Sample Category Title

The All-Important Jobs Report

For most of this year, the market was focused on inflation numbers, as inflation was all that mattered for the Federal Reserve (Fed) expectations. And inflation fainted thanks to a significant downside correction in energy prices compared to last year and due to waning supply chain disruptions, which resulted in higher supply. But now, it becomes increasingly clear that we come toward the end of what we could get from post-Covid normalization and… energy prices. Therefore, the US jobs market must do the rest of the heavy lifting if the Fed wants to see inflation return and steady around its 2% monetary policy target. That makes the US employment and unemployment numbers critical for investors, again.

Today’s data could be one of the most important jobs data of the year because the US bond and equity markets are at a crossroads. The US 2-year yield refuses to lose the 5% mark from sight, while the US 10 and 30-year claim a further rise to 5% on expectations that inflation will remain higher for longer and that would require interest rates to stay higher for longer.

The S&P500 on the other hand is waiting in ambush, a few points above the critical 200-DMA (4205). Below, at 4180, the major 38.2% Fibonacci retracement is waiting to judge whether the S&P500 should remain in the positive trend, or sink its teeth into a medium-term bearish consolidation zone. The S&P500 kicked off the year at around 3850, and gains for the good part of the S&P493 have already vanished. Today’s jobs data could help investors find the next direction for the S&P500. Or not.

The US economy is expected to have added 170K new nonfarm jobs in September. That makes sense as last month’s figure stood at 187K and we expect the numbers to gently come down. Last year’s average remains at a strong 270K, but the last 6-month average is down to 235K additions in average per month and the last 3-month average is slightly below 200K job additions. The wages growth on the other hand is seen steady at around 4%, meaningfully above the actual CPI number (3.7%). T

Today, a reasonable wages growth data combined with another NFP number below 200K, preferably near the expectation of 170K, or ideally lower, should pour some cold water on bond yields, especially on the longer portion of the yield curve. But the impact of a cool down in US sovereign markets doesn’t mean that the stocks are out of the woods. For stocks to continue to perform well, the earnings expectation should keep up with the yields, and if the economy is slowing – a signal that we could get from eventually softer jobs data – investors may remain reluctant to return to stock markets.

In the series of Keeping Up with the Fed Members, Richmon Fed President Barkin said that there is a lot of fiscal issuance that’s creating a lot of supply, combined with the strong data and the Fed’s QT, the increased treasury issuance sure contributes to pushing yields higher. SF Fed President Mary Daily said yesterday that the Fed could refrain from raising rates again as the latest meltdown in the bonds market has had about the same effect than on more rate hike. Going into the data, activity in Fed funds futures gives around 78% chance for another pause in November, it appears that traders are betting historic sums on the outcome of the November meeting. That outcome depends on jobs and inflation numbers. So, I stop here, and let the numbers talk.

In energy, the oil selloff extended to a second day, prices fell in five over the past six trading days. The barrel of US crude hit the $82.5pb level yesterday. The selloff could extend toward $80pb level no matter what, if the market focus remains on ‘growth’ and ‘demand’. In case of a soft set of US jobs data, economic slowdown fears would boost the oil bears. In case of strong jobs data, the hawkish Fed expectations would fan recession worries and push oil to $80pb. I however don’t see the barrel of crude sink below the $80pb without OPEC intervening, at least verbally.

It’s Payrolls Day

Market movers today

Today we get the key US jobs report for September. We expect data to be generally consistent with a further cooling of the economy and expect non-farm payrolls growth at +140k and average hourly earnings at +0.2 % m/m SA, both is a bit below consensus.

German factory orders from August are published. Factory orders have declined both this year and last year in sync with the extremely weak manufacturing sector.

The 60 second overview

US yields rose from the long end again extending the recent trends. The recent uptick in long-end UST yields reflects rising term premium, while risk-neutral rate expectations have remained stable. We published Research US - Yields not bound to remain high for long, 5 October, in which we also examine the unfavourable supply-demand dynamics that are likely to persist into Q4, but we still see improving demand driving yields lower, with 12M 10y forecast at 3.70%, though risk is tilted to the upside.

