Sample Category Title

News from the Fed Push Down EUR/USD Price to a Year Low

Financial markets were buoyant last night due to news from the Fed. Interest rates remained unchanged — as expected. However, somewhat unexpected was the harsh rhetoric of Jerome Powell, who said that:

→ interest rate reduction in March is unlikely;

→ the Fed needs to see more data to be confident in the rate change.

This cooled financial market expectations for a rate cut in March, which in turn led to a strengthening of the US dollar relative to other currencies and a decline in stock indices, with risk assets falling especially sharply.

The strengthening of the US dollar caused the EUR/USD rate to drop below 1.079 today for the first time since mid-December last year.

The EUR/USD chart today shows that the price is falling towards the lower border of the ascending channel (shown in blue), and the market is very sensitive to psychological levels:

→ the level of 1.100 (which we paid attention to in the analysis on November 29 and December 15) in January acted as an important resistance twice, preventing the price from rising.

→ Level 1.075, from which reversals were formed, may provide support. Bulls can also pin their hopes on it, since the lower boundary of the ascending channel passes near the level of 1.075.

→ The 1.050 level seems unattainable - but who knows, if the Fed continues to keep rates high “for as long as necessary,” this could lead to a breakdown of the ascending channel, opening the way to support 1.05.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Eurozone’s manufacturing PMI finalized at 46.6, persistent contraction with glimmers of hope in the south

Eurozone PMI Manufacturing was finalized at a 10-month high of 46.6 in January, up from December's 44.4. Despite this, caution is advised as the index still hovers below the critical expansion threshold. Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, highlights that although there's been a consistent rise over the past three months, including in forward-looking indicators like new orders, the majority of the sub-indices, including the headline index, remain in the contraction zone.

This rebound in manufacturing is particularly evident in the "southern economies", with Greece leading at a 21-month high of 54.7 and both Spain (49.2) and Italy (48.5) showing encouraging trends. However, among the largest Eurozone economies, Germany, despite an 11-month high, remains in contraction at 45.5, and France's economic situation continues to be concerning, at 43.2.

The upward trend in sub-indicators such as stock of purchases, backlogs of work, and output, along with a growing optimism for higher output in the coming year, offers a glimmer of hope. This gradual recovery in the manufacturing sector, spearheaded by the southern economies, may serve as a crucial catalyst to pull the larger Eurozone economies out of the recessionary environment.

