Sample Category Title

BoE survey shows business inflation expectations cool

BoE's Decision Maker Panel survey for September indicating an anticipated ease in output price inflation, slowly easing CPI inflation expectation, and subtle nuances in wage growth predictions

A notable takeaway from the survey is the anticipated decline in output price inflation over the next year. Businesses foresee their year-ahead own-price inflation at 4.8%, a slight moderation from the 5.0% noted in the preceding three months to August. This decline hints at an expectation of easing price pressures, offering a counter-narrative to prevalent inflation concerns.

On the consumer front, one-year ahead CPI inflation expectations inched higher to 4.9% in September from 4.8% in August. However, a broader perspective reveals a decline, with the three-month moving average dipping by 0.3 percentage points to 5%. Looking further ahead, three-year CPI inflation expectations held steady at 3.2% in September, unaltered from August.

In the realm of wages, the anticipated year-ahead wage growth was static at 5.1% on a three-month moving average basis. September's single-month reading did register a slight uptick to 5.2%, a 0.2 percentage point increment from August. However, these expectations are notably subdued compared to realised wage growth.

ECB’s Kazimir strongly believe that latest hike was last

ECB Governing Council member Peter Kazimir said today, "I strongly believe that our rate hike at the last meeting was the last one" The focus, he outlined, now shifts to the upcoming December and March forecasts, as “only real data can persuade us that we're at the peak.”

Kazimir addressed inflation concerns, observing that, "We see the overall inflation and also core inflation on a downward trend, though this is lasting a bit longer than we'd wanted." He further highlighted the ripple effects of past rate hikes, pointing out that they "have an increasingly significant impact on the real economy."

Shedding light on the broader economic repercussions, he mentioned that "Financing conditions are tightening and are weakening demand for investments, in production and affecting overall economic growth." With this context, Kazimir emphasized the urgency to manage inflation effectively and swiftly.

On the topic of ECB's PPEP reinvestments, Kazimir treaded cautiously, suggesting the bank was "ready for debate" but reiterated the importance of maintaining balance. The topic of altering the balance sheet's reduction pace will be broached only when the Council is confident further rate hikes won’t be necessary.

Crypto Hits a Glass Ceiling

Market Picture

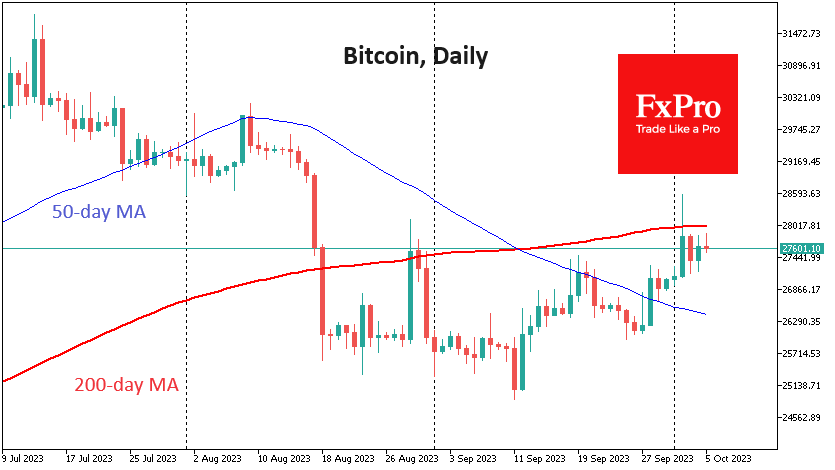

The crypto market is struggling to break above the $1.09 trillion cap, having turned south from that level on Thursday morning, bringing the total market valuation down to $1.084 trillion.

Bitcoin continues to tend to sell on growth, failing to make a fresh attack on the 200-day. Bitcoin has recently outperformed the stock market but is now retreating against the buying in the indices. In the short term, bitcoin seems more at risk of falling than rising.

Ethereum also seems to be on the bears’ side, losing for the fifth consecutive session, tied to the downward-sloping 50-day moving average.

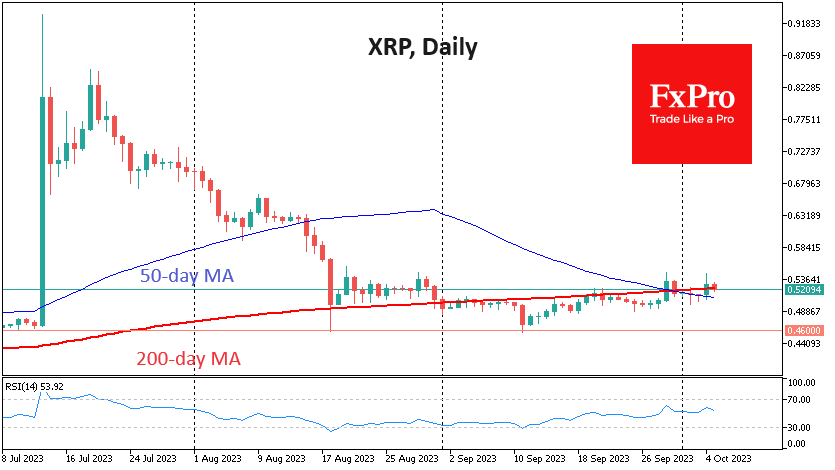

XRP has been trading at arm’s length from its 200-day moving average since the second half of August, most of the time acting as resistance.

The entire cryptocurrency market seems to be waiting for a substantial pullback in the top coins to buy in for the long term.

News background

The court rejected the SEC’s appeal in the Ripple case, noting that the regulator did not provide enough evidence and that the request would not “materially advance the ultimate dismissal of the case.”

The Bank for International Settlements (BIS) has developed a prototype system for monitoring Bitcoin transfers to give authorities a clearer picture of how, when and where the cryptocurrency is being used. The new monitoring system could form the basis for regulating the cryptocurrency sphere.

Indian authorities have begun developing a global cryptocurrency transaction tracking system that will allow government authorities to monitor transactions in digital assets across all cryptocurrency exchanges worldwide.

El Salvador launched the first local Bitcoin mining pool. The Volcano Energy project started mining the first cryptocurrency on Lava Pool in partnership with Luxor Technology.

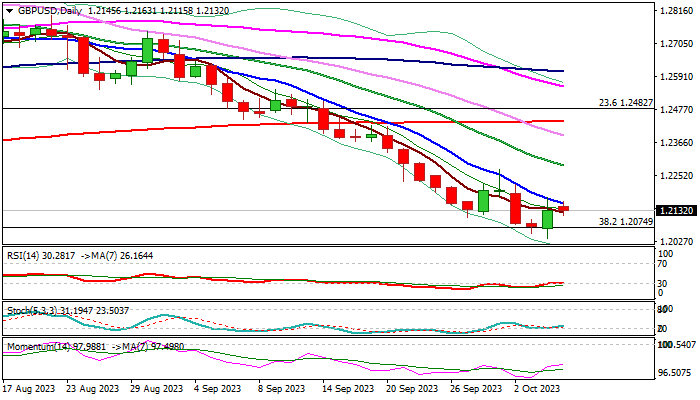

GBP/USD: Falling 10DMA Continues to Cap Recovery Attempts

Cable started to lose traction in early European trading on Thursday, after Wednesday’s recovery, supported by better than expected UK services PMI and US ADP miss, stalled under initial resistance – falling 10DMA (1.2173), which continued to cap the action.

UK construction PMI (released this morning) dipped well below expectations in September and slid below 50 threshold for the first time since March 2020, adding to fresh negative signals.

Technical picture on daily chart remains firmly bearish with strong downside risk while 10DMA continues to limit recovery attempts.

Larger bears faced a double rejection at pivotal Fibo support (38.2% of 1.0348/1.3141) at 1.2074, but mild correction (capped by 10DMA) keeps the downside vulnerable, with eventual break here to expose psychological 1.20 support and daily cloud top at 1.1988.

Meanwhile, the pair may hold in extended consolidation within 1.2074/1.2173 range before bears resume.

Conversely, sustained break above 10DMA would ease downside pressure, but stronger reversal signals expected on lift above falling 20DMA (1.2286).

Res: 1.2173; 1.2217; 1.2286; 1.2328.

Sup: 1.2115; 1.2074; 1.2037; 1.2000.

Japanese Yen Steadies as Intervention Speculation Subsides

- USD/JPY drifting for a second straight day

- BoJ likely did not intervene in currency markets

The Japanese yen has posted slight gains on Wednesday. In the European session, USD/JPY is trading at 148.97, down 0.10%.

Yen spike was likely not due to intervention

The yen has stabilized after a massive spike on Tuesday. The yen spiked upwards close to 2% in a matter of seconds on Tuesday after the yen breached the 150 line for the first time since October 2022. This raised a flurry of speculation that the Bank of Japan intervened in the currency markets in order to prop up the yen. It remained unclear if the spike was driven by an intervention or a technical movement, and the fact that Japanese officials refused to comment only added to the mystery.

It now appears that the BoJ did not intervene, based on an analysis of the Bank of Japan’s current account figures. The Ministry of Finance publishes intervention records monthly, which means investors will have to wait until October 31st to answer the intervention question with certainty. If there was no intervention, the yen’s spike at 150 demonstrates nervousness in the markets which is hanging in the air.

The BoJ may not have intervened on the currency markets, but the central bank did intervene in the bond markets on Wednesday and made an emergency bond purchase. The move failed to stop yields from rising on 10-year yields of Japanese government bonds, which have risen to 0.816% today, the highest level since 2013. The BoJ has insisted that it will not phase out its ultra-loose policy, but speculation continues that tightening is only a matter of time.

USD/JPY Technical

- USD/JPY tested support at 148.50 earlier. Below, there is support at 147.84

- 149.10 is a weak resistance line, followed by resistance at 149.97

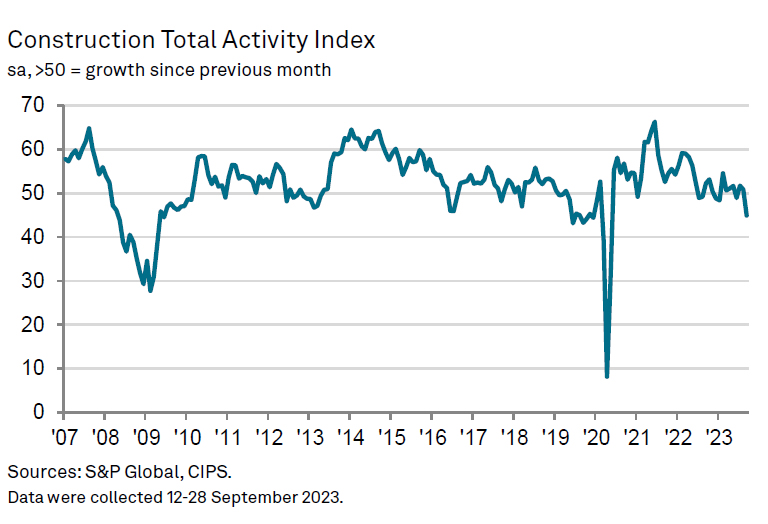

UK PMI construction dives to 45, sharp decline and worst since 2020

UK's construction sector is experiencing a significant setback, as evidenced by the sharp fall in PMI Construction index to 45.0 in September, a level not seen since May 2020 and far below the anticipated 49.9.

The report shows a distinct contraction in the industry, with residential work plunging to an index of 38.1, indicating the steepest decline amongst all sectors. Civil engineering activity isn't faring much better, posting a 45.7 index, while commercial building has shown some resilience, albeit still in the contraction zone at 47.7.

Tim Moore, Economics Director at S&P Global Market Intelligence, paints a grim picture of the current state of the sector. "Output levels declined across the UK construction sector for the first time in three months during September, and the latest downturn marked the worst overall performance since the early stages of the pandemic," he stated.

The future outlook for the construction sector does not instill confidence. Moore points out that the survey's forward-looking measures have remained somewhat pessimistic. "Order books decreased at an accelerated pace and business activity expectations eased to the lowest so far this year," Moore explained. The decrease in project starts has led to an increase in sub-contractor availability, reaching levels not seen since the summer of 2009.

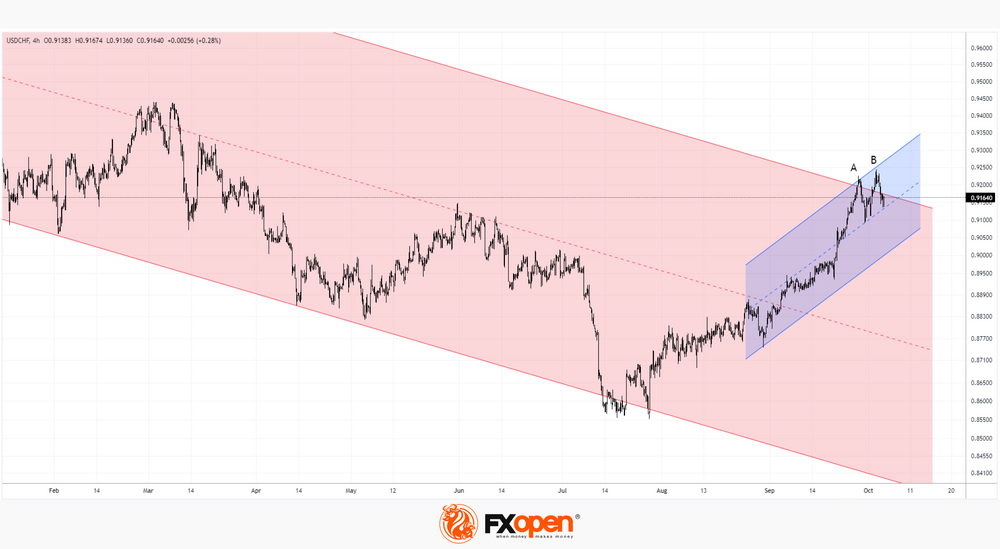

USD/CHF Analysis: Rate Rises to Its Highest in Six Months

This happened against the backdrop of rising US bond yields. Reuters writes that it is in the region of a 16-year high. It is reasonable to assume that big capital was balancing its defensive portfolio by selling the franc, considered a safe haven, and buying dollars to invest in American bonds, which also have high-quality status.

On July 13, we wrote that the franc could rebound from the lower line of the channel (shown in red). This was supposed to be facilitated by hawkish rhetoric from Fed officials and, as a result, the strengthening of the dollar.

However, now the situation has reversed. The USD/CHF rate expanded the range of a larger downward channel and reached its upper limit. It even tried to break out of it on October 3 (but without noticeable success).

Will the bullish trend described by the rising channel (shown in blue) continue?

Signs of technical analysis provide grounds for doubt:

→ extremes A and B are similar to the double-top pattern. Moreover, the fact that the second peak is higher than the first can be interpreted as a bull trap;

→ the formation of divergence on indicators – as an indication of weakening demand for the dollar;

→ bearish activity may intensify as the listed signs are formed near the upper border of the red channel.

Thus, the likelihood of a decline to the lower border of the blue channel increases, and in the longer term, attempts at its bearish breakout.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

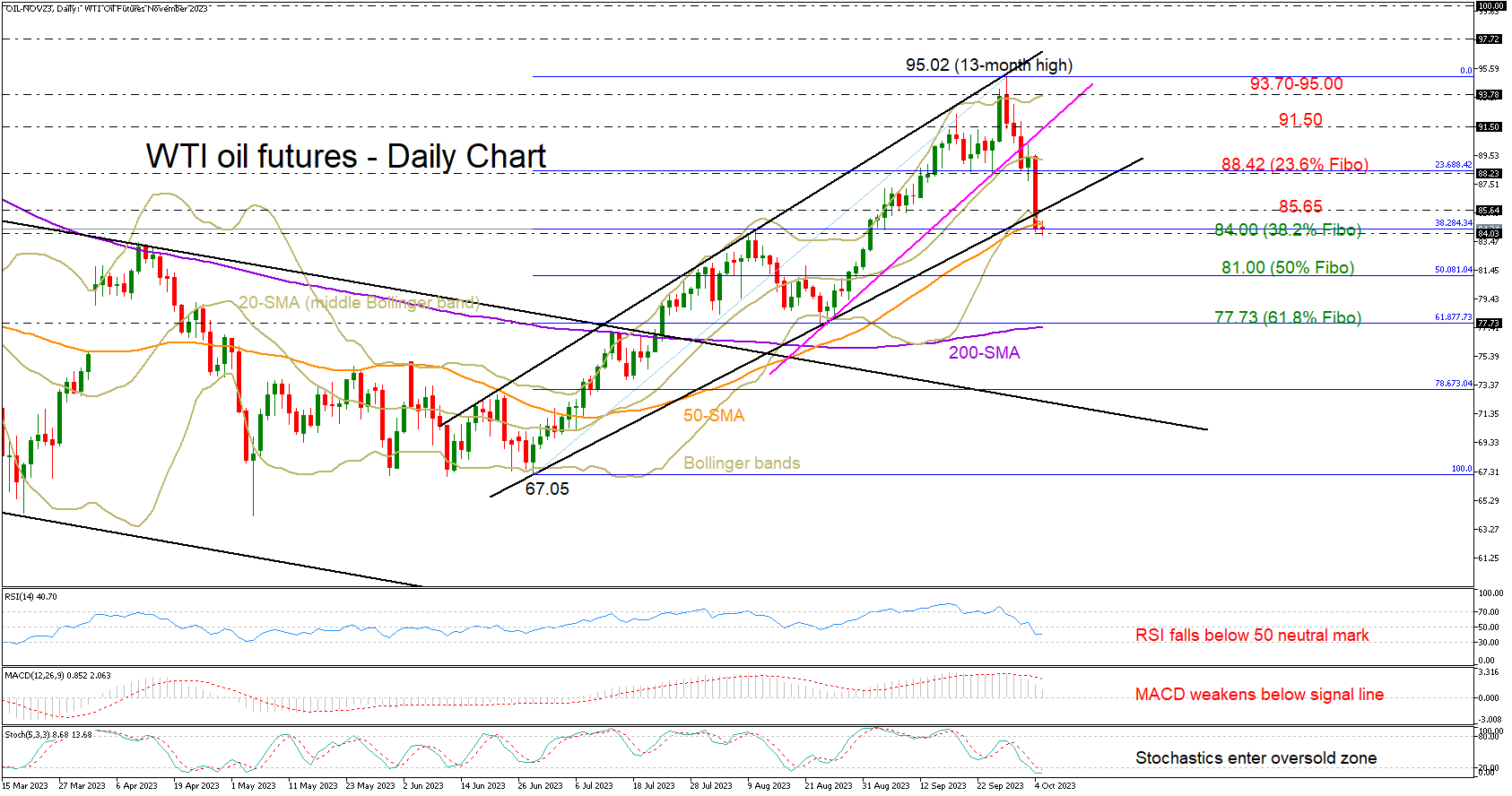

WTI Oil’s Uptrend Faces Hazards

- Oil rally at risk near 84.00 after latest freefall

- Bearish continuation likely, but patience required

WTI oil futures closed with heavy losses on Wednesday near a one-month low of 84.16 following the rejection near the 20-day simple moving average (SMA) at 89.40.

The 50-day SMA put the brakes on the bear run marginally below the support trendline from June. But the negative trajectory in the RSI, which has slipped below its 50 neutral mark, and the downward move in the MACD are currently suggesting the freefall has not bottomed out yet.

On the other hand, the oversold signals detected by the stochastic oscillator are leading to speculation that a consolidation phase or an upside correction could be underway. Note that the price is trading around the lower Bollinger band.

Hence, sellers could hold off until the price violates the June-September uptrend clearly below the 84.00 mark and the 38.2% Fibonacci retracement of the latest upleg. Such a downfall could pressure the price towards the 50% Fibonacci of 81.00 and then down to the 61.8% Fibonacci of 77.73, where the 200-day SMA is hovering.

Alternatively, a positive change in sentiment could encourage some buying, especially if the price crawls back above the broken support trendline at 85.65. In this case, the price could advance towards the 23.6% Fibonacci of 88.42 and again fight the 20-day SMA at 89.20. A successful move higher is expected to slow down around 91.40 before stretching towards the critical 93.70-95.00 resistance area.

Summing up, WTI oil futures are still vulnerable to downside risks, with selling forces expected to pick up pace below 84.00. Otherwise, the market may attempt to climb back above 85.65.

