Sample Category Title

Loonie Sinks Despite BoC’s Hawkish Hold, Aussie Rally Fizzles Out

Canadian Dollar encountered heavy headwinds after BoC made the anticipated decision to keep interest rates steady. The bank's hawkish tone persisted, highlighting concerns over the sluggish pace of disinflation. However, the central bank also acknowledged emerging signs indicating that past rate hikes might be curbing economic activity.

Earlier in the day, Australian Dollar experienced a boost on the back of robust CPI data, prompting major financial institutions such as Commonwealth Bank of Australia and ANZ to change their tune regarding interest rate forecasts. Both banks now anticipate a 25 basis point rate hike come November.

Yet, the buoyancy of Aussie was short-lived, reverting to a mixed stance shortly thereafter. This change in sentiment is reflective of a broader realization in the markets: many major central banks, like BoC, are grappling with inflation rates that are more resilient than initially expected.

Presently, the market's attention has pivoted back to rising treasury yields and a general inclination towards risk aversion. Commodity currencies, with Canadian Dollar at the forefront, are trailing behind as the day's most underwhelming performers. This trend is mirrored by Aussie and Kiwi.

On the flip side, Dollar stands tall as the day's top performer, trailed the Yen the Euro. Sterling and Swiss Franc, meanwhile, oscillate, reflecting a more ambivalent performance in the markets.

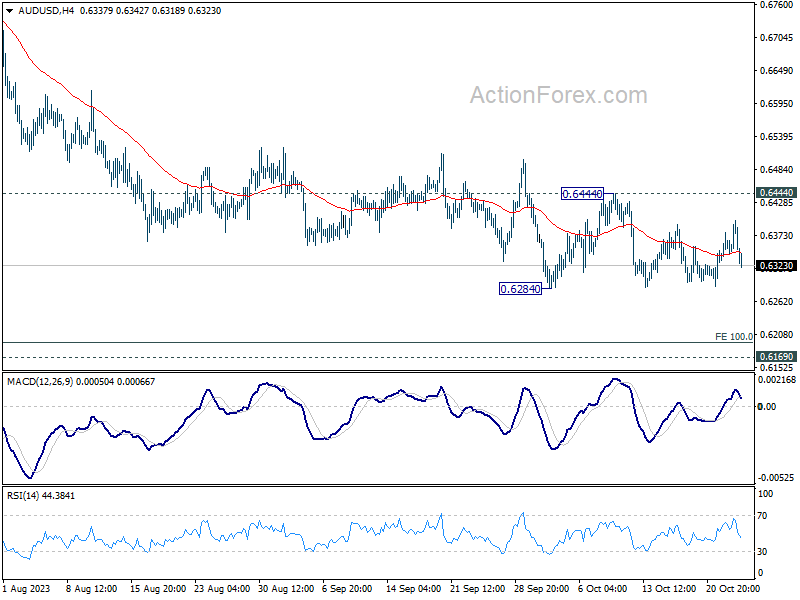

Technically, as AUD/USD's earlier rebound falters, focus could be back on 0.6284 support in the near term. Decisive break there will resume the whole down trend from 0.7156 to 100% projection of 0.7156 to 0.6457 from 0.6894 at 0.6195, which is close to 0.6169 medium term support.

In Europe, at the time of writing, FTSE is down -0.22%. DAX is down -0.55%. CAC is down -0.45%. Germany 10-year yield is up 0.0590 at 2.886. Earlier in Asia, Nikkei rose 0.67%. Hong Kong HSI rose 0.55%. China Shanghai SSE rose 0.40%. Singapore Strait Times dropped -0.17%. Japan 10-year JGB yield rose 0.0065 to 0.861.

