Sample Category Title

Has German Business Climate Bottomed Out?

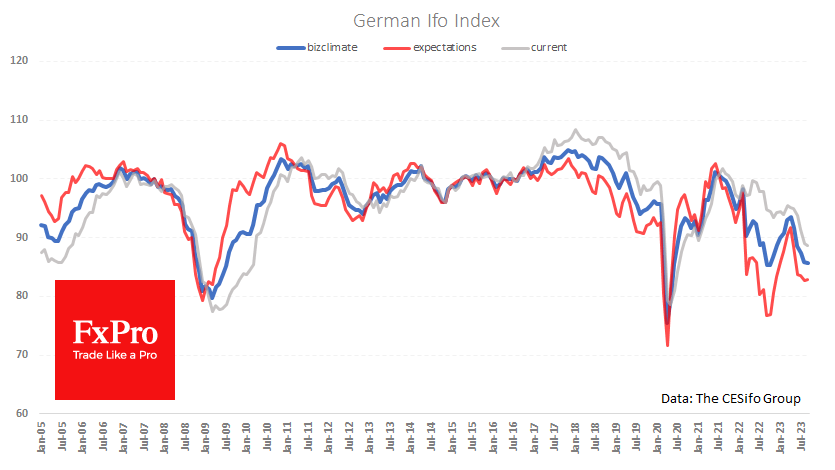

Germany’s Ifo business climate index held steady in September at the previous month’s level despite expectations of further deterioration.

The business climate indicator fell from 85.8 to 85.7, better than the expected 85.1 but still the lowest since mid-2020. Excluding this spike, the only time in modern history that sentiment was worse was in the nine months between November 2008 and July 2009.

The Current Situation Index is trying to find a floor, falling from 89.0 to 88.7. Expectations have slightly improved, with the relevant component rising from 82.7 to 82.9. It may be too early to talk about a turnaround, but previous turning points in this component have coincided with the EURUSD’s turnaround in the following months. From this perspective, it is a reliable leading indicator for the markets.

On previous occasions, however, the expectations index reversed sharply because of monetary easing and fiscal stimulus. This is not the case now, and the improvement in sentiment is in response to a period of low gas prices and slowing inflation. However, neither the issue of reliable gas supplies and energy prices in general nor the slowdown in inflation has been resolved.

Moreover, the ECB raised interest rates less than two weeks ago, in contrast to sharp cuts on previous occasions when business sentiment in Germany and the eurozone was similarly low. A further deterioration in sentiment cannot be ruled out without support from the government and ECB measures. In these circumstances, the scenario of a weaker single currency directly correlated with risk appetite remains a priority.

EUR/USD: Dollar Rallies Alongside Surging Yields

- Fed rate hike expectations for November 1st stand at 18.6% vs 30% from a week ago

- Germany IFO Business climate declines for a fifth straight month

- 10-year Treasury yield surges 7.7bps to 4.511%

The euro softened earlier after an uninspiring German business outlook suggests the eurozone’s largest economy still has a rough road ahead. This was the fifth straight month of declines for Germany’s business confidence. Investors focused on the expectations survey’s slight miss. The IFO economists believe that a third quarter contraction is likely. As long as the ECB is done raising rates, the outlook should gradually improve for Germany.

US dollar strength remains as global bond yields shift higher on fears that central banks will follow the Fed’s lead and keep rates higher over the long-term. It is a slow start to Monday, with one economic release and one Fed speaker, but right now it seems a weaker consumer is steadily getting priced in.

The Chicago Fed National Activity index showed slower growth in August, which didn’t surprise anyone.

Fed’s Goolsbee, one of the more dovish members, noted that the risk of inflation staying too high is the bigger risk. He is still holding onto hopes that a soft landing is possible, but he will likely be data dependent. Inflation flare up risks are growing and that still suggests the Fed might have to do more tightening despite the trajectory of the economy.

Retail/US consumer

Retail stocks, Foot Locker and Urban Outfitters both got downgraded to hold by Jefferies as the consumer is faced with headwinds. Softer spending with apparel and footwear will be driven on the resumption of student loan repayments.

