Sample Category Title

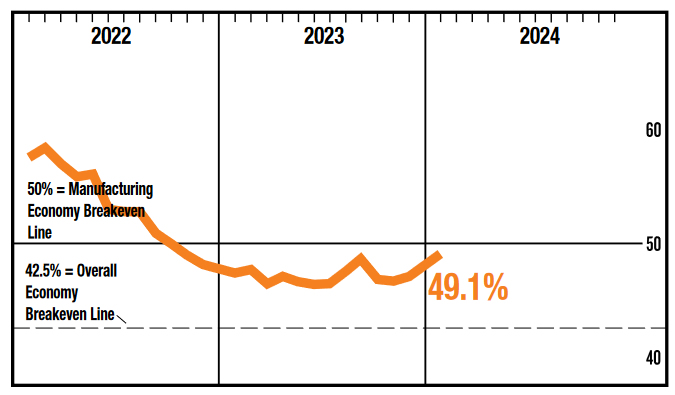

ISM manufacturing rises to 49.1, nears expansion threshold, with rising prices and stronger orders

US manufacturing sector, as indicated by ISM Manufacturing PMI, showed signs of resilience in January 2024, slightly missing the mark of expansion. The index climbed from 47.1 to 49.1, surpassing market expectations of 47.7, yet marking the 15th consecutive month of contraction.

A significant highlight was the jump in new orders, which soared to 52.5, reaching its highest level since May 2022. Production also showed modest improvement, ticking up from 49.9 to 50.5. However, employment index continued its downward trajectory, recording a fourth consecutive month of contraction at 47.1, down from 47.5.

A notable surge was observed in the prices index, which escalated sharply from 45.2 to 52.9. This marks the highest point since April 2023, signaling increasing cost pressures within the sector.

Overall, the current ISM Manufacturing PMI level is historically aligned with a 1.9% annualized growth in real GDP.

Sunset Market Commentary

Markets

The Bank of England kept its policy rate unchanged at 5.25% in a 3-way split with two members (Mann & Haskel) preferring a 25 bps rate increase to 5.5% and one member (Dhingra) voting in favour to reduce it by 25 bps to 5%. That compares with consecutive 6-3 votes (3 in favour of +25 bps) in November and December. The UK central bank dropped forward guidance saying that further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures, replacing it by the message that the Monetary Policy Committee will keep under review for how long the Bank Rate should be maintained at the current level. The MPC published a new policy report conditioned on a market-implied path for the Bank Rate that declines from 5.25% to 3.25% by the end of the forecast period, almost 1 ppt lower on average than in November. CPI inflation is now expected to slide further to the 2% target by Q2 2024, before picking up again (energy-related) and remaining above the 2% inflation target until the end of 2026. This reflects the persistence of domestic inflationary pressures, despite an increasing degree of slack in the economy. Conditioned on the alternative assumption of constant interest rates at 5.25%, the path for CPI inflation is significantly lower with inflation falling below the 2% target from 2025 Q4 onwards. Risks to the inflation outlook became more balanced. GDP growth is expected to pick up gradually during the forecast period (0.5% from Q1 2024 to Q1 2025 and 0.8% from Q1 2025 to Q1 2026), in large part reflecting a waning drag on the rate of growth from past increases in Bank Rate. Business surveys are consistent with an improving outlook for activity in the near term. At the press conference, BoE governor Bailey stressed the change in forward guidance but warned that the BoE isn’t there yet. He didn’t pre-commit to a specific timing on a first rate cut. As with the January ECB and Fed policy meetings, the market reaction was extremely modest. Sterling traded slightly on the backfoot going into the meeting, reversing the move afterwards. From an EUR/GBP point of view, support at 0.8493 (2023 YTD low) seems now cemented. UK bond yield changes range between 2 and 3 bps across the curve. UK money markets fully discount a rate cut by the June 20 BoE meeting.

Other post-FOMC market moves are very orderly as well. German Bunds marginally outperform US Treasuries though daily yield changes for both are negligible. European inflation fell as expected by 0.4% M/M in January, but both the headline and core CPI Y/Y-prints remained a tad above consensus at respectively 2.8% (from 2.9%) and 3.3% (from 3.4%). US eco data included slightly higher weekly jobless claims (224k from 215k) and a smaller than expected increase in Q4 unit labour costs (+0.5% Q/Q vs +1.2%). The manufacturing ISM will still be released later this afternoon. EUR/USD set a new YTD low at 1.0780 before returning just above the 1.08 handle. European stock markets are mixed with US indices already forgetting about yesterday’s beating (up to +0.7%). We finally mention a significant outperformance of Hungarian rates (up to -15 bps) as PM Orban gave up resistance against a €50bn aid package for Ukraine. A similar reversal of risk premia is also, but less, visible in EUR/HUF (383).

