Sample Category Title

AUD/USD Daily Report

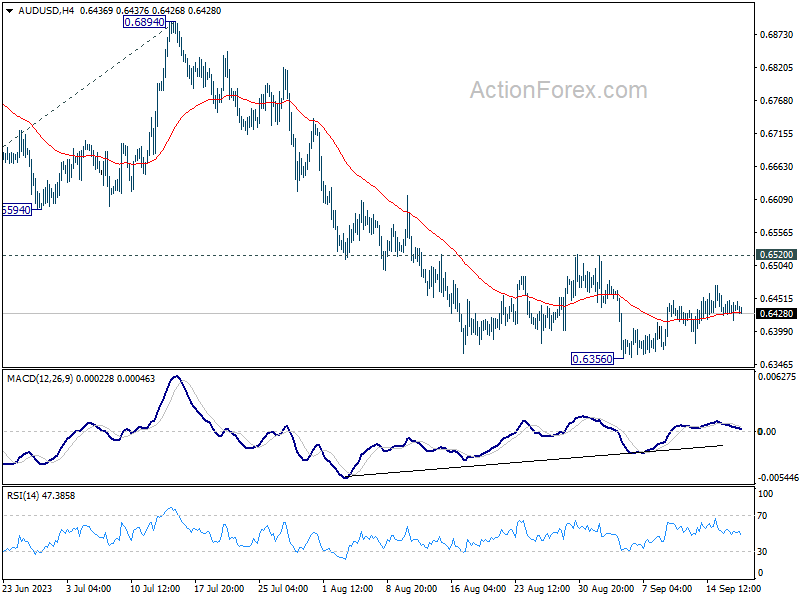

Daily Pivots: (S1) 0.6418; (P) 0.6436; (R1) 0.6454; More...

Intraday bias in AUD/USD remains neutral for the momentum. Outlook stays bearish with 0.6520 resistance intact. On the downside, break of 0.6356 will resume larger down trend to 100% projection of 0.7156 to 0.6457 from 0.6894 at 0.6195.

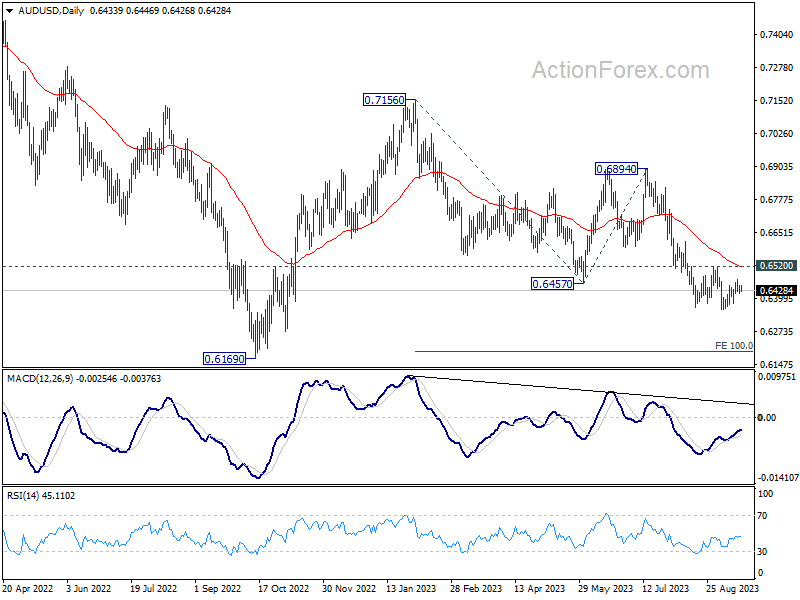

In the bigger picture, down trend from 0.8006 (2021 high) is possibly still in progress. Decisive break of 0.6169 will target 61.8% projection of 0.8006 to 0.6169 to 0.7156 at 0.6021. This will now remain the favored case as long as 0.6894, in case of strong rebound.

