Sample Category Title

USD/CHF Weekly Outlook

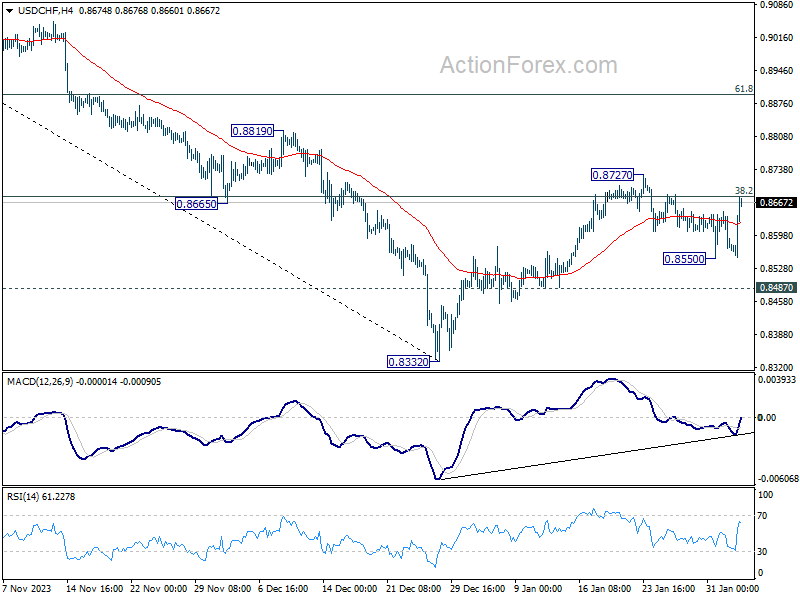

USD/CHF dipped further to 0.8550 last week but recovered since then. Initial bias remains neutral this week first On the upside, above 0.8727 will resume the rebound from 0.8332, and target 61.8% retracement of 0.9243 to 0.8332 at 0.8995. On the downside, below 0.8550 will resume the fall from 0.8727 for 0.8487 support.

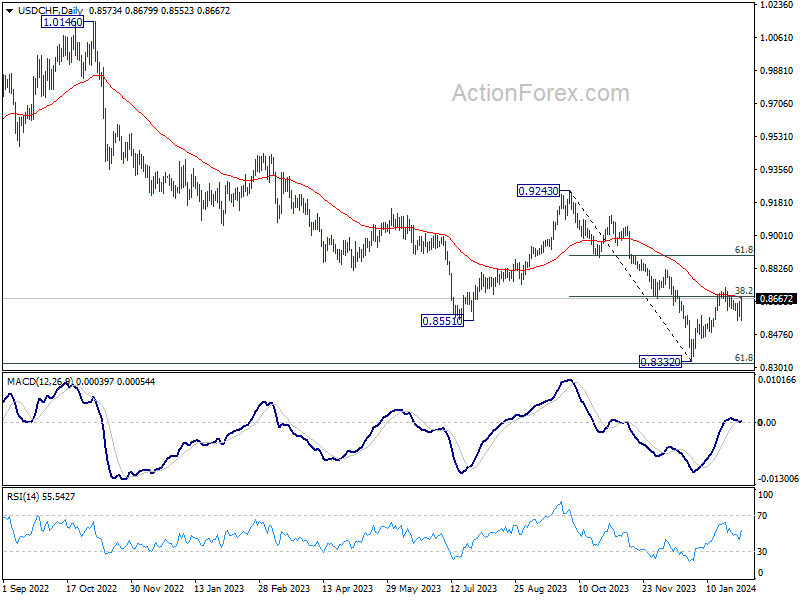

In the bigger picture, there is prospect of medium term bottoming at 0.8332 considering possible bullish convergence condition in W MACD, and the support from 0.8317 long term fibonacci support. Sustained trading above 55 D EMA (now at 0.8672) will affirm this case, and bring stronger rise back towards 0.9243 resistance, even as a corrective move.

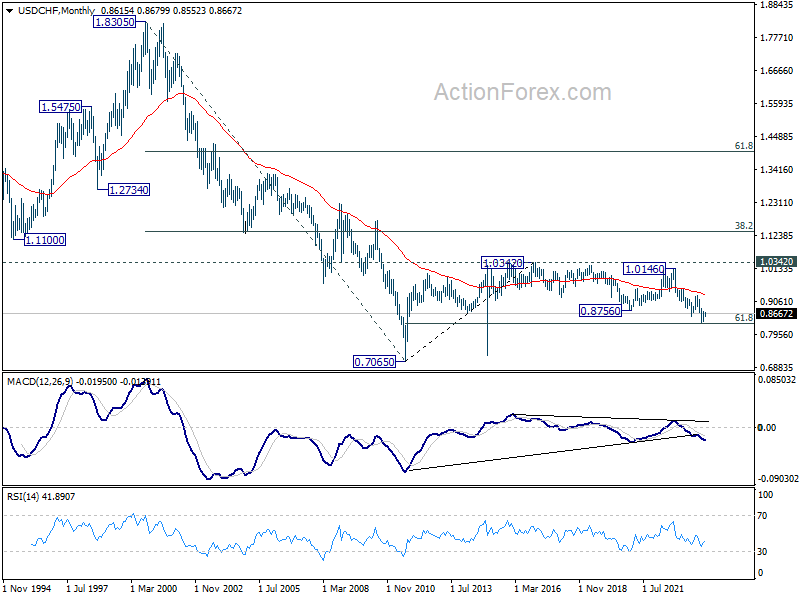

In the long term picture, price action from 0.7065 (2011 high) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high) . Strong rebound from 61.8% retracement of 0.7065 to 1.0342 (2016 high) will start the third leg as a medium term rally. But there will be no sign of long term reversal until firm break of 38.2% retracement of 1.8305 to 0.7065 at 1.1359.