News & Views

The Swedish Riksbank today left its policy rate unchanged at 4.0% as expected. However, the RB substantially changed is assessment on future policy compared to end November. Rate increase have contributed to lower inflationary pressures. Inflation (CPIF 2.3%, CPIF excluding energy 5.3% has developed in line with the Riksbank’s forecast. This creates greater certainty with respect to the RB’s assessment of inflation. Activity in the Swedish economy also materially cooled. With especially core inflation still being too high and an going risk of setbacks, RB expects that a contractionary monetary policy is still needed to stabilize inflation close to the 2% target. The RB sees less risk of inflation becoming entrenched at levels that are too high. In this respect, the RB doesn’t exclude a first reduction in the policy rate in the first half of this year. This is a material change from its assessment in November when the RB still left the door open for an final additional rate hike. At that time it only saw room to cut the policy rate in 2025. The RB accelerates the sales of bonds from its QE portfolio from SEK 5 bln p/month to 6.5 bln. Changes in Swedish yields were limited. Still, the soft U-turn of the RB triggered renewed selling of the krone. EUR/SEK jumped from the 11.24 area to currently 11.30.

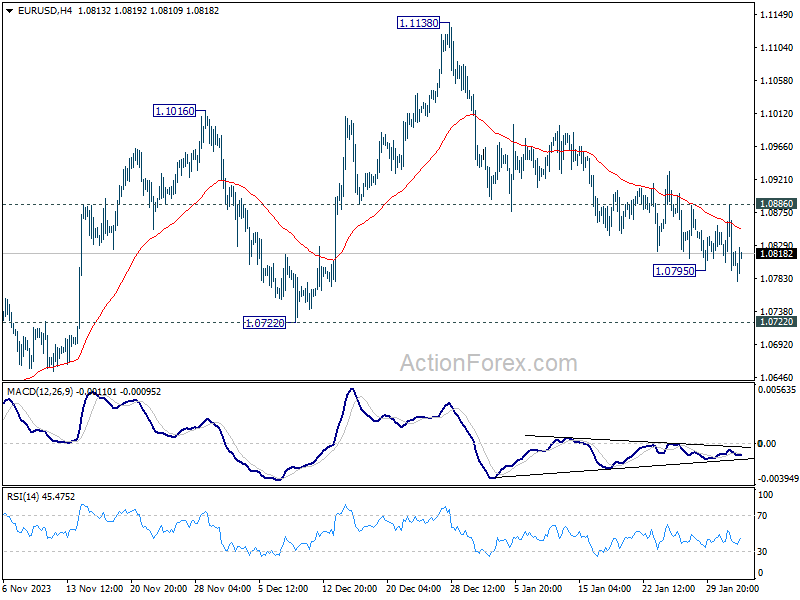

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0820; (P) 1.0838; (R1) 1.0865; More...

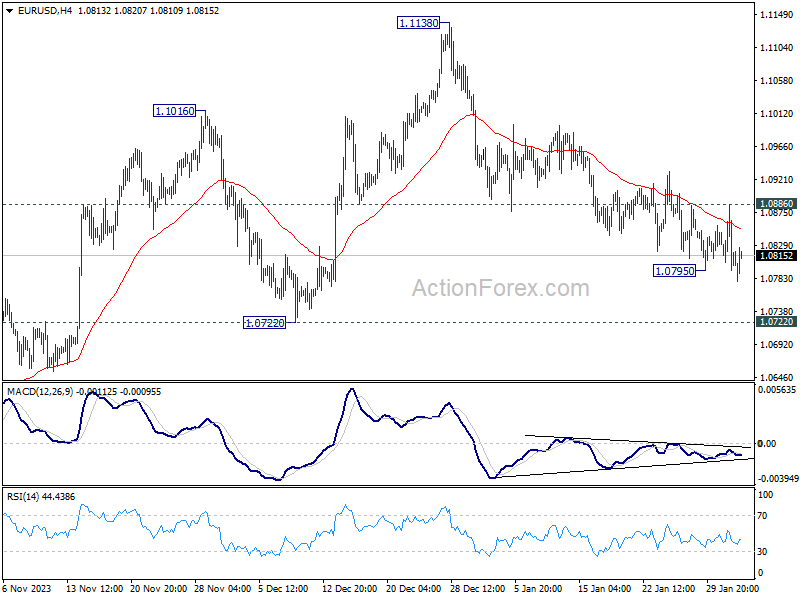

Intraday bias in EUR/USD is back on the downside with breach of 1.0795 temporary low. Fall from 1.1138 is trying to resume to 1.0722 structural support. Decisive break there will argue that whole rise from 1.0447 has completed, and target this low. On the upside, however, break of 1.0931 will turn bias back to the upside for stronger rebound instead.

