Sample Category Title

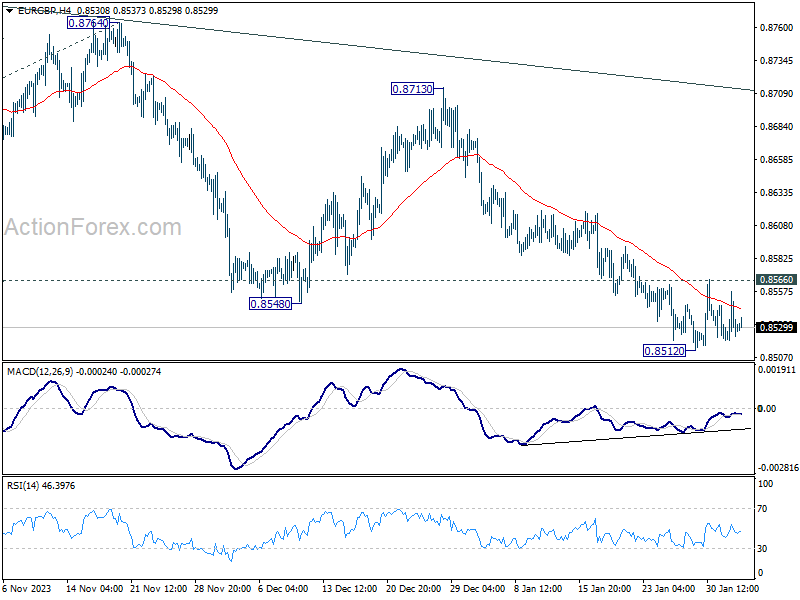

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8515; (P) 0.8537; (R1) 0.8553; More...

EUR/GBP is staying in tight range above 0.8512 and intraday bias remains neutral. On the downside, below 0.8521 will resume the fall from 0.8764 to retest 0.8491. Break there will extend larger down trend to 0.8464 projection level. On the upside, above 0.8566 minor resistance will suggest short term bottoming, on bullish convergence condition in 4H MACD. Intraday bias will be turned to the upside for stronger rebound to 55 D EMA (now at 0.8602).