Yesterday's US jobless claims did not provide any evidence of a noteworthy cooling of the US labour market. Initial jobless claims came in more or less in line with expectations at 207k (cons.: 210k, prior: 205k), while continuing claims stood at 1664k (cons.: 1671k, prior: 1665k). The four-week moving average of initial claims edged down to 209k, the lowest level since February. After mixed signals on the latest development in the US labour market during the week (strong JOLTS data and weak ADP employment report), we look for non-farm payrolls at 140k today, which is 30k lower than the consensus. Additionally, we expect average hourly earnings at 0.2% m/m, slightly below consensus of 0.3% m/m. If we are right, EUR/USD will most likely move higher on the release, in line with our tactical case based on US data starting to disappoint.

Equities: Yields stalled which was enough for equities to calm. Europe somewhat higher (Stoxx 600 +0.3%) and US a tad lower (S&P 500 -0.1%) but both a bit off best levels. Growth and quality sectors outperformed as the rates-fear eased, with sectors such as real estate, health care, financials and utilities in the lead (Evolution, Atlas, Nibe, Orsted in the Nordics). Our Nordic select list member Pandora also surging 12% amid higher financial ambitions at the CMD. One sector worth noting is consumer staples, down -2% in the US session. This has been one of the worst performing sectors in the rates surge and underlines the risk of being overweight defensives when risk free alternatives (bonds) are rising.

FI: European yields were trading mostly sideways yesterday until late afternoon when European curves shifted lower by 3-5bp with the move slightly more pronounced in the longer end. Real rates edged slightly lower with inflation swaps broadly unchanged on the day. The news flow yesterday was mainly characterised by central bank speakers indicating that they are done on rates, where particularly ECB's Kazimir said that changing PEPP reinvestments may be considered once they are certain that they are done hiking rates. Villeroy said that past expectations for rate cuts were too optimistic and also that he sees no justification for rate hikes. The transatlantic spread widened again yesterday by 2bp to 183bp in the 10y UST vs. 10y Bunds. This is the widest since November last year.

FX: In yesterday's session EUR/USD extended the latest rebound with the cross hitting the 1.0550 level. Meanwhile, the rally in EUR/NOK and EUR/SEK eased while USD/JPY dropped to 148.50 on the decline in global yields.

Credit: Overall the slightly weak tone in credit markets continued yesterday with iTraxx Main 2bp wider at 87bp while iTraxx X-over was 7bp wider at 461bp. Due to the general market turmoil following higher interest rate levels primary activity remained muted - although we saw some activity both in Scandi and European space.

Nordic macro

In Norway, the government will be unveiling its fiscal budget for 2024. We are most interested in how expansionary the budget will be - in other words, how the proposals would affect economic activity. We expect the budget to be more or less neutral, which would tie in nicely with Norges Bank's projections in the September monetary policy report.

The main event in Sweden is the Debt Office's release of the September budget balance. The accumulated difference vs. forecast up to and including August is a hefty SEK 46bn surplus. The main reason for this was much smaller than expected payments in August for company electricity support (SEK 30bn less than assumed), but corporate taxes were also higher than expected. The Debt Office forecasts a SEK 8bn deficit in September and it seems fair to assume that delayed payment of electricity support can push that deficit considerably higher.