BoC stands pat, concerned on slow disinflation progress

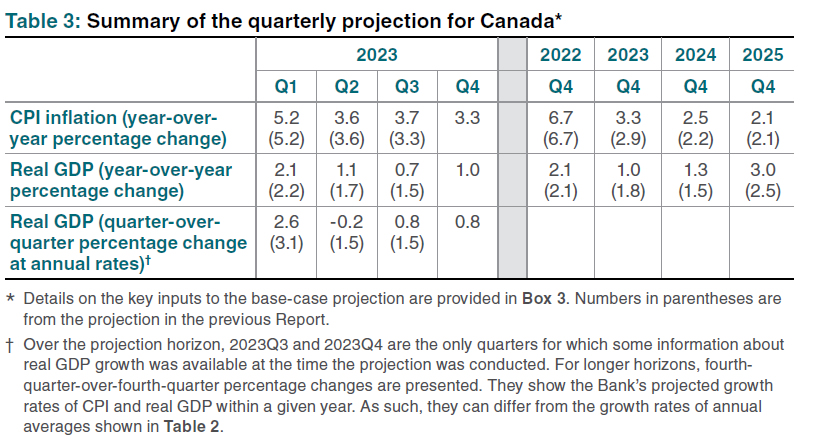

BoC left overnight rate unchanged at 5.00% as widely expected. Bank Rate and deposit rate are held at 5.25% and 5.00% respectively. The Governing Council expressed concerns that "progress towards price stability is slow and inflationary risks have increased". The central bank is "prepared to raise the policy rate further if needed", maintaining hawkish bias.

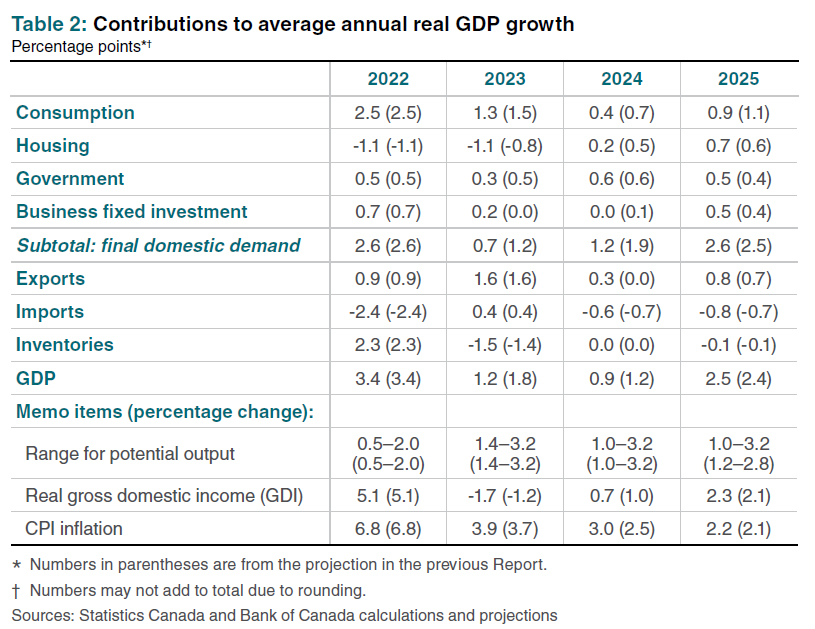

Growth projections are revised notably lower for 2023 and 2024, but raised slightly for 2025. GDP growth is projected to be at 1.2% in 2023 (vs prior 1.8%), 0.9% in 2024 (vs prior 1.2%), and 2.5% in 2025 (vs prior 2.4%).

CPI inflation forecasts are revised higher through the projection horizon, at 3.9% in 2023 (vs prior 3.7%), 3.0% in 2024 (vs prior 2.5%), and 2.2% in 2025 (vs prior 2.1%).

German Ifo business climate rose to 86.9, seeing a silver lining

German Ifo Business Climate rose from 85.8 to 86.9 in October. Current Assessment Index rose from 88.7 to 89.2. Expectations Index rose from 83.1 to 84.7.

By sector, manufacturing rose from -16.2 to -15.9. Services rose from -4.9 to -1.5. Trade dropped from -25.0 to 27.2. Construction ticked up from -31.2 to -31.1.

Ifo said: "Managers were less pessimistic in their view of the coming months. Germany's economy can see a silver lining ahead."

Australia CPI slows to 5.4% yoy in Q3, but rises to 5.6% yoy in Sep

Australia's CPI for Q3 registered a 1.2% qoq rise, exceeding expectation of 1.1% qoq and marking an acceleration from the previous quarter's 0.8% qoq. Notably, some of the most pronounced price hikes were observed in automotive fuel (+7.2%), rents (+2.2%), new dwelling purchases by owner-occupiers (+1.3%), and electricity (+4.2%).

Over the twelve months, inflation saw a deceleration, with CPI moving from 6.0% yoy to 5.4% yoy in Q3. However, this figure surpassed the anticipated 5.3% yoy. It's essential to note that this is the third consecutive quarter where the annual inflation rate has experienced a downturn, dropping from its high of 7.8% in Q4 2022.