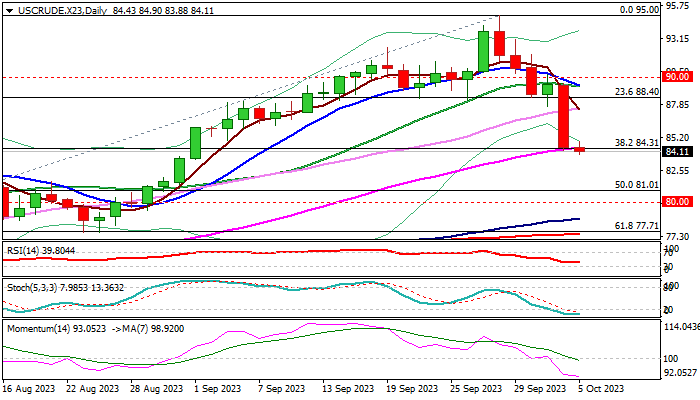

WTI Oil Remains Under Increased Pressure after Falling by 5.5% on Wednesday

Renewed concerns about demand after the latest soft economic data raised possibilities of further slowdown in global economic growth, soured the sentiment.

The OPEC+ group held their meeting on Wednesday and left the oil output policy unchanged, as Saudi Arabia and Russia decided to keep their voluntary output cut by 1 million bpd and 300,000 bpd respectively, unchanged for the rest of the year.

Oil price fell to the lowest in over one month, with Wednesday’s sharp fall contributing to formation of reversal pattern on daily chart.

Fresh weakness probes through pivotal Fibo support at $84.31 (38.2% of $67.02/$95.00 rally, where the action on Wednesday found temporary footstep) signaling that larger bears from $95.00 (2023 top, posted on Sep 28) may resume.

Daily studies maintain very strong bearish momentum and Wednesday’s massive bearish daily candle weighs heavily, opening way for fresh drop towards targets at $81.00 zone (top of rising daily cloud / 50% retracement) and $80.00 (psychological) in extension.

On the other hand, 14-d momentum is overstretched and stochastic in oversold territory, warning that bears may start to lose traction, though upticks should be limited and offer better selling levels in current conditions.

Former consolidation floor and broken Fibo 23.6% at $88.00/40 zone should cap extended upticks to keep bears in play.

Res: 84.90; 86.00; 87.54; 88.00.

Sup: 83.88; 81.71; 81.00; 80.00.

Markets Bounce Ahead Of US NFP Report

Asian shares staged a rebound on Thursday following the broadly positive cues from Wall Street overnight as plunging oil prices and weak US jobs data lifted market sentiment. European futures are pointing to a positive open amid the improving mood with investors directing their attention toward Friday’s US payrolls report which could support or hinder the market rally.

Looking at currencies, the yen is up roughly 0.3% this morning following the aggressive spike in value on Tuesday after touching 150 in USD/JPY. Given how it was the sole gainer versus the dollar, this fuelled speculation around official Japanese intervention. However, markets are still guessing what exactly triggered the move.

In the commodity space, oil prices plunged over 5% on Wednesday thanks to demand-side fears and a huge build in gasoline inventories. Gold is lingering near its lowest level since March, drawing some support from a weaker dollar and falling Treasury yields. Nevertheless, the precious metal remains vulnerable to further losses with sustained weakness below $1830 opening a path towards $1810.

US NFP in focus

The combination of economic data and speeches from Fed officials today could trigger more dollar volatility ahead of the highly anticipated non-farm payrolls report on Friday. Financial markets remain highly sensitive to US Treasury yields, and this continues to be reflected through the dollar rally.

The US economy is forecast to have created 170,000 jobs in September following August’s increase of 187,000 while the unemployment rate is seen cooling to 3.7% from 3.8% in the previous month.

A strong-than-expected US jobs report may support the “higher for longer” expectations around US interest rates, boosting the dollar as a result. However, further evidence of a cooling labour market may support the argument that the Fed is finished with hiking rates this year, weakening the greenback. As of writing, traders are currently pricing in a 20% probability of a 25-basis point hike in November, with this jumping to around 40% by December, according to Fed Funds futures.