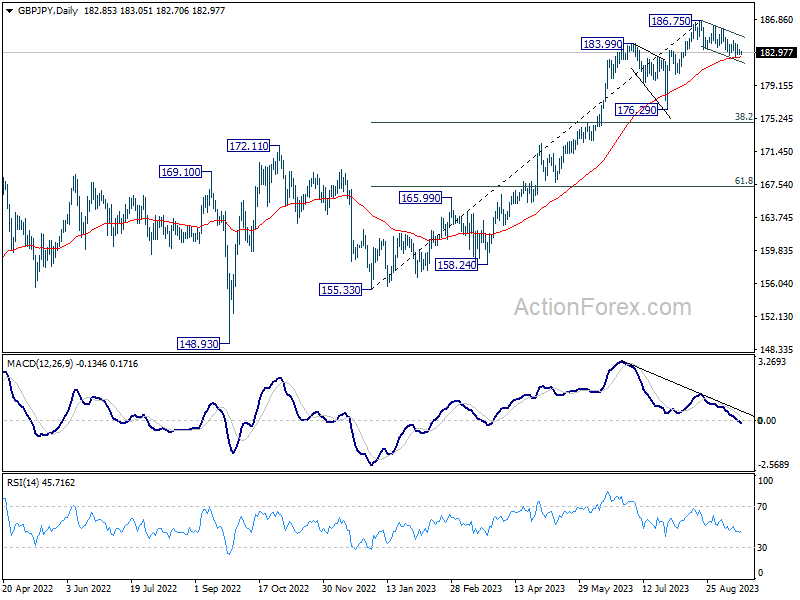

GBP/JPY Daily Outlook

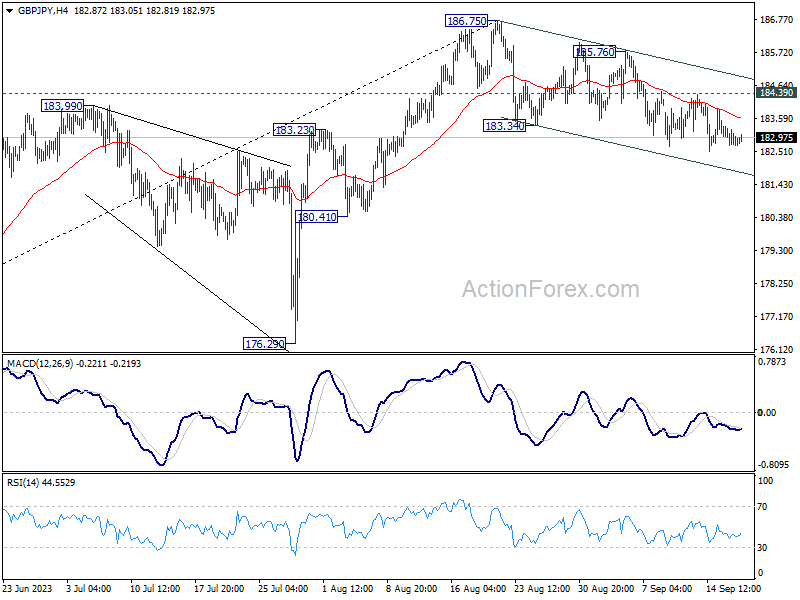

Daily Pivots: (S1) 182.57; (P) 182.96; (R1) 183.20; More...

No change in GBP/JPY's outlook as further fall is in favor with 184.39 resistance intact. Choppy decline from 186.75 is expected to continue. Sustained trading below 55 D EMA (now at 182.46) will argue that it's already in a larger scale correction and target 176.29 support next. On the upside, break of 184.39 resistance will argue that the pull back from 186.75 has completed. Intraday bias will be turned back to the upside for 185.76 resistance next.

In the bigger picture, as long as 176.29 support holds, larger up trend from 123.94 (202 low) should still be in progress. Break of 186.75 will target 195.86 (2015 high). Nevertheless, firm break of 176.29 will confirm medium term topping, and turn outlook neutral for lengthier and deeper consolidations.

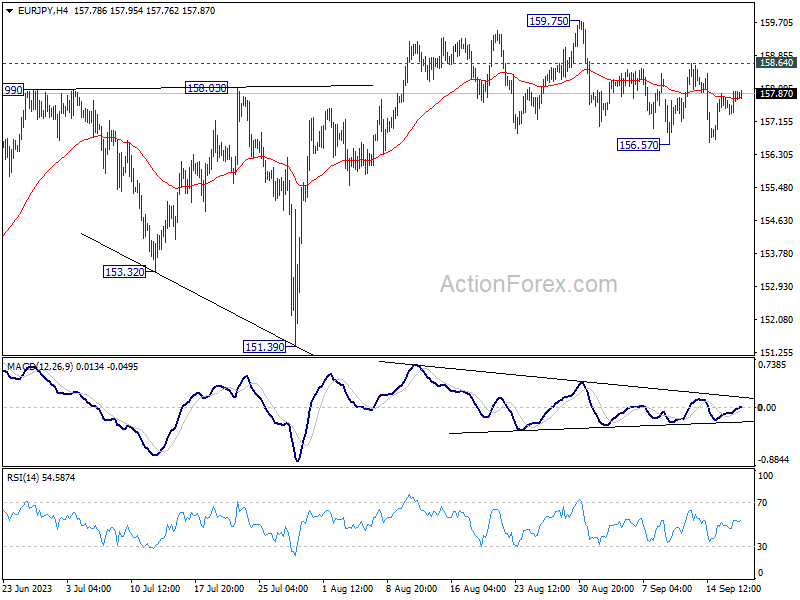

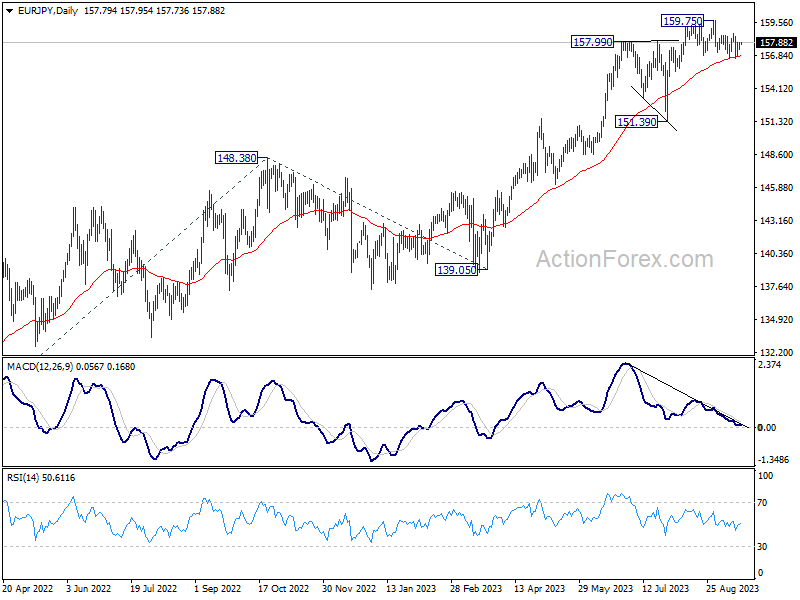

EUR/JPY Daily Outlook

Daily Pivots: (S1) 157.47; (P) 157.70; (R1) 158.06; More....