The trimmed mean CPI, which excludes volatile items, recorded a 1.2% qoq increase again outpacing the forecasted 1.1% qoq and the previous quarter's 1.0% qoq . When analyzing the annualized data, the trimmed mean CPI decelerated from 5.9% yoy to 5.2% yoy, surpassing the predicted 5.1% yoy.

Commenting on the latest figures, Michelle Marquardt, ABS head of price statistics, highlighted that "prices continued to rise for most goods and services." However, she also noted a few sectors that registered price declines, notably child care, vegetables, and domestic holiday travel and accommodation.

Furthermore, the monthly CPI for September recorded acceleration from 5.2% yoy to 5.6% yoy , which was above the anticipated 5.4% yoy. Significant price surges in this period were identified in Housing (+7.2%), Transport (+9.4%), and Food and non-alcoholic beverages (+4.7%).

Reflecting on these trends, Marquardt stated, "This is the second consecutive rise in the annual movement up from 5.2% in August and 4.9% in July. While many industries' price increases are slowing, automotive fuel has had large annual increases in the last two months, which has been driving the movement higher."

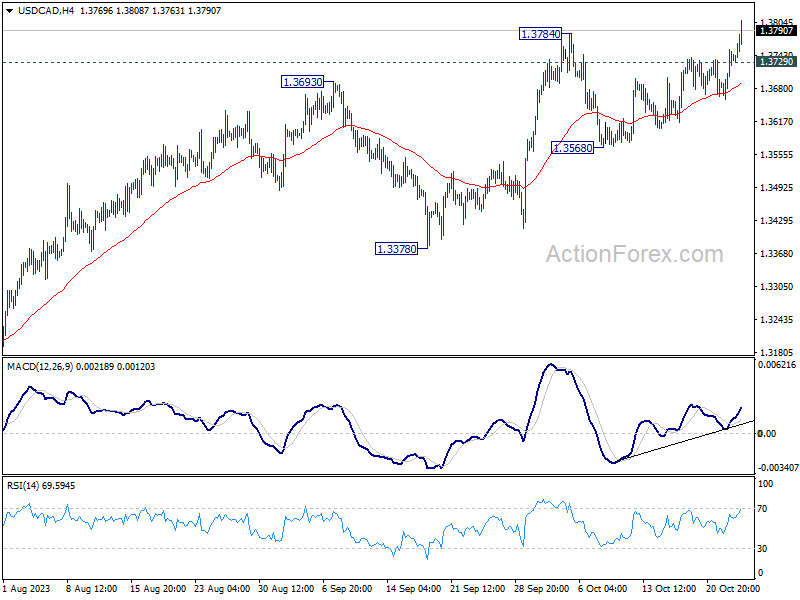

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3660; (P) 1.3698; (R1) 1.3729; More...

USD/CAD's solid break of 1.3784 resistance confirm resumption of the rally from 1.3091. Intraday bias is back on the upside for retesting 1.3976 high. Decisive break there will resume larger up trend. On the downside, below 1.3729 minor support will turn intraday bias neutral and bring consolidations. But near term outlook will remain bullish as long as 1.3568 support holds.

In the bigger picture, current development revives the case that corrective pattern from 1.3976 (2022 high) has completed with three waves down to 1.3091. Decisive break of 1.3976 high will confirm resumption of up trend from 1.2005 (2021 low). Next target will be 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. This will now remain the favored case as long as 1.3378 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Monthly CPI Y/Y Sep | 5.60% | 5.40% | 5.20% | |

| 00:30 | AUD | CPI Q/Q Q3 | 1.20% | 1.10% | 0.80% | |

| 00:30 | AUD | CPI Y/Y Q3 | 5.40% | 5.30% | 6.00% | |

| 00:30 | AUD | RBA Trimmed Mean CPI Q/Q Q3 | 1.20% | 1.10% | 1.00% | |

| 00:30 | AUD | RBA Trimmed Mean CPI Y/Y Q3 | 5.20% | 5.00% | 5.90% | |

| 08:00 | CHF | Credit Suisse Economic Expectations Oct | -37.8 | -27.6 | ||

| 08:00 | EUR | Germany IFO Business Climate Oct | 86.9 | 85.9 | 85.7 | 85.8 |

| 08:00 | EUR | Germany IFO Current Assessment Oct | 89.20 | 88.5 | 88.7 | |

| 08:00 | EUR | Germany IFO Expectations Oct | 84.7 | 83.3 | 82.9 | 83.1 |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Sep | -1.20% | -1.70% | -1.30% | |

