Sample Category Title

The Weekly Bottom Line: Slow Your Roll

U.S. Highlights

- Minutes from the January 30th-31st FOMC underscored that policymakers are adopting a cautious approach on when to pivot to policy easing.

- A number of Fed Governors spoke this week, and all urged patience on rate cuts, particularly in light of the uptick in inflationary pressures in January.

- Market pricing is now positioned for the first cut to come in June (previously May) with 100 bps of easing by year-end – closely aligning to TDE’s forecast.

Canadian Highlights

- Canadian inflation for the month of January surprised to the downside and is now back in the Bank of Canada’s (BoC) 1–3% target range. Core inflation metrics also moved lower, a welcome development for the BoC.

- The BoC might shift marginally to a more dovish tone at the March 6th policy meeting, but the overall narrative remains intact: inflation is still too high, and more evidence is needed that it is moving durably towards 2%.

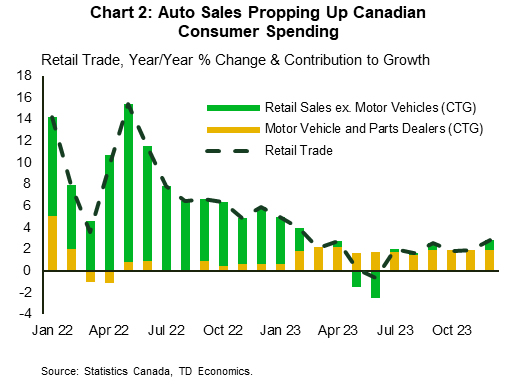

- Canadian retail sales capped off the year with a solid reading in December. Aside from still-robust spending on autos, other areas of consumer spending are weakening. This trend is expected to persist in the first half of this year.

U.S. – Slow Your Roll

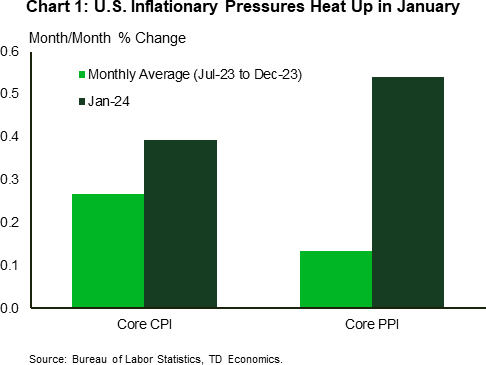

Slow your roll. That was the messaging communicated in the Federal Reserve’s meeting minutes released earlier this week. In hindsight, Fed officials had every reason to remain cautious in timing the pivot to policy easing. Since the January 30th-31st FOMC meeting, the economic data has done little to instill further confidence that inflationary pressures will continue to recede over the coming months. Not only did the January employment report come in more than double expectations, but a few inflation indicators (including CPI, PPI, and ISM price sub-indices) all came in much hotter-than-expected in January (Chart 1).

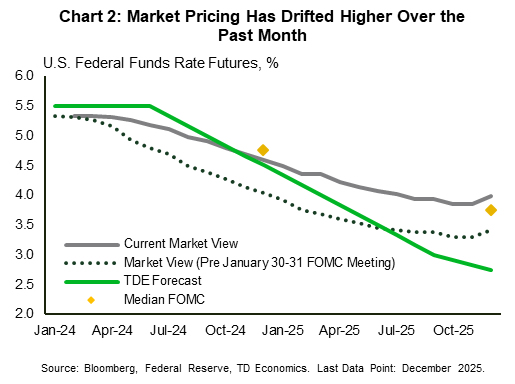

Market pricing has adjusted accordingly in recent weeks, with investors now positioned for a June rate cut and 100 basis points (bps) of policy easing by year-end – a trajectory that more closely aligns to both the FOMC’s and our own forecast (Chart 2).

While Fed officials acknowledged that inflation and employment risks are coming back into better balance, the minutes revealed that most participants remain concerned about the risk of “moving too quickly to ease the stance of policy”. Moreover, some officials cited the risk that stronger aggregate demand or a slow-down in the supply-side recovery could impede further progress on the inflation front. All of this argues for a more agile, data dependent approach to reducing the policy rate.

This is especially true given the recent growth dynamics. Economic growth remained incredibly resilient through the second half of last year – averaging an impressive 4% (annualized) or more than double its long-run potential. While first-quarter momentum looks to have lost a step, it’s still tracking a relatively robust 2-2.5%. As highlighted in our Quarterly Q&A publication released earlier this week, our current forecast assumes economic momentum will continue to soften as the year progresses. However, this is largely predicated on a further cooling in the labor market, resulting in slower income growth and weaker consumer spending. Should the labor market prove more resilient, then there’s an obvious upside risk to both spending and near-term inflation dynamics.

Next week we’ll get a pulse check on consumer spending and income trends for January. Accompanying the release will be the core PCE inflation data, which is likely to show an increase of 0.4% month-on-month – the strongest monthly gain in a year. It remains to be seen if January’s acceleration is a one-off, perhaps influenced by businesses increasing prices at the start of the year in a way that may not be fully captured by seasonal adjustment factors, or whether it’s the beginning of something more insidious. Either way, the recent uptick in inflationary pressures serves as a reminder that the descent back to 2% will likely come with some turbulence.

This is exactly why Fed Governors have been preaching patience over the past few weeks. Perhaps no one said it better than Christopher Waller, who noted “the strength of economy and the recent data on inflation mean it is appropriate to be patient, careful, methodical, deliberate – pick your favorite synonym”. “Whatever word you pick, they all translate to one idea: What’s the rush?”.

Canada – Good News on the Inflation Front

If the new year's resolution for Canadian inflation was to retreat back into the Bank of Canada's (BoC) 1–3% target range, then January's CPI update is a good start. Prices in January dipped to 2.9% year-on-year (y/y) and are now sporting a two-handle for the first time since June 2023. This is a welcome development for Canadian consumers waiting for interest rate relief, but like all new-year goals, success will be judged on how well inflation sticks to the script. Markets took the news as a sign the BoC might be inching closer to their first interest rate cut, adding slightly more probability to a move before the summer. The 2 and 10-year Canadian yields both slipped by around 8 bps on the week, while the Canadian dollar stayed roughly flat.

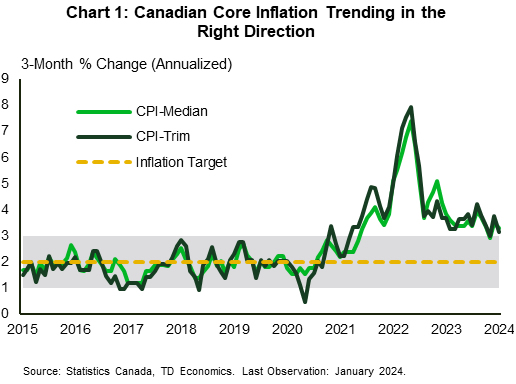

The details of January's CPI report were encouraging. Gasoline prices were key in guiding inflation lower, while decelerating food, travel services, and clothing and footwear inflation also made meaningful contributions to the drop in the headline figure. More importantly, CPI-trim and CPI-median edged lower in January, and despite some head fakes in recent months, both measures are trending in the right direction (Chart 1). However, as has been a theme for many months, the shelter component of CPI, currently running above 6% y/y, continues to be the single biggest factor in preventing the BoC from achieving price stability.