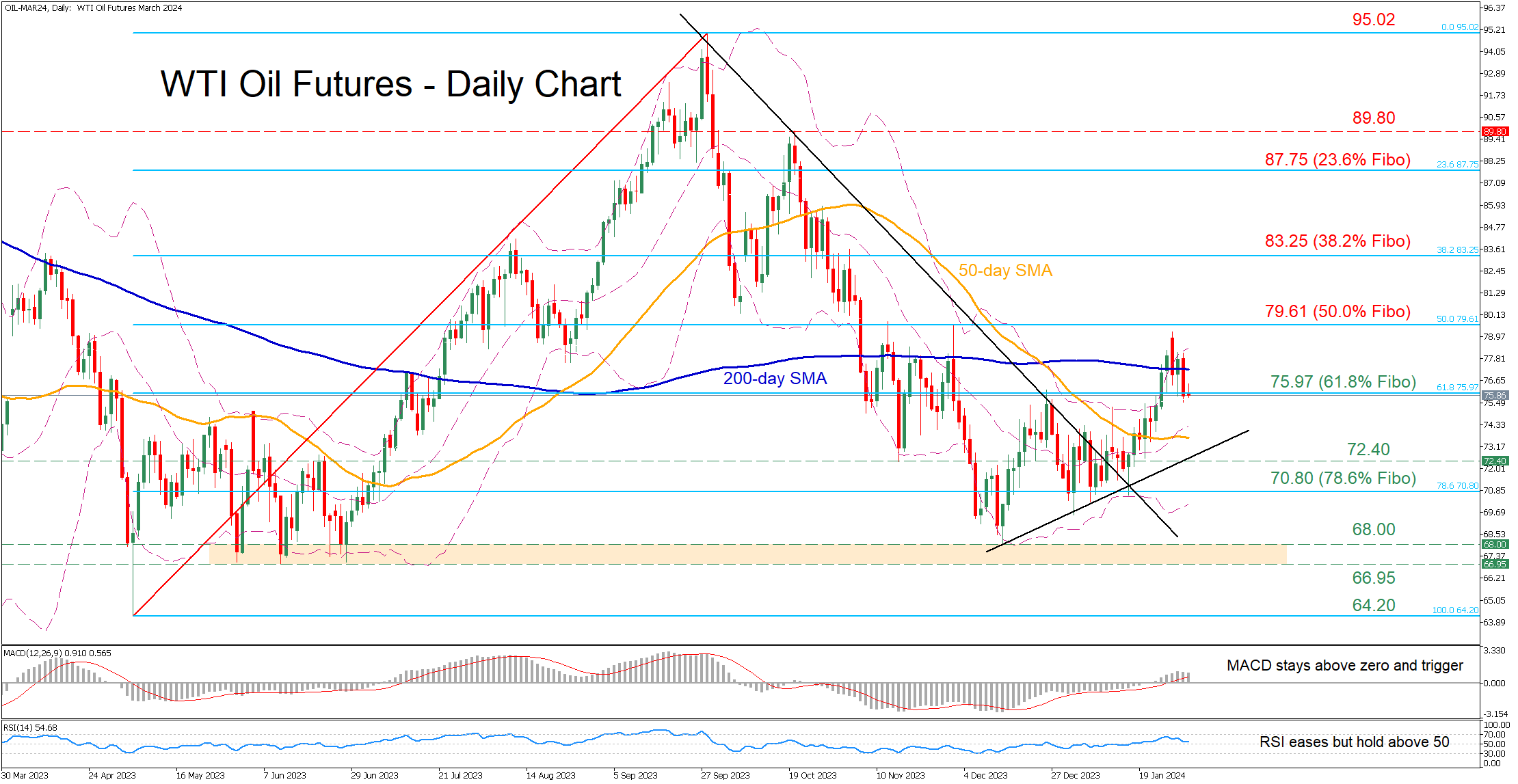

WTI Oil Futures Battle With 61.8% Fibo

- WTI futures retreat after hitting 2-month high

- Violate 200-day SMA but 61.8% Fibo pauses decline

- Momentum indicators weaken but remain positive

WTI oil futures (March delivery) had been staging a comeback from the December bottom of 68.00, jumping above both the 50- and 200-day simple moving averages (SMAs). However, the advance got rejected a tad below the 50.0% Fibonacci retracement of the 64.20-95.02 upleg, albeit the 61.8% Fibo prevented further retreats.

Should bearish pressures persist and the price dive below the 61.8% Fibo of 75.97, the November low of 72.40 could act as the first line of defence. Sliding beneath that floor, the price may descend towards the 78.6% Fibo of 70.80. A successful break below that zone could pave the way for the 66.95-68.00 support range defined by June lows and the recent six-month bottom.

On the flipside, if buyers re-emerge and propel oil above the 200-day SMA, immediate resistance could be found at the 50.0% Fibo of 79.61. Further upside attempts could then stall around the 38.2% Fibo of 83.25. Conquering this barricade, the bulls could attack the 23.6% Fibo of 87.75.

In brief, WTI oil futures experienced a downward spike following their rejection slightly below the 80.00 psychological mark, but the 61.8% Fibo has been acting as a strong floor. Hence, a clear close beneath the latter could accelerate the recent retreat.

