Sample Category Title

Canada’s Trade Accounts Flip to a Surplus In August

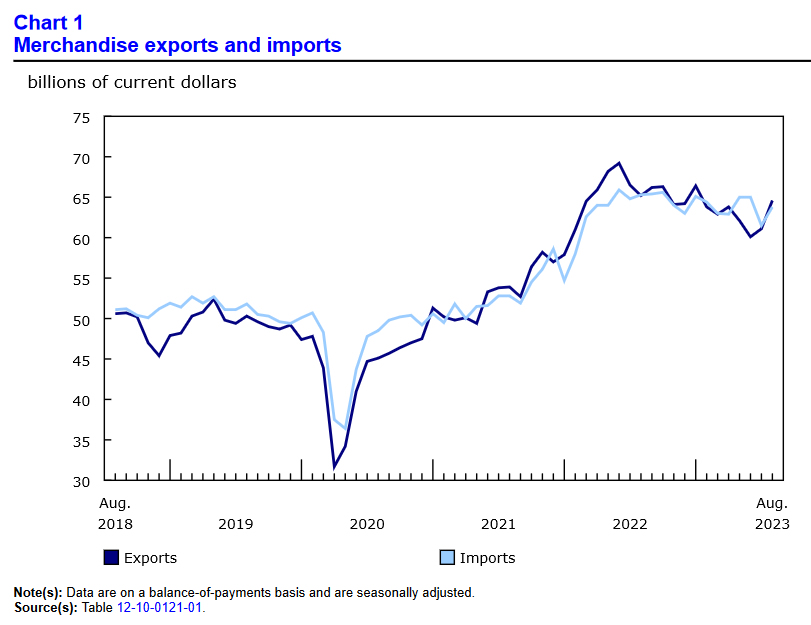

Canada's merchandise trade account registered a $718 million surplus in August after three consecutive months of deficits. This comes after July's deficit was revised upward to $437 million.

Exports increased by a healthy 5.7% month-on-month (m/m) in August. Gains were broad-based as 7 of 11 sectors posted increases, with exports of unwrought gold and crude oil doing most of the heavy lifting. Exports of unwrought gold, silver, and platinum metals (+89.5% m/m) were driven by higher exports to the U.S. Due to rising oil prices, crude oil exports rose 19% m/m. As port activity resumed from the B.C. strikes, strong gains in coal (+14.2%), potash (+21.4%), and lumber (+5.8%) were observed.

Meanwhile, total imports bounced back from a weak July, up 3.8% m/m to $63.8 billion. Increases in import activity were driven by many sectors: Industrial machinery and equipment imports rose by 7.5% m/m, imports of chemical products were up 11.2%, and metal ores and non-metallic minerals gained 13.6% m/m. Aircraft equipment and parts imports lagged other sectors (-15.9% m/m). Once again, imports were helped by the port strike resumption, with consumer goods imports edging up 2.2% and electronic equipment and parts gaining 3.7%. Imports were up in 9 of 11 sectors.

In volume terms, overall imports increase by 1.2% m/m while exports moved up by 3.0% m/m in August.

Canada's trade surplus with the United States widened from $8.2 billion in July to $10.4 billion in August, driven by higher exports of energy products.

In a separate report, Statistics Canada noted the country's services trade deficit widened from $1.2 billion in July to $1.5 billion in August.

Key Implications

August's trade data provided further evidence that net exports bounced back in the third quarter of this year. Recall that last quarter, export volumes were effectively flat after a strong Q1 showing, while imports edged higher, leading to a net drag on growth through the trade channel. As it stands, given trade data through July and August, we should see a sizable net contribution to Canada's third quarter GDP.

Last month's trade report cited that the effect of backlogs have affected trade activity. But given the healthy activity in trade this month, especially out of sectors most impacted by the strike, we'd say that the impact from the strike has largely dissipated. The broad-based improvement in imports and exports suggest some resilience in domestic and international demand with key trading partners.

Pound Shrugs Off Soft Construction PMI

- UK Construction PMI declines

The British pound has ticked higher on Thursday. In the North American session, GBP/USD is trading at 1.2149, up 0.09%.

UK Construction PMI declines

The UK Construction PMI fell to 45.0 in September, down significantly from 50.8 in August and below the consensus estimate of 49.9. This was the first decline in three months and the steepest decline since May 2020. The survey found that high mortgage rates and weak demand for house purchases had a negative impact on the construction industry. As well, business expectations fell to their lowest level this year.