Range trading continues in EUR/JPY and intraday bias remains neutral. Risk will be mildly on the downside as long as 158.64 resistance holds. Break of 156.57 support, and sustained trading below 55 D EMA (now at 156.80) will argue that fall from 159.75 is a larger scale correction. Deeper decline would be seen back towards 151.39 support. Nevertheless, above 158.64 would bring retest of 159.75 high instead.

In the bigger picture, as long as 151.39 support holds, rise from 114.42 is still expected to continue. Next target is 100% projection of 124.37 to 148.38 from 139.05 at 163.06. Sustained break there will pave the way to retest long term resistance at 169.96.

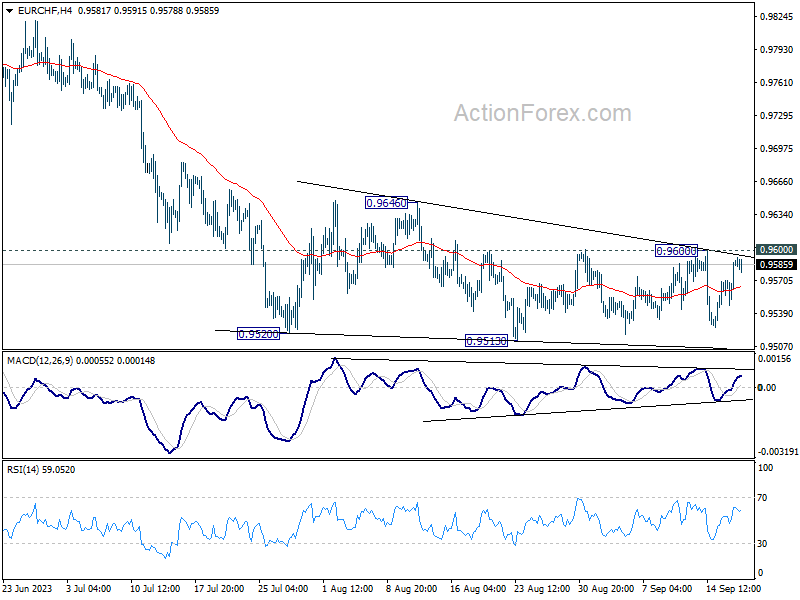

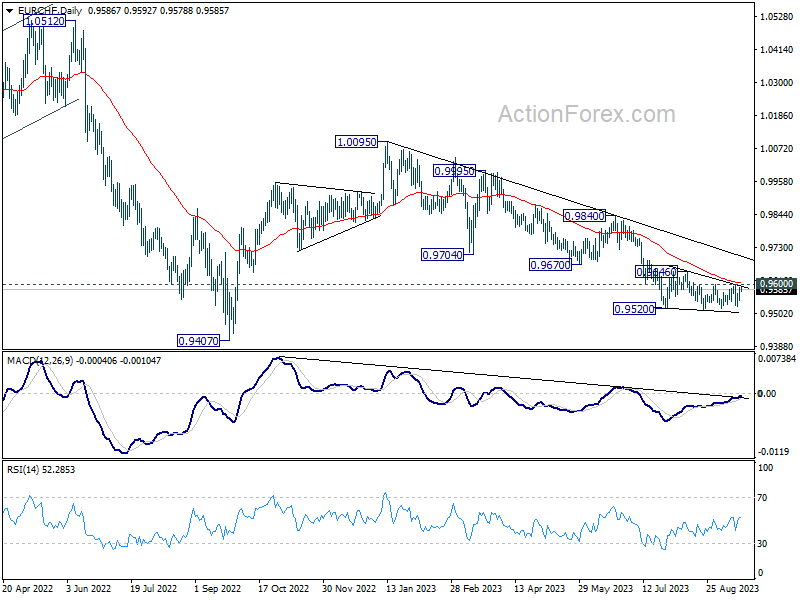

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9563; (P) 0.9578; (R1) 0.9607; More...

Range trading continues in EUR/CHF and intraday bias stays neutral. As long as 0.9600 resistance holds, downside breakout is in favor. Firm break of 0.9513 will resume larger fall from 1.0095 to 0.9407 low. Nevertheless, on the upside, sustained break of 0.9066 resistance will indicate that strong rebound is underway, and turn bias back to the upside for 0.9840 resistance.

In the bigger picture, medium term outlook is staying bearish as the cross is capped well below falling 55 W EMA (now at 0.9818). Down trend from 1.2004 (2018 high) is in favor to continue. Sustained break of 0.9407 will target 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. For now, this will remain the favored case as long as 0.9670 support turned resistance holds, in case of strong rebound.