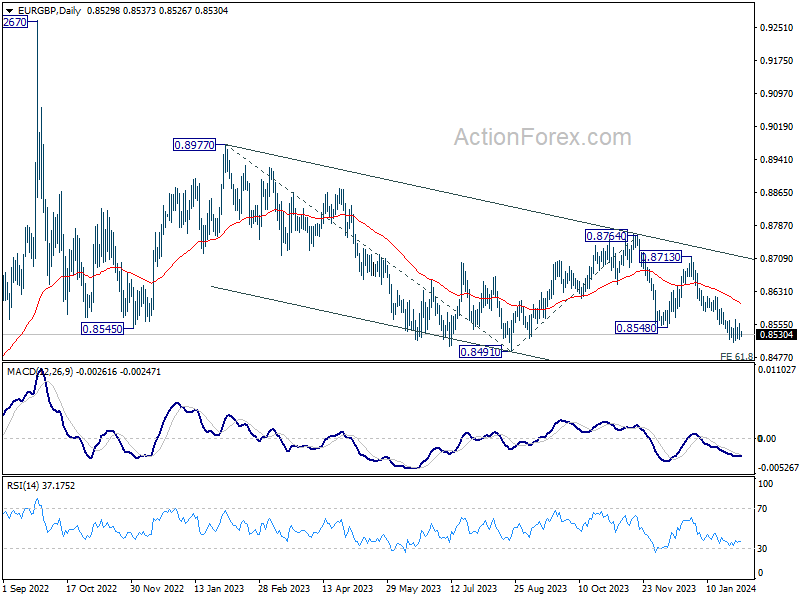

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

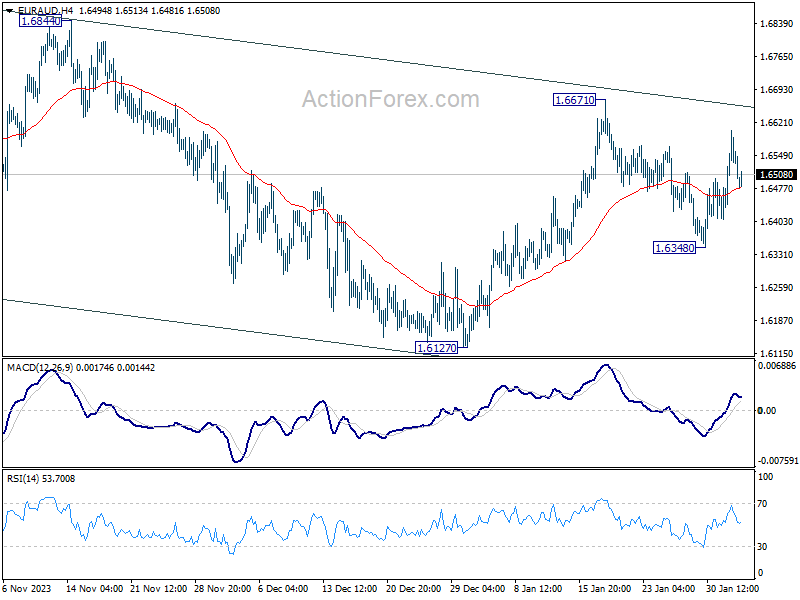

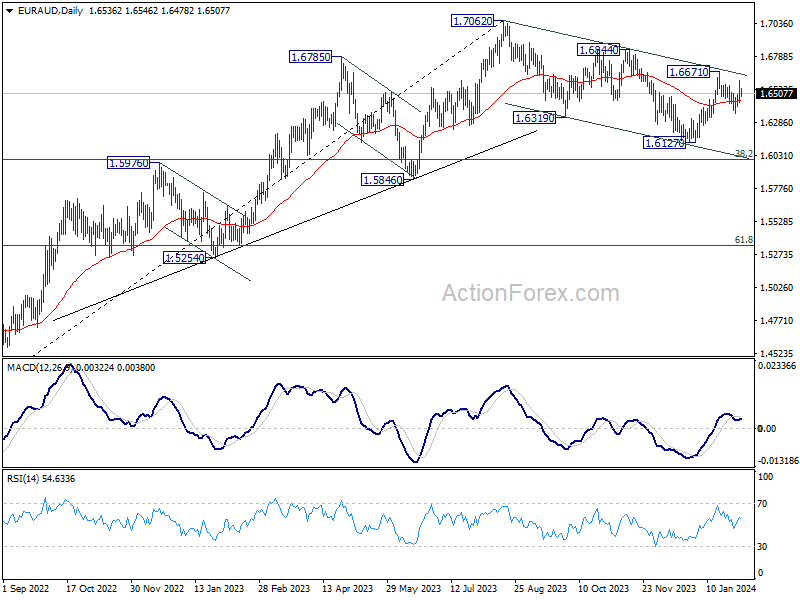

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6453; (P) 1.6529; (R1) 1.6621; More...

EUR/AUD failed to break through 1.6671 resistance and retreated sharply. Intraday bias is turned neutral again first. On the upside, decisive break of 1.6671 will revive the case that whole correction from 1.7062 has completed with three waves down to 1.6127. Further rally should then be seen to 1.6844 resistance for confirmation. Nevertheless, break of 1.6438 will bring deeper fall back to 1.6127 support instead.

In the bigger picture, fall from 1.7062 medium term top is seen as correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

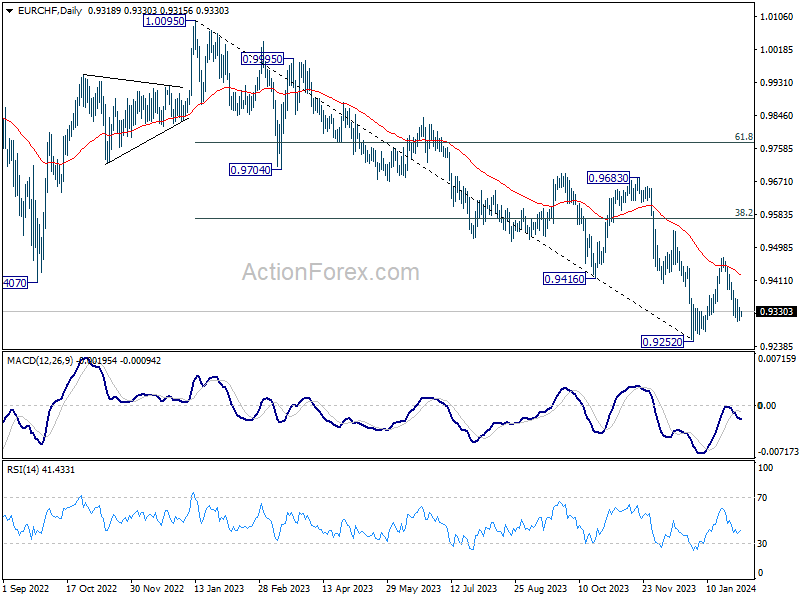

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9309; (P) 0.9325; (R1) 0.9342; More...

Further decline could be seen in EUR/CHF with 0.9363 minor resistance intact. But strong support is still expected above 0.9252 low to bring rebound. On the upside, above 0.9363 minor resistance will turn bias back to the upside. Further break of 0.9471 will resume the rebound from 0.9252 to 38.2% retracement of 1.0095 to 0.9252 at 0.9574.

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Current fall from 1.2004 (2018 high) is part of the multi-decade down trend. Another decline is in favor after rebound from 0.9252 completes. However, firm break of 0.9683, and sustained trading above 55 W EMA (now at 0.9638) will argue that EUR/CHF is already in a medium term rally, even as a corrective move.

GBP/USD: Poised for Potential Bullish Breakout Ex-post BoE

- BoE offered dovish guidance but projected that inflation may run hot again in Q1 2025.

- GBP has remained the top outperformer major currency against the US dollar.

- Technical analysis suggests a potential bullish breakout for GBP/USD.

The British pound sterling (GBP) made another remarkable intraday recovery yesterday after the Bank of England (BoE) maintained its policy Bank Rate at a 16-high of 5.24% for the fourth consecutive time as expected and toned down its prior hawkish rhetoric.

Interestingly for the first time since 2008, the Monetary Policy Committee members of BoE have voted for both rate cuts and hikes at the same meeting; 2 members voted for a hike (down from 3 in the prior meeting), 1 member voted for a cut (0 members voted for cut in the prior meeting), and six members voted for no change in rate.

