Sample Category Title

Weekly Economic & Financial Commentary: A March Rate Cut Bites the Dust

Summary

United States: A March Rate Cut Bites the Dust

- It was a busy week for economic data, but Friday's employment report stole the show. Nonfarm payrolls rose 353K in January, almost double the consensus expectation. While we suspect the Federal Reserve will put more weight on the Employment Cost Index's soft reading on labor cost growth in Q4, the pickup in average hourly earnings and overall strength in hiring suggest the odds of a rate cut in March are quickly fading.

- Next week: ISM Services (Mon.), Trade Balance (Wed.), Consumer Credit (Wed.)

International: Eurozone Inflation Slows as Growth Remains at a Standstill

- Eurozone GDP was flat in Q4, while CPI inflation eased slightly further in January. As long as growth remains weak and inflation trends keep improving, we believe the European Central Bank could cut its policy rate as early as April. This week also saw monetary policy announcements from several other foreign central banks, which saw rate cuts delivered in Brazil, Chile, Colombia and Hungary and rates held steady in the United Kingdom and Sweden.

- Next week: RBA Policy Rate (Tue.), Japan Labor Cash Earnings (Tue.), Banxico Policy Rate (Thu.)

Interest Rate Watch: FOMC Removes “Bias” to Tighten

- As universally expected, the FOMC decided to make no changes to its monetary policy stance, keeping the fed funds target range at 5.25%-5.50% and maintaining the current pace of quantitative tightening. Importantly, the Committee removed its implicit “bias” to tighten policy further in its post-meeting statement.

Topic of the Week: China's Property Crisis Grows Ever Grander

- On Monday, a Hong Kong court ordered the liquidation of Evergrande, China’s second-largest property developer, marking the most significant blow yet to China’s struggling real estate sector. China’s real estate crisis has intensified over the past couple of years, but challenges for the sector have been evident for some time.

Canada’s January Unemployment Rate to Hit 5.9%—Highest Since Pandemic

Canadian jobs numbers for January will be centre stage next Friday as policymakers and market watchers look for signs of deterioration in the labour market. The data for the first month of 2024 will tell a similar story to the one we have observed over 2023—employment is rising but not quickly enough to prevent an increase in the unemployment rate.

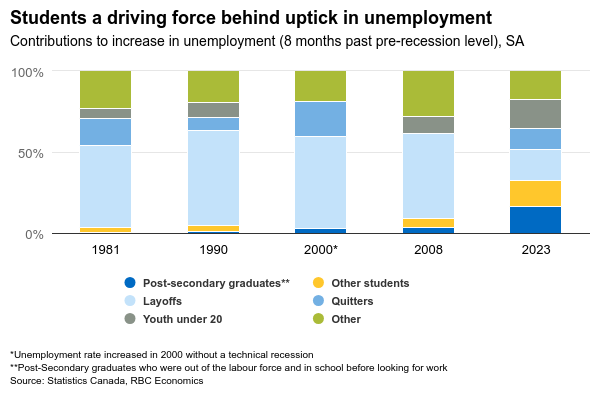

We expect Canada’s unemployment rate likely hit 5.9% in January—up almost a full percentage point from 5% a year earlier. That’s the highest rate since the pandemic—January 2022. We expect to see another 10,000 jobs added from December, but that’s not fast enough to keep up with the country’s record pace of population growth.

There are also signs hiring demand is continuing to slow. Job postings from Indeed.com were down more than 6% in January from December. Fewer job postings mean fewer opportunities for new people to enter the labour market. In recent months, students and new graduates searching for work accounted for half of the increase in the unemployment rate. While employment counts continued to rise in Q4, actual hours worked outright declined.

The Bank of Canada will be closely watching wage growth for further evidence that labour markets are softening. To date, growth in average hourly earnings has remained firm, and there is still room for growth particularly as unionized worker contracts continue to catch up to inflation. That will keep a floor under wage increases in the near term. But business surveys also widely suggest that wage growth will begin to slow as hiring demand cools.

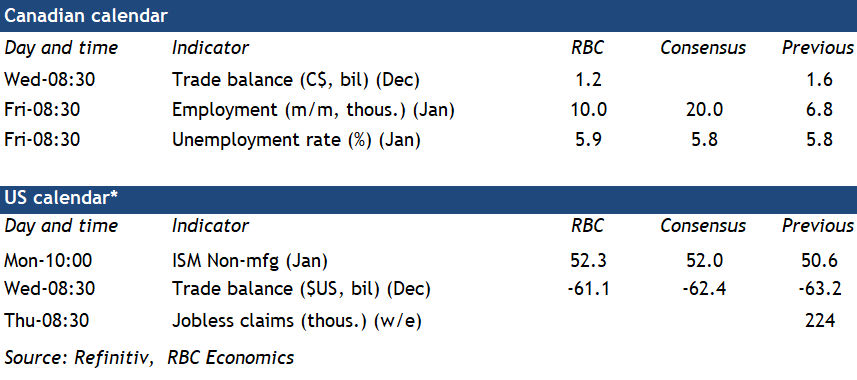

Week ahead data watch

Canada’s trade surplus in December likely shrank to $1.2 billion from November. Exports likely fell (we expect -2.2%) on lower motor vehicle shipments and oil prices. The former is consistent with industry data pointing to a pullback in motor vehicle production in December.

We expect the overall U.S. trade balance for December to come in at $-61.1 billion with the deficit narrowing from $-63.2 billion in November. According to advanced economic indicators, the U.S. goods sector deficit was down by $900 million from November, led by higher goods exports (+2.5%). Goods imports also rose by 1.3%.

Groundhog Day: Hiring Once Again Starts the Year at Blistering Pace

Summary

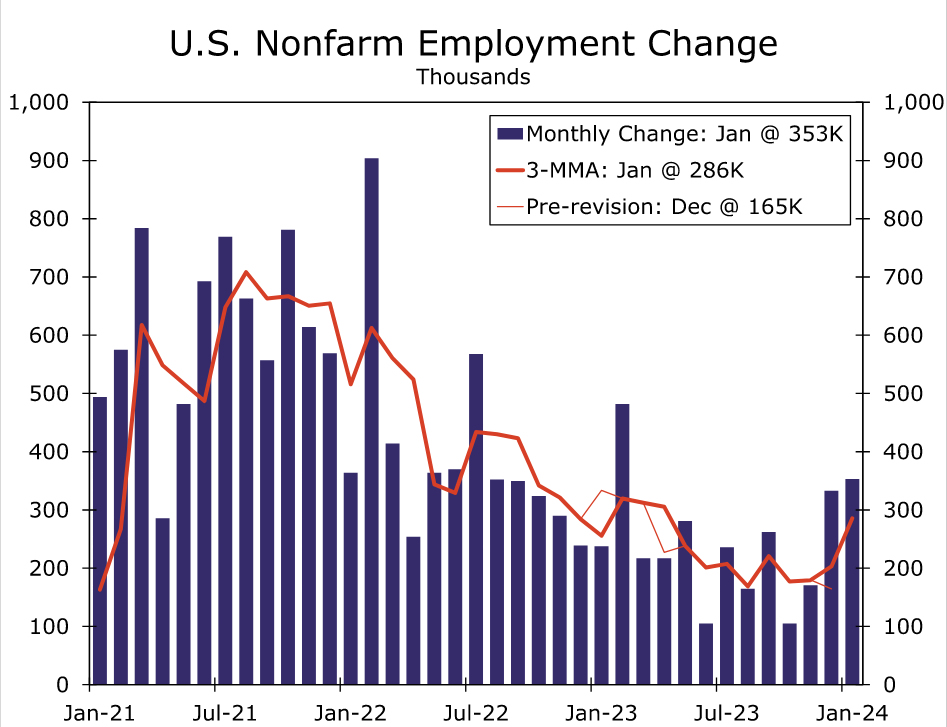

Hiring once again came out of the gate strong in 2023. Nonfarm payrolls rose by 353K in January, blowing past consensus expectations for a 185K gain. What's more, revisions point to stronger momentum in hiring through the end of last year; payrolls in the fourth quarter of 2023 are now reported to have grown an average of 203K compared to 165K prior to today's report.