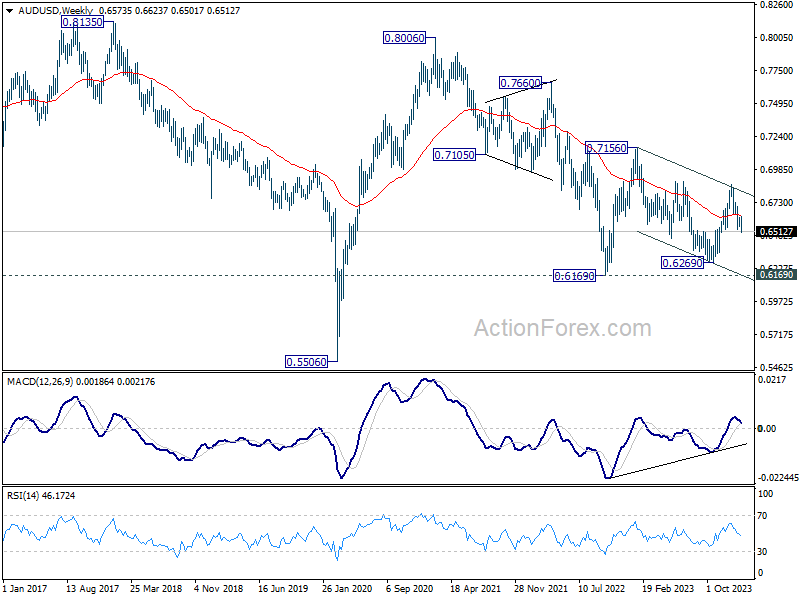

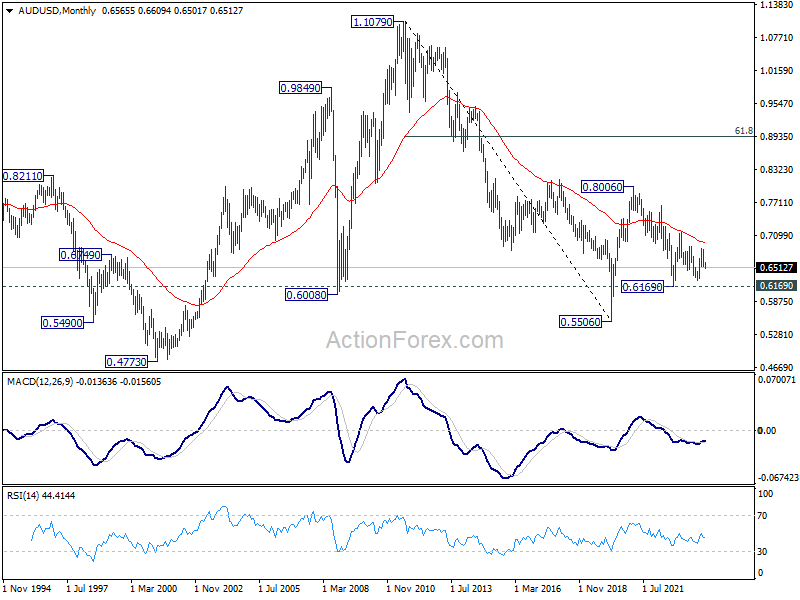

AUD/USD Weekly Report

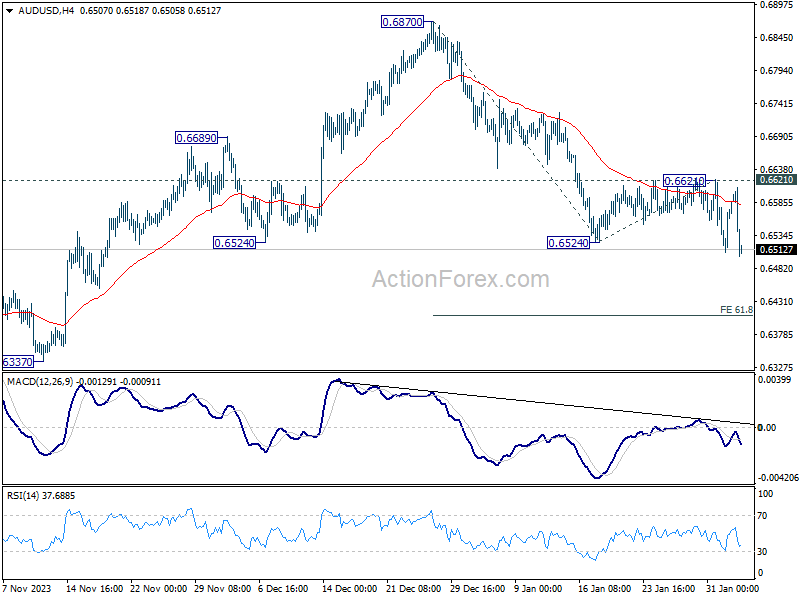

AUD/USD's decline from 0.6870 resumed last week and edged lower to 0.6501. Initial bias is now on the downside for 61.8% projection of 0.6870 to 0.6524 from 0.6621 at 0.6407. On the upside, break of 0.6621 resistance is needed to signal short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which might still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

In the long term picture, the down trend from 1.1079 (2011 high) should have completed at 0.5506 (2020 low) already. It's unsure yet whether price actions from 0.5506 are developing into a corrective pattern, or trend reversal. But in either case, fall from 0.8006 is seen the second leg of the pattern. Hence, in case of deeper decline, strong support should emerge above 0.5506 to bring reversal.

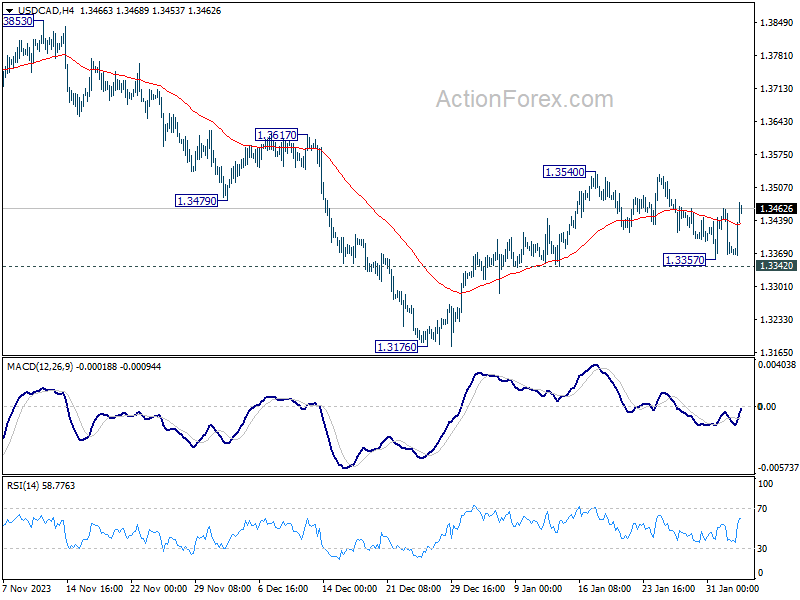

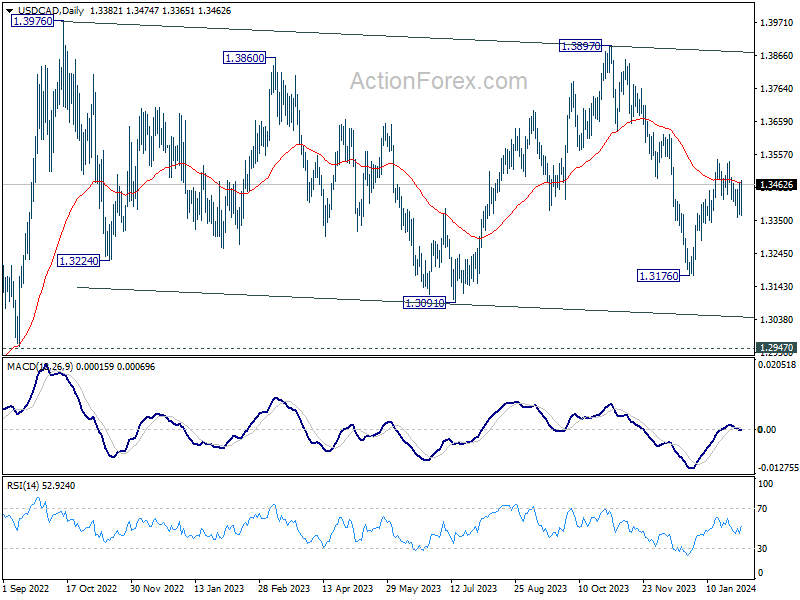

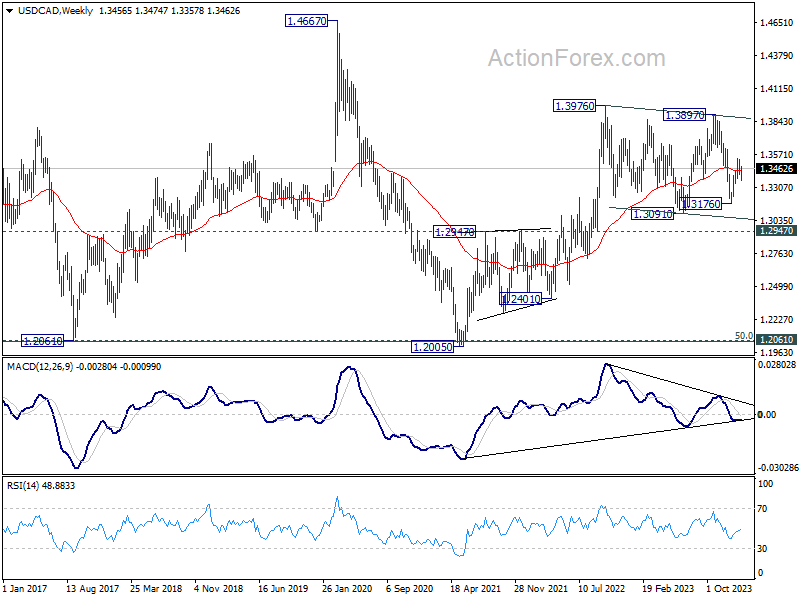

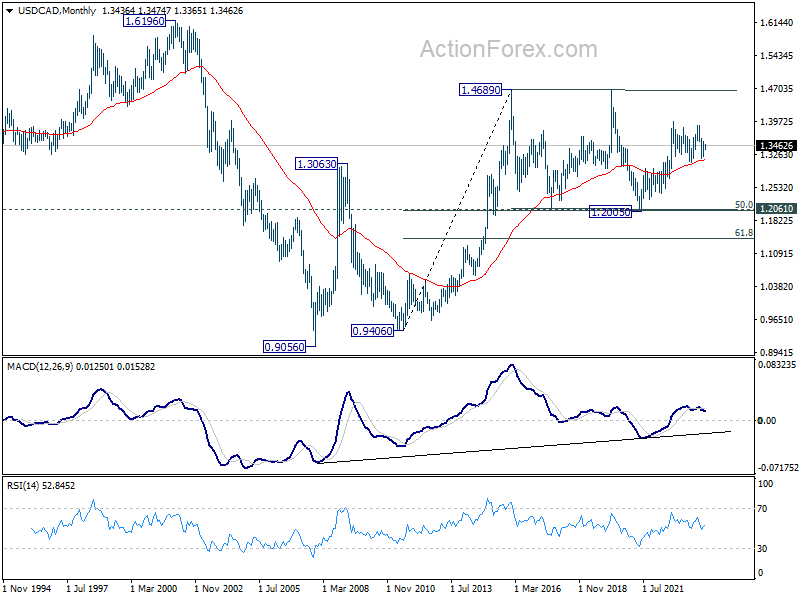

USD/CAD Weekly Outlook

USD/CAD's correction from 1.3540 extended lower to 1.3357 last week but recovered since then. Initial bias stays neutral this week first. On the upside, break of 1.3540 will resume the rise from 1.3176. That will also revive that case that whole fall from 1.3897 has completed. Nevertheless, firm break of 1.3342 support will argue that rebound from 1.3176 has completed at 1.3540, and target this low for resuming whole fall from 1.3897.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

In the longer term picture, price actions from 1.4689 (2016 high) are seen as a consolidation pattern, which might have completed at 1.2005. That is, up trend from 0.9506 (2007 low) is expected to resume at a later stage. This will remain the favored case as long as 1.2947 resistance turned support holds.