A slightly dovish tilt from BoE but issued a lukewarm inflation forecast

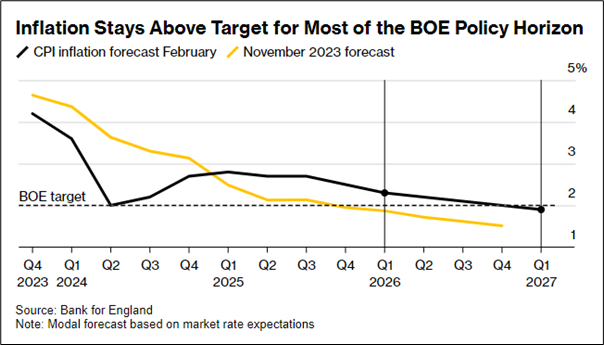

Fig 1: BoE inflation forecasts as of 2 Feb 2024 (Source: Bloomberg News, click to enlarge chart)

In addition, BoE Governor Bailey commented that inflation was moving in the right direction, interest rates would be kept “under review”, and dropped a previous warning that the Bank Rate could increase further due to the risk of inflationary pressure resurging.

Overall, the BoE has issued dovish guidance on its monetary policy, a first move away from its prior “staunch” hawkish view that inflationary pressures remain elevated, in line with the Fed and ECB but to a lesser degree.

BoE has also released its latest UK inflationary forecasts where it projected that headline CPI inflation is likely to decelerate at a faster pace in the first half of 2023 versus its prior forecast made in November 2023, and it expects inflation to dip towards BoE’s target of 2% in Q2 2024.

But thereafter, the headline inflationary pressure is likely to revive and increase to 2.8% y/y in Q1 2025 and only starts to taper off in Q3 2025, as well as staying above the 2% target till Q3 2026 (see Fig 1).

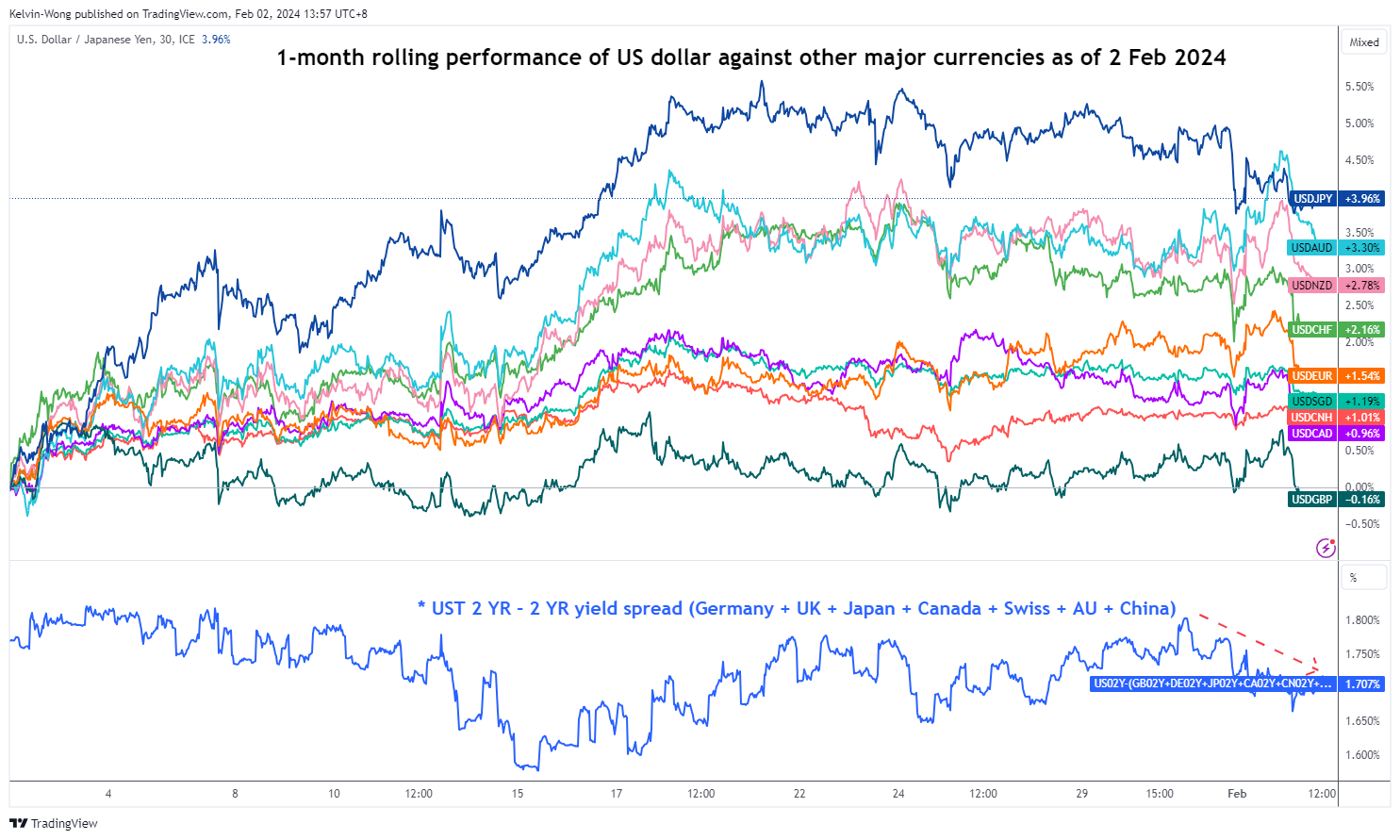

GBP remains the strongest currency among the majors

Fig 2: 1-month rolling performances of major currencies against US dollar as of 2 Feb 2024 (Source: TradingView, click to enlarge chart)

Hence in the mindsets of BoE officials, there is still a “lingering fear” of the resurgence of inflationary pressure that suggests a tinker of hawkish vibes which in turn may trigger a lag in BoE’s anticipated interest cut versus a more relatively dovish modus operandi from the Fed and ECB; market participants have priced in four interest rate cuts from BoE, below six cuts expected from Fed and ECB respectively in 2024.