It is still important to zoom out and avoid putting too much emphasis on one data point. Recall that just one month ago, an upside inflation surprise led to a volatile market reaction in the other direction. In the months leading up to the CPI release, markets and forecasters were flip-flopping between the first BoC interest rate cut occurring in either in April or June. As we near the BoC's March 6th interest rate announcement, current inflation trends and the surprising strength in the Canadian economy to end the year have markets leaning towards the latter, in line with our view.

Will this report change the Bank of Canada's tone? Probably slightly. They will likely acknowledge that progress is being made in returning inflation back to target. But the narrative remains intact, inflation remains too high to start cutting rates now, and the Bank will need more evidence that inflation is durably moving towards 2%.

A healthy gain in December retail sales was consistent with the better consumer spending momentum we had seen in the fourth quarter. While auto sales did lots of the heavy lifting in December retail trade, core sales also moved higher and were led by general merchandise stores, food and beverage stores and miscellaneous retailers. Over the past several months, auto sales have driven the majority of the y/y gains in retail trade, while spending across other major components has slowed (Chart 2). The advance reading for January sales also points to momentum fizzling in the new year, consistent with our own view.

Looking ahead to next week's GDP release, we anticipate Canada's economy will return to modest growth in the fourth quarter, after contracting in the third quarter, supported by a solid showing in consumer spending.

Weekly Economic & Financial Commentary: Why Put Off Until Tomorrow What Can Be Put Off Until the Next Day?

Summary

United States: Stowin' Away the Time

- The economic calendar was quiet the past few days, so market participants continued to digest last week's slew of data. Stronger-than-expected inflation, underpinned by the mildly hawkish minutes from the January FOMC meeting, drove a move higher in mortgage rates. We currently forecast the first rate cut to take place in May, but the timing of that cut is at risk of slipping further into the summer.

- Next week: New Home Sales (Mon.), Durable Goods (Tue.), Personal Income (Thu.)

International: European February PMIs Show Modestly Firmer Growth, Persisting Price Pressures

- European February PMI surveys were mildly encouraging: The Eurozone services PMI rose more than expected, and the U.K. services PMI remained steady and comfortably in growth territory. Those same surveys showed persisting cost and price pressures across Europe. The reports increase the risk that the European Central Bank will wait until June (rather than April) to cut interest rates, while we expect the Bank of England to start lowering interest rates in June as well.

- Next week: Canada GDP (Thu.), China PMIs (Fri.), Eurozone CPI (Fri.)

Interest Rate Watch: Why Put Off Until Tomorrow What Can Be Put Off Until the Next Day?

- In the seven months since the Fed’s last rate hike in July, Chair Powell has cautioned the best policy prescription might be to keep rates higher for longer and that any policy decision would be dependent upon the data. Financial markets have not always taken that at face value. We unpack how the expected timing of cuts has changed.

Topic of the Week: Personal Food Expenditure: Eating Out Taking a Bigger Bite of What's Coming In

- Consumer outlays on food as a share of disposable personal income have shifted higher over the past two years. Digging down, consumer spending on eating out as a share of income has come back with a vengeance from its brief decline during the pandemic, and it has been the biggest driver of food taking a bigger bite out of consumers’ wallets.

Forward Guidance: Q4 GDP Likely Edged Higher But Not Enough to Prevent Sixth Per-Capita Decline

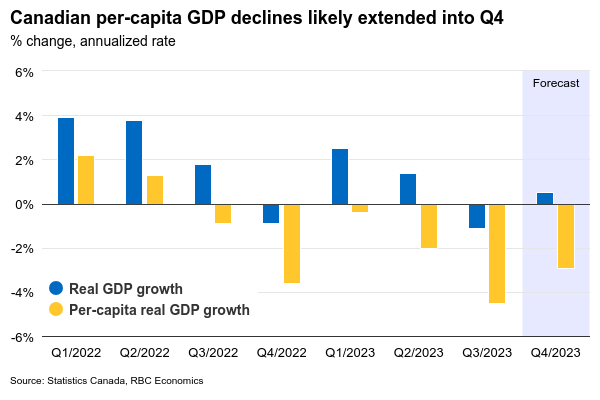

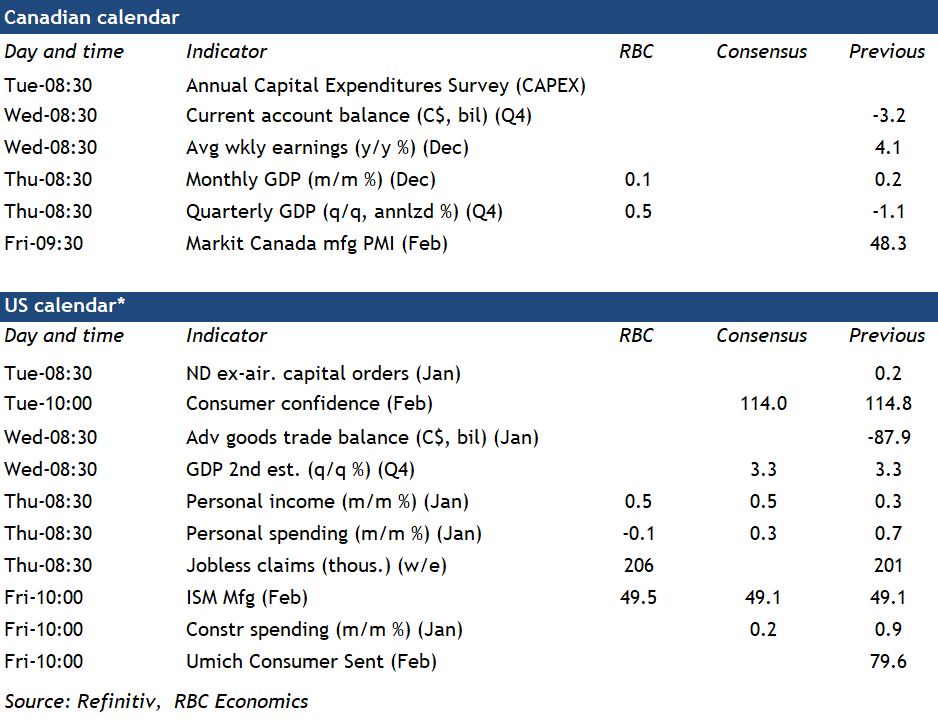

Canadian Q4 and December GDP growth numbers will be in focus for the Bank of Canada after a busy week where inflation numbers for January broadly surprised to the downside.

We expect Q4 GDP growth to remain in positive territory with a small annualized increase of 0.5%. That will prevent the economy from seeing two consecutive quarters of contraction, which is often used as the definition of a “technical” recession. But when measured against the country’s rapid population growth, it’s the sixth straight quarterly decline on a per-capita basis, alongside a rising unemployment rate.

Consumer spending bounced back in Q4—retail sale volumes jumped at an annualized rate of 5.3%. But business spending appears to have softened with lower imports of equipment and declining construction activity. While employment continued to rise in the quarter, actual hours worked declined outright for the first time since the initial pandemic lockdowns in Q2 2020.

On a monthly basis, we expect GDP edged up 0.1% in December, building on the 0.2% increase in November but below the 0.3% preliminary estimate from Statistics Canada a month ago, which is highly prone to revision. Oil and gas extraction activity jumped higher in December, and retail sales volumes rose 0.8% from November. But manufacturing and wholesale sales volumes both declined and Quebec’s public sector strikes will weigh on output. Our tracking is pointing to softer consumer discretionary spending in January as households unwind from a robust holiday shopping period.