Last week, Bankrate’s survey noted that 40% of Americans feel financially burdened by holiday shopping. Two weeks ago, Deloitte forecasted soft holiday sales.

It is no surprise that the consumer won’t be spending as much this holiday season given excess savings will have disappeared, credit card balances will become crippling with higher rates, and the labor market will be seeing some type of a slowdown.

Sticky inflation which comes with renewed dollar strength risks remain a risk on the table as oil prices appear poised to remain elevated all the way through the winter. Also on the minds of traders is the rising risk of a government shutdown next week.

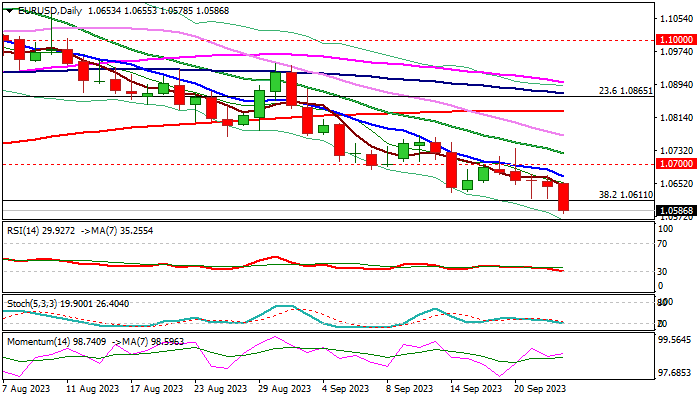

EUR/USD Daily Chart

The dollar remains king but that could show some signs of exhaustion once the euro falls towards the 1.05 handle. As long the global outlook doesn’t fall apart, the dollar should be nearing a peak.