Given such a hint of “residual” hawkish vibes derived from BoE’s latest inflation projections, the GBP has remained the top outperformer among the major currencies against the USD dollar where it has recorded a gain of +0.16% versus the US dollar according to one-month rolling performance calculations (see Fig 2)

Positive momentum condition flashed out for GBP/USD after compression for 5 weeks

Fig 3: GBP/USD medium-term trend as of 2 Feb 2024 (Source: TradingView, click to enlarge chart)

Fig 4: GBP/USD short-term trend as of 2 Feb 2024 (Source: TradingView, click to enlarge chart)

Through the lens of technical analysis, positive elements have surfaced in the price actions of GBP/USD. It has consolidated in a “Symmetrical Triangle” range configuration in place since 28 December 2023; a consolidation or “resting moment” to retrace the impulsive upmove sequence of its recent medium-term uptrend phase from 4 October 2023 low of 1.2037 to 28 December 2023 high of 1.2828.

So far, it has traded above its upward-sloping 50-day moving average since 14 November 2023 and yesterday’s (1 February) price action (a daily gain of +0.44%) has formed a bullish candlestick body that has managed to engulf the prior consecutive small candlestick bodies in place since 18 January 2024 (see Fig 3).

In addition, the daily RSI momentum indicator has just staged a bullish breakout above its prior parallel descending resistance at the 55 level. This observation suggests a potential leading bullish signal for a possible imminent bullish price action breakout.

The rising 2-year UK Gilt-US Treasury sovereign bond spread is also advocating a potential bullish momentum resurgence for GBP/USD.

Watch the 1.2610 key short-term pivotal support and clearance above 1.2760 (upper boundary of the “Symmetrical Triangle” range) sees the next intermediate resistances coming in at 1.2820 and 1.2880 in the first step.

On the other hand, a break below 1.2610 invalidates the bullish tone for another leg of minor corrective decline to expose the next intermediate support zone at 1.2550/2500 (also the 200-day moving average).

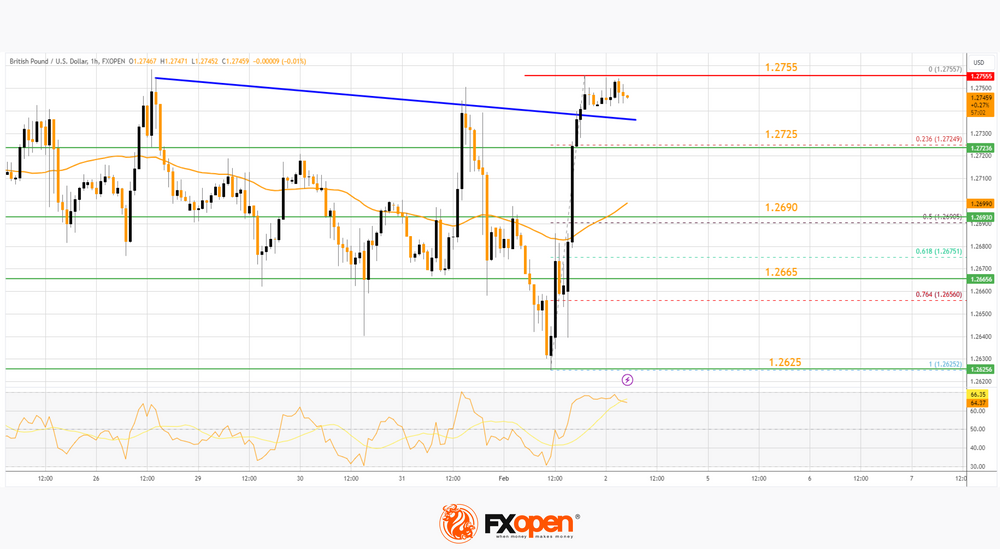

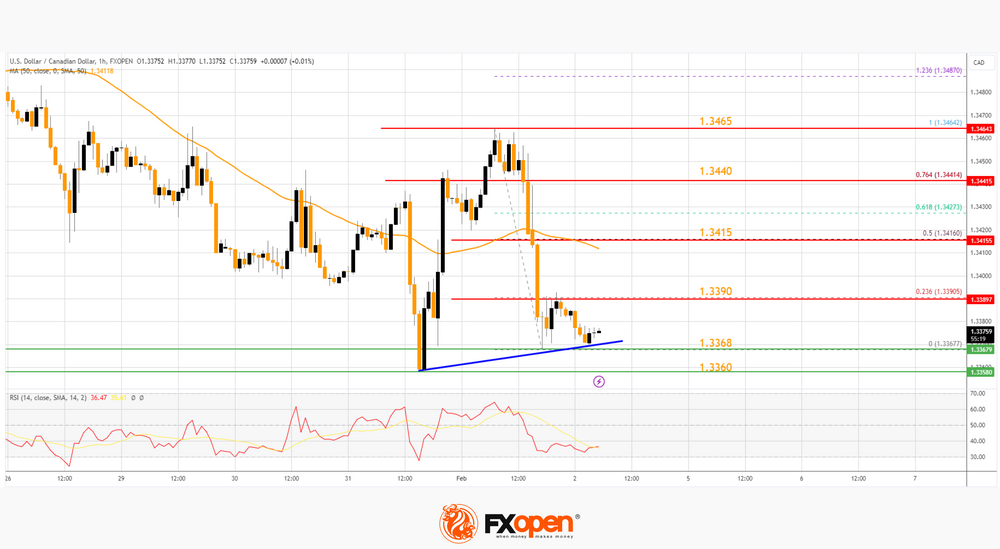

GBP/USD Regains Strength While USD/CAD Dips Again

GBP/USD started a fresh increase above the 1.2625 zone. USD/CAD is declining and trading below the 1.3415 support.