The bottom hasn’t fallen out of the economy in a way that would force the BoC to rush into easing interest rates, and inflation is slowing but still above the central bank’s 2% target. Our base case remains that the first interest rate cut from the BoC will come in June, contingent on inflation continuing to drift lower.

Week ahead data watch

Canada’s Annual Capital Expenditures Survey (CAPEX) on Tuesday will be closely watched for signs on whether cautious business spending will persist into 2024. Business spending on machinery and equipment has been weaker in recent months. The BoC’s Business Outlook Survey shows businesses are still planning to invest more in machinery and equipment in the year ahead but at a modest pace.

U.S. personal consumption expenditure likely ticked down 0.1% in January from December, driven by lower retail sales and gas prices. That would be the first month-over-month decline since March 2023. We expect personal income to edge up 0.5%, boosted by resilient labour markets and a large annual cost of living adjustment for social security benefits.

Job openings and wages will be closely watched in Canada’s SEPH labour market data. Job openings edged higher in October and November but are still running 25% below year-ago levels. Other data from Indeed.com suggest that job postings continued to decline through most of January.

Weekly Focus – Strong Market Sentiment Continues

The leading AI chip designer Nvidia stole market headlines this week with a record daily jump in market capitalization of USD277bn on Thursday as its' stock rose 16% after it released blowout results and provided upbeat expectations. The news drove a turn higher in stock markets with both EuroStoxx50 and S&P500 hitting new record highs. More signs of a manufacturing recovery in the US added support to the market. Metal prices moved up over the week helped by a surprise 25bp cut in the Chinese benchmark for mortgage rates. Even Chinese stocks had a strong week after a very turbulent start to the year that was exacerbated by the 'quant quake' where forced selling by leveraged quant funds triggered a sharp decline. A hedge fund manager described it as the industry's biggest black swan moment.

Minutes from the latest central bank meetings in both the Fed and the ECB confirmed that policy makers still believe it is too soon to cut rates. This week we pushed out our expectation of the first cut from the Fed from March to May (see Reading the Markets USD - We now see the first Fed cut in May, 20 February) while we still see the first cut from the ECB in June. Bond yields had a slight tilt higher again this week on the back of robust risk sentiment and the still cautious signals by the central banks. The market prices close to four cuts from the ECB this year, which is still a bit more than the three we look for but much less than the six cuts that were seen early this year. The market now sees around three cuts by the Fed this year in line with our expectations. In FX markets, EUR/USD regained some ground after the decline in January and early February. Improving sentiment in China has given some support to the cross. We still see the US economy as the strongest economy, though, and look for EUR/USD to head lower in the medium term.

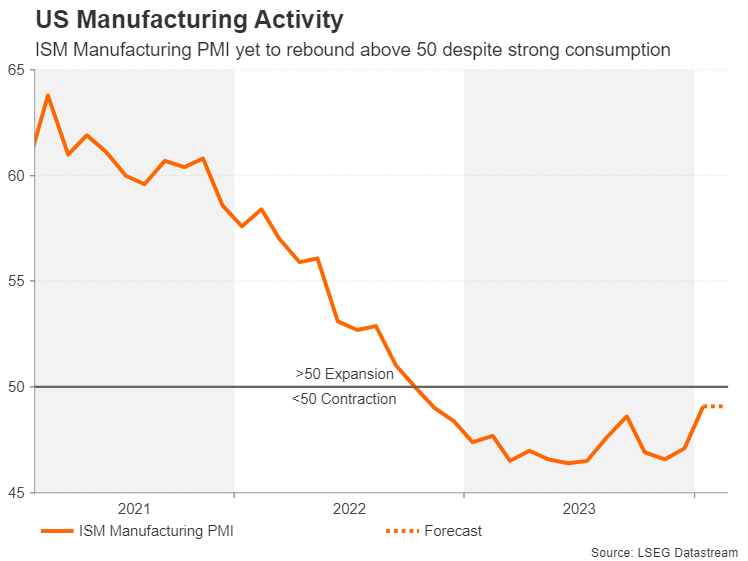

Economic data this week was a mixed. Euro area PMIs showed a return to a two-speed recovery with service PMI rising from 48.4 in January to 50.0 in February while PMI manufacturing dropped back to 46.1 from 46.6 breaking the rising trend of the past three months. Service employment also picked up. We still expect the manufacturing sector to see gradual improvement over the coming quarters driven by a turn in the global manufacturing cycle. With services also improving we look for a slight lift in GDP growth in Q1. The US showed the opposite split with soft service PMI but PMI in manufacturing moving higher. The latter is in line with the latest increase in ISM manufacturing and fits with the positive signals we have seen out of Asia over the past quarters. The weekly US jobless claims were strong, falling to 201k from 213k which is a very low level pointing to a continued robust labour market.

Over the coming week focus will again be on manufacturing with the US and China releasing ISM and PMI manufacturing, respectively. Inflation is also in the spotlight with Euro Flash CPI for February and Japanese CPI and US PCE inflation for January. We expect the Euro CPI to still be well behaved measured on monthly momentum in the core CPI, which the ECB is watching closely. We also get unemployment data for the euro area, which is still at record low levels at 6.4% despite the economic slowdown.

Week Ahead – US and Eurozone Inflation, RBNZ Meeting to Test Rate Cut Bets

- US core PCE and Eurozone flash CPIs to keep inflation worries in the foreground

- Japanese and Australian inflation numbers also coming up

- RBNZ might strike a hawkish tone

- Manufacturing PMIs also in the spotlight

PCE inflation to headline busy US data week

The Fed is in no rush to ease policy and markets are finally starting to come round to the prospect of no rate cuts before the summer. Yet, stock markets have remained bullish, suggesting that the fact alone that interest rates will start to fall this year is enough to spur optimism.

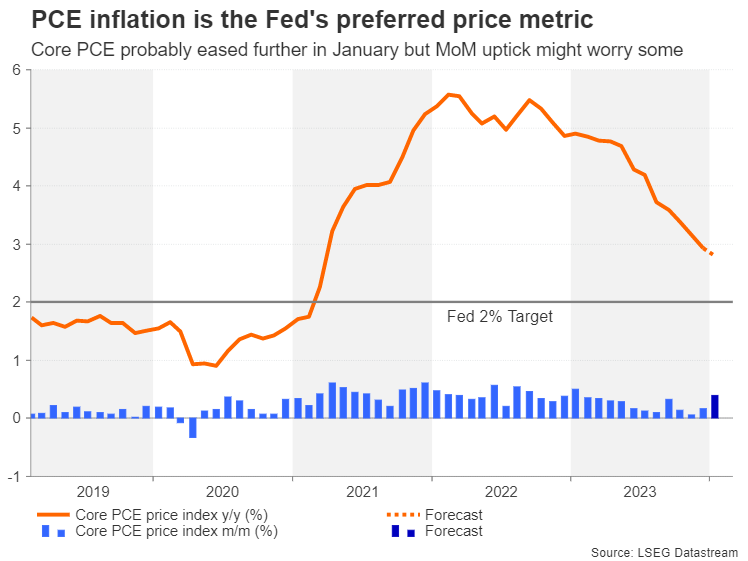

For the US dollar, however, any further delay could be crucial for its year-to-date uptrend, hence, next week’s releases will form one of the last pieces of the puzzle before the March FOMC meeting. Specifically, all eyes will be on the personal income and outlays report for January that includes the all-important core PCE price index, which is the Fed's inflation indicator of choice.

