Sample Category Title

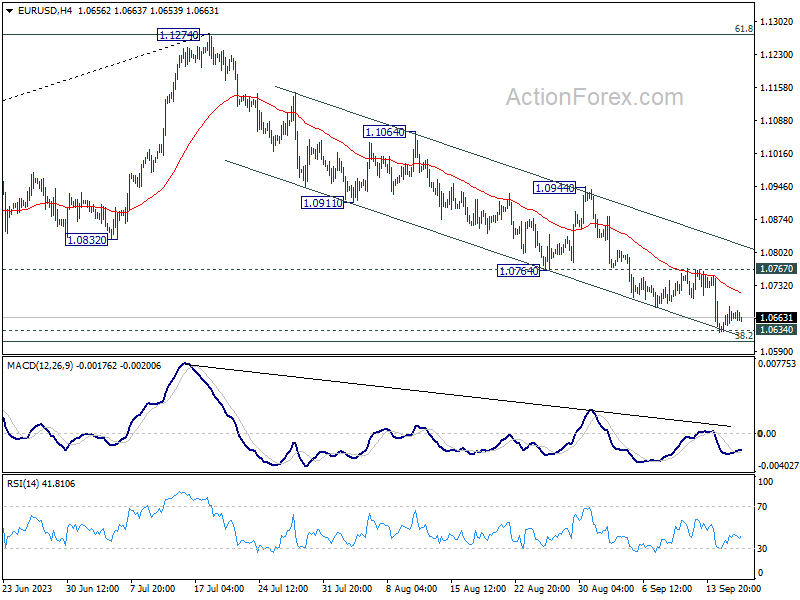

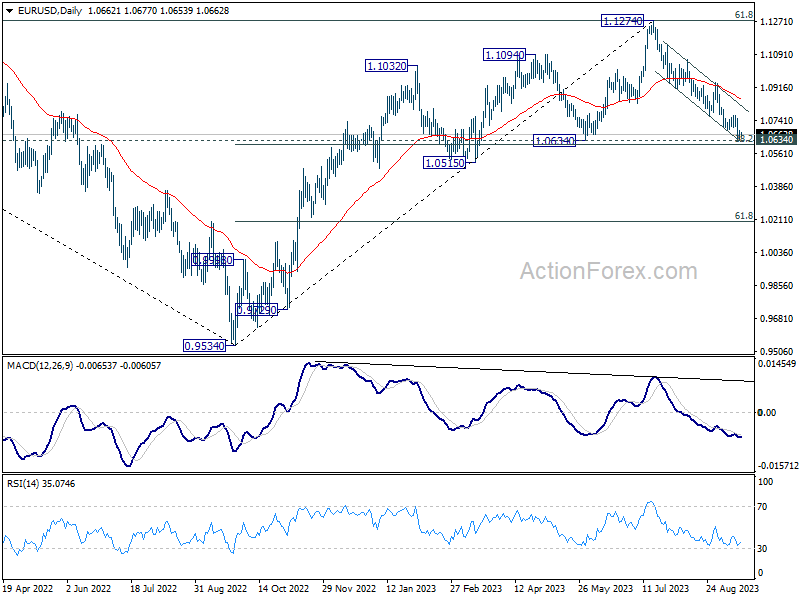

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0633; (P) 1.0660; (R1) 1.0688; More...

Outlook in EUR/USD is unchanged and intraday bias stays neutral. Strong rebound from current level, followed by break of 1.0767 resistance, should confirm short term bottoming. Intraday bias will be back on the upside for 1.0944 resistance. However, sustained break of 1.0609/34 support zone will carry larger bearish implication, and target 1.0515 support next.

In the bigger picture, fall from 1.1274 medium term top is seen as a correction to up trend from 0.9534 (2022 low). Strong support could be seen from 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609) to bring rebound, at least on first attempt. However, sustained break of 1.0609/0634 will raise the chance of bearish trend reversal, and target 61.8% retracement at 1.0199.

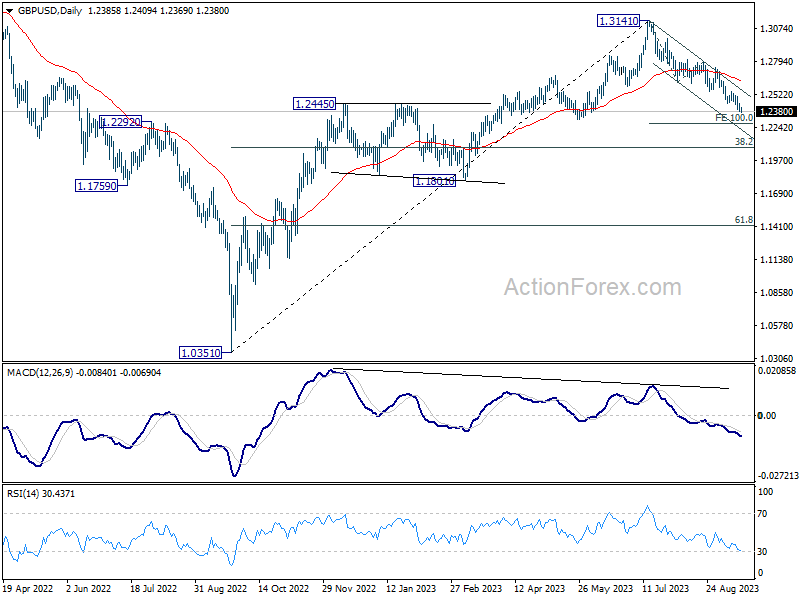

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2359; (P) 1.2402; (R1) 1.2426; More...