| 14:00 | USD | New Home Sales Sep | 759K | 684K | 675K | |

| 14:00 | CAD | BoC Interest Rate Decision | 5.00% | 5.00% | 5.00% | |

| 14:30 | USD | Crude Oil Inventories | -0.5M | -4.5M | ||

| 15:00 | CAD | BoC Press Conference |

BoC stands pat, concerned on slow disinflation progress

BoC left overnight rate unchanged at 5.00% as widely expected. Bank Rate and deposit rate are held at 5.25% and 5.00% respectively. The Governing Council expressed concerns that "progress towards price stability is slow and inflationary risks have increased". The central bank is "prepared to raise the policy rate further if needed", maintaining hawkish bias.

Growth projections are revised notably lower for 2023 and 2024, but raised slightly for 2025. GDP growth is projected to be at 1.2% in 2023 (vs prior 1.8%), 0.9% in 2024 (vs prior 1.2%), and 2.5% in 2025 (vs prior 2.4%).

CPI inflation forecasts are revised higher through the projection horizon, at 3.9% in 2023 (vs prior 3.7%), 3.0% in 2024 (vs prior 2.5%), and 2.2% in 2025 (vs prior 2.1%).

Full BoC statement and Monetary Policy Report here.

(BOC) Bank of Canada maintains policy rate, continues quantitative tightening

The Bank of Canada today held its target for the overnight rate at 5%, with the Bank Rate at 5¼% and the deposit rate at 5%. The Bank is continuing its policy of quantitative tightening.

The global economy is slowing and growth is forecast to moderate further as past increases in policy rates and the recent surge in global bond yields weigh on demand. The Bank projects global GDP growth of 2.9% this year, 2.3% in 2024 and 2.6% in 2025. While this global growth outlook is little changed from the July Monetary Policy Report (MPR), the composition has shifted, with the US economy proving stronger and economic activity in China weaker than expected. Growth in the euro area has slowed further. Inflation has been easing in most economies, as supply bottlenecks resolve and weaker demand relieves price pressures. However, with underlying inflation persisting, central banks continue to be vigilant. Oil prices are higher than was assumed in July, and the war in Israel and Gaza is a new source of geopolitical uncertainty.

In Canada, there is growing evidence that past interest rate increases are dampening economic activity and relieving price pressures. Consumption has been subdued, with softer demand for housing, durable goods and many services. Weaker demand and higher borrowing costs are weighing on business investment. The surge in Canada's population is easing labour market pressures in some sectors while adding to housing demand and consumption. In the labour market, recent job gains have been below labour force growth and job vacancies have continued to ease. However, the labour market remains on the tight side and wage pressures persist. Overall, a range of indicators suggest that supply and demand in the economy are now approaching balance.

After averaging 1% over the past year, economic growth is expected to continue to be weak for the next year before increasing in late 2024 and through 2025. The near-term weakness in growth reflects both the broadening impact of past increases in interest rates and slower foreign demand. The subsequent pickup is driven by household spending as well as stronger exports and business investment in response to improving foreign demand. Spending by governments contributes materially to growth over the forecast horizon. Overall, the Bank expects the Canadian economy to grow by 1.2% this year, 0.9% in 2024 and 2.5% in 2025.

CPI inflation has been volatile in recent months—2.8% in June, 4.0% in August, and 3.8% in September. Higher interest rates are moderating inflation in many goods that people buy on credit, and this is spreading to services. Food inflation is easing from very high rates. However, in addition to elevated mortgage interest costs, inflation in rent and other housing costs remains high. Near-term inflation expectations and corporate pricing behaviour are normalizing only gradually, and wages are still growing around 4% to 5%. The Bank's preferred measures of core inflation show little downward momentum.

In the Bank's October projection, CPI inflation is expected to average about 3½% through the middle of next year before gradually easing to 2% in 2025. Inflation returns to target about the same time as in the July projection, but the near-term path is higher because of energy prices and ongoing persistence in core inflation.