After both the CPI and PPI figures surprised to the upside, another hot inflation print could cast doubt on even a June rate cut. It’s possible though that January’s PCE inflation readings due Thursday will not sway rate cut odds in either direction.

The core PCE price index is forecast to have cooled slightly on an annual basis from 2.9% to 2.8%, but an acceleration in the month-on-month rate to 0.4% would likely keep investors on their toes.

In the event of a mixed set of PCE price data, the market reaction could be determined by how strong the personal income and spending numbers are. Personal consumption unexpectedly jumped by 0.7% m/m in December. It’s projected to have moderated to 0.3% in January, potentially easing concerns about an overheating US economy.

Will data flurry provide a lift to the dollar?

Inflation and consumer spending will not be the only data in focus as there’s a slew of other releases on the US agenda next week. Building permits and new home sales for January are out on Monday. Durable goods orders and the consumer confidence index will follow on Tuesday, while on Wednesday, the Q4 GDP growth estimate is expected to be left unrevised in the second reading. The Chicago PMI and pending home sales are up next on Thursday.

Rounding up the week on Friday is the ISM manufacturing PMI. The closely watched PMI gauge is forecast to have stayed unchanged at 49.1 in February, pointing to ongoing contraction in the sector.

If the data paint a broadly healthy picture, the US dollar might just be able to resume its ascent, though any gains would likely be limited without additional catalysts.

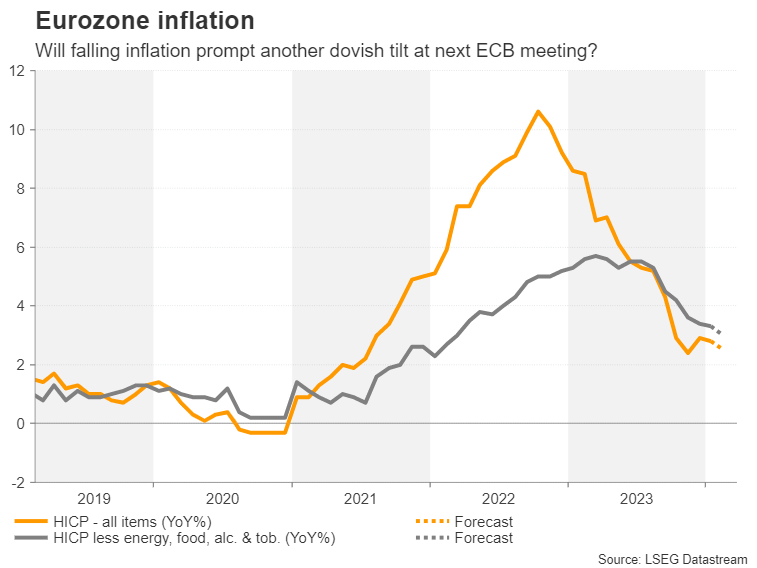

Last flash CPI report before March ECB meeting

The European Central Bank’s next policy meeting is fast approaching on March 7 and there is intense speculation as to whether or not policymakers will flag a rate cut soon. Inflationary pressures in the euro area are somewhat more subdued than in America, thanks mainly to a much weaker economy. Headline inflation dipped to 2.8% year-on-year in January, confounding expectations of a return to the 3.0% handle.

The flash estimates for February are due on Friday and if there is a further decline, markets will probably perceive that as a green light for policymakers to formally pave the way for a rate cut in the summer.

However, it’s also likely that policymakers will not want to pre-commit to a rate cut before there’s been further progress in lowering underlying inflation. The core figure excluding food and energy stood at 3.6% in January, while the measure that also excludes tobacco and alcohol prices was slightly lower at 3.3% but nevertheless some distance away from the 2% target.

The euro has been enjoying a bit of a rally against the greenback lately despite Fed rate cut bets being pushed back. However, there’s a risk of those gains being reversed if the inflation numbers are on the soft side as that would increase the odds of the ECB cutting rates before the Fed.

Euro traders will also be keeping an eye on Wednesday’s economic sentiment indicator and the bloc’s jobless rate on Friday.

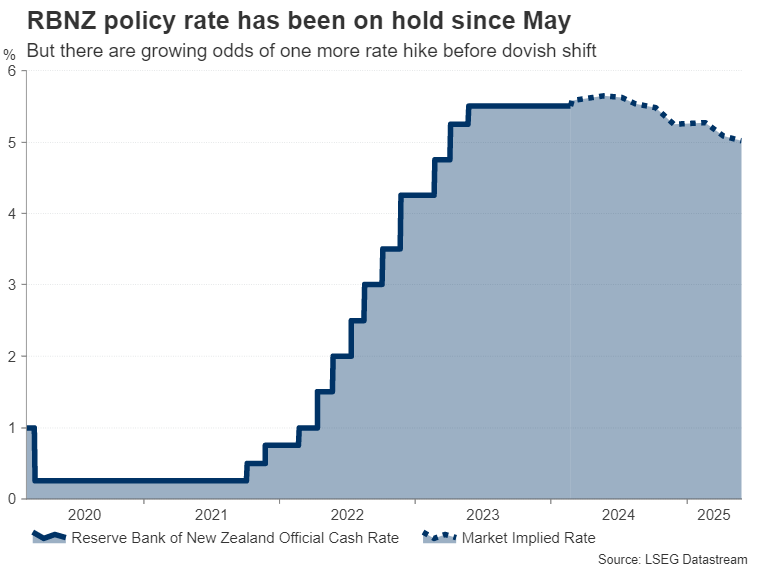

RBNZ might buck the rate cut trend

As most central bankers start to openly discuss shifting to an easing stance soon, the Reserve Bank of New Zealand has taken a hawkish turn. In recent comments, Governor Adrian Orr seemed to imply that there was a risk inflation would not return to the 1-3% target band without further tightening.

Although growth in New Zealand has been sluggish over the past few quarters and the labour market has cooled somewhat, business confidence is on the rise. The latest ANZ business outlook survey is out on Thursday. More importantly, CPI remains elevated at 4.7%, raising fears about persistent price pressures.

The odds of an additional rate hike have subsequently shot up, reaching almost 60% for the May meeting. For the February decision on Wednesday, markets have assigned a 30% probability. What is more certain, however, is that the RBNZ won’t be cutting rates anytime soon, if at all in 2024.

In its last quarterly projections, the RBNZ had forecast that rates would not start to fall before the first quarter of 2025. Should those forecasts be further pushed back in the quarterly Monetary Policy Report to be published on Wednesday, the New Zealand dollar could stretch its recent impressive gains.

Can the aussie extend its rebound?