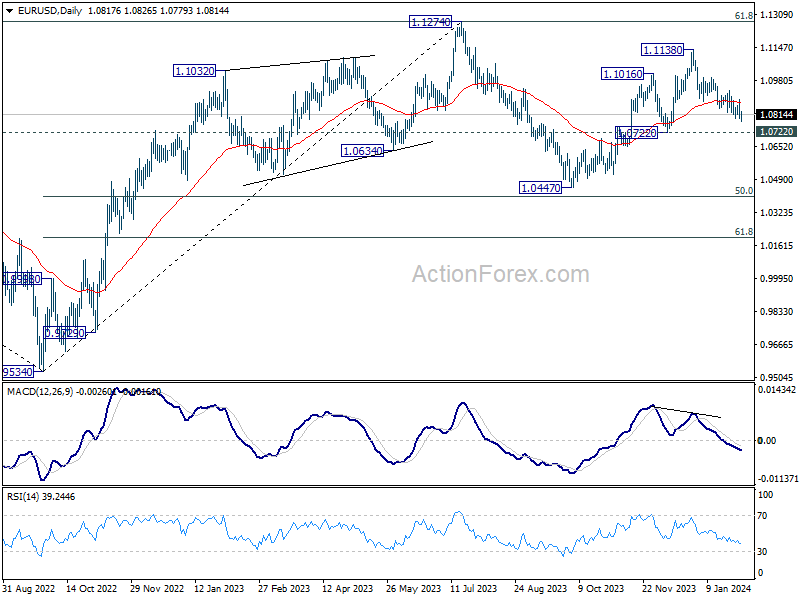

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

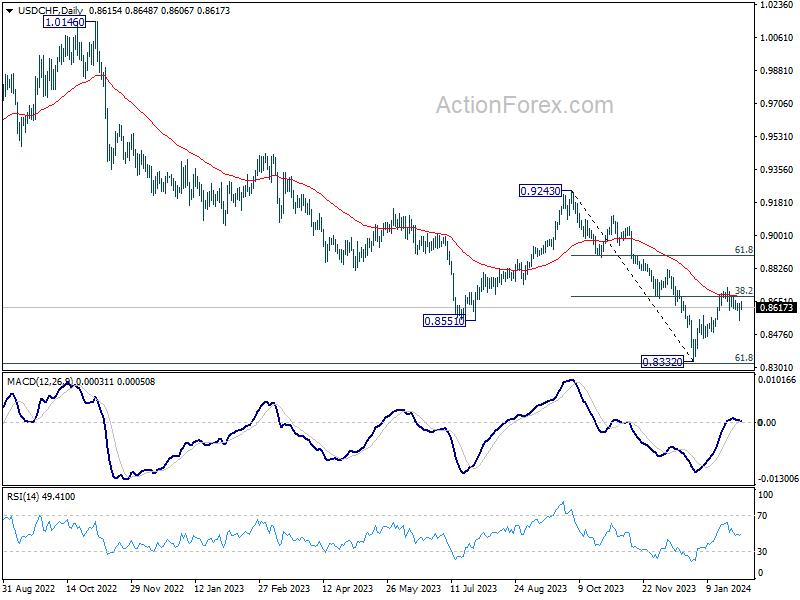

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8562; (P) 0.8603; (R1) 0.8655; More....

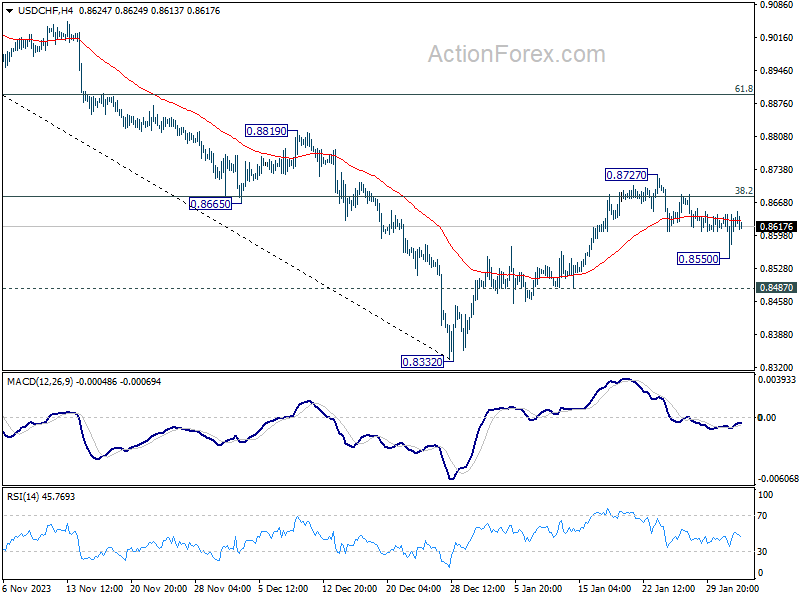

Intraday bias in USD/CHF remains neutral at this point. On the downside, below 0.8550 will resume the fall from 0.8727 for 0.8487 support. Break there will argue that rebound from 0.8332 has completed, and bring retest of this low. On the upside, firm break of 0.8727 will resume the rebound to 61.8% retracement of 0.9243 to 0.8332 at 0.8995 instead.

In the bigger picture, while rebound from 0.8332 could be strong, there is no clear sign of medium term bottoming yet. This rebound is tentatively seen as a corrective move for now. Also, outlook will stay bearish as long as 0.9243 resistance holds. Larger down trend from 1.0146 (2022 high) should resume through 0.8332 low at a later stage.