No change in GBP/USD's outlook as fall from 1.3141 is extending today. Intraday bias remains on the downside for 100% projection of 1.3141 to 1.2618 from 1.2799 at 1.2276. On the upside, though, firm break of 1.2547 resistance will now indicate short term bottoming, and bring stronger rebound.

In the bigger picture, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. However, sustained break of 1.2075 will raise the chance of bearish trend reversal.

Markets Steady as Traders Await Insights from RBA’s Meeting Minutes

In today's rather subdued trading sessions, most of the movements in the financial markets are limited. European indexes are somewhat in red, albeit with contained losses for the time being. Meanwhile, yields in US and Europe have experienced a minor increase. In the currency sphere, Sterling is mildly weaker, closely followed by Dollar and Euro. Conversely, Canadian Dollar is showing strength, with Yen and Kiwi Dollar tailing not far behind.

As we look forward to the upcoming Asian session, all eyes are on Australian Dollar, gearing up to be the focal point. This heightened attention comes as RBA plans to publish the minutes of its meeting held on September 5. Remarkably, the meeting marked the third consecutive time RBA chose to maintain the status quo on interest rate.

The financial streets are buzzing with speculation as market participants are split in their expectations; while RBA hasn't definitively closed the door on another rate hike, a segment of the market conjectures that the interest rates have attained their peak. The upcoming minutes are set to offer a deep well of insights, providing a closer look at the discussions held during the meeting — mainly focusing on whether there was serious contemplation on a rate hike, thereby presenting a clearer picture of the likelihood of such a move later.

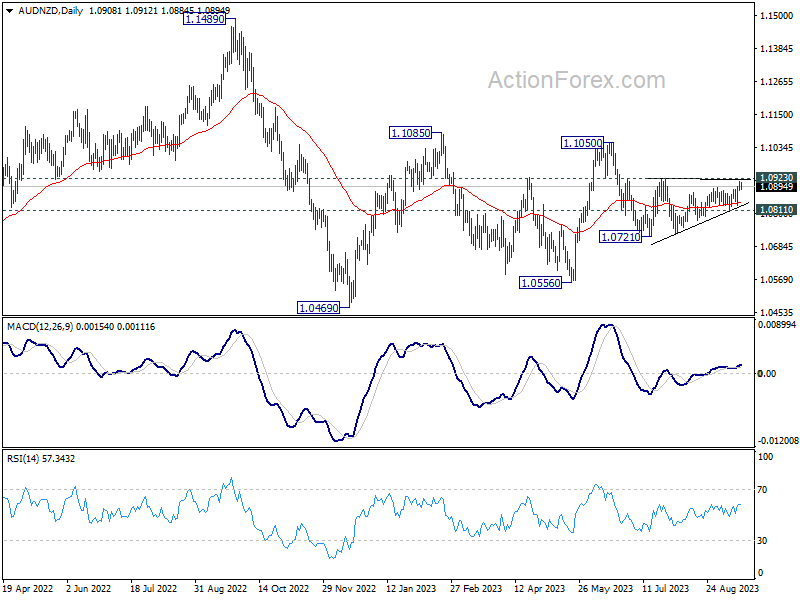

On the technical front, AUD/NZD is seen oscillating in a triangular consolidation pattern since dipping to 1.0721. This pattern hints that the decline from 1.1050 has yet to reach its end. A set of RBA minutes that leans more towards the dovish end of the spectrum could potentially knock down the cross from 1.0923 resistance. Further break of 1.0811 support will argue that AUD/NZD is ready to fall through 1.0721 support towards 1.0056. However, firm break of 1.0923 resistance will dampen this view, and target 1.1050/1.1085 resistance zone instead.

In Europe, at the time of writing, FTSE is down -0.46%. DAX is down -0.82%. CAC is down -1.20%. Germany 10-year yield is up 0.0273 at 2.707, above 2.7 handle. Earlier in Asia, Japan was on holiday. Hong Kong HSI dropped -1.39%. China Shanghai SSE rose 0.26%. Singapore Strait Times dropped -0.53%.

ECB's Kazimir: Cannot rule out further hike, premature to bet on cut

ECB Governing Council member and head of Slovakia's central bank, Peter Kazimir, indicated in an opinion piece that the possibility of further rate hikes remains on the table. Also, it's premature to bet on the timing of the first rate cut.

Kazimir emphasized that the forthcoming March forecast will be a decisive factor in ascertaining whether the inflation target is within reachable limits, stating, "Only the March forecast can confirm that we are heading unequivocally and steadily towards our inflation goal."

"That is why I cannot rule out the possibility of further rate increases today,: he added.