With clearer signs that monetary policy is moderating spending and relieving price pressures, Governing Council decided to hold the policy rate at 5% and to continue to normalize the Bank's balance sheet. However, Governing Council is concerned that progress towards price stability is slow and inflationary risks have increased, and is prepared to raise the policy rate further if needed. Governing Council wants to see downward momentum in core inflation, and continues to be focused on the balance between demand and supply in the economy, inflation expectations, wage growth and corporate pricing behaviour. The Bank remains resolute in its commitment to restoring price stability for Canadians.

Information note

The next scheduled date for announcing the overnight rate target is December 6, 2023. The Bank will publish its next full outlook for the economy and inflation, including risks to the projection, in the MPR on January 24, 2024.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0551; (P) 1.0623; (R1) 1.0662; More...

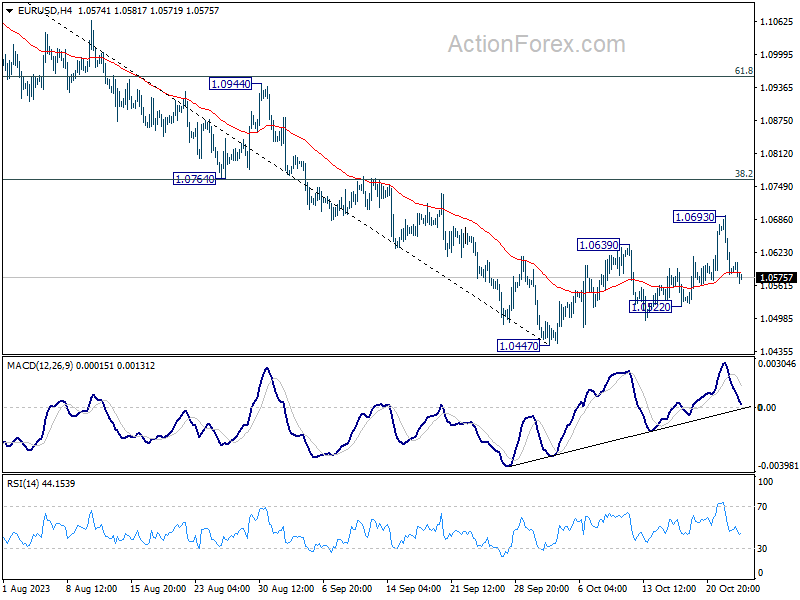

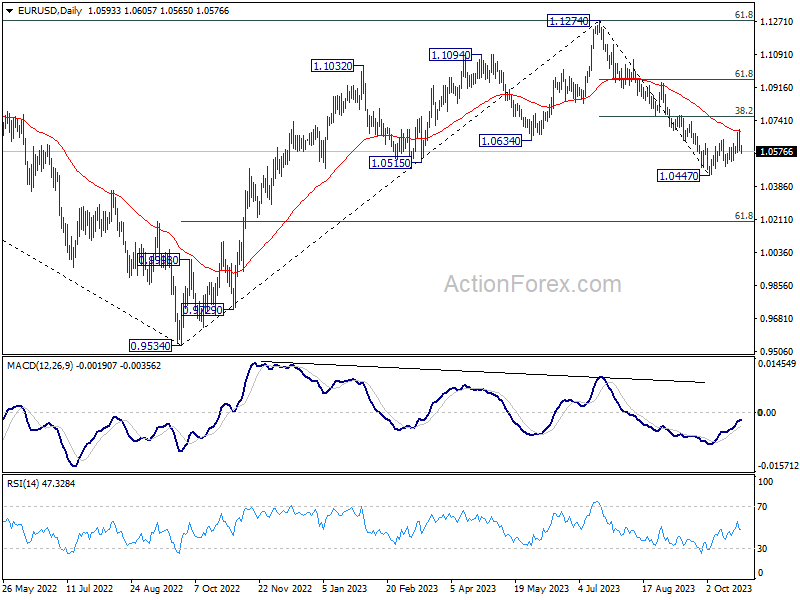

Intraday bias in EUR/USD is remains neutral and outlook is unchanged. On the upside, above 1.0693 will resume the rebound from 1.0447 to 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763). On the downside, break of 1.0522 support will retain near term bearishness for resuming the whole decline from 1.1274 through 1.0447 next.