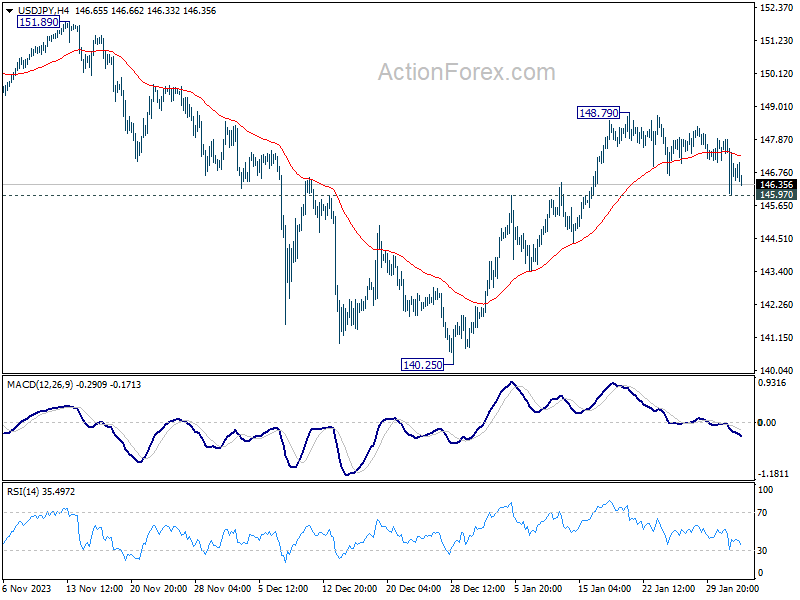

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.16; (P) 147.54; (R1) 147.99; More...

USD/JPY is still holding above 145.97 resistance turned support. Intraday bias stays neutral at this point, and further rally is still in favor. As noted before, corrective fall from 151.89 should have completed at 140.25 already. Break of 148.79 will resume the rise from there for retesting 151.89/93 key resistance zone. However, firm break of 145.97 will dampen this view, and turn bias to the downside for deeper fall towards 140.25.

In the bigger picture, stronger than expected rebound from 140.25 dampened the original bearish review. Strong support from 55 W EMA (now at 142.49) is also a medium term bullish sign. Fall from 151.89 could be a correction to rise from 127.20 only. Decisive break of 151.89/93 will confirm resumption of long term up trend. This will now be the favored case as long as 140.25 support holds.

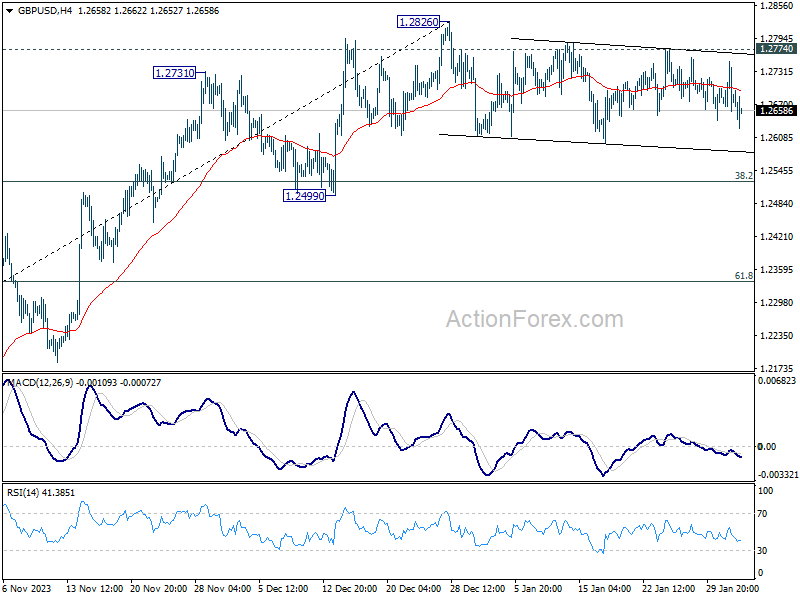

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2646; (P) 1.2699; (R1) 1.2739; More...

No change in GBP/USD's outlook and intraday bias remains neutral. Consolidation from 1.2826 is extending and deeper fall cannot be ruled out. But downside should be contained above 1.2499 support to bring rebound. On the upside, firm break of 1.2774 resistance will suggest that consolidation pattern has completed. Further rise should be seen through 1.2826 to resume the rally from 1.2036. Next target will be 1.3141 high.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

BoE’s Three-Way Split Vote Muddles Sterling’s Path, Yen Strength Continues

Sterling is currently trading with indecisiveness following BoE's rate decision, which has provoked mixed reactions in the markets. The decision, notable for its combination of hawkish and dovish signals, resulted in a rare three-way voting split—the first occurrence since 2008—with two members favoring a rate hike, one a cut, and the rest opting for no change. This split highlights the complexities and differing perspectives within the MPC.