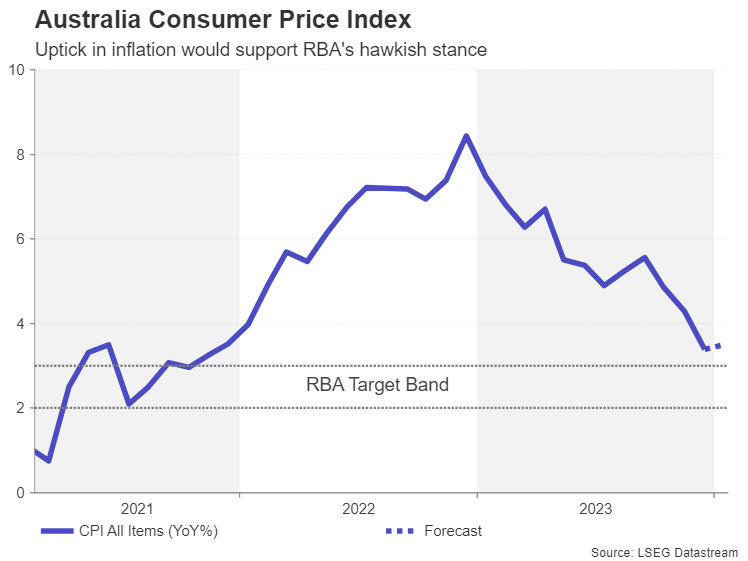

Another central bank that looks set to lag others in cutting rates is the Reserve Bank of Australia. However, inflation in Australia has now started to drop more quickly. The monthly headline rate had tumbled to 3.4% y/y in December. The January numbers are out on Wednesday and are forecast to show a slight uptick, giving the RBA more reason to remain hawkish.

Stalling disinflation would be positive for the Australian dollar, which recently broke above its bearish channel. But economic data, both domestically and from its largest trading partner – China – pose a downside risk. The fourth quarter estimate for capital expenditure is out on Thursday, while China’s official manufacturing and Caixin manufacturing PMIs are due on Friday.

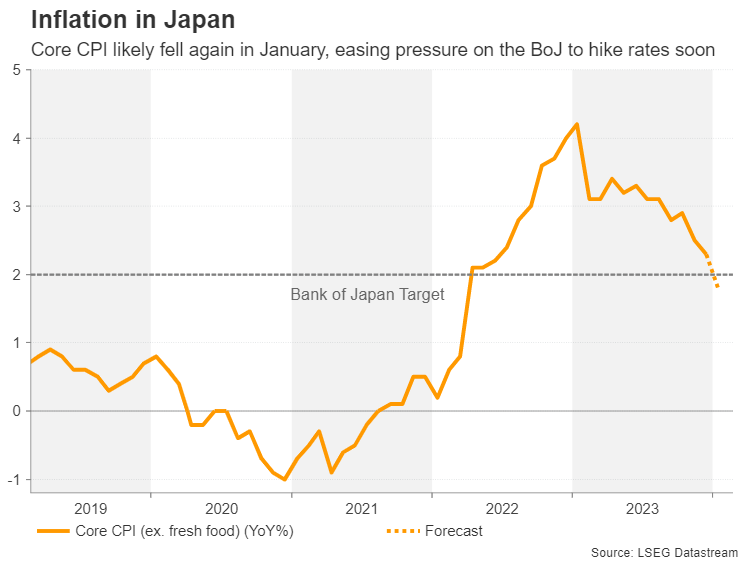

Japanese CPI unlikely to halt yen’s slide

Inflation will also be the highlight in Japan as the Bank of Japan ponders whether to exit from negative interest rates. The core consumer price index is expected to have risen by 1.8% y/y in January, in what would be a slowdown from the 2.3% rate in December, removing any urgency for policymakers to lift rates soon.

The yen could come under pressure from weaker-than-expected figures, although the BoJ’s primary focus right now is the spring wage negotiations, so any reaction would probably be modest.

Other releases will include preliminary industrial output and retail sales numbers for January on Thursday, followed by jobs stats on Friday.

Elsewhere, Canada reports fourth quarter GDP data on Thursday. The Canadian economy contracted in the third quarter, but a bounce back is likely in the final three months of 2023. A solid GDP reading could provide a much-needed boost to the Canadian dollar, which has failed to follow its peers in staging a rebound against its US counterpart over the past 10 days.

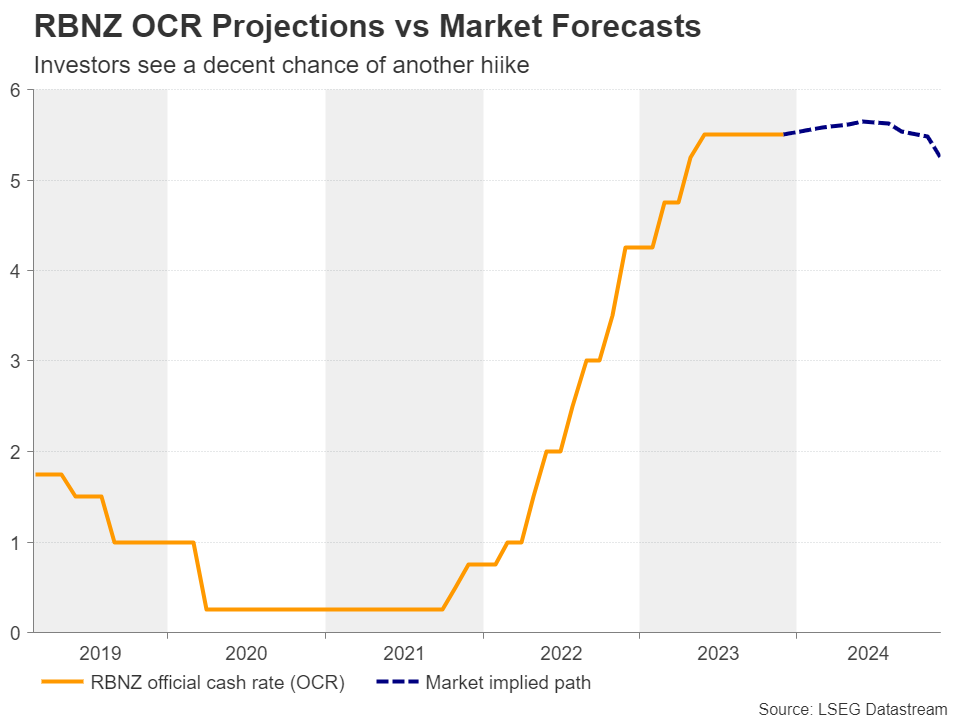

Will RBNZ Resume Interest Rate Hikes?

- RBNZ among the few central banks maintaining a tightening bias

- ANZ prompts investors to place rate hike bets

- Inflation slows but remains well above RBNZ’s target range

- The Bank meets on Wednesday at 01:00 GMT

Investors see decent chance for another hike

The Reserve Bank of New Zealand (RBNZ) is among the few central banks that are maintaining a tightening bias on concerns about ongoing inflationary pressures. At its latest gathering, on November 29, the Bank kept interest rates steady at 5.5%, but noted that should inflation prove stickier than anticipated, the Official Cash Rate (OCR) would likely need to increase further. What’s more important is that they revised their OCR projections up to signal a high probability of another rate hike by the end of 2024.

Nonetheless, although the kiwi gained back then on policymakers’ hawkish stance, investors were not convinced that another hike could be on the cards. They only changed their minds a couple of weeks ago, after the Australia and New Zealand Banking Group (ANZ) said it expects the RBNZ to lift its official cash rate by another 50bps to 6%. They clarified that they believe a 25bps hike will be delivered this month and another one in April.

Currently, investors are assigning around a 30% probability for a quarter-point hike at next week’s gathering, with that percentage rising to around 60% in May. That’s still a more cautious approach than the ANZ’s projections, but is it justified? Could the RBNZ actually hit the hike button this coming Wednesday?

