Sample Category Title

USDCAD Rally Likely Fail in 3, 7, 11 Swing

Short Term Elliott Wave view in USDCAD suggests that rally to 1.354 ended wave (B). Pair has since turned lower in wave (C). However, confirmation is needed to validate this view and pair still needs to break below the previous low on 12.27.2023 at 1.3172. Down from wave (B), wave (i) ended at 1.3475 and rally in wave (ii) ended at 1.3528. Pair extended lower in wave (iii) towards 1.3417 and wave (iv) ended at 1.3444. Final leg wave (v) ended at 1.3413 which completed wave ((i)). Pair then rallied in wave ((ii)) which subdivides into a zigzag structure.

Up from wave ((i)), wave (a) ended at 1.349 and pullback in wave (b) ended at 1.3425. Wave (c) higher ended at 1.3534 which completed wave ((ii)). Pair has turned lower in wave ((iii)) towards 1.3411 and rally in wave ((iv)) ended at 1.3467. Pair then made another low in wave ((v)) as a diagonal. Down from wave ((iv)), wave (i) ended at 1.3424 and wave (ii) ended at 1.3465. Wave (iii) lower ended at 1.3397, wave (iv) ended at 1.3446, and wave (v) ended at 1.3396. This completed wave ((v)) of 1 in higher degree. Expect pair to rally in wave 2 to correct cycle from 1.17.2024 high before it resumes lower. Near term, as far as pivot at 1.354 high stays intact, expect rally to fail in 3, 7, 11 swing for further downside.

USDCAD 45 Minutes Elliott Wave Chart

USDCAD Elliott Wave Video

https://www.youtube.com/watch?v=dJgU-m8T8x4

Risk is Fed Powell Doesn’t Want to Sound Too Hawkish

Markets

The EU economy avoided a recession in 2023H2 (0.0% q/q growth in Q4) thanks to southern Europe while inflation readings from Spain (and Belgium) showed price pressures reaccelerating. The latter pushed euro area yields higher, with changes in Germany amounting to 2.6-3.8 bps across the curve. Consumer confidence in the US (Conference Board), meanwhile, rose to the highest since December 2021 (114.8) thanks to a sharp improvement in the current assessment (best since the pandemic hit). Job openings in the country unexpectedly picked up again from 8925k to 9026k for a third month straight in December. The quits rate, which indicates confidence in finding a new job after quitting one, stabilized around pre-pandemic highs. Yesterday’s numbers triggered a US yield spike but it was a long shot given the looming Fed policy meeting. The US curve eventually flattened with the front adding 1.5 bps still but longer maturities shedding up to 6.3 bps (30-y). Bourses finished with gains in Europe and mixed in the US. EUR/USD ended an uninspired session a fraction higher at 1.0845. Sterling ahead of the BoE meeting and in a technical setback after nearing the lower bound of the May sideways EUR/GBP trading range lost ground. EUR/GBP rose to 0.854.

A jampacked eco calendar kicked off this morning in China where PMI business confidence creeped a little higher to 50.9 (composite). The minutes of last week’s BoJ meeting revealed rising internal pressure to exit the sub-zero rate environment with one policymaker arguing the central bank risks missing the window of opportunity. GJGB’s lose ground this morning. The yen trades flat. Sticking to central banks, the Fed meets later today. The policy rate will remain untouched. Powell’s pushback against current (in our view too aggressive) market pricing will be critical. The risk is he doesn’t want to sound too hawkish since inflation does ease, creating room for rate cuts at some point in time. That, however, could trigger a bond rally and ease financial conditions further before the Fed even started doing so. The latest meeting minutes flagged the debate about tapering QT (currently $95b/month) has begun. Powell could use that theme as a lightning rod. Discussing and deciding over QT first buys the central bank some time before moving on to rate cuts. If successful and markets do pare some of the excessive bets, we may see a modest yield advance. If US data later this week (payrolls, ISM) underscore the message, there is potential for something larger. The US dollar should appreciate in line with rising US yields, especially against an ailing euro. Inflation figures from Germany and France following the Spanish example could limit the damage for EUR but nothing more.