Elaborating on the current stance of the policy rates, Kazimir metaphorically commented, "Assume we're at the top. If so, we may have to stay camping here for quite some time and spend the winter, spring, and summer here."

Hence, it would be "premature to place market bets on when the first interest rate cuts will occur."

Meanwhile, he did leave the door open for potential adjustments in the bank's quantitative tightening measures, contingent on economic data. He noted, "As soon as incoming economic data and analyses confirm that further tightening is unnecessary, I see room for a debate about adjusting the pace of our quantitative tightening."

New Zealand's services sector continues its descent, a deeper dive

New Zealand's BusinessNZ Performance of Services Index reported another slump in August, marking the third consecutive month of declining in the services sector. This downturn saw PSI slip from 48.0 in July to 47.1 in August, notably falling short of long-term average of 53.5.

Looking into the components, while there were marginal improvements in activity/sales, which climbed from 39.7 to 43.4, and employment, which rose from 49.1 to 50.9, other areas did not fare as well. New orders/business made a meager ascent from 44.5 to 47.3. Conversely, stocks/inventories dipped from 54.0 to 52.5, and supplier deliveries took a hit, declining from 52.0 to 49.2.

BusinessNZ's Chief Executive, Kirk Hope, offered a bleak perspective, highlighting that August's data provided little hope for a swift recovery.

This sentiment was further cemented by the proportion of negative comments received in the survey. In August, 63.9% of the comments were negative, a slight improvement from July's 67% but a significant jump from June's 55.6%. The cloud of uncertainty hanging over the upcoming General Election, combined with persisting challenging economic conditions, were predominant themes among these comments.

BNZ's Senior Economist Doug Steel noted that the PSI and PMI results resonate with RBNZ's projections of an impending recession rather than Treasury's more optimistic forecast of sustained, albeit moderate, growth in the near future.

NZ economic growth to remain subdued according to NZIER forecasts

Latest forecasts from New Zealand Institute of Economic Research anticipate a period of subdued economic growth over the next few years. The annual average GDP growth is expected to decline to 0.4% in the fiscal year ending March 2024, followed by modest growth of 1.1% in 2025.

This sluggish pace is partly attributable to the ripple effect of consecutive hikes in RBNZ's OCR, currently standing at 5.50%, which have started to curb demand in the broader economy. Moreover, diminishing demand for exports, spurred mainly by China's weaker growth outlook, poses downside risk to the nation's economic vitality.

Shifting focus to inflation sphere, there has been a notable upward revision for the projections as of March 2024, with annual CPI inflation predicted to retreat to 4.3% in 2024, and further dip to 2.4% in the subsequent year.

As for currency outlook, NZD Trade Weighted Index forecasts have undergone revisions, showing a downturn for the approaching year but portraying an uplift in 2025.

NZD has not encountered significant fluctuations against other currencies in recent times in terms of yield attractiveness. This steadiness, however, is anticipated to meet challenges due to reduced export demand from China.

The forecast encapsulates expectation of NZD TWI oscillating between 70.8 and 71.6 in the period spanning 2024 to 2027.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2359; (P) 1.2402; (R1) 1.2426; More...

No change in GBP/USD's outlook as fall from 1.3141 is extending today. Intraday bias remains on the downside for 100% projection of 1.3141 to 1.2618 from 1.2799 at 1.2276. On the upside, though, firm break of 1.2547 resistance will now indicate short term bottoming, and bring stronger rebound.

In the bigger picture, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. However, sustained break of 1.2075 will raise the chance of bearish trend reversal.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Aug | 47.1 | 47.8 | 48 | |

| 23:01 | GBP | Rightmove House Price Index M/M Sep | 0.40% | -1.90% | ||

| 12:15 | CAD | Housing Starts Aug | 253K | 257K | 255K | |

| 12:30 | CAD | Industrial Product Price M/M Aug | 1.30% | 0.50% | 0.40% | |

| 12:30 | CAD | Raw Material Price Index Aug | 3.00% | 3.80% | 3.50% | |

| 14:00 | USD | NAHB Housing Market Index Sep | 50 | 50 |

ECB’s Kazimir: Cannot rule out further hike, premature to bet on cut

ECB Governing Council member and head of Slovakia's central bank, Peter Kazimir, indicated in an opinion piece that the possibility of further rate hikes remains on the table. Also, it's premature to bet on the timing of the first rate cut.

Kazimir emphasized that the forthcoming March forecast will be a decisive factor in ascertaining whether the inflation target is within reachable limits, stating, "Only the March forecast can confirm that we are heading unequivocally and steadily towards our inflation goal."

"That is why I cannot rule out the possibility of further rate increases today,: he added.

Elaborating on the current stance of the policy rates, Kazimir metaphorically commented, "Assume we're at the top. If so, we may have to stay camping here for quite some time and spend the winter, spring, and summer here."

Hence, it would be "premature to place market bets on when the first interest rate cuts will occur."

Meanwhile, he did leave the door open for potential adjustments in the bank's quantitative tightening measures, contingent on economic data. He noted, "As soon as incoming economic data and analyses confirm that further tightening is unnecessary, I see room for a debate about adjusting the pace of our quantitative tightening."

