Sample Category Title

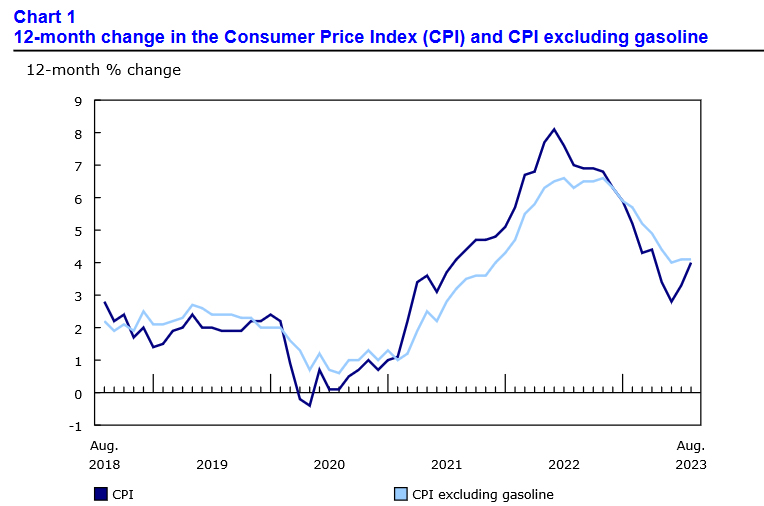

Canada CPI jumps to 4% yoy on gasoline, above expectation of 3.8% yoy

Canada CPI accelerated to 4.0% yoy in August, up from July's 3.3% yoy, above expectation of 3.8% yoy. The in CPI was largely the result of higher year-over-year prices for gasoline in August (+0.8%) compared with July (-12.9%). Excluding gasoline, CPI was unchanged at 4.1% yoy.

CPI median rose from 3.7% yoy to 4.1% yoy, above expectation of 3.7% yoy. CPI trimmed rose from 3.6% yoy to 3.9% yoy, above expectation of 3.5% yoy. CPI common was unchanged at 4.8% yoy, matched expectations.

On a monthly basis, CPI rose 0.4% mom in August, double expectation of 0.2% mom.

EUR/USD – Edges Higher Even as Eurozone Inflation Revised Slightly Lower

- Headline HICP inflation falls to 5.2% (5.3% expected) while core HICP remains at 5.3%

- Further declines expected over the remainder of the year

- Divergence warns of potential exhaustion in the sell-off

Eurozone headline inflation was slightly lower than initially reported in August while core was unrevised and is now modestly higher.

Both are expected to fall going into next year and today’s revisions are unlikely to alter the view of the ECB which has already decided that no more rate hikes will likely be needed. As with all favorable data though, it may come as a small relief that surprises in the data are finally in the right direction.

Shortly after the data, the OECD released its growth forecasts for this year and next and it won’t come as a surprise that the eurozone has seen its downgraded by 0.3% and 0.4%, respectively. That lower activity is likely what’s led to the ECB probably calling it a day on rate hikes.

Also interesting from the forecasts ahead of the Fed meeting was that the US saw upgrades for both years, very much against the trend. That resilience has contributed to inflation rising higher than expected and being harder to contain and may encourage the Fed to hold off from signaling the end of the cycle tomorrow, as the ECB did last week.

Can we see a correction after the recent sell-off?

From a fundamental perspective, it is possible as the ECB has now adopted a more dovish stance than many anticipated and is unlikely to become more dovish soon. The Fed could match it which may make things interesting but there may be more hesitancy there.

Source – OANDA on Trading View

Then there’s the technicals which are also starting to point to exhaustion in the sell-off. The MACD histogram is making higher lows as the price makes lower lows while the moving averages and the stochastic are flattening which may suggest we’re at a turning point. Such a divergence doesn’t point to an imminent reversal in itself, but it does suggest the trend is weakening.

It’s run into support around 1.07 and is now testing support from a couple of weeks ago after only recently breaking through the 200/233-day simple moving average band. The recent high around 1.0770 could be interesting, if broken, and point to a potential corrective move in the pair.