News & Views

Australian inflation slowed more than expected, from 1.2% Q/Q in Q3 2023 to 0.6% Q/Q in Q4 (vs 0.8% consensus and 0.9% RBA estimate). It was the smallest quarterly rise since Q1 2021. Y/Y inflation fell from 5.4% to 4.1% (vs 4.3% expected) which is the slowest pace since Q4 2021. Underlying details show that housing (+1.5% Q/Q for new dwellings) remains one of the more sticky inflation components, driven by high labour and material costs. It’s a trend seen in other nations as well. The increase in rental prices (+0.9% Q/Q) would have been even higher if it weren’t for changes to rent assistance (+2.2%). Underlying inflation measures slowed slightly more than hoped as well. The annual trimmed mean rose by 0.8% Q/Q and by 4.2% Y/Y. Today’s inflation figures suggest that the RBA at next week’s meeting could pivot away from its hawkish guidance to a more neutral stance preparing the road for rate cuts. The RBA will have the backing of new growth and inflation forecasts. The Aussie dollar underperforms this morning with AUD/USD trading at 0.6560 (YTD low at 0.6526). AUD swap rates drop up to 18 bps for the 3-yr.

The German Council of Economic Experts yesterday published some possible proposals to changing the country’s debt brake. The constitutional rule limits Germany’s structural deficit to 0.35% of GDP since 2016. It was suspended during the Covid-pandemic and after Russia’s invasion in Ukraine. The GCEE finds the rule more rigid than necessary currently, restricting fiscal space for future-oriented expenditure. One proposal would be a softer transition period after periods of suspension. Another would tie the structural deficit to certain debt-to-GDP threshold, allowing a higher structural deficit when debt is low. The debt brake came back into focus after Germany’s constitutional court last year slammed off-budget vehicles to circumvent it. Any changes to the rule would require a 2/3rd majority in German parliament with the liberal FDP and the CDU opposing any changes for the moment.

Anything Less Than Mind-Blowing is Meh

We had good news, bad news and news that are fundamentally good for the economy and bad for the global rate cut expectations.

Good news. The European economies performed better than expected last quarter. Spanish and Italian growth tempered the German contraction, fueled the idea that the Eurozone is also having a lighter version of ‘soft landing’. The IMF raised its global growth forecast from 2.9% to 3.1% this year saying that the strong US growth and stimulus measures in China should show in better growth numbers. Yes, but the latest PMI numbers showed that manufacturing in China shrank for the 4th month and the CSI 300 index already gave back all gains accumulated on last week’s series of stimulus news; the China story remains in limbo.

Bad news. Good growth in Spain came along with an unexpected jump in inflation. More euro area countries will be releasing their inflation figures today. And given that growth numbers were better-than-expected, a set of stronger-than-expected inflation data for the Eurozone should throw a floor under the euro’s weakness, by weakening the European Central Bank (ECB) doves’ hands. The euro which partially reversed yesterday’s losses, is still under a decent selling pressure this morning with a crowded resistance into the 200-DMA which stands near the 1.0840 level. The current market pricing suggests a 75% chance for an April ECB cut. But April feels early with the upside risks building for inflation. Therefore, uptick inflation figures could help the EURUSD go back above its 200-DMA.

All eyes on the Fed

The Federal Reserve (Fed) will announce its latest decision today and Jay Powell will tell investors about his version of where things are going. Data-wise, we had a mixed bag of news from the US as well, both in terms of economic data and corporate results.

The bad good news was that the US job openings increased in December - not cool when you helplessly want the US jobs market to loosen so that the Fed could cut rates.

But the bad, good news is that we still have many layoff news on the headlines. PayPal cuts 2500 jobs, UPS plans 12’000 job cuts, Meta, Amazon, Google and even Microsoft cut jobs. So far in January, 23’500 jobs were terminated.

The ADP report is expected to print a fairly soft 145K new private job openings in January.

Anything less than mind-blowing is weak

Microsoft released its latest quarterly results after the bell yesterday. Both earnings and revenue were better than expected, the cloud unit Azure made 30% more last quarter compared to the final quarter of last year where OpenAI was not yet part of our lives. Their results overshadowed Google’s cloud business – which grew only 24% more than the same time a year earlier.

BUT. But Microsoft stocks fell up to 2% in the afterhours trading because the company gave a light quarterly outlook. Anything less than mind-blowing is weak at the current valuations. Therefore, profit taking in Microsoft and elsewhere is perhaps on today’s menu. Google fell almost 6% and AMD fell more than 6% in the afterhours trading after their results failed to match expectations.

Is this the beginning of profit-taking and correction? Could be. The S&P500 has been running from record to record this January, mostly due to the extension of the Big Tech rally. MAMAA stocks are up by more than 10% since the beginning of January. Nvidia – which became the icon of the AI rally and which hit a fresh record yesterday, is up by almost 35% since the beginning of this month. Investors have been piling in despite overbought market conditions and overstretched valuations. Yet the earnings misstep could well be a trigger for long-awaited profit taking across the US technology stocks. If that’s the case, even a soft Fed could hardly make investors feel better.

Bear in mind that despite the rise in interest rates last year, technology stocks, which are usually responsive to Federal Reserve rates, largely disregarded these increases. The dominance of AI in the market overshadowed every economic development. It's worth noting that profit-taking might occur even in the face of potential improvements in financial conditions.