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0684) holds, in case of rebound.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2113; (P) 1.2201; (R1) 1.2249; More

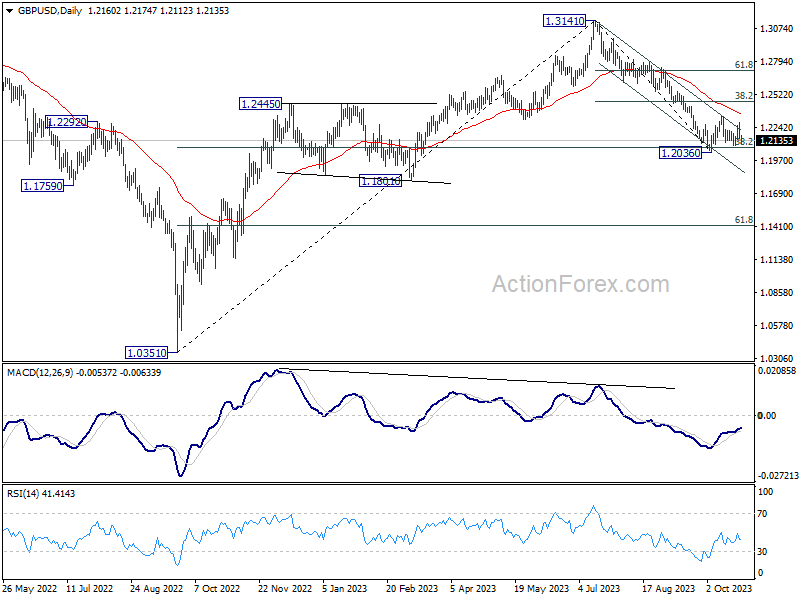

No change in GBP/USD's outlook as consolidation from 1.2036 is extending. Downside breakout is still mildly in favor. On the downside, decisive break of 1.2036 will resume whole decline from 1.3141 for 1.1801 support next. However, break of 1.2336 will turn bias back to the upside for 38.2% retracement of 1.3141 to 1.2036 at 1.2458.

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2384) holds, in case of rebound.

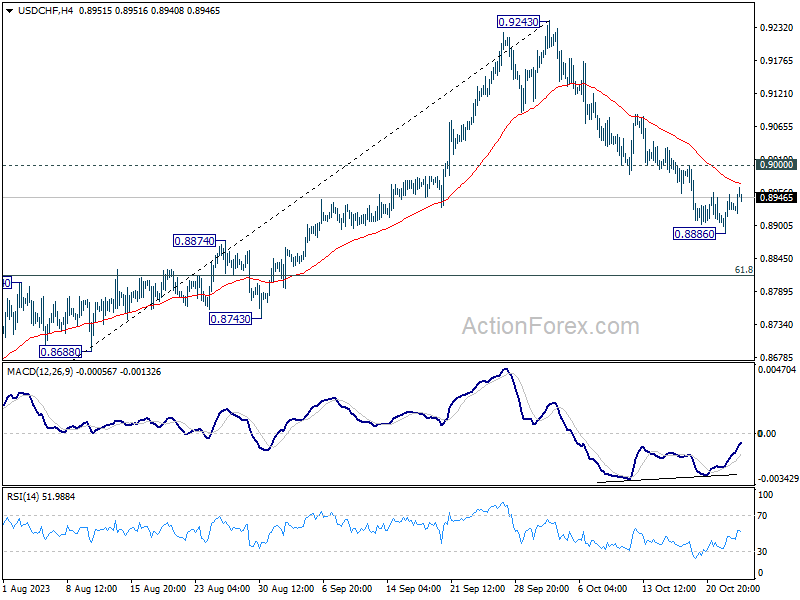

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8895; (P) 0.8924; (R1) 0.8960; More....

USD/CHF is extending the consolidation from 0.8886 and intraday bias remains neutral. Further decline is expected as long as 0.9000 resistance holds. Below 0.8886 will resume the fall from 0.9243 to 61.8% retracement of 0.8551 to 0.9243 at 0.8815 next. Sustained break there will pave the way to retest 0.8551 low. Nevertheless, break of 0.9000 will turn bias back to the upside for stronger rebound.

In the bigger picture, the firm break of 55 D EMA (now at 0.8974) argues that rebound from 0.8551 might be completed as a correction at 0.9243. In other words, larger fall from 1.0146 (2022 high) is possibly not over yet. Risk will now stay on the downside as long as 0.9243 resistance holds. Firm break of 0.8551 will confirm down trend resumption.