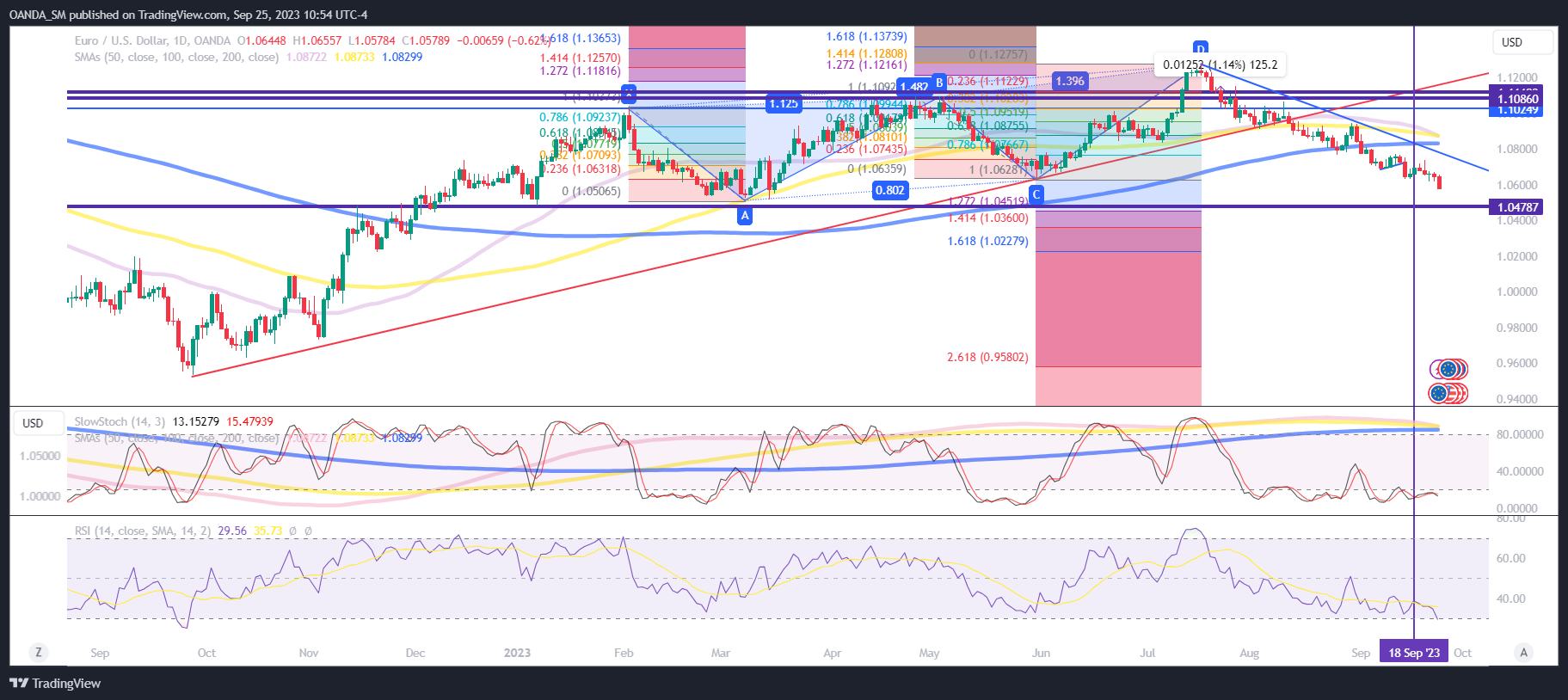

EURUSD Dips to Lowest in Over Six Months on Weak German Data and Firmer Dollar

EURUSD came under renewed pressure in mid-European / early US trading on Monday and broke through pivotal support at 1.0611(Fibo 38.2% of 0.9535/1.1275 rally), after bears were repeatedly rejected last Thu/Fri.

Fresh weakness signals continuation of larger downtrend, which was paused for consolidation in past six days, with bearish signal being generated on break of 1.0611 pivot (confirmation of signal requires daily close below here.

The pair is trading at the lowest in 6 ½ months and bears eye next strong support at 1.0553 (weekly cloud top).

Stronger headwinds could be expected in this zone as ascending weekly cloud is thickening and stochastic and RSI indicators are entering oversold territory on daily chart.

Although bears still firmly hold grip on all timeframes and there are no any signs of reversal so far, some price adjustment should be anticipated in coming sessions.

Upticks are likely to be limited and not to exceed falling 10DMA (1.0670) to keep bears intact.

Penetration of weekly cloud to expose targets at 1.0405 (50% retracement) and 1.0284 (weekly cloud base, in extension).

Res: 1.0611; 1.0642; 1.0670; 1.0700

Sup: 1.0553; 1.0483; 1.0405; 1.0290

Sunset Market Commentary

Markets

New week, same trends. Starting with the core bond sell-off and underperformance of the (very) long end of the curve. Daily yield changes are similar for German Bunds, US Treasuries and UK Gilts: near flat at the front end (2-yr) and up to 10 bps higher at 30-yr tenors. It needs no explanation that we arrive at new cycle tops for example at the US 10-yr yield (4.52%). The German 10-yr yield breaks above the YTD high at 2.77% to trade above 2.8% for the first time since 2011. The German 30-yr yield tests the psychologic 3% mark, a level which is now clearly broken for the EU 30-yr swap rate (3.07%). Higher real rates are firmly in the driving seat after the Fed last week opened final deniers’ eyes with an end of 2024 policy rate projection above 5%. The increase in real rates continues to hurt risk sentiment. Key European stock indices trade with losses of more than 1%. More importantly, the likes of the EuroStoxx 50 are losing key technical support. The support area around 4200, which survived three earlier tests this year, is giving away. The move has further to go with next technical references at 4017 (38% retracement 2022-2023 rally) to 3981 (YTD low). The US S&P 500 opens below the neckline of a technical double top formation (4335) and so does Nasdaq (13162). This spells trouble. The dollar benefits from the real rate increase and risk aversion. EUR/USD moves below 1.0635/11 support to currently change hands around the 1.06 big figure. Next support stands at 1.0516/1.0484 (March & Jan lows). The trade-weighted dollar is already testing the March (YTD) high at 105.88. USD/JPY outperforms (148.80), suggesting the Japanese ministry of finance and/or Bank of Japan officials will soon be on the radar with (ineffective) verbal interventions. Despite the risk-off context, sterling manages to keep even with the single currency with EUR/GBP 0.87 resistance holding at least for now. Less liquid Central European currencies hold relatively strong despite the market context, with HUF the exception. EUR/HUF is bumping into the 390.50/394.50 resistance area. The Hungarian central bank (MNB) better keeps an eye at the currency when defining forward guidance at this week’s central bank meeting where they are to cut the overnight deposit rate by the final 100 bps, bringing it in line with the 13% base rate.