Focus Turns to the Fed

In focus today

Tonight at 20:00 CET the rate decision of this week's meeting in the FOMC is announced. We expect no monetary policy changes. With no new economic projections, focus will be on Powell's remarks in the press conference starting at 20:30 CET. We do not expect the meeting to be a major market mover, but see risks tilted towards a modestly hawkish reaction if Powell pushes back against the notion of rapid rate cuts and/or end to QT. Read more in our Fed preview - Patience and gradualism, 26 January. On the data front, January ADP private sector employment and Q4 Employment Cost Index will be released ahead of the rate decision.

In the euro area focus today is on German and French inflation data for January that will give an indication of where we can expect the euro area print to land tomorrow.

In China, Caixin PMI for January is due out. It has increased in the past two months, and we see some downside risk in January. The Caixin PMIs have been higher than the NBS version that we got overnight, where we saw an increase, see below. We expect the two figures to converge. In December the Caixing Manufactuing PMI was 50.8.

Economic and market news

What happened overnight

In China we got the official PMIs from NBS. Manufacturing PMI increased a little from 49.0 to 49.2. Hence, manufacturing remains in contractionary territory for the fourth month in a row. Service PMI increased from 50.4 to 50.7.

In Australia we got fourth quarter CPI. Consumer prices rose 0.6% q/q SA (Q3 1.2%, Consensus 0.8%), while RBA's key measure of underlying inflation, the trimmed-mean CPI, grew 0.8% (Q3 1.2%, consensus 0.9%). That said, the easing in underlying inflation came in mostly from the goods side, while services price pressures remained more persistent. We have argued that the market pricing for the Reserve Bank of Australia's rate path has been too hawkish relative to the Fed. After the release, markets are now pricing more than 50% probability of a first cut already in May.

What happened yesterday

In the US there were 9.026mn job openings in December. This is higher than in November where 8.925 job openings and exceeded expectations at 8.750mn. Labour demand remains elevated, which is a hawkish signal for the Fed. Layoffs increased modestly, but at the same time hiring picked up after somewhat weaker November. Conference Board's January Consumer survey paints a similar positive picture, as Jobs plentiful index rose (45.5; Dec. 40.4). Consumer confidence generally improved as well, especially the current situation assessment rebounded. Inflation expectations continue easing, which is naturally a positive thing for the Fed.

The euro area economy stagnated in the last quarter of 2023 as Q4 GDP growth came in at 0.0% q/q. While activity stagnated in Q4, it was far from collapsing amid a strong labour market. Overall, the growth figures buy ECB more time before the first interest cut. Spanish inflation in January was higher than expected when looking at both headline and core, posing as a topside risk to the euro area print. Headline HICP at 3.5% (cons: 3.0%, prior: 3.3%) and core CPI at 3.6% (cons: 3.3%, prior: 3.8%). We knew that energy inflation would be high as government support measures were rolled back, but the uptick in core also suggests sizeable menu price adjustments.

The European Commission economic confidence indicators were stable in January as both service and industry confidence ticked marginally up. Selling price expectations in the service sector increased for the fifth consecutive month mimicking the PMI service output prices, a sign that service inflation still poses an upside risk for the inflation outlook.

In Sweden we got the NIER economic tendency survey for January. It showed a broad-based rise in all business sectors and in consumer confidence. Hiring plans also gained, a positive sign for the labour market. When it comes to price plans, these rose in manufacturing but remain in a pre-pandemic range. More importantly, price plans dropped slightly in both retail trade and private services, but they remain too high.

Saudi Arabia's surprise decision to scrap a planned investment to increase oil production capacity 1mb/d might carry great symbolic weight but should not affect oil prices in the short run. The Saudis have about 3md/d spare capacity as it is, which it could quickly tap into should oil prices rise above, e.g. USD100/bbl.

Equities: Global equities were lower yesterday with banks and value in substantial outperformance. Not surprisingly, the macro print of both a stronger than expected JOLT and consumer confidence boosted the higher-for-longer scenario. Yields were also higher in the move, but it is worth nothing the inflation expectation dropping in the consumer confidence survey. Hence, the higher-for-longer is growth- and not inflation-driven which is the perfect outcome for the banks. In US Dow +0.4%, S&P 500 -0.1%, Nasdaq -0.8% and Russell 2000 -0.8%. Asian markets are mixed this morning, Japan is higher while China is leading the rest lower. European futures are mixed while US tech futures are lower after some late hour disappointing tech reporting yesterday.