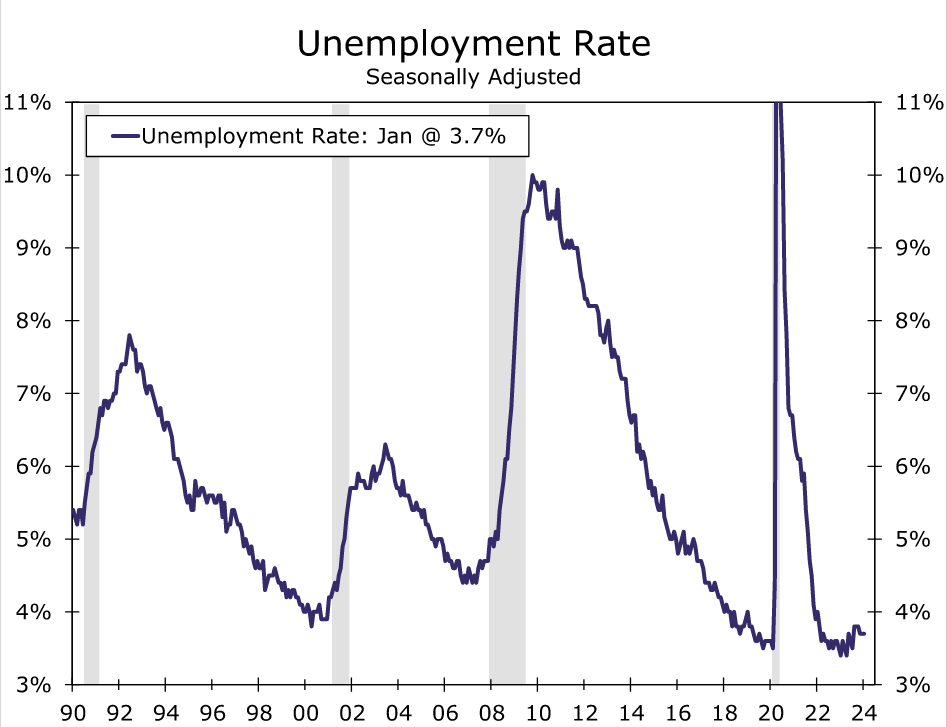

Overall, the jobs market appears to be on firmer footing than implied only a month ago. In addition to the solid number of jobs added, employment gains broadened across industries in January. Joblessness also remains low, with the unemployment rate unchanged at 3.7%. Average hourly earnings growth of 0.6% in January, double the expected gain, further points to a still-strong labor market.

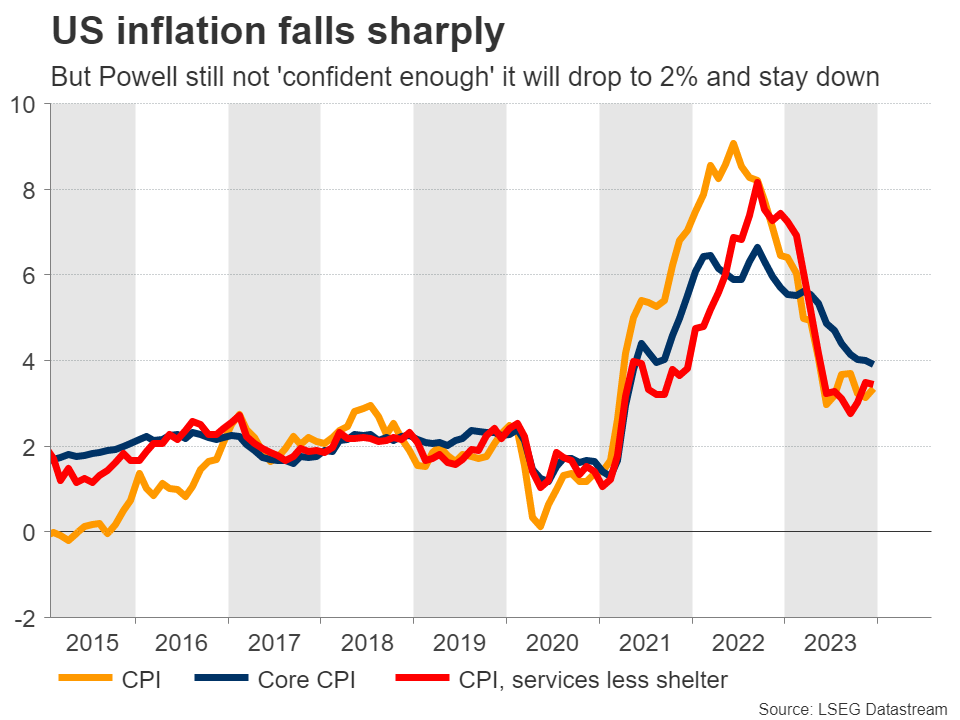

Chair Powell made clear in his post-meeting press conference on Wednesday that a rate cut in March was not the Committee's base case. But he left open the possibility that a cut could occur if the economic data came in unexpectedly soft. Today's employment report reinforces the view that a March rate cut is not in the cards. Rate cuts are coming this year, but we think it will take until the May meeting for the FOMC to reach a consensus that inflation is on a sustainable path to 2%.

A Knockout Report

Nonfarm payroll growth in January blew past expectations, rising 353K compared to consensus expectations for a 185K gain. The sizzling print reflects that while employers are not as eager to take on new workers as they were a year or two ago, they remain reluctant to let existing workers go. January typically sees sharp drops in employment on a non-seasonally adjusted basis, and this January payrolls fell by 2.64 million compared to an average of 2.74 million the prior five years and 2.94 million the five years preceding the pandemic.