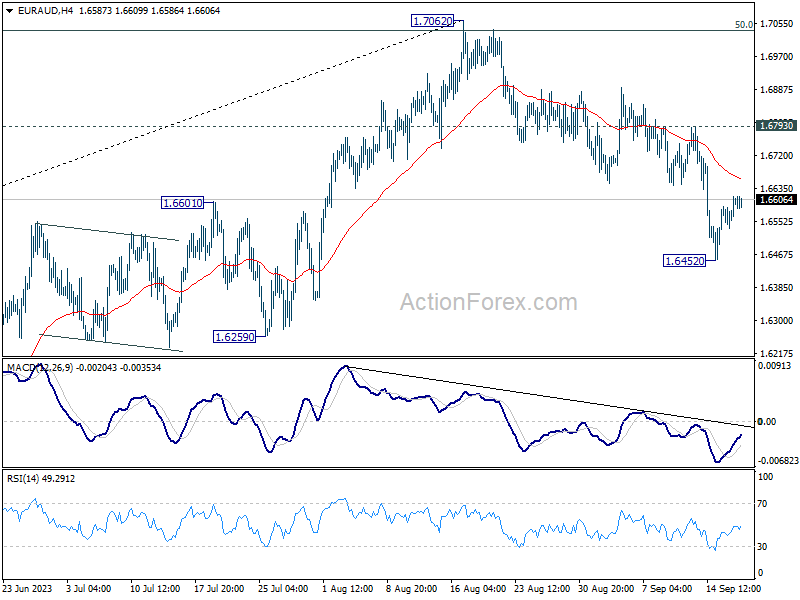

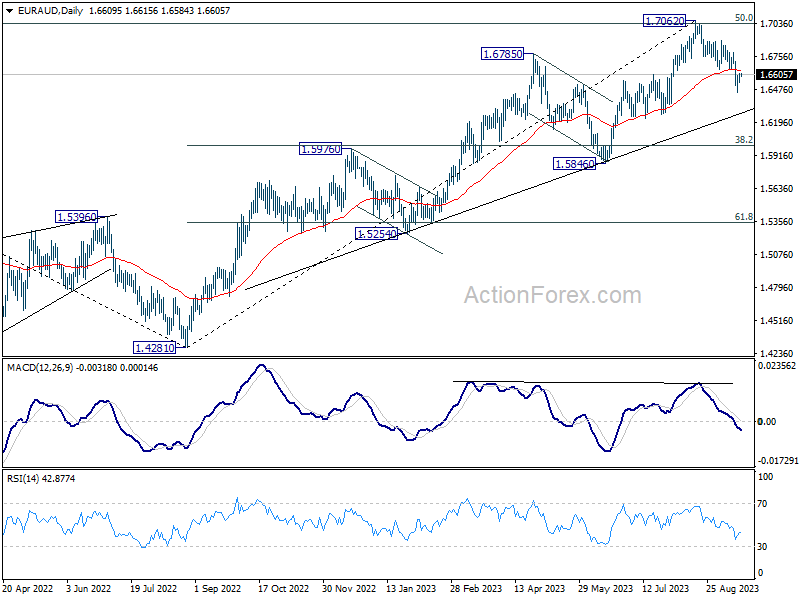

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6559; (P) 1.6588; (R1) 1.6639; More...

Intraday bias in EUR/AUD remains neutral for consolidation above 1.6452 temporary low. But further decline is in favor as long as 1.6793 resistance holds. Fall from 1.7062 is seen as a larger scale correction. Below 1.6452 will target 1.6000 fibonacci level.

In the bigger picture, current development argues that fall from 1.7062 is probably correcting whole up trend from 1.4281. Deeper decline would be seen to 38.2% retracement of 1.4281 to 1.7062 at 1.6000. Strong support should be seen there to bring rebound, at least on first attempt.

Nasdaq 100 Technical: Slipped Back Below 50-Day Moving Average as Fed FOMC Looms

- Bullish tone dissipated last Friday, 15 September ex-post Arm’s IPO spectacularly first-day positive performance as the Nasdaq 100 had a weekly close below the 50-day moving average for the 4th time in the past six weeks.

- Rising market-based inflationary expectations in line with recent magnificent rallies seen in oil prices may cause the Fed to be less dovish on the timing to enact the first interest rate cut in 2024.

- 15,540 is the key short-term resistance to watch.

The price actions of the US Nas 100 Index (a proxy for the Nasdaq 100 futures) have whipsawed in the past four weeks, it cleared above the 15,135 short-term resistance (also the 20-day moving average) as highlighted in our previous report but the bulls failed to make any headway above the 15,460/15,540 medium-term resistance and staged a weekly close below its 50-day moving average on last Friday, 15 September.

Last week’s bullish hesitancy is primarily driven by the fears that the US central bank, the Fed in the upcoming FOMC meeting this coming Wednesday, 20 September together with the latest “dot-plot” release may indicate a stance or guidance that a higher level of interest rate can persist for a longer period of time after the last hike on the Fed funds rate in 2023 (either in the November or December FOMC based on interest rates futures data from CME FedWatch tool as of 18 September 2023).