Important Takeaways for GBP/USD and USD/CAD Analysis Today

- The British Pound is eyeing more gains above the 1.2755 resistance.

- There was a break above a key bearish trend line with resistance near 1.2740 on the hourly chart of GBP/USD at FXOpen.

- USD/CAD started a fresh decline after it failed to clear the 1.3465 resistance.

- There is a short-term connecting bullish trend line forming with support near 1.3368 on the hourly chart at FXOpen.

GBP/USD Technical Analysis

On the hourly chart of GBP/USD at FXOpen, the pair formed a base above the 1.2625 level. The British Pound started a decent increase above the 1.2665 resistance zone against the US Dollar, as mentioned in the previous analysis.

The pair gained strength above the 1.2690 level. The bulls even pushed the pair above the 1.2725 level and the 50-hour simple moving average. More importantly, there was a break above a key bearish trend line with resistance near 1.2740.

The pair tested the 1.2755 zone and is currently consolidating gains. If there is a downside correction, the pair could test the same trend line at 1.2740.

The first major support sits at the 23.6% Fib retracement level of the upward move from the 1.2625 swing low to the 1.2755 high. The next major support is 1.2690 and the 50-hour simple moving average.

The 50% Fib retracement level of the upward move from the 1.2625 swing low to the 1.2755 high is also at 1.2690. If there is a break below 1.2690, the pair could extend the decline. The next key support is near the 1.2665 level. Any more losses might call for a test of the 1.2625 support.

Conversely, the bulls might aim for more gains. The RSI moved above the 65 level on the GBP/USD chart and the pair is now approaching a major hurdle at 1.2755. An upside break above the 1.2755 zone could send the pair toward 1.2800. Any more gains might open the doors for a test of 1.2850.

USD/CAD Technical Analysis

On the hourly chart of USD/CAD at FXOpen, the pair climbed toward the 1.3440 resistance zone before the bears appeared. The US Dollar formed a high near 1.3642 and recently declined below the 1.3415 support against the Canadian Dollar.

There was also a close below the 50-hour simple moving average and 1.3390. The bulls are now active near the 1.3370 level. There is also a short-term connecting bullish trend line forming with support near 1.3368.

The first major support is near 1.3360. A close below the 1.3360 level might trigger a strong decline. In the stated case, USD/CAD might test 1.3300. Any more losses may possibly open the doors for a drop toward the 1.3250 support.

If there is a fresh increase, the pair could face resistance near the 23.6% Fib retracement level of the downward move from the 1.3464 swing high to the 1.3367 low.

The next key resistance on the USD/CAD chart is near the 50-hour simple moving average at 1.3415. The 50% Fib retracement level of the downward move from the 1.3464 swing high to the 1.3367 low is also at 1.3415.

If there is an upside break above 1.3415, the pair could rise toward the 1.3440 resistance. The next major resistance is near the 1.3465 level, above which it could rise steadily toward the 1.3500 resistance zone.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

US 10-y Yield Should Find Support in December Correction Low (3.78%)

Markets

Yesterday’s eco calendar’s market moving potential didn’t fully materialize. Ranging from slightly higher-than-expected European (y/y) inflation over the BoE dropping its hawkish bias to the US’ sub-consensus unit labor costs & weekly jobless claims vs an unexpected improvement in the manufacturing ISM (with solid new orders and rising prices). Oil prices fell off a cliff (see below). But none of that really left a mark on markets. German yields whipsawed, resulting in changes between +2.9 bps (2-y) to -3.4 bps (30-y). Long end outperformance was also visible in the US market, where yields dropped up to 5 bps (30-y). Easing core bond yields helped recoup Wall Street some of the Fed-induced losses to the tune of 1-1.5%. The regional banking index in the wake of the New York Community Bancorp earnings shocker for a second day fell more than 6% intraday before cutting losses in half. It suggests ongoing nervousness and therefore deserves everyone’s attention still. The dollar slipped amid general risk-on. EUR/USD bounced of 1.0793 support to close at 1.0872. DXY dropped towards the 103 area and USD/JPY extended Wednesday decline to finish at 146.43. Sterling held up very well given the BoE’s shift to a stance more on par with the ECB and Fed, ie. giving markets the prospect of rate cuts (conditioned on inflation easing further). EUR/GBP jumped to an intraday high of 0.8558 after the decision but in the end eked out only a marginal gain to 0.8531.