Bank of England Preview: Peak Approaching – GBP Headwinds to Set In

- We expect the Bank of England (BoE) to hike the Bank Rate by 25bp on 21 September, although august inflation released the day before marks a joker.

- We expect a peak in the Bank Rate of 5.50%. We see current market pricing of a peak in the policy rate of 5.60% as broadly fair.

- EUR/GBP is set to end the day higher on dovish commentary.

BoE call. We expect the Bank of England (BoE) to hike the Bank Rate (key policy rate) by 25bp on 21 September, bringing it to 5.50%. We expect the vote split to be 8-1 favouring a 25bp hike over keeping the Bank Rate unchanged. Markets are currently pricing around 18bp for the meeting this week. Note, there will be no updated projections at this meeting nor a press conference following the announcement.

While forward guidance is likely to be limited, we expect the MPC to strike a dovish tone indicating that a peak in the Bank Rate is near if not already reached by Thursday. Likewise, we expect the MPC to repeat that "current monetary policy stance is restrictive" and that they "will ensure that Bank Rate is sufficiently restrictive for sufficiently long". The final point has recently been reiterated by several MPC members, with prominently BoE's chief economist Pill recently stating that he prefers a "table mountain" approach, where rates are held steady for longer.

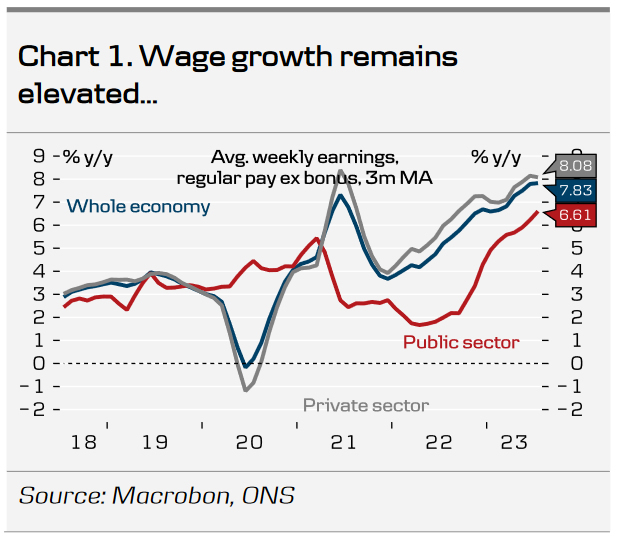

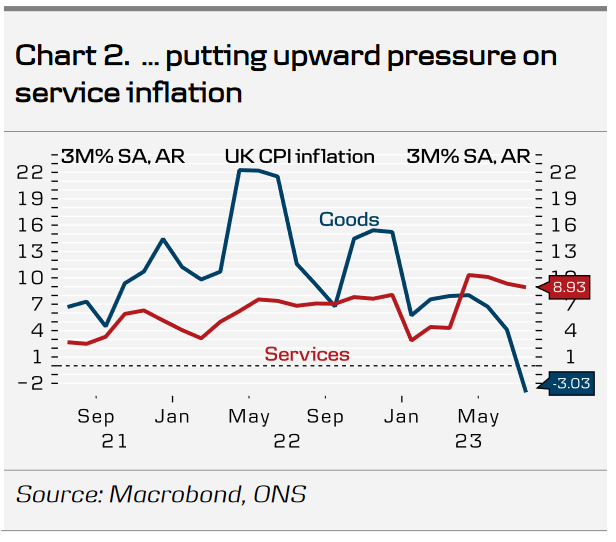

Since the last monetary policy decision in August, data releases have been mixed. The unemployment rate increased to 4.3% in July and unfilled vacancies continued to decline indicating some rising slack in the labour market. Likewise, the REC/KPMG report showed the steepest decline in permanent placements in over three years. PMIs for August surprised to the downside and pointed to growth weakening further in the months ahead with both composite and service indices falling below 50 at 48.6 and 49.5, respectively. That said, wage growth remains elevated with wage growth excl. bonuses at 7.8% 3M/YoY. Pay growth in the private sector slowed marginally suggesting a peak might be near. With wages being the largest input cost factor in the service sector and therefore highly determining for service inflation, the continued high wage growth favours another increase in the Bank Rate. Although inflation figures for August will not be published until the day before the rate announcement, the July figures exceeded expectations for both headline and core inflation with most notably service inflation reaccelerating (see chart 2).

We maintain our call that a 25bp hike at the upcoming meeting will mark the final hike of this hiking cycle and see the Bank Rate peaking at 5.50%. This is broadly in line with current market pricing. We expect no rate cuts until 2024. As pre-warned in the August monetary policy report the MPC will present a target for gilt stock reduction over the coming 12-month period.

FX. In our base case of a 25bp hike, we expect EUR/GBP to end the day higher on dovish commentary. We anticipate the statement to strike a dovish tone, noting that monetary policy is restrictive while reiterating the BoE's data dependent approach. We expect the BoE to highlight that elevated wage growth and service inflation remain the upside risks. We continue to forecast EUR/GBP to move modestly higher the coming year to 0.88 on the UK economy performing relatively worse than the euro area.