FI: EGB yields drifted higher during yesterday's session as national inflation figures for Spain and Belgium came in stronger than expected (0.6% MoM and 0.5% MoM, respectively). 10Y Bund yields rose 3bp throughout the day, while the 2Y point ended up 5bp. 10Y UST yields fell during the evening, now trading marginally above 4%. The Bund ASW-spread widened slightly, while long inflation swap rates (e.g. 5y5y) rose a couple of basis points. The German 30Y syndication yesterday saw very strong demand, indicating that the appetite for duration is currently strong. The bid-to-cover ratio came in at a substantial 12.3. Today, Germany will tap EUR4.5bn in the 10Y segment (2.2% 2034).

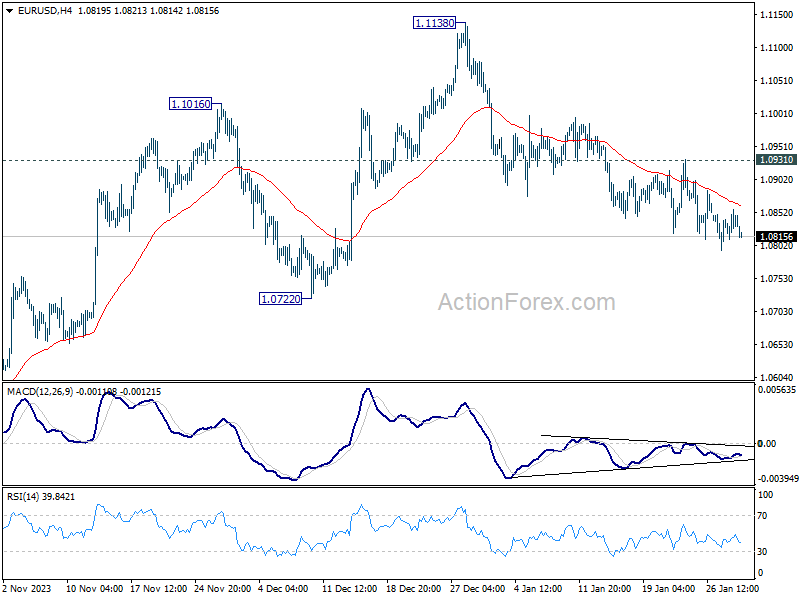

FX: EUR/USD remains below the 1.0850 mark in another strong session for the broad USD where US data surprised to the topside. Today focus turns to the Fed meeting. EUR/NOK ended the day higher with focus today on Norges Bank announcement of the fiscal NOK sales pace for February, where we see the risk of an increase to the sales amount, which could act as a headwind for NOK. AUD/USD fell overnight after Australian Q4 inflation data came out below expectations.

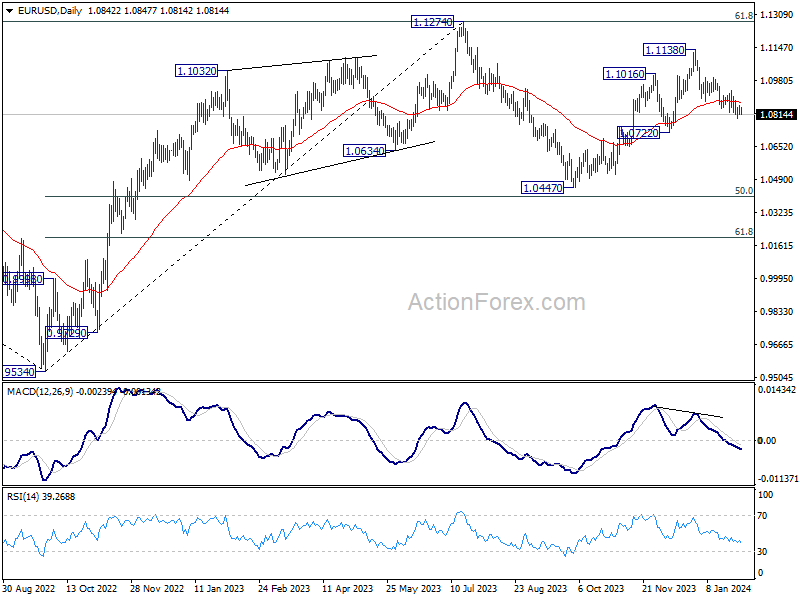

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0820; (P) 1.0838; (R1) 1.0865; More...