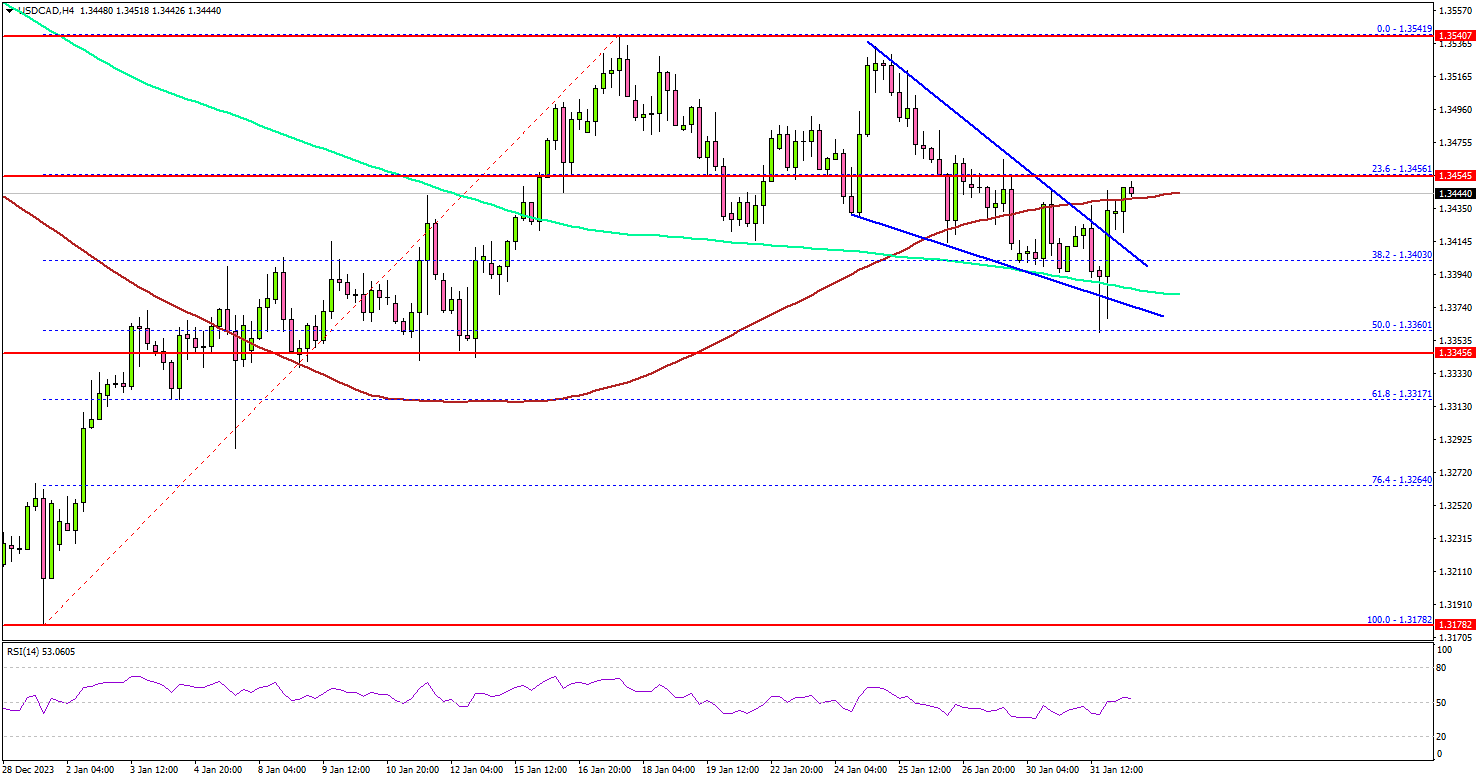

USD/CAD Bulls Aims Fresh Surge – Here’s Why

Key Highlights

- USD/CAD is moving higher from the 1.3320 support zone.

- It broke a key contracting triangle with resistance near 1.3420 on the 4-hour chart.

- EUR/USD is gaining bearish momentum below the 1.0820 support.

- The BoE interest rate decision is scheduled today (forecast 5.25%, versus 5.25% previous).

USD/CAD Technical Analysis

The US Dollar is showing positive signs from the 1.3250 zone against the Canadian Dollar. USD/CAD is gaining pace above 1.3400 and might continue to rise.

Looking at the 4-hour chart, the pair broke a key contracting triangle with resistance near 1.3420. Earlier, the pair found support near the 50% Fib retracement level of the upward move from the 1.3178 swing low to the 1.3541 high.

The pair is now trading above the 100 simple moving average (red, 4 hours) and the 200 simple moving average (green, 4 hours). On the upside, the bulls are facing hurdles near the 1.3450 level.

The next key resistance is near the 1.3500 level. A close above the 1.3500 zone could open the doors for more upsides. The next stop for the bulls might be 1.3550. Any more gains might send EUR/USD toward the 1.3620 level.

If there is another decline, the pair might find bids near the 1.3420 level. The main support sits near the 1.3360 level. If there is a downside break below the 1.3360 level, the pair could even dive below 1.3320. The next major support is 1.3250. Any more losses might call for a drop toward the 1.3200 support.

Looking at EUR/USD, the pair is gaining bearish momentum and there could be more losses below the 1.0800 support zone.

Economic Releases

- BoE Interest Rate Decision - Forecast 5.25%, versus 5.25% previous.

- US ISM Manufacturing Index for Jan 2023 – Forecast 47.0, versus 47.4 previous.

Pound Looking to Bank of England for Further Guidance

Markets

A mixture of market moving elements pushed US yields down yesterday from earnings over disappointing data to the Fed. Earnings news was perhaps not so much related to the likes of Microsoft & Alphabet as it was to New York Community Bancorp. The regional US bank rekindled March 2023 bank collapse fears after setting aside a big pile of cash to buffer for commercial real estate loan risks. Disappointing eco data (ADP job growth & ECI) added to the intraday decline with the Fed policy meeting delivering the final blow. The policy as expected stayed unchanged but the statement swapped its hawkish bias for a more balanced one. Chair Powell in the press conference noted inflation is on a promising track and the labour market is getting more balanced but he wants further confirmation before deciding to cut rates. He deflected several questions that gauged for a specific trigger or a timing. The only thing he wanted to disclose is that a cut in March (which was given a 50-50 chance in the previous days) isn’t the base case. Other than a temporary yield spike, it sparked market speculation for a first move in May. Powell did mention an in-depth study on the balance sheet runoff in March, suggesting a tweak to the current $95bn pace. Yields at the front end of the curve declined up to 13.6 bps, eventually closing around the intraday lows it hit earlier on the day. Longer maturities fell between 8.3-12 bps with safe haven flows strengthening the downleg into the close. US stock indices gapped lower at the open (earnings) and suffered an additional blow from Powell’s March comment. The Nasdaq underperformed with 2.23% losses. The US regional bank story was the dominant story for German yields as well, although slower-than-expected French inflation and in-line German CPI didn’t help either. The German curve lost 9.1-11.3 bps across all maturities. Risk aversion supported the dollar against the euro but not the yen. EUR/USD fell from 1.0845 to 1.0818. USD/JPY eased below 147.