BoE has notably relinquished its tightening bias, and significantly lowering the conditioned rate path, which now sees interest rate to fall to 3.9% by the onset of next year. Despite this dovish tilt, the bank simultaneously revised its inflation forecasts upward, suggesting that inflationary pressures will persist above target until 2026. Governor Andrew Bailey's remarks were also clear in that the central bank is not yet in a position to contemplate rate reductions.

Meanwhile, Japanese Yen continues to assert its strength, capitalizing on weakening global benchmark yields. US 10-year yield is teetering on the brink of falling below the 3.9% mark, while its UK counterpart exhibits a similar downward trajectory. German 10-year yield, is merely holding its ground, lacking the momentum for a significant recovery.

Euro, the second strongest for the day after Yen, finds itself buoyed slightly by higher than expected inflation readings in both the headline and core CPI in Eurozone. Dollar, trailing as the third strongest, faces challenges in making decisive progress. In contrast, Australian Dollar is positioned as the weakest, followed by New Zealand Dollar. Sterling and Canadian Dollar, though weaker, are not as severely impacted, while Swiss Franc displays mixed performance.

Technically, while EUR/USD dipped again earlier in the day, it quickly found its way back into familiar range. Downside momentum is clearly waning as seen in 4H MACD. It's now a crucial decision point for traders on whether to push EUR/USD through 1.0722 key structural support to confirm near term bearish reversal. Or, the bears will just give up and let EUR/USD bounce through 1.0886 minor resistance to confirm short term bottoming. This decision is likely to become clear shortly.

In Europe, at the time of writing, FTSE is up 0.18%. DAX is down -0.07%. CAC is down -0.54%. UK 10-year yield is down -0.0271 at 3.774. Germany 10-year yield is up 0.009 at 2.182. Earlier in Asia, Japan 10-year JGB yield fell -0.0412 to 0.695. Nikkei fell -0.76%. Hong Kong HSI rose 0.52%. China Shanghai SSE fell -0.64%. Singapore Strait Times fell -0.32%.

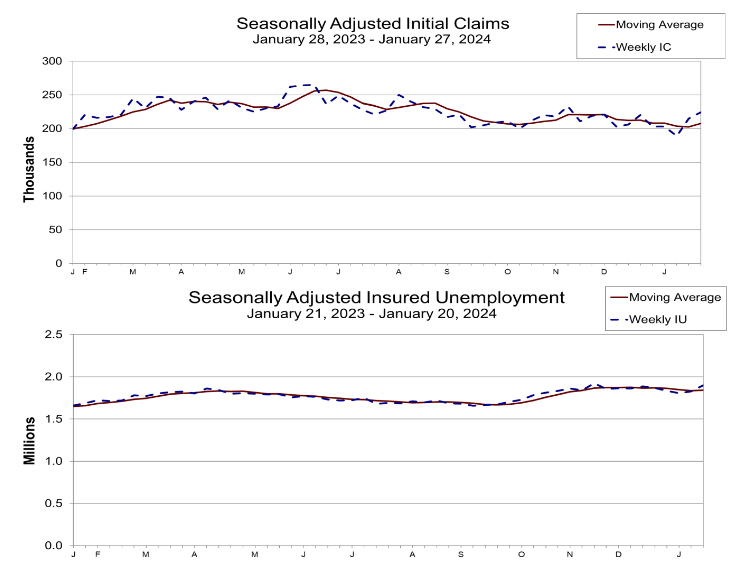

US initial jobless claims rises to 224k, abv exp 211k

US initial jobless claims rose 9k to 224k in the week ending January 27, above expectation of 211k. Four-week moving average of initial claims rose 5k to 208k.

Continuing claims rose 70k to 1898k in the week ending January 20. Four-week moving average of continuing claims rose 7.5k to 1841k.

BoE stands pat, two vote for hike, one for cut

BoE left the Bank Rate unchanged at 5.25% as widely expected. However, two MPC hawks (Jonathan Haskel and Catherine Mann) voted for another 25bps to 5.50%. Meanwhile, one dove (Swati Dhingra) voted for a 25bps cut to 5.00%. That resulted in a 6-3 vote for the decision.

Nevertheless, the central bank dropped tightening bias by omitting the language that "Further tightening in monetary policy would be required...." Instead, it's now "prepared to adjust monetary policy as warranted by economic data".

BoE will continue monitor a range of measures of "the underlying tightness of labour market conditions, wage growth and services price inflation."

CPI is projected to fall temporarily to 2% in Q2 2024, before rising again in Q3 and Q4. BoE sees CPI to be at to be at 2.8% in Q1 2025 (up from prior 2.5%), then 2.3% in Q1 2026 ( up from 1.9%), then 1.9% in Q1 2027 (new).

Four-quarter GDP growth is seen at 0.5% in Q1 2025 (up from 0.0%), the 0.8% in Q1 2026 (up from 0.6%), and 1.5% in Q1 2027 (new).