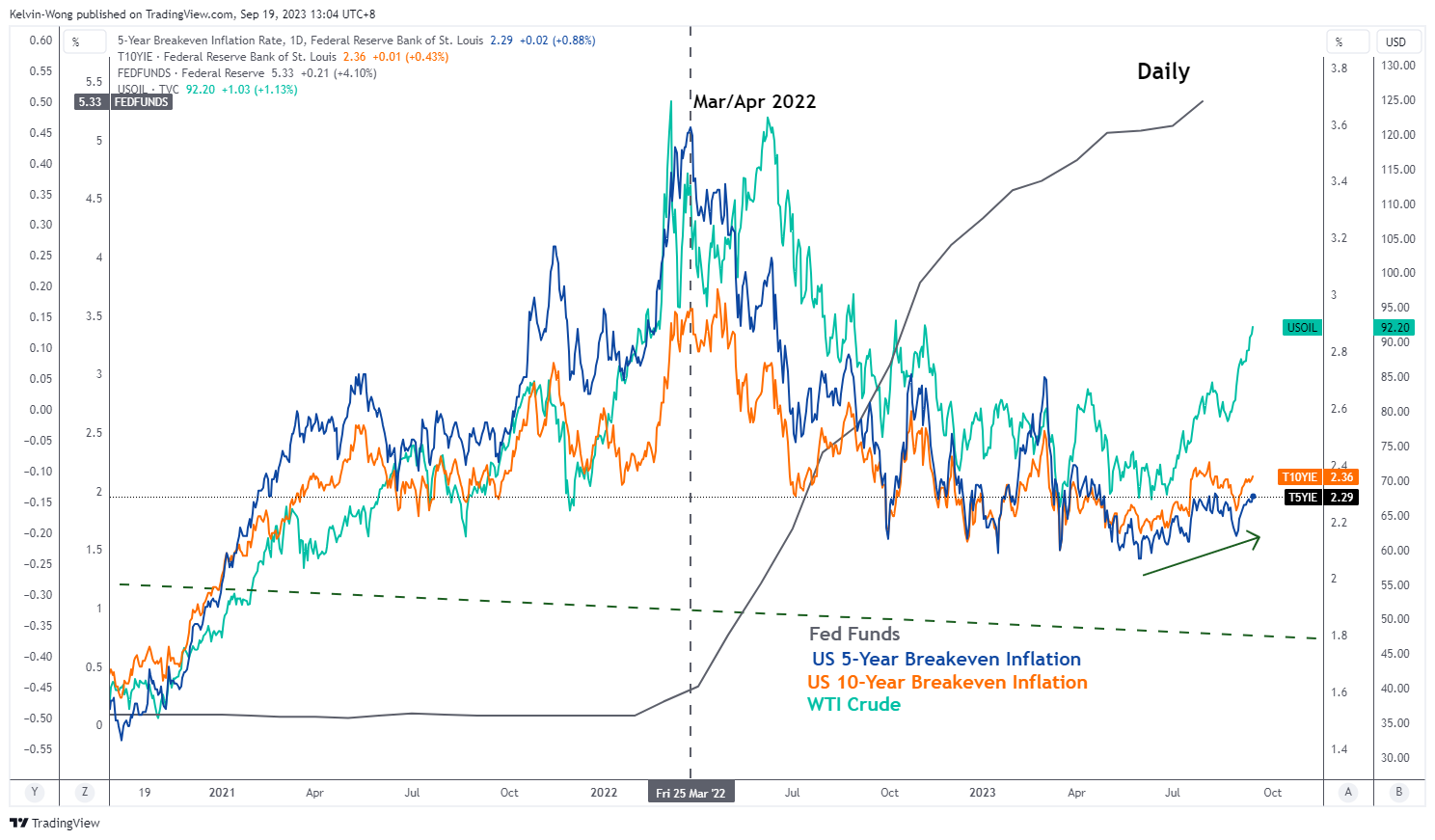

Rising market-based inflationary expectations may catch dovish market participants off guard

Fig 1: Correlation between WTI crude oil and US 5-year & 10-year breakeven inflation rates as of 19 Sep 2023 (Source: TradingView, click to enlarge chart)

A potential Fed’s guidance that indicates a persistent longer period of higher interest rates for next year that stretches beyond Q2 of 2024 due to higher oil prices that have driven up market-based inflationary expectations (5-year & 10-year break-even inflation rates) may catch the market off guard as there is a high chance of 55% for the Fed to enact its first interest rate cut in June 2024 FOMC as inferred from the CME FedWatch tool.

The US Nas 100 Index falls under the “long-duration” risk asset classification that is vulnerable to a higher interest rates environment that persists for a longer-term horizon where profit margins of the top component stocks; the magnificent seven mega-caps (Apple, Amazon, Alphabet, Meta, Microsoft, Tesla & Nvidia) are primarily dependent on longer-term revenues or cash inflows that are likely to be received further far out in the future which in turn tend to have lower present values if discounted by a higher interest rate factor, hence higher opportunity costs for holding such mega-cap stocks.

To offset such potentially higher opportunity costs, the current lofty valuations (forward price to earnings ratios) of these mega-cap stocks need to come down considerably either by higher earnings growth or lower share prices. If the global demand environment remains lackluster or even slips into a recession or stagflation in 2024, the latter is more likely to occur which can put downside pressure on the US Nas 100 Index.

Medium-term momentum remains bearish

Fig 2: US Nas 100 medium-term trend as of 19 Sep 2023 (Source: TradingView, click to enlarge chart)

Last week’s close below the 50-day moving average of the US Nas 100 Index has occurred in conjunction with a bearish momentum condition reading as indicated by the daily RSI.

The daily RSI has inched downwards and shaped a “lower low” right below a former key parallel ascending support now turns pull-back resistance at the 60 level which suggests a potential resurgence of medium-term bearish momentum.