US economic data today includes weekly jobless claims and the manufacturing ISM ahead of the payrolls report tomorrow. They’ll need to confirm the idea of an economy too resilient for fast and a lot of rate cutting if we want to see yields building/holding on the minor gains of this morning. More NY Community Bancorp news stories obviously serves as the wild card via the general risk climate. The latter is still fragile in early European dealings, keeping the US dollar in pole position for now. EUR/USD is testing the 1.0793 support area. The pound traded strong over the past couple of weeks and is now looking to the Bank of England for further guidance. The recent uptick in UK CPI leaves the central bank basically little options but to stress the need for a tight enough monetary policy but it wouldn’t be the first time Bailey surprises. EUR/GBP is nearing critical technical levels at the lower bound of the sideways trading range.

News & Views

The president of Japanese labor union UA Zensen, Matsuura, wants to raise wages enough for the BoJ to be able to take policy steps to correct the yen’s depreciation which has gone too far. The 1.8mn retail/restaurant union plans to push pay gains above 6% in an effort to start a virtuous wage-price cycle. Japanese largest labour union, Rengo, earlier called for 5% or more. Initial results of wage negotiations are due on March 15 with the next BoJ policy meeting scheduled for March 19. The Japanese yen strengthened from USD/JPY 147.75 to the high 146-area though the move is more linked to global risk sentiment and lower core bond yields.

Polish President Duda triggered a new escalation between him and new PM Tusk by sending the 2024 budget for a top court review. That court is packed by judges picked by the previous Law & Justice party, too which Duda is closely linked. The President threatened to further obstruct policy making by sending all legislation passed by the government for review until two Law & Justice officials, accused of abuse of power but pardoned by the president, are reinstated as lawmakers. The Polish zloty isn’t affected yet by the political bickering with EUR/PLN holding close to multi-year best PLN-levels (EUR/PLN 4.33).