From the overnight news flow we retain that Powell is appearing on CBS News’s 60 Minutes on Sunday. The Fed chair has been interviewed by America’s most-watched news magazine show before as a way to communicate monetary policy to the broader public. This time around, he’s showing up at a time the Fed is preparing for a rate pivot. Investors will be on high alert. Testament to an otherwise quiet session are the muted changes on both bond and currency markets. Brent oil stabilizes after yesterday’s whammy. Investors are probably keenly awaiting the release of the US payrolls report later today. There are several warnings for the January edition, however, with factors including weather (cold snap in January), re-benchmarking, season factors and (population) revisions making it tricky to draw firm conclusions. Either way, consensus expects a net job growth of 185k following the 216k in December, suggesting ongoing labour market resilience. The unemployment rate is seen rising to 3.8% but to the extent it is accompanied with the expected increase in the participation rate, this shouldn’t be seen as a worrying sign. Hourly earnings are anticipated at an average 0.3% m/m and 4.1% y/y. Despite the slew of statistical and technical warnings, we do believe markets will (mainly) react to a downward surprise. The US 10-y yield in such a case should find support in the December correction low (3.78%) though. Barring a huge miss, first resistance around EUR/USD 1.0945/1.096 is probably safe.

News & Views

Wards total vehicle sales declined from 15.83mn in December to 15mn in January (seasonally adjusted, annualized basis), the lowest level since March last year and way below 15.70mn consensus. Light vehicle sales are down 5.2% M/M and 4.7% Y/Y. In a separate report, Wards indicates that the combined sales of hybrid vehicles, plug-in hybrids and battery vehicles in the US rose from 12.9% of total sales in 2022 to 16.3% of total new light vehicle sales in 2023. The introduction of several more models, especially in the crossover and luxury segment, fiscal support and significant price cuts (especially Tesla) helped boost EV growth.

OPEC+ yesterday committed to their 900k barrel/day production cut for Q1 2024 (complemented by an additional 1mn barrel/day cut by Saudi Arabia), but sources suggest that these cuts our up to review when the cartel meets in March. Brent crude prices slid from $81.5/b to $79/b as yesterday’s talk was interpreted as the start of a return to additional supply. Such move would come as question marks are placed about global oil demand this year.

Happy Jobs Friday

The Bank of England (BoE) kept its rates unchanged yesterday but opened the door to rate cuts mentioning ‘good news on inflation’. Cable rebounded despite a dovish takeaway from the MPC meeting as the US dollar fell sharply despite better-than-expected ISM manufacturing survey. In the euro area, inflation fell slower than expected in January. Combined with a softer US dollar, the EURUSD jumped from 1.0780, a few pips above the 100-DMA. The Swedish Riksbank also held rates steady yesterday and gave the happy news that a rate cut will be coming in H1.

The year starts with the sweet smell of the upcoming interest rate cuts, like a freshly baked apple pie ready to come out of oven. We can’t wait to have a taste of it before the commercial real estate dives into darkness with more than half of commercial loans in the US due to come to maturity by the end of 2025 – and these loans make up to almost 30% of the small banks’ assets. So, let’s hope that the Fed won’t burn the pie.

Happy US jobs day

The US is expected to have added less than 200K jobs this January, for around the same pay growth of 4.1% and unemployment rate is seen ticking slightly higher to 3.8%. A reasonably weak number should revive the Federal Reserve (Fed) doves, while a strong number should melt the March rate cut expectations. The probability of a March hike fell to 35% after the Fed said that March was probably too early to cut rates – while this probability was around 80% at the start of the year. Everyone is focused on the May meeting now, with more than 90% probability priced in for the first Fed cut.

The rational with the jobs data is, the softer the data, the sooner the Fed could start cutting rates. And with the number of layoff news on the newswire, it looks safe to bet that today’s NFP will be as soft as Wednesday’s ADP report. But note that Fed Chair Jerome Powell said that they sense that the US economy is accelerating based on anecdotes and chats with private sector. And that’s not in line with the layoff news that crowd the headlines. A reasonably soft jobs data is good for the Fed doves and should further weigh on the US dollar, a stronger than expected figure – if not abnormally strong - should not impact the May cut expectations and keep the dollar bulls contained.

Earnings roundup

Three US tech giants revealed their Q4 results yesterday, after the bell and the results were mixed. Meta jumped 15% in the afterhours trading – the kind of post-earnings move we love to see - after its revenue jumped 25% compared to the same time a year ago. The company gave a bright sales forecast, announced a $50bn buyback and its first ever dividend of 50 cents starting from March. As such, Meta will jump past the $400 per share at open and hit a fresh record. What a comeback!

Amazon gained a bit more than 2.5% after reporting strong sales and gave a better-than-expected operating income. AWS made only 13% more compared to the same time last year and that’s well shy of Microsoft and Google’s, but it’s not about how much you grow but how much you grow compared to expectations; the 13% growth was well digested. Amazon could extend gains and eventually return to its long-term ascending base. Amazon lacks colour compared to its Magnificent 7 buddies which run from record to record. But the company has potential to develop its cloud business and integrate AI on it.

Less enthusiastic, Apple shares almost 3% in the afterhours trading as sales in China dropped 13%. The company, however, returned to growth after four quarters of contraction and overall iPhone sales were a beat. But investors couldn’t get over the worsening outlook in China. Maybe it’s time for Apple to look for another milk cow. India, maybe?

Today, Exxon and Chevron are due to announce how well they did last quarter. Yesterday, Shell announced a $28bn profit and $3.5bn share buyback. The $28bn is much lower than the $40bn the company announced in stellar 2022 – after Russia invaded Ukraine, and oil’s inability to gain sustainable positive momentum remains a headache for oil revenues, but Shell jumped 2% after the results, OPEC signaled that it will keep oil restrictions intact until the end of this year, and US crude fell below the $74bn as the US could choose not to escalate tensions with Iran after the weekend attacks. But is it the calm before a storm? Time will tell. Geopolitical risks prevail and oil should find support near the $73-73.50 region, that includes the 50-DMA.