The Construction PMI release is further evidence that the Bank of England’s sharp tightening cycle has cooled down the economy. This week’s Services and Manufacturing PMIs both pointed to contraction in September, with readings below the 50 level. The British pound didn’t react to the Construction PMI release, but the pound continues to fall toward the symbolic 1.20 line and the currency will likely face further headwinds if upcoming releases remain soft.

As inflation continues to ease, many major central banks are close to or at the end of their rate-tightening cycle. The Federal Reserve, Bank of England and the ECB were all late to the rate-hike party and don’t want to prematurely declare that rate hikes are over. Inflation remains well above target for all three central banks and stating that rate hikes remain on the table means that policy makers can raise rates if needed without losing credibility.

The BoE paused in September and another hike at the November meeting is a strong possibility, barring a nasty inflation surprise ahead of the meeting. The BoE, which still has its hands full with inflation, says that rate cuts remain a long way off, but that could change if economic growth continues to weaken and inflation falls sharply.

GBP/USD Technical

- GBP/USD tested support earlier at 1.2120. The next support level is 1.2035

- There is resistance at 1.2196 and 1.2256

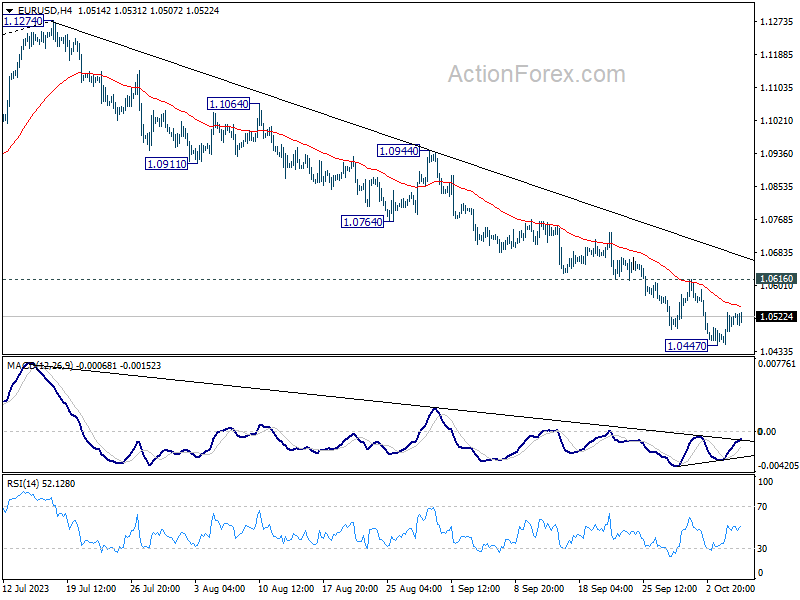

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0460; (P) 1.0496; (R1) 1.0540; More...

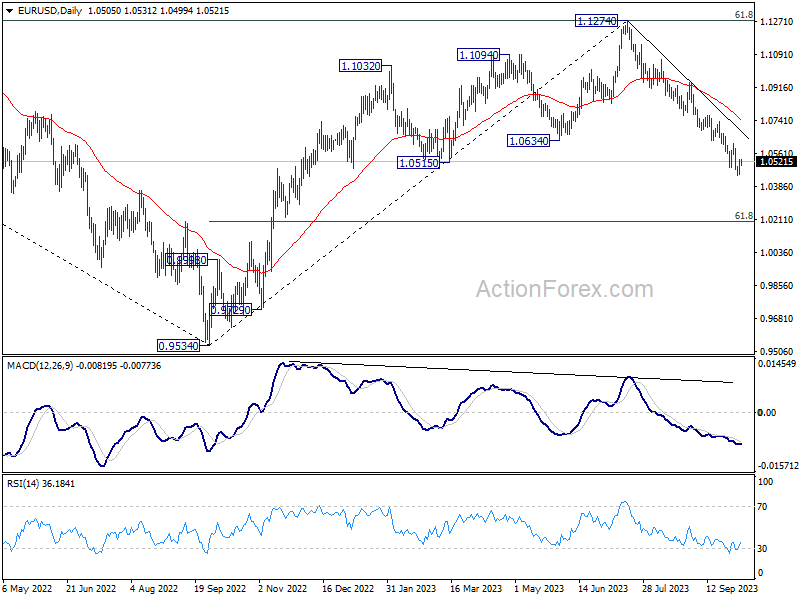

Intraday bias in EUR/USD stays neutral for the moment. Consolidation continues above 1.0447. Outlook will remain bearish as long as 1.0616 resistance holds. Break of 1.0477 will resume the fall from 1.1274 to 1.0199 fibonacci level next. Nevertheless, firm break of 1.06161 will confirm short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0759) holds, in case of rebound.

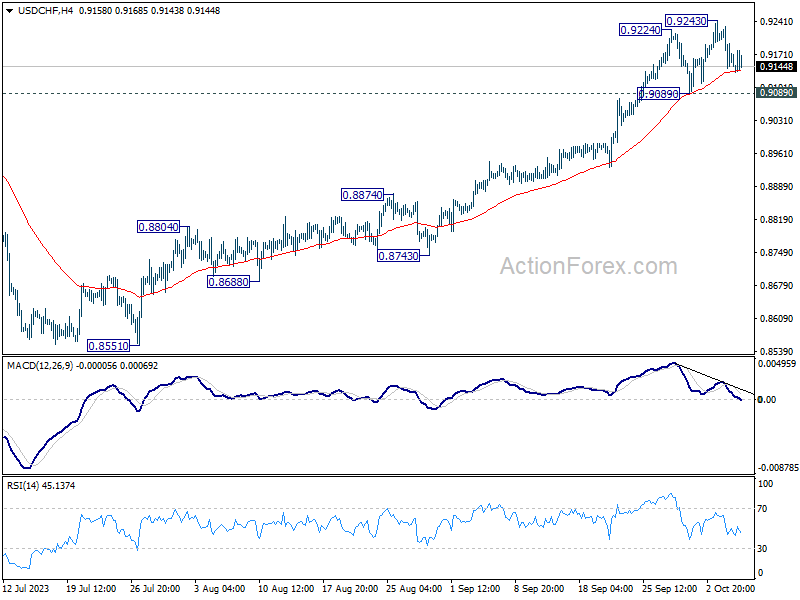

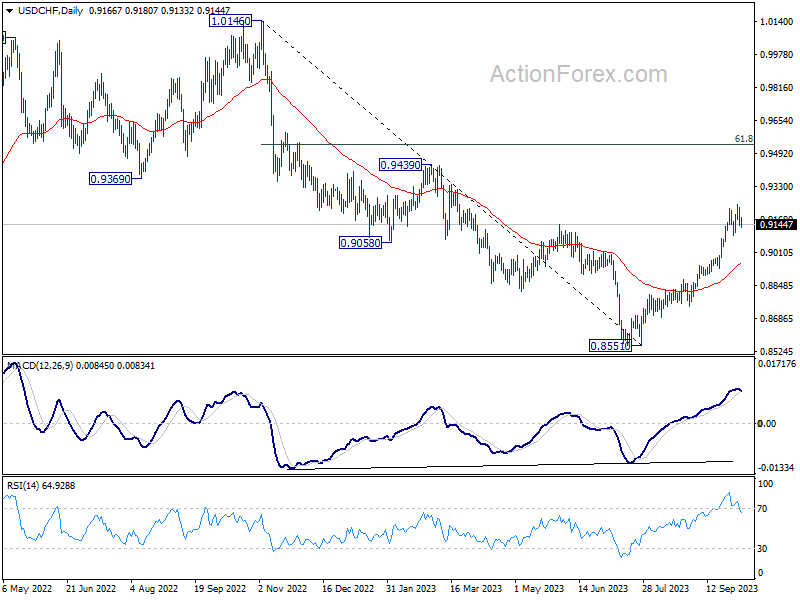

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9134; (P) 0.9183; (R1) 0.9223; More....

Intraday bias in USD/CHF stays neutral at this point. Consolidation is continuing below 0.9243. Near term outlook will stay bullish as long as 0.9089 support holds. On the upside, break of 0.9243 will resume the rally from 0.8551 and target 0.9439 resistance next. However, firm break of 0.9089 will confirm short term topping, and turn bias back to the downside for deeper pull back.

In the bigger picture, current development indicates that rise from 0.8551 is reversing whole down trend from 1.0146. Further rally would then be seen to 61.8% retracement at 0.9537 and above. For now, this will be the favored case as long as 55 D EMA (now at 0.8942) holds, even in case of deep pullback.

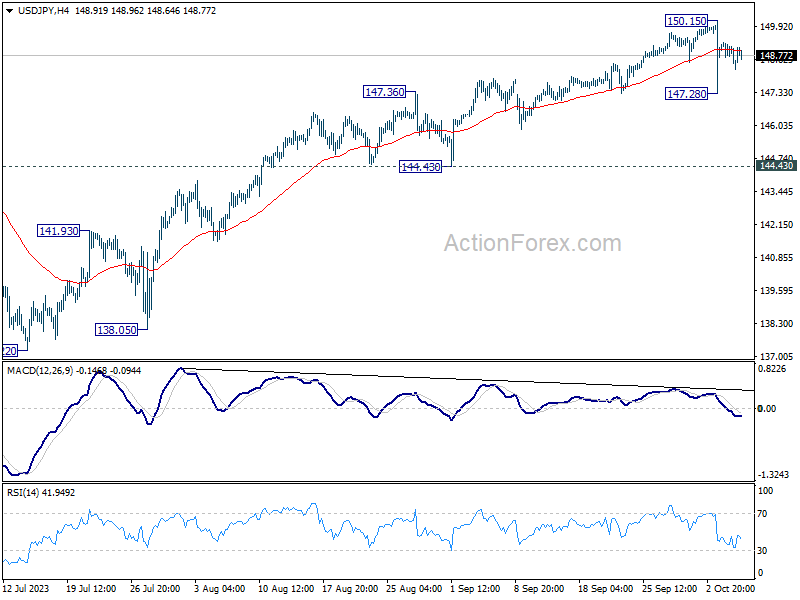

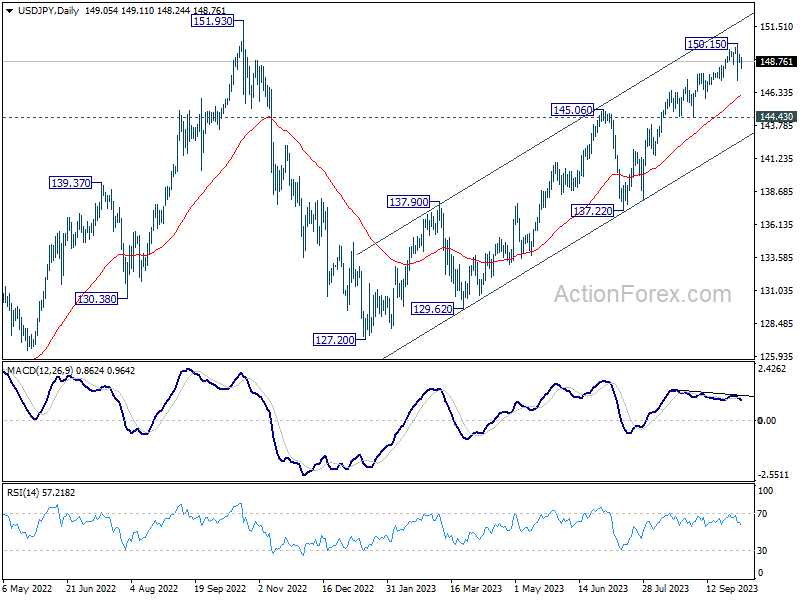

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.81; (P) 149.06; (R1) 149.39; More...

Intraday bias in USD/JPY stays neutral at this point. Sideway trading could continue below 150.15. On the downside, below 147.28 will turn bias to the downside for deeper pull back. But there is no confirmation of bearish trend reversal before firm break of 144.43 support. Another rally remains mildly in favor through 150.15 to retest 151.93 high.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will be the first sign that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

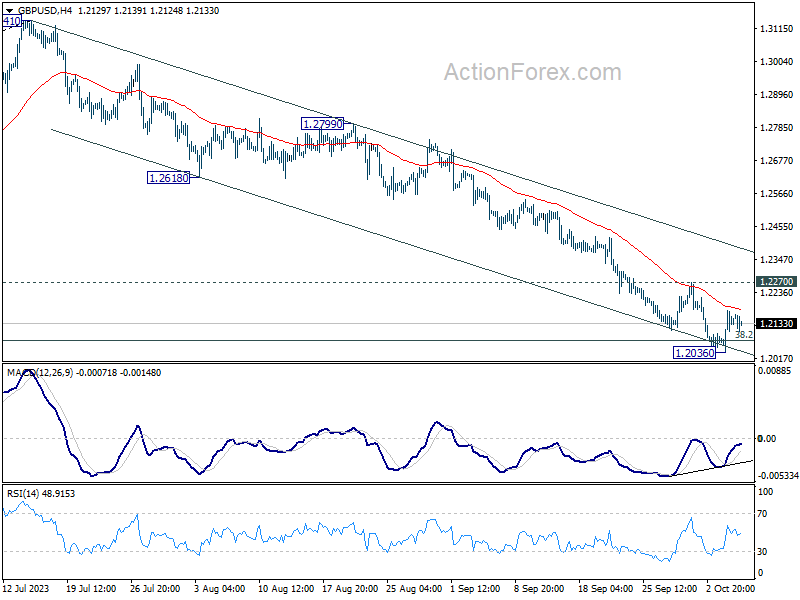

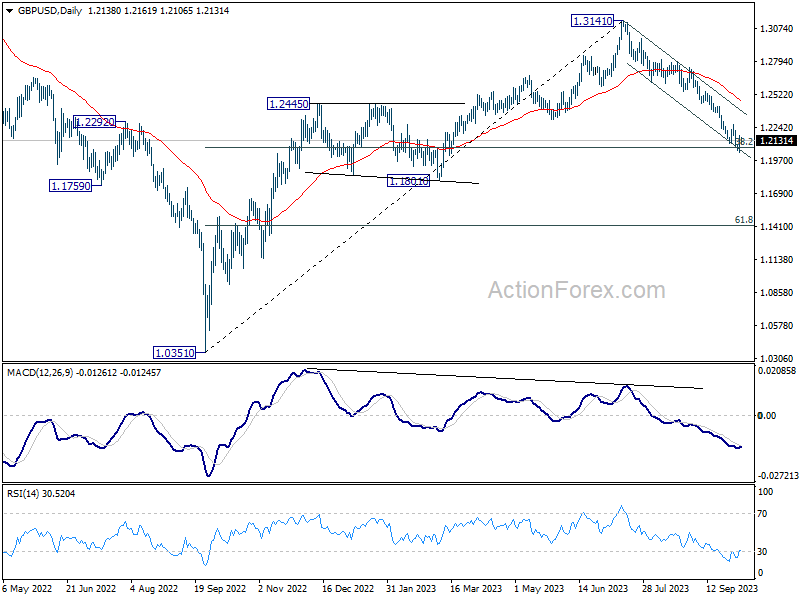

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2056; (P) 1.2116; (R1) 1.2196; More...

GBP/USD is staying in consolidation above 1.2036 and intraday bias remains neutral for the moment. Outlook will stay bearish as long as 1.2270 resistance holds. Break of 1.2026 will resume the fall from 1.3141. Sustained trading below 1.2075 fibonacci level would carry larger bearish implication, and target 1.1801 support next. On the upside, firm break of 1.2270 resistance will indicate short term bottoming, and turn bias back to the upside.

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2486) holds, in case of rebound.

Sterling Underwhelms amid Market Consolidation; Gold Heading Lower Again

British Pound emerged as the weakest link, facing headwinds following subpar construction data. Not far behind in performance was the Canadian Dollar, which felt the pressure from the ongoing plunge in oil prices. Dollar, while still in a commanding position, appears to be taking a pause, digesting its recent upticks. Contrastingly, Australian and New Zealand Dollars found some respite as the market's risk aversion sentiment momentarily eased. Meanwhile, Euro, Swiss Franc, and Yen are all moving within a mixed range, with no clear directional bias discernible.

However, it's crucial to underscore that today's performance is likely transient, serving as brief consolidations rather than indicative of any established trends. Yen, though challenged to prolong its intervention-boosted rally, remains the top-performer. Dollar holds its ground as second, albeit with an air of caution as market participants await Non-Farm Payrolls release tomorrow. Aussie and Kiwi Dollars, despite today's modest bounce-back, continue to languish at the bottom. Among European currencies, Sterling's underperformance stands out.

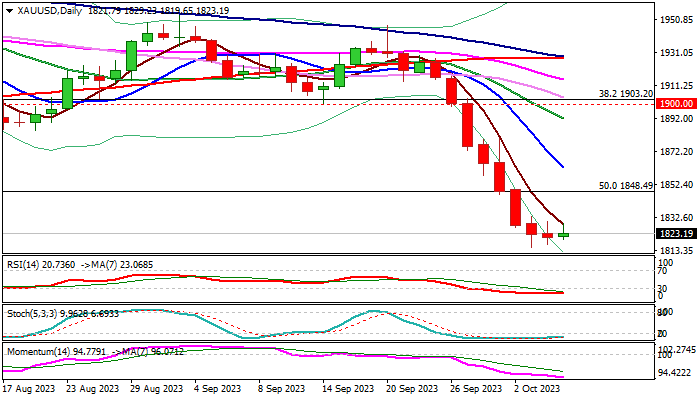

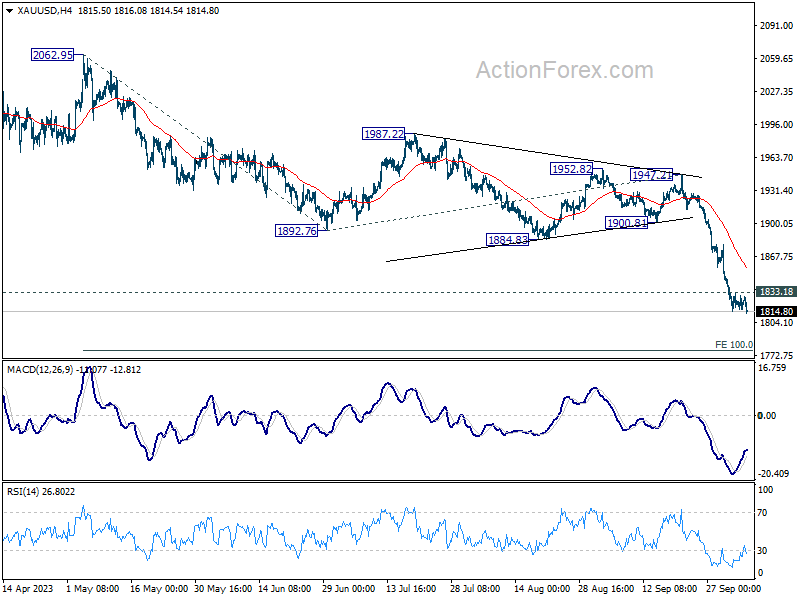

Technically, Gold is trying to resume recent decline in early US session. For now, further fall is expected as long as 1833.18 resistance holds. Next target is 100% projection of 2062.95 to 1892.76 from 1947.21 at 1777.02. However, break of 1833.18 resistance will bring a stronger corrective rebound first, before staging another decline.

In Europe, at the time of writing, FTSE is up 0.54%. DAX is flat. CAC is up 0.08%. Germany 10-year yield is up 0.001 at 2.924. Earlier in Asia, Nikkei rose 1.80%. Hong Kong HSI rose 0.10%. Singapore Strait Times rose 0.24%. Japan 10-year JGB yield dropped -0.003 to 0.805.

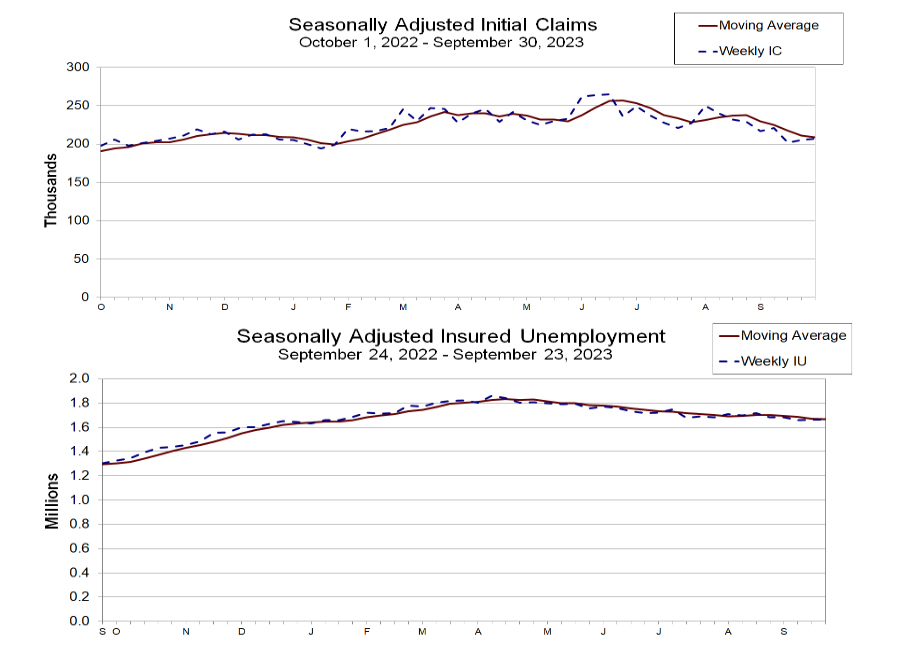

US initial jobless claims rose to 207k, below expectations

US initial jobless claims rose 2k to 207k in the week ending September 30, below expectation of 211k. Four-week moving average of initial claims dropped 2.5k to 209k.

Continuing claims dropped -1k to 1664k in the week ending September 23. Four-week moving average of continuing claims fell -5k to 1668k.

Canada records unexpected trade surplus in Aug as exports surge

Canada reported merchandise trade surplus of CAD 718m in August, marking its first monthly trade surplus since April. This comes after a deficit of CAD 437m in July and defies market expectations of a CAD -1.4B deficit.

Driving this positive turnaround, exports in August jumped by 5.7% mom, marking the most robust growth since October 2021. This surge was widespread, with gains registered in 7 of the 11 product sections.

Meanwhile, imports also witnessed a 3.8% mom uptick, with increments seen in 9 of the 11 product sections.

BoE survey shows business inflation expectations cool

BoE's Decision Maker Panel survey for September indicating an anticipated ease in output price inflation, slowly easing CPI inflation expectation, and subtle nuances in wage growth predictions

A notable takeaway from the survey is the anticipated decline in output price inflation over the next year. Businesses foresee their year-ahead own-price inflation at 4.8%, a slight moderation from the 5.0% noted in the preceding three months to August. This decline hints at an expectation of easing price pressures, offering a counter-narrative to prevalent inflation concerns.

On the consumer front, one-year ahead CPI inflation expectations inched higher to 4.9% in September from 4.8% in August. However, a broader perspective reveals a decline, with the three-month moving average dipping by 0.3 percentage points to 5%. Looking further ahead, three-year CPI inflation expectations held steady at 3.2% in September, unaltered from August.

In the realm of wages, the anticipated year-ahead wage growth was static at 5.1% on a three-month moving average basis. September's single-month reading did register a slight uptick to 5.2%, a 0.2 percentage point increment from August. However, these expectations are notably subdued compared to realised wage growth.

UK PMI construction dives to 45, sharp decline and worst since 2020

UK's construction sector is experiencing a significant setback, as evidenced by the sharp fall in PMI Construction index to 45.0 in September, a level not seen since May 2020 and far below the anticipated 49.9.

The report shows a distinct contraction in the industry, with residential work plunging to an index of 38.1, indicating the steepest decline amongst all sectors. Civil engineering activity isn't faring much better, posting a 45.7 index, while commercial building has shown some resilience, albeit still in the contraction zone at 47.7.

Tim Moore, Economics Director at S&P Global Market Intelligence, paints a grim picture of the current state of the sector. "Output levels declined across the UK construction sector for the first time in three months during September, and the latest downturn marked the worst overall performance since the early stages of the pandemic," he stated.

The future outlook for the construction sector does not instill confidence. Moore points out that the survey's forward-looking measures have remained somewhat pessimistic. "Order books decreased at an accelerated pace and business activity expectations eased to the lowest so far this year," Moore explained. The decrease in project starts has led to an increase in sub-contractor availability, reaching levels not seen since the summer of 2009.

ECB's Kazimir strongly believe that latest hike was last

ECB Governing Council member Peter Kazimir said today, "I strongly believe that our rate hike at the last meeting was the last one" The focus, he outlined, now shifts to the upcoming December and March forecasts, as "only real data can persuade us that we're at the peak."

Kazimir addressed inflation concerns, observing that, "We see the overall inflation and also core inflation on a downward trend, though this is lasting a bit longer than we'd wanted." He further highlighted the ripple effects of past rate hikes, pointing out that they "have an increasingly significant impact on the real economy."

Shedding light on the broader economic repercussions, he mentioned that "Financing conditions are tightening and are weakening demand for investments, in production and affecting overall economic growth." With this context, Kazimir emphasized the urgency to manage inflation effectively and swiftly.

On the topic of ECB's PPEP reinvestments, Kazimir treaded cautiously, suggesting the bank was "ready for debate" but reiterated the importance of maintaining balance. The topic of altering the balance sheet's reduction pace will be broached only when the Council is confident further rate hikes won't be necessary.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2056; (P) 1.2116; (R1) 1.2196; More...

GBP/USD is staying in consolidation above 1.2036 and intraday bias remains neutral for the moment. Outlook will stay bearish as long as 1.2270 resistance holds. Break of 1.2026 will resume the fall from 1.3141. Sustained trading below 1.2075 fibonacci level would carry larger bearish implication, and target 1.1801 support next. On the upside, firm break of 1.2270 resistance will indicate short term bottoming, and turn bias back to the upside.

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2486) holds, in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Trade Balance (AUD) Aug | 9.64B | 8.61B | 8.04B | 7.32B |

| 06:00 | EUR | Germany Trade Balance (EUR) Aug | 16.6B | 14.3B | 15.9B | 16.0B |

| 06:45 | EUR | France Industrial Output M/M Aug | -0.30% | -0.40% | 0.80% | 0.50% |

| 08:30 | GBP | Construction PMI Sep | 45 | 49.9 | 50.8 | |

| 11:30 | USD | Challenger Job Cuts Y/Y Sep | 58.20% | 266.90% | ||

| 12:30 | USD | Initial Jobless Claims (Sep 29) | 207K | 211K | 204K | |

| 12:30 | USD | Trade Balance (USD) Aug | -58.3B | -65.1B | -65.0B | -64.7B |

| 12:30 | CAD | Trade Balance (CAD) Aug | 0.7B | -1.4B | -1.0B | -0.4B |

| 14:00 | CAD | Ivey PMI Sep | 50.8 | 53.5 | ||

| 14:30 | USD | Natural Gas Storage | 97B | 90B |

US initial jobless claims rose to 207k, below expectations

US initial jobless claims rose 2k to 207k in the week ending September 30, below expectation of 211k. Four-week moving average of initial claims dropped 2.5k to 209k.

Continuing claims dropped -1k to 1664k in the week ending September 23. Four-week moving average of continuing claims fell -5k to 1668k.

Canada records unexpected trade surplus in Aug as exports surge

Canada reported merchandise trade surplus of CAD 718m in August, marking its first monthly trade surplus since April. This comes after a deficit of CAD 437m in July and defies market expectations of a CAD -1.4B deficit.

Driving this positive turnaround, exports in August jumped by 5.7% mom, marking the most robust growth since October 2021. This surge was widespread, with gains registered in 7 of the 11 product sections.

Meanwhile, imports also witnessed a 3.8% mom uptick, with increments seen in 9 of the 11 product sections.

Full Canada trade release here.

Gold: Bears Pausing ahead of US NFP Report

Gold price turned sideways and holding within a narrow range for the second straight day, consolidating after seven-day steep fall.

Larger bears slowed pace ahead of key release of this week – US non-farm payroll report for September- which is expected to generate fresh direction signal.

Gold was deflated by strong dollar on expectations that the Fed would keep high interest rates for longer period, but the latest economic data raised a question mark above signals that the economy is resilient despite strong negative impact from high borrowing cost.

Reports from US labor sector were so far mixed as job openings rose above forecast but hiring in private sector slowed well below expectations.

Focus turns towards the more comprehensive non-farm payrolls report, which will provide more details about conditions in labor sector and generate clearer direction signals.

Firmly bearish daily studies are also deeply oversold and point to a pause in recent steep downtrend, which found temporary footstep at 200WMA ($1814).

Consolidation was so far narrow, with initial direction signals expected on break of $1862 (falling10DMA) at the upside, or dip below $1814/04 (200WMA / Feb 28 trough) on the downside.

Res: 1830; 1848; 1862; 1885.

Sup: 1814; 1804; 1793; 1765.