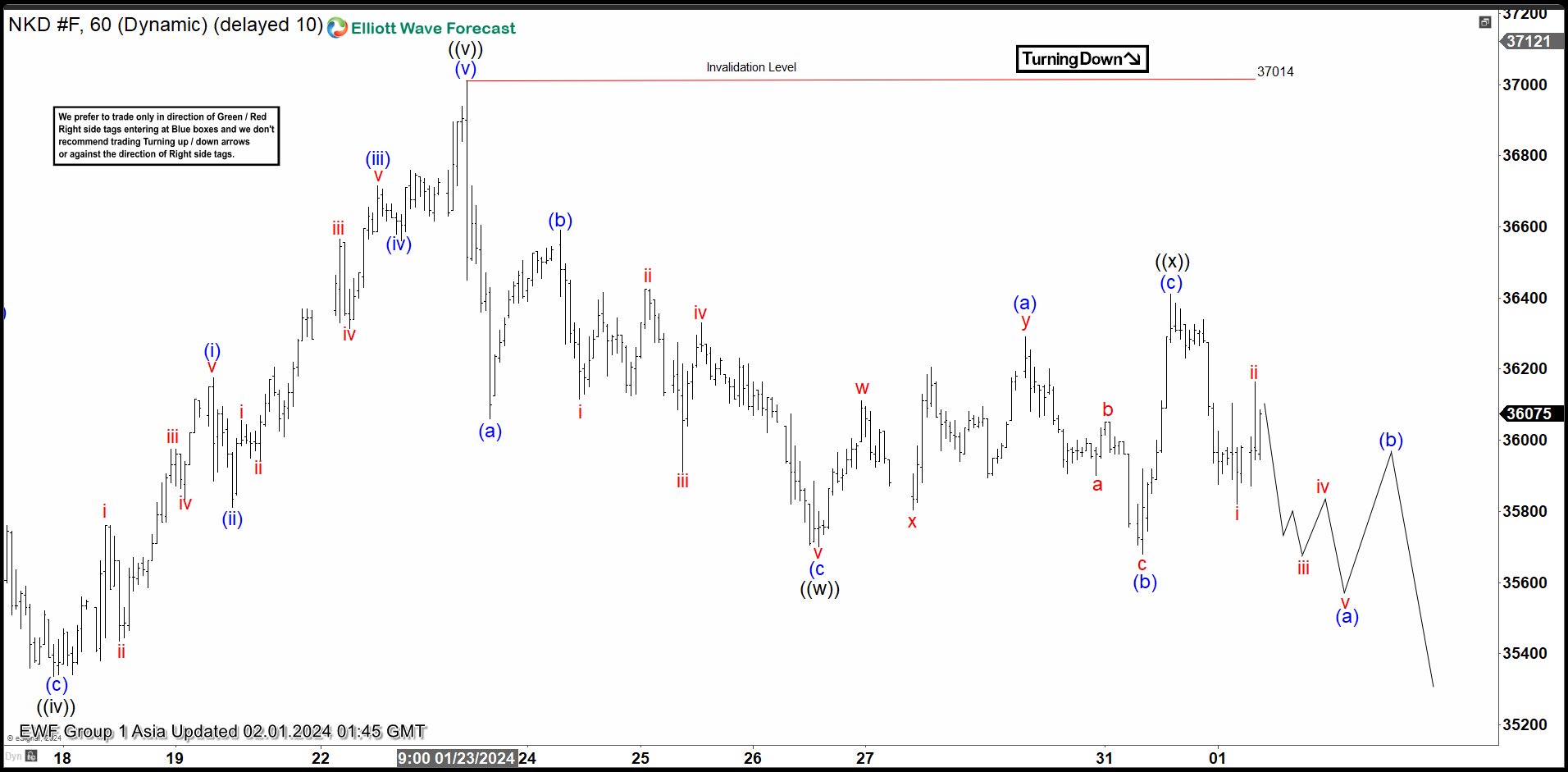

Nikkei (NKD_F) Looking for Further Downside Correction

Short Term Elliott Wave view in Nikkei (NKD_F) suggests that rally to 37014 ended wave 3. Wave 4 pullback is currently in progress as a double three Elliott Wave structure. Down from wave 3, wave (a) ended at 36060 and wave (b) ended at 36590. Down from there, wave i ended at 36115 and wave ii ended at 36425. Wave iii ended at 35910, wave iv ended at 36330, and final leg wave v ended at 35700. This completed wave (c) of ((w)) in higher degree. The Index then rallied in wave ((x)) with internal subdivision as an expanded flat.

Up from wave ((w)), wave (a) ended at 36290 and wave (b) ended at 35680. Wave (c) higher ended at 36410 which completed wave ((x)) in higher degree. The Index has turned lower in wave ((y)), but it still needs to break below wave ((w)) at 35700 to rule out any double correction. Down from wave ((x)), wave i ended at 35820 and wave ii ended at 36165. Expect the Index to see further downside to end wave (a) of ((y)) as an impulse. Then it should rally in wave (b) of ((y)) before turning lower again in wave (c) of ((y)) of 4. Near term, as far as pivot at 37014 high stays intact, expect rally to fail in 3, 7, 11 swing for further downside.

Nikkei (NKD_F) 60 Minutes Elliott Wave Chart

NKD_F Elliott Wave Video

https://www.youtube.com/watch?v=J6srm5Rnpe0

Oh No

We knew that yesterday was not going to be a bright day, as Microsoft, Google and AMD have all seen a negative market reaction to their fantastic quarterly results that failed to match the huge market expectations. And because most investors have been waiting in ambush for the slightest misstep to take advantage of selling the overstretched tech rally, the tech stocks got hammered after Microsoft’s light guidance for the current quarter. Microsoft fell more than 2.5% from a record high, Google tumbled more than 7%, AMD lost 2.5% and Nvidia retreated about 2%.

Yesterday’s tech selloff was broadly expected before the session opened. What was not expected however was a surprise Q4 loss at New York Community Bancorp – which slashed its dividend following its asset purchases from the bankrupt Signature Bank led to higher loan-loss provisions and charge-offs. The bank also warned of building trouble in the office-space sector. New York Community Bancorp shares tumbled near 38% yesterday, bringing back the worries regarding the US regional banks, the commercial real estate threat, and the possibility of seeing other small regional players go into trouble. As such, the SPDR’s S&P Regional Banking ETF sold off nearly 6%, and even big banks which have largely benefited from the regional banks’ misfortune last year traded down.

Apple, Amazon and Facebook’s Meta will post results after the bell today. They’d better blow investors’ minds. Otherwise, the tech selloff is poised to gather momentum – despite the falling yields.

Speaking of yields

Resurfacing worries of another potential bank stress sent the US yields tumbling yesterday. The US 2-year yield tipped a toe below 4.20%, and the 10-year yield sank below 4% on a weaker than expected ADP report, lower than expected employment cost in Q4, on news that US Treasury will stop increasing the size of its auctions starting from May, and of course on fear that another bank stress could hurt the US growth and get the Federal Reserve (Fed) to hurry up on cutting rates to calm down the market nerves. But we are not there just yet!

The Fed has kept its rates unchanged at yesterday’s meeting as expected, they removed the statement that talked about ‘additional policy firming’ and replaced it with ‘rate cuts won’t be appropriate until the committee has gained greater confidence that inflation is moving sustainably toward 2%’.