Price actions have broken down below the 20-day moving average

Fig 3: US Nas 100 minor short-term trend as of 19 Sep 2023 (Source: TradingView, click to enlarge chart)

Last Friday’s 15 September price actions of the Index staged a bearish breakdown below its 20-day moving average and yesterday’s 18 September minor rebound seen at the start of the US session has halted at the 20-day moving average. These observations suggest that short-term bearish momentum remains intact.

Watch the 15,540 key short-term pivotal resistance and a break below 15,085 may trigger a further slide towards the next intermediate support at 14,750 in the first step.

On the other hand, a clearance above 15,540 invalidates the bearish tone for the next intermediate resistance to come in at 15,800 (27 July/ 29 July 2023 minor swing highs).

Mild Setback in US (Real) Yields Took Some Shine of Dollar

Markets

In a session deprived of key eco data and with markets awaiting more concrete guidance from tomorrow’s Fed decision/economic projections, the by default trend in yields was still north. Additional (Fed and even ECB) rate hikes beyond September remain an option and it will take a lot of progress on inflation for centrale bankers to ease the ‘higher for longer’ mantra. Aside from changes in interest rates, central bankers also have other ‘technical options’ to drain excess liquidity/tighten monetary conditions (cf Reuters article on ECB sources published yesterday afternoon infra). In this context, the ECB pause didn’t prevent EMU/German yields to gain further traction. Bund yields added between 4.3 bps (5-y) and 2.7 bps (30-y). The German 30-y yield touched a new cycle top just below 2.86%. The 10-y (2.71%) is nearing cycle peak levels in 2.74%/2.77% area. US yields initially followed the uptrend, but momentum dwindled mid-morning, maybe due an unexpected sharp setback in the NAHB home builders confidence. NAHB analyzed that “High mortgage rates are clearly taking a toll on builder confidence and consumer demand, as a growing number of buyers are electing to defer a home purchase until long-term rates move lower.” Many builders indicated to have recurred to incentives, including price concessions. Whatever, the reason Treasuries found a bottom. The 2-y yield kept a gain of 2.1 bps. Longer maturities lost op to 3.3 bps (30-y). ‘Improving’ sentiment in in Treasuries also helped an intraday bottoming in equities. The three major US index finished the little changed. Rising oil prices remains a source of uncertainty both for bonds and equities, with Brent testing the $95 p/b barrier. The mild setback in US (real) yields also took some shine of the dollar. DXY eased from the 105.3 area to close near 105.1. USD/JPY is holding close to the 147.95 recent top, but no new attack occurred, for now. EUR/USD initially didn’t go anywhere, but captured a better bid after the Reuters article on potential further ECB steps (close 1.0692). The latter move also propelled EUR/GBP back above the 0.86 level ( close 0.863).

Today’s eco calendar is thin with only US housing starts and permits, the OECD economic outlook and final EMU CPI to guide intraday trading. We expect the downside in yields to remain well protected going into tomorrow’s Fed decision. Fed governors might reinforce the higher for longer mantra by lowering expected rate cuts next year. A higher dot for the neutral rate, if it were to occur, also would be an important sign. Over the previous two sessions, the dollar took a breather, but we still expect the greenback to have the better cards in a context of global tightening of monetary conditions. Recent top levels (DXY 105.44, USD/JPY 147.95, EUR/USD 1.0635/32) stay within reach.

News and Views

News agency Reuters quoted sources in an article on the ECB’s next steps. They indicated that tackling inflation is top of their mind right now, after raising the deposit rate a tenth consecutive time last week, to 4%. Discussions center around three topics. First, the amount of reserves banks must park unremunerated at the ECB. People close to the matter suggest several policy makers want to raise the minimum reserve ratio from 1% currently to 3% or 4%. That would take away €330bn-495bn from the current €3.7tn excess liquidity. Second, the ECB is looking into a faster reduction of its €4.8tn bond portfolio (APP + PEPP). Options include active sales from the APP or ending PEPP reinvestments before the current shelf date (“at least until end 2024”). Finally, the ECB is looking into switching back from to a corridor-system from the current floor-based system. That requires significantly shrinking excess liquidity and doesn’t seem to be something which can be implemented in the near term. The Reuters article suggests that policy makers are split between bundling decisions altogether (takes time) or using a step-by-step approach In which raising the minimum reserve ratio could be enforced as soon as October, with a decision on APP/PEPP coming in December at the very earliest, but more likely only in March of next year.

Chinese holdings of US Treasuries fell by $13.6bn in July to $776bn, the lowest level since mid-2009. Treasury holdings ranged between roughly $1tn and $1.3tn between mid-2010 and early 2022. This year, China did rotate into higher yielding US agency debt. Holdings of Japan, the biggest foreign owner of US Treasuries, increased by $6.9bn to $1.1tn (down from $1.325tn record end 2021). The UK’s holdings, number 3, fell by $9.9bn to $662.4bn. That remains near the highest level on record for the country.

Hawkish Pause?

Strikes at GM, Ford and Stellantis factories dampened overall market sentiment on Monday. The walkout led by United Auta Workers (UAW) began last Friday and saw little progress as the union refused a 21% pay rise offered to workers. Shawn Fain, who is at the helm of the movement, demands a 40% pay rise and 32-hour workweek – unprecedented for the US. Good luck to both parties in these negotiations.

