Sample Category Title

USD/JPY Could Correct Lower, US Nonfarm Payrolls Next

Key Highlights

- USD/JPY struggled above 150.00 and reacted to the downside.

- It traded below a key bullish trend line with support at 149.00 on the 4-hour chart.

- Gold prices are accelerating lower and might drop toward the $1,780 support.

- The US nonfarm payrolls could increase by 170K in Sep 2023, down from 187K.

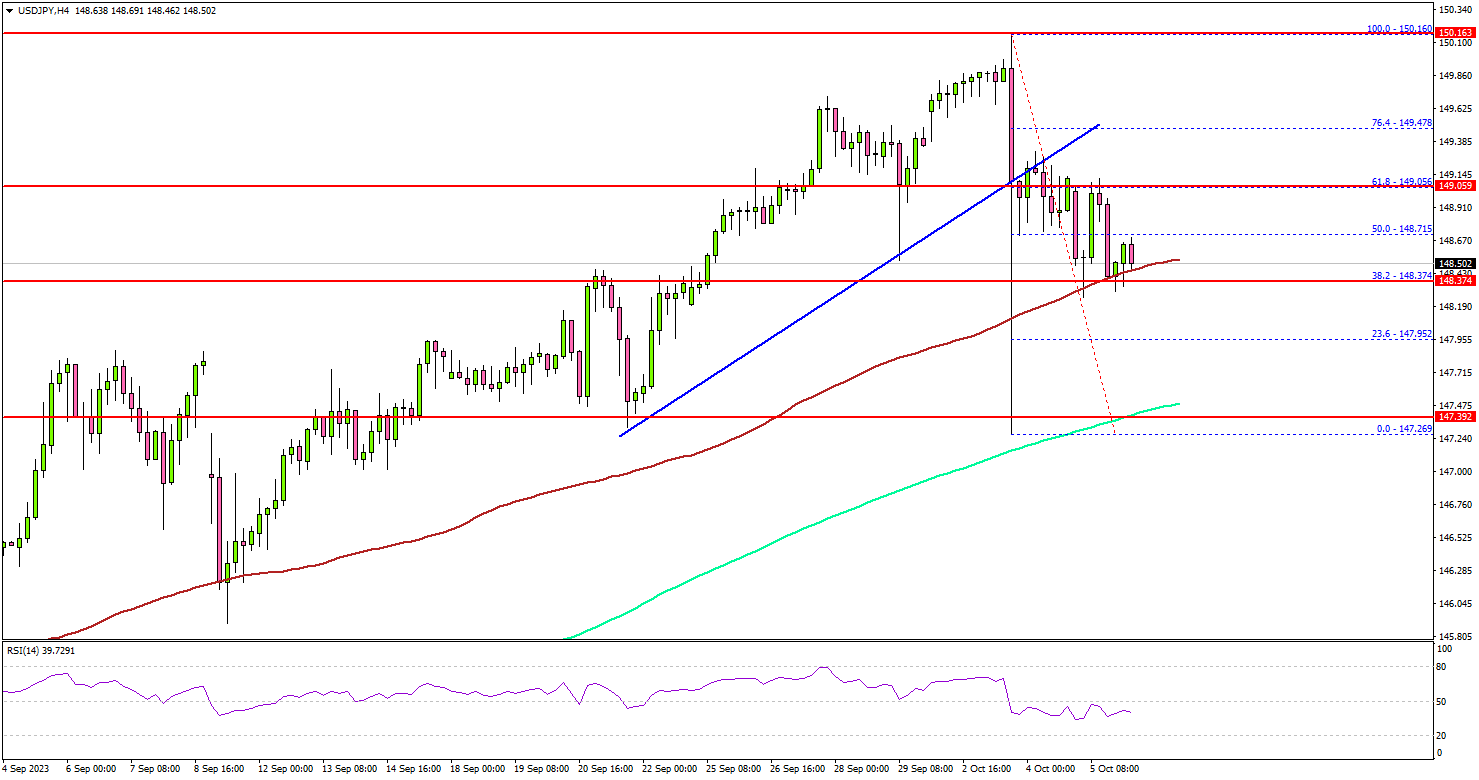

USD/JPY Technical Analysis

The US Dollar rallied above the 148.00 resistance zone against the Japanese Yen. USD/JPY even broke the 149.50 and 149.80 levels before the bears appeared.