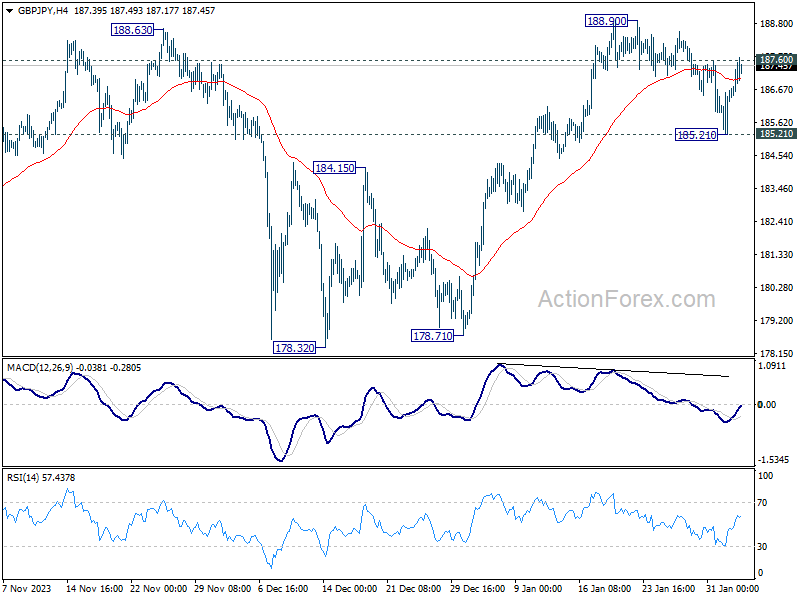

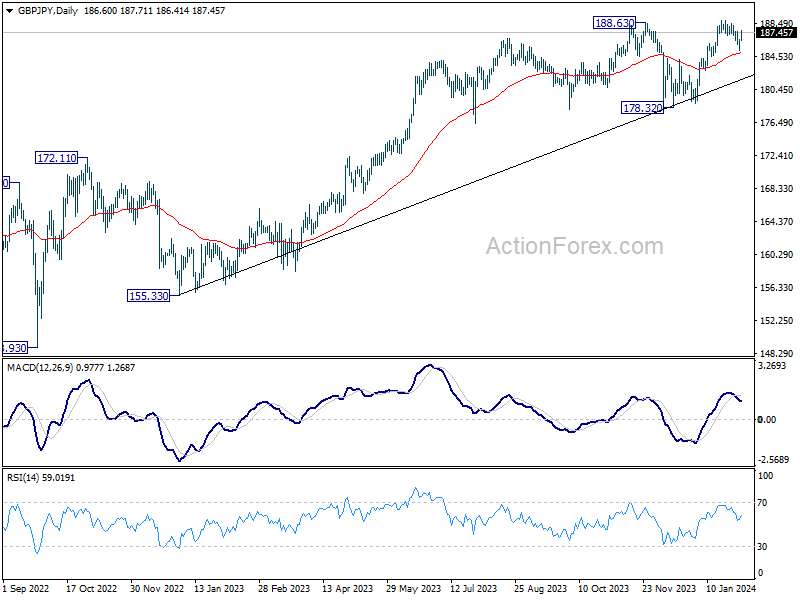

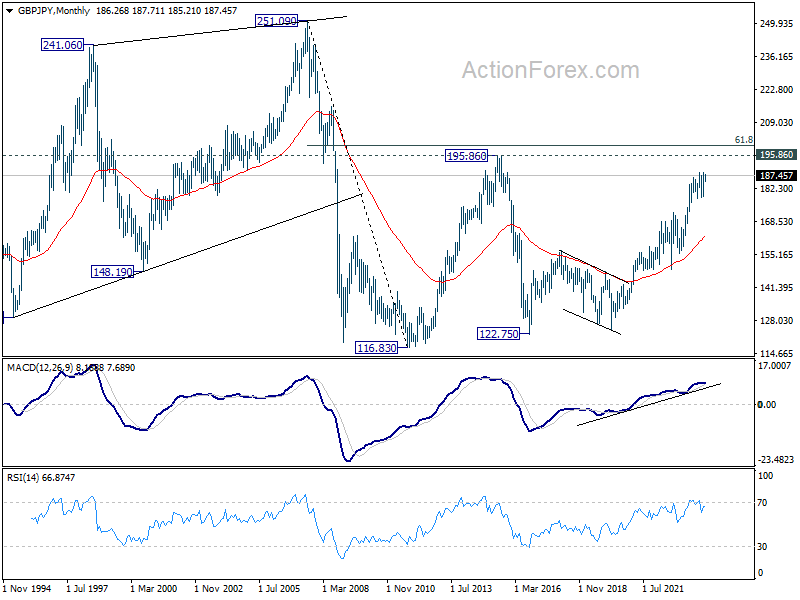

GBP/JPY Weekly Outlook

GBP/JPY's pull back from 188.90 extended to 185.21 last week but recovered since then. Initial bias remains neutral this week first. Firm break of 187.60 will turn bias to the upside for 188.90. Break there will confirm resumption of larger up trend. Meanwhile, below 185.21 will turn bias to the downside and extend the correction from 188.90.

In the bigger picture, up trend from 123.94 (2020 low) in in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

In the longer term picture, rise from 122.75 (2016 low) in still in progress despite loss of upside momentum as seen in W MACD. Further rise will remain in favor, as long as 172.11 support holds, to retest 195.86 (2015 high).

