Sample Category Title

Week Ahead – US Inflation and Earnings, Central Banker Appearances in Abundance

US

This week will deliver a make-or-break moment for Fed rate hike expectations. The main event will be the September inflation report. Expectations are for both headline and core inflation to post 0.3% month-over-month gains in September, while headline year-over-year inflation will drop a tick to 3.6% and core’s annual reading will ease from 4.3% to 4.1%. In September, gas prices were relatively stable, car prices rose, and some core services were sticky.

Before Wall Street locks in on Thursday’s CPI release and weekly jobless claims, traders will pay close attention to the PPI release on Wednesday. On Friday, the University of Michigan sentiment report will closely be watched, with the focus falling on near-term inflation expectations. Last month, consumers saw prices rising 3.2% over the next 12 months, which was the lowest level since 2021.

Clarity is expected as to who will be the frontrunner to become the speaker of the House, which will play a critical role in avoiding a government shutdown come mid-November.

The banks kickoff earnings on Friday and it seems many are expecting the financials to highlight a much weaker consumer given surging delinquencies and exhausted excess savings. JPMorgan, Wells Fargo, Blackrock, and Citigroup report earnings before the NY open.

Fed officials will be making 14 appearances throughout the week. Bostic and Collins speak after the inflation report and Harker makes the lone Friday appearance.

Eurozone

A pretty quiet week for the euro area, with an appearance from ECB President Christine Lagarde probably among the few highlights. The ECB minutes release on Thursday is probably the key event of the week considering how debated the dovish hike likely was. The message was clear though but it will be interesting to see how united the committee was.

UK

The focus next week will be the array of BoE appearances which come at a time of great uncertainty for central banks, most notably in the UK. The MPC surprised markets last month with a decision to leave interest rates unchanged – just – and a lot of the language around it was more neutral than would have been expected under those circumstances. We can sometimes read too much into these things so it will be interesting to hear what the thoughts of the various policymakers are. We also have GDP figures on Thursday.

Russia

Inflation data on Wednesday is the standout release next week and once more, it’s expected to rise, this time to 5.8%. Pressure will mount on the central bank to keep raising rates with inflation increasing at this rate and the rouble still sitting near its 18-month lows.

South Africa

A couple of economic releases are on the agenda next week but both are tier two or three and therefore unlikely to be game-changing.

Turkey

Another quiet week but there are a couple of releases worth noting, with unemployment and industrial production figures due on Tuesday.

Switzerland

Next week offers very little with the only release being PPI on Friday.

China

Financial markets in China will be back in action after the Golden Week holiday. On Wednesday, M2 money supply, new yuan loans, and vehicle sales data for September will be released.

The key consumer and producer prices inflation data for September will be out on Friday where the consensus is expecting a tick higher to 0.2% y/y from 0.1% in August. That would be the second consecutive month of y/y growth in consumer prices.

A similar consensus for the PPI where its negative growth is expected to shrink slightly to -2.4% y/y from -3% in August. That would be the third consecutive month of deceleration in producer deflation.

The balance of trade data for September will be released on Friday as well; the trade surplus is expected to expand slightly to US$70 billion from $68.36 billion. The consensus for export growth is almost unchanged at -8.3% y/y versus -8.8% in August, while import growth is expected to contract at a lesser magnitude of -6% y/y from -7.3% in August.

India

Industrial production data for August is released on Thursday and it is expected to rise to 9.3% y/y from 5.7% in August. The inflation rate for September out on the same day is expected to inch lower to 5.45% y/y from 6.83%. That would be the second consecutive month of contraction from July print of 7.44%, the highest level since April 2022.

On Friday, we will have the balance of trade data for September where the deficit is forecasted to shrink to $23 billion from $24.2 billion.

Australia

Consumer and business confidence data will be released on Tuesday and the Westpac consumer confidence is expected to improve to -0.7% m/m from -1.5% .in September.

The NAB business confidence for September is expected to fall to -2 from 2 in August.

New Zealand

Two key data to focus on; food inflation for September on Thursday which is expected to dip to 7.5% y/y from 8.9%. That would be the third consecutive month of growth deceleration in food prices.

The manufacturing PMI for September will be released on Friday and a contraction reading is forecasted at 46.9, almost unchanged from August’s 46.1.

Japan

On Tuesday, we will get the current account data which is expected to show a further surplus of JPY 3.091 trillion from JPY 2.772 trillion.

Banking lending & PPI data for September will be released on Wednesday. Bank lending is forecasted to dip to 2.4%y/y from 3.1% in August. That would be the lowest growth rate since September 2022. PPI is expected to decelerate further in September to 2.3% y/y from 3.2% in August.

Singapore

Two key events to watch on Friday. Firstly, the advance estimate for Q3 GDP growth, the consensus is expecting a lackluster growth rate of 0.4% y/y from 0.7% in Q2. That would be the third consecutive quarter of y/y growth below 1%. The risk of a recession has increased for next year.

On the same day, the Monetary Authority of Singapore (MAS) will release its semi-annual monetary policy statement; it is expected that the MAS will likely maintain the prevailing rate of appreciation of the S$NEER policy band as inflation pressures have started to cool in the past three months while the external demand environment has remained weak.

Economic Calendar

Saturday, Oct. 7

Economic Data

- China forex reserves

Sunday, Oct. 8

Economic Events

- UK Labour Party conference in Liverpool through Wednesday

- German regional elections in Bavaria and Hesse

- National Association for Business Economics conference in Dallas, through Tuesday

Monday, Oct. 9

Economic Data/Events

- US Markets closed for Colombus Day and Canada observes Thanksgiving

- China aggregate financing, money supply, new yuan loans

- Germany industrial production

- Mexico CPI

- Singapore GDP

- Public holidays in Japan, South Korea and Taiwan

- World Bank-IMF annual meetings begin

- French President Macron is expected to discuss AI with German Chancellor Scholz

- LME Week, annual gathering of the global metals community in London

- Fed’s Barr speaks at the American Bankers Association annual convention in Nashville

- Fed’s Logan speaks at National Association of Business Economics annual meeting in Dallas

- Fed Governor Jefferson speaks at NABE conference

- BOE’s Mann speaks at NABE conference

- ECB’s Centeno and Brazilian central bank President Neto speak in Lisbon

Tuesday, Oct. 10

Economic Data/Events

- US wholesale inventories

- Australia Westpac consumer confidence

- Chile copper exports, trade

- Italy industrial production

- Japan balance of payments

- Mexico international reserves

- New Zealand home sales

- Turkey industrial production

- Earnings results from PepsiCo

- BOE releases minutes of financial policy meeting

- The IMF issues its latest world economic outlook

- Fed’s Bostic participates in a moderated conversation at ABA convention in Nashville

- Fed’s Waller speaks at monetary policy conference hosted by George Mason University

- Fed’s Kashkari in a town hall event at Minot State University in North Dakota

- Fed’s Daly speaks at town hall event hosted by the Chicago Council on Global Affairs

Wednesday, Oct. 11

Economic Data/Events

- US FOMC minutes, PPI

- Germany CPI

- Russia CPI

- Taiwan trade

- Turkey current account

- NATO defense ministers meeting in Brussels, through Thursday

- Citi Australia & New Zealand investment conference through Thursday

- US House Republicans plan speaker election

- Fed’s Bowman speaks in Marrakesh during World Bank-IMF meetings in Morocco

- Fed’s Bostic speaks at Metro Atlanta Chambers event

- OPEC members attend Russia Energy Week in Moscow

Thursday, Oct. 12

Economic Data/Events

- US September CPI M/M: 0.3%e v 0.6% prior; Y/Y (headline): 3.6%e v 3.7% prior; Core M/M: 0.3%e v 0.3% prior; Y/Y: 4.1%e v 4.3% prior, initial jobless claims