A rotation lower from here and below 1.07 would be interesting, especially if we see further divergences forming between price and the MACD and stochastic. The next most notable level below is 1.05, having been a key level in this pair over a number of years.

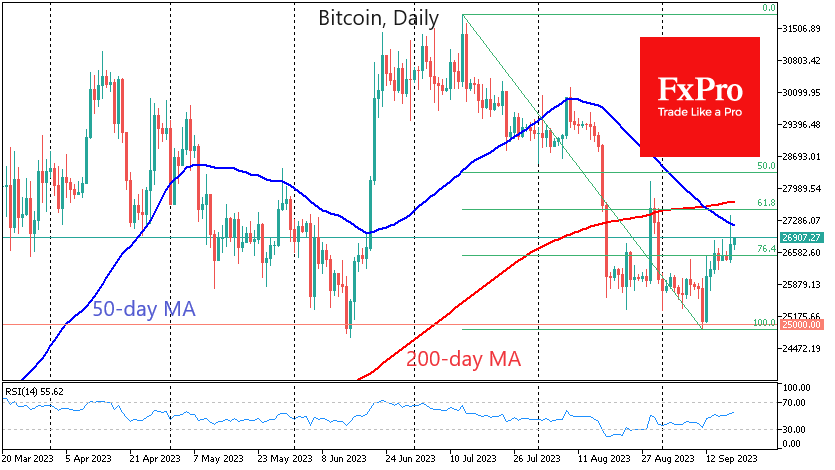

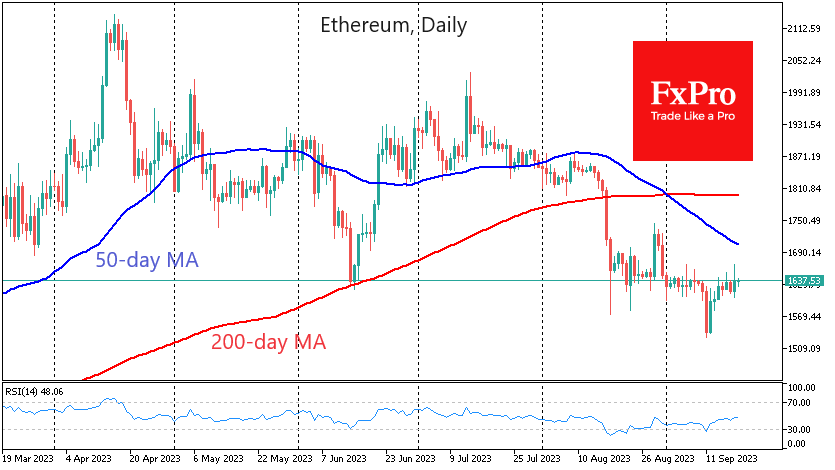

Crypto Market Fails to Accelerate Its Growth

Market picture

Crypto market capitalisation exceeds $1.07 trillion (+0.6% in 24h), maintaining its upward trend over the last seven days.

Bitcoin hit $27.4K on Monday for the first time since late August but quickly pulled back to $26.8K. This was the second failed attempt to break above the 50-day moving average since early August and the second downward reversal on the approach to the 200-day MA. This is an important signal that the bears are still in control of the situation in the largest cryptocurrency, even though they gave some space to “play” as we expected yesterday.

Ethereum, unlike the first crypto, is moving strictly to the right, almost pegged to $1640. The long consolidation removes oversold conditions and prepares liquidity for a new round of declines. However, much for the two largest cryptos this week depends on big central banks comments, from the Fed to the Bank of Japan. They can either bring back risk appetite or completely undermine it.

News background

According to CoinShares, investments in crypto funds decreased by $54M last week, with outflows for 8 of the previous nine weeks. Bitcoin investments decreased by $45M, Ethereum investments fell by $5M, and acquisitions in funds that allow shorting Bitcoin fell by $4M.