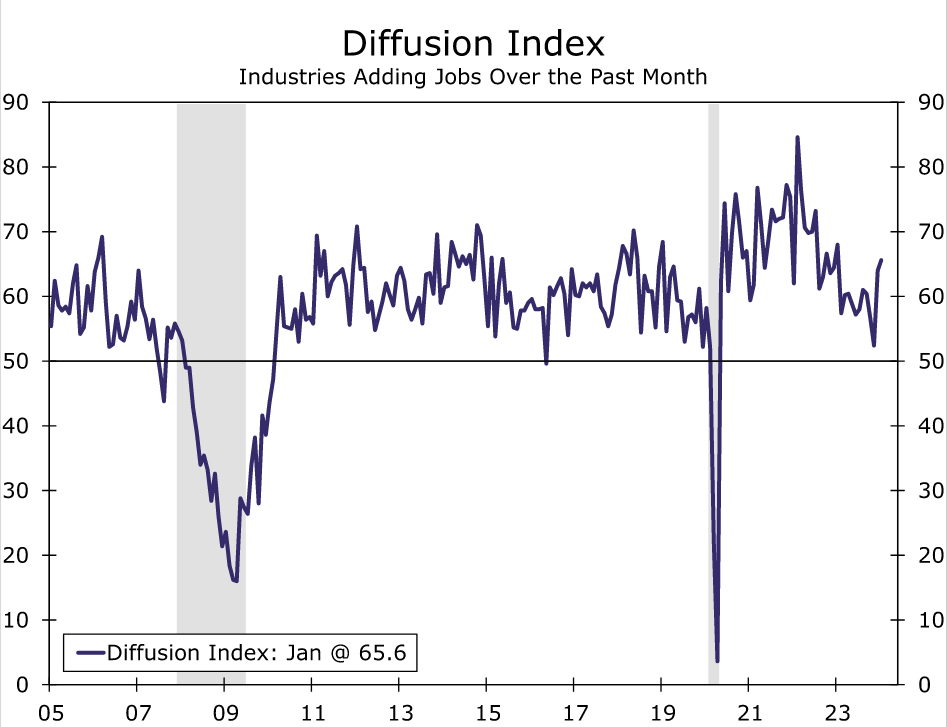

Employment growth in January was more broadly-based across industries relative to recent months. The labor market diffusion index, a measure of job growth breadth, posted its highest reading since January 2023. Job gains were led by professional and business services (+74K), health care (+70K), retail trade (+45K) and government (+36K).

The good news extended beyond just January. Revisions to the prior two months' added another 126K to job growth in December and November. This pushed the three-month moving average on nonfarm payroll growth up to 286K, its highest reading since April 2023.

In addition to the usual revisions due to late survey responses to the prior two months data, today's report included annual benchmark revisions along with revised seasonal factors to the Establishment Survey. The benchmark showed a more moderate pace of hiring in 2022 and early 2023. The level of payrolls as of March 2023 was revised down by 266K, which was a bit smaller than the preliminary estimates for a decline of 306K and the largest downward revision since 2019 (-489K). The monthly trend in hiring late in the year looks stronger than it did before the revisions. Payrolls in the fourth quarter are now reported to have increased an average of 203K per month compared to 165K prior to today's report.

In another sign that the labor market remains on solid footing, the unemployment rate held at 3.7%, bucking expectations for an increase to 3.8%. January's Household Survey data included new population controls, but unlike the Establishment Survey, prior monthly data were not revised. Therefore, the changes in the level of household employment and the labor force are ineffective this month, but ratios such as the labor force participation rate and unemployment rate are more reliable. The unemployment rate points to a still-tight jobs market as the robust growth in labor supply through much of 2023 has started to fizzle. The labor force participation rate was unchanged at 62.5% in January, down from 62.8% as recently as November.

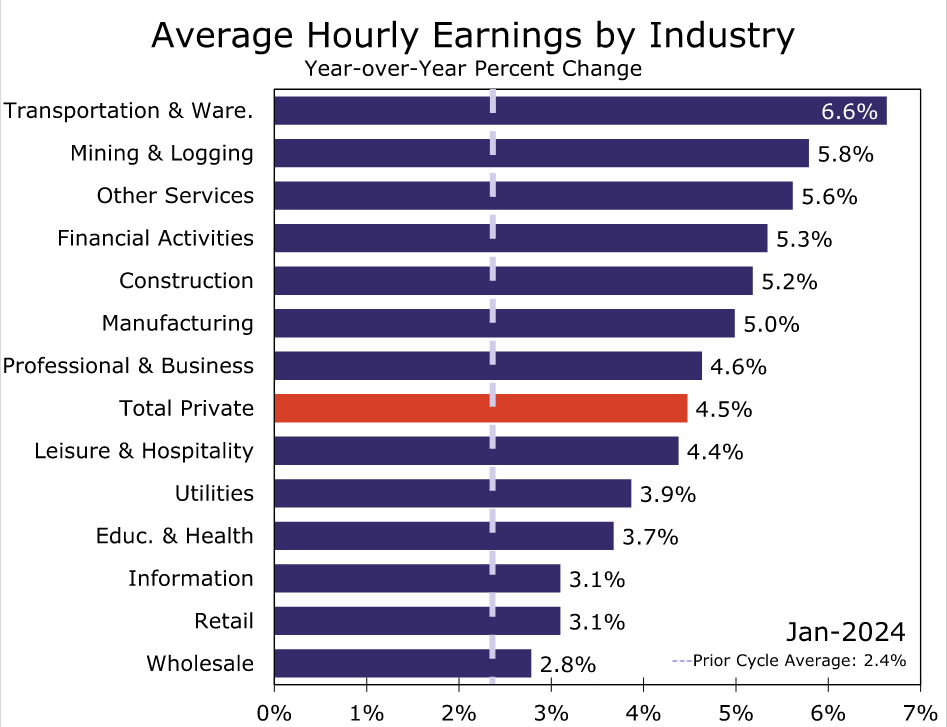

January's average hourly earnings (AHE) further demonstrate that the jobs market is far from weak. AHE rose 0.6% in January, double the consensus forecast for a 0.3% increase. What's more, strength was broad based, with nine of the 13 major industries posting monthly gains of at least 0.4%. Average hourly earnings among private sector workers have increased at a 5.4% annualized pace on a three-month basis and 4.5% on a 12-month basis. The pickup contrasts with the recent signal from the employment cost index that labor costs are falling back in line with the pace consistent with the Fed's inflation target. However, average hourly earnings can be volatile on a monthly basis and are prone to revision, in addition to providing a narrower look at compensation costs (the ECI includes benefit costs in addition to wages & salaries as well as public sector workers). We put more weight on the ECI, and we suspect the FOMC will do the same. That said, the AHE data from today are yet another weight on the scale pointing to a stronger-than-expected labor market to start the year.

March Rate Cut Odds Fade Further

In his press conference after this week's FOMC meeting, Chair Powell threw cold water on the idea of a rate cut at the next meeting on March 19-20. Powell stated that "based on the meeting today, I would tell you that I don't think it's likely that the Committee will reach a level of confidence by the time of the March meeting to identify March as the time [to cut rates]. But that's to be seen." Two employment reports and two CPI reports between the January and March meetings, as well as a slew of other economic data, left the door ajar for a March cut should the data point to more softness in inflation and the economy than expected.

Today's employment report clearly reinforces the view that a rate cut is not coming at the March meeting. Nonfarm payroll growth is humming along at a much stronger pace than previously reported, and the unemployment rate remains low at 3.7%. The doves on the FOMC should feel comforted that the labor market is not on the precipice of a material deterioration in the near term, while the hawks likely will feel emboldened to wait for at least a few more inflation data points to ensure that the inflation genie is back in the bottle.

Week Ahead – RBA Decision and US Data on the Menu

- Dollar cannot sustain Fed-fueled advance, will ISM data help?