These are conditioned on a lowered market-implied path for Bank Rate that declines from 5.1% in Q1 2024 (prior 5.3%), then falls to 3.9% in Q1 2025 (down from 5.0%), and then 3.3% in Q1 2026 (down from 4.4%), and 3.2% in Q1 2027 (new).

UK PMI manufacturing finalized at 47.0, challenged by cost pressures and supply disruptions

UK PMI Manufacturing was finalized at 47.0 in January, up from December's 46.2. This modest improvement, however, did not signal an end to the sector's downturn, with continued contractions observed across key areas.

Rob Dobson, Director at S&P Global Market Intelligence, highlighted the pervasive nature of the contraction, noting declines in output, new orders, and employment across various manufacturing sub-industries. He pointed out that manufacturers are adopting a cost-cautious approach, focusing on cutting back on purchasing and stock holdings to improve efficiency, maintain cash flow, and protect margins in these challenging times.

The industry faces compounded difficulties due to the ongoing "Red Sea crisis", which is exacerbating supply chain disruptions. The rerouting of inputs from the Asia-Pacific region is leading to increased costs and longer supplier lead times, intensifying the strain on production schedules and amplifying inflationary pressures. This situation is particularly problematic as manufacturers grapple with weak domestic and international demand.

Eurozone CPI down to 2.8%, core falls to 3.3%, both above expectations

Eurozone CPI slowed from 2.9% yoy to 2.8% yoy in January, above expectation of 2.7% yoy. CPI core (excluding energy, food, alcohol & tobacco) slowed from 3.4% yoy to 3.3% yoy, above expectation of 3.2% yoy.

Looking at the main components, food, alcohol & tobacco is expected to have the highest annual rate in January (5.7%, compared with 6.1% in December), followed by services (4.0%, stable compared with December), non-energy industrial goods (2.0%, compared with 2.5% in December) and energy (-6.3%, compared with -6.7% in December).

Eurozone's manufacturing PMI finalized at 46.6, persistent contraction with glimmers of hope in the south

Eurozone PMI Manufacturing was finalized at a 10-month high of 46.6 in January, up from December's 44.4. Despite this, caution is advised as the index still hovers below the critical expansion threshold. Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, highlights that although there's been a consistent rise over the past three months, including in forward-looking indicators like new orders, the majority of the sub-indices, including the headline index, remain in the contraction zone.

This rebound in manufacturing is particularly evident in the "southern economies", with Greece leading at a 21-month high of 54.7 and both Spain (49.2) and Italy (48.5) showing encouraging trends. However, among the largest Eurozone economies, Germany, despite an 11-month high, remains in contraction at 45.5, and France's economic situation continues to be concerning, at 43.2.

The upward trend in sub-indicators such as stock of purchases, backlogs of work, and output, along with a growing optimism for higher output in the coming year, offers a glimmer of hope. This gradual recovery in the manufacturing sector, spearheaded by the southern economies, may serve as a crucial catalyst to pull the larger Eurozone economies out of the recessionary environment.

Japan's PMI manufacturing finalized at 48.0, depressed economy and escalating cost pressures

Japan's PMI Manufacturing was finalized at 48.0 in January, a minimal increase from December's 47.9, yet still indicative of ongoing challenges in the sector.

According to S&P Global, this figure represents a "modest deterioration" in the health of the manufacturing sector, marking a "sustained downturn" at the start of the year.

Usamah Bhatti of S&P Global Market Intelligence highlights the "depressed economic conditions" both domestically and globally as significant contributors to the sector's struggles. The data also shows notable declines in both output and new orders, with the latter experiencing a particularly sharp drop.

Manufacturers in Japan are also facing heightened pressures related to costs and supply. The cost burdens have been rising sharply, driven by increased prices of raw materials, labor, and fuel.

Additionally, supplier performance has deteriorated significantly, marked as the worst in three months. Issues such as delivery and logistical delays have been frequently mentioned, with some attributing these challenges to the ongoing disruption in the Red Sea.

China's Caixin PMI manufacturing unchanged at 50.8, economic challenges persist

China's Caixin PMI Manufacturing was unchanged at 50.8 in January, matched expectations. The sector showed modest production growth, although the overall sales expansion softened. Notably, this period marked the first rise in new export business in seven months, and business confidence reached a nine-month high. However, the employment sector continued to contract, and the market faced ongoing deflationary pressures.

Wang Zhe, Senior Economist at Caixin Insight Group, highlighted that despite the stability in manufacturing, the Chinese economy still grapples with "significant challenges", including weak demand, employment pressures, and subdued market expectations. He emphasized that these issues are yet to see a "fundamental shift reversal".

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2646; (P) 1.2699; (R1) 1.2739; More...