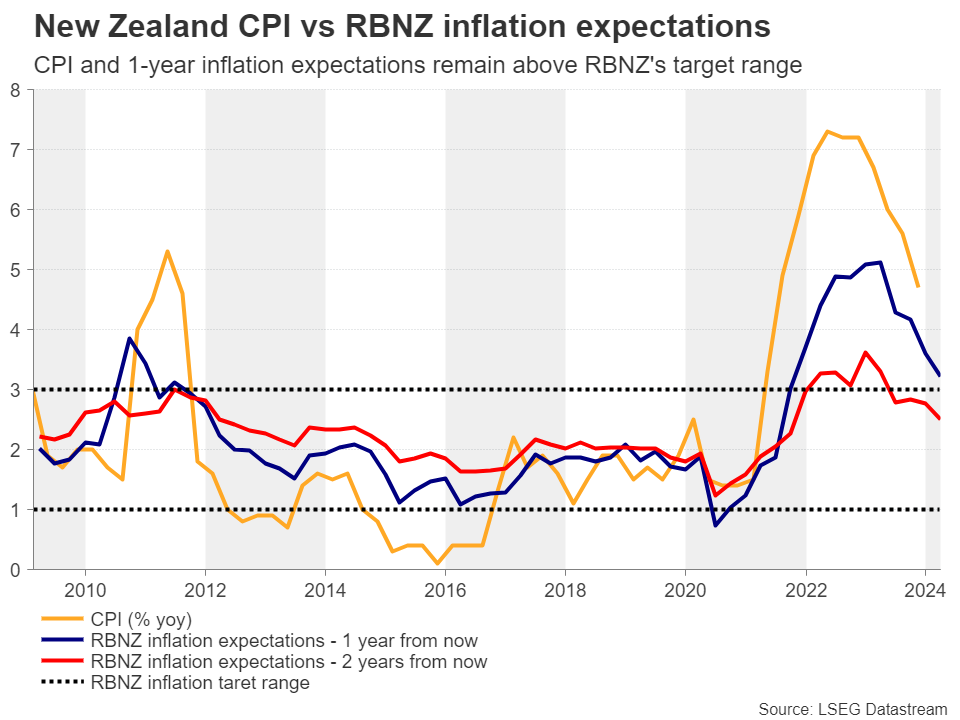

Economy contracts but inflation and wages remain sticky

Data after the November meeting revealed that the economy unexpectedly contracted 0.3% q/q in Q3, and that the CPI slowed notably to 4.7% y/y from 5.6% in Q4. However, not only does the CPI rate stand well above the upper bound of the RBNZ’s target range of 1-3%, but the Bank’s 1-year inflation expectations remain above that boundary. On top of that, the employment report for Q4 revealed a tighter than expected labor market, with the labor costs index accelerating to 1.0% q/q from 0.8%, driving the y/y rate only fractionally lower to 3.9% from 4.1%.

All these numbers, combined with recent remarks by RBNZ Governor Orr that there is still more work to be done to bring inflation to target, suggest that indeed there is a decent chance for policymakers to raise interest rates by another 25bps, even as soon as next week.

How may the kiwi respond to the decision?

With the market assigning a 30% chance for such a move, if a quarter-point hike is delivered, the kiwi is likely to add to its gains, especially if officials continue to signal that should inflationary pressures persist, interest rates could go even higher.

For the kiwi to fall notably and the outlook to turn bearish, not only does the Bank need to stand pat, but also to drop its hiking bias, a scenario that seems to be the least likely. Yes, the kiwi could still slide if officials stand pat but keep the bias untouched, but should upcoming data add to inflation concerns, the kiwi could rebound again on expectations that eventually the Bank will hike at one of its upcoming meetings.

From a technical standpoint, kiwi/dollar emerged above the key resistance (now turned into support) zone of 0.6155 on February 20, thereby completing a short-term triple bottom formation. This suggests that the bulls are likely to stay in the driver’s seat for a while longer.

The next obstacle on their way north may be the 0.6275 zone marked by the high of January 12. A break higher could put the 0.6370 barrier on their radar. That zone has been acting as a ceiling for more than a year. On the downside, the move signaling that the bears have stolen all the bulls’ weapons may be a dip below the recent lows of 0.6050, which acted as both support and resistance during the past year.

Sunset Market Commentary

Markets

ECB members came out “en masse” today, resembling the recent push by the US central bank. Hawkish Austrian ECB Holzmann immediately pulled an interesting string. He supports our “sequence” call, stressing that he didn’t see any circumstances for the ECB to cut policy rates before the Fed. We’re on the same line, arguing that the ECB won’t risk a weaker currency by moving ahead of the FOMC. Its credibility and especially inflation goal are at stake if the central bank risks taking the first leap while inflation is still running above the 2% inflation target. Given that Fed members are openly pushing back first rate cuts bets to the June meeting (at best), it implies that the window of opportunity for the ECB only opens at the July meeting, our preferred scenario. Holzmann continued by preferring a later but faster cycle compared to a rapid start with gentle moves lower. The main argument for erring on the hawkish side of expectations is the persistence of elevated wage pressure. Shorty after the Holzmann comments, the ECB published consumer survey inflation expectations for January. They slightly increased on the 1-yr horizon (3.3% from 3.2%) while keeping level on the 3-yr tenor (2.5%). ECB Schnabel lined up next, arguing that internal models suggest that the peak impact from interest increases may already be over. This again argues in favour of keeping policy rates higher for longer with inflation sticky above target and EMU growth set to recover from last year’s standstill. Bundesbank president Nagel added to the hawkish rhetoric by saying that officials mustn’t be tempted to cut rates earlier as the inflation outlook isn’t clear enough yet. He’s more comfortable with current market pricing (first move in June; max 100 bps of cuts this year) compared with say a month ago (start in April and cumulative 150 bps of cuts in 2024). Premature cuts could result in the worse outcome, reigniting inflation when it hasn’t actually been conquered. ECB President Lagarde underlined the importance of Q1 wage data which will only be at the central bank’s disposal by the June policy meeting. Lithuanian ECB Simkus is happy with Lagarde’s guidance of a first rate cut in “summer” while dovish Greek ECB member Stournaras is more precise, singling out the June meeting as his preferred kick-off point.

ECB rhetoric failed to inspire trading in an uneventful session. German Bund yields currently give up around 3 bps after setting YTD highs yesterday. Changes on the US yield curve are more modest, varying between +1 bp and -1 bp. EUR/USD treads water at 1.0830 with European stock markets slightly benefiting from yesterday’s WS momentum (EuroStoxx +0.4%;new cycle high).

News & Views

French finance minister Le Maire called for action in the creation of a Capital Markets Union (CMU). In his pitch before his European colleagues he noted the project has dragged on for a decade but that high financing needs for the green and digital overhaul underscore the need. France and Germany estimate these costs at some €500bn a year, which may be difficult to finance through public funds only. The many different financial systems and legal settings in the 27 EU countries make it very challenging to create the CMU. That’s why Le Maire suggests to kick off the project on a voluntary basis, beginning with three to four (unspecified) countries. His proposal would entail the submission to single EU supervision of banks, stock exchanges and asset management as well as the creation of a European savings product.