More importantly, Jay Powell hinted at a slowdown in the pace of QT in the foreseeable future. And that’s a big deal, as unwinding QT will leave the market with more liquidity than otherwise, and all that extra liquidity that are not sucked away could continue to be in the financial markets and support asset prices. In summary, we may not see a rate cut right away, but a slowing QT sounds better for relaxing the financial conditions asset valuations than your regular rate cuts. What’s sure is that the Fed will never ever be able to pull out the GFC and pandemic liquidity out of the market. Ever. Enjoy.

Coming back to rates, Powell wanted it to be clear for everyone that a rate cut in March in UNLIKELY. Still, activity on Fed fund futures gives around 65% chance for a March rate cut as yesterday’s bank worries play in favour of a sooner rather than a later rate cut. But remember, the last time the US went through a decent banking stress, the US economy didn’t slow. Or if did, it still eked out an above average growth.

In the FX, the US dollar swung between gains and losses yesterday, and is slightly above its 200-DMA at the wake of the latest Fed decision. The EURUSD extends losses to 1.08 psychological mark as French and German inflation figures were soft enough to keep inflation worries and the European Central Bank (ECB) hawks at bay. With both the ECB and Fed meetings out of the way, the next natural target for the euro bears is the 100-DMA which stands at the 1.0775.

Across the Channel, the Bank of England (BoE) will give its latest policy verdict today. British policymakers will likely push back on early rate cut expectations after the latest inflation numbers in the UK revealed a mini U-turn in easing price dynamics. But Brits are expected to deliver a brighter outlook for their economy, lower inflation forecasts and open the door for rate cuts later this year.

The sharp fall in US yields amid the mounting US regional bank worries sent the 10-year gilt yield below the 3.80% level yesterday, but gilts had their worst month since May, the FTSE 100 recorded its first drop since October, and sterling topped at 1.2830 against the greenback. Improved economic forecasts and a balanced hawkish tone should contain the selling pressure in sterling, but Cable is more likely to test 1.25 than 1.30 in the foreseeable future.

Powell Pushes Back on Rate Cut Expectations

In focus today

In the euro area, focus is on the inflation print for January today. We expect HICP to decline to 2.8% y/y from 2.9% in December and core inflation to decline to 3.2% y/y from 3.4%. The prints from the individual countries we have received this week indicate that we are close to hitting our expectations. Our core inflation estimate implies another month with a monthly inflation rate that is consistent with the 2% target when annualized. We also get the unemployment rate for December, which we expect remained at 6.4% as indicated by the PMI employment index.

In the UK, we expect the Bank of England to keep the Bank Rate unchanged at 5.25%, which is in line with consensus and current market pricing. Overall, we expect the MPC to deliver a dovish tilt to its guidance coupled with a downward revision to its inflation forecast, see more in Bank of England Preview - Topside risk to EUR/GBP as BoE removes tightening bias, 26 January.

In Sweden the Riksbank is not expected to make any changes to the policy rate, and given that it is a "smaller" meeting without a full monetary report or new macroeconomics forecasts it could be argued that the meeting is the least exciting in a while. We will look for verbal tweaks to the repo rate path suggesting it will cut the repo rate by summer. QT is expected to be raised from 5bn SEK per month to 7bn.

From the US, ISM Manufacturing Index will be released for January while preliminary labour productivity data is due for release for Q4. Earlier flash PMIs pointed towards an uptick in manufacturing activity, while the Fed will keep a close eye on productivity, where the recent surprisingly brisk growth has helped to ease the rise in unit labour costs.

Economic and market news

What happened overnight

In China the Caixin PMI was unchanged from a month ago at 50.8, hence according to this release China's manufacturing sector expanded for the third consecutive month. This means that we continue to see the Caixin PMI being elevated compared to the national NBS PMI survey, which in yesterday's release were 49.2.

What happened yesterday

In the US the Fed kept its monetary policy unchanged as widely expected, hence rates were kept at 5.25-5.50%. Powell signalled optimism on inflation but pushed back on expectations for a March cut. We stick to our call for a first cut in March followed by gradual quarterly reductions thereafter, as we think the approach still fits well with the Fed's risk management stance. Market prices in around 35% probability for the March cut. For more details, see Research US - Fed review: In a risk management mode, 31 January. On the data front, labour costs increased less than expected by 0.9% in Q4 against 1.2% in Q3. This is still on the high side for the Fed. However, it is a dovish signal since it is trending downward more than expected. The ADP report signalled signs of cooling labour market. It came in at 107K, much lower than the expected 145K and the December print was revised downwards.

Yesterday in the US we saw renewed fears in the market for turmoil in the banking sector. The New York Community Bancorp (NYCB), the bank that bought the failed Signature Bank after last year's bank turmoil closed down 38%, having dropped to 46% earlier. The drop came after the bank's earnings dropped and it cut its dividends, which executives from the bank said was a result of its deal to take over Signature Bank. Combined with Powell pushing back on rate cuts and disappointing earnings from the US tech giants, equities in the US dropped during yesterday's session. S&P500 dropped 1.6%, which is the biggest drop since September.