Fed Set to Skip a September Hike, But Will It Flag One for November?

- Fed expected to pause again in September

- But will it signal that it is done with rate hikes?

- Risks for the dollar are symmetrical heading into the meeting

- Decision is expected at 18:00 GMT on Wednesday

A pause with strings attached?

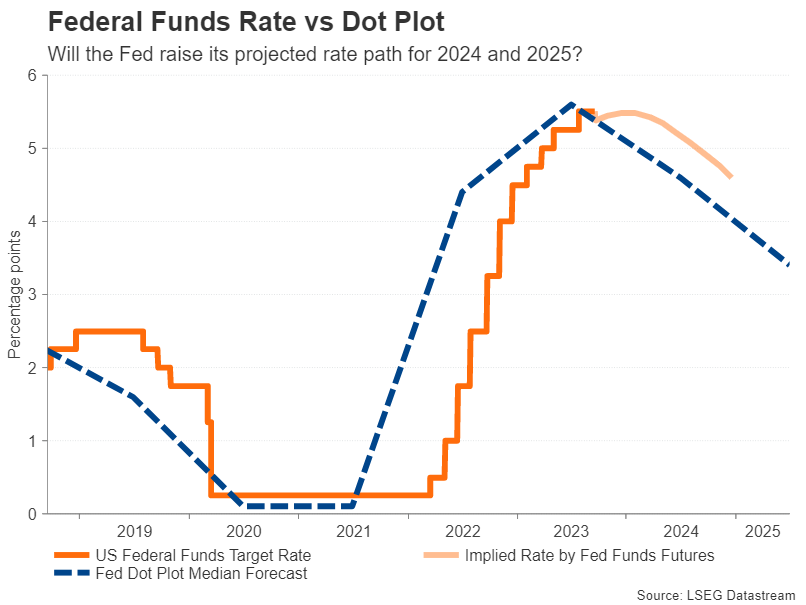

The Federal Reserve is widely anticipated to keep interest rates unchanged at its September meeting but what investors are more anxious to find out is whether policymakers will keep the door open to further hikes. The other big discussion point is about the rate path in 2024, specifically, if the median dot plot will be revised higher.

The US economy continues to perform well by most measures even if there are signs of some cooling off, particularly in the tight labour market. With recession odds being slashed and a soft landing looking more attainable, inflation is once again the primary concern for investors and policymakers as how quickly it falls from hereon will determine how soon the Fed can begin cutting rates.

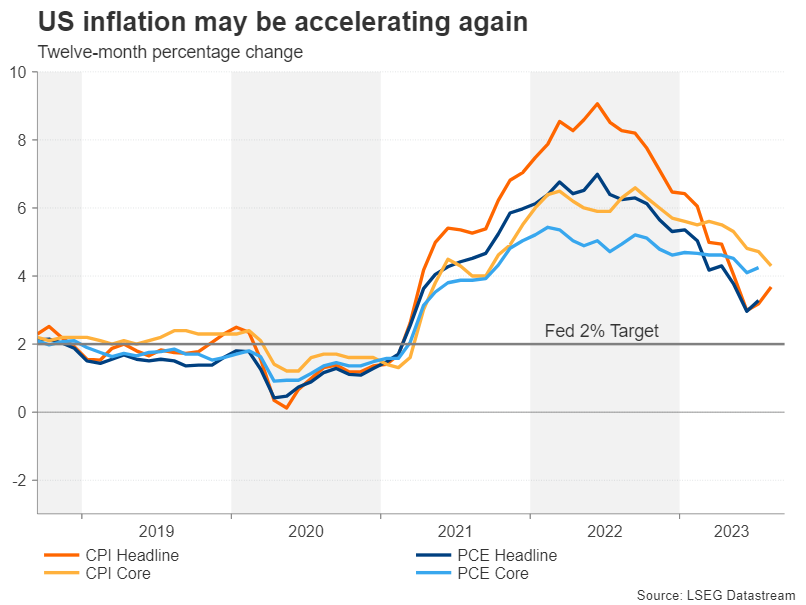

Inflation is creeping up again

Looking at the latest CPI numbers, it’s fair to say that there’s been a bit of a setback in the progress lately. The annual rate of CPI has quickened from 3.0% to 3.7% over the past two months. That trend could continue if oil prices maintain their ascent. However, most investors are looking through this latest increase, hoping that it will be temporary, and focusing on the decline in core CPI for clues as to what the Fed will do next.

Another striking datapoint that markets are not overreacting to is the big jump in consumption over the summer, which was likely boosted by one-off factors that are expected to fade in the final months of 2023. One might therefore deduce that this leaves the Fed in a neutral position as far as the outlook is concerned and a pause in September and beyond is justified.

Fed is fearful of overtightening

However, there are two significant unknowns here. One is the extent of the effects from the existing tightening that haven’t been felt yet. The other is whether energy prices will rally further, making inflation even stickier than it already is.

The Fed has become very mindful of the transmission lag of policy tightening during the course of 2023, downshifting the pace of rate increases contrary to data suggesting otherwise. The policy lag has been the main argument of the more dovish leaning FOMC members. Chair Jerome Powell falls into this camp.