Intraday bias in EUR/USD stays on the downside at this point. Fall from 1.1138 is in progress to 1.0722 support first. Decisive break there will argue that whole rise from 1.0447 has completed, and target this low. However, on the upside, break of 1.0931 will turn bias back to the upside for stronger rebound instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

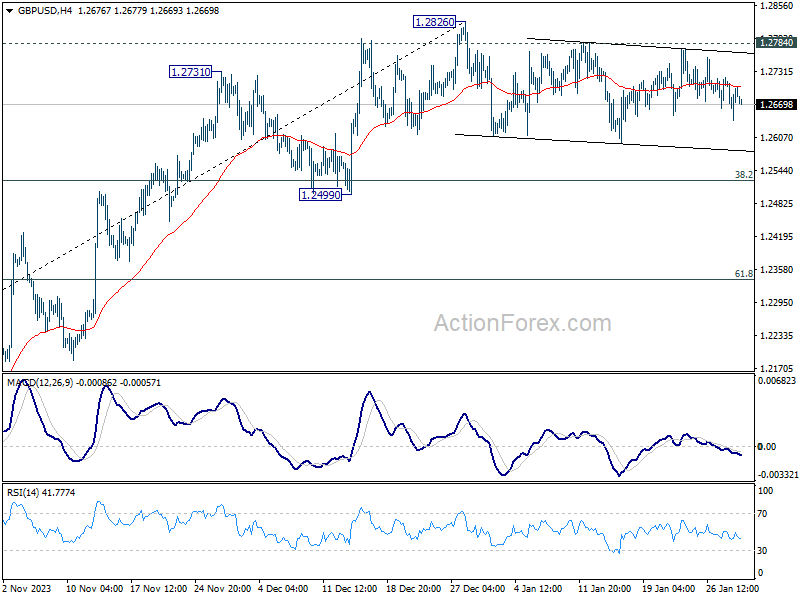

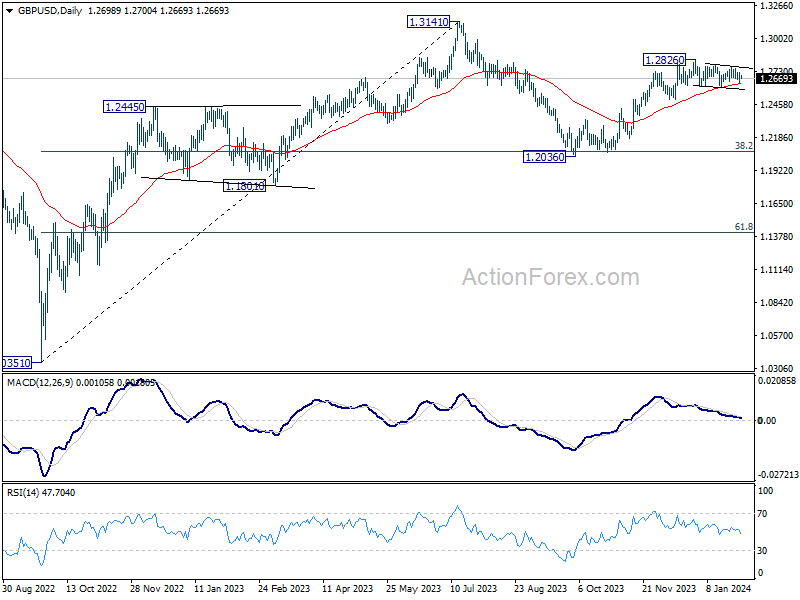

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2653; (P) 1.2687; (R1) 1.2734; More...

Intraday bias in GBP/USD remains neutral at this point, as sideway trading continues. Another fall cannot be ruled out, but downside should be contained above 1.2499 support to bring rebound. On the upside, firm break of 1.2784 resistance will suggest that consolidation pattern has completed. Further rise should be seen through 1.2826 to resume the rally from 1.2036. Next target will be 1.3141 high.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