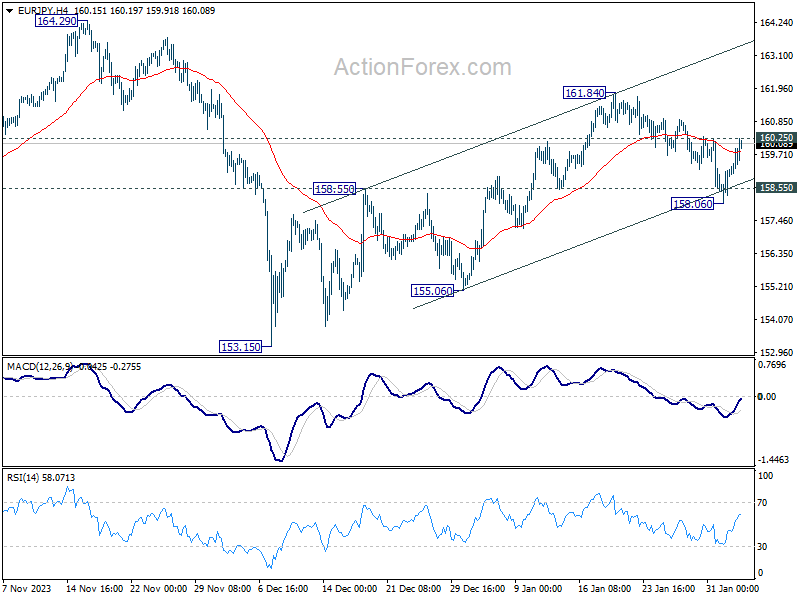

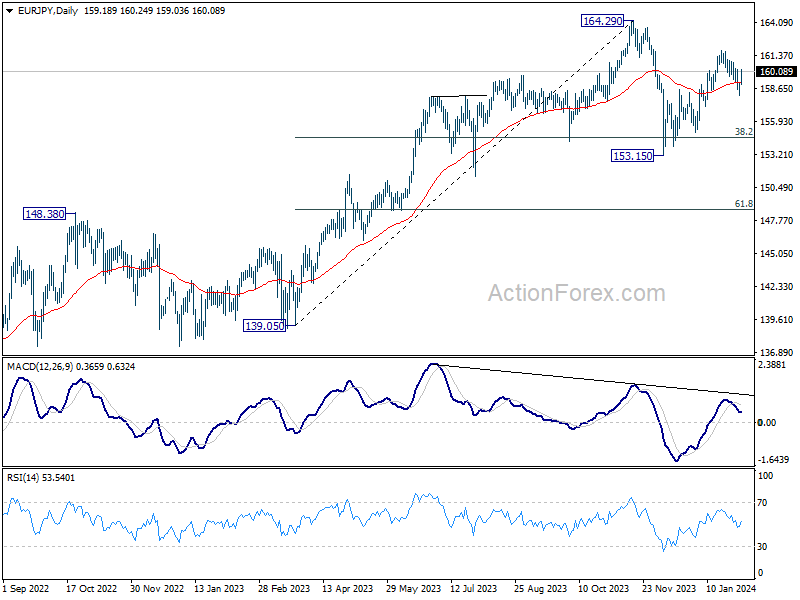

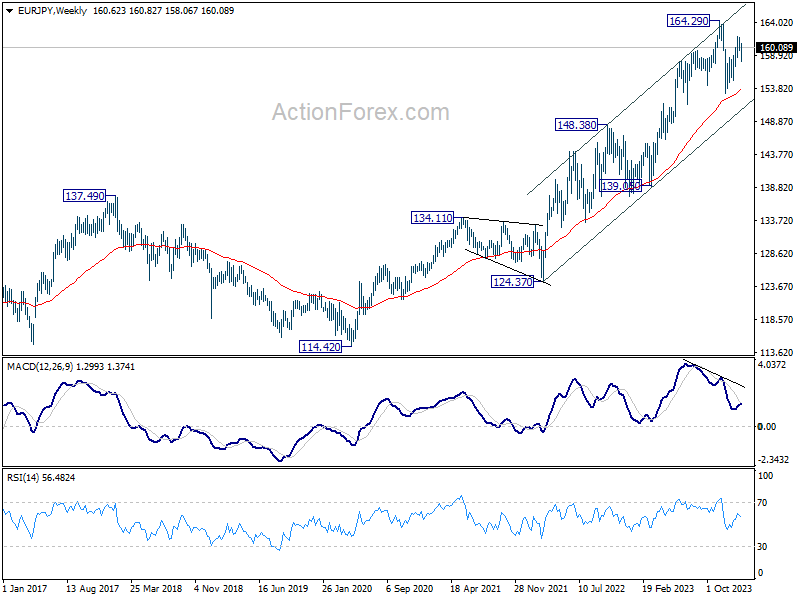

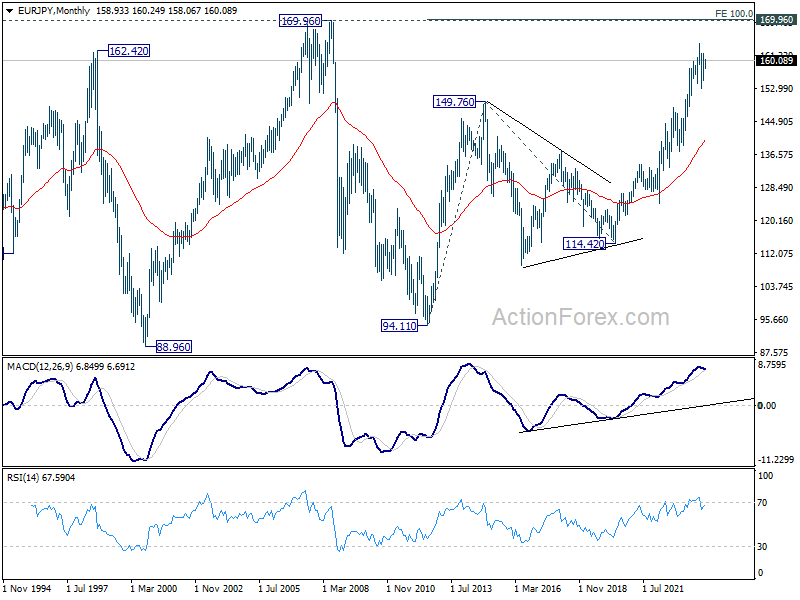

EUR/JPY Weekly Outlook

While EUR/JPY's correction from 161.84 extended to 158.06, it drew some support from 158.55 and near term rising channel and rebounded. Initial bias remains neutral this week first. On the upside, firm break of 160.25 will indicate that rise from 153.15 is ready to resume, and turn bias back to the upside for 161.84 first. Nevertheless, break of 158.06 will now suggest that the rise from 153.15 has completed and turn bias back to the downside.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 only. As long as 148.38 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage.

In the long term picture, rise from 114.42 (2020 low) is seen as the third leg of the whole up trend from 94.11 (2012 low). Next target is 100% projection of 94.11 to 149.76 from 114.42 at 170.07 which is close to 169.96 (2008 high). This will remain the favored case as long as 148.38 resistance turned support holds.

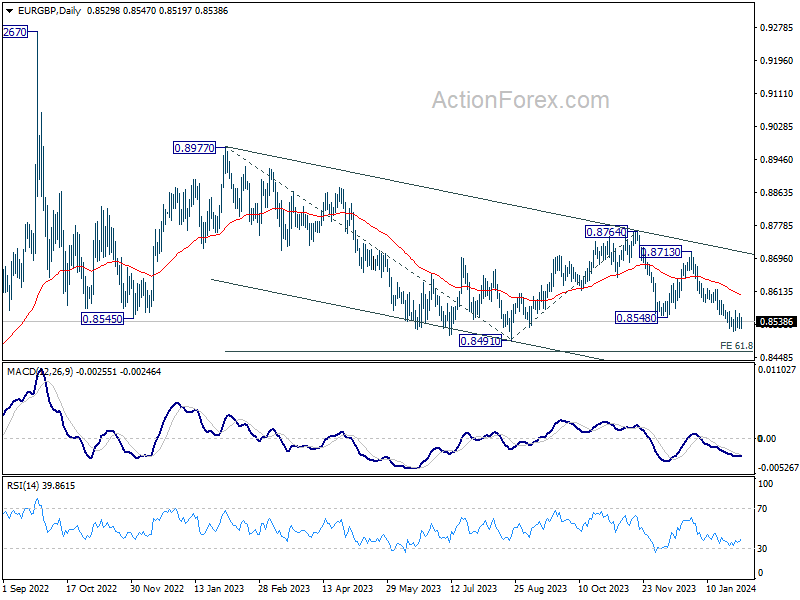

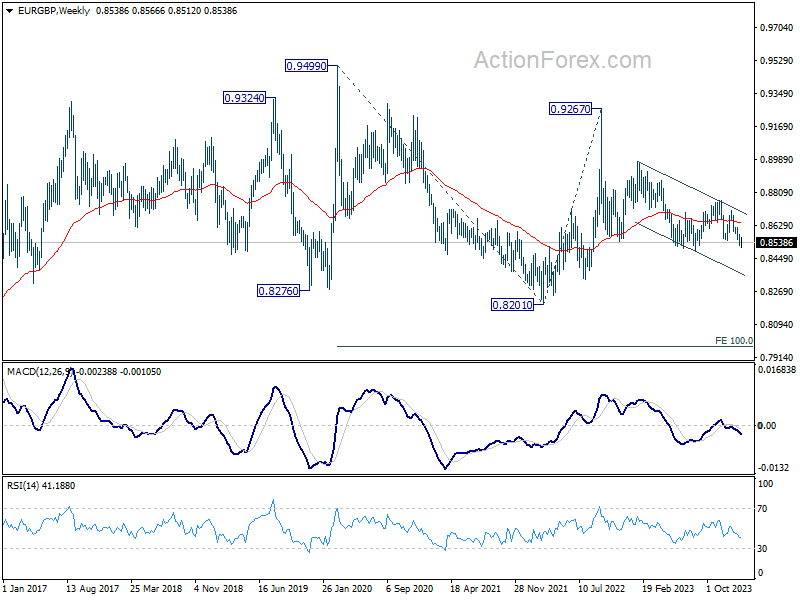

EUR/GBP Weekly Outlook

EUR/GBP edged lower to 0.8512 last week but recovered since then. Initial bias remains neutral this week for some more consolidations. But near term outlook will stay bearish as long as 0.8591 resistance holds. Below 0.8512 will resume the decline from 0.8713 to 0.8491, and then 0.8464 projection level. However, firm break of 0.8591 will turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

