective.

Over the past 13 years, bitcoin has ended March with eight declines and only five gains. The average decline was 15%, while the average gain was 17.5%.

Altcoins such as Uniswap and Theta have gained around 90% in the last 30 days, including +50% in the last seven days. The same can be said for Dogecoin, which has added around 50% over the month and 42% over the last seven days.

Is this the season for altcoins? We doubt it, given that the first cryptocurrency still accounts for over 50% of total market capitalisation and that this figure has been rising since the beginning of 2023.

News background

According to data from Bloomberg and BitMEX Research, net daily inflows into bitcoin ETFs reached a record $673 million, of which $612.1 million came from BlackRock’s IBITs. The previous high of $655.2 billion was set on the instrument’s first day of trading on 11 January.

ETF demand for bitcoin (2,800 BTC per day) is three times greater than its mining (900), according to CoinShares. The resulting demand shock contributed to a further decline in bitcoin balances on centralised exchanges.

The Coinbase exchange suffered a technical failure due to the frenzy of demand for cryptocurrencies. The problem occurred amid a “huge” influx of users.

The Gemini exchange will pay a $37m fine for “serious compliance violations” and refund $1.1bn to users of its Earn staking programme as part of a settlement with the New York State Department of Financial Services.

Two top Binance executives were arrested in Nigeria as the country cracks down on cryptocurrency exchanges.

El Salvador’s unrealised profit from bitcoin investments was 40%, or about $41.6 million, according to the country’s president, Nayib Bukele. The country’s leaders do not yet intend to sell the coins.

Eurozone CPI slows to 2.6%, core down to 3.1%, both above expectations

Eurozone CPI slowed from 2.8% yoy to 2.6% yoy in February, above expectation of 2.5% yoy. CPI core (ex-energy, food, alcohol & tobacco) slowed from 3.3% yoy to 3.1% yoy, above expectation of 2.9% yoy.

Breaking down the main components, food, alcohol & tobacco is expected to have the highest annual rate in February (4.0%, compared with 5.6% in January), followed by services (3.9%, compared with 4.0% in January), non-energy industrial goods (1.6%, compared with 2.0% in January) and energy (-3.7%, compared with -6.1% in January).

UK PMI manufacturing finalized at 47.5, impacts of Red Sea crisis continue

UK PMI Manufacturing was finalized at 47.5 in February, up from January's 47.0. This marks the highest reading since April 2023, yet the sector has been contracting for 19 consecutive months.

Rob Dobson, Director at S&P Global Market Intelligence, said the impact of the Red Sea crisis was particularly pronounced, causing delays in raw material deliveries, inflating purchase prices, and impairing production capabilities. This crisis also had a knock-on effect on demand, with new export orders suffering due to supply chain disruptions and escalated shipping costs.

The crisis has exerted considerable pressure on both prices and supplies. Input cost inflation reached an 11-month high, necessitating further increases in selling prices, while average supplier lead times extended to the greatest extent since mid-2022.

Dobson suggests that this inflationary pressure may prompt policymakers to reconsider the timing of anticipated interest rate cuts, hinting at the broader economic implications of the manufacturing sector's current challenges.

Eurozone PMI manufacturing finalized at 46.5, one-year industrial recession not ending yet

Eurozone PMI Manufacturing was finalized at 46.5 in February, down slightly from January's 46.6.

Greece, Ireland, and Spain notably marked significant highs in their manufacturing PMI, with Greece reaching a 24-month high at 55.7, Ireland a 20-month high at 52.2, and Spain entering growth territory with a 20-month high at 51.5.

These figures contrast starkly with the larger economies within such as Germany and France, where manufacturing activity continued to contract, with Germany hitting a 4-month low at 42.5, and France at 11-month high at 47.1.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, stated the Eurozone's "industrial recession" extends beyond a year without signs of abating. The continued decline in output, particularly in the region's economic powerhouses Germany and France, underscores the persistent challenges facing the manufacturing sector.

Despite the overall contraction, there's a "glimmer of hope" as the pace of decline in new orders across Eurozone has softened. This slight improvement suggests that demand conditions could be stabilizing, potentially laying the groundwork for a gradual recovery in the manufacturing sector.