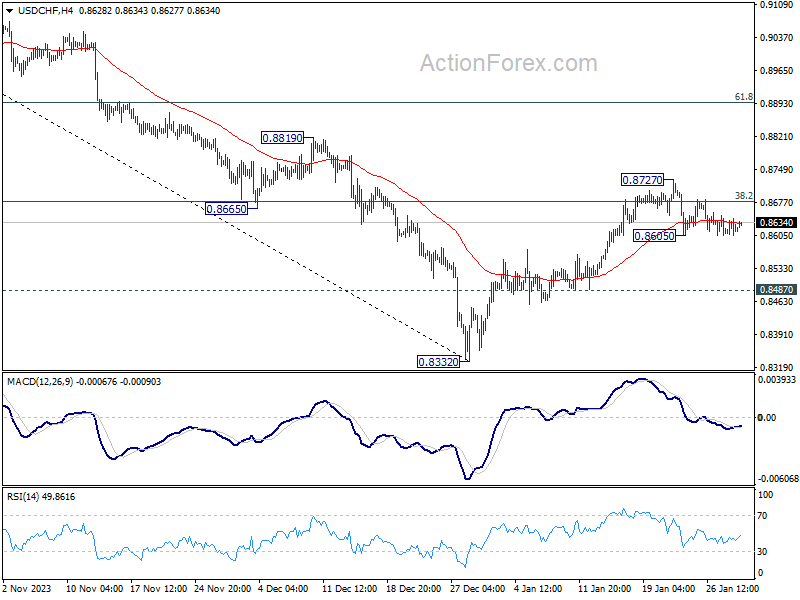

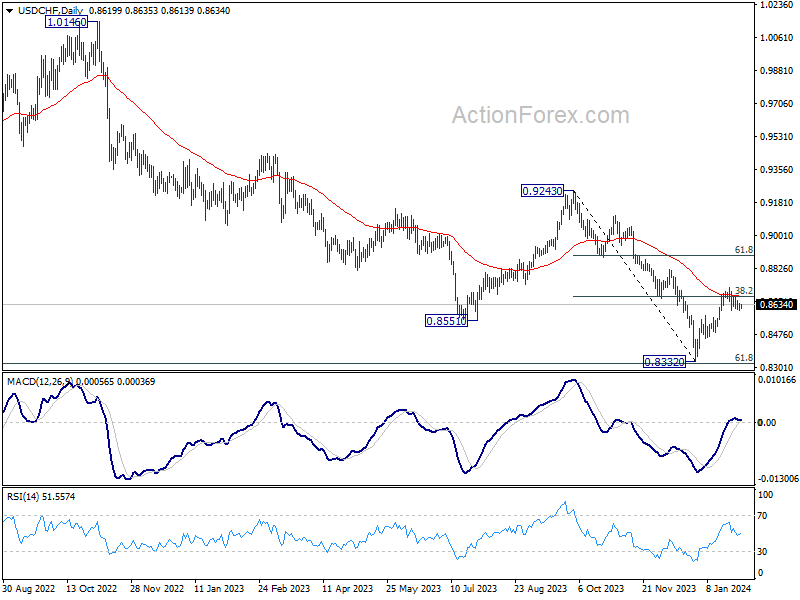

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8602; (P) 0.8622; (R1) 0.8639; More....

Intraday bias in USD/CHF remains neutral and outlook is unchanged. On the downside, below 0.8605 will resume the pull back from 0.8727 to 0.8487 support. Break there will argue that rebound from 0.8332 has completed, and bring retest of this low. On the upside, firm break of 0.8727 will resume the rebound to 61.8% retracement of 0.9243 to 0.8332 at 0.8995 instead.

In the bigger picture, while rebound from 0.8332 could be strong, there is no clear sign of medium term bottoming yet. This rebound is tentatively seen as a corrective move for now. Also, outlook will stay bearish as long as 0.9243 resistance holds. Larger down trend from 1.0146 (2022 high) should resume through 0.8332 low at a later stage.