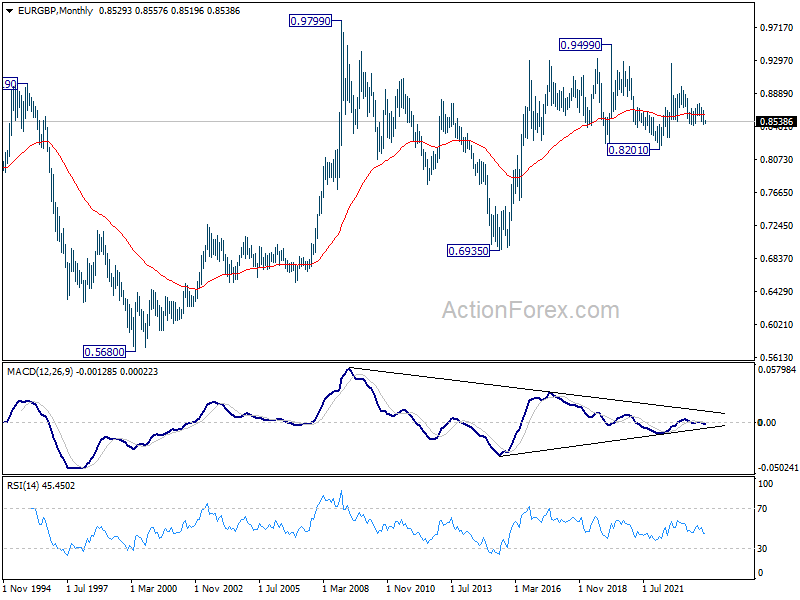

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Fall from 0.9267 is the third leg of the pattern from 0.9499. Break of 0.8201 (2022 low) will target 100% projection of 0.9499 to 0.8201 from 0.9267 at 0.7969.

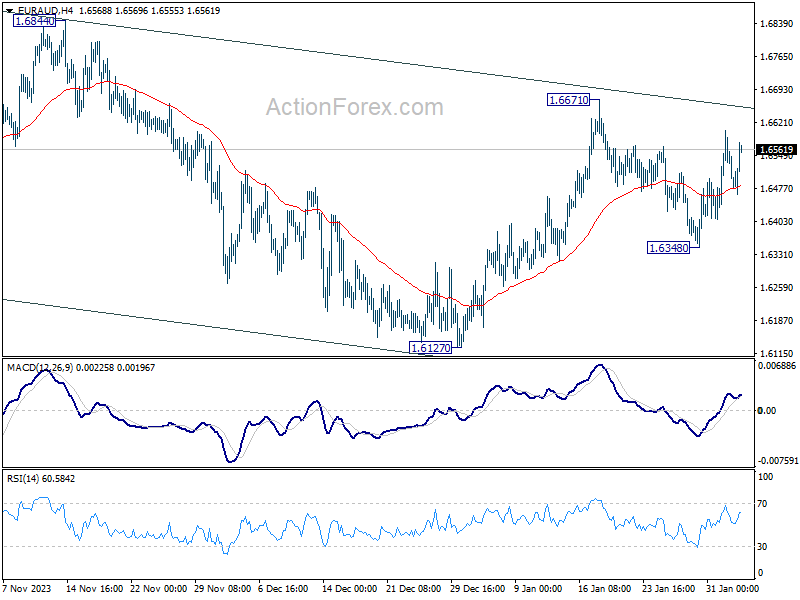

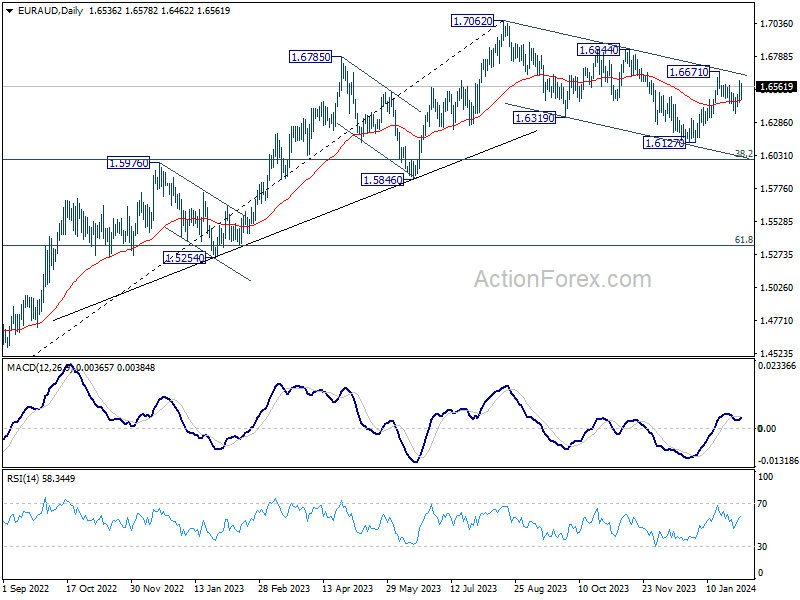

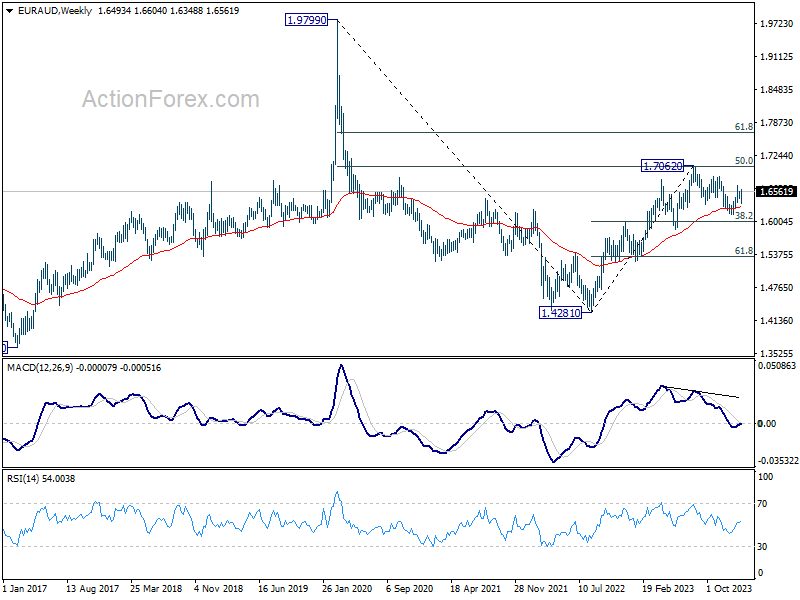

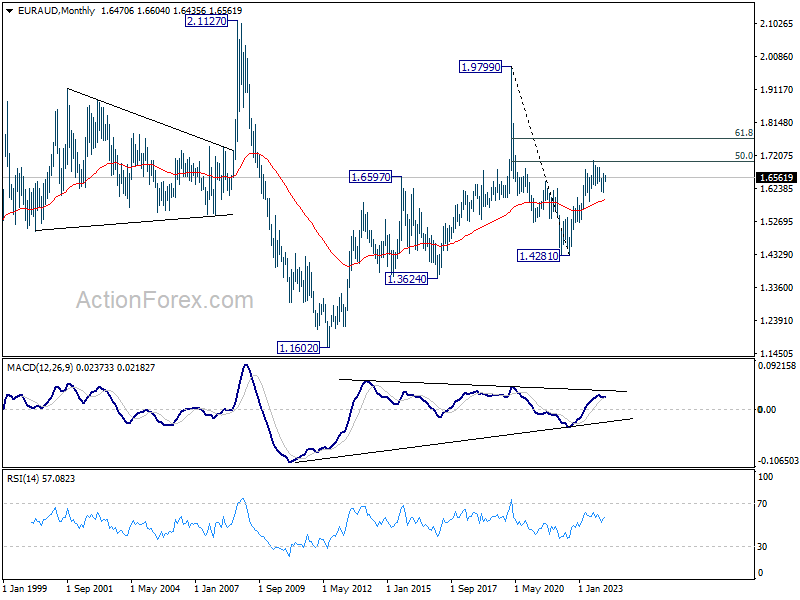

EUR/AUD Weekly Outlook

EUR/AUD's pull back from 1.6671 extended to as low as 1.6348 last week but rebounded since then. Initial bias remains neutral this week first. On the upside, decisive break of 1.6671 will revive the case that whole correction from 1.7062 has completed with three waves down to 1.6127. Further rally should then be seen to 1.6844 resistance for confirmation. Nevertheless, break of 1.6438 will bring deeper fall back to 1.6127 support instead.