Belgian business confidence improved in February from -16.4 to -12.8. Doing so, the NBB’s company gauge reversed the setback from January with better readings across all sector. The smoothed series, indicating the underlying economic trend, increased only slightly but that does bring an end to the downward path in place since last May. Trade (from -17.8 to -11.9) posted the sharpest recovery on better forecasts for orders to be placed with suppliers, in response to growing demand expectations. Business-related services sector confidence (+9.1 from +4.6) was shored up by all sub indicators, from the assessment on current and expected activity to anticipated demand. Manufacturing (-18.5 vs. -22) also responded more favourably on all accounts with the biggest improvement seen in future demand. The upturn in confidence was the smallest in the building industry (-10.3 from -12.8).

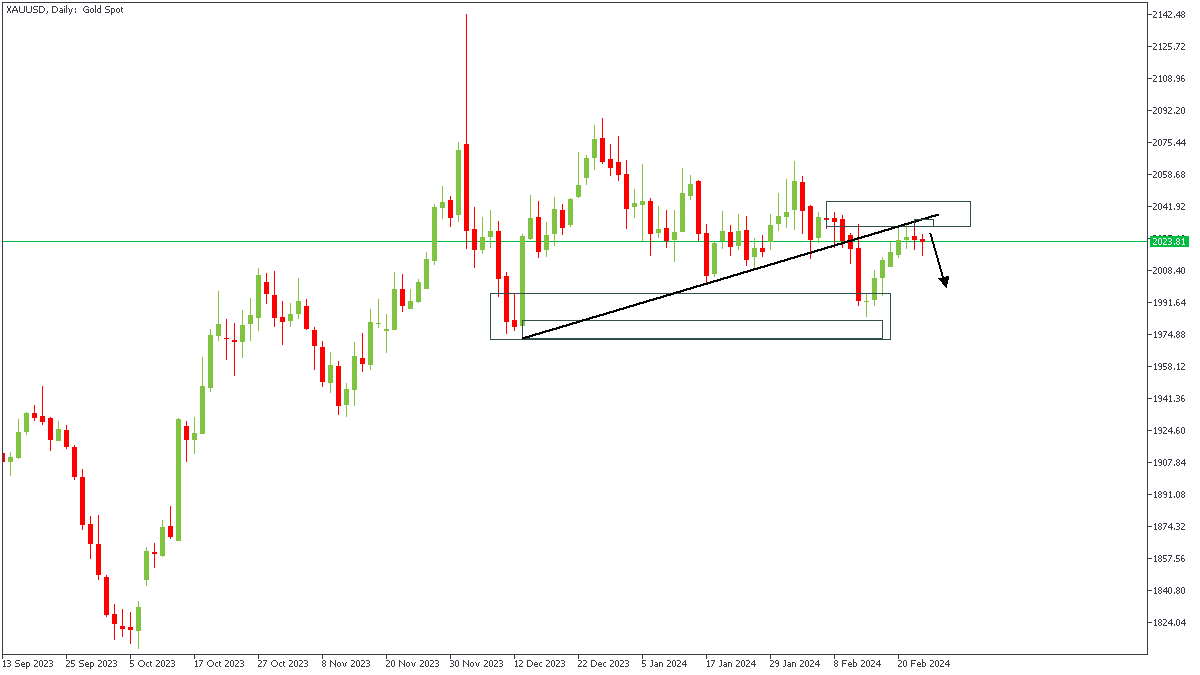

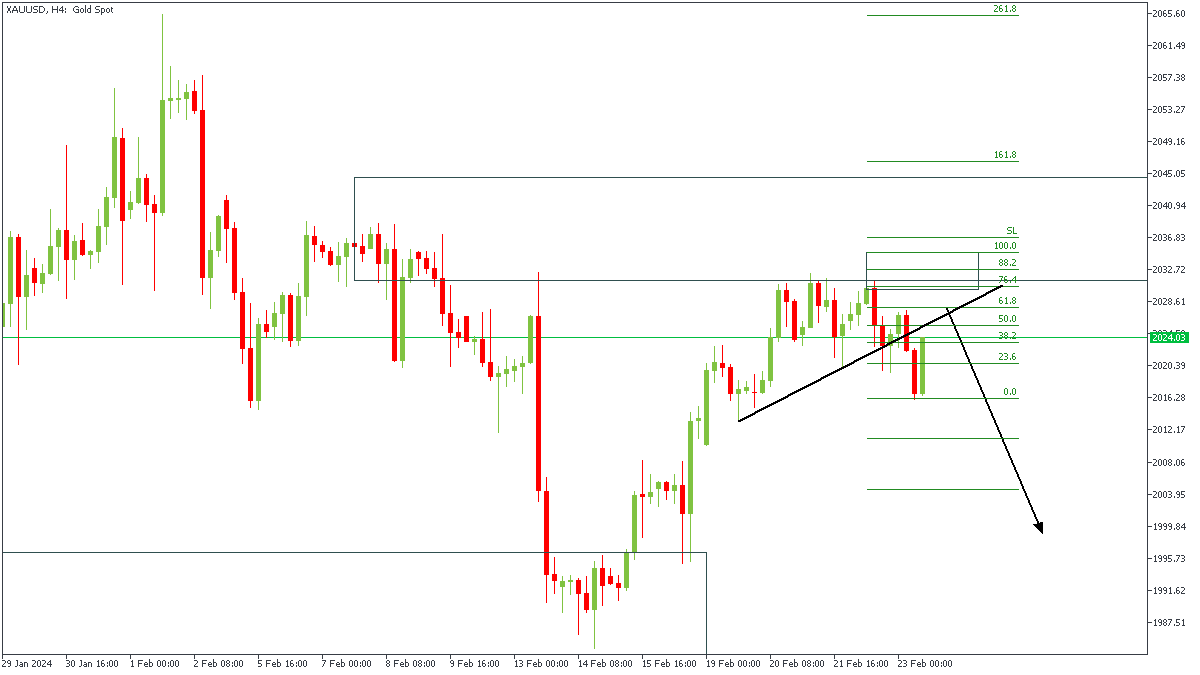

XAUUSD: Bears Prepare To Takeover

On Friday, the gold price (XAUUSD) retreated from a recent two-week high, facing selling pressure. This decline was driven by hawkish minutes from the FOMC meeting, indicating the Fed's reluctance to cut interest rates. Elevated US Treasury bond yields, supported by a "higher-for-longer" narrative, further weakened demand for gold, as investors favored yield-bearing assets. However, the US dollar struggled to gain momentum, staying near three-week lows, potentially supporting gold as a safe-haven asset amid geopolitical tensions in the Middle East. Moving forward, market attention will focus on US bond yields and USD dynamics, with short-term opportunities in XAUUSD influenced by broader risk sentiment.

XAUUSD - D1 Timeframe

Price action on the daily timeframe of XAUUSD shows price currently reacting from the rally-base-drop supply zone, albeit in a subtle manner. We also see that the previous low has been broken, which means that price can be said to have completed the retracement. The added confluence to this is the trendline resistance that price seems to also be reacting to at this time.

XAUUSD - H4 Timeframe

After reacting from the supply zone on the daily timeframe, here on the 4-hour chart of XAUUSD, we see that a change of character has already occurred from the recent break of structure. Following this, I expect to see a proper rejection from the trendline resistance and the Fibonacci retracement level. My target for this idea is the previous demand zone as shown on the chart.

Analyst’s Expectations:

- Direction: Bearish

- Target: $2,004.62

- Invalidation: $2,044.96

CONCLUSION

The trading of CFDs comes at a risk. Thus, to succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.