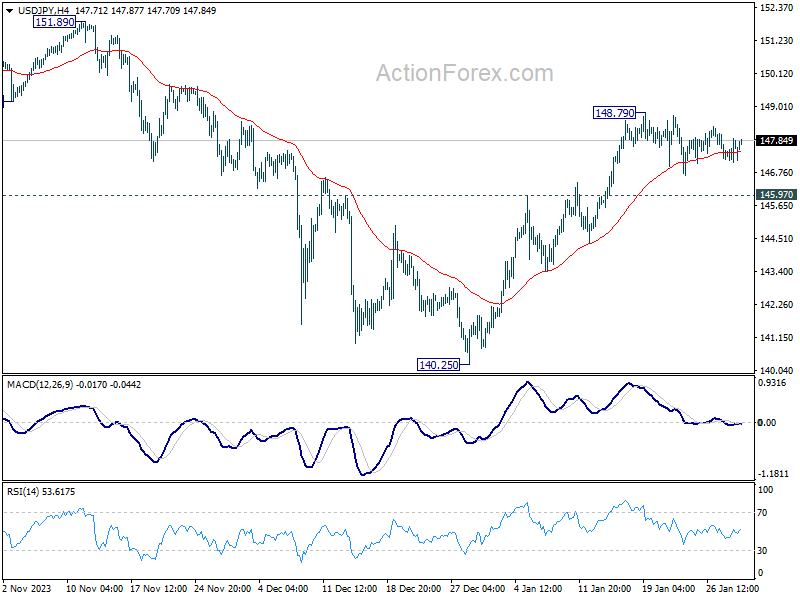

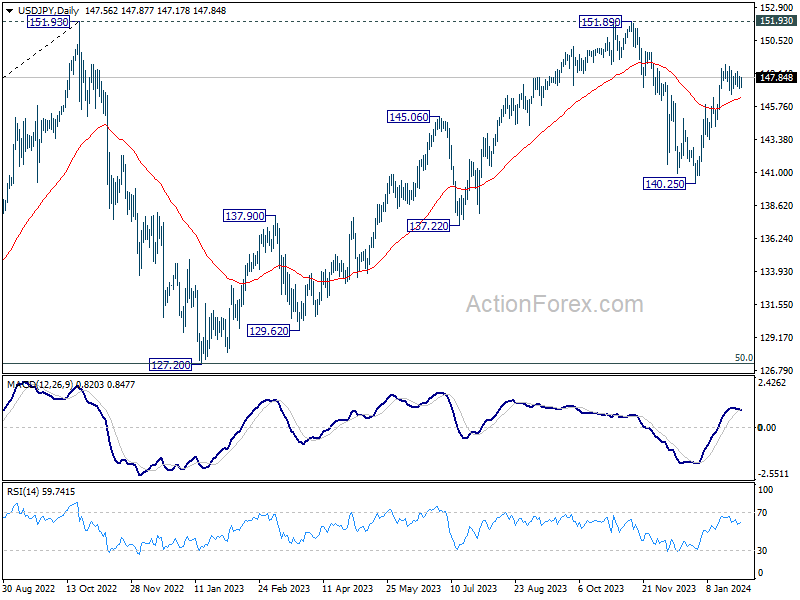

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.16; (P) 147.54; (R1) 147.99; More...

Intraday bias in USD/JPY stays neutral at this point as consolidation from 148.79 is still extending. With 145.97 resistance turned support intact, further rally is in favor. As noted before, corrective fall from 151.89 should have completed at 140.25 already. Break of 148.79 will resume the rise from there for retesting 151.89/93 key resistance zone.

In the bigger picture, stronger than expected rebound from 140.25 dampened the original bearish review. Strong support from 55 W EMA (now at 142.33) is also a medium term bullish sign. Fall from 151.89 could be a correction to rise from 127.20 only. Decisive break of 151.89/93 will confirm resumption of long term up trend. This will now be the favored case as long as 140.25 support holds.

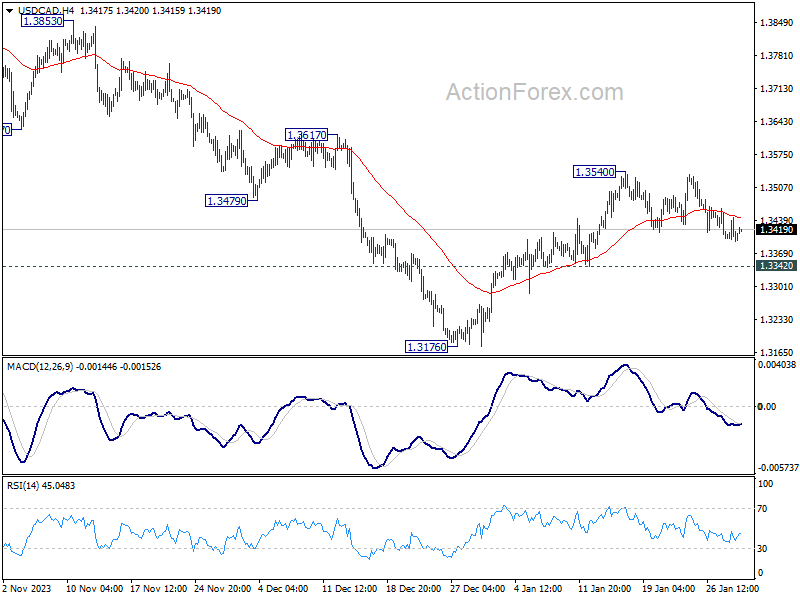

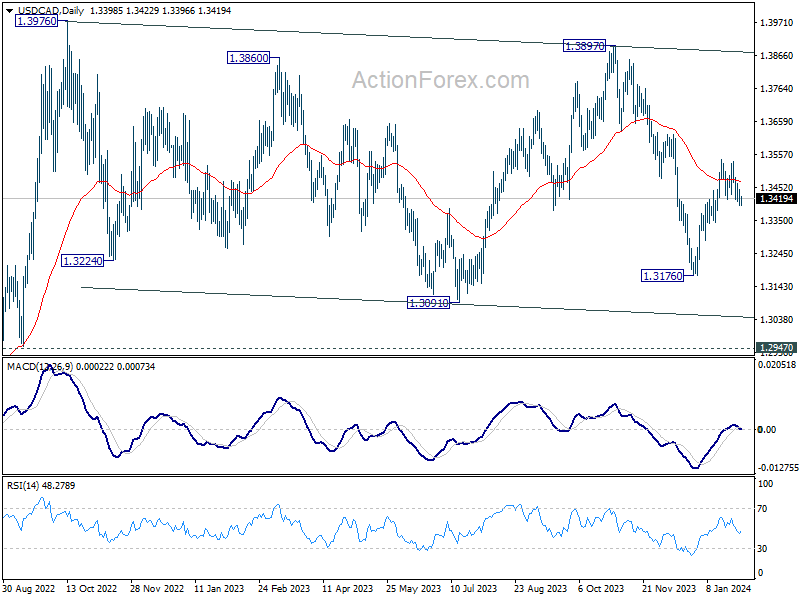

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3381; (P) 1.3413; (R1) 1.3431; More...