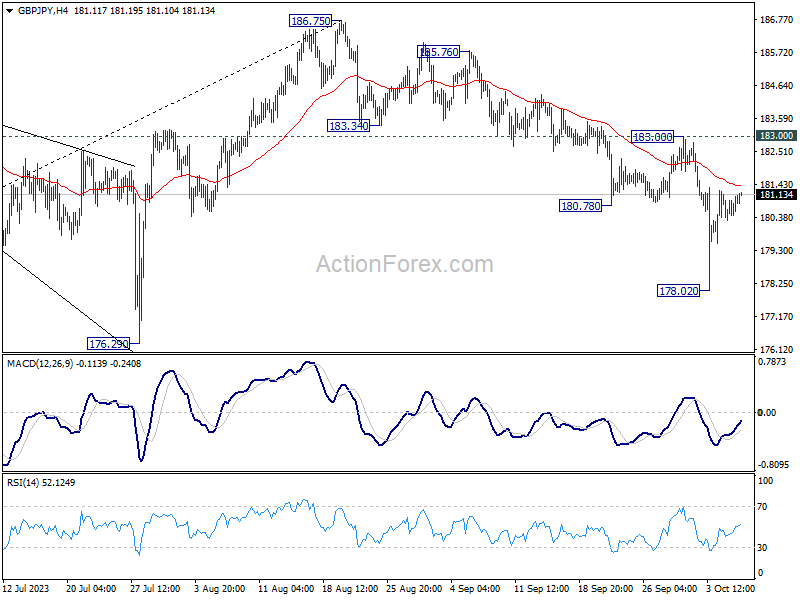

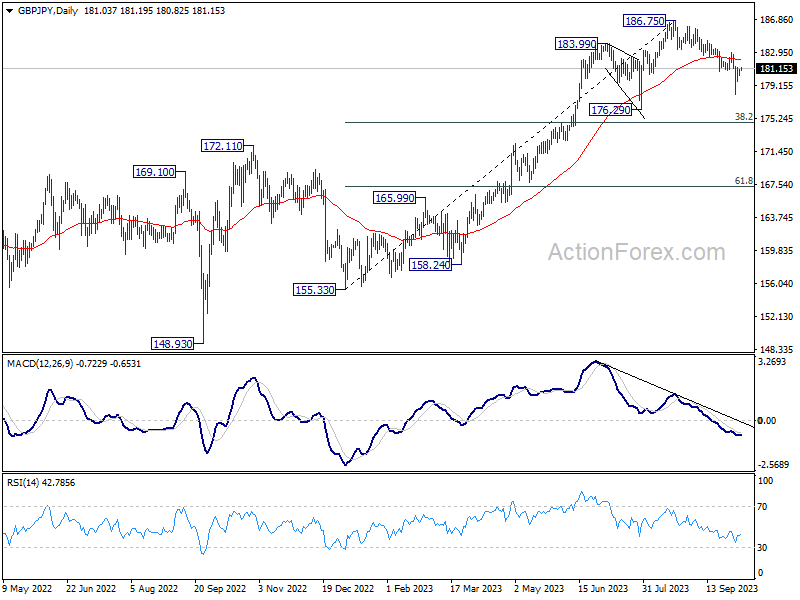

GBP/JPY Daily Outlook

Daily Pivots: (S1) 180.55; (P) 180.81; (R1) 181.34; More...

Intraday bias in GBP/JPY stays neutral at this point. Near term outlook stays bearish as long as 183.00 resistance holds. Break of 178.02 will resume the fall from 186.75 to 176.29 support. However, firm break of 183.00 will argue that the pull back has completed, and turn bias back to the upside.

In the bigger picture, fall from 186.75 is currently seen as a corrective move only. As long as 176.29 support holds, larger up trend from 123.94 (202 low) should still be in progress. Break of 186.75 will target 195.86 (2015 high). Nevertheless, firm break of 176.29 will confirm medium term topping, and bring lengthier and deeper consolidations.