US Jobs Report Will Set the Tone for Markets

In focus today

In the US, we will get the US January job report. We expect the employment growth to have slowed down to 180k from 216k in December, which is a robust pace in historical terms. We expect average hourly earnings growth to have slowed to 0.3% m/m SA from 0.4% in December.

In Norway, we will get unemployment data for January. The Norwegian labour market remains tight. Employment growth is holding up relatively well, but falling activity means that productivity growth has now become negative. Without an immediate boost in activity there is a risk that unemployment will begin to rise. However, we believe that January was too early and that seasonally adjusted unemployment rate was unchanged at 1.9%.

Economic and market news

What happened yesterday

In the UK the Bank of England (BoE) maintained the Bank Rate at 5.25% as widely expected. The BoE shifted towards a more neutral approach to monetary policy removing its tightening bias, a less hawkish vote split than previously and overall being more confident in developments in the persistence of inflation, as expected. The tilt fell slightly short of market expectations but overall, a muted reaction in markets. We continue to expect the first 25bp rate cut in June, and see yesterday's meeting as supportive of this, and markets have subsequently shifted towards this as well. We still see relative rates as a slight positive for the cross and note the important signal delivered yesterday in opening the door for cuts. For more details see Bank of England Review - Removing the tightening bias, 1 February.

In Sweden the Riksbank kept the policy rate unchanged as expected at yesterday's policy meeting. In terms of guidance, the Riksbank noted that "if the prospects for inflation remain favourable, the possibility of the policy rate being cut during the first half of the year cannot be ruled out". This was to the dovish side, which provided headwind for the SEK. We continue to expect the first 25bp cut in June followed by consecutive quarterly cuts, totalling 75bp for the year. Additionally, the QT pace was increased from 5bn SEK per month to 6.5bn per month. January PMIs were a bit of a disappointment as headline dropped to 47.1 rather than rising as we expected. It seems production, orders and employment pulled the index lower while delivery times and inventories pushed higher.

In the euro area HICP headline and core came in higher than expected by consensus but in line with signals from country data. Headline HICP rose 2.8% y/y and core inflation came in at 3.3% y/y. Overall, a print close to expectations with core slightly higher but a print ECB should be satisfied with. Euro area unemployment rate remained at record low levels in December at 6.4%. Business surveys show that labour demand is still elevated especially in the service sector although it has come down a bit. These factors together with large wage increases highlight that service inflation is still a worry for the ECB. With weak but not collapsing growth the ECB should be able to remain cautious towards the first rate cut due to the upside risks to inflation from service prices.

In the US Q4 productivity growth surprised to the upside again and remains clearly above pre-Covid average levels at 3.2% q/q at annualized rate. As a result, despite the still quite rapid nominal wage growth, unit labour cost growth has remained very modest (only +0.5% q/q AR). While productivity is difficult to forecast, this should make it easier for the Fed to feel confident about cooling underlying inflation. Meanwhile initial jobless claims surprise to the upside, still at low levels though (224k). We also got surprisingly strong ISM data. The uptick was in line with PMIs, but it was stronger than many of the regional manufacturing surveys suggested. Recovery in order-inventory balances reflects similar developments elsewhere in the global economy as well, although export orders remain at low levels. Employment index falls while prices index ticks higher.

Equities: Global equities ended higher yesterday driven by a lift in US markets while Europe and Japan ended lower. These days are extremely interesting as there are many moving parts and not surprisingly it makes investors a little uncertain on what to think. However, it is worth highlighting that we are getting strong macro data, softer inflation prints, monetary policy makers are opening to policy loosening and lately earnings reporting has been very solid. With that in place, it takes more than some bad banking news, geopolitical noise and Chinese property sector crisis to bring down equities. This was also the conclusion yesterday. Major indices in US did very well despite the regional bank index being down more than 2% and reemerging of the fear of loan losses in regional banks. In US yesterday Dow +1.0%, S&P 500 +1.3%, Nasdaq +1.3%, Russell 2000 +1.4%. Asian markets are mixed this morning, China is lower while South Korea is up 3%(!). Strong PMI from South Korea coupled with a very solid US ISM fuelling the hopes of a strong tech led manufacturing recovery where South Korea will be a major beneficiary. European and US futures are higher, partly lifted by some strong after hour earnings in the US.

FI: The global bond market rallied yesterday as the market "ignored" the comments from Fed Chairman Powell from the FOMC meeting on Wednesday regarding the timing for the first rate cut. The US curve "bull-flattened" with 10Y US Treasury yields declining some 5bp, while 2Y yield fell 1bp. In Europe, yields initially rose yesterday morning before the rally began later Thursday, and Bund ended the day 5bp lower.

FX: The first Riksbank decision of 2024 was broadly in line with our expectations, however with a slight dovish twist, which provided support for EUR/SEK. EUR/GBP initially dipped briefly following the Bank of England announcement. While the Committee delivered a dovish tilt and signalled an important shift towards a more neutral approach to monetary policy, it fell slightly short of market expectations. EUR/USD moved higher over the course of the day, breaching back above the 1.08 mark as global bond markets rallied. Today, focus turns to the non-farm payrolls from the US, where focus is on whether the US will continue to show underlying strength.