In the bigger picture, fall from 1.7062 medium term top is seen as correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

In the longer term picture, price actions from 1.9799 (2020 high) are seen as a long term decline at the same scale as the rise from 1.1602 (2012 low). Rebound from 1.4281 is seen as the second leg. As long as 55 M EMA (now at 1.5905) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

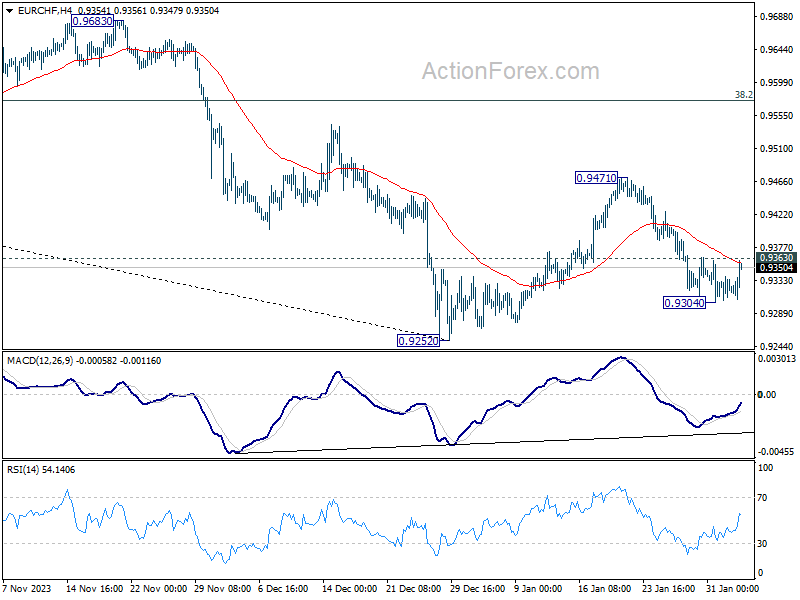

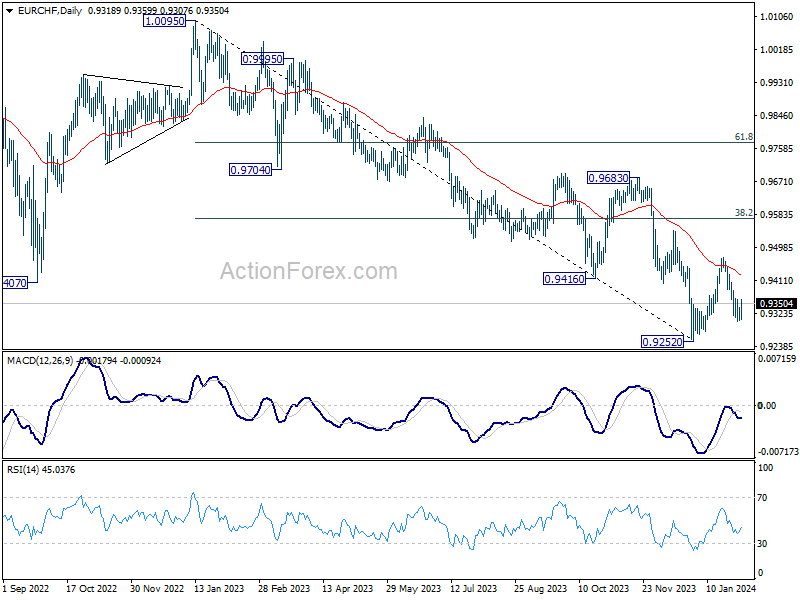

EUR/CHF Weekly Outlook

EUR/CHF's pull backed from 0.9471 continued last week but lost momentum and turned sideway after hitting 0.9304. Initial bias remains neutral this week first. While another decline cannot be ruled out, downside should be contained above 0.9252 low to bring rebound. On the upside, firm break of 0.9363 minor resistance will argue that the correction has completed, and turn bias back to the upside for 0.9471 first.

In the bigger picture, price actions from 0.9252 are tentatively seen as a correction to the five-wave down trend from 1.0095 (2023 high). Further rise would be seen to 38.2% retracement of 1.0095 to 0.9252 at 0.9574. But overall medium term outlook will remain bearish as long as 0.9683 resistance holds.

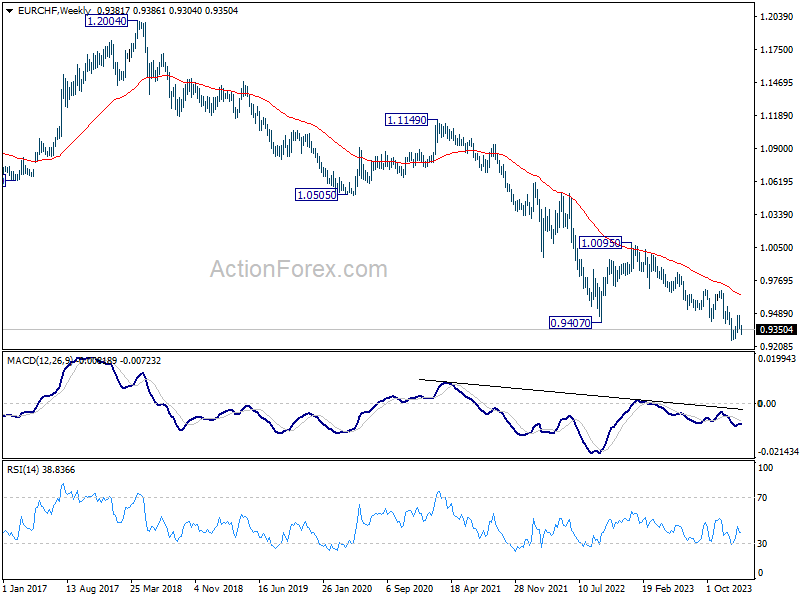

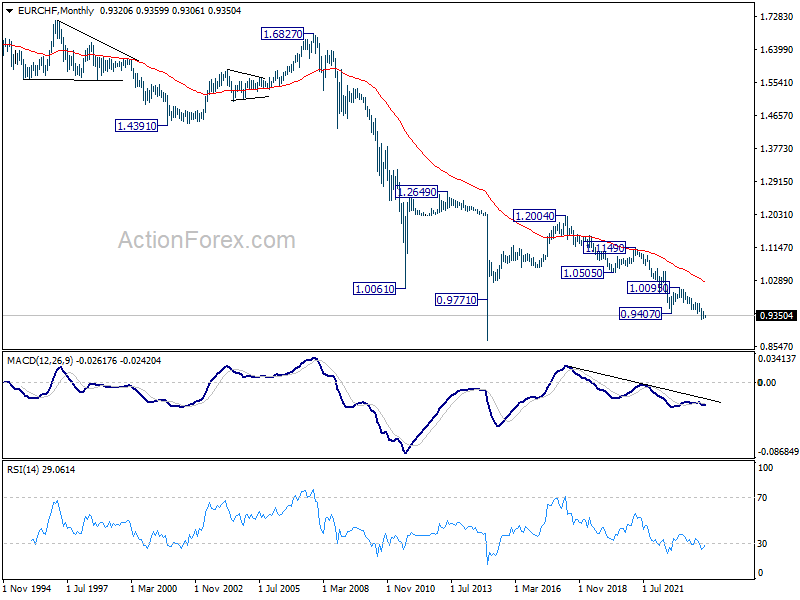

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Firm break of 1.0095 resistance is needed to be the first sign of long term bottoming. Otherwise, outlook will remain bearish.