Weekly trading volume rose to $1 billion, up 42% over the previous week. Cumulative outflows over the past two months totalled $455 million, with net inflows since the beginning of the year down to just $51 million, CoinShares noted.

Central and South Asian countries are leading the way in terms of cryptocurrency adoption, according to research from Chainalysis. India topped the list, with Nigeria and Vietnam rounding out the top three. The global index of mass adoption of cryptocurrencies is still very far from the historic highs of 2021 and shows a downward trend.

Ethereum developers failed to launch the Holesky test network and scheduled a new attempt in two weeks. The failure was due to a misconfiguration in the Genesis source file.

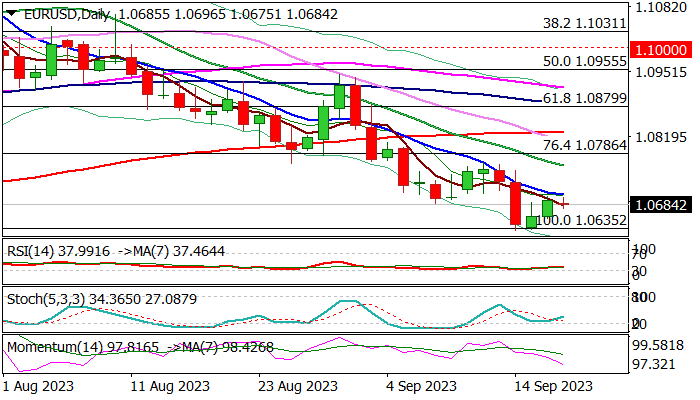

EUR/USD: Recovery Losing Traction

EURUSD is trading within a narrow range during European session on Tuesday, following strong rebound in past two days after larger bears were rejected at key support at 1.0635 (May 31 low).

Technical picture remains increasingly bearish on daily chart (rising negative momentum / MA’s in full bearish setup) and warn that corrective action might be near its end (capped by daily Tenkan-sen).

Inflation in the Eurozone was slightly lower than expected in August, which should add pressure on the currency, though consumer prices are still over two times above ECB’s 2% target.

This keeps the central bank alerted, despite dovish signals from the last policy meeting, as the policymakers left the door opened for possible further hikes, should the situation deteriorate.

Near-term action can be described as consolidation while moving between 1.0700 (daily Tenkan-sen / psychological barrier) and 1.0635 support, with sustained break above 1.0700 to allow for stronger correction and expose upper pivots at 1.0768 (Sep 12 high) and 1.0792 (daily Kijun-sen).

Conversely, firm break of 1.0635 support would open way for test of next key supports at 1.0611 (Fibo 38.2% of 0.9535/1.1275 uptrend) and 1.0553 (daily Ichimoku cloud top).

Res: 1.0700; 1.0752; 1.0768; 1.0792.

Sup: 1.0675; 1.0654; 1.0635; 1.0611.

Australian Dollar Edges Higher after RBA Minutes

- RBA minutes show that central bank considered rate hike

- China to announce loan prime rate decision on Wednesday

The Australian dollar continues to trade quietly this week. In Tuesday’s European session, AUD/USD is trading at 0.6456, up 0.30%.

The Reserve Bank of Australia released the minutes of this month’s meeting earlier today. The central bank considered a quarter-point hike but eventually decided to maintain the benchmark cash rate unchanged at 4.1%. RBA board members were split in previous decisions and this meeting seems to have repeated the pattern. The minutes noted that weak growth and high inflation supported the case for increasing interest rates, but the board ultimately opted to pause, due to the risk that the effects of the tightening cycle were yet to be felt (“lags in the transmission of policy through the economy”).

The minutes noted that board members listed weak domestic demand and contagion from China’s slowdown as risk factors for an economic slowdown. Despite these concerns, the RBA has signalled that inflation remains too high and has left the door open to further hikes. Inflation is currently running at 6% and the RBA has forecast that inflation will slow to around 3.25% by the end of 2024 and won’t fall back into the 2%-3% target range until late 2025.