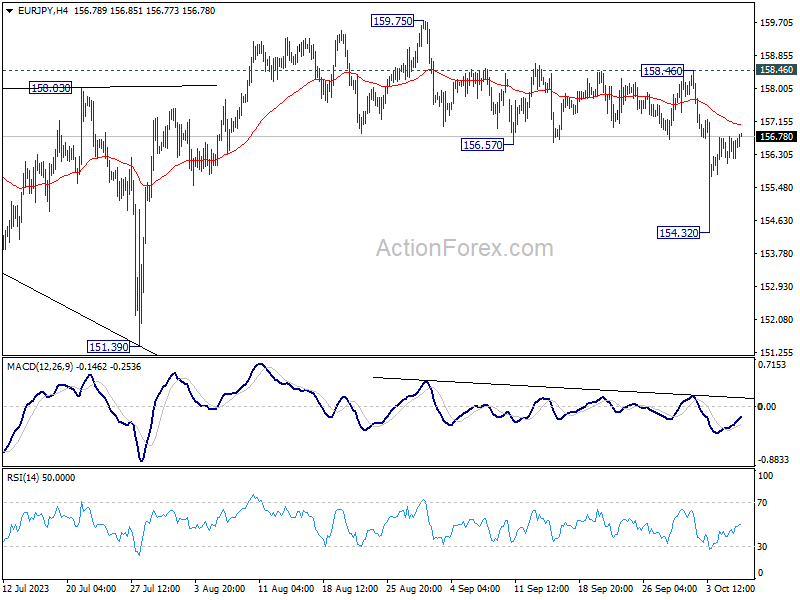

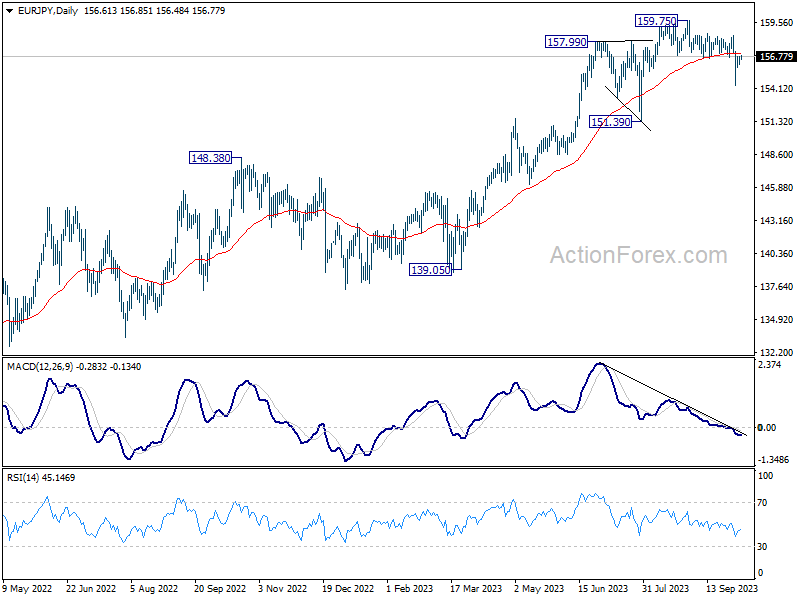

EUR/JPY Daily Outlook

Daily Pivots: (S1) 156.26; (P) 156.52; (R1) 156.96; More....

Intraday bias in EUR/JPY remains neutral for the moment. Near term outlook stays bearish as long as 158.46 resistance holds. Break of 154.32 will resume the whole fall from 159.75 to 151.39 support. Nevertheless, break of 158.464 will argue that the pull back has completed, and turn bias back to the upside.

In the bigger picture, price actions from 159.75 are views as a corrective pattern for now. As long as 151.39 support holds, rise from 114.42 (2020 low) is still expected to continue through 159.75 at a later stage. Nevertheless, firm break of 176.29 will confirm medium term topping, and bring lengthier and deeper correction.