Summary 2/5 – 2/9

Monday, Feb 5, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | AUD | TD Securities Inflation M/M Jan | 1.00% | |

| 00:30 | AUD | Goods Trade Balance (AUD) Jan | 10.50B | 11.44B |

| 01:45 | CNY | Caixin Services PMI Jan | 52.7 | 52.9 |

| 07:00 | EUR | Germany Trade Balance (EUR) Dec | 22.3B | 20.4B |

| 08:45 | EUR | Italy Services PMI Jan | 50.8 | 49.8 |

| 08:50 | EUR | France Services PMI Jan F | 45 | 45 |

| 08:55 | EUR | Germany Services PMI Jan F | 47.6 | 47.6 |

| 09:00 | EUR | Eurozone Services PMI Jan F | 48.4 | 48.4 |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Feb | -15 | -15.8 |

| 09:30 | GBP | Services PMI JanF | 53.8 | 53.8 |

| 10:00 | EUR | Eurozone PPI M/M Dec | -0.20% | -0.30% |

| 10:00 | EUR | Eurozone PPI Y/Y Dec | -8.80% | |

| 14:45 | USD | Services PMI Jan F | 52.9 | 52.9 |

| 15:00 | USD | ISM Services PMI Jan | 52.1 | 50.6 |

| 23:30 | JPY | Labor Cash Earnings Y/Y Dec | 1.30% | 0.70% |

| 23:30 | JPY | Household Spending Y/Y Dec | -2.10% | -2.90% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | AUD | TD Securities Inflation M/M Jan | |

| Forecast: | Previous: 1.00% | ||

| 00:30 | AUD | Goods Trade Balance (AUD) Jan | |

| Forecast: 10.50B | Previous: 11.44B | ||

| 01:45 | CNY | Caixin Services PMI Jan | |

| Forecast: 52.7 | Previous: 52.9 | ||

| 07:00 | EUR | Germany Trade Balance (EUR) Dec | |

| Forecast: 22.3B | Previous: 20.4B | ||

| 08:45 | EUR | Italy Services PMI Jan | |

| Forecast: 50.8 | Previous: 49.8 | ||

| 08:50 | EUR | France Services PMI Jan F | |

| Forecast: 45 | Previous: 45 | ||

| 08:55 | EUR | Germany Services PMI Jan F | |

| Forecast: 47.6 | Previous: 47.6 | ||

| 09:00 | EUR | Eurozone Services PMI Jan F | |

| Forecast: 48.4 | Previous: 48.4 | ||

| 09:30 | EUR | Eurozone Sentix Investor Confidence Feb | |

| Forecast: -15 | Previous: -15.8 | ||

| 09:30 | GBP | Services PMI JanF | |

| Forecast: 53.8 | Previous: 53.8 | ||

| 10:00 | EUR | Eurozone PPI M/M Dec | |

| Forecast: -0.20% | Previous: -0.30% | ||

| 10:00 | EUR | Eurozone PPI Y/Y Dec | |

| Forecast: | Previous: -8.80% | ||

| 14:45 | USD | Services PMI Jan F | |

| Forecast: 52.9 | Previous: 52.9 | ||

| 15:00 | USD | ISM Services PMI Jan | |

| Forecast: 52.1 | Previous: 50.6 | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Dec | |

| Forecast: 1.30% | Previous: 0.70% | ||

| 23:30 | JPY | Household Spending Y/Y Dec | |

| Forecast: -2.10% | Previous: -2.90% | ||

Tuesday, Feb 6, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 03:30 | AUD | RBA Interest Rate Decision | 4.35% | 4.35% |

| 04:30 | AUD | RBA Press Conference | ||

| 07:00 | EUR | Germany Factory Orders M/M Dec | 0.30% | 0.30% |

| 09:30 | GBP | Construction PMI Jan | 47.2 | 46.8 |

| 10:00 | EUR | Eurozone Retail Sales M/M Dec | -1.30% | -0.30% |

| 13:30 | CAD | Building Permits M/M Dec | 1.20% | -3.90% |

| 15:00 | CAD | Ivey PMI Jan | 55 | 56.3 |

| 21:45 | NZD | Employment Change Q4 | 0.30% | -0.20% |

| 21:45 | NZD | Unemployment Rate Q4 | 4.30% | 3.90% |

| 21:45 | NZD | Labour Cost Index Q/Q Q4 | 0.80% | 0.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 03:30 | AUD | RBA Interest Rate Decision | |

| Forecast: 4.35% | Previous: 4.35% | ||

| 04:30 | AUD | RBA Press Conference | |

| Forecast: | Previous: | ||

| 07:00 | EUR | Germany Factory Orders M/M Dec | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 09:30 | GBP | Construction PMI Jan | |

| Forecast: 47.2 | Previous: 46.8 | ||

| 10:00 | EUR | Eurozone Retail Sales M/M Dec | |

| Forecast: -1.30% | Previous: -0.30% | ||

| 13:30 | CAD | Building Permits M/M Dec | |

| Forecast: 1.20% | Previous: -3.90% | ||

| 15:00 | CAD | Ivey PMI Jan | |

| Forecast: 55 | Previous: 56.3 | ||

| 21:45 | NZD | Employment Change Q4 | |

| Forecast: 0.30% | Previous: -0.20% | ||

| 21:45 | NZD | Unemployment Rate Q4 | |

| Forecast: 4.30% | Previous: 3.90% | ||

| 21:45 | NZD | Labour Cost Index Q/Q Q4 | |

| Forecast: 0.80% | Previous: 0.80% | ||

Wednesday, Feb 7, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Dec P | 109.5 | 107.6 |

| 06:45 | CHF | Unemployment Rate M/M Jan | 2.20% | 2.20% |

| 07:00 | EUR | Germany Industrial Production M/M Dec | -0.20% | -0.70% |

| 07:45 | EUR | France Trade Balance (EUR) Dec | -6.0B | -5.9B |

| 08:00 | CHF | Foreign Currency Reserves (CHF) Jan | 654B | |

| 09:00 | EUR | Italy Retail Sales M/M Dec | 0.20% | 0.40% |

| 13:30 | USD | Trade Balance (USD) Dec | -62.3B | -63.2B |

| 13:30 | CAD | Trade Balance (CAD) Dec | 1.1B | 1.6B |

| 15:30 | USD | Crude Oil Inventories | 1.2M | |

| 18:30 | CAD | BoC Summary of Deliberations | ||

| 23:50 | JPY | Bank Lending Y/Y Jan | 3.20% | 3.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Dec P | |

| Forecast: 109.5 | Previous: 107.6 | ||

| 06:45 | CHF | Unemployment Rate M/M Jan | |

| Forecast: 2.20% | Previous: 2.20% | ||

| 07:00 | EUR | Germany Industrial Production M/M Dec | |

| Forecast: -0.20% | Previous: -0.70% | ||

| 07:45 | EUR | France Trade Balance (EUR) Dec | |

| Forecast: -6.0B | Previous: -5.9B | ||

| 08:00 | CHF | Foreign Currency Reserves (CHF) Jan | |

| Forecast: | Previous: 654B | ||

| 09:00 | EUR | Italy Retail Sales M/M Dec | |

| Forecast: 0.20% | Previous: 0.40% | ||

| 13:30 | USD | Trade Balance (USD) Dec | |

| Forecast: -62.3B | Previous: -63.2B | ||

| 13:30 | CAD | Trade Balance (CAD) Dec | |

| Forecast: 1.1B | Previous: 1.6B | ||

| 15:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 1.2M | ||

| 18:30 | CAD | BoC Summary of Deliberations | |

| Forecast: | Previous: | ||

| 23:50 | JPY | Bank Lending Y/Y Jan | |

| Forecast: 3.20% | Previous: 3.10% | ||

Thursday, Feb 8, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:01 | GBP | RICS Housing Price Balance Jan | -28% | -30% |

| 01:30 | CNY | CPI Y/Y Jan | -0.50% | -0.30% |

| 01:30 | CNY | PPI Y/Y Jan | -2.60% | -2.70% |

| 05:00 | JPY | Eco Watchers Survey: Current Jan | 50.3 | 50.7 |

| 09:00 | EUR | ECB Economic Bulletin | ||

| 13:30 | USD | Initial Jobless Claims (Feb 2) | 220K | 224K |

| 13:30 | CZ | CNB Interest Rate Decision | 6.75% | |

| 15:00 | USD | Wholesale Inventories Dec F | 0.40% | 0.40% |

| 15:30 | USD | Natural Gas Storage | -197B | |

| 23:50 | JPY | Money Supply M2+CD Y/Y Jan | 2.20% | 2.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:01 | GBP | RICS Housing Price Balance Jan | |

| Forecast: -28% | Previous: -30% | ||

| 01:30 | CNY | CPI Y/Y Jan | |

| Forecast: -0.50% | Previous: -0.30% | ||

| 01:30 | CNY | PPI Y/Y Jan | |

| Forecast: -2.60% | Previous: -2.70% | ||

| 05:00 | JPY | Eco Watchers Survey: Current Jan | |

| Forecast: 50.3 | Previous: 50.7 | ||

| 09:00 | EUR | ECB Economic Bulletin | |

| Forecast: | Previous: | ||

| 13:30 | USD | Initial Jobless Claims (Feb 2) | |

| Forecast: 220K | Previous: 224K | ||

| 13:30 | CZ | CNB Interest Rate Decision | |

| Forecast: | Previous: 6.75% | ||

| 15:00 | USD | Wholesale Inventories Dec F | |

| Forecast: 0.40% | Previous: 0.40% | ||

| 15:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: -197B | ||

| 23:50 | JPY | Money Supply M2+CD Y/Y Jan | |

| Forecast: 2.20% | Previous: 2.30% | ||

Friday, Feb 9, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 07:00 | EUR | Germany CPI M/M Jan F | 0.20% | 0.20% |