But with real interest rates turning positive as all inflation metrics drop below 5% and the Fed funds rate reaches the 5.25%-5.50% range, the hawks are also increasingly confident that policy is restrictive enough. Thus, regardless of whether the Fed hikes one more time or not this year, the end of tightening is just around the corner.

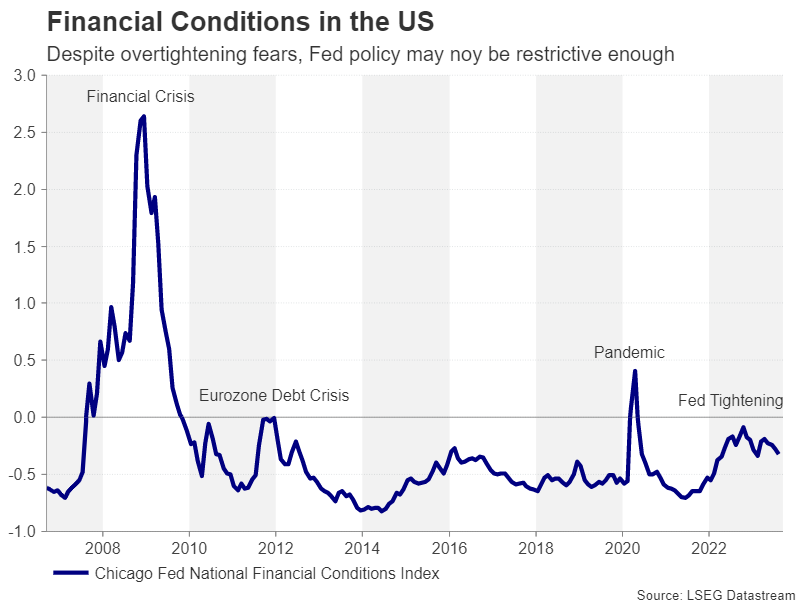

Will new dot plot embrace higher for longer?

The question now is if the economy will slow at an alarming enough pace to trigger a wave of rate cuts. Some indicators, such as the Chicago Fed’s National Financial Conditions Index imply that financial conditions may not be tight enough. This raises the possibility of a resumption of rate hikes at some point in the future, even without a fresh acceleration in energy prices. At the very least, there remains a strong case for ‘higher for longer’.

However, markets have yet to be convinced as traders have about a 90-basis-point worth of rate cuts priced in. A pricing out of those cuts would not happen overnight and is potentially more of a 2024 story, but the process could start this week if FOMC members revise up their median projection of where they see rates in the next couple of years.

In the June dot plot, the median projection for 2024 was 4.6% and for 2025 it was 3.4%. If the Fed sees rates a lot higher in 2024 in the updated dot plot than in June, this would add more fuel to the US dollar’s latest uptrend.