- Reserve Bank of Australia could abandon its tightening bias

- Crucial data releases also from China, Canada, and New Zealand

Fed warns against early rate cuts

It was an eventful week in global markets. The spotlight fell on the Federal Reserve, which shot down expectations it would cut interest rates in March, with Chairman Powell stressing that this is not the “base case" scenario.

Even though inflation has declined substantially, Powell downplayed speculation that rate cuts are just around the corner, arguing that the Fed is still not fully confident it has won the war. He pointed to solid economic growth, resilient consumer spending, and a tight labor market as factors that could keep inflation above 2% for some time.

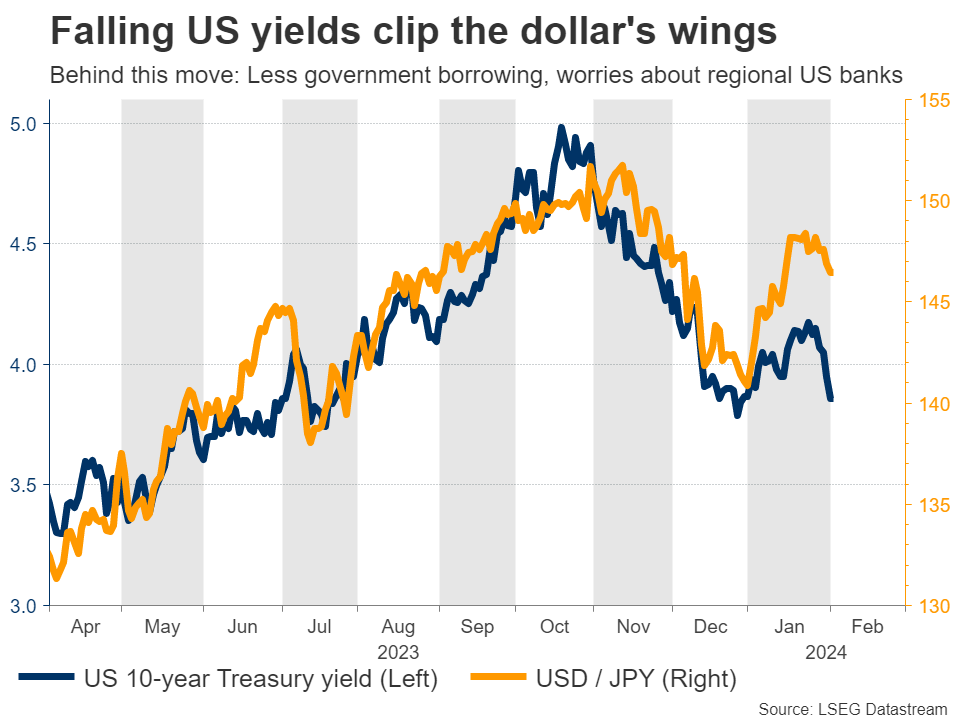

Reading between the lines, his broader message was that rates will eventually come down, but not quite as quickly as markets had hoped. As a result, traders scaled back bets on a March rate cut, slashing the probability to around 35% from 60% ahead of the Fed decision.

This translated into a boost for the US dollar. However, the dollar could not sustain those gains, mostly because the market didn’t change its view on the total amount of rate cuts that will be delivered this year - it simply pushed back the timing. Nearly six rate cuts are still priced in for the year.

A sharp decline in US bond yields was another element behind the dollar’s inability to rally, as lower yields diminish the dollar’s interest rate advantage. This slide was fueled by the government’s announcement that it will borrow less this quarter than previously estimated, as well as renewed concerns about the health of US regional banks after some poor earnings.

Looking ahead, the main event next week will be the ISM non-manufacturing survey, due on Monday. This is one of the most important leading economic indicators of the US economy, and forecasts point to a meaningful increase in January. If that is the case, the market could continue to unwind some of its Fed rate cut bets, helping the dollar regain some momentum.

RBA meets, will it abandon its tightening bias?

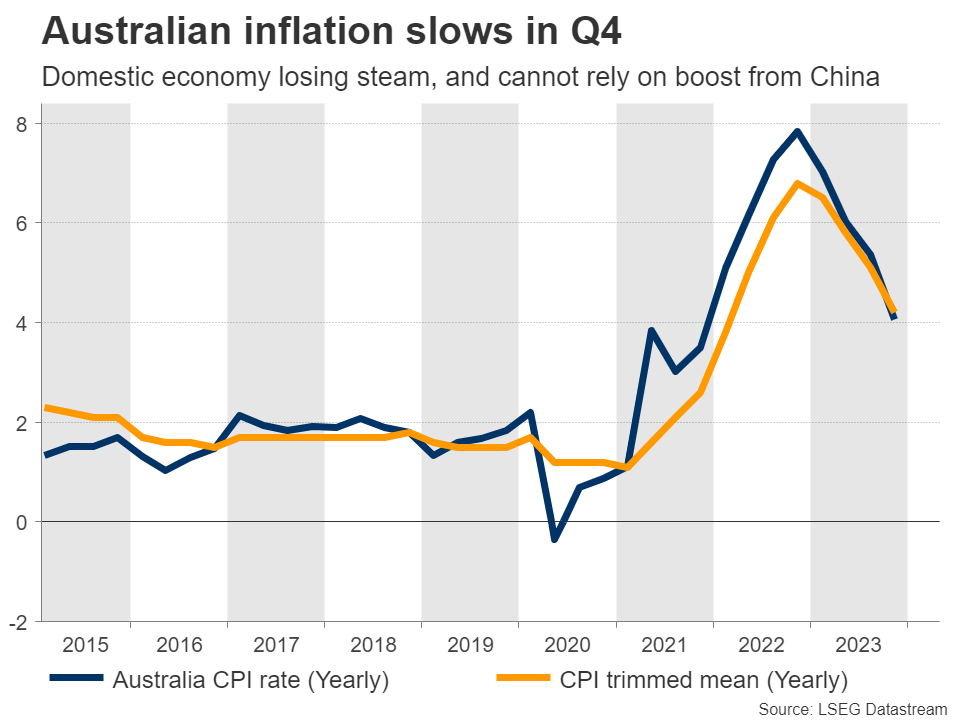

Over in Australia, the Reserve Bank will meet on Tuesday. Market pricing suggests interest rates will be kept unchanged, so the focus will fall mostly on whether the central bank will keep further rate increases on the table.

The minutes of the December meeting showed that policymakers discussed another rate increase, but decided against it. Since then, incoming data has been on the weaker side with inflation slowing sharply in Q4, the labor market losing jobs, and consumer spending disappointing during the holiday season.

Even though policymakers may keep the option of raising rates again on the table, it is becoming clear that this is unlikely to happen. The domestic economy is losing steam and Australia’s largest trading partner - China - is in bad shape as it deals with the implosion of its property market.

Therefore, even if the Australian dollar spikes higher in the case the RBA maintains a tightening bias, the general outlook for the currency seems gloomy. It would probably take a meaningful recovery in China and commodity prices, before the currency can stage a sustainable rally.

Speaking of China, the latest inflation stats will be released on Thursday. Forecasts suggest the world’s second largest economy sunk deeper into deflation in January, which could reignite concerns around the future outlook, keeping local stock markets and the China-linked Australian dollar on the defensive overall.

New Zealand and Canada release job numbers

Staying in the sphere of commodity currencies, employment data out of New Zealand and Canada will also be in focus on Tuesday and Friday, respectively.