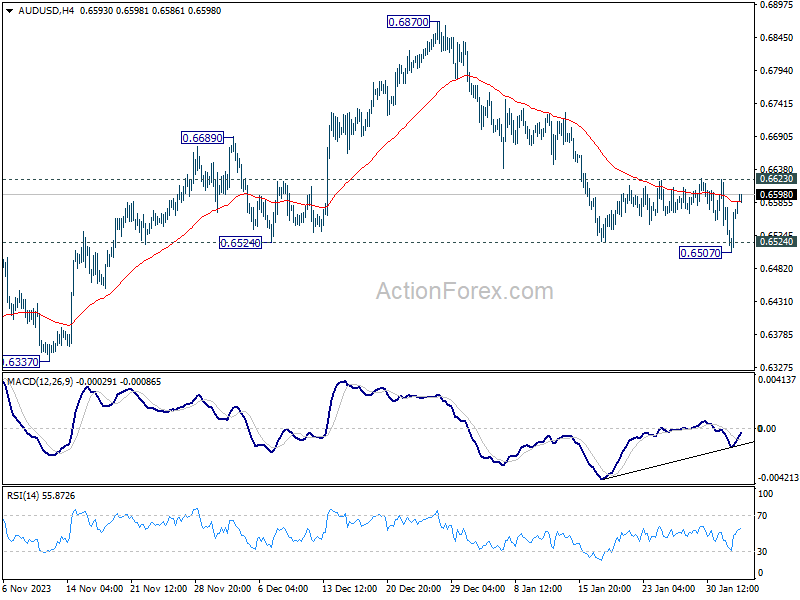

AUD/USD Daily Report

Daily Pivots: (S1) 0.6527; (P) 0.6553; (R1) 0.6598; More...

AUD/USD recovered quickly after breaching 0.6524 support and intraday bias stays neutral. On the downside, decisive break of 0.6524 argue that whole rebound from 0.6269 has completed, and bring deeper fall to this support. However, considering bullish convergence condition in 4H MACD, firm break of 0.6623 minor resistance will confirm short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

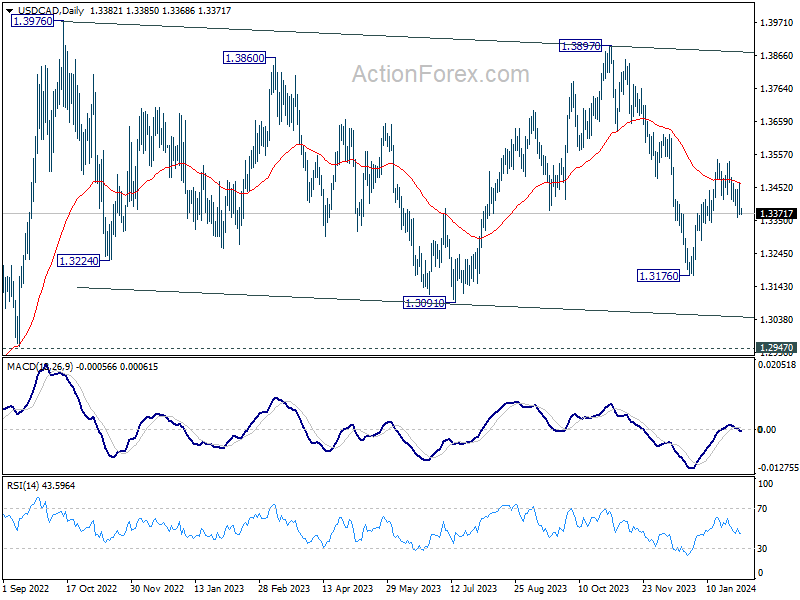

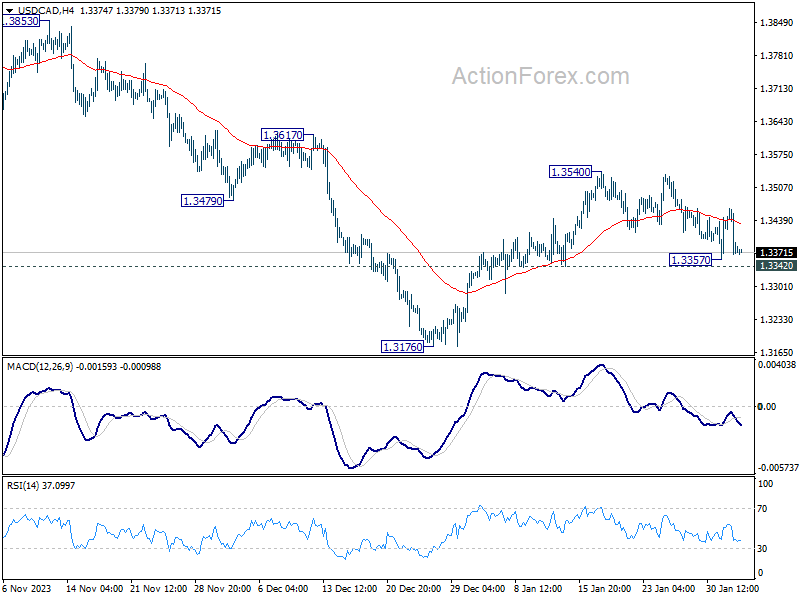

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3349; (P) 1.3406; (R1) 1.3445; More...

Intraday bias in USD/CAD remains neutral for the moment. On the downside, firm break of 1.3342 support will argue that rebound from 1.3176 has completed at 1.3540, and target this low for resuming whole fall from 1.3897. On the upside, however, break of 1.3540 will resume the rebound from 1.3176 instead.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.