No change in GBP/USD's outlook and intraday bias remains neutral. Consolidation from 1.2826 is extending and deeper fall cannot be ruled out. But downside should be contained above 1.2499 support to bring rebound. On the upside, firm break of 1.2774 resistance will suggest that consolidation pattern has completed. Further rise should be seen through 1.2826 to resume the rally from 1.2036. Next target will be 1.3141 high.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Q4 | -6 | -1 | ||

| 00:30 | AUD | Building Permits M/M Dec | -9.50% | 0.10% | 1.60% | |

| 00:30 | AUD | Import Price Index Q/Q Q4 | 1.10% | 0.60% | 0.80% | |

| 00:30 | JPY | Manufacturing PMI Jan F | 48 | 48 | 48 | |

| 01:45 | CNY | Caixin Manufacturing PMI Jan | 50.8 | 50.8 | 50.8 | |

| 08:30 | CHF | Manufacturing PMI Jan | 43.1 | 44.5 | 43 | |

| 08:45 | EUR | Italy Manufacturing PMI Jan | 48.5 | 47.3 | 45.3 | |

| 08:50 | EUR | France Manufacturing PMI Jan F | 43.1 | 43.2 | 43.2 | |

| 08:55 | EUR | Germany Manufacturing PMI Jan F | 45.5 | 45.4 | 45.4 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Jan F | 46.6 | 46.6 | 46.6 | |

| 09:30 | GBP | Manufacturing PMI Jan F | 47 | 46.9 | 47.3 | |

| 10:00 | EUR | Eurozone Unemployment Rate Dec | 6.40% | 6.40% | 6.40% | |

| 10:00 | EUR | Eurozone CPI Y/Y P | 2.80% | 2.70% | 2.90% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y P | 3.30% | 3.20% | 3.40% | |

| 12:00 | GBP | BoE Interest Rate Decision | 5.25% | 5.25% | 5.25% | |

| 12:00 | GBP | MPC Official Bank Rate Votes | 2--1--6 | 2--0--7 | 3--0--6 | |

| 12:30 | USD | Challenger Job Cuts Y/Y Jan | -20.00% | -20.20% | ||

| 13:30 | USD | Initial Jobless Claims (Jan 26) | 224K | 211K | 214K | 215K |

| 13:30 | USD | Nonfarm Productivity Q4 P | 3.20% | 2.40% | 5.20% | 4.90% |

| 13:30 | USD | Unit Labor Costs Q4 P | 0.50% | 2.10% | -1.20% | -1.10% |

| 14:30 | CAD | Manufacturing PMI Jan | 45.4 | |||

| 14:45 | USD | Manufacturing PMI Jan F | 50.3 | 50.3 | ||

| 15:00 | USD | ISM Manufacturing PMI Jan | 47.7 | 47.4 | ||

| 15:00 | USD | ISM Manufacturing Prices Paid Jan | 45.6 | 45.2 | ||

| 15:00 | USD | ISM Manufacturing Employment Index Jan | 48.1 | |||

| 15:00 | USD | Construction Spending M/M Dec | 0.50% | 0.40% | ||

| 15:30 | USD | Natural Gas Storage | -202B | -326B |

US initial jobless claims rises to 224k, abv exp 211k

US initial jobless claims rose 9k to 224k in the week ending January 27, above expectation of 211k. Four-week moving average of initial claims rose 5k to 208k.

Continuing claims rose 70k to 1898k in the week ending January 20. Four-week moving average of continuing claims rose 7.5k to 1841k.