Intraday bias in USD/CAD stays mildly on the downside and deeper fall could be seen to 1.3342 support. Firm break there will argue that rebound from 1.3176 has completed at 1.3540, and target this low for resuming whole fall from 1.3897. On the upside, however, break of 1.3540 will resume the rebound from 1.3176 instead.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

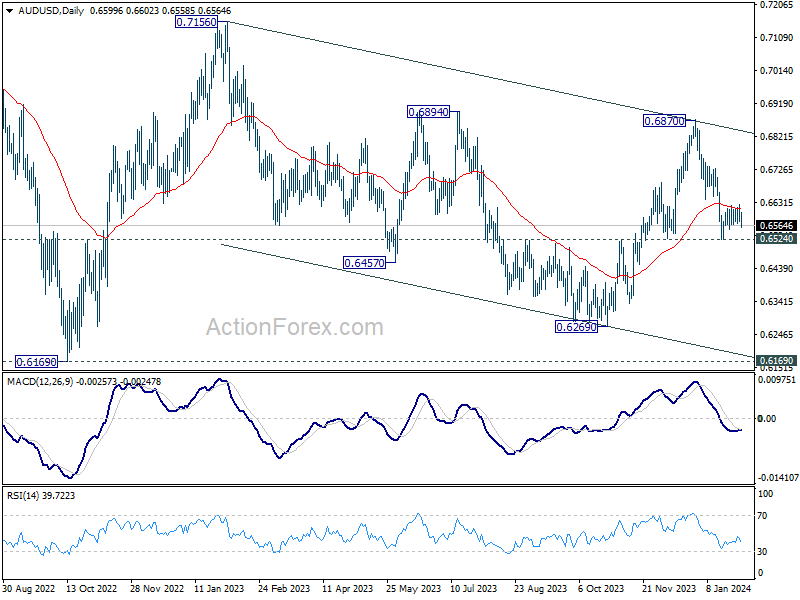

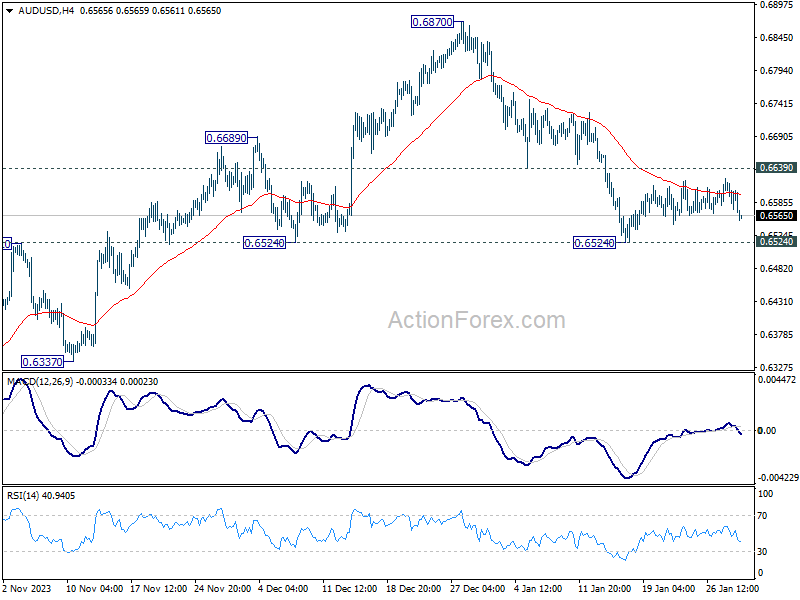

AUD/USD Daily Report

Daily Pivots: (S1) 0.6577; (P) 0.6601; (R1) 0.6626; More...

AUD/USD dips notably today but still stays in range of 0.6524/6639. Intraday bias remains neutral and further fall is still expected. On the downside, firm break of 0.6524 support will argue that whole rebound from 0.6269 has completed, and bring deeper fall to this support. On the upside, however, firm break of 0.6639 will turn bias back to the upside for stronger rebound instead.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.