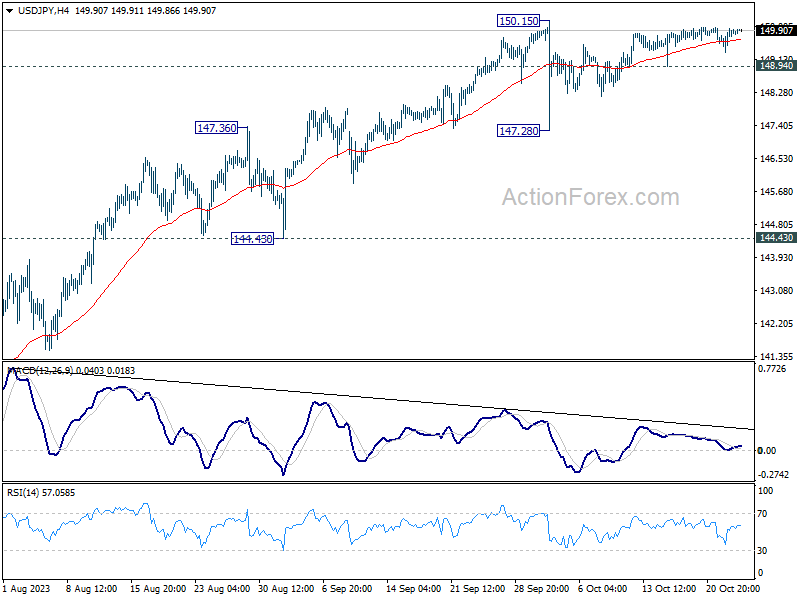

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.51; (P) 149.72; (R1) 150.12; More...

USD/JPY is still extending the consolidation from 150.15 and intraday bias stays neutral. On the downside, below 148.94 minor support will turn bias to the downside for another down leg towards 147.28. On the upside, firm break of 150.15 will resume larger up trend to test 151.93 high.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will be the first sign that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

Inflation Surprise Doesn’t Help the Aussie

Australian inflation surprised on the upside, reigniting expectations of another rate hike as early as November. However, the Aussie could not enjoy the buying momentum for long as the US dollar strengthened.

In the third quarter, CPI rose 1.2%, accelerating from 0.8% three months earlier due to fuel and energy cost dynamics. Annual inflation slowed to 5.4% from 6.0%, above expectations of 5.3%.

Monthly data showed that inflation accelerated to 5.6% y/y in September from 5.2% in August and 4.9% in July. This looks like a dangerous and sustained uptrend, although it is yet to be seen in the quarterly numbers, which are the central bank’s primary focus.

AUDUSD came close to 0.6400, adding two-thirds of a cent shortly after the news. However, the round level and touching of the 50-day moving average also triggered heavier selling in the pair, repeating what we saw in EURUSD a day earlier.

At the time of writing, the Aussie has pulled back to 0.6330, erasing the gains made early Tuesday. Technically, the Aussie remains in the hands of the bears as it makes a series of lower local highs and stumbles off the 50-day moving average. There is significant support at 0.63, from which the pair has been bought on the downtrend since the beginning of the month. A break below this level would open the door for a quick fall back below 0.62.

The risk of the AUD falling into a downward spiral should raise the RBA’s alert level. But will it happen?

USD/CAD Eyes Bank of Canada Decision

- Bank of Canada expected to hold rates at 5.0%

The Canadian dollar is steady on Wednesday. In the European session, USD/CAD is trading at 1.3758, up 0.12%.

Bank of Canada expected to hold rates

The Bank of Canada meets later today and the markets are widely expecting the Bank to hold the benchmark cash rate at 5.0%. The BoC has aggressively raised rates to levels not seen since 2001 in order to curb inflation. The economy has cooled as elevated rates continue to filter through the economy and inflation eased to 3.8% in September. Still, this remains close to double the BoC’s inflation target of 2%, and central banks have come to realize that the final ‘sprint’ to getting inflation back down to target may be the most difficult phase in the battle to curb inflation.

The BoC is doing its utmost to hold rates and not inflation further pain on households. I don’t anticipate the BoC cutting rates before inflation is back at the 2% target, which won’t occur before sometime next year at the earliest.

US GDP expected to jump to 4.5%

Over in the US, the economy remains strong, raising hopes that the Fed will be able to guide the economy to a soft landing. The US releases third-quarter GDP on Thursday and the consensus estimate stands at a massive annual rate of 4.5%, compared to 2.1% in the second quarter. This would mark the highest level since Q4 2021, when the economy was in recovery mode from the Covid pandemic.