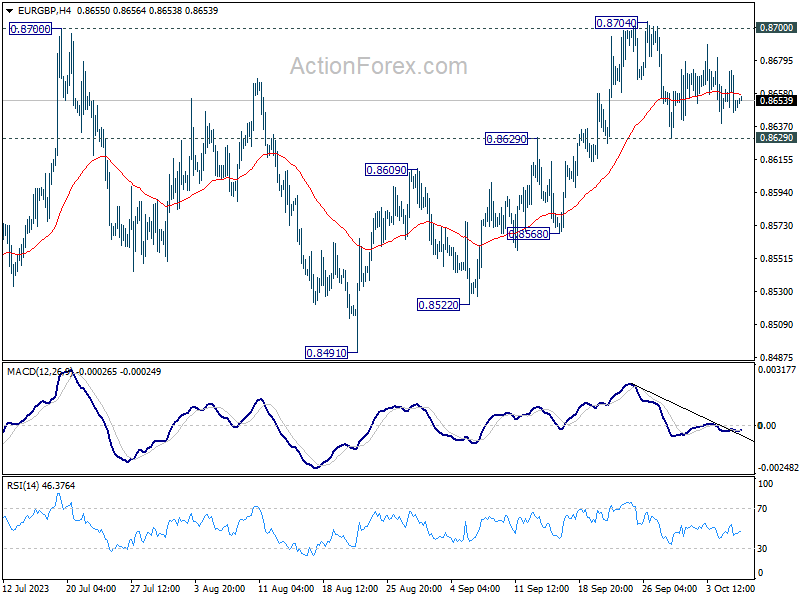

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8637; (P) 0.8656; (R1) 0.8672; More....

EUR/GBP is still bounded in range trading and intraday bias stays neutral. On the upside, decisive break of 0.8700 resistance will carry larger bullish implication and bring stronger rally to 0.8874 resistance next. Nevertheless, rejection by this resistance will maintain bearish outlook that larger down trend is not over. Firm break of 0.8629 resistance turned support will turn bias back to the downside for 0.8568 support first.

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Decisive break of 0.8700 resistance will argue that this decline has completed with three waves down to 0.8491. Rise from 0.8491 could then be another leg inside the pattern and targets 0.8977 and above. However, rejection by 0.8700 will keep the down trend alive for another fall through 0.8491 at a later stage.