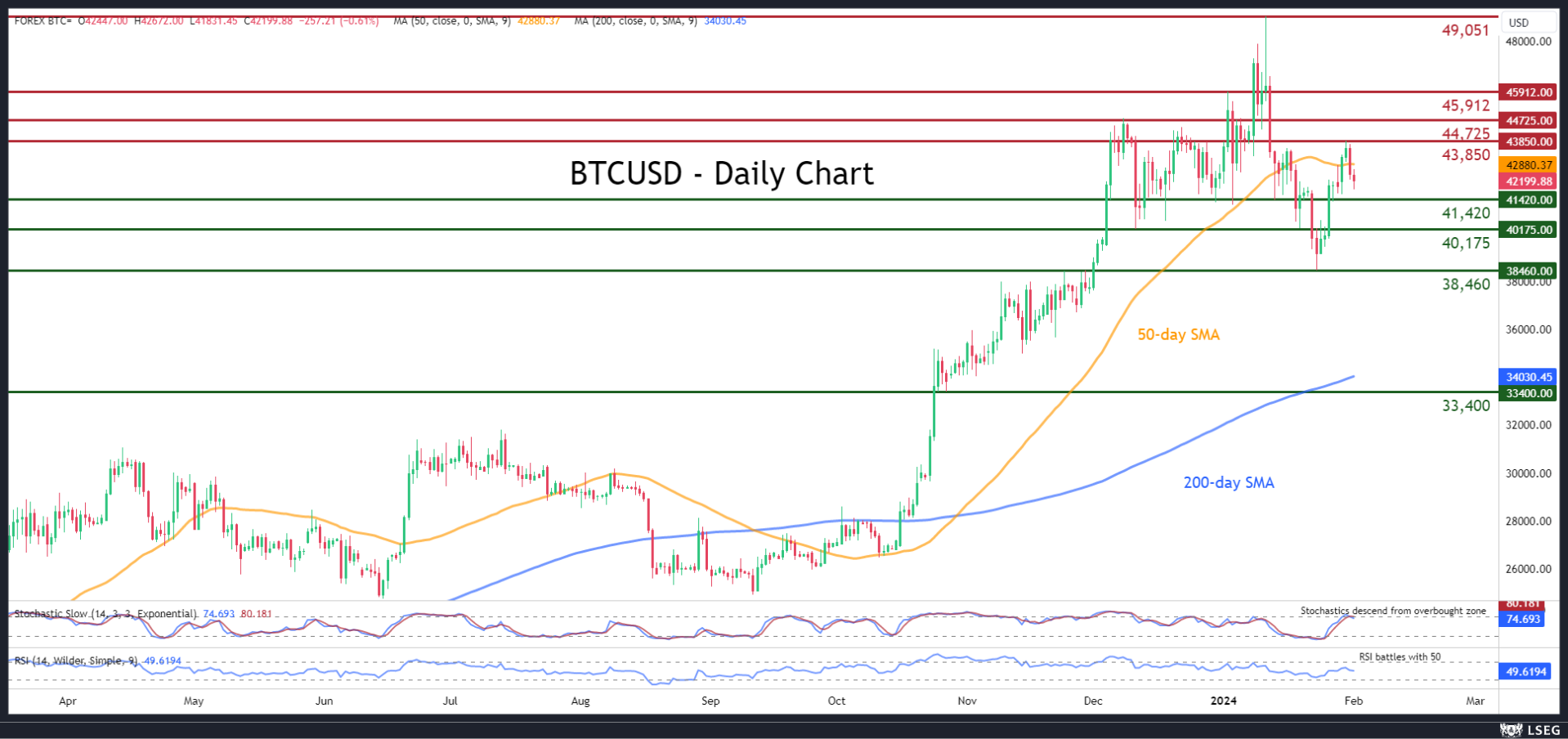

BTCUSD Drops Below 50-day SMA

- BTCUSD bounces off 2024 low and reclaims 40,000

- But price dips back below 50-day SMA after advance pauses

- Momentum indicators suggest weakening buying pressures

BTCUSD (Bitcoin) experienced a strong decline from its recent two-year peak of 49,051, dropping to as low as 38,460. Despite the price’s attempt for recovery, a new round of weakness has begun, with Bitcoin dropping below the 50-day simple moving average (SMA) following a rejection near 43,850.

If the slide resumes, the inside swing low of 41,420 could act as the first line of defence. In case of a downside violation, the price may face the December support of 40,175. Further declines might encounter strong support at the 2024 bottom of 38,460.

Alternatively, should bearish pressures abate, Bitcoin could surge towards the recent rejection region of 43,850. Conquering this barricade, the bulls might attack the December high of 44,725. A jump above the latter could shift the spotlight to 45,912.

In brief, BTCUSD has been losing ground in the near-term after its rebound met strong resistance. Nevertheless, a break above the 50-day SMA could revive the bulls’ hopes for a sustained recovery.

Australian Dollar Falls to 10-Week Low after Fed Decision

The Australian dollar is sharply lower on Thursday after the Fed policy meeting a day earlier. In the European session, AUD/USD is trading at 0.6514, down 0.78%. Earlier, the Australian dollar dropped as low as 0.6508, its lowest level since November 20.

Powell says March rate cut unlikely

The Federal Reserve met on Wednesday and there was no surprise as the Fed left interest rates unchanged for a fourth straight month. The rate-tightening cycle has largely achieved its aim of lowering inflation and there’s little doubt that the Fed is done with tightening. Fed Chair Jerome Powell pivoted at the December meeting and signalled that rate cuts were coming in 2024. The markets proceeded to price in a March cut but the Fed has been pushing back on these expectations, even though some US economic releases were stronger than expected.

The Fed’s pushback has forced the markets to pare expectations of a March cut, from over 80% in December to 48% prior to the Fed meeting. In the aftermath of the meeting, the odds of a March cut have fallen even further, to 35% according to the CME FedWatch tool. The markets are now eyeing the May meeting and have widely priced in an initial rate cut at that time.

The rate statement from yesterday’s meeting noted that it “does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward two per cent.” This was a strong signal to the markets not to expect a rate cut in March.

This stance was reiterated by Powell in his press conference. Powell said it was unlikely that the Fed would lower rates in March, although he did not rule out the possibility completely. The Fed Chair noted that inflation had declined without dragging down the economy or causing high unemployment, a message to the markets that he was not in any rush to start chopping rates.

Australian data is pointing to a weakening economy, just ahead of the Reserve Bank of Australia’s meeting on February 6. Inflation eased to 4.1% y/y in the fourth quarter, down from 5.4% in Q3, while retail sales sunk in December with a decline of 2.7% m/m. The RBA is virtually certain to pause next week and is expected to start to trim rates later this year.

AUD/USD Technical

- AUD/USD is testing support at 0.6538. Next, there is support at 0.6510

- There is resistance at 0.6581 and 0.6609