Sample Category Title

WTI oil eyes critical resistance zone at 90 amid supply constraints

Oil prices climbed to their highest level in 10 months today, as robust demand coupled with supply restrictions imposed by the top members of OPEC+ significantly tightened global fuel markets. WTI crude oil is now facing an important resistance zone at 90.

OPEC's Monthly Oil Market Report underscored a looming supply crunch that threatens to eclipse anything seen in over a decade, indicating a daily shortfall exceeding 3 million barrels. On the other hand, OPEC maintained its upbeat forecasts of daily global oil demand increase of 2.25m barrels in 2024, just slightly less than growth of 2.44m barrels expected in 2023.

Technically, WTI crude oil is now heading very close to an important resistance around 90 psychological level, with 38.2% retracement of 131.82 to 63.67 at 89.70. Decisive break of level raise the chance that the rally from 63.67 is developing into a more sustainable medium term up trend. Next target would be 100% projection of 66.94 to 84.91 from 77.95 at 95.20. Meanwhile, outlook will only be neutral at worst as long as 84.91 resistance turned support holds, even in case of rejection by 90.

XAU/USD: Gold Loses Ground ahead of US Inflation Report

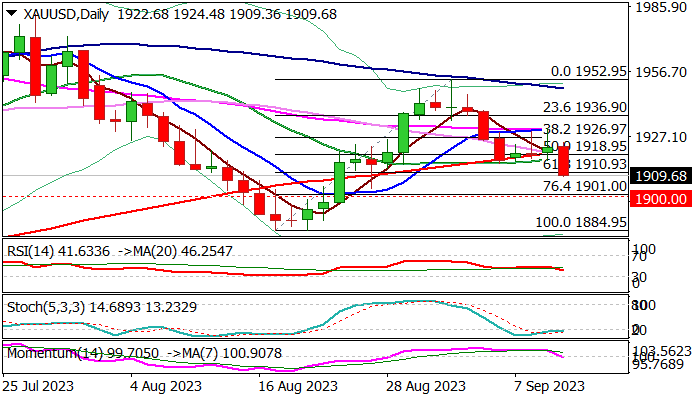

Gold price fell on Tuesday, hitting the lowest in more than two weeks, pressured by fresh strength of dollar, just a day ahead of this week’s key event – US inflation report for August.

Inflation in the US is likely to rise in August, due to higher energy prices, which would partially offset wide expectations that the Fed is done with interest rates for this year.

US CPI numbers are expected to strongly contribute to the US central bank’s rate trajectory in the near future, with values above expectations to revive dollar bids and make the yellow metal less attractive for investors.

Economists expect annualized inflation to rise to 3.6% in August from 3.2% previous month, while core CPI, which excludes volatile food and energy components is expected to drop to 4.3% from 4.7% in July.

Markets remain highly concerned about still strongly elevated core inflation and remain cautious that the Fed may opt for continuation of its tightening cycle.

Structure on daily chart is weakening as fresh weakness eventually broke below 200DMA (1919) and signals an end of three-day consolidation, shifting near-term focus lower.

Falling 14-d momentum is about to break into negative territory and MA’s turned to full bearish setup, adding to downside risk.

Close below 200DMA (also Fibo 50% of $1884/$1982 upleg) to boost negative signal and open way towards psychological $1900 level and key support at $1884 (Aug 17 low).

Res: 1930; 1938; 1940; 1948.

Sup: 1910; 1900; 1884; 1872.

Australian Dollar Dips on Soft Consumer Confidence

- Australia’s consumer confidence falls sharply

- Australia’s business conditions improve

- Markets eye US inflation report on Wednesday

The Australian dollar has edged lower on Tuesday after starting the week with massive gains. In the North American session, AUD/USD is trading at 0.6412, down 0.28%.

Australia’s consumer confidence slides

Australian consumers are in a sour mood, as they feel the squeeze of high interest rates and stubborn inflation, which has led to heavily-debted households. The Westpac Consumer Sentiment Index fell by 1.5% in September to 79.7, following a decline of 0.4% in August. This missed the consensus estimate of 0.6%. Consumer sentiment remains at its lowest levels since 2020, during the Covid pandemic.

The corporate sector is showing more confidence than consumers, as businesses have shown stronger resilience to higher rates and increasing inflationary pressures than consumers. NAB Business Conditions climbed to 13 in August, up from 11, while business confidence remained at 2 points, indicative of slight optimism.

The Australian dollar roared out of the gates on Monday, gaining 0.85%. The driver of the uptick was China’s August inflation release. CPI rose 0.1% y/y, after a surprise decline of 0.3% in July. China’s slowdown has raised alarm bells about the impact it will have on global growth, and the Asian giant is Australia’s number one trading partner. The Aussie is sensitive to economic developments in China, as we saw on Monday, and China’s Industrial Production, which will be released on Friday, could be a market-mover for the Aussie.

Next week features a host of central bank meetings, and one of the most closely watched will be the Federal Reserve meeting on September 20th. Jerome Powell has broadcast loud and clear that the battle against inflation isn’t over and rate hikes remain on the table, but are the markets paying attention? Investors have priced in a pause in September at 93% and are talking about rate hikes in 2024.

The US releases the August inflation report on Wednesday, which is unlikely to change expectations about a September hold, although the inflation release could have an impact on the Fed’s rate path for the final quarter of the year.

AUD/USD Technical

- AUD/USD is putting strong pressure on support at 0.6405. Below, there is support at 0.6330

- There is resistance at 0.6453 and 0.6528

Sunset Market Commentary

Markets

This morning’s UK labour market report had the potential to sway markets in one direction or the other in the long run-up to next Thursday’s Bank of England policy meeting. Only … it didn’t. Employment growth in the three months through July fell by 207k, more than the -195k expected. A preliminary gauge for August (-1k) missed the bar (+30k) as well. The unemployment rate meanwhile ticked up to 4.3%, a historically low level still but nonetheless the highest since 2021. Wage growth, however, hit a record high - barring a surge driven by base effects in 2021 - since data collection began early 2001. Average weekly earnings rose by 8.5% in the three months through July. That’s up from 8.4% in June. Excluding for bonuses, employees saw wages rise by 7.8% (unchanged vs. June). All in all a mixed report that markets did little with. A speech by the Bank of England’s deputy governor nominee Breeden couldn’t inspire either. She said the MPC would have to balance “the risk of inflation becoming embedded and more persistent” against the already delivered amount of monetary tightening, much of which that has yet to filter through to the economy. In this respect, she doesn’t expect a UK recession but GDP is probably to stay “relatively flat over the next couple of years”. Breeden’s first vote is at the November 2 meeting. Sterling in a first, brief reaction to the higher wage growth appreciated against the euro. Those gains evaporated as quickly as they came though. EUR/GBP is currently changing hands in the high 0.858 area, a tad higher than yesterday’s close. UK gilts do outperform global peers. Yields dropped straight at the open and currently lose between 3.8-7.6 bps. The 2-y yield tries to hold north of 5%. UK money markets reckon the BoE will hike once more to 5.5%, if not next week then at the November meeting. A second, final 25 bps move hangs in the air in a 50-50 split.

Tomorrow’s US CPI numbers and Thursday’s cliff-edge ECB decision is keeping investors in core areas at the edge of their seat. Both US Treasuries and German Bunds barely budge, resulting in minimal yield changes. US rates add 1.5 bps at the front while easing 0.3 bps at the 30-y. German yield changes range between -1.2 and +2.2 bps in a similar curve shift. The dollar gains against all G10 peers, recouping some or all of yesterday’s (contained) losses. EUR/USD went from an intraday high of 1.0769 to 1.071 currently. DXY in a mirror move moved higher towards but below the 105 zone. The yen already forfeits its Ueda-driven modest gains. USD/JPY bounces from 146.59 to 147.14. Brent oil rises further and is set for a close above $91/b after OPEC said that following the output cut extension from the Saudis (and Russia) there will be a supply shortfall of more than 3 million barrels a day next quarter – the biggest deficit in a decade.

News & Views

A business survey by the German Ifo institute shows that residential construction cancellations rose to their highest level since the survey started in 1991. 20.7% of companies reported cancelled projects compared to 18.9% in July. The head of surveys, Wohlrabe, says that as a result of the rapid rise in construction costs and much higher interest rates, many projects that were still profitable in early 2022 are now no longer viable. Not to mention the scaling back of subsidies because of tighter energy regulations, which is also putting a strain on builders’ calculations. 44.2% of participants reported a lack of orders, up from 40.3% in July. At the same time last year, the share was only 13.8%. Some businesses are already struggling to keep their heads above water. Currently, 11.9% of residential construction companies report financing difficulties. That’s the highest proportion for over 30 years.

At an interim meeting, the Hungarian central bank (MNB) further studied possibilities for simplifying the monetary policy toolkit. They decided that excess reserves will be remunerated at the base rate (13%) from October 1st as the gap between (emergency) overnight deposit rates and the base rate is almost closed. In other news, Hungarian finance minister Varga said that his government’s previous GDP growth forecast for this year (1.5%) is too optimistic. He believes that growth will rather end up near 0% as consumer spending gets whacked by inflation. Therefore it is of utmost important that the Hungarian disinflation process continues with single digit inflation expected from November (16.4% Y/Y in August). The forint didn’t respond to today’s news, but overall EUR/HUF remains remarkably stable despite recent underperformance from regional peers (CZK/PLN).

Euro Dips on Soft Confidence Data

- Eurozone ZEW Economic Sentiment worsens

- German ZEW Economic Sentiment improves but remains negative

- ECB rate decision up in the air and could go to the wire

The euro started the week higher but has reversed directions on Tuesday and pared most of those gains. In the North American session, EUR/USD is trading at 1.0709, down 0.38%.

German and eurozone confidence data indicate pessimism

There hasn’t been much to cheer about with regard to German and eurozone data lately, so it’s no surprise that the ZEW Economic Sentiment indexes remain stuck in negative territory. The eurozone ZEW declined to -8.9 in September from -5.5 in August and missed the consensus estimate of -6.2. The news was a bit better in Germany, which improved from -12.3 to -11.4, above the estimate of -15. The outlook is quite gloomy, with inflation relatively high and the ECB contemplating further rate hikes.

The ECB meets on Thursday and it remains unclear what Lagarde & Co. will decide. The markets are split. with a rate hike priced at 45%, which would raise the benchmark cash rate to an even 4.0%. The central bank has been aggressively raising rates, with no pauses in the current tightening cycle. Still, inflation has proven stickier than expected and is currently at 5.3%, nowhere near the ECB’s 2% target. Germany is grappling with an inflation level of 6.2%.

The slowdown in the German and eurozone economies is a strong factor in favour of the ECB taking a pause, as further rate hikes could trigger a recession. ECB hawks argue that inflation has to be contained as priority number one, while the doves counter that weaker growth means inflation will continue to fall on its own and a pause would provide some relief to businesses and households. ECB President Lagarde has a difficult rate decision on her hands and the live decision could mean some volatility for the euro after the rate announcement.

EUR/USD Technical

- EUR/USD is testing support at 1.0732. Below, there is support at 1.0654

- There is resistance at 1.0777 and 1.0855

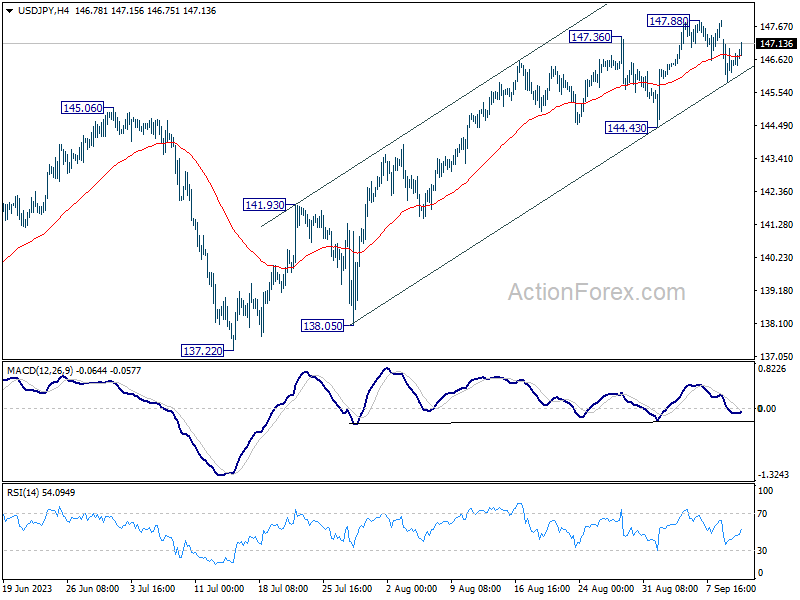

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.91; (P) 146.59; (R1) 147.27; More...