German HICP inflation was in line with consensus expectation at -0.2% m/m but slightly lower on the yearly growth rate at 3.1% y/y (cons: 3.2% y/y). French inflation was weaker than expected in January. French HICP rose 3.4% y/y (cons: 3.6% y/y, prior: 4.1% y/y) and monthly HICP came in at -0.2% m/m (cons: -0.1% m/m, prior: 0.1% m/m). As mentioned earlier, the country data overall points towards euro area being in line with expectations at tomorrows release.

Equities: Global equities were somewhat lower yesterday with sizeable US underperformance. Very high intraday volatility with big news coming from both earnings, macro and the monetary side. Tech, growth and a broader set of cyclicals were led lower although yields came down as well. One could think this sounds like a classic risk-off, but that was not the case as part of the drop in yields came from benign wage data in the US. Hence, this was much more about some profit taking after too high hopes and a strong run in equities leading up to this. In US yesterday, Dow +0.8%, S&P 500 -1.6%), Nasdaq -2.2% and Russell 2000 -2.5%. Asian markets are more positive this morning lifted by Chinese markets as officials are signalling more stimuli will be coming. US futures are higher while European futures are marginally lower.

FI: Yesterday's myriad of key events was overshadowed by new uncertainty on US regional banks following the earnings release from NY Bancorp. Bund yields fell about 10bp across the curve throughout the day, while peripherals underperformed by a couple of basis points. Credit spreads widened with Bund/Schatz ASW-spreads following the US banking jitters, and implied volatility in swaptions market added to the rising tendency seen over the past weeks. UST yields fell through the FOMC meeting despite Powell's statement, that March is not the most likely timing for the first cut.

FX: EUR/USD was in for a whirlwind yesterday, first from inflation data out in Europe, then renewed concerns about the health of US regional banks and then hawkish pushback from Powell. In the end, EUR/USD finished close to the 1.08 level and about flat on the day. The amount of foreign exchange that Norges Bank purchases on behalf of the government was left unchanged yesterday and EUR/NOK ended the day higher. Today, focus turns to euro area inflation data for January and the Riksbank and Bank of England monetary policy meetings.