GM, Ford and Stellantis fell yesterday. The barrel of US crude traded past the $92 level, as Brent crude advanced past $95pb. I believe that we are approaching a peak in the actual oil rally and we should see a downside correction of at least 5-6% from the actual levels, yet the damage from rising oil prices is already showing in inflation numbers. That’s partly why the European Central Bank (ECB) announced a ‘dovish hike’ last week.

A hawkish pause?

This week, the US policymakers will certainly opt for a ‘hawkish pause’. The Fed will likely revise its growth expectations significantly higher on the back of resilient consumer spending and solid growth. The looming talk of another government shutdown, the student loan repayments and the UAW strikes will sure have a negative impact on US growth numbers, but US Treasury Secretary Janet Yellen defends the scenario of ‘soft landing’ as labour market is still healthy, industrial output is rising and inflation is coming down, she says.

Despite the latest softness in the jobs data, the US inflation figures last week surprised to the upside. A major part of disinflation since last summer was due to waning post-Covid supply issues that led to higher supply, hence slower price growth. But the improvement in supply could be coming to an end, and oil prices are rising. Therefore, the Fed will certainly sound cautious and reasonably hawkish this week. The so called dot plot will certainly point at another rate hike before the year end, and a higher median rate throughout next year.

The US dollar index tested the important 38.2% Fibonacci resistance last week, especially after the euro sold off following the ECB rate hike. The Fed announcement could push the US dollar index into the medium-term bullish consolidation zone.

A dovish hike?

If the Fed is not expected – not even a little bit – to hike rates this week, the Bank of England (BoE) could hike the bank rate by a final 25bp on Thursday. It’s possible that a hawkish pause from the Fed propels the dollar higher, while a dovish hike from the BoE has the opposite impact on sterling. Cable slid below its 200-DMA last week and is now back in a long-term bearish trend.

And nothing?

In Japan, not much is expected to change this week. Warnings from Japanese officials that a further yen selloff would spark a direct FX intervention slowed down but not reversed the JPY selloff. The USDJPY is trading just below the 148 level, with, sure, limited upside potential, and of course a good downside potential, but that downside potential must be unlocked by a reasonably hawkish BoJ, and I don’t see that coming this week.

Risk Sentiment Falters Ahead of Central Bank Flurry

Market movers today

Today we receive the final August inflation figures for the euro area where we do not expect any revisions compared to the flash estimate. The flash estimate showed that inflation in August was slightly higher than expected. Headline inflation remained at 5.3% and core inflation ticked down from 5.5% to 5.3% y/y. In today's release, it will be interesting to see the underlying dynamics of the aggregate prints especially the details on the decline in core inflation. For more details on inflation, see Global Inflation Watch: Underlying price pressures remain sticky, 13 September.

The OECD will publish its updated projections for the global economy.

In the US, data for housing starts and building permits in August will be released.

Overnight, we get 1-year and 5-year loan prime rates from China but since the rates were just cut last month and no changes were made last week in the medium-term lending rate, we expect unchanged loan prime rates this time.

The 60 second overview

Sentiment: With ECB governors on the wires warning that rates will remain high for some time, and ahead of a flurry of central bank meetings, market sentiment is faltering. Oil price has climbed above USD 95 level, and with the barrel price more than 20 dollars higher than in June, stagflationary fears are again raising their head. In an FT-Booth survey over the weekend, majority of the respondents cited oil supply restrictions as their biggest concern regarding inflation outlook. Weak risk sentiment weighed heavily on Scandi currencies yesterday with EUR/SEK reaching a new all-time-high level.

Geopolitics: EU-China trade tensions are brewing with an EU probe into Chinese EV subsidies. We think these increasing tensions are worth monitoring as EU trade deficit with China has grown sharply in recent years. Imports of EVs to Europe was bound to become a flash point of tensions sooner or later, not least considering the ongoing challenges in the German auto sector. While tensions are growing between Europe and China, US weapons sale to Taiwan under sovereign-nation program has fed new tensions between the two, and China has increased the intensity of military exercises around Taiwan lately. Meanwhile, if we zoom in on Europe, Ukraine has made significant advance in the battlefield, successfully breaking through the first Russian line of defence in the south. If they are able to push further, they could eventually be able to attack key Russian logistics routes. Read more in our monthly Geopolitical radar - EU-China trade tensions brewing, Ukraine makes advance, 19 September.

US: The US Congress continues to struggle to pass a funding bill to avert a looming government shutdown on 30 September. On Sunday, the leaders of the hardline republican House Freedom Caucus struck a deal with representatives from the more moderate Main Street Caucus on a short-term 'continuing resolution' funding bill until 30 October, which House speaker McCarthy will bring to the House floor on Thursday. But as the bill contains immediate 8% spending cuts to several federal agencies, and excludes further aid to Ukraine as well as disaster relief, it will not gain support from the Democratic-controlled Senate, even if it passes the House vote. Unless the hardliners eventually agree on a passable deal, McCarthy can either move towards passing a bipartisan deal negotiated in the Senate with support from House democrats, or lead the government towards a shutdown. The former could risk McCarthy's position as House speaker, as some Republicans including Florida representative Matt Gaetz, have already threatened to bring up a motion-to-vacate, while the latter would disrupt public services and salary payments, potentially adding to the current downside risks to the economy.