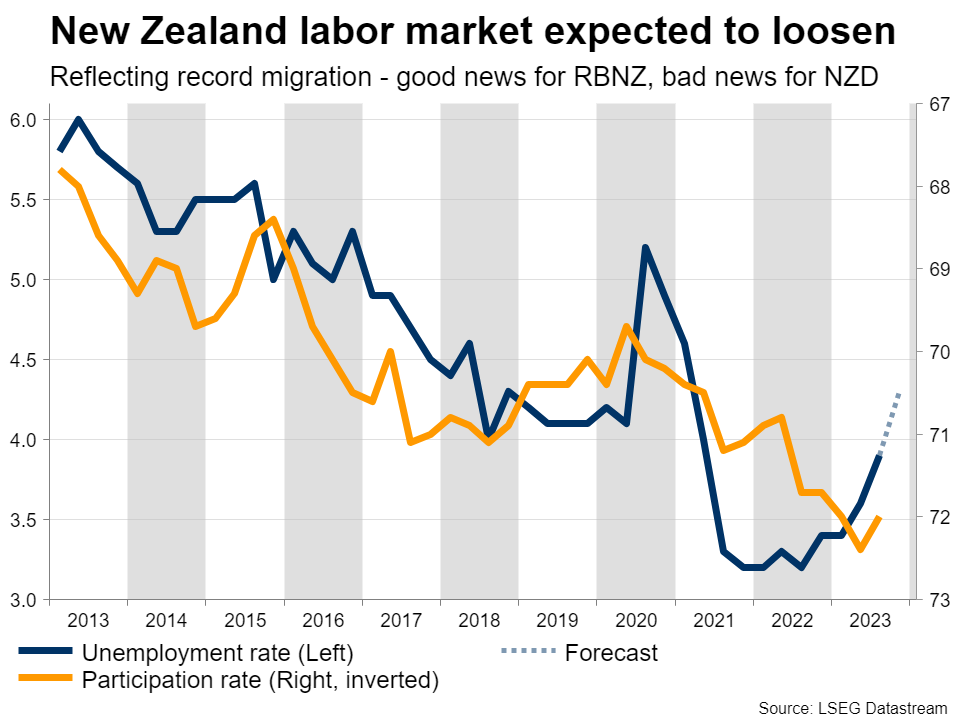

In New Zealand, forecasts point to a looser labor market in Q4, with the unemployment rate projected to rise to 4.3% from 3.9% in the previous quarter and wage growth set to cool off. Most of this loosening reflects increasing labor supply amid record migration inflows, which will be welcome news for the Reserve Bank as it will help cool inflation.

That said, the New Zealand dollar might react negatively to this dataset, as a softer labor market strengthens the case for cutting interest rates.

Over in Canada, the show will begin on Wednesday with the summary of deliberations from the latest Bank of Canada meeting. This is similar to the meeting minutes, and will give investors a detailed account of what was discussed. Then on Friday, the employment report for January will reveal whether the trend of a rising unemployment rate continues.

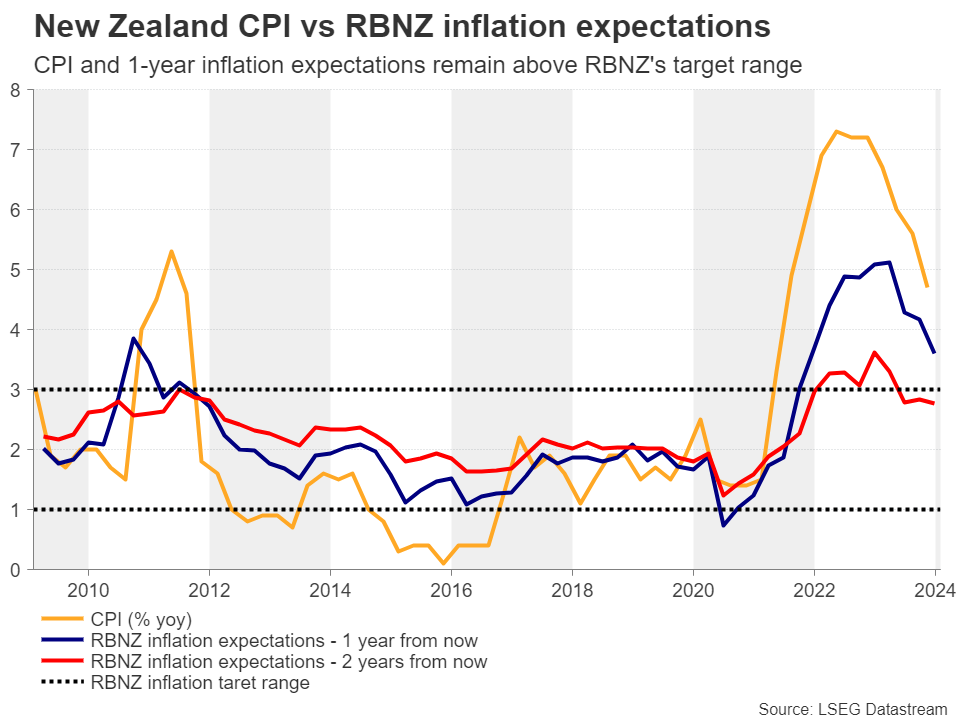

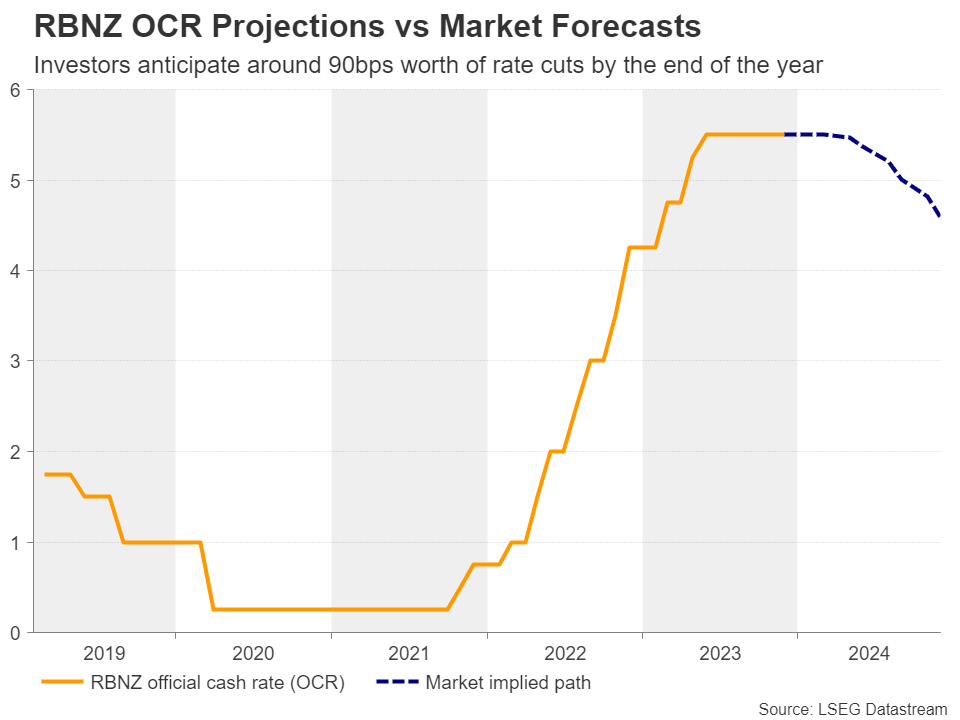

Will Weak Jobs Data Prompt RBNZ to Drop Hiking Bias

- RBNZ remains hawkish despite slowing inflation and weaker growth

- Investors price in 90bps rate cuts by the end of 2024

- Focus turns to jobs data for Q4 on Tuesday at 21:45

Despite hawkish RBNZ, data drive investors to price in rate cuts

At its November gathering, the RBNZ held its official cash rate (OCR) steady at 5.5% and noted that inflation remains too high and that if price pressures were to become stronger than anticipated, interest rates would likely need to rise further. Officials also lifted their OCR projections to signal a decent chance for another 25bps hike before this tightening crusade ends.

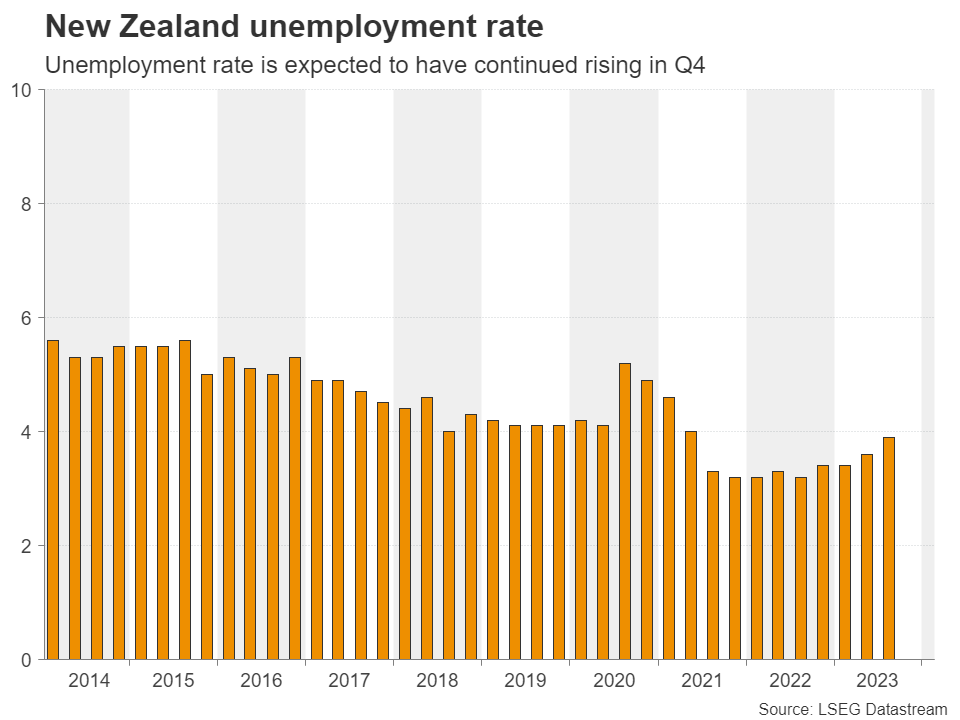

Data since then revealed that New Zealand’s economy unexpectedly contracted by 0.3% q/q in Q3, while the growth rate for Q2 was revised notably down to 0.5% from 0.9%. On top of that, headline inflation slowed to 4.7% y/y in Q4 from 5.6%, with the core standardized rate also sliding to 4.7% y/y from 5.0%. One-year inflation expectations have also been coming down at a relatively fast pace.

Taking that into account, investors don’t believe that higher rates are on the table anymore. On the contrary, they are anticipating around 90bps worth of rate reductions by the end of the year, with a quarter-point cut more-than-fully priced in for July.

Governor Orr says jobs data to impact next decision

Nearly three weeks after the GDP data were out, RBNZ Governor Andrian Orr told parliament that surprisingly weak Q3 economic data was a “complex situation,” adding that although interest rates continue to constrain spending, the Bank remains wary of inflationary surprises. He noted that the Bank was analyzing the data but other key data points before the February meeting, including employment, would also impact the decision.

This likely adds an extra degree of importance to next week’s jobs report for Q4 due out late on Tuesday, during the early Asian session Wednesday. The unemployment rate is forecast to have continued rising to 4.3% from 3.9%, while the labor cost index is seen slowing to 3.7% y/y from 4.1%, which could raise speculation that inflation may continue cooling.

Such numbers may confirm the market’s view that the RBNZ will be forced to lower borrowing costs at some point this year, although shifting from a hiking bias to immediately signaling rate reductions may not be the case at the February gathering.

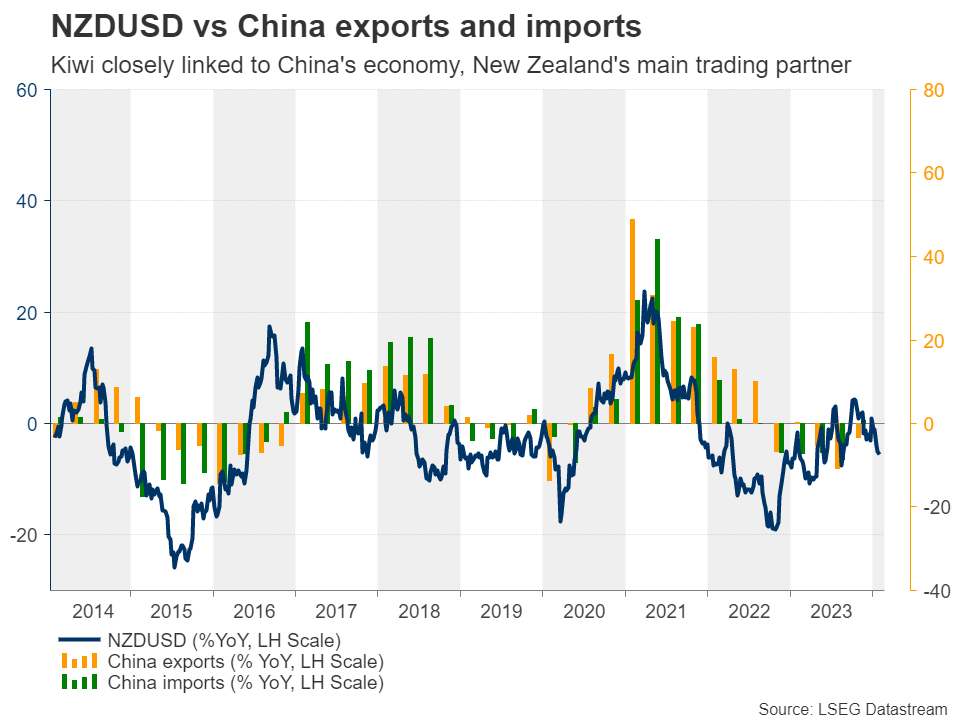

China also a big variable in the kiwi equation

What’s more, apart from domestic data, the kiwi seems to be sensitive to developments surrounding China, as the world’s second-largest economy is New Zealand’s main trading partner. On Friday, China’s Shanghai Composite fell further, logging its worst week in five years as concerns about the property sector after Evergrande was ordered to be liquidated overshadowed earlier optimism sparked by the nation’s announcement of measures to stabilize the market. Thus, those concerns could continue weighing on the kiwi.

Are kiwi bears waiting behind the bushes?

Kiwi/dollar has staged a decent recovery lately, after hitting support at 0.6060 on January 23 and now looks to be headed towards the 0.6170 resistance zone. That said, the pair remains below the prior uptrend line drawn from the low of October 26, which means that the bears may still be willing to jump into the action.

If they do so from near the 0.6170 barrier, they may feel confident to drive the action back down to the 0.6060 zone, the break of which would confirm a lower low and perhaps carry extensions towards the round number of 0.6000, which offered support on November 22 and resistance on November 6. For the outlook to turn positive, the pair may need to climb all the way above the 0.6275 zone, which acted as resistance between January 3 and 12.

Weekly Focus – Wait and See Mode in Central Banks

In a week with no big data or central bank surprises, renewed fears of turmoil in the US banking sector on the back of the free fall of the New York Community Bancorp (NYCB) stock, drove longer dated yields lower as markets largely ignored hawkish Fed comments. With decent macro data and declining inflation as a solid backbone, equity markets did not suffer any big blows on the back of the NYCB situation.

January inflation data played well into the optimistic market perception that central banks will be able to cut rates aggressively this year. Euro area inflation declined slightly, and core price pressures remained modest for the sixth month in a row. Many annual price adjustments happen in January and thus the modest price increase removes some upside risk to the inflation outlook. With unemployment flat at a record-low 6.4% in December there are no signs of slowing wage pressures, though, and we continue to believe markets are too optimistic on the number of rate cuts this year.

The euro area barely avoided a technical recession with flat GDP growth in Q4 2023. The manufacturing recession is still weighing heavy on the German economy, which shrunk 0.3%, while Southern Europe and particularly Spain got a boost from a strong tourism sector.

Global manufacturing bellwethers like South Korean semiconductor exports and PMIs and Taiwan and ASEAN PMIs ticked in quite strong in January which indicate the worst of the global manufacturing recession is behind us. Elsewhere in Asia, Chinese PMIs indicate a continued muddling through scenario with the service sector importantly not falling out of the bed.

Fed remained on hold as widely expected, as Fed chair Powell signalled optimism on inflation but pushed back on a March rate cut. He said that data seen so far has been 'good enough' and that the Fed simply needs to see more similar evidence on disinflation to initiate the cutting cycle. Data were mixed with more job openings in December but higher initial jobless claims. For the third consecutive quarter, productivity growth was reported a lot higher than expected and even if such data is by definition uncertain, it does support cooling inflation.

Also the Bank of England kept (BoE) and the Riksbank kept policies unchanged at their respective policy meetings. The BoE removed its tightening bias but caused little market reaction. We expect both to cut rates for the first time in June.

Next week is thin on the data front. In the US, we will look out for ISM services. December PMIs indicate a rebound here after a relatively weak December. In China, we will likely see another deflation print. It is partly driven by food prices, though, and we still do not see broad-based declines in core prices.

US: January Delivers a Scorching Hot Employment Report

Non-farm payrolls rose by 353k in January, well ahead of the consensus forecast calling for a smaller gain of 185k.

- This morning's report also included annual benchmark revisions as well as revised seasonal factors. The revisions showed a slightly weaker rate of job growth over 2022 and early-2023. The total level of nonfarm employment for March 2023 was revised down by 188K (seasonally adjusted) or -0.1%. However, revisions through the H2'2023 showed a slightly more robust pace of hiring, with the monthly upward revision over the last six months averaging 27k. This was in part boosted by December's revisions, which were revised higher by a sizeable 117k.

Private payrolls rose by 317k – slightly higher than the 278k reported in December. Gains in the service sector (+289k) were widespread, with health care & education (+112k), professional & business services (+74k) and retail trade (+45k) seeing the strongest gains. Goods-producing industries (+28k) also had a solid month, with hiring in both construction (+11k) and manufacturing (+23k) recording gains. Government added 36k jobs.

In the household survey, new population controls were introduced last month (as is the case every January), but the historical household data was not revised. This distorts the month-to-month changes for household employment and labor force. However, the ratios in the survey (i.e., the unemployment and participation rates) remain largely unaffected. Both the unemployment rate and participation rate held steady at December's levels of 3.7% and 62.5%, respectively.

Average hourly earnings rose sharply, rising 0.6% month-on-month (m/m) – a notable acceleration from last month's 0.4% m/m gain. On a twelve-month basis, wage growth ticked up to 4.5% – the strongest pace of growth since September. The three-month annualized rate of change rose to 5.4% (from 4.2% in December).

Key Implications

Strong employment readings for the month of January have become a recurring theme post-pandemic. Not only did job growth handily beat expectations, but job gains were also reasonably widespread as evidenced by the private-sector diffusion index rising sharply to 65.6 – the highest level since January 2022. Monthly wage growth also accelerated by the fastest pace in nearly two years, pushing the year-on-year measure up to a five-month high.

Despite the incredibly strong employment report, post-payrolls market pricing for a May cut (60% priced) has barely budged – likely the result of Powell having recently downplaying the impact of strong economic data. Although the labor market remains hot, productivity (measured as output per worker) continued to firm through the fourth quarter of last year, helping to restrain the inflationary impulse from higher wage growth and posing less of a threat to the inflation outlook. From that perspective, a further easing in inflationary pressures over the coming months could provide the FOMC enough reassurance that inflation remains on a sustainable path back to 2%. This suggests that the Fed could argue that a May rate cut is still justified despite the ongoing labor market strength.

Aussie Slides After Hot US Nonfarm Payrolls

The Australian dollar has fallen almost 1% after the US nonfarm payrolls and has given up today’s earlier gains. In the North American session, AUD/USD is trading at 0.6644, down 0.40%.

The US dollar has started 2024 on the right foot, recording gains against most of the major currencies in the month of January. The Australian dollar slipped 3.59% against the US dollar in January and on Thursday, the Aussie dollar dropped as low as 0.6508, its lowest level since November 20.

US nonfarm payrolls shocker

The week wrapped up in dramatic fashion, as the US nonfarm payroll report was red-hot, surging to 353,000 in January and blowing past the market estimate of 180,000. The December release was revised upwards to 333,000, up from 216,000. The massive job gain has propelled the US dollar higher against the major currencies, as expectations of a March rate cut have nosedived. In the aftermath of the nonfarm payroll report, the probability of a March cut has dropped to 19%, compared to 38% just a day ago according to the CME FedWatch tool.

Federal Reserve Chair Powell dampened hopes for a March cut at this week’s meeting, when he said that a March cut was not likely, although he was careful not to completely rule out such a scenario. The markets are pinning their hopes on the May meeting, with the likelihood of a quarter-point cut at 62%, according to CME’s FedWatch.

The Reserve Bank of Australia meets on February 6 amid signs that the economy continues to cool down. Inflation eased to 4.1% y/y in the fourth quarter, down from 5.4% in Q3, while retail sales sunk in December with a decline of 2.7% m/m. The RBA is virtually certain to pause next week and is expected to start to trim rates later this year.

AUD/USD Technical

- AUD/USD is testing support at 0.6544. Next, there is support at 0.6514

- There is resistance at 0.6613 and 0.6652

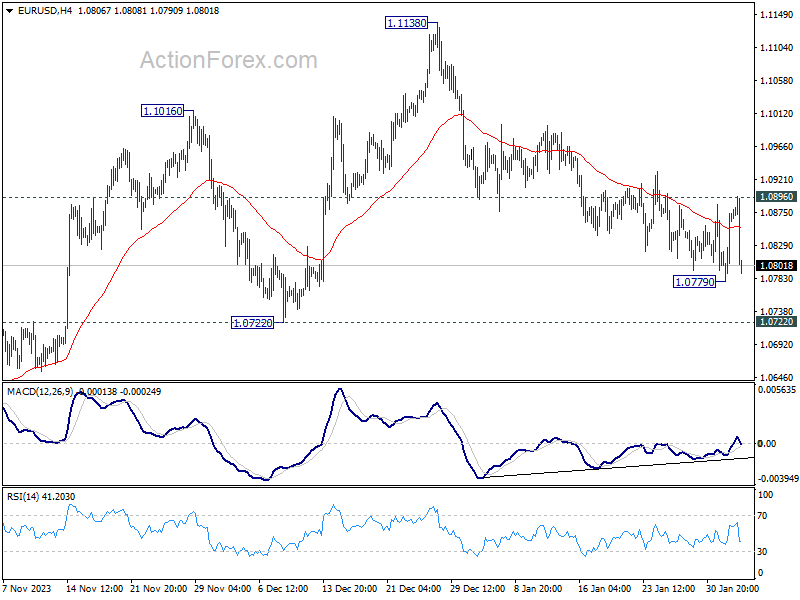

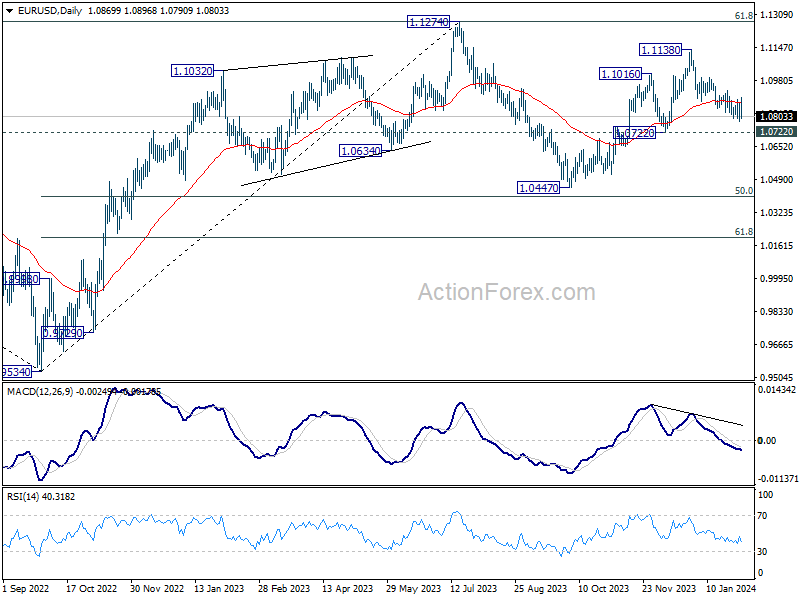

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0810; (P) 1.0843; (R1) 1.0905; More...

EUR/USD falls sharply in early US session but stays above 1.0779 temporary low. Intraday bias remains neutral first. On the downside, below 1.0779 will resume the fall from 1.1138. But considering bullish convergence condition in 4H MACD, strong support could be seen from 1.0722 to bring rebound. Nevertheless, decisive break of 1.0722 will argue that whole rise from 1.0447 has completed, and target this low.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

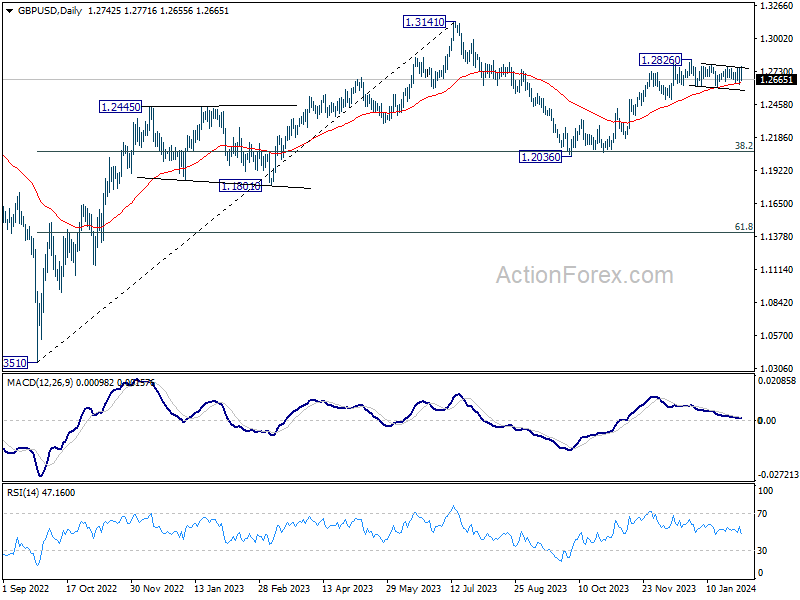

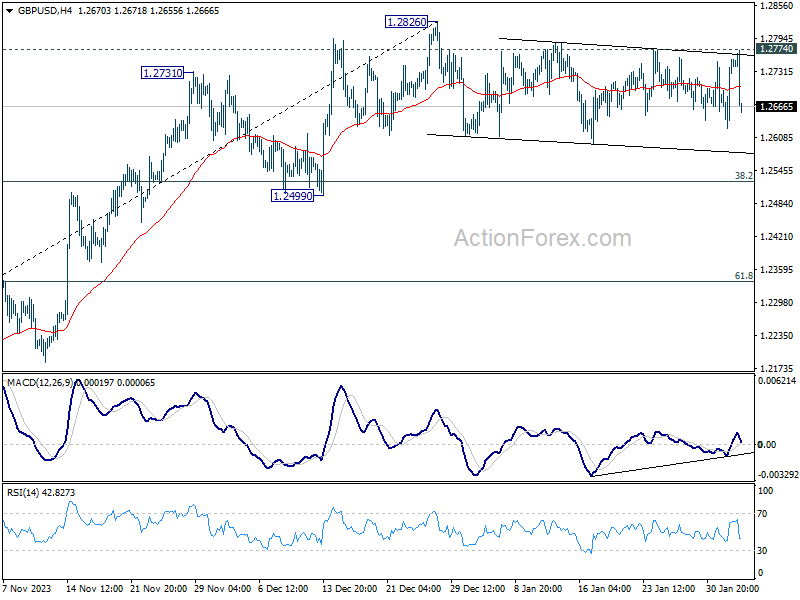

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2661; (P) 1.2708; (R1) 1.2792; More...

Range trading continues in GBP/USD with today's sharp fall, and intraday bias remains neutral. Consolidation from 1.2826 could still extend further, and deeper fall cannot be ruled out. But downside should be contained above 1.2499 support to bring rebound. On the upside, firm break of 1.2774 resistance will suggest that consolidation pattern has completed. Further rise should be seen through 1.2826 to resume the rally from 1.2036. Next target will be 1.3141 high.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.