News & Views

The Swedish krone outperforms global peers today. EUR/SEK is moving from 11.86 at the open to 11.72 currently, extending gains from last week Friday. Exactly one week ago, the pair was flirting with an all-time high around EUR/SEK 12. The strong SEK is surprising given the that risk aversion is dominating over other markets, including equities. Two elements may explain the move though. First off, one of the country’s biggest but struggling landlords took important steps to stabilize its finances. At the very least, it eased some concerns about possible knock-on effects that could filter through into the wider economy. Second, the Swedish central bank began its programme to hedge its FX reserves against the possibility of a recovery in the Swedish krone. It announced to do so at the policy meeting last week. The move is done from a risk management point of view – SEK appreciation would saddle up the central bank with substantial losses in its FX portfolio. But one could also consider it a signal that the Riksbank believes the current SEK decline is overdone.

The NBB’s Belgian business confidence marginally improved in September, halting a decline in place since April this year. The uptick from -14.9 to -14.4 does conceal wide sectoral differences though. There was a clear improvement in business-related services on the account of significantly better activity expectations. A near stabilization in the manufacturing industry comes amid more optimistic employment but worse demand expectations. The latter was especially the case for trade, explaining the decline of confidence in this sector. The steep drop in the building industry was broad-based across all subsectors. The trend in orders as well as equipment fell off a cliff. Demand expectations were the exception, which held up despite the prevailing gloom, the NBB said. It remains to be seen whether it is the start of a slow bottoming out process.

Fed’s Goolsbee optimistic on walking the golden path

Chicago Fed President Austan Goolsbee shared his upbeat sentiments on the US economy's direction in an interview with CNBC. He emphasized that the nation is walking the "golden path," capable of curbing inflation while concurrently staving off a recession.

Goolsbee voiced confidence in the US's capacity to sidestep a recession, even as Fed contemplates interest rate hikes to bring inflation down. In his words, "I've been calling that the golden path and I think it's possible, but there are a lot of risks and the path is long and winding."

Highlighting the job market's resilience, Goolsbee mentioned the latest unemployment rate, which stood at 3.8% last month. This figure is strikingly close to last year's unemployment rate during a period when inflation was notably higher.

On the topic of interest rates, Goolsbee noted that Fed is getting close to questions about how long to hold , rather than how high.

ECB’s Lagarde: Current rates will bring inflation to target by 2025 end

ECB President Christine Lagarde, in her address to a European Parliament committee, expressed confidence in the current policy rates, emphasizing their effectiveness in steering inflation back towards the intended target.

"Based on our latest assessment," Lagarde mentioned, "we consider that our policy rates have reached levels that, maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to our target."

Lagarde also highlighted the headwinds faced by the euro area's economy. After broadly stagnating during the first half of 2023, the economy has demonstrated signs of weakening further in the third quarter. This is particularly concerning given the previously resilient services sector, which is also starting to display weakness.

Lagarde elaborated, "The services sector, which had been resilient until recently, is now also weakening," noting that "job creation in the services sector is moderating and overall momentum is slowing."

Domestic price pressures, however, continue to remain formidable. A surge in holiday and travel spending combined with substantial wage growth is holding up services inflation.

Nevertheless, according to staff projections, "inflationary pressures are expected to moderate and that inflation is set to reach our target by the end of 2025."

Yen’s Downward Trajectory Continues as Market Anticipates BOJ’s Move

The USD/JPY pair is drawing nearer to the closely watched 150.00 level, currently experiencing most of its activity around 148.40, as of Monday. The market remains in anticipation of potential financial interventions from the Bank of Japan (BOJ). The BOJ has maintained its ultra-accommodative monetary policy, leaving the yen lingering near ten-month lows.