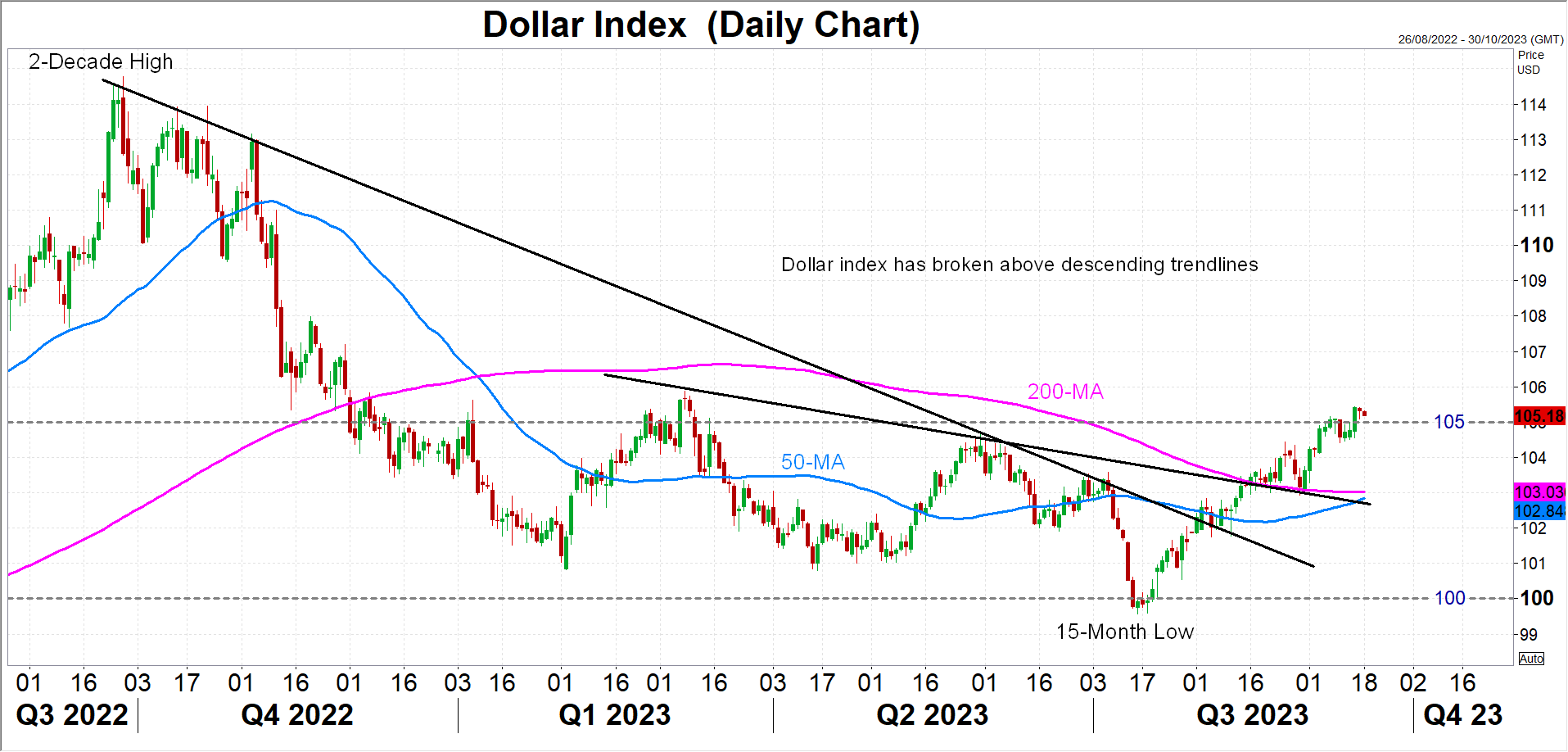

Dollar’s bullish streak may not be over

Sending a clear signal on higher for longer would be one way for the Fed to possibly compensate for not committing to a final rate hike this year. The recent data has been neither too strong nor too soft, so keeping the option for a further rate rise on the table without pre-committing to it seems like a sensible middle-of-the-road approach.

For the dollar, the most bullish outcome is if the Fed hints at a good chance for another hike as well as raises its projected rate path. This could push the dollar index past the March peak of 105.88, extending its winning streak.

However, the recent rally also exposes the greenback to a corrective selloff should the rate path not be revised up substantially, if at all, and Powell sounds upbeat on the prospect of inflation returning to the 2% target over the medium term in his press conference. The dollar index would be at risk of tumbling towards its 200-day moving average around 103.00 in such a scenario.

AUD/USD Eyes RBA Minutes

The Australian dollar continues to drift as we start the new trading week. In Monday’s European session, AUD/USD is trading at 0.6438, up 0.11%.

The Reserve Bank of Australia releases its minutes of this month’s meeting. The RBA extended a pause in rates for a third month, holding the official cash rate at 4.10%. This was ex-Governor Philip Lowe’s final meeting. Lowe noted that “passed its peak” but was “still too high and will remain so for some time yet”, as he kept the door open to further rate hikes. The markets are more dovish and are looking ahead to the RBA trimming rates sometime in 2024. Investors will be looking for clues in the minutes with regard to future rate moves.

Michelle Bullock takes over today as the new Governor of the RBA. Bullock is not expected to make any major policy shifts and has stated that the upcoming rate decisions will be data-dependent. The new governor will have her hands full with implementing major changes at the bank, after a government committee urged an overhaul at the central bank which is intended to streamline the Bank’s activities and create greater transparency.

The US ended last week on a mixed note. The Empire State Manufacturing Index surprised to the upside, jumping to 1.9 in September from -19 in August, above the market consensus of -10. The UoM consumer sentiment index slowed to 67.7 in September, down from 69.5 in August and shy of the market consensus of 69.1 points. Inflation Expectations fell to 3.1% in August, down from 3.5% in July and the lowest level since March 2021. This is another sign that inflation is weakening and supports a pause at the Federal Reserve meeting on Wednesday. The markets have priced in a pause at 99%, according to the CME FedWatch tool, up from 92% one week ago.

AUD/USD Technical

- AUD/USD tested support at 0.6428 earlier. The next support line is 0.6381

- 0.6477 and 0.6524 are the next resistance lines

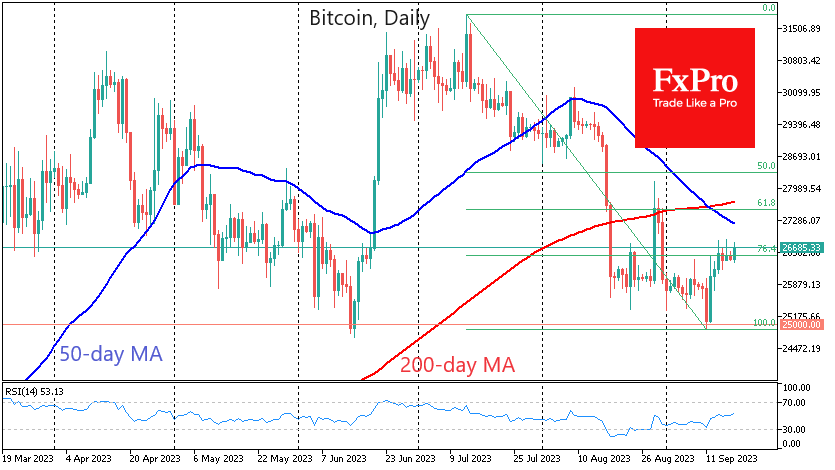

Bitcoin Has Not Yet Reached Resistance

Market picture

The crypto market gained around 3% last week, taking its capitalisation to $1.06 trillion – the highest since late August. The market dip at the start of the previous week has fuelled buyers’ appetite.