The new RBA Governor, Michelle Bullock, will have to determine a rate path that is suitable for a weak Australian economy that is grappling with high inflation. Bullock has said that upcoming rate decisions will be based on data, but a more proactive approach may be needed rather than simply reacting to the data around the time of a rate meeting.

The Australian dollar is sensitive to Chinese releases and investors will be keeping an eye on the PBOC decision on one-year and five-year loan prime rates on Wednesday. These rates are likely to remain unchanged, but any surprises could have an impact on the movement of the Aussie. China’s slowdown has weighed on the Australian dollar, but the August retail sales and industrial production reports beat expectations and have raised hopes that China’s economic downturn is abating.

AUD/USD Technical

- AUD/USD is putting pressure on resistance at 0.6477. The next resistance line is 0.6524

- 0.6381 and 0.6332 are the next support levels

Eurozone Inflation Revised Lower, OECD Downgrades Growth, RBA Considered Another Hike

Eurozone headline inflation was slightly lower than initially reported in August while core was unrevised and is now modestly higher.

Both are expected to fall going into next year and today's revisions are unlikely to alter the view of the ECB which has already decided that no more rate hikes will likely be needed. As with all favourable data though, it may come as a small relief that surprises in the data are finally in the right direction.

Shortly after the data, the OECD released its growth forecasts for this year and next and it won't come as a surprise that the eurozone has seen its downgraded by 0.3% and 0.4%, respectively. That lower activity is likely what's led to the ECB probably calling it a day on rate hikes.

Also interesting from the forecasts ahead of the Fed meeting was that the US saw upgrades for both years, very much against the trend. That resilience has contributed to inflation rising higher than expected and being harder to contain and may encourage the Fed to hold off from signalling the end of the cycle tomorrow, as the ECB did last week.

RBA signals the tightening cycle is probably over

Minutes from the RBA meeting earlier this month show the board considered raising interest rates by another 25 basis points but decided the downside risks to inflation from the lagged effect of past hikes outweigh upside risk factors including high services inflation.

While the central bank remains open to further increases in the future, it would appear the RBA can add its name to the list of central banks that are likely done with their tightening cycles, with plenty more likely joining them this week.

Oil rally maintains momentum as OPEC+ continues to drive prices higher

Oil prices are continuing to trend higher, with Brent surpassing $95 a barrel for the first time since November as the OPEC+ alliance continues to restrict supply. While members may insist the goal is to rebalance the market, unlike other times over the last year, the measures are now having a significant impact on the price which should force a rethink over the coming months.

At a time when central banks are starting to see the light at the end of the inflation tunnel, $100+ oil will be incredibly unwelcome and unhelpful. I'm not sure there's much economic sense in tipping the global economy into recession if OPEC+ persevered with these cuts, which makes me question how high the price will go and how sustainable it will be.

Cautious trading in Gold ahead of the Fed decision

Gold is trading a little flat on Tuesday, perhaps showing a little caution ahead of the Fed meeting after a decent recovery in recent days. The yellow metal slipped back toward $1,900 amid resilient economic figures from the US that fed into fears of interest rates staying high for longer, as the central bank has repeatedly warned.

The question now for gold traders is whether the Fed is willing to acknowledge that it's probably done with rate hikes, as we heard from the ECB last week, or continue to insist another is likely. The dot plot will be key to this but as always, traders will hang on Powell's every word. A hawkish tone from the Fed could put $1,900 in jeopardy.

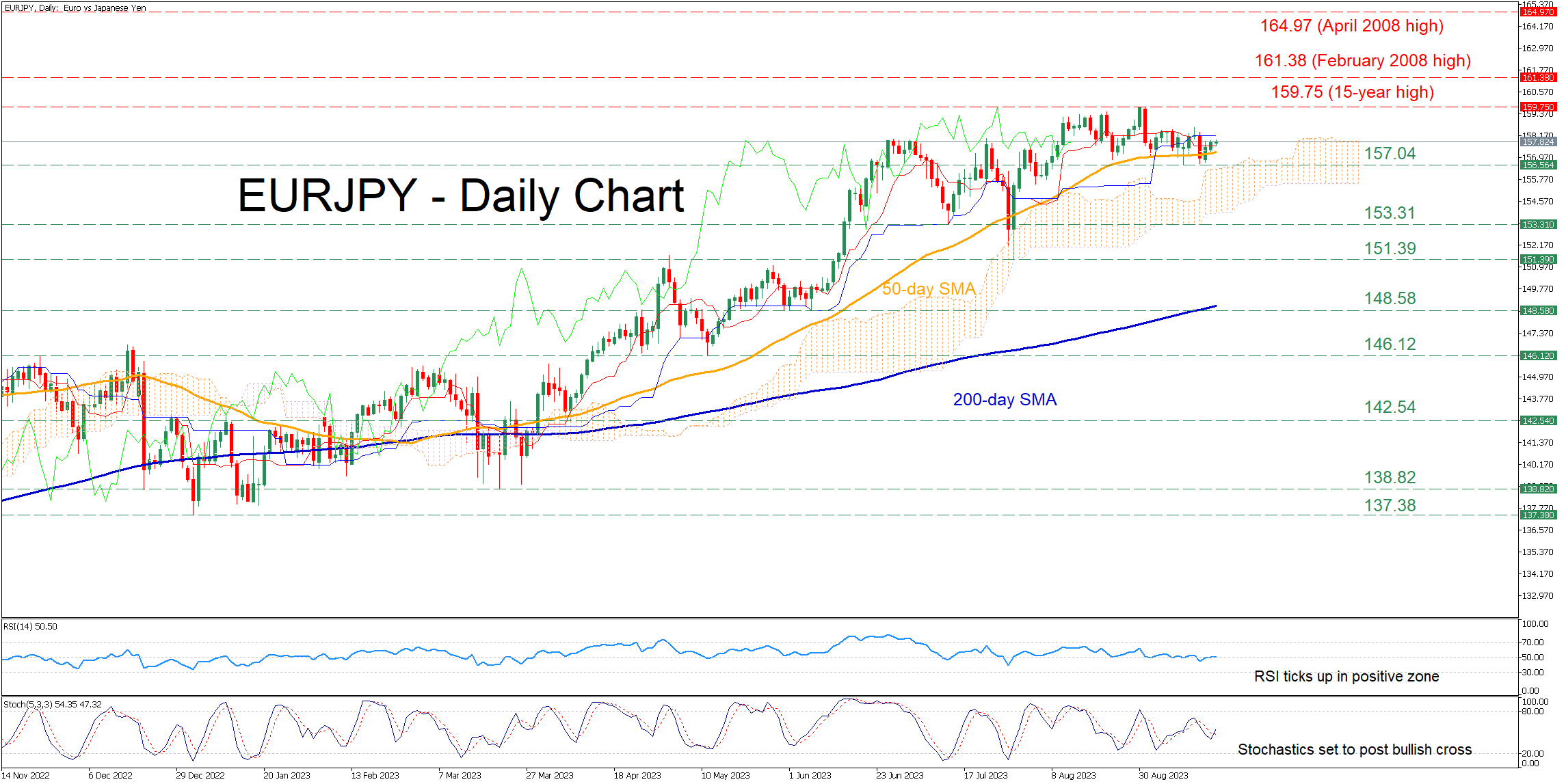

EURJPY Stabilises a Tad Below 15-Year Highs

- EURJPY stuck in a tight range during September

- Hovers just below 15-year peaks supported by 50-day SMA

- Momentum indicators tilt to the bullish side

EURJPY has been in a prolonged uptrend since the beginning of the year, posting a fresh 15-year peak of 159.75 on August 31. Since then, the price has been trading without a clear direction around the 158.00 handle, while the short-term oscillators are reflecting a neutral-to-positive near-term bias.

If the sideways pattern breaks to the upside, the bulls might aim at the 15-year high of 159.75. Jumping above that zone, the pair could storm to fresh multi-year highs, where the February 2008 peak of 161.38 may curb further advances. Failing to halt there, the price might then ascend to challenge the April 2008 high of 164.97.

On the flipside, should the pair cross below the 50-day simple moving average (SMA), immediate support could be found at 157.04, which held strong twice in September. A violation of that zone could trigger a retreat towards 153.31. Even lower, the July bottom of 151.39 may prove to be a tough hurdle for the bears to overcome.

In brief, EURJPY has been silent for the past couple of weeks, appearing to be lacking directional impetus. Given that the short-term oscillators are indicating intensifying buying interest, can the pair revisit its recent multi-year highs?

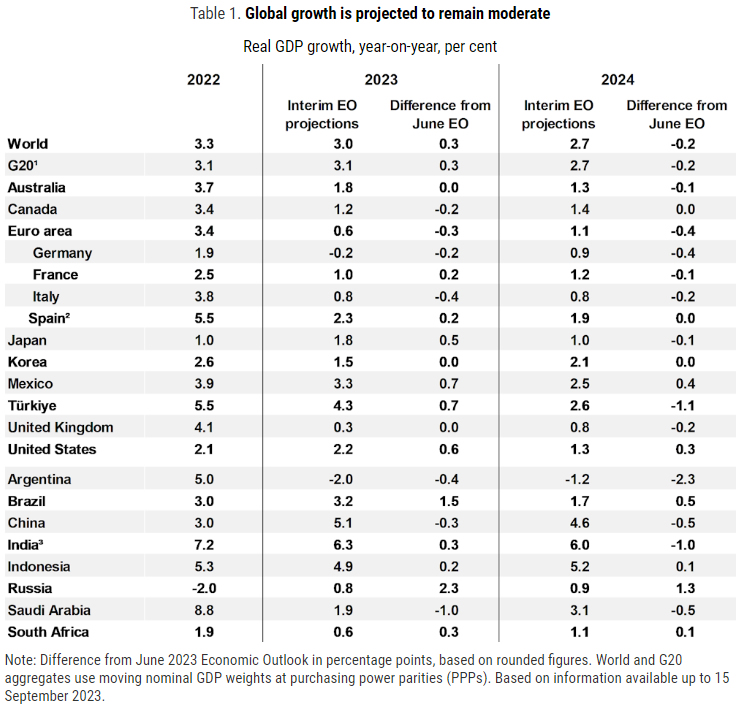

OECD downgrades 2024 global growth, interest rate close to current levels into 2024

The latest OECD Interim Economic Outlook has revealed revised global growth forecasts, with an incremental uptick for 2023 followed by a slight dip in 2024. The updated predictions reflect a blend of uplifted expectations for some economies and dampened hopes for others, amidst a backdrop of inflation concerns and the repercussions of a more sluggish recovery in China.

For 2023, the global economic growth forecast now stands at 3.0%, marking a 0.3% increase from previous predictions. Conversely, projections for 2024 have seen a decrease of -0.2%, bringing the anticipated growth down to 2.7%.

Dissecting the outlook on a regional basis unveils a mixed bag of prospects:

- US: A positive revision with growth estimates standing at 2.2% for 2023, up by 0.6%, and a 1.3% prediction for 2024, reflecting a 0.3% increase.

- Eurozone: Here the expectations have been trimmed down with 2023 forecasts reduced by -0.3% to a mere 0.5%, and a 2024 estimate of 1.1%, down by -0.4%.

- Japan: The outlook for 2023 appears brighter with a 0.5% increase to 1.8%, although the 2024 forecast has been slightly reduced by -0.1%, standing at 1.0%.

- China: Forecasts have been negatively revised to 4.1% in 2023, a drop of -0.3%, and 4.6% in 2024, reflecting a decrease of -0.5%.

The OECD outlook points out considerable downside risks, emphasizing potential persistency in inflation accompanied by potential disruptions in the food and energy markets. Slowdown in China's economy stands as a prominent concern, with ripple effects expected to diminish growth in global trading partners and possibly undercut business confidence universally.