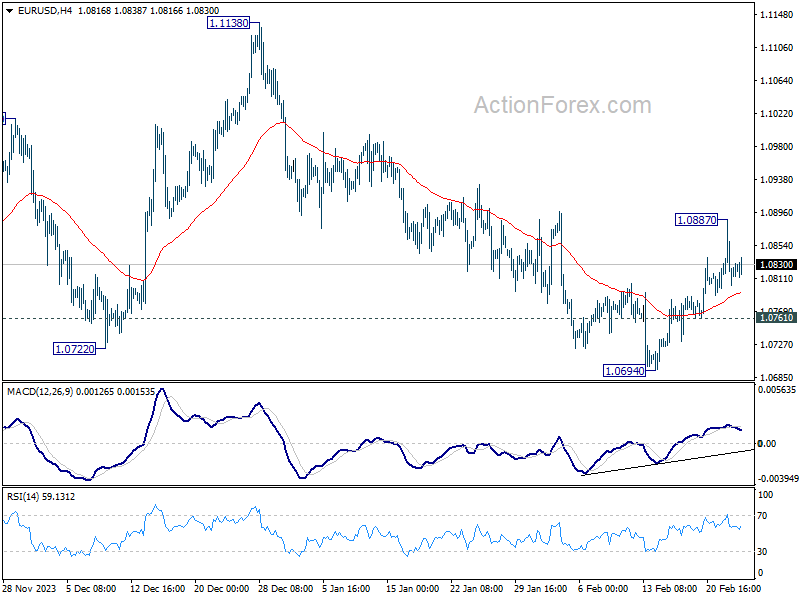

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0788; (P) 1.0838; (R1) 1.0872; More...

Outlook in EUR/USD is unchanged and intraday bias stays neutral. On the upside, break of 1.0887 will affirm the case that fall from 1.1138 has completed, and target this resistance. However, break of 1.0761 will turn bias back to the downside for retesting 1.0694 support.

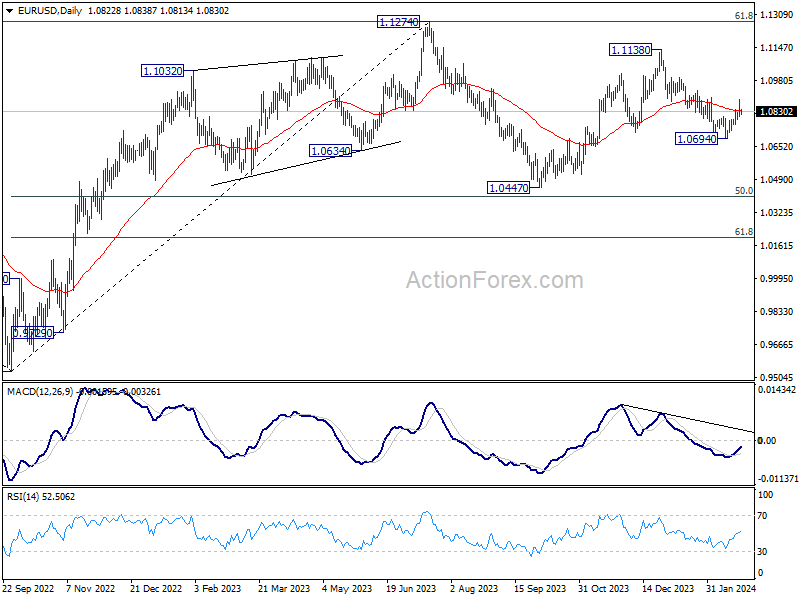

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

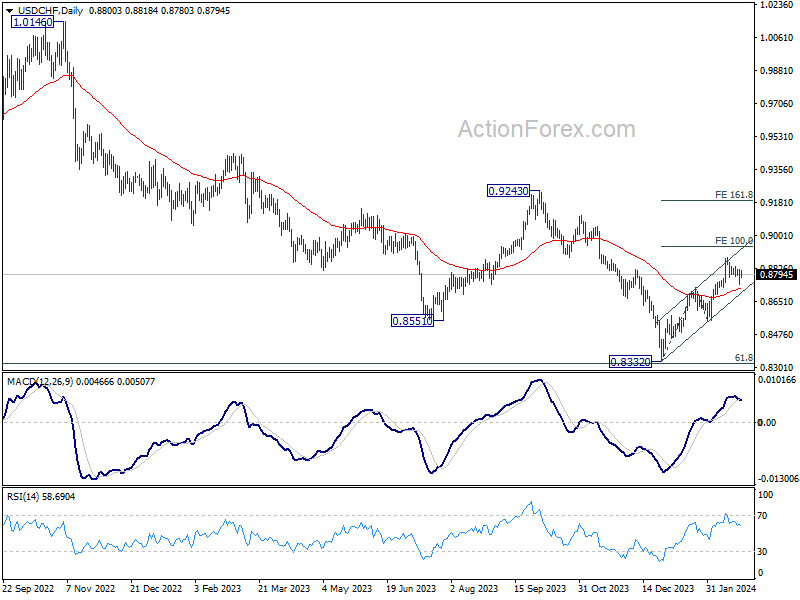

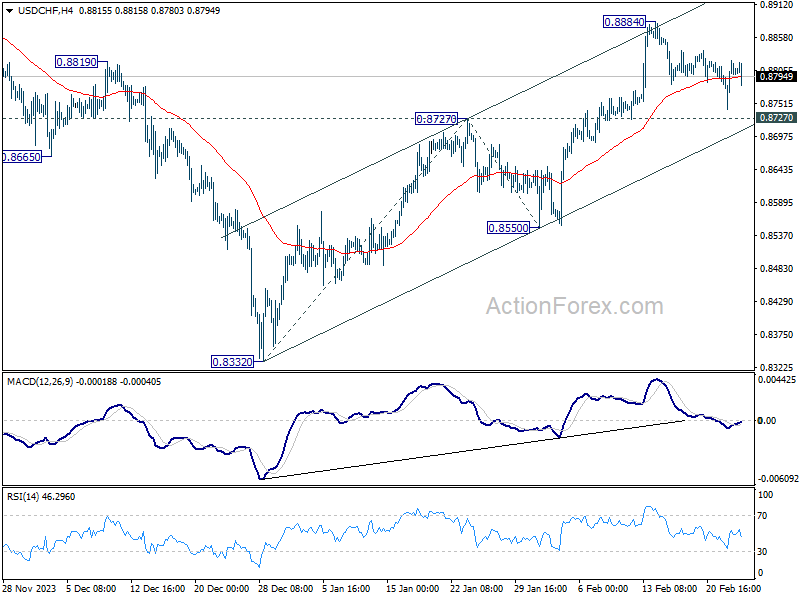

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8756; (P) 0.8789; (R1) 0.8835; More....

No change in USD/CHF's outlook as consolidation is extending. Intraday bias remains neutral. With 0.8727 resistance turned support intact, further rally is expected. On the upside, break of 0.8885 will resume the rise from 0.8332 and target and 100% projection of 0.8332 to 0.8727 from 0.8550 at 0.8954. However, sustained break of 0.8727 will dampen this bullish view, and turn bias back to the downside for 0.8550 support instead.

In the bigger picture, a medium term bottom should be formed at 0.8332, on bullish convergence condition in W MACD, just ahead of 0.8317 long term fibonacci support. It's still early to decide if the larger down trend from 1.0146 (2022 high) is reversing. But further rise should be seen to 0.9243 resistance even as a correction.