| 07:00 | EUR | Germany CPI Y/Y Jan F | 2.90% | 2.90% |

| 09:00 | EUR | Italy Industrial Output M/M Dec | 0.50% | -1.50% |

| 13:30 | CAD | Net Change in Employment Jan | 15.0K | 0.1K |

| 13:30 | CAD | Unemployment Rate Jan | 5.90% | 5.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 07:00 | EUR | Germany CPI M/M Jan F | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 07:00 | EUR | Germany CPI Y/Y Jan F | |

| Forecast: 2.90% | Previous: 2.90% | ||

| 09:00 | EUR | Italy Industrial Output M/M Dec | |

| Forecast: 0.50% | Previous: -1.50% | ||

| 13:30 | CAD | Net Change in Employment Jan | |

| Forecast: 15.0K | Previous: 0.1K | ||

| 13:30 | CAD | Unemployment Rate Jan | |

| Forecast: 5.90% | Previous: 5.80% | ||

The Weekly Bottom Line: Resilient Labor Demand and A Patient Fed

U.S. Highlights

- The Federal Reserve opted to hold rates steady in their first decision of the year in order to give themselves more time to assess the sustainability of current disinflation trends.

- Employment gains in January nearly doubled expectations as strong upward revisions to December carried forward into 2024.

- U.S. Treasury markets experienced volatility this week as a decline in yields prompted by a dovish interpretation of Wednesday’s Federal Reserve decision was reversed by stronger than expected employment data on Friday.

Canadian Highlights

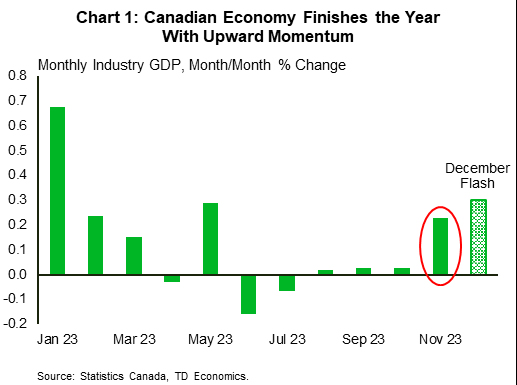

- Canadian GDP growth appears to have ended 2023 on a stronger footing than previously expected, according to Statistics Canada’s preliminary monthly GDP estimates.

- The Bank of Canada (BoC) will keep an eye on growth trends while managing sticky underlying inflation pressures. A rate cut by June is not off the table, but recent developments risk pushing the cut further down the line.

- Updated jobs data for January will be the key release next week. We expect a modest employment gain to be met with a larger gain in labour supply.

U.S. – Resilient Labor Demand and A Patient Fed

January ended with a big week for economic data, including the first Federal Reserve decision of the year and the first employment data reading. While the Fed’s statement dropped any tightening bias, Chair Powell’s press conference curtailed market hopes for a near-term pivot to less restrictive monetary policy. This saw Treasury yields fall steeply after the meeting. However, this descent was ultimately short-lived, as much stronger than expected employment data on Friday sent yields higher. At time of writing, the ten-year Treasury yield was 12 basis-points lower on the week.

Overall, the messaging from the Federal Reserve on Wednesday was positive. Chair Powell stated that the committee was pleased by the progress made thus far on returning inflation to their 2% target, but noted that they would require more time to assess the sustainability of current disinflation trends (Chart 1). With economic growth accelerating last year on the back of strong consumption growth, the labor market remaining solid, and geopolitical tensions posing challenges to supply chains (and hence inflation), caution is likely wise. Chair Powell also stated that he viewed it as unlikely that the FOMC would possess the confidence to reduce interest rates by the March meeting in six week’s time.

Powell’s caution was further validated when we received the January employment data on Friday. Not only did we see a very strong 353k jobs added in the first month of the year, but last year’s total job gains were also revised up to 3.1 million, well above the prior reading for 2.7 million, with much of the revised strength coming through the second half of the year (Chart 2). Furthermore, wage growth appears to be accelerating, with the three-month annualized change in average hourly wages rising to a twenty-month high in January. Although near-term strength in the labor market is expected to recede over the coming months, sustained imbalances in the labor market is a risk that the Fed is acutely aware of.

Elsewhere this week, the ISM Manufacturing Purchasing Managers’ Index (PMI) showed that industrial activity continued to contract in January, but by less than expected. Elevated interest rates continue to weigh on the sector, but demand has begun to show signs of improvement, which has stabilized aggregate production output. Forward pricing in financial markets for the eventual decline in interest rates expected this year will likely provide relief to the manufacturing sector moving forward as the demand for goods improves.

The lingering question, however, is when will the Federal Reserve begin to drawdown interest rates? Markets have broadly abandoned their hopes for a March cut after this week, with May now being the expected timeline with about 80% probability as of the time of writing. Upcoming data will likely provide greater clarity on the timing of the introduction of less restrictive monetary policy, including a 60 Minutes interview with Chair Powell on Sunday and the Federal Reserve Senior Loan Officer Opinion Survey on Monday.

Canada – Welcome Back Growth

Canadian markets likely took their cue from events south of the border this week, with a light domestic data calendar. The 2-Year Canada yield finished the week flat while the 10-Year yield slipped around 10 bps. The Loonie's early-week gains were erased on Friday, finishing the week flat at 0.7420. On the data front, the lone GDP update for November printed at 0.2% month-on-month (m/m), exceeding Statistics Canada's initial guidance and market expectations. What's more, the flash estimate for December GDP growth was a sturdy 0.3% m/m, which would mark the hottest growth reading since May.

It has been several months since Canada's economy has recorded any meaningful growth. In fact, between Jun.–Oct. 2023, real GDP flatlined (Chart 1). Not a bad outcome given the current interest rate environment, but still evidence that output was hitting a wall. This week's update poured cold water on the idea that the economy is completely out of steam. We are hesitant to call this a newly emerging growth trend, but it would be remiss to ignore it.

There is clearly some degree of underlying strength in Canada's economy despite the turbulent second and third quarter this year. Strength in this sense is relative. GDP for Q4-2023 is tracking above expectations, around 1.2% quarter-on-quarter (q/q) annualized, but still below trend-growth. A range of indicators however, namely housing sales, retail spending and manufacturing, have showed a pulse in recent months. These fresh GDP readings also introduce upside risk to the BoC's growth projection in last week's Monetary Policy Report (MPR), which now pegs fourth quarter growth at 0%, down from their 0.8% projection in October.

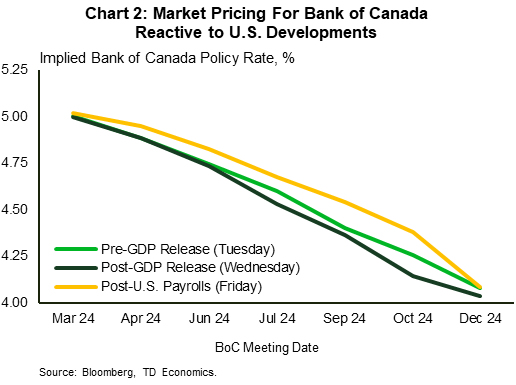

The BoC is now forced to divert some attention back to growth while trying to manage underlying inflation pressures. The ultimate focus for the BoC is to get inflation back to their 2% target, and they have reiterated that they believe trends in growth–and inflation– are headed in the right direction. The GDP release alone didn't move the needle on the market's expectations for a first Bank of Canada rate cut, but it appears hawkish data stateside did (Chart 2). At the time of writing, markets are pricing a 30% chance of a rate cut in April and an 80% probability assigned to June. Prior to U.S. payrolls, market expectations for a June cut were fully priced in.

Next week's main focus is job market updates for January. Encouragingly, the labour market is cooling and looks positioned to avoid a worst-case scenario. The pace of monthly job gains, notably in the private sector, has retreated in recent months while the unemployment rate grinds higher. Expect a modest gain in January employment to be met with stronger labour force growth, a theme that has been playing out for several months.