Last Friday, the BOJ opted to sustain the negative interest rate at -0.10% per annum. The Governor of the central bank highlighted the necessity for additional time to scrutinize the economy and assess the data. For currency market participants and those observing the yen exchange rate, the key concern is not the rate decision per se, but the absence of indications regarding any alterations in the monetary policy framework.

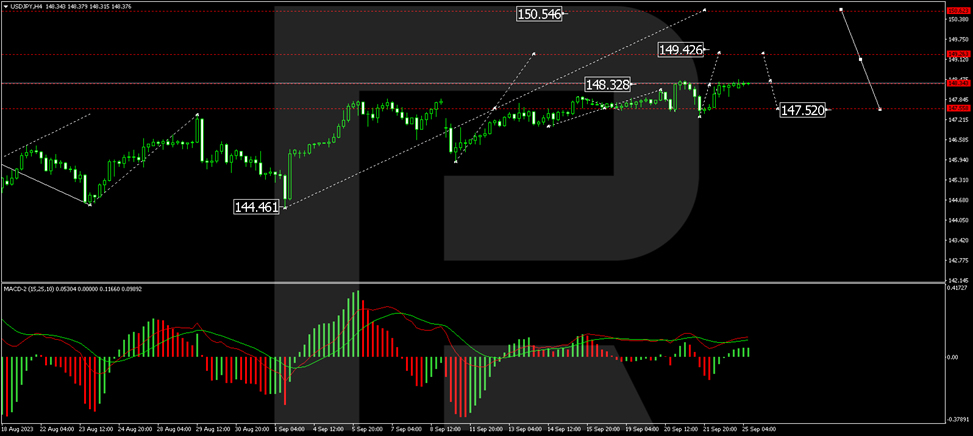

USD/JPY technical analysis

The H4 chart illustrates that USD/JPY has reached the projected target of a growth wave at 148.44 and underwent a correction to 147.33. The market has finalized a growth structure to 148.47 and is currently forming a consolidation range beneath this level. An upward breakout is anticipated, with the price potentially advancing to 149.42. Upon reaching this level, a correction to 148.44 may occur, followed by a rise to 150.50. The MACD oscillator substantiates this scenario, with its signal line positioned above zero and pointing strictly upwards.

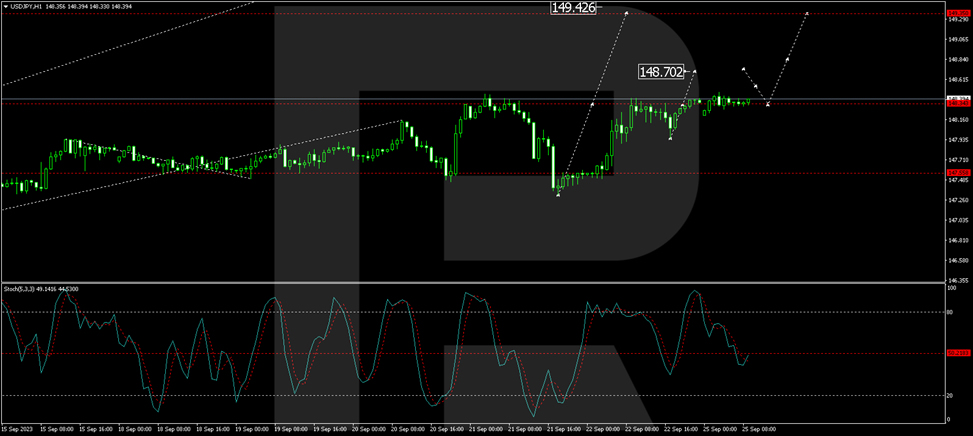

On the H1 chart, a consolidation range has emerged around 148.33. The market is currently on an upward trajectory, aiming for 148.70, with the potential to extend to 149.90. The Stochastic oscillator confirms this scenario, as its signal line, having rebounded from 50, is directed strictly upwards.

The yen continues its descent, with market participants keenly observing any signs of change in the BOJ's monetary policy framework. Technical analysis suggests potential further growth for USD/JPY, but traders will closely watch for developments and adjust their positions accordingly.