Projections for headline inflation in G20 nations indicate a gradual decrease through 2023, moving from 7.8% in 2022 to 6.0% in 2023, and further dwindling to 4.8% in 2024. However, core inflation, primarily fueled by the services sector and relatively taut labour markets, is predicted to linger, necessitating a sustained restrictive posture in monetary policy across several countries.

As economies globally grapple with these changing dynamics, the emphasis remains on steering a cautious course, with a keen eye on inflation patterns as a decisive factor in shaping future policy directions. The evolving economic narrative dictates a necessity for many countries to maintain interest rates close to their present markers, extending well into 2024.

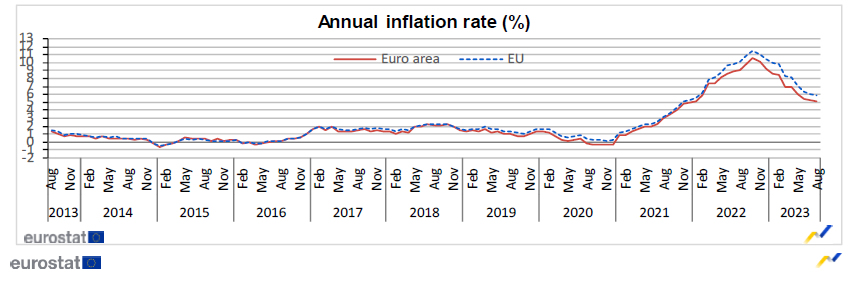

Eurozone CPI finalized at 5.2% in Aug, core CPI at 5.3%

Eurozone CPI was finalized at 5.2% yoy in August, down from 5.3% yoy in July. CPI core (all-items ex-energy, food, alcohol & tobacco) was finalized at 5.3% yoy, down from 5.5% yoy in July. Services prices slowed from 5.6% yoy to 5.5% yoy. Energy prices rose from -6.1% yoy to -3.3% yoy.

EU CPI was finalized at 5.9% yoy, down from 6.1% yoy in July. The lowest annual rates were registered in Denmark (2.3%), Spain and Belgium (both 2.4%). The highest annual rates were recorded in Hungary (14.2%), Czechia (10.1%) and Slovakia (9.6%). Compared with July, annual inflation fell in fifteen Member States, remained stable in one and rose in eleven.

Markets Cautious Ahead Of Central Bank Decisions

Investors will likely remain cautious ahead of a week packed with key data and policy decisions from major central banks.

Asian shares declined on Tuesday as concerns about the Chinese property sector hit risk appetite. This negative sentiment, coupled with overall caution was reflected in European markets this morning. In the currency space, the dollar is drawing some support from the tense mood while in the commodity arena, Brent touched $95 and gold retreated from a two-week high.

Fed decision in focus

The Federal Reserve is widely expected to leave interest rates unchanged at 5.25 - 5.50% at this week’s meeting. However, much focus will be on what clues the economic projections, dot plots, and Jerome Powell's press conference offer on future rate hikes. The key question is whether the updated dot plot will still forecast one more 25-basis point rate hike this year. As of writing, traders are currently pricing in a 32% probability of a 25-basis point hike by November with this jumping to 47% by December.

Currency spotlight – GBPUSD

It could be especially volatile for GBPUSD which has to contend with the Fed/UK CPI/BoE combo over the space of 30 hours.

The day before the BoE decision, the latest UK inflation figures will be published with economists forecasting CPI to rise 7.0%, up from the July print of 6.8%. Core inflation is projected to cool 6.8% year-on-year, down from 6.9% in the previous month.

Markets widely expect the BoE to raise interest rates by 25-basis points, marking the 15th straight hike and taking the key rate to 5.5%. The main question is whether this will be the final rate hike as policymakers weigh sticky inflation against stagnant economic growth.

Talking technicals, GBPUSD remains under pressure on the daily charts with 1.2430 acting as a key level of interest.