Equities: It was a dull session on Monday, with little news and thereby little equity moves. US closed unchanged while Europe sold off about -1% in catch-up with the weak US Friday session. Last week's losers rebounded, including big tech, semis and homebuilders. Industrials performed well in the European and Nordic sessions and banks underperformed. The wait-and-see mode for Fed lingers today, with US futures unchanged this morning and Asian markets mostly lower too.

FI: Rates rose across the board driven by the front end, with 2y around 4bp higher to 3.26%. ECB governors were on the wires saying it is premature to discuss rate cuts, and rates may peak for the winter, spring and summer. Today, focus turns to the euro area final inflation print.

FX: NOK and SEK were under pressure on Monday amid poor risk sentiment and negative equities. EUR/SEK printed a new all-time-high at 11.995 and EUR/NOK tested 11.60. Both Scandies regained most or some of the losses in the evening session, though. Meanwhile, EUR/USD was relatively stable, yet a little bit higher toward 1.0680. USD/JPY moved sideways around 147.60 and GBP/USD oscillated just below 1.24.

Credit: The slightly sour sentiment in the equities markets rubbed off on the credit markets yesterday, where iTraxx main widened 0.2bp to 69.3bp and Xover widened 0.9bp to 389bp. That said, liquidity improved in the cash bond market where the spread performance was also better. Also the primary markets continue to work, exemplified by EUR deals announced from the local issuers Elisa and Spar Nord and the closure of a EUR600m NPS Commerzbank issue.

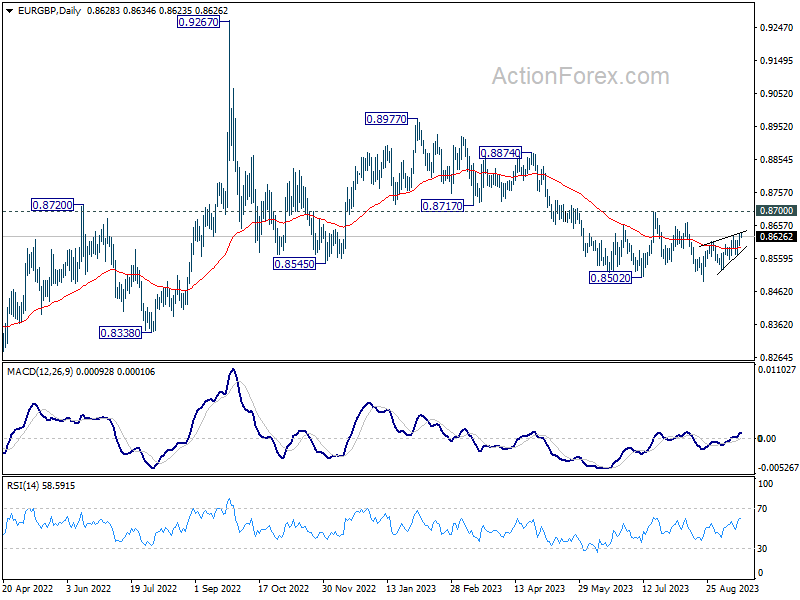

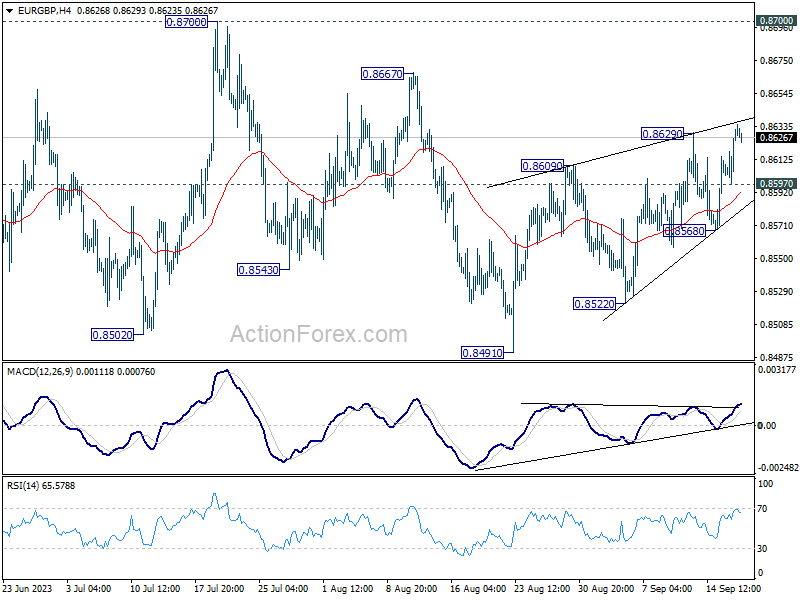

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8610; (P) 0.8622; (R1) 0.8645; More...

EUR/GBP's rebound from 0.8491 resumed by breaking 0.8629 and intraday bias is back on the upside. This rise is seen as the third leg of the corrective pattern from 0.8502. Upside should be limited by 0.8667/8700 resistance zone. On the downside, below 0.8597 minor support will turn intraday bias neutral first. Further break of 0.8568 support will turn bias back to the downside for retesting 0.8491 low.

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Fall from 0.8977 is seen as the third leg. As long as 0.8700 resistance holds, further decline is still expected. Break of 0.8491 will resume the fall towards 0.8201 (2022 low). Nevertheless, firm break of 0.8700 will now be a sign of bullish reversal.