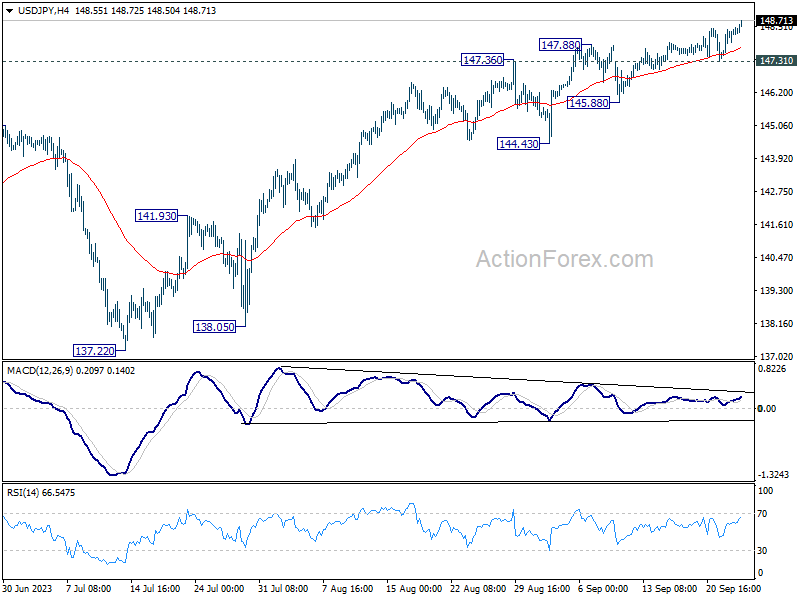

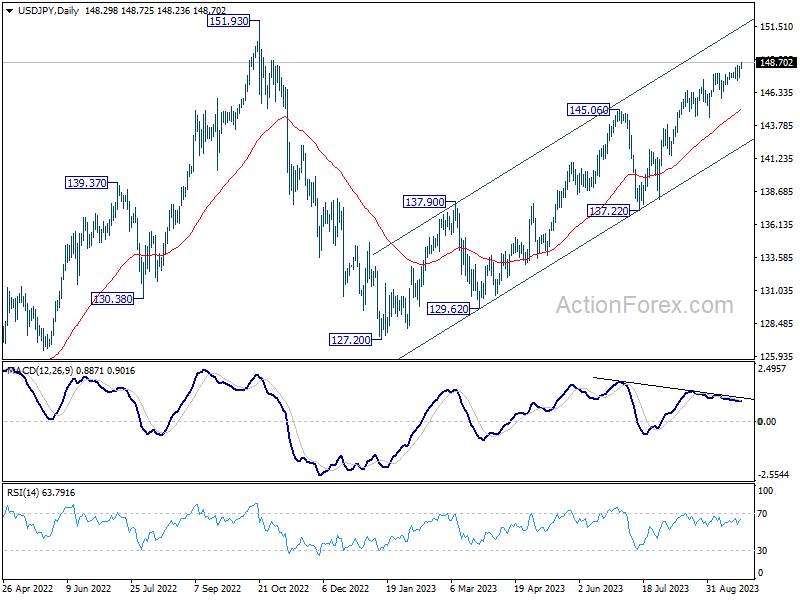

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.77; (P) 148.10; (R1) 148.70; More...

Intraday bias in USD/JPY remains on the upside for the moment. Current rise from 127.20 is in progress to retest 151.93 high. On the downside, however, firm break of 147.31 support will should confirm short term topping, and turn bias to the downside for 145.88 support and below.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by break of 137.22 support will indicate that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