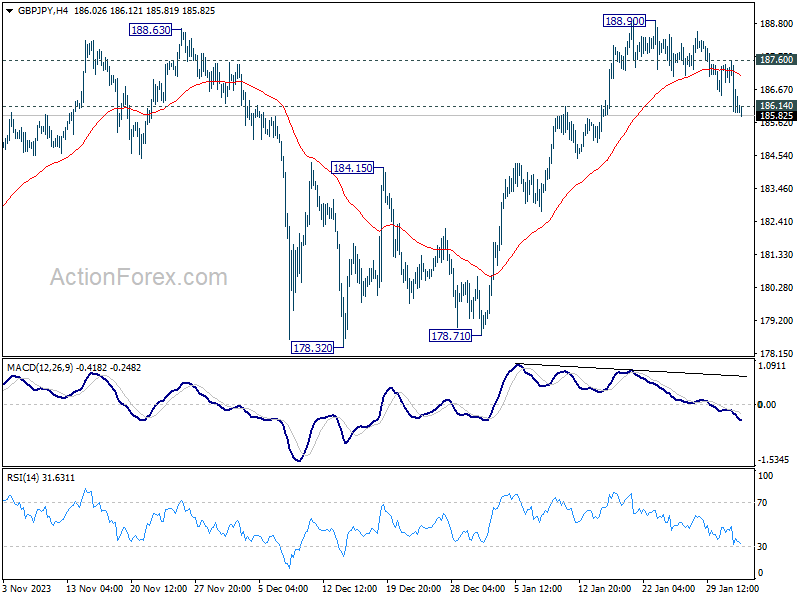

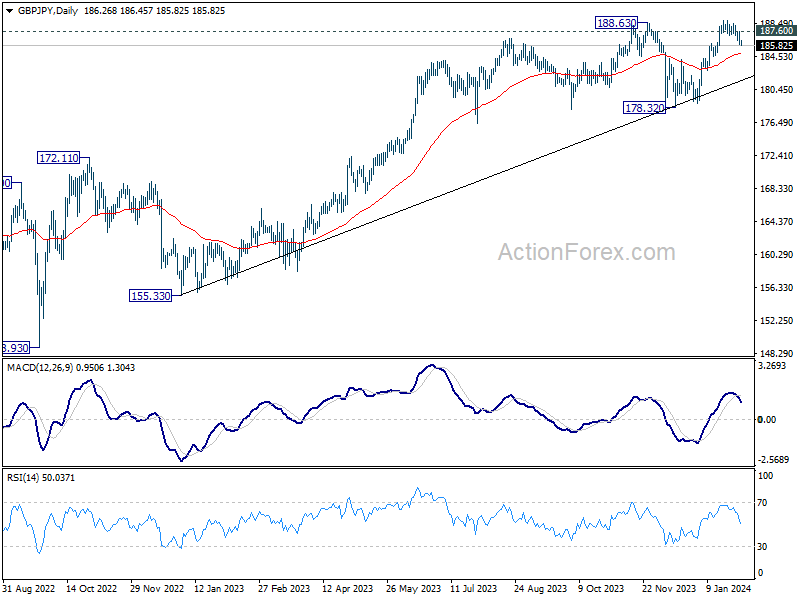

GBP/JPY Daily Outlook

Daily Pivots: (S1) 185.74; (P) 186.68; (R1) 187.39; More...

GBP/JPY's break of 186.14 minor support confirms short term topping at 188.90. Intraday bias is back on the downside for deeper pull back to 55 D EMA (now at 184.89) and possibly below. On the upside, break of 187.60 minor resistance will argue that the pull back has completed, and bring retest of 188.90 instead.

In the bigger picture, up trend from 123.94 (2020 low) in in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

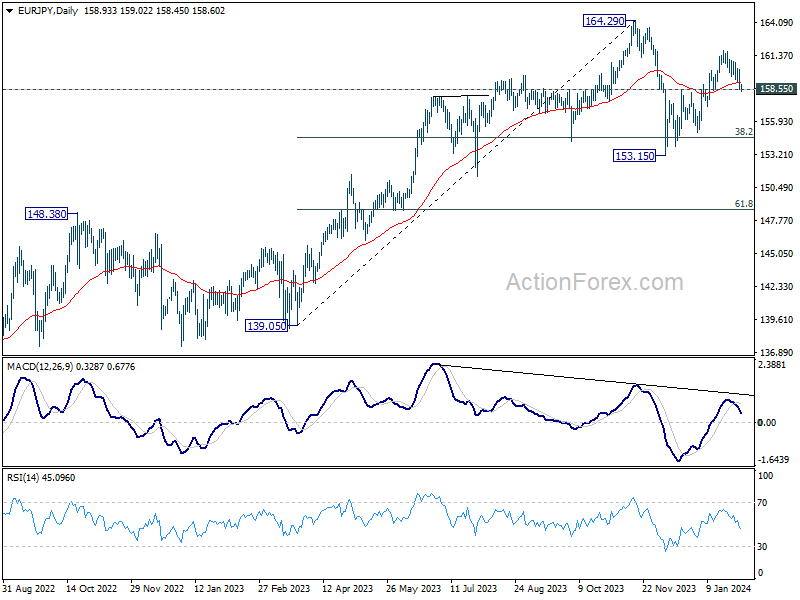

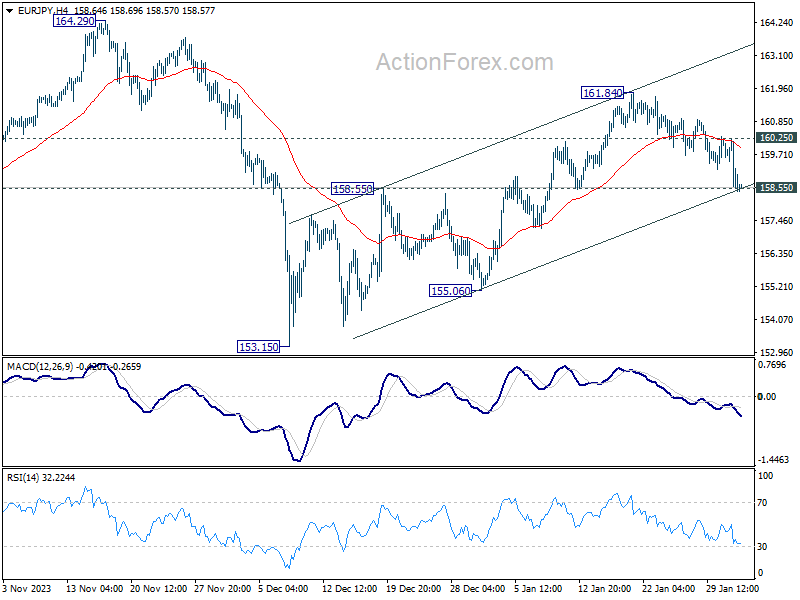

EUR/JPY Daily Outlook

Daily Pivots: (S1) 158.28; (P) 159.28; (R1) 159.98; More...

Immediate focus is now on 158.55 support in EUR/JPY. Sustained break there will argue that rebound from 153.15 has completed at 161.84 already. Fall from there is then seen as the third leg of the pattern from 164.29 high. Intraday bias will be turned back to the downside for 155.06 support next. On the upside, above 160.25 minor resistance will retain near term bullishness, and bring retest of 161.84 first.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 only. As long as 148.48 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage.