Sample Category Title

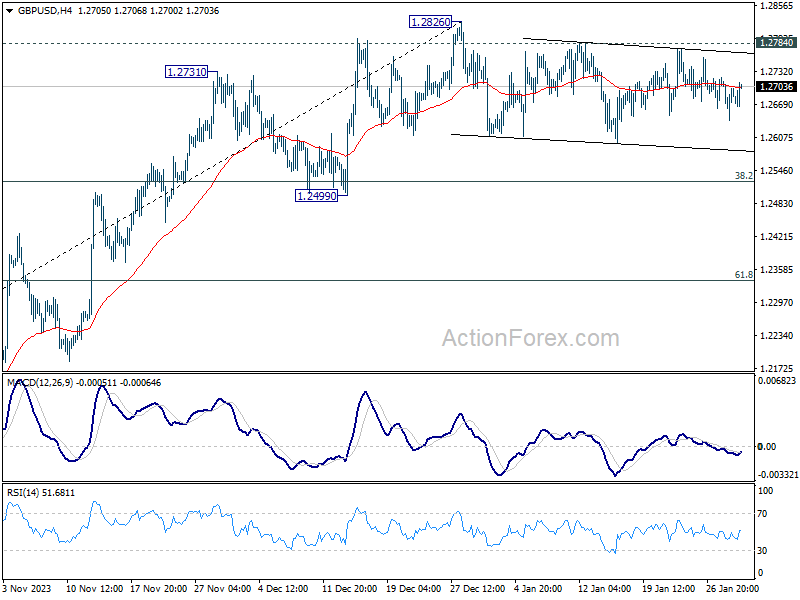

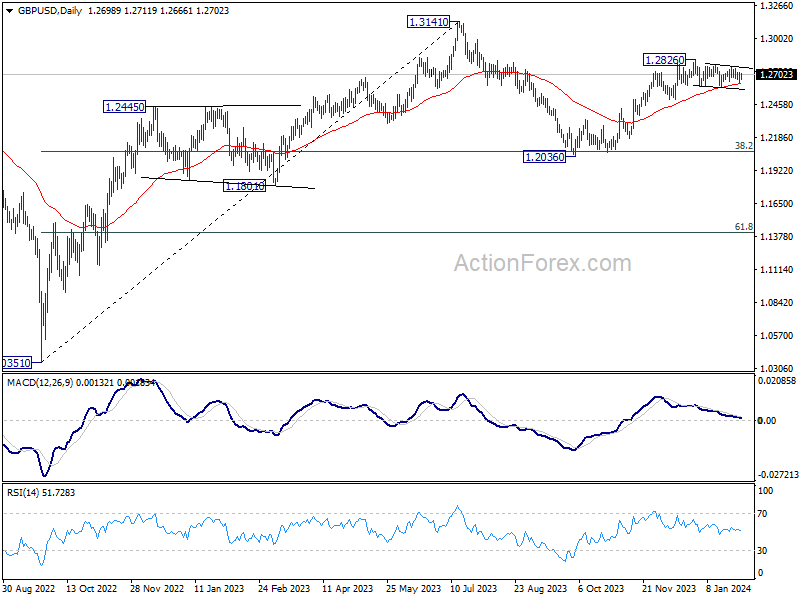

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2653; (P) 1.2687; (R1) 1.2734; More...

Range trading continues in GBP/USD and intraday bias remains neutral. Another fall cannot be ruled out, but downside should be contained above 1.2499 support to bring rebound. On the upside, firm break of 1.2784 resistance will suggest that consolidation pattern has completed. Further rise should be seen through 1.2826 to resume the rally from 1.2036. Next target will be 1.3141 high.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Dollar Dips on Weak ADP Jobs Data; Markets Await FOMC Outcome

Dollar weakens slightly in early US session, as dragged down by disappointing ADP private sector job data. Despite this, the downturn is contained, as market participants remain cautious ahead of FOMC rate decision later in the day. While no changes in interest rates are anticipated, considerable attention is centered on Fed Chair Jerome Powell's commentary. A prevalent risk is that if Powell's tone is not sufficiently assertive on inflation, it might be construed as a dovish inclination, and with markets responding correspondingly.

Other major currencies are displaying a lack of significant movement too, with most pairs and crosses hovering within yesterday's range. Euro is showing resilience against Germany's lower-than-expected CPI data and dovish remarks from ECB Vice-President. On the other hand, Canadian Dollar is gaining mild traction, bolstered by Canada's GDP data that surpassed expectations. Australian Dollar remains the weakest link, pressured by Australia's inflation figures falling short of forecasts, though it's attempting to regain some ground. Sterling is trading within a narrow range as the market also awaits BoE's rate decision tomorrow. Japanese Yen continues its near-term consolidation.

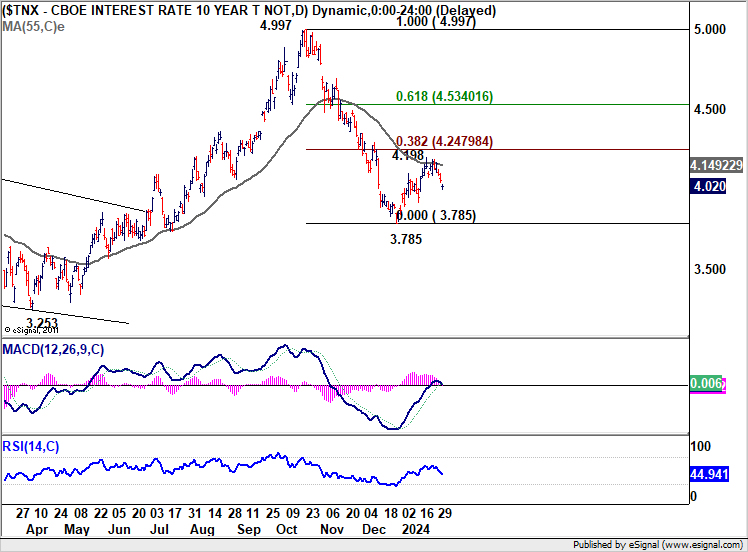

Technically, US 10-year yield is worth some attention today. This week's decline is raising the chance that rebound from 3.785 has already completed at 4.198, ahead of 38.2% retracement of 4.997 to 3.785 at 4.247, and after rejection by 55 D EMA. Sustained break of 4.000 handle will affirm this case, and bring deeper fall back towards 3.785 low. If materialized, such a development in yields could exert downward pressure on Dollar or at least limit its upward momentum.

In Europe, at the time of writing, FTSE is up 0.15%. DAX is down -0.12%. CAC is up 0.15%. UK 10-year yield is down -0.029 at 3.876. Germany 10-year yield is down -0.037 at 2.237. Earlier in Asia, Nikkei rose 0.61%. Hong Kong HSI fell -1.39%. China Shanghai SSE fell -1.48%. Singapore Strait Times rose 0.09%. Japan 10-year JGB yield rose 0.245 to 0.736.

Canada's GDP grows 0.2% mom in Nov, primarily driven by goods-production sectors

Canada's GDP grew 0.2% mom in November, above expectation of 0.1% mom. Growth was primarily driven by goods-producing industries, which marked the highest expansion rate since January 2023 at 0.6% mom.

Services-producing industries experienced a modest increase of 0.1% mom during the same period. This slight rise came despite the adverse impacts of strikes within Quebec's public sector, which began in November.

Overall, 13 of 20 industrial sectors increased in November.

Additionally, preliminary data suggests continued upward trend, with an anticipated increase of 0.3% mom in real GDP for December.

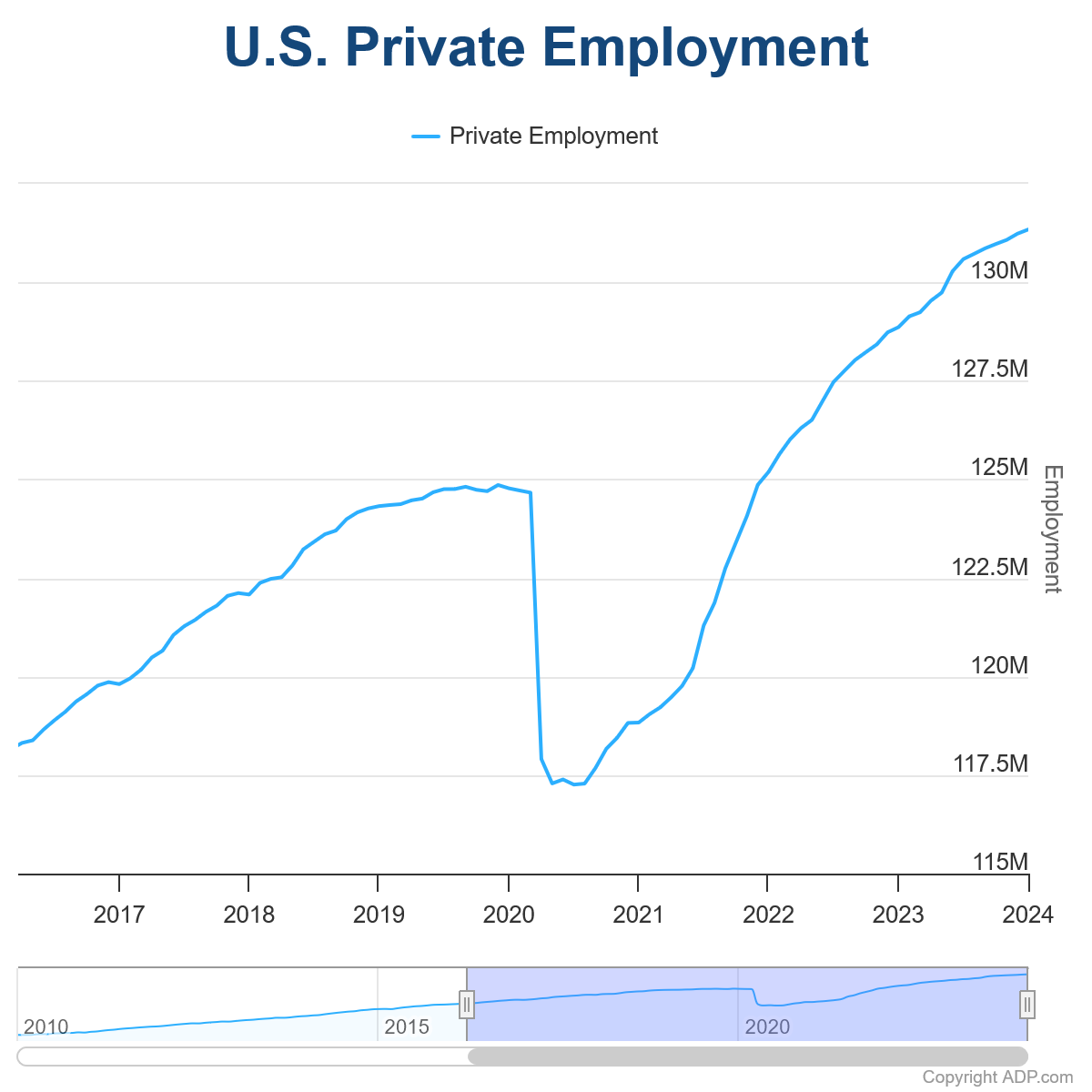

US ADP jobs grows 107k, below expectation 143k

US ADP private employment grew 107k in January, below expectation of 143k. By sector, goods-producing jobs rose 30k while service-providing jobs rose 77k. By establishment size, small companies added 25k jobs, medium added 61k, large added 31k.

Pay gains for job-stayers slowed from 5.4% yoy to 5.2% yoy. Pay gains for job-changers slowed to 7.2% yoy, smallest gain since May 2021.

"Progress on inflation has brightened the economic picture despite a slowdown in hiring and pay," said Nela Richardson, chief economist, ADP. "Wages adjusted for inflation have improved over the past six months, and the economy looks like it's headed toward a soft landing in the U.S. and globally.

ECB's de Guindos see lower growth and inflation than Dec forecasts

ECB Vice President Luis de Guindos, in an interview with Die Zeit, offered indicated that the growth forecast for the region, previously set at 0.8% for this year, might fall short of expectations.

De Guindos highlighted several factors contributing to this revised outlook, saying, "The prospects have even deteriorated." He pointed out the key issues impacting the forecast: a slowdown in world trade, heightened geopolitical uncertainties, and the more rapid than anticipated impact of ECB's interest rate hikes on the economy.

De Guindos also touched upon inflation trends, noting a shift from previous projections. The December projections had inflation returning to the 2% target by the second half of 2025. However, recent data suggest a more optimistic scenario.

De Guindos observed, "But inflation figures have mostly brought positive surprises recently." He further speculated that inflation might settle "slightly lower" than their predictions.

BoJ summary of opinions suggests rate hike within reach

The Summary of Opinions from BoJ's meeting on January 22-23 signaled the central bank's intensified focus on initiating its first rate hike since 2007 and moving away from its long-standing negative interest rate policy. The deliberations, however, stopped short of providing a clear timeline for these policy shifts.

A notable hawkish sentiment within BoJ pointed to the "growing possibility" of significant wage revisions in the upcoming spring, at "relatively higher levels" than in the past. This perspective is underpinned by the recognition of "improving trend" in both economic activities and price. Such developments suggest that the necessary conditions for revising monetary policy, including ending the negative interest rate regime, are increasingly "being met".

Concurrently, the impact of Noto Peninsula Earthquake on is a key factor under close observation. One opinion suggested that, after a thorough assessment of the earthquake's effects over "the next one or two months", BoJ is "highly likely to reach a point where it can normalize monetary policy".

On the other side of the spectrum, a more cautious stance was also expressed. While acknowledging that the probability of achieving the BoJ's 2 percent price stability target is becoming "more realistic", it was noted that certainty in reaching this goal is not yet fully established. However, this view also supports the initiation of discussions regarding the exit from the current monetary policy stance.

Japan's industrial production rises 1.8% mom in Dec, a bounce in seesawing pattern

Japan's industrial production rose 1.8% mom in December, rebounding from prior month's -0.9% mom contraction, but missed expectation of 2.4% mom.

Manufacturers have tempered expectations for the coming months, predicting a -6.2% mom drop in production in January, followed by a modest 2.2% mom increase in February. The Ministry of Economy, Trade and Industry maintains its assessment of "seesawing" on production.

As an METI official indicated, the recent Noto Peninsula earthquake's impact on manufacturing appears minimal for January. However, production forecasts are clouded by the suspension of operations at Daihatsu due to issues with collision-safety test irregularities.

"Although we believe that the production sentiment of companies is gradually getting out of the bearish phase, for the time being, we need to pay attention to the impact of the suspension of auto manufacturers' operation," the official said.

In separate release, retail sales grew 2.1% yoy in December, well below expectation of 5.0% yoy.

Australia's CPI down to 4.1% yoy in Q4, monthly CPI down to 3.4% yoy in Dec

Australia's inflation data for Q4 show notable easing in price pressures. CPI rose by 0.6% qoq, a considerable slowdown from the previous quarter's 1.2% qoq and below expectation 0.8% qoq. This marks the smallest quarterly increase since Q1 2021. On an annual basis, CPI decelerated from 5.4% yoy to 4.1% yoy, coming in lower than the forecasted 4.3% yoy.

RBA's trimmed mean CPI, which is a measure of core inflation, also reflected this trend. It increased by 0.8% qoq and 4.2% yoy, down from 1.2% qoq and 5.2% yoy respectively in the previous quarter. These figures were below the expected 0.9% qoq and 4.3% yoy. Notably, this represents the fourth consecutive quarter of declining annual trimmed mean inflation, falling from a peak of 6.8% in Q4 2022.

Additionally, monthly CPI showed a sharp slowdown from 4.3% yoy to 3.4% yoy, undershooting expectation of 3.7% yoy.

NZ ANZ business confidence rises to 36.6, inflation expectations lowest since Nov 2021

New Zealand ANZ Business Confidence rose from 33.2 to 36.6 in January. However, Own Activity Outlook fell from 29.3 to 25.6.

In a significant development, inflation expectations decreased from 4.61% to 4.28%, reaching their lowest point since November 2021. Despite this decline in inflation expectations, a high number of firms still plan to increase their prices, with the pricing intentions index only marginally decreasing from 50.2 to 49.7. Cost expectations also saw a slight reduction, moving from 76.2 to 75.6, but they remain at elevated levels.

ANZ's commentary on the situation pointed out that the New Zealand economy is at a critical point, expressing a cautiously optimistic outlook. They anticipate that RBNZ has implemented sufficient tightening measures and expect a gradual realization of their impact, leading to a possible initiation of "a steady stream of OCR cuts" by August.

China's NBS PMI manufacturing ticks up to 49.3, contraction continues

China's manufacturing sector remained in contraction for the fourth consecutive month, with NBS PMI Manufacturing index marginally rising from 49.0 to 49.3 in January, slightly below the expected 49.3.

The continued manufacturing contraction is evident in the subindexes: new orders was 49.0, marking the fourth month of contraction, while new export orders index stood at 47.2, contracting for the tenth consecutive month. A concerning detail is the employment subindex, which fell to a 13-month low of 47.6, indicating contraction for 11 straight months.

On a positive note, the manufacturing sector's production index attained a 4-month high, advancing to 51.3, and has sustained expansion for eight consecutive months.

In contrast, PMI Non-Manufacturing saw a slight improvement, rising from 50.4 to 50.7, marginally above the forecast of 50.6. Consequently, PMI Composite, which encompasses both manufacturing and services sectors, reached a four-month peak of 50.9, up from 50.3 in the previous month.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2653; (P) 1.2687; (R1) 1.2734; More...

Range trading continues in GBP/USD and intraday bias remains neutral. Another fall cannot be ruled out, but downside should be contained above 1.2499 support to bring rebound. On the upside, firm break of 1.2784 resistance will suggest that consolidation pattern has completed. Further rise should be seen through 1.2826 to resume the rally from 1.2036. Next target will be 1.3141 high.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 23:50 | JPY | Industrial Production M/M Dec P | 1.80% | 2.40% | -0.90% | |

| 23:50 | JPY | Retail Trade Y/Y Dec | 2.10% | 5.00% | 5.30% | 5.40% |

| 00:00 | NZD | ANZ Business Confidence Jan | 36.6 | 33.2 | ||

| 00:30 | AUD | CPI Q/Q Q4 | 0.60% | 0.80% | 1.20% | |

| 00:30 | AUD | CPI Y/Y Q4 | 4.10% | 4.30% | 5.40% | |

| 00:30 | AUD | RBA Trimmed Mean CPI Q/Q Q4 | 0.80% | 0.90% | 1.20% | |

| 00:30 | AUD | RBA Trimmed Mean CPI Y/Y Q4 | 4.20% | 4.30% | 5.20% | |

| 00:30 | AUD | Monthly CPI Y/Y Dec | 3.40% | 3.70% | 4.30% | |

| 00:30 | AUD | Private Sector Credit M/M Dec | 0.40% | 0.40% | 0.40% | |

| 01:00 | CNY | NBS Manufacturing PMI Jan | 49.2 | 49.3 | 49 | |

| 01:00 | CNY | NBS Non-Manufacturing PMI Jan | 50.7 | 50.6 | 50.4 | |

| 05:00 | JPY | Housing Starts Y/Y Dec | -4.00% | -6.20% | -8.50% | |

| 05:00 | JPY | Consumer Confidence Jan | 38 | 37.6 | 37.2 | |

| 07:00 | EUR | Germany Import Price Index M/M Dec | -1.10% | -0.50% | -0.10% | |

| 07:00 | EUR | Germany Retail Sales M/M Dec | -1.60% | 0.60% | -2.50% | |

| 07:30 | CHF | Real Retail Sales Y/Y Dec | -0.80% | 0.90% | 0.70% | -1.50% |

| 08:55 | EUR | Germany Unemployment Change Jan | -2K | 10K | 5K | |

| 08:55 | EUR | Germany Unemployment Rate Jan | 5.80% | 5.90% | 5.90% | |

| 09:00 | CHF | Credit Suisse Economic Expectations Jan | -19.5 | -23.7 | ||

| 09:00 | EUR | Italy Unemployment Dec | 7.20% | 7.50% | 7.50% | 7.40% |

| 13:00 | EUR | Germany CPI M/M Jan P | 0.20% | 0.20% | 0.10% | |

| 13:00 | EUR | Germany CPI Y/Y Jan P | 2.90% | 3.40% | 3.70% | |

| 13:15 | USD | ADP Employment Change Jan | 107K | 143K | 164K | |

| 13:30 | CAD | GDP M/M Nov | 0.20% | 0.10% | 0.00% | |

| 13:30 | USD | Employment Cost Index Q4 | 0.90% | 1.00% | 1.10% | |

| 14:45 | USD | Chicago PMI Jan | 48.2 | 46.9 | ||

| 15:30 | USD | Crude Oil Inventories | -0.8M | -9.2M | ||

| 19:00 | USD | Fed Interest Rate Decision | 5.50% | 5.50% | ||

| 19:30 | USD | FOMC Press Conference |

Canada’s GDP grows 0.2% mom in Nov, primarily driven by goods-production sectors

Canada's GDP grew 0.2% mom in November, above expectation of 0.1% mom. Growth was primarily driven by goods-producing industries, which marked the highest expansion rate since January 2023 at 0.6% mom.

Services-producing industries experienced a modest increase of 0.1% mom during the same period. This slight rise came despite the adverse impacts of strikes within Quebec's public sector, which began in November.

Overall, 13 of 20 industrial sectors increased in November.

Additionally, preliminary data suggests continued upward trend, with an anticipated increase of 0.3% mom in real GDP for December.

US ADP jobs grows 107k, below expectation 143k

US ADP private employment grew 107k in January, below expectation of 143k. By sector, goods-producing jobs rose 30k while service-providing jobs rose 77k. By establishment size, small companies added 25k jobs, medium added 61k, large added 31k.

Pay gains for job-stayers slowed from 5.4% yoy to 5.2% yoy. Pay gains for job-changers slowed to 7.2% yoy, smallest gain since May 2021.

"Progress on inflation has brightened the economic picture despite a slowdown in hiring and pay," said Nela Richardson, chief economist, ADP. "Wages adjusted for inflation have improved over the past six months, and the economy looks like it's headed toward a soft landing in the U.S. and globally.

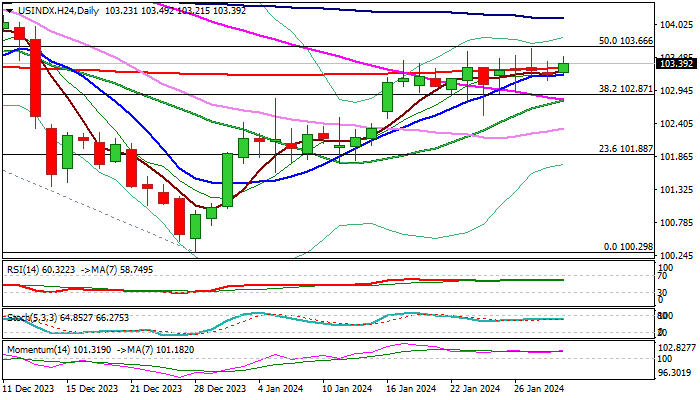

Dollar Index Standing at the Front Foot Ahead of Fed

The dollar index firmed on Wednesday, as markets await the Fed rate decision, at the end of the first policy meeting this year.

Although the price rose slightly, it remains within the larger congestion and lacks direction as a number of long-legged Doji candles in pat days signals strong indecision.

Fresh gains probe again through 200DMA (103.31) which limited several attacks and kept the price in a sideways mode.

Near-term action, however, remains slightly bullishly aligned, as rising 10DMA (103.20) continues to underpin and bullish momentum is strengthening.

Close above 200DMA to generate initial bullish signal, with break above 103.66 pivot (daily cloud top / 50% retracement of 107.03/100.29 downtrend) to signal continuation of bull-leg from 100.29 (Dec 28 low).

The dollar is on track for 2.3% gain in January after heavy losses in past two months, lifted by fading expectations on the speed and scale of rate cuts after recent economic data signaled that the economy remains resilient and performs better than expected.

Bets for rate cuts as early as March dropped significantly since the start of the year, providing fresh boost to the greenback.

All eyes are on Fed, which is widely expected to keep interest rates unchanged, but signals about the central bank’s next steps will have the strongest impact on markets.

Hawkish stance (unchanged rates but signals that the first cut will not occur in March) will provide fresh support to dollar.

Res: 103.66; 104.11; 104.24; 104.46.

Sup: 103.20; 102.80; 102.32; 101.75.

ECB’s de Guindos see lower growth and inflation than Dec forecasts

ECB Vice President Luis de Guindos, in an interview with Die Zeit, offered indicated that the growth forecast for the region, previously set at 0.8% for this year, might fall short of expectations.

De Guindos highlighted several factors contributing to this revised outlook, saying, "The prospects have even deteriorated." He pointed out the key issues impacting the forecast: a slowdown in world trade, heightened geopolitical uncertainties, and the more rapid than anticipated impact of ECB's interest rate hikes on the economy.

De Guindos also touched upon inflation trends, noting a shift from previous projections. The December projections had inflation returning to the 2% target by the second half of 2025. However, recent data suggest a more optimistic scenario.

De Guindos observed, "But inflation figures have mostly brought positive surprises recently." He further speculated that inflation might settle "slightly lower" than their predictions.

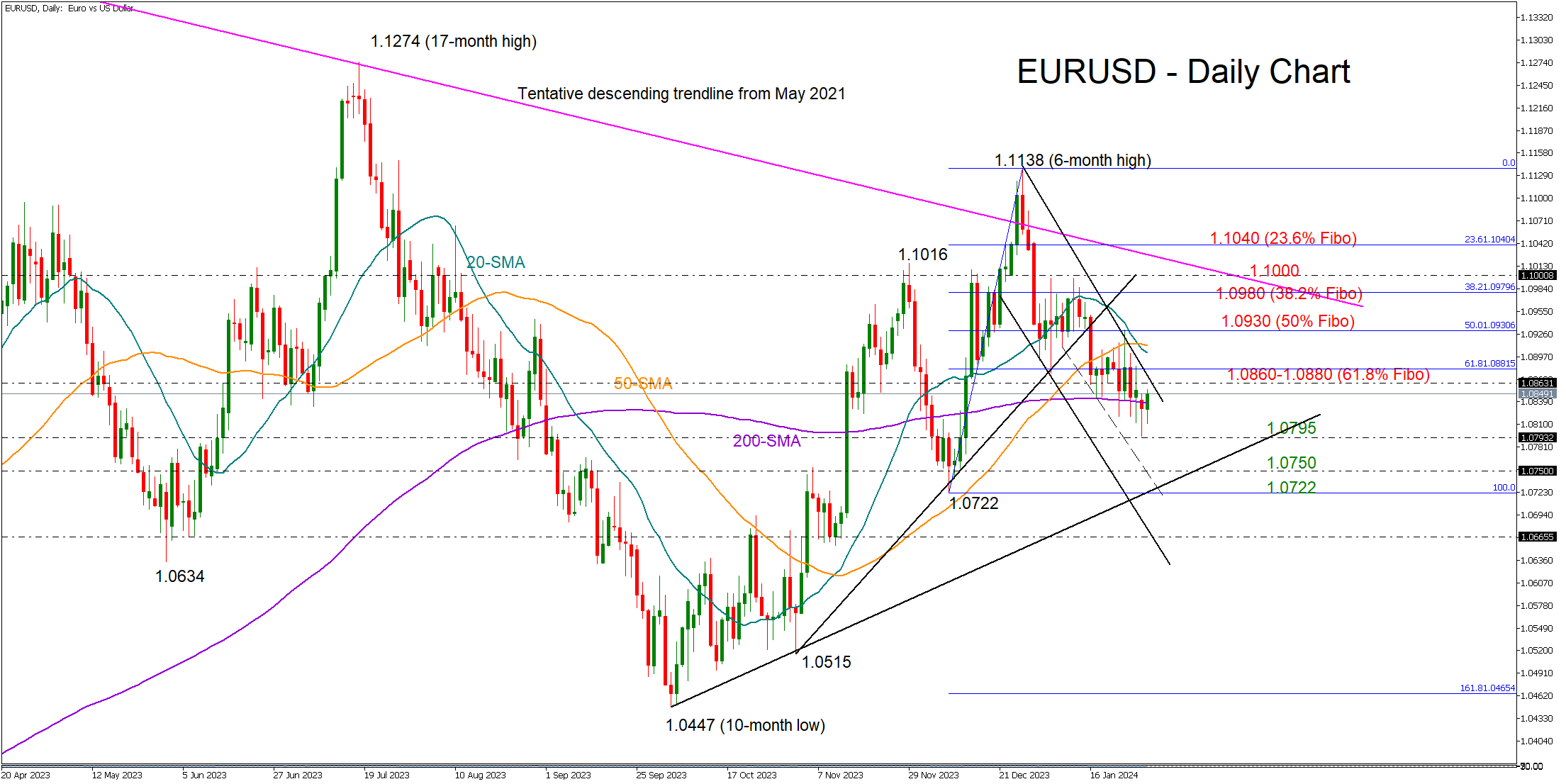

How Will Eurozone Flash CPI Affect Euro?

- Preliminary CPI inflation to slow down in January

- Investors to stick to their rate cut projections as GDP stagnates

- FOMC policy announcement might have a bigger impact on EURUSD

Eurozone economy avoids recession but not Germany

It’s not a secret that the Eurozone has been lagging the US economy for more than a decade, but the gap widened significantly in 2023 when the former started to move in the wrong direction in the face of post-pandemic inflation pressures, high interest rates and heightened geopolitical tensions in Ukraine and the Middle East. On the other hand, the US economic engine managed to finish the year on a positive note despite elevated interest rates and persistent inflation, marking a 3.3% growth in the last quarter of the year.

On Tuesday, Eurozone’s preliminary Q4 GDP growth figures showed zero quarterly expansion after a -0.1% contraction in Q3 and a slight annual pickup of 0.1%. While the whole bloc managed to escape a mild technical recession again, with Spain and Portugal marking the highest growth among member states, Germany, which is the industrial powerhouse, continued to shrink for the fourth consecutive quarter, ending 2023 weaker by -0.3% q/q.

The biggest Eurozone economy has been in the doldrums as its export-oriented and energy-sensitive business model has been suffering from slowing exports to China, stricter climate rules, high energy costs, and tighter financial conditions. Besides, while the switch from Russian gas to American LNGs was the fastest solution to protect the Eurozone's business activities, its energy security is still out of its control and depends on external factors miles away.

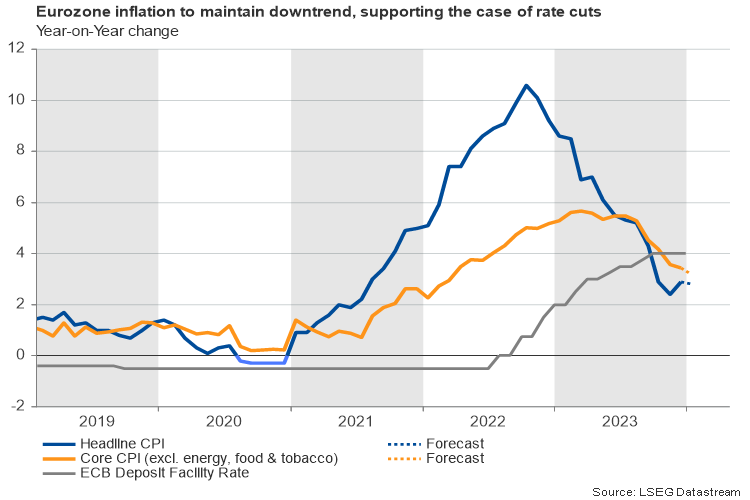

Flash CPI inflation next in the agenda

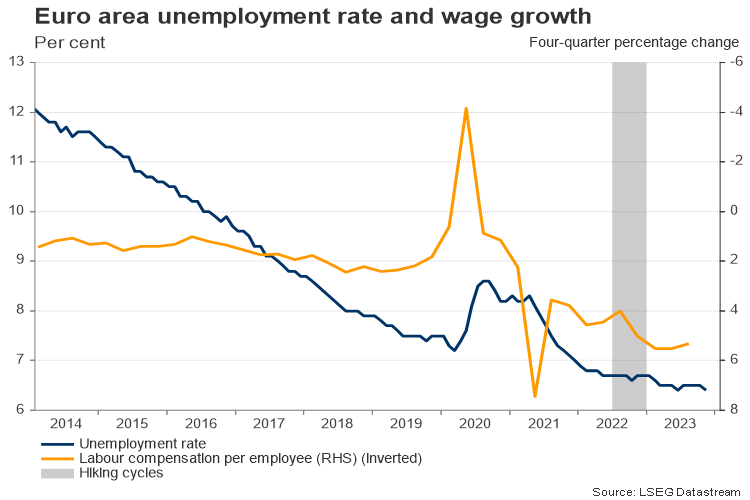

Nevertheless, the euro gained some positive traction against its major peers and especially against the British pound following the GDP release. But for a continuation higher, flash CPI inflation figures due on Thursday will have to reduce the odds for a rate cut in April. Theoretically cheaper borrowing costs would boost economic activity, though according to the labor statistics, the unemployment rate is still at historic lows, suggesting that money keeps circulating through consumers. Hence, cutting interest rates could provide more bargaining power to households, consequently reheating inflation pressures.

Economic growth is not a priority for the European Central Bank, but inflation is. Wednesday’s flash CPI inflation figures are expected to show a slightly softer increase of 2.8% y/y in January versus 2.9% in December. The core measure, which excludes energy, food, alcohol and tobacco, could ease to 3.2% y/y from 3.4% previously, suggesting that some patience might be needed before policymakers become confident that inflation is sustainably moving towards the 2.0% target.

Upside risks to inflation

The ECB held interest rates unchanged in its first meeting of the year and chief Christine Lagarde tried to play down expectations for a rate cut as soon as in March last week, saying that such an action would be premature given the conflicts in the Red Sea and the implications on shipping costs and deliveries.

The impact of labor shortages and wages on inflation seems to be another puzzle for the central bank. Negotiations for higher payrolls could still force businesses to transfer increased labor costs to consumers. Yet, ECB members may not get new wage data before April’s gathering, and hence June’s meeting could be the right time to decide whether rate cuts are necessary. Of course, if inflation starts to fall more aggressively than expected and financial conditions deteriorate, the central bank will not wait that long to slash borrowing costs.

How will EUR/USD react?

In any case, investors have not locked their rate projections for March and April yet, and any data surprises could still affect their outlook, even though the ECB showed a preference for a summer rate cut. Softer-than-expected inflation prints could press EUR/USD towards the 1.0795 support zone. Significant downside pressures could emerge a day earlier on Wednesday if the Fed delays rate cut signals. In this case, the price could sink towards December’s support zone of 1.0722-1.0750.

For the bulls to regain power, the pair will have to accelerate above the bearish channel at 1.0860 and beyond the 1.0880 resistance territory. The 20- and 50-day simple moving averages (SMAs) and the previous high of 1.0930 might be tested on the way up to 1.0980, especially if the Fed provides more details about when the first rate cut will take place.

Australian Dollar Lower After Soft CPI Data

The Australian dollar has lost ground after Australia’s CPI was lower than expected. In the European session, AUD/USD is trading at 0.6578, down o.37%. The Aussie continues to struggle and has declined 3.4% in January.

Australia’s CPI eases to 3.4%

Australia’s inflation rate continues to decline, which will be sweet music to the ears of central bank policy makers. CPI for Q4 2023 fell to 4.1% y/y, down sharply from 5.4% in Q3 and below the market estimate of 4.3%. Inflation has decelerated for a third straight month and has fallen to its lowest since November 2021. The drop in inflation was felt across the economy and goods and services inflation eased. A key core CPI indicator, the trimmed mean, fell to 4.2% y/y, down sharply from 5.2% and just below the market estimate of 4.3%. The decline in inflation was also apparent on a quarterly basis. CPI fell from 1.2% to 0.6% in the fourth quarter and the trimmed-mean CPI dropped to 0.8%, down from 1.2% in the third quarter.

The inflation report is the final key release before the Reserve Bank of Australia meets on February 6. The RBA isn’t expected to start cutting rates until the second half of 2024 and it’s a virtual certainty that the RBA will hold rates next week at 4.35%. The RBA hasn’t signalled it will cut rates, but inflation has been moving in the right direction and the economy has been cooling down, with consumer spending falling and the labour market showing cracks.

This week’s retail sales report was a reminder that consumers are being squeezed by the cost of living crisis. December retail sales plunged 2.7% m/m, as Black Friday sales contributed to the November reading of 1.6%. Consumers did their Christmas shopping early and that led to a very soft reading in December.

AUD/USD Technical

- AUD/USD is testing support at 0.6583. Next, there is support at 0.6544

- There is resistance at 0.6613 and 0.6652

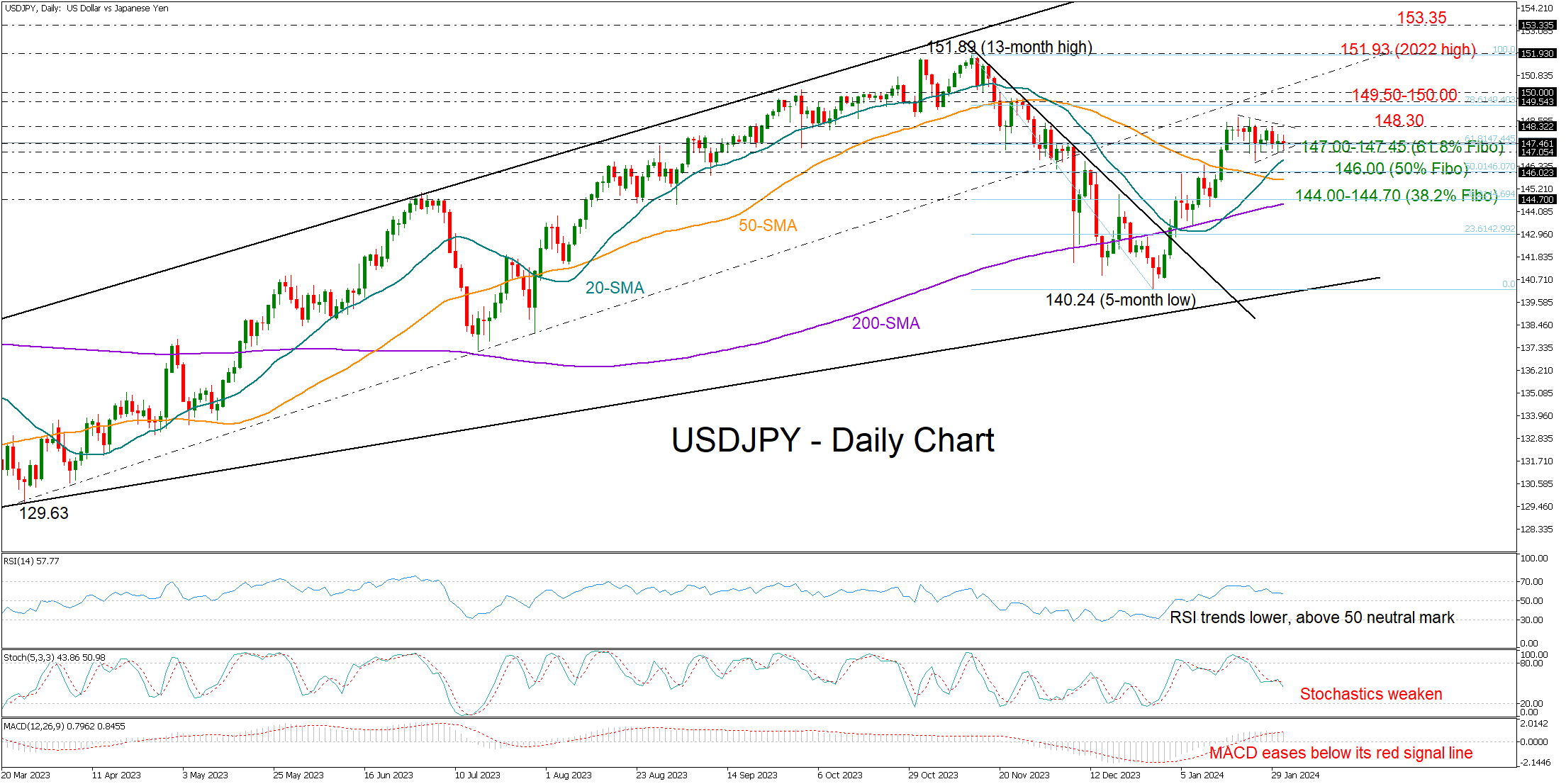

USDJPY Sustains Its 2024 Bullish Setup

- USDJPY consolidates its 2024 upleg between key boundaries

- Momentum indicators point lower, but trend signals remain positive

- FOMC policy announcement due at 19:00 GMT

USDJPY has been facing difficulties in surpassing the 148.30 region for almost two weeks, but the 147.45 region, which coincides with the 61.8% Fibonacci retracement of the November-December downleg, kept bearish forces in control, sustaining January's almost 5% rally.

The momentum indicators have shifted southwards, pointing to more losses ahead as investors are hoping to get more details about the timing of rate cuts when the Fed announces its policy decision today at 19:00 GMT. On the other hand, the trend signals are more encouraging. The 20-day simple moving average (SMA) crossed above the 50- and 200-day SMAs, providing some optimism that the 2024 upleg has not peaked yet.

A close above the nearby 148.30 resistance is required for an acceleration towards the 149.50-150.00 territory. If the latter proves easy to pierce through, the door will open for the 13-month high of 151.89 registered in November and the 2022 top of 151.93. Additional gains from there could face some congestion near the 153.35-153.60 barrier taken from 1990 and 1987.

On the downside, a slide below 147.00 and the 20-day SMA could immediately pause around the 50% Fibonacci level of 146.00. Breaking lower and beneath the 50-day SMA, the bears could head for the 200-day SMA currently converging towards the 38.2% Fibonacci mark of 144.70. If the 144.00 bar fails to stop the decline too, the next stop could be around the 23.6% Fibonacci of 142.92.

In brief, USDJPY is sending mixed signals. An extension above 148.30 or below 147.00 could provide new direction to the market.

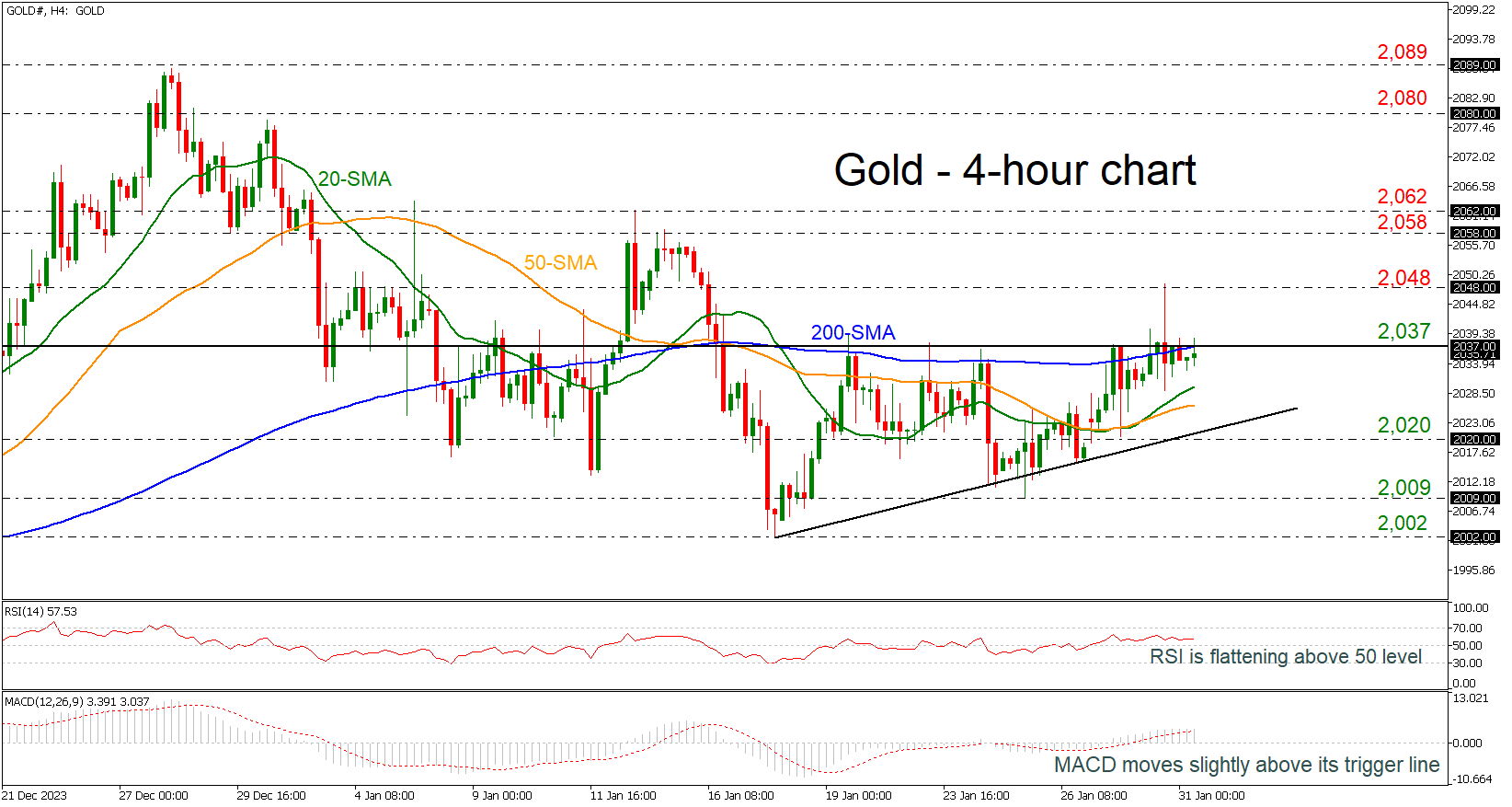

Gold Develops Ascending Triangle in Near-Term

- Gold struggles to surpass 2,037 and 200-period SMA

- RSI and MACD move horizontally

- Short-term outlook looks neutral-to-bullish

Gold prices are flirting with the 2,037 resistance level and the 200-period simple moving average (SMA) in the 4-hour chart, creating an ascending triangle.

Technically, the RSI is moving horizontally above the 50 level, while the MACD is standing slightly above its trigger line in the positive territory, both confirming the recent weak momentum in price.

On the upside, the price could attempt to overcome the 2,037 high and retest the 2,048 barricade. Should traders continue to buy the commodity, bringing the medium-term uptrend back into play, resistance could then run towards the 2,058-2,062 zone.

A reversal to the downside, however, could find immediate support at the 20- and 50-period SMAs at 2,029 and 2,026 respectively, while slightly lower the near-term ascending line of the triangle at 2,023 could also come into view. If the latter fails to halt bearish movements, the next target could be the 2,020 support ahead of 2,009.

Turning to the medium-term trading picture, the outlook has become neutral-to-bullish over the past two weeks and only a decisive close above 2,037 could resume the long-term bullish trend. On the other hand, a significant decline below 2,002 could shift the outlook to bearish.