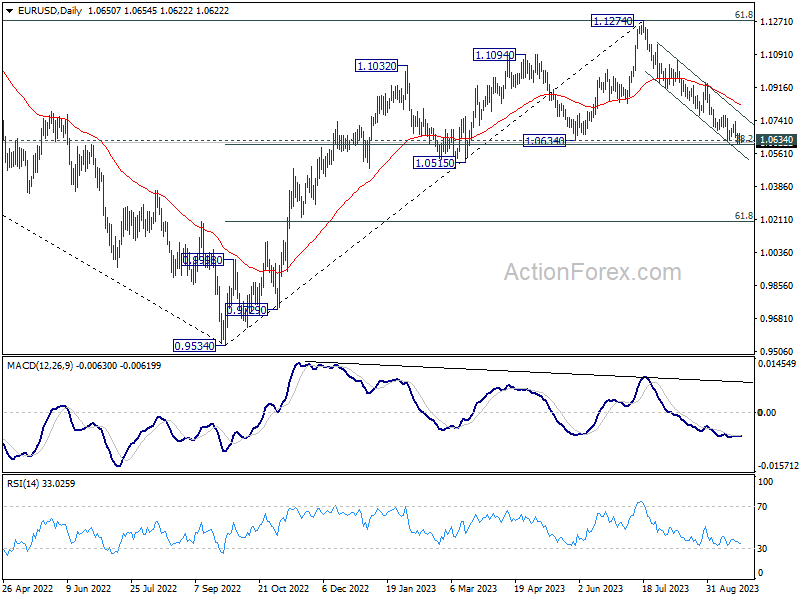

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0616; (P) 1.0644; (R1) 1.0673; More...

Intraday bias in EUR/USD remains neutral and outlook is unchanged. On the downside, sustained break of 1.0609/34 cluster support will carry larger bearish implication. Fall from 1.1274 should then target 1.0515 support next. Nevertheless, strong rebound from current level, followed by break of 1.0767 resistance, should confirm short term bottoming. Intraday bias will be back on the upside for 1.0944 resistance.

In the bigger picture, fall from 1.1274 medium term top is seen as a correction to up trend from 0.9534 (2022 low). Strong support could be seen from 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609) to bring rebound, at least on first attempt. However, sustained break of 1.0609/0634 will raise the chance of bearish trend reversal, and target 61.8% retracement at 1.0199.

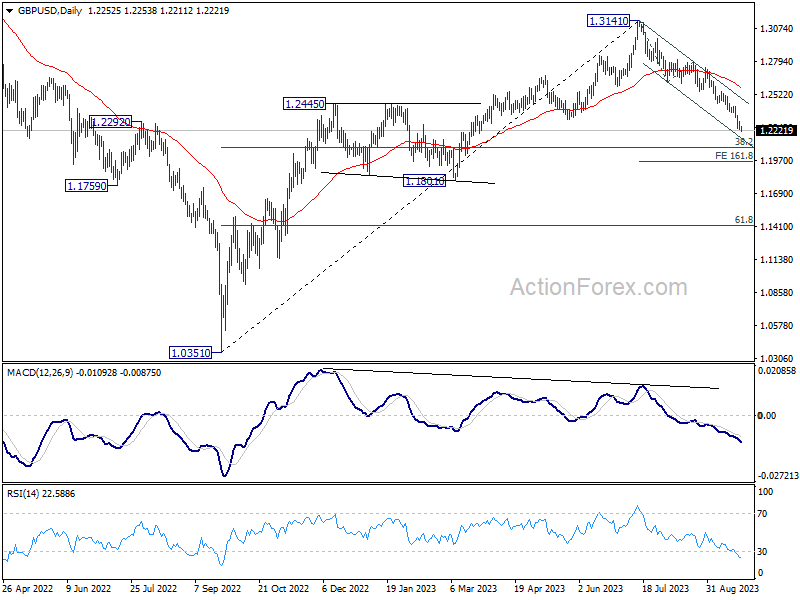

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2213; (P) 1.2257; (R1) 1.2284; More...

GBP/USD's decline is still in progress and intraday bias stays on the downside at this point. Current fall from 1.3141 should target 1.2075 fibonacci level. On the upside, above 1.2369 minor resistance will turn intraday bias neutral and bring consolidations. But near term outlook will stay bearish as long as 1.2618 support turned resistance holds, in case of strong recovery.

In the bigger picture, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. However, sustained break of 1.2075 will raise the chance of bearish trend reversal and target 1.1801 structural support next.