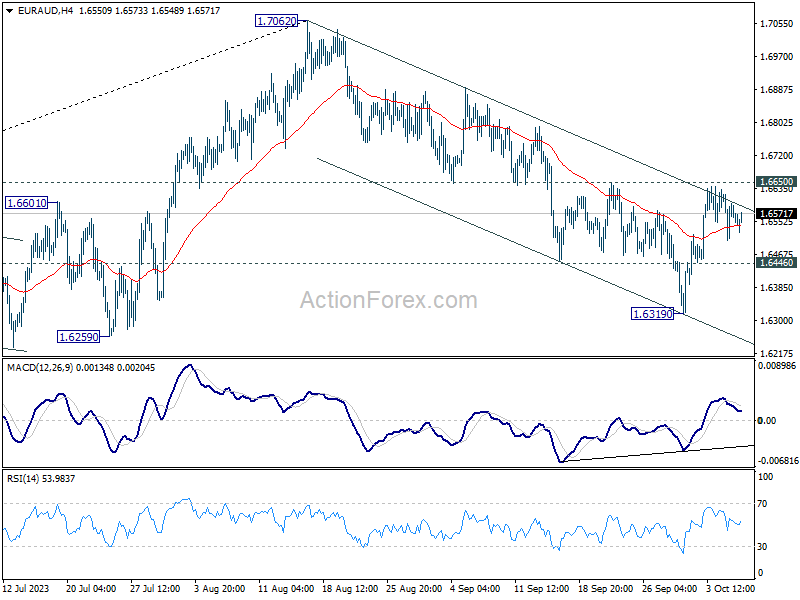

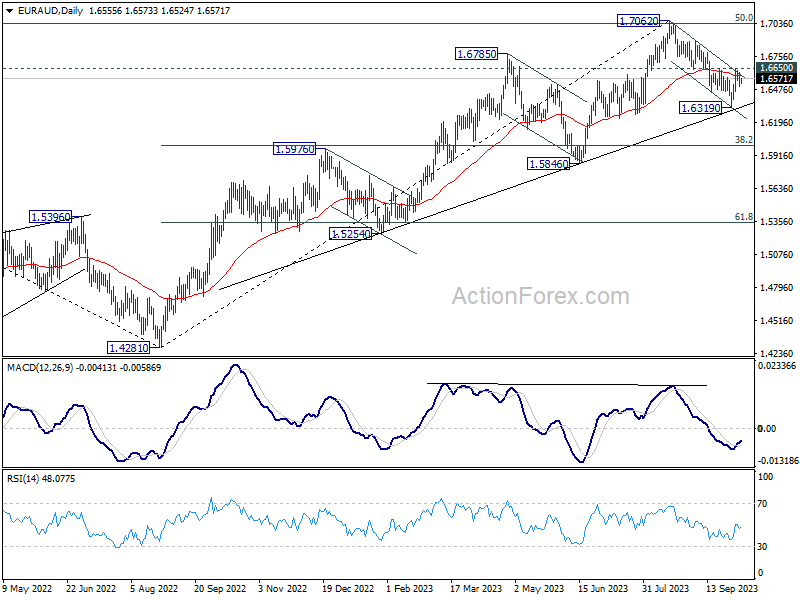

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6502; (P) 1.6565; (R1) 1.6625; More...

Range trading continues in EUR/AUD and intraday bias remains neutral. With 1.6650 resistance intact, fall from 1.7062 is still expected to continue. Below 1.6446 minor support will bring retest of 1.6319 first. Break there will resume the decline to 1.6000 fibonacci level. On the upside, firm break of 1.6650 resistance will argue that pull back from 1.7062 has completed, after drawing support from medium term rising trend line. Further rally would be seen back to retest 1.7062.

In the bigger picture, fall from 1.7062 is probably correcting whole up trend from 1.4281 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.4281 to 1.7062 at 1.6000. Strong support could be seen there to bring rebound, at least on first attempt. This will remain the favored case as long as 1.6650 resistance holds.

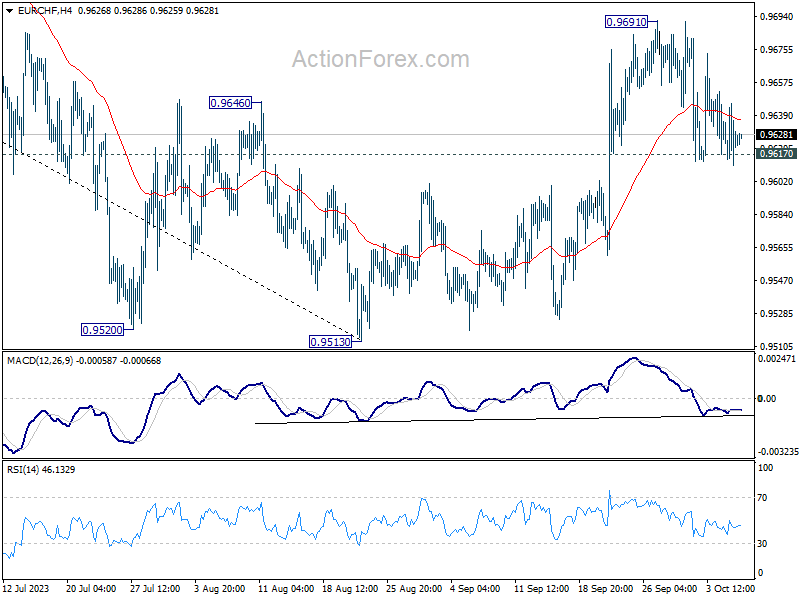

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9610; (P) 0.9629; (R1) 0.9645; More...

Intraday bias in EUR/CHF stays neutral and outlook is unchanged. Another rally is still mildly in favor as long as 0.9617 support holds. Above 0.9691 will resume the rebound from 0.9513 to 38.2% retracement of 1.0095 to 0.9513 at 0.9735. However, firm break of 0.9617 will turn bias back to the downside for retesting 0.9513 low.

In the bigger picture, medium term outlook will stay bearish as long as the cross is capped well below falling 55 W EMA (now at 0.9804). That is, down trend from 1.2004 (2018 high) could still resume through 0.9407 (2022 low). However, sustained trading above the 55 W EMA will raise the chance that 0.9470 is already a long term bottom. Further rise would then be seen to 1.0095 resistance to indicate bullish trend reversal.