- India industrial production, CPI

- Japan machinery orders, PPI

- Mexico industrial production

- New Zealand food prices

- South Africa manufacturing production

- UK industrial production

- ECB Minutes to the September policy meeting

- Fed’s Bostic speaks at the National Agriculture Conference at Atlanta Fed

- BOJ’s Noguchi speaks in Niigata

- BOE’s Pill speaks at the Marrakesh Economic Festival

Friday, Oct. 13

Economic Data/Events

- US University of Michigan consumer sentiment

- Canada existing home sales

- China CPI, PPI, trade

- Eurozone industrial production

- France CPI

- India trade

- Japan M2 money stock

- New Zealand manufacturing PMI

- Poland CPI

- Spain CPI

- Financial earnings from Citigroup, JPMorgan, Wells Fargo, and BlackRock

- G20 finance ministers and central bankers meet as part of IMF gathering

- ECB President Lagarde speaks on an IMF panel with IMF Managing Director Georgieva and WTO Director-General Okonjo-Iweala

- Fed’s Harker speaks at a virtual event with the Delaware State Chamber of Commerce

- BOE’s Bailey and Cunliffe speak at the Institute of International Finance meeting in Marrakesh

Sovereign Rating Updates

- Czech Republic (S&P)

- European Union (Moody’s)

- Saudi Arabia (Moody’s)

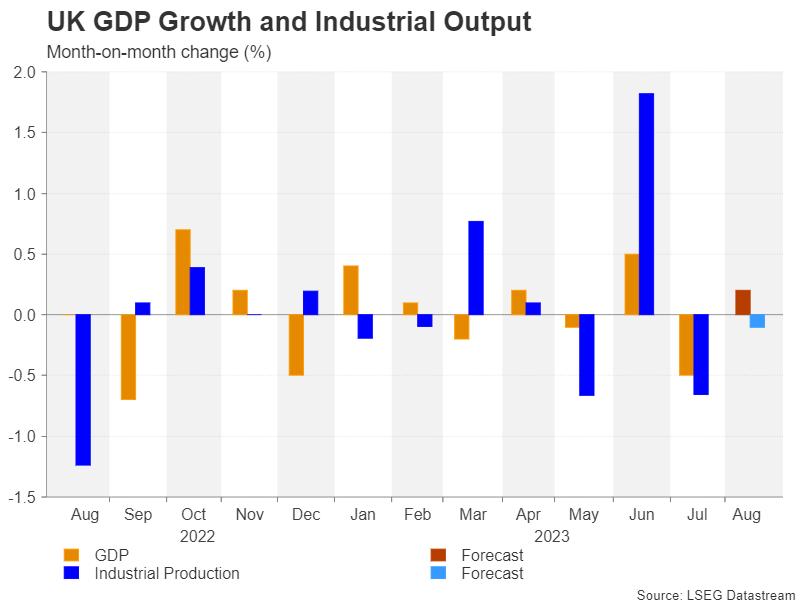

Will the Drumbeat of Bleak UK Economic Data Continue?

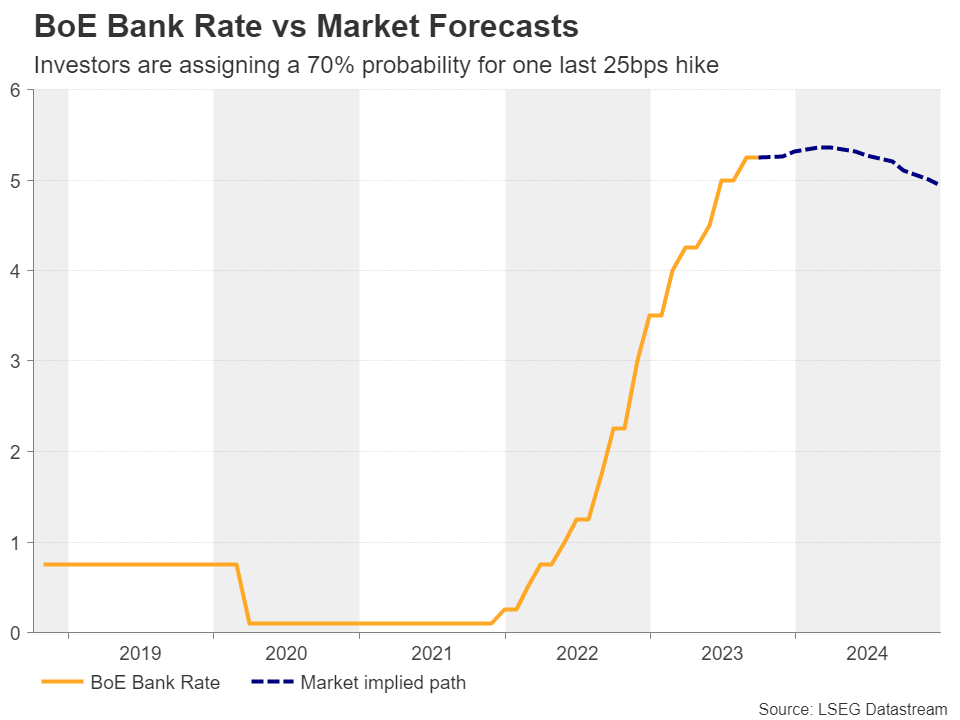

- BoE keeps rates unchanged, citing slowing UK economic activity

- Data since then corroborate the gloomy picture

- Upcoming indicators include monthly GDP and industrial production

- Will the pound weaken after they come out on Thursday at 06:00 GMT?

UK business surveys ring the recession alarm bells

At its latest gathering on September 21, the Bank of England decided to keep rates steady at 5.25%, citing slowing economic activity and a cooling labor market. Although officials accelerated the pace of their quantitative tightening program, the disappointment on interest rates resulted in a selloff in the British pound.

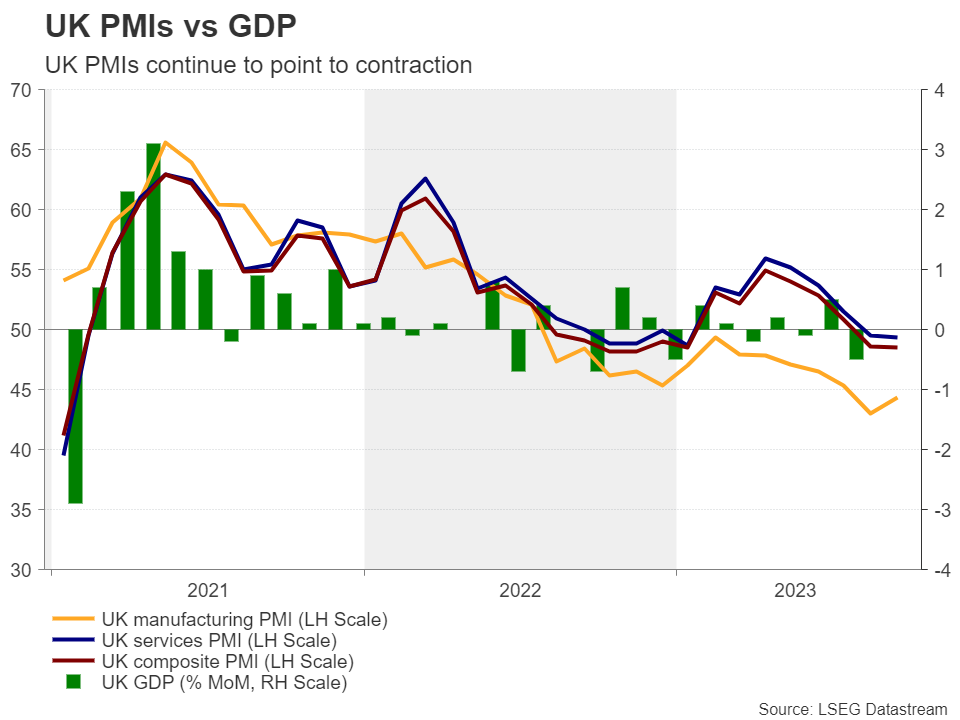

Data since then continued to paint a gloomy picture, with retail sales for August still down on yearly terms and the September PMIs still ringing recession alarm bells. Although the y/y rate of retail sales rose to -1.4% from -3.1%, a negative figure at a time when inflation is cooler than a year ago suggests that consumers continue to struggle. As for the PMIs, although the final releases revealed decent upward revisions from the very disappointing preliminary prints, all the indices remained below the boom-or-bust zone of 50, with the composite index ticking down to 48.5 from 48.6.

With inflation in the UK coming down faster than expected, the bleak economic outlook and the cautious approach by the BoE have prompted investors to scale back their bets regarding future hikes. Currently, they are assigning a nearly 72% probability for the BoE to stay sidelined at the November 2 gathering, with the remaining 28% pointing to one last 25bps hike. They believe that a final hike is more likely to happen after the turn of the year, with a 70% probability assigned to the March decision. However, this could well change if data continues to come on the soft side.

UK monthly GDP and industrial production are next

On Thursday, the UK releases more growth-related data. The monthly GDP for August is due out, accompanied by the industrial and manufacturing production rates, as well as the trade balance for the month. Although the PMIs are already providing a glimpse of how the economy has performed in September, disappointing results on Thursday could raise concerns that activity in Q3 has been softer than previously thought. Following the 0.5% m/m GDP contraction in July, expectations for August are for a modest 0.2% expansion.

With elevated wage growth being the only data point corroborating more interest rate increases by the BoE, a concerning picture painted by other indicators could force investors to further scale back their hike bets and start considering more rate cuts by the end of next year. Currently, the market’s implied path suggests that interest rates are likely to end 2024 at around 5%, 25bps below current levels.

Pound could stay on the back foot

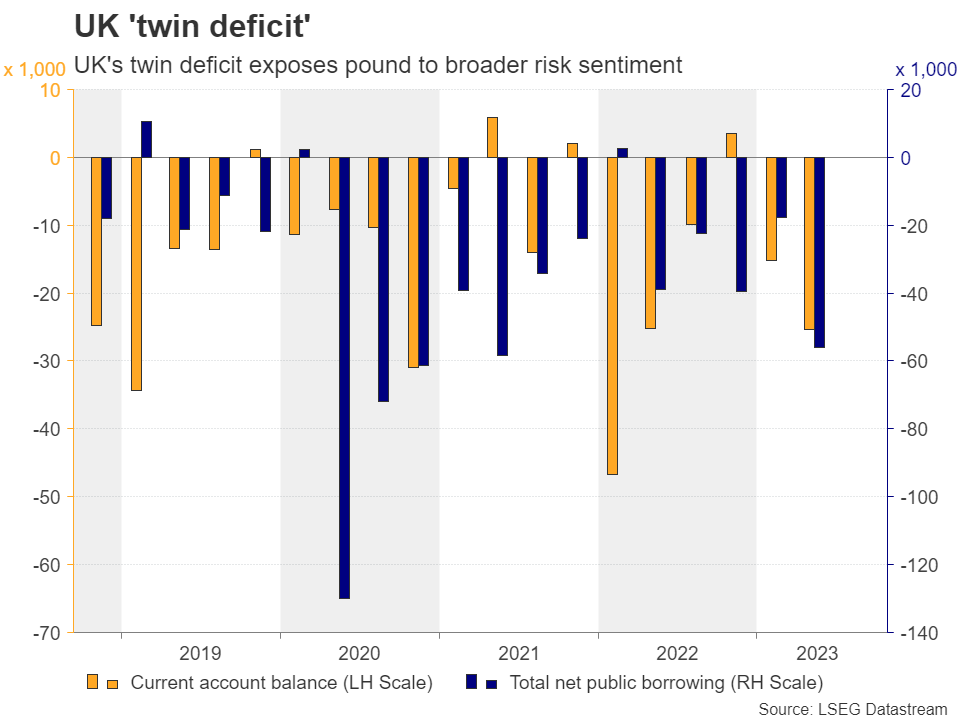

Ergo, the risks surrounding the British pound are likely to remain tilted to the downside, and pound/dollar may be the best proxy to exploit further sterling losses, as the dollar has been receiving support recently from the Fed’s ‘higher for longer’ narrative, but also from concerns surrounding the economic performance of other major economies, like China and the Eurozone. The pound is also affected by the broader market sentiment and in addition by the UK’s twin deficit, which has notably widened in Q2.

Cable has been in a recovery mode since Wednesday, when it hit support around 30 pips above the round number of 1.2000. However, it continues to trade below the key territory of 1.2310, the downside break of which likely confirmed a bearish trend reversal on the daily chart. As long as the pair remains below that zone and below the downtrend line drawn from the high of July 14, there are decent chances for the bears to take charge again and drive the battle back down to, or even below, the psychological zone of 1.2000.

Even if pound/dollar climbs above 1.2310, the chart would still be far from suggesting a positive outlook as the price will only return within the consolidation area that was containing most of the price action between March and September. For the picture to be considered bullish, Cable may need to climb all the way above the 1.2800 zone.

Week Ahead – US Inflation and Fed Minutes to Test Dollar, Bond Markets

- US CPI report and Fed minutes to take centre stage

- Will they fuel or dent the rally in yields and the dollar?

- Chinese inflation and UK growth data to also be eyed

- Otherwise, a quieter week awaits with Monday a holiday in the US

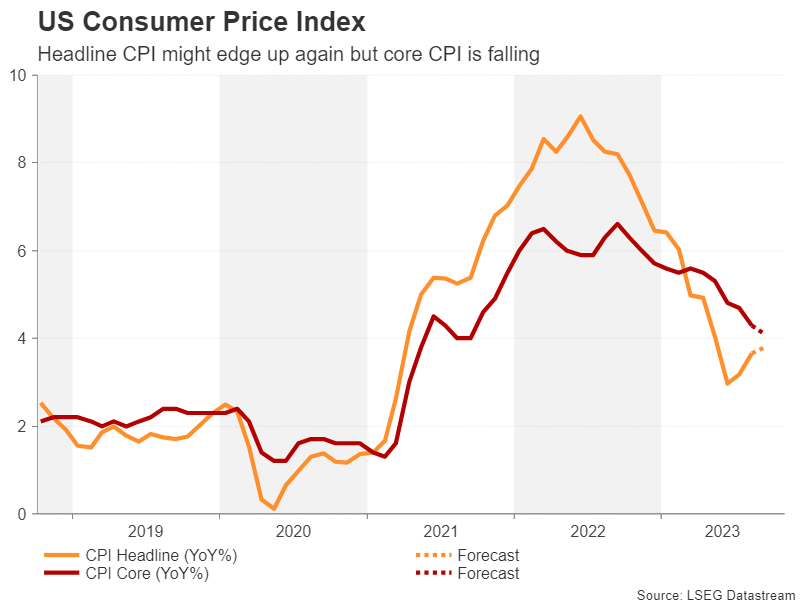

US headline CPI could rise again

As speculation about whether or not the Fed will hike one more time goes into overdrive, the latest report on the US consumer price index will be the big highlight of the week. With the next FOMC decision less than four weeks away, there is a sense of driving blindfolded for both policymakers and traders amid conflicting data on where the economy is headed.

The September CPI report could clear some of the fog away on Thursday, or it may only add to the confusion. Headline CPI edged up in the previous two releases, rising to 3.7% y/y in August. The recent jump in gasoline prices was the main contributor to the increase and the month-on-month gain in CPI accelerated to 0.6% in August.

Forecasts point to a slight moderation in September to 0.3% m/m, but the annual figure is expected to have ticked up further to 3.8%.

Markets might well interpret this as a sign the effects from the energy price spike are beginning to level off, so unless the CPI numbers come in hotter than expected, they’re not likely to react negatively.

However, the core CPI print will also be important, if not more, as it strips out any distortions from food and energy prices. Core CPI has been steadily declining over the past 12 months and is forecast to have eased further to 4.1% y/y in September, potentially adding to the view that inflationary pressures are receding.

Will Fed minutes relay the hawkish tone?

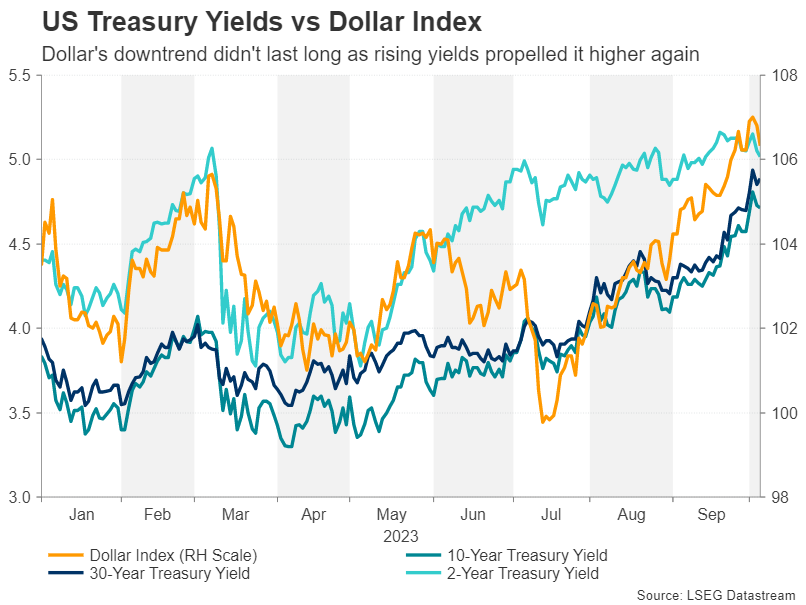

Heading into the CPI report, though, the mood will be determined by the producer price index as well as the minutes of the Fed’s September meeting that are due on Wednesday. The Fed may have kept rates unchanged at the last meeting, but a string of policymakers have since been beating the hawkish drum so loud that Treasury yields have skyrocketed to new cycle highs.

The 10-year yield briefly hit a 16-year peak of 4.88% last Tuesday, turbocharging the US dollar. Investors will likely weigh out concerns in the minutes about a slowing economy against fears of inflation firing up again. If Fed officials are less worried about a slowdown than sticky inflation, yields could climb to fresh highs. However, any boost to yields and the dollar will not be sustainable unless it’s followed up by a hot CPI report.

Finally, the University of Michigan’s preliminary consumer sentiment survey will be watched on Friday, particularly, the readings on inflation expectations.

UK economy: not as bad, but not strong enough

The pound has been hammered lately by a combination of a resurgent US dollar, the Bank of England’s unexpected dovish tilt and a bleaker outlook for the UK economy. In the process, sterling has lost its crown as the year’s best performer in the FX arena.

However, it hasn’t been all doom and gloom on the economy. The Office for National Statistics recently published revisions to its GDP calculations and it is now estimated that the British economy is 1.8% larger than it was before the pandemic compared to the previous estimate of being 0.2% smaller, putting the UK in no worse position than its major European counterparts. In addition, the September services PMI was revised up sharply in the final reading, easing fears about an imminent recession.

Yet, the pound hasn’t been able to stage much of a rebound. This suggests that investors remain downbeat about Britain’s growth potential and that sterling’s main advantage versus the greenback before the BoE’s shock decision to pause was that rates in the UK would peak above those in the US.

Thus, Thursday’s barrage of data on monthly GDP output and production as well as trade are unlikely to have a significant bearing on the pound’s near-term prospects other than a knee-jerk reaction. As long as a soft landing remains the base case scenario for the US economy, there will either have to be a series of upside surprises in UK growth indicators or downside surprises in inflation to shake off the stagflation risks pinning cable down.

Risk assets hoping for China boost

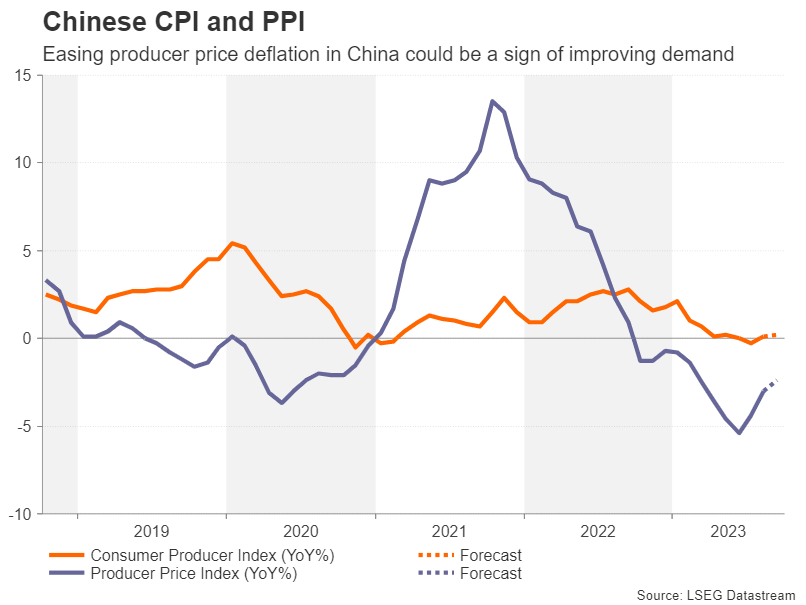

Another hope for those currencies that have been badly bruised by the US dollar is if there’s a turnaround in risk sentiment. In particular, risk-sensitive currencies such as the Australian dollar might be able to pare some of their recent losses if there’s some upbeat data out of China. However, the forecasts suggest otherwise.

Producer prices in China are expected to have fallen by 2.4% y/y in September versus by 3.0% in August, pointing to a mild improvement in demand for goods churning out of Chinese factories. Meanwhile, the yearly CPI rate is projected to have quickened only marginally to 0.2%.

Friday’s releases will also include trade figures, with exports forecast to have dropped 8.3% y/y in September, making it the fifth straight month of decline.

Any promising signs of a rebound in China’s economy from better-than-expected numbers would also aid equities, as well as crude oil prices, which took a tumble in the past week.

Even the euro stands to gain from positive China-related headlines in the absence of any other developments. The European Central Bank is set to publish its account of the September policy meeting on Thursday but it’s doubtful whether it will have much of a market impact.

ECB policymakers have been very active post the meeting, providing plenty of commentary, and the doves appear to have become more vocal lately calling for a pause in rate hikes. It’s likely therefore that even if the minutes maintain a tightening bias, investors will consider them as outdated.

Weekly Focus – Rise in US Yields Not Going to Last

A massive sell-off in bond markets have over the past weeks pushed long US government bond yields to new highs. The 10Y UST yield has risen 60bp over the past couple of weeks, and the current level is now trading at 4.72% - an increase of 100bp since June and close to the highest level since 2007. Market inflation expectations have only risen marginally, which has left real rates significantly higher. And apparently without a clear macro trigger as growth data has generally been in line with expectations, core CPI is still on the downward trajectory and the Fed communication has been very similar to the 'higher for longer' signals presented at the September meeting. So what is going on? A number of factors have likely worked to shift the supply-demand balance in the market. A record high issuance of long-end US bonds has increased the supply of bonds. At the same time demand has been weak due to investor positioning being overweight long bonds, the Fed is doing quantitative tightening (QT) and demand from China and Japan seems to have come down. However, we do not believe the increase is sustainable. It adds to financial tightening and puts downside risks to growth forecasts in 2024, which in turn could lead to earlier Fed cuts. The rise also comes on top of other new headwinds to US private consumption from US student loan payments that resumed on 1 October and the rise in gasoline prices eroding household purchasing power. There is also a risk that new skeletons fall out of the closet due to the sharp rise in yields, as was the case in March with the collapse of Silicon Valley Bank. We thus continue to look for lower yields with US 10Y yield falling to 3.70% on a 12M basis, see also Research - US: Yields not bound to be high for long, 5 October

The Fed has not commented a lot on the latest run-up in yields, but Cleveland Fed President Loretta Mester did say Thursday that officials are watching the rise in yields, while adding that it's not clear the increase would be sustained.

On the economic front there are some signs that the global manufacturing may be at a turning point, at least temporarily. The US ISM index for September showed a rise in the new orders index to 49.2 from 46.8 in August and up from the low of 42.6 in May. Export data out of Asia have also improved lately, normally a sign of a manufacturing inflection point. However, it is likely mostly related to a turn in the inventory cycle, which will only give a temporary lift if underlying demand is not improving and we see downside risks to the latter. While manufacturing looks to improve, the service sector has been weakening. It was also confirmed by a decline in the US ISM service order index to 51.8 in September from 57.5 in August. US labour market data were mixed with the JOLTS job openings showing a renewed increase, while ADP employment disappointed (US non-farm payrolls were released after the deadline of this publication). We haven't had much economic news in the Euro area or China (where it has been Golden Week holiday), but we released the Euro area macro monitor: Data still supporting soft landing, 2 October, which provides an overview of recent developments.

Next week focus will also be on the US with the release of CPI for September. We forecast both headline and core CPI below consensus expectations at +0.2% in m/m SA terms (consensus 0.3%) underpinning the picture of slowing underlying inflation and our forecast that the Fed will stay on hold, not least in light of the latest financial tightening.

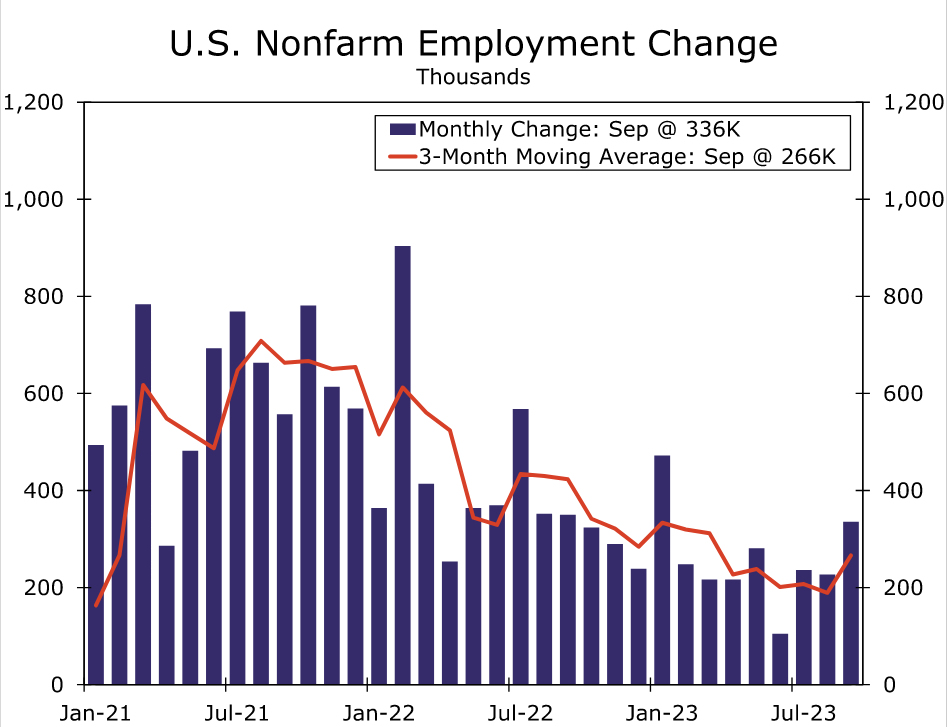

September Employment: Wow

Summary

The September employment was strong across-the-board. Nonfarm payrolls grew at a robust 336K pace in the month, and upward revisions to job growth in July and August further flattered the employment figures. Job growth was driven by both public and private hiring and a diverse set of industries. The labor force continued to grow, helping to restrain wage growth. Average hourly earnings grew just 0.2% for the second month in a row, bringing the year-over-year pace down to 4.2%, the slowest pace in more than two years and about a percentage point above where it was before the pandemic.

Today's report drove yet another increase in Treasury yields and fanned the flames that the FOMC may hike the federal funds rate one more time at one of its two remaining meetings of the year. Another rate hike before the end of the year is a possibility, but for now our base case remains that the last rate hike of the tightening cycle occurred in July. Next week's CPI report and the Q3 Employment Cost Index to be released on October 31 will help the FOMC determine if progress is continuing in its inflation fight despite the surprising strength in employment gains in recent months.

Jobs Market Still Flying High

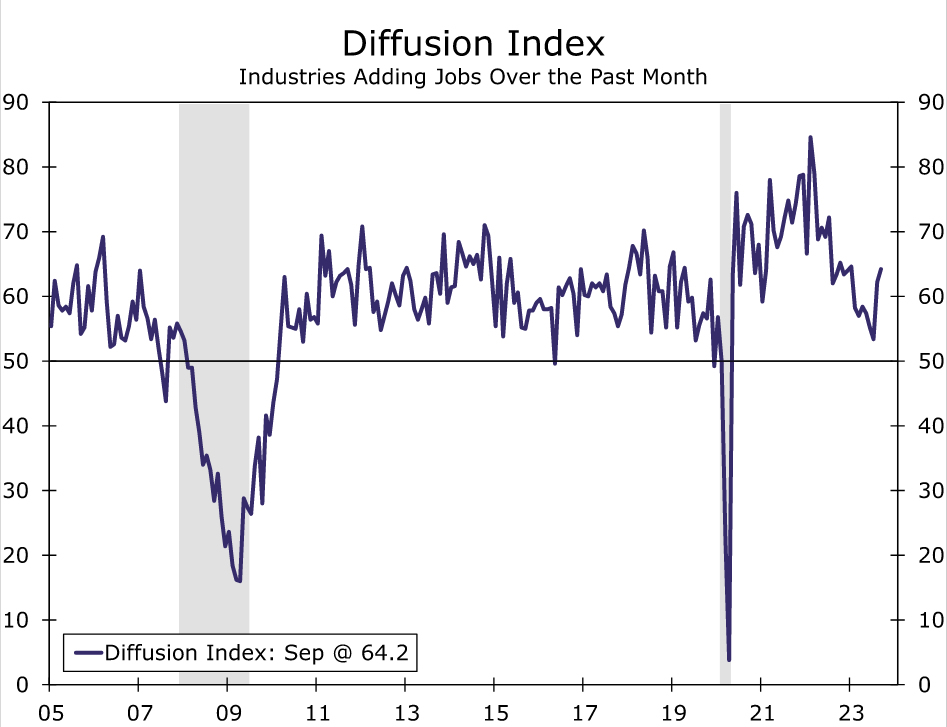

U.S. job growth blew past expectations in September, rising by 336K compared to consensus expectations for a 170K gain. Revisions to the previous two months increased employment by an additional 119K. Not only was aggregate job growth impressively strong, but employment gains were broad-based across most industries. The employment diffusion index, a measure of hiring breadth across industries, jumped to 64.2, the highest reading since January. Leading the charge were leisure & hospitality (+96K) and government (+73K), two industries where payrolls are quickly closing in on their pre-COVID levels. Health care (+41K), professional, scientific & technical services (+29K) and manufacturing (+17K) also posted notable gains.

Despite all the headlines about strikes in recent weeks, labor disputes had little bearing on the change in nonfarm payrolls in September. The UAW walkouts and Hollywood writers' deal both occurred too late in the month to be reflected, although the net conclusion of a handful of smaller strikes gave a small (~4K) boost to payrolls.

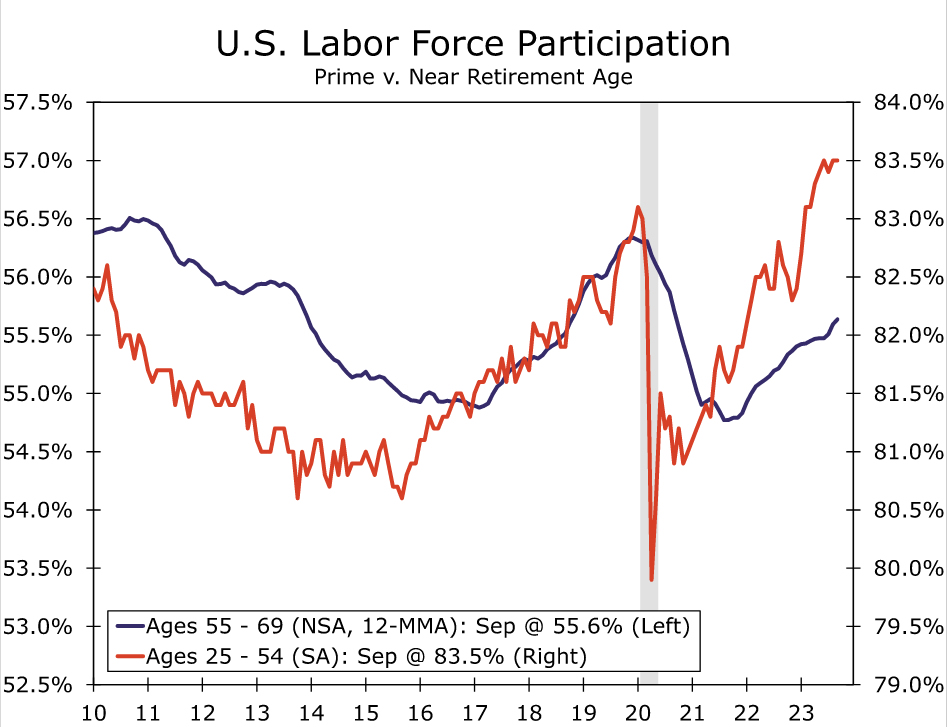

A marked increase in labor supply over the past year has helped to support overall hiring. An additional 90K workers entered the labor force in September on the heels of what was already a major swell in August. The labor force participation rate was unchanged at 62.8%, continuing its now 11-month streak of avoiding a decline despite the headwinds caused by an aging population. Prime-age women have led the charge, although men ages 25-54 have also seen participation rebound strongly. Participation among older workers also has edged higher over the past year (chart). We see scope for labor force growth to remain solid in the near-term as the still-strong jobs market pulls in workers and deteriorating finances give other workers a push. September's moderate rise in the labor force roughly matched the increase in the household survey's measure of employment (86K). As a result, the unemployment rate was unchanged at 3.8%.

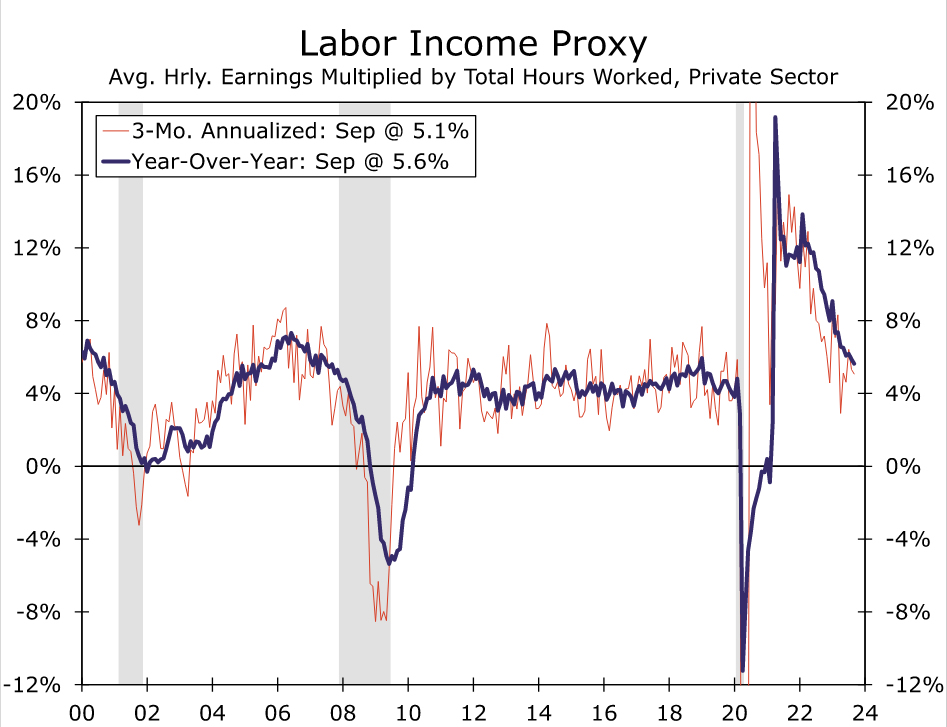

The more abundant supply of workers along with a less frenzied pace of hiring is helping to dampen wage pressures. Average hourly earnings came in a touch softer than expected, up 0.2% in September. On a year-ago basis, average hourly earnings have risen 4.2%—the slowest pace in more than two years—while the 3.4% annualized growth in AHE the past three months suggests a further drop in the year-over-year number is coming. While labor cost growth still needs to subside somewhat further to be consistent with 2% inflation over time, the moderation is a welcome step in the right direction for the inflation-fighting Fed. While the typical worker may be experiencing a slower pace of wage growth, the still-solid rate of hiring suggests growth in aggregate income derived from the labor market continues on at a decent clip, which should support overall consumer spending (chart).

After Employment, FOMC Watching CPI, ECI Closely

Today's resoundingly strong employment report will likely keep the FOMC on guard as it watches for signs that a tight labor market could prevent inflation from returning to 2% on a sustained basis. Another rate hike before the end of the year is a possibility, but for now our base case remains that the last rate hike of the tightening cycle occurred in July. Core inflation continues to grind lower, and we expect another relatively tame reading in next week's CPI report. In addition, robust labor supply growth has helped restrain labor cost growth, as indicated by the softness in average hourly earnings. The earnings data from the employment report are a somewhat crude measure of wages, so the Employment Cost Index (ECI) to be released on October 31 will be critical to confirming that labor costs are indeed decelerating. If the CPI and ECI data cooperate, we would expect the FOMC to remain on hold at its upcoming November 1 meeting.

USD/JPY: Hot NFP Report Sends Dollar Higher after US Economy Has Best Job Growth Since January

- US jobs gains broadest since January; 336,000 created vs 170,000 eyed

- Wages unexpectedly came in cooler than expected; holding steady with a 0.2% monthly pace and on annual basis down from 4.3% to 4.2%.

- Dollar surges across the board with the exception to the Canadian dollar (Canada posted a robust 63,800 job gain themselves, tripling their consensus estimate).

The US economy is not ready to break. The September jobs report shocked Wall Street as 336,000 jobs were created, a strong enough of a number that could force the Fed to move again in November. This is a hot report as the headline job gains nearly doubled the consensus estimate and as the prior reading was revised 40,000 higher. This will be a peak for hiring as the job gains occurred in leisure and hospitality; government; health care; professional, scientific, and technical services; and social assistance.

Wages were slightly soft, but that is getting overlooked this time as 455,000 jobs were created when you include the two-month revision of 119,000.

Market reaction.

US stocks plunged after a hot jobs report sent Treasury yields soaring. Good news about the economy means corporate America is going to have to deal with higher interest rates for the rest of this year and probably most of 2024. Interest rate sensitive stocks and small companies are not going to do well with this current macro backdrop.

King dollar returned after job hiring hit the best pace since the start of the year. The Fed might get the all-clear signal to deliver one last rate hike if the October 12th CPI report shows disinflation struggles. Treasury yields are surging and higher-for-longer just got higher and longer. The spread between 2- and 10-year Treasury yield resteepened to the smallest inversion of the year. The yield curve isn’t quite ready to turn positive, but it sure is heading in the right direction.

Even if the Fed doesn’t deliver one more rate hike, the movement with Treasury yields will do the Fed’s tightening work for them. Yesterday, Fed’s Daly noted that with the rise in yields, the need to do additional tightening is not there. Today’s movement in yields bolsters her argument.

USD/JPY (euro) 15 minute chart

Labor Disruptions

The Kaiser Permanente workers entered a third day of strikes. The largest healthcare strike in history saw 75,000 workers walk off the job. The workers are demanding higher pay and additional benefits, which includes a 4-day work week.

United Auto Workers President Shawn Fain is expected to announce at 2pm if current negotiations have made enough progress that they won’t have to expand their strike. The gap was narrowed as it seems a 20% pay increase along with cost-of-living adjustments will get the automakers closer to the 30% wage gain sought over the life of the contract.

Once these strikes are over, wages will go up and undoubtedly other unions will seek to take advantage of the peak of this current economic cycle.

Sunset Market Commentary

Markets:

Today’s US payrolls had to decide whether markets recently discounted enough tightening. Markets took a ‘mild’, indecisive bias going into the release with Treasuries tentatively in the defensive while major European equities added modest gains. The dollar ceded few ticks. This week’s ADP at least again wasn’t a good pointer. The US economy in September added 336k jobs! In addition, data for the previous two months were upwardly revised by 119k. The goods producing sectors added 29K jobs. Services sector employment grew 234k with health services adding 66k and leisure and hospitality up 96K. The government sector also hired a net 73k of new employees. Other data subseries were less spectacular. Average hourly earnings printed at a modest 0.2% M/M (was 0.3% in August) and 4.2% Y/Y, marginally lower than expected. The unemployment rate, derived from another statistical basis (Hhousehold survey) stabilized at 3.8%. According to this series both employment (86k) and the labour force (90k) grew modestly and far less than in previous month. Despite this ‘statical noise’, after a brief hesitation, bonds couldn’t but resume the sell-off. No smooth sailing going into the Columbus Day long weekend. In volatile trading, US yields currently add between 8 bps (-2-y) and 13 bps (10-y). Yields across the US curve neared (< 7-y) or touched (>10-y) new cycle peak levels (30-y +5%, 10-y touched 4.88%), but it’s unsure whether these peak levels will hold into the close. Markets raised the chance of an additional Fed rate hike later this year to 50%. This is still rather modest given recent Fed talk mostly supporting the 25 bps additional step guided in the dots. Maybe investors ponder whether soft wage growth still gives the Fed some room to wait-and see. Anyway, the countdown to next Thursday’s US September CPI has started. German Bunds feel some collateral damage with yields in a steepening move rising between 1.5 bps (2-y) and 5 bps (30-y). European equity markets briefly reversed earlier gains upon the release, but the EuroStoxx 50 currently again trades about 0.5% in green. US indices are ceding about 0.6% (S&P 500 & Nasdaq) after the open. Here as well, the damage could have been bigger. Oil stabilized near $84/b.

Higher (real) yields evidently favour the dollar. However, gains for now aren’t excessive. Recent peak levels in the likes of the DXY (106.67 VS 107.34 top on Wednesday) still are some distance away. EUR/USD dropped from 1.0560 to currently test the 1.05 barrier. USD/JPY is changing hands near 149.5. So, the BoJ again should be on alert if it wants to defend the 150 barrier. Sterling (EUR/GBP) is hardly affected by the broader move with the pair holding tight near the 0.855 pivot.

News & Views:

Canadian September payrolls beat consensus as well. The economy added 63.8k jobs (vs 20k) expected) with details showing both increases in part time (47.9k) and full time (15.8k) occupations. The upward trend in employment continues to occur in the context of the highest population growth since 1957. The employment rate—the proportion of the population aged 15 years and older who are employed— rose 0.1 percentage points to 62.0%. The unemployment rate stabilized at 5.5% even as the participation rate ticked up from 65.5% to 65.6%. The hourly wage rate for permanent employees unexpectedly accelerated from 5.2% Y/Y to 5.3% Y/Y. The Canadian loonie manages to set its foot against a strong dollar with USD/CAD even dipping back below 1.37. Canadian swap rates rise by 6 to 7 bps across the curve with the market implied probability of another rate hike by the Bank of Canada before year-end rising from 50% to 75%.

Czech August retail sales disappointing falling by 0.8% M/M and 2.8% Y/Y (from -2.1% Y/Y in July). Real consumption of (cheaper) food is gradually picking up while consumers remain cautious on spending at big ticket items. We downwardly revise our Q3 GDP forecast to -0.1% Q/Q with 2023 and 2024 projections now at -0.3% (from -0.1%) and 2.4% (from 2.6%). The Czech National Bank today also published Minutes of the September policy meeting which showed that at least 3 policymakers (out of 7) believe that a first policy rate cut will occur this year. Our base scenario remains for unchanged rates in November and a 50 bps rate cut in December. The Czech koruna holds firm today (EUR/CZK 24.45) despite the soft data/minutes and the new rise in global core interest rates.

USD/CAD Unchanged as Canada, US Post Strong Job Numbers

- Canada records 63,800 jobs in September

- US nonfarm payrolls posts a massive gain of 336,000

- Fed rate odds of a November hike rise sharply

The Canadian dollar is showing limited movement on Friday. In the North American session, USD/CAD is trading at 1.3705, almost unchanged. USD/CAD gained ground immediately after the nonfarm payroll report but has given up these gains.

The week ended with better-than-expected job growth in both Canada and the US. Canada’s economy created 63,800 jobs in September, up from 39,900 a month earlier and blowing past the forecast of 20,000. This marked an eight-month high, although the lion’s share of the increase was part-time jobs (47,900). The unemployment rate remained at 5.5%, just below the estimate of 5.6%. Wage growth ticked higher to 5.3%, up from 5.2% but shy of the estimate of 5.5%.

The US nonfarm payroll report was a barn-burner, with an increase of 336,000 in September. This follows an upwardly revised gain of 227,000 in August and crushed the forecast of 170,000. Wage growth remained at 0.2% m/m, below the forecast of 0.3 m/m, and the unemployment rate was unchanged at 3.8%, compared to the forecast of 3.7%.

The strong nonfarm payrolls has raised the odds of a quarter-point hike in November. Prior to the release, the odds of a quarter-point increase were 19%; this has jumped to 29% after the release, according to the CME FedWatch Tool.

The Canadian dollar is under pressure and has declined close to 1% in October. The economy posted negative growth in the second quarter and is in danger of another negative quarter in Q3. The Canadian dollar is also getting squeezed by falling oil prices, as oil is a major export for Canada. Crude oil prices slid about $5 on Wednesday, the biggest daily drop in over a year, and have fallen around 10% in October. Crude is under strong selling pressure over signs that demand is falling and concerns that interest rates will remain “higher for longer”. Today’s massive nonfarm payrolls gain will only exacerbate these concerns..

USD/CAD Technical

- USD/CAD faces resistance at 1.3806 and 1.3864

- 1.3695 and 1.3638 are the next support lines

Payroll Gains Smash Expectations in September, Tilting Odds Heavily in Favor of Another Rate Hike

Non-farm payroll employment rose by 336k in September, well ahead of expectations calling for a gain of 170k. Revisions to the two prior months were also meaningfully higher, adding an additional 119k to the previously reported figures.

- Hiring over the last three-months averaged 266k jobs per-month, well above August's 189k but still below the 334k reported in January.

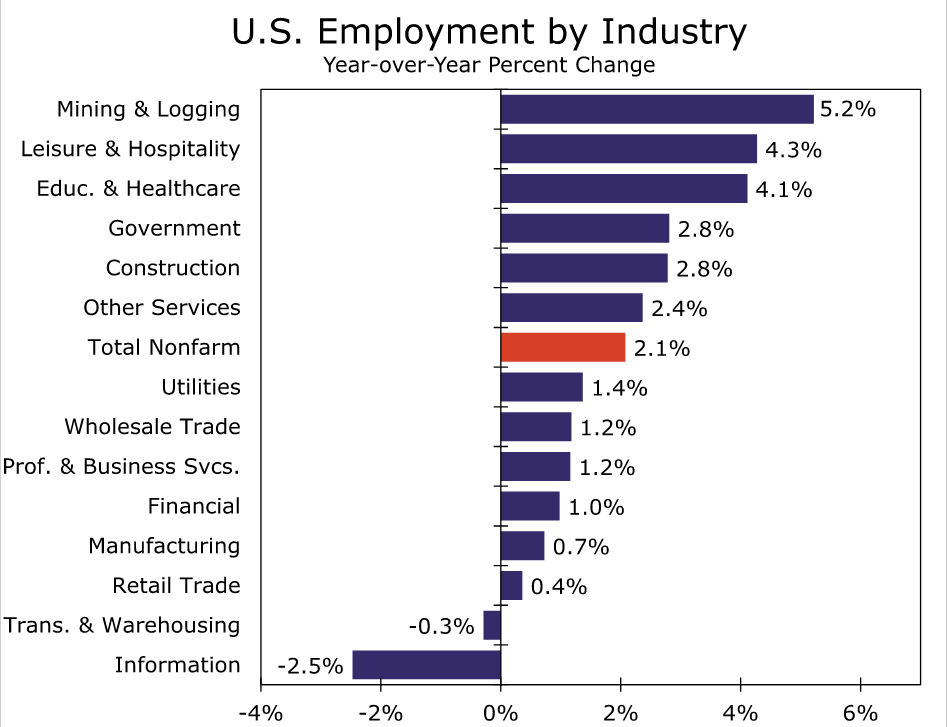

Private payrolls rose 263k – the strongest pace of monthly gains since January. Service-sector gains (+234k) were concentrated in leisure & hospitality (+96k), health care & social assistance (+66k), retail trade (+20k) and professional & business services (+21k). Goods producing industries added 29k jobs last month, with gains spread across construction (+17k), manufacturing (+13k), and mining & logging (+1k). Government also chipped in with a sizeable 73k.

- The breadth of hiring – as captured by the diffusion index widen to 64.2% – which is the highest level since January 2023.

In the household survey, gains in civilian employment (+86k) nearly matched those of the labor force (+90k), which resulted in the unemployment rate holding steady at 3.8%. The participation rate also held steady at its cyclical high of 62.8%.

Average hourly earnings were up 0.2% month-on-month (m/m) – matching August's gain. The twelve-month change inched a tick lower to 4.2%, while the truncated three-month annualized change slipped to 3.4% (previously 4.4%).

Key Implications

Job growth was considerably stronger than expected in September, expanding by the fastest pace since January. Sizeable revisions to the prior months also contributed to an abrupt U-turn in what had previously looked like a steady downward trend in the pace of hiring. While wage growth came in under expectations, Fed officials won't be able to look past the fact that labor force growth is slowing at a time when job openings remain elevated, which if left unchecked, will likely pressure wages higher over the coming months.

This morning's employment report provided another shot in the arm to Treasury yields, with the 10-year rising to 4.85%. Even with the recent tightening in financial conditions and inflation trending favorably in recent months, this morning's report showed clear evidence that the labor market remains far too hot. At this point, another rate hike in November seems inevitable. And while next week's CPI report will provide another key piece of the puzzle, policymakers are likely to put more weight on today's employment numbers as the continued labor market resilience remains an upside threat to inflation.

Canada’s Labour Market Gains in September

The Canadian labour market added 63.8k positions in September, with full-time employment up 15.8k and part-time employment up 47.9k.

The unemployment rate was unchanged at 5.5% and the participation rate rose 0.1 percentage point to 65.6%.

Employment by sector showed gains in educational services (+66k), and transportation and warehousing (+19k). Job losses were seen in finance, insurance, real estate, rental and leasing (-20k), construction (-18k), and information, culture and recreation (-12k).

Lastly, total hours worked were down 0.2% month-on-month and wages were up 5.0% year-on-year (unchanged compared to August).

Key Implications

The Canadian jobs market has surprised to the upside once again. Today's headline print was double the trend pace over 2023, boosted by Canada's continued population boom (+82k m/m in population) and a surge of workers entering the job market (+72k m/m). While the headline figures will be grabbing most of the attention, we'd caution on getting too excited. Almost all the gains were in the historically volatile Education sector. And when looking at cyclically driven private sector firms, hiring only increased by 1k this month. Furthermore, most of the job gains were in part-time employment, causing the number of hours worked to decline. These details should throw some cold water on a seemingly hot jobs report.

The Bank of Canada has been looking for evidence that past rate hikes are starting to bite. Today's employment report muddies the outlook. Financial markets are cementing pricing for another 25bps rate hike in the coming months, causing the Canada 2-year yield to surge over 15bps this morning. There will be a lot more data coming out between now and the next BoC rate decision (CPI, housing, retail sales) and the Bank will likely need to see significant weakness in these reports to prevent it from pulling the trigger on another hike.