But we are also seeing interest in crypto, in contrast to the sell-off in tech giants. We saw something similar in the spring as capital fled regional banks in the US. Isn’t it a sign that something is brewing in the banking sector again?

Trading at $26.5K, Bitcoin has recovered to 76.4% of the decline from the July peak to the September trough. Recent optimism shows that we could see a classical correction to 61.8%, near $27.5K. The 200-day moving average and the late August peak area are concentrated near that level. So, the battle for the trend, which has now eased slightly, is set to intensify.

News background

Bitfinex said investors withdrew $55 billion from the crypto market last month. August was the worst month for Bitcoin since November 2022.

The SEC has asked the court to unseal confidential documents in its case against Binance, Binance.US and CEO Changpeng Zhao. SEC lawyers argue that confidential material in the Binance case significantly delays the litigation and the regulator’s case.

Australian banking group ANZ completed a test transaction with the Australian dollar-backed stablecoin A$DC using Chainlink’s interconnect protocol.

Billionaire Mark Cuban was attacked by hackers who accessed his hot wallet and withdrew $870,000 worth of crypto assets. He said, the attackers infected his computer with a virus and waited patiently for him to log into his MetaMask wallet before they began withdrawing cryptocurrency.

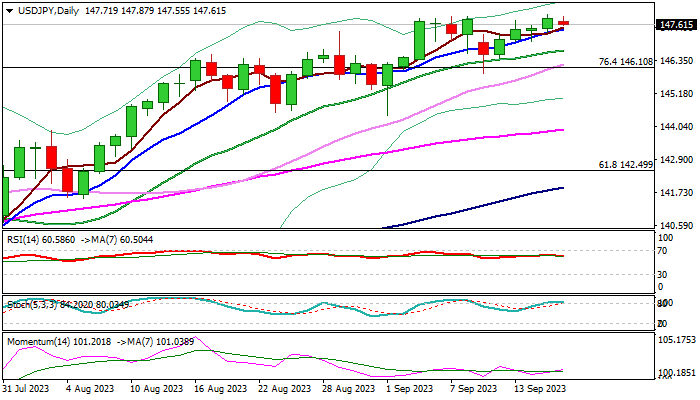

USD/JPY: Bulls Hold Grip Ahead of Fed and BOJ Policy Meetings

USDJPY keeps firm tone and holds within a narrow range just under new multi-month highs (147.87/95) in European trading on Monday.

Today’s quiet mode is mainly due to lower volumes as Japan is shut for holidays, while traders became more cautious ahead of two key events this week – US Federal Reserve and Bank of Japan policy meetings.

The Fed will end its two-day meeting on Thursday and BOJ meets on Friday, with both central banks widely expected to stay on hold this time, though surprises cannot be ruled out, especially after recent comments from BOJ governor who mentioned possible earlier than expected start of tightening monetary policy.

Markets are likely to face increased volatility this week, with focus on comments from FOMC, in light of recent solid economic data, which partially ease pressure on Fed and BOJ’s guidance about the conditions required to start reversing current negative policy.

Technical structure is positive and reinforced by four consecutive weekly closes above former pivotal resistance, now reverted to strong support at 146.10 (Fibo 76.4% of 151.94/127.22) as well as strong bullish momentum.

Near-term bias is expected to remain with bulls while the action stays above 146.10 and keep in play hopes of final push towards psychological 150 barrier (last time tested in mid-October 2022).

Caution on break below 146.10 which would risk deeper pullback and.

Res: 148.00; 148.59; 148.84; 149.70.

Sup: 147.16; 146.10; 145.06; 144.44.

Gold Challenges Crucial Downward Sloping Trendline

- Gold in a congested technical territory, capped by 50-day SMA

- A decisive close above the trendline could shift the short-term picture to bullish

- Momentum indicators endorse latest advance

Gold has been edging higher in the past few sessions, rebounding strongly from its drop below the 200-day simple moving average (SMA). Furthermore, the short-term oscillators suggest that bullish forces are strengthening as the price is testing the important trendline that connects its recent lower highs.

Should the buying interest persist, the bulls could attempt to conquer the May low of 1,932, which overlaps with the 50-day SMA. Surpassing that zone, the price may ascend towards the February peak of 1,959. Further advances could then cease at the July high of 1,987.

Alternatively, should bullion reverse back lower, the recent support of 1,901 could act as the first line of defense. A break beneath that zone might set the stage for the June low of 1,893. Even lower, the five-month bottom of 1,884 may provide downside protection.

In brief, gold marched towards the congested region that includes the descending trendline and its 50-day SMA. Looking forward, a clear jump above both obstacles is needed to turn the technical outlook back to bullish.