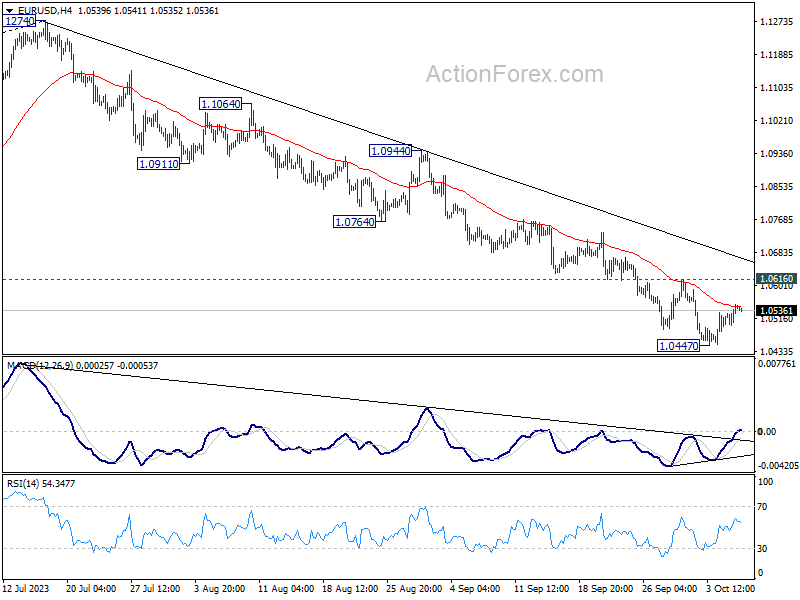

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0517; (P) 1.0534; (R1) 1.0569; More...

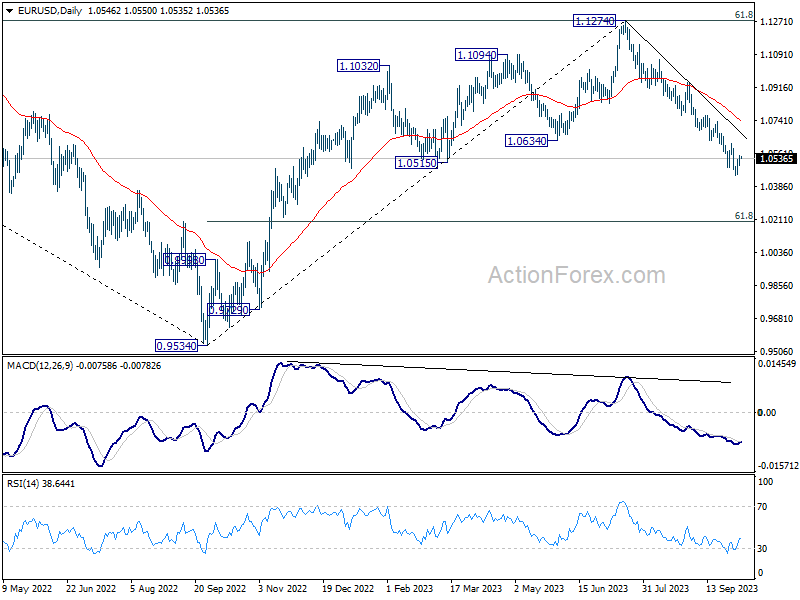

EUR/USD is staying in consolidation from 1.0447 and intraday bias remains neutral. Outlook will stay bearish as long as 1.0616 resistance holds. Break of 1.0477 will resume the fall from 1.1274 to 1.0199 fibonacci level next. Nevertheless, firm break of 1.0616 will confirm short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0759) holds, in case of rebound.