As the major economies grapple with weak growth, US exceptionalism has been marked by a strong labour market which is driving consumer spending. The Fed is clearly worried, with Jerome Powell stating last week that continuing strong growth could complicate the efforts to rein in inflation and force the Fed to raise rates. As far as the Fed is concerned, a strong GDP release could be “too much of a good thing” and would add pressure to raise rates.

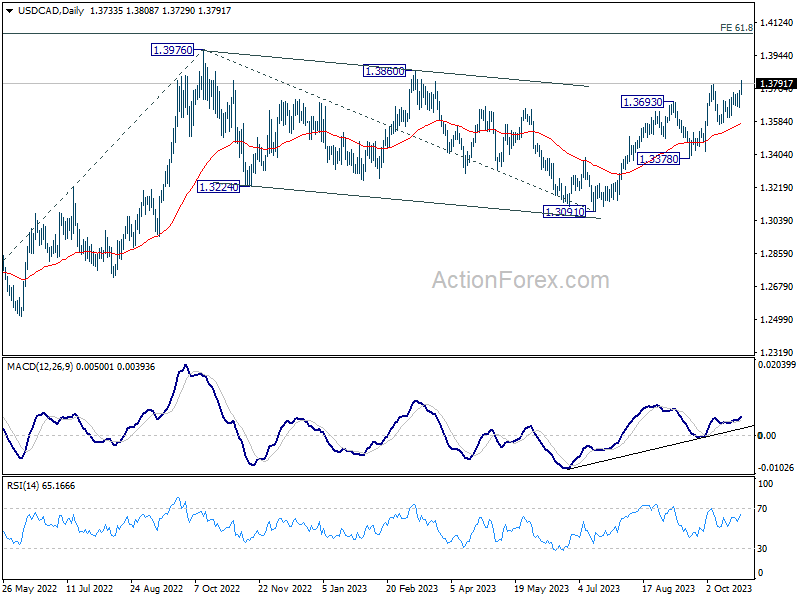

USD/CAD Technical

- USD/CAD tested resistance at 1.3768 earlier. Above, there is resistance at 1.3822

- There is support at 1.3688 and 1.3634

Australian Dollar Falls Despite CPI Rise

- Australia’s CPI accelerates

- US PMIs show slight improvement

The Australian dollar rose about 40 basis points on Wednesday after Australia’s CPI surprised to the upside, but has reversed directions and is in negative territory. In the European session, AUD/USD is trading at 0.6335, down 0.32%.

Australia’s CPI accelerates

Australian inflation was hotter than expected in the third quarter and that could translate into the Reserve Bank of Australia hiking rates after four consecutive pauses.

Australian CPI rose 1.2% q/q in the third quarter, up from 0.8% in Q2 and higher than the consensus estimate of 0.8%. For September, CPI jumped 5.6% y/y, up from 5.2% in August. The trimmed mean, a key core CPI indicator, rose to 1.2% q/q, up from a revised 1.0% in September and higher than the consensus estimate of 1.1%. The fact that headline CPI and the trimmed mean both decelerated on an annual basis was cold comfort to the markets, which have raised the odds of a rate hike next month to 66%, compared to 35% a day ago.

The RBA remains hawkish over inflation, and Governor Bullock said on Tuesday that the RBA would increase rates if there was “a material upward revision to the outlook for inflation”. I’ll leave it to the number-crunchers at the central bank to determine if today’s inflation report meets that definition, but it’s clear that the upswing in inflation will put pressure on the RBA to raise rates at the November 2nd meeting. Two major Australian banks, the Commonwealth Bank of Australia and ANZ switched their rate stance in the aftermath of the inflation report and are now projecting a quarter-point hike next month.

It wasn’t a spectacular upswing but US manufacturing and services PMI gained ground in September. Manufacturing PMI rose from 49.8 to 50.0 is September, above the market consensus of 49.5 and hitting a six-month high. The Services PMI rose to 50.9, up from 50.1 in September, above the market consensus of 49.8 and the highest level in three months. The PMI releases are the latest sign that the US economy has been able to weather the Federal Reserve’s tightening cycle.

AUD/USD Technical

- AUD/USD has support at 0.6240 and 0.6184

- 0.6343 and 0.6399 are the next resistance lines