Looking at the 4-hour chart, the pair struggled above 150.00 and reacted to the downside. A high was formed near 150.16 before the pair declined. There was a move below a key bullish trend line with support at 149.00.

The pair flash crashed toward the 147.25 level before recovering to 149.00, the 100 simple moving average (red, 4 hours), and the 200 simple moving average (green, 4 hours).

However, the pair is struggling to clear the 149.00 resistance. A close above 149.00 could start a steady increase. In the stated case, USD/JPY might rise and recover toward the 150.00 resistance zone.

Immediate support is near the 148.35 level. The next key support is seen near the 148.00 level, below which it could test 147.40 and the 200 simple moving average (green, 4 hours). Any more losses might send the pair toward the 146.60 level.

Looking at gold, the bears remained in control, and they seemed to be aiming for a move toward the $1,780 support zone.

Economic Releases

- US nonfarm payrolls for Sep 2023 – Forecast 170K, versus 187K previous.

- US Unemployment Rate for Sep 2023 - Forecast 3.7%, versus 3.8% previous.

- Canada’s Employment Change for Sep 2023 – Forecast 20K, versus 39.9K previous.

- Canada’s Unemployment Rate for Sep 2023 - Forecast 5.6%, versus 5.5% previous.

Japanese wages growth underwhelm as real income sinks for 17th mth

Subdued wage growth data in Japan is raising eyebrows, particularly at BoJ. An essential element for the central bank's policy normalization is the establishment of a harmonious cycle between wage growth and prices. The recent figures, however, indicate that this equilibrium remains elusive.

In August, labor cash earnings in Japan rose by a meager 1.1% yoy. This increase, while consistent with the prior month, fell short of the anticipated 1.5% growth. Furthermore, base salary growth, although increasing to 1.6% yoy from the preceding month's 1.4%, has yet to manifest signals of a robust and sustainable upward momentum.

The bright spot, perhaps, is the increase in overtime pay, which is often used as an indicator of business vibrancy, as 1.0% yoy ascent was observed, rebounding from July's flat growth.

However, inflation-adjusted real wages continued their downward spiral for the 17th consecutive month. August's real wages declined by -2.5% yoy, surpassing the projected -2.1% yoy dip. This trend starkly reveals that despite any increments, wages are struggling to keep up with the consistent price surges, placing added strain on the average consumer's pocket.

Also released, household spending, a critical driver of economic activity, contracted by -2.5% yoy, a figure that, while better than the anticipated -4.3% yoy decline and an improvement from July's -5.0% yoy reduction, still underscores constrained consumer expenditure.

Fed’s Barkin links yield surge to robust data, abundant supply

Richmond Fed President Thomas Barkin expressed a cautious stance yesterday, indicating it's "too early to know if another rate increase would be needed this year."

He further elaborated on the need for a wait-and-see approach, suggesting, "We have time to see if we've done enough or whether there's more work to do."

"The path forward depends on whether we can convince ourselves inflationary pressures are behind us or whether we see them persistent." Alongside inflation, Barkin pinpointed the labor market as a pivotal area of focus.

Addressing the recent surge in Treasury yields, Barkin attributed it to an abundant fiscal issuance, indicating, "There's a lot of fiscal issuance out there. That's creating a lot of supply." He also acknowledged the role of recent strong economic data in pushing the yields higher.

Fed’s Daly points to rising yields and diminishing need for rate hike

San Francisco Fed President Mary Daly weighed in on the implications of the recent spike in the benchmark 10-year Treasury note yield, which marked a 16-year peak at 4.8%.

"If financial conditions... remain tight, the need for us to take further action is diminished," she said yesterday, adding that the role of the financial markets in this scenario, suggesting that "they've done the work."

On the market's response to rising bond yields, she observed a dip in probabilities for another hike at the upcoming November meeting. "To me, that says the markets are understanding how we think about things and they do have the reaction function in mind," she elaborated.

Daly reiterated that continual observation of economic indicators, specifically a "cooling labor market" and inflation gravitating towards target, could justify steadiness in interest rates.

She elaborated that maintaining rates isn't a passive stance but an "active policy action," especially as declining inflation augments the restrictive impact of existing policy measures.

However, she also emphasized adaptability, hinting that should economic indicators such as growth and inflation not decelerate as expected, or if financial conditions become overly relaxed, Fed is prepared to raise rates until monetary policy achieves its desired restrictiveness. "We need to keep an open mind, and have optionality," she underscored.

ECB’s Villeroy points to plateau in rates; dismisses need for rate hike

ECB Governing Council member Francois Villeroy de Galhau, in an interview with the German newspaper Handelsblatt published yesterday, weighed in on the current debate surrounding ECB's interest rates. Stating his view clearly, Villeroy remarked, "Today, I think there's no justification for an additional increase in the ECB rates."

Rather than focusing on the peak in rates, Villeroy believes the dialogue should shift towards the concept of a rate "plateau." In his words, "we'll remain on this plateau as long as necessary."

Villeroy also provided reassurance regarding the economic outlook of the eurozone. Contrary to the hard landing fears that loomed last winter, he noted, "We are not facing the worst-case scenario." Elaborating further, he added, "I believe our monetary policy can and should now aim for a soft landing for the euro zone: We'll exit inflation, and we'll probably do so without a recession."

Commenting on the broader market sentiments, Villeroy observed that expectations, both in Europe and US, have historically been "a little too optimistic regarding a future rate cut."

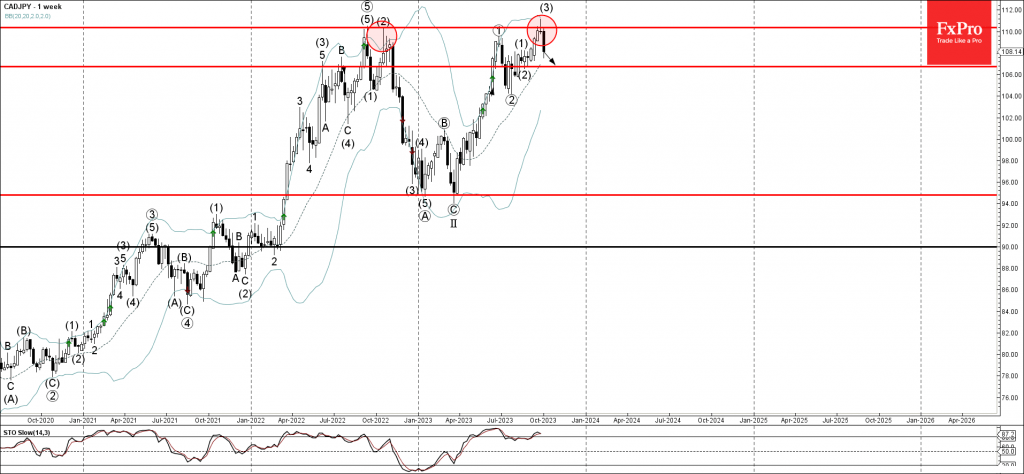

CADJPY Wave Analysis

- CADJPY reversed from powerful resistance level 110.35

- Likely to fall to support level 106.7

CADJPY currency pair recently reversed down from the powerful resistance level 110.35 (which stopped the previous weekly uptrend in 2022) standing near the upper weekly daily Bollinger Band.

The downward reversal from the resistance level 110.35 is currently forming the weekly Evening Star – strong sell signal for this currency pair.

Given the bearish divergence one the weekly Stochastic, CADJPY currency pair can be expected to fall further toward the next support level 106.7.

Stocks and Oil Prices Not Seeing Typical Calm Before NFP Friday

Stocks are slightly lower as calm emerges in the bond market. Wall Street is still seeing a lot of strength in the labor market. The S&P 500 index turned negative after slightly lower-than-expected weekly jobless claims. The risk for higher rates remains as a labor market slowdown was supposed to happen before the holiday hiring season.

Positioning ahead of tomorrow’s NFP report will likely be limited given it seems most leading indicators suggest job growth will remain healthy, which should keep the bond market selloff going strong. A strong headline number will likely be expected given we only saw the ADP private payroll miss. Eventually the surging cost of capital will support a softening of the labor market, but it doesn't seem like that will be reflected in tomorrow's report.

As companies are getting ready to show their books to investors next week, in the quarterly ritual known as earnings season, traders want to know if third quarter results come in as good as the first half of the year. The banks kickoff earnings at the end of next week and it seems many are expecting the financials to highlight a much weaker consumer given surging delinquencies and exhausted excess savings. Pessimism for the consumer won't be going away anytime soon and that is probably why stocks are selling off today.

US Data

The last labor market reading before the NFP report provided another reminder that the labor market is still strong. Worker filings for unemployment benefits held steady at 205,000 in the week ending on September 30th. The UAW strikes have yet to really impact the data as Michigan saw only 1,282 claims, Ohio had 1,422, and Missouri only had 532.

The Challenger, Gray & Christmas report showed planned job cuts fell from a 266% year-over-year pace in August to 58%. Companies announced plans to fill over 590,000 jobs last month, which was up 55% from a year ago.

FX

The US dollar is softer across the board as FX traders reduce positions ahead of a key jobs report. The higher-for-longer trade has mostly been priced in for the dollar against all of its major trading partners. CFTC data shows leveraged funds have ramped up dollar futures contract bets to the best levels since June. Unless we see US job growth fall below 100,000, the king dollar trade might remain in place a little while longer.

Oil

This oil market reversal must be frustrating the Saudis. Brent crude has fallen over $10 since the end of last month as surging global bond yields have crippled the global growth outlook. Energy stocks have gone from Wall Street's best trade to it is time to abandon ship. US gasoline demand destruction is intensifying and given how overbought the energy market was in September, momentum oil selling has been fierce.

When oil prices tank, it is hard to estimate where prices could find support. Brent crude’s five-day plunge however could find support around the $83 level, which is around both the 100- and 200-day SMA. If China’s outlook continues to improve, we could easily see a return back to the $90 level. Further bearishness could also trigger further output cuts by OPEC+. OPEC+ worked hard to get oil back to $90 a barrel and they will likely continue to do whatever it takes to make sure we don’t see prices return to the lows of the year, which is around the $70 level.

Gold

Gold prices are softer after another weekly jobless claims report refused to show a labor market slowdown has arrived. Jobless claims are still at historically low levels and that will keep Fed officials sticking to the hawkish script. Wall Street is still mostly maintaining a bearish stance for equities, which should eventually lead to safe-haven flows for gold. Gold just needs the peak in rates in place but we might not have a clear picture until the release of both Friday’s US jobs report and the October 12th inflation data.

Sunset Market Commentary

Markets:

Global (interest rate) markets today were looking for direction after several high profile yield levels were touched earlier this week (3% German 10-y, 5% 30-y US yield). A softer than expected ADP job growth yesterday and a substantial correction of the oil price (brent $84/b this morning from a peak of $97+/b last week) were a good reason for investors to take a more cautious approach going into tomorrow’s key US payrolls report. However, don’t call it a correction yet. The only market relevant US data series, the weekly jobless claims at least didn’t support yesterday’s ‘correction’. Claims stayed at a very low207k. Yields briefly ticked up, but currently again trade near pre-claims levels. The belly of the US curve outperforms (5-y -5 bps). The 30-y still adds 1 bp. The German curve shows a similar pattern, with the 2-y/5-y easing about 2.5 bps but the 30-y rebounding 1 bp (was even higher earlier today). Intra-EMU 10-y spreads versus Germany stay near/at recent peak levels. The 10-y Italian spread (+4 bps revisits the 2% barrier). The tentatively more benign (or is it less negative) sentiment on bond markets slowed the equity down leg. However, with the EuroStoxx 50 ‘gaining’ 0.3% and US indices opening little changed, it’s much too early too call a risk-rebound. Sentiment and the technical picture in most major equity indices remain fragile, to say the least. For example a return of the EuroStoxx 50 above the 4200 previous range bottom for now doesn’t look that evident.

A fragile/cautious underlying risk sentiment explains ongoing USD resilience. Which currency presents itself as alternative for the reference currency carrying a 2%+ long term real yield combined with economic outperformance? At 106.75, the tradeweighted DXY easily holds within the established uptrend channel since mid-July. EUR/USD (1.0525) struggles to prevent a relapse below the 1.05 big figure. Commodity/oil related currencies especially stay in the defensive. USD/CAD intraday touched the 1.378 area, the weakest level for the loonie since March. EUR/NOK rebounds to revisit the EUR/NOK 11.60/62 resistance. AUD/USD (0.634 area) also remains within striking distance of YTD low (0.6286) touched earlier this week. The Swiss franc is looking for a ‘bottom’ after the end September correction (EUR/CHF 0.965). EUR/GBP is holding a tight range, close too, mostly slightly above 0.865. BoE deputy Governor Broadbent indicated that he sees clear signs that the economy is weakening including ‘the beginning of some rise in unemployment’. His comments suggest that the bar for additional BoE hiking is becoming ever higher.

News & Views:

The Bank of England published its Monthly Decision Maker Panel data for September today. The DMP is a survey of CFO’s at UK firms. Firms reported that their output prices rose by an average annual rate of 7.4% in the three months to September, unchanged from August. They expect output price inflation to be 4.8% a year-ahead (down from 5%). One-year ahead CPI inflation expectations increased slightly to 4.9% (up from 4.8%). Three-year ahead CPI inflation expectations remained flat at 3.2%. Current perceived CPI inflation was 7.1%, compared to an official ONS figure of 6.7%. Expected year-ahead wage growth remained unchanged at 5.1% on a three-month moving average basis, down from 6.9% realized wage growth for the three months to September this year. 51% of firms reported that the overall level of uncertainty facing their business was high or very high, marginally lower than 53% in August. Finally, they indicated that the average interest rate that they were paying on their borrowing was 6.6% (from 6.2%) with a year-ahead expectation of 6.3%. Overall, the DMP survey suggests that the BoE better continues to keep a close eye on price (expectations) before calling victory too early.

The WTO lowers its trade growth forecast for this year amid a global manufacturing slowdown. Projections have been scaled back amid a continued slump that began in Q4 2022. The effects of persistent inflation and tighter monetary policy, togethers with strained property markets in China and consequences of the war in Ukraine all cast their shadow. The volume of world merchandise trade is now expected to grow by 0.8% this year (vs 1.7% forecast in April). The 3.3% growth estimate for 2024 remains nearly unchanged.

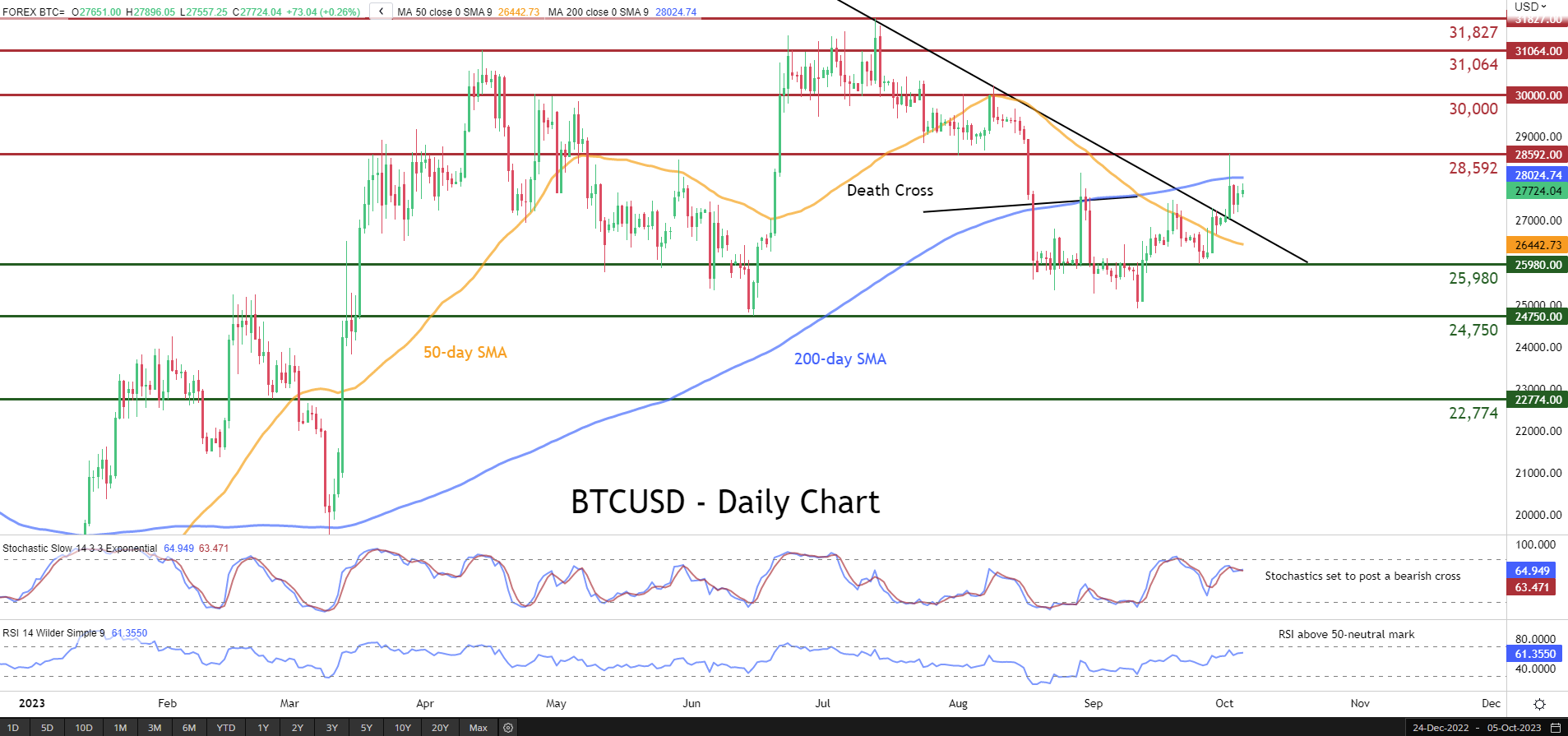

BTCUSD Gets Capped by 200-day SMA

- Bitcoin in a steady advance, jumping above crucial descending trendline

- Despite the jump above 28,000, 200-day seems a tough obstacle

- Death cross points to losses but momentum indicators diverge

BTCUSD (Bitcoin) has been forming a structure of higher highs and higher lows since its bounce off the September bottom of 24,915. Interestingly, the completion of a bearish cross between the 50- and 200-day simple moving averages (SMAs) has failed to trigger a decline.

If buying interest intensifies, the king of cryptos could initially attempt to break above the 200-day SMA before it tests the recent rejection region of 28,592. Even higher, the crucial 30,000 psychological mark could prove to be a tough one for the price to overcome. A jump above that zone may pave the way for the April peak of 31,064.

On the flipside, should the price reverse lower, the recent support of 25,980 could act as the first line of defence. Piercing through that floor, the digital coin might then descend towards the June bottom of 24,750. Further retreats could then come to a halt at 22,774, which has acted both as support and resistance in the past few months.

Overall, BTCUSD seems to be extending its recent upside move amid diverging technical signals. Nevertheless, a break below the downward sloping trendline could be the starting point of a fresh downleg.