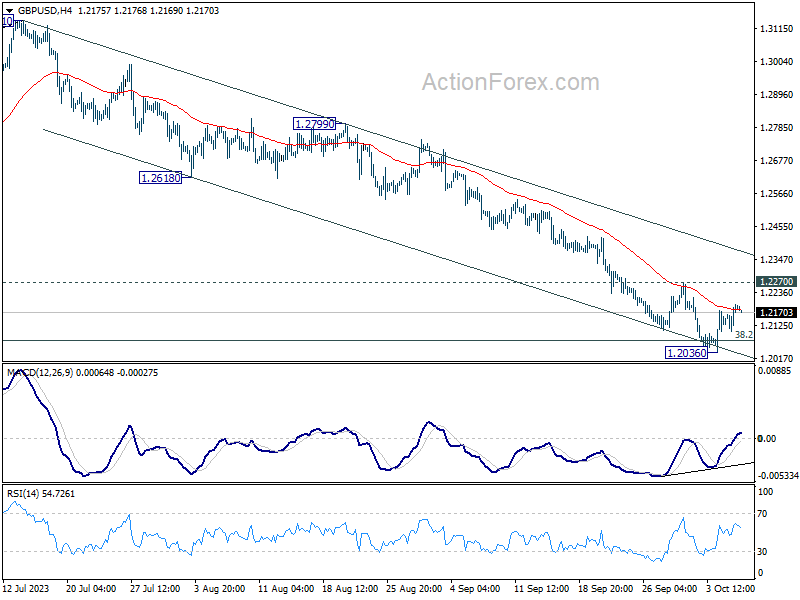

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2135; (P) 1.2166; (R1) 1.2223; More...

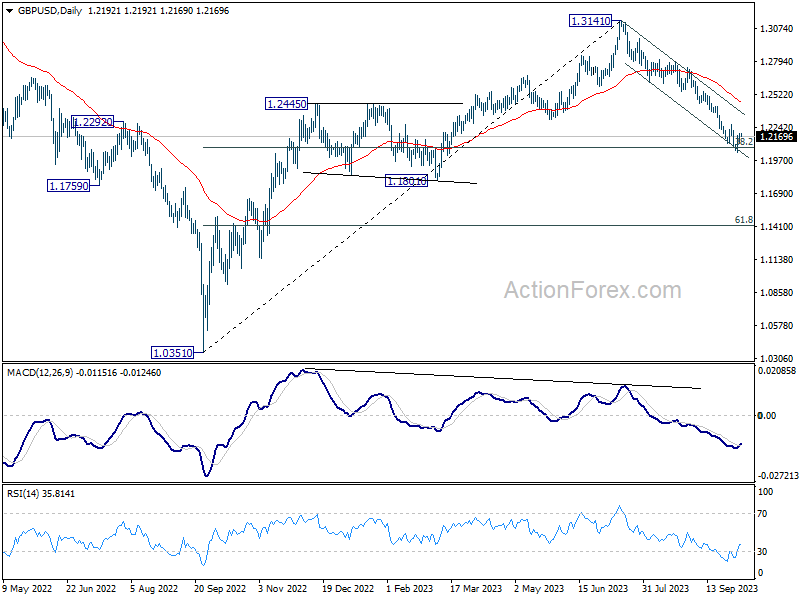

GBP/USD's consolidation from 1.2036 is still in progress and intraday bias remains neutral. Outlook will stay bearish as long as 1.2270 resistance holds. Break of 1.2026 will resume the fall from 1.3141. Sustained trading below 1.2075 fibonacci level would carry larger bearish implication, and target 1.1801 support next. On the upside, firm break of 1.2270 resistance will indicate short term bottoming, and turn bias back to the upside.

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2486) holds, in case of rebound.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9103; (P) 0.9142; (R1) 0.9164; More....

USD/CHF is extending the consolidation from 0.9243 and intraday bias remains neutral. Near term outlook will stay bullish as long as 0.9089 support holds. On the upside, break of 0.9243 will resume the rally from 0.8551 and target 0.9439 resistance next. However, firm break of 0.9089 will confirm short term topping, and turn bias back to the downside for deeper pull back.

In the bigger picture, current development indicates that rise from 0.8551 is reversing whole down trend from 1.0146. Further rally would then be seen to 61.8% retracement at 0.9537 and above. For now, this will be the favored case as long as 55 D EMA (now at 0.8963) holds, even in case of deep pullback.