USD/JPY is staying in consolidation from 147.88 and intraday bias remains neutral. While deeper pullback cannot be ruled out, outlook remains bullish with 144.43 support intact. On the upside, above 147.88 will resume larger rise from 127.20, to retest 151.93 high.

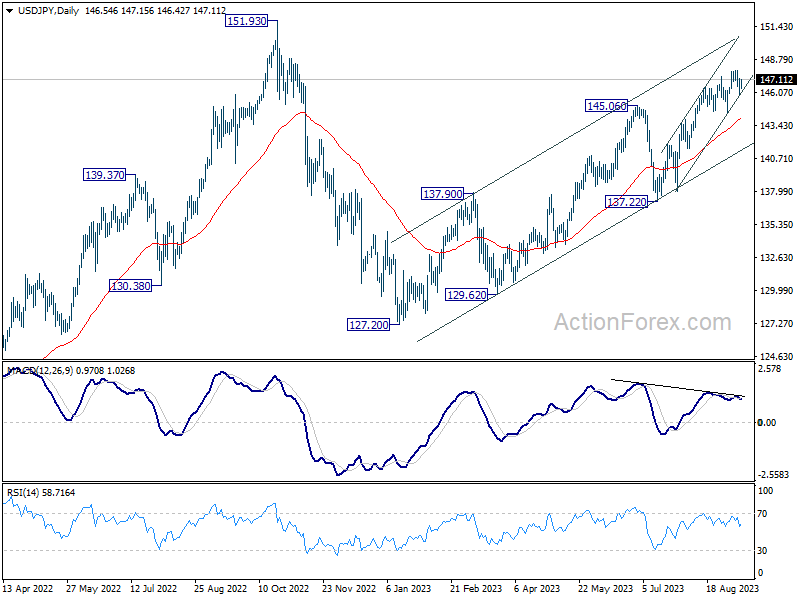

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by break of 137.22 support will indicate that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

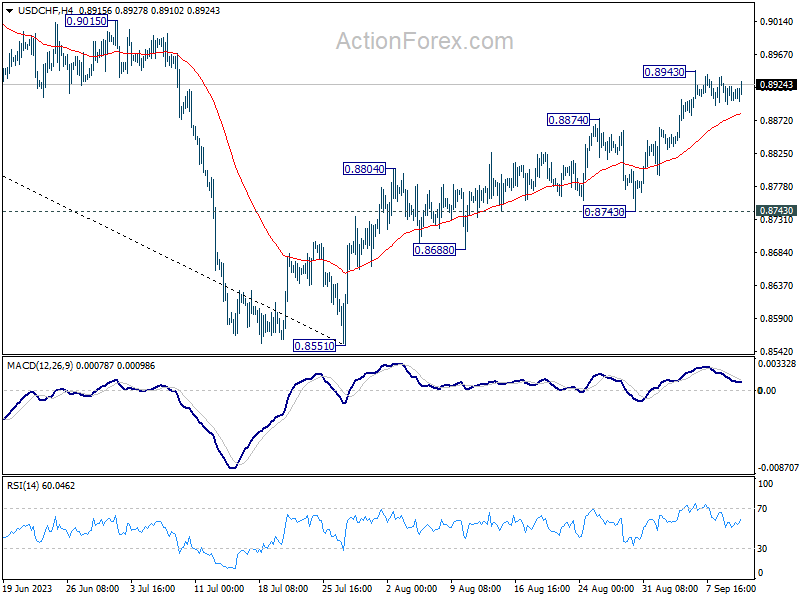

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8895; (P) 0.8911; (R1) 0.8925; More....

No change in USD/CHF's outlook as consolidation from 0.8943 is extending. While deeper pull back cannot be ruled out, downside should be contained above 0.8743 support to bring another rally. Break of 0.8943 will extend the rise from 0.8551 to 0.9146 cluster resistance.

In the bigger picture, rebound from 0.8551 medium term bottom is currently seen as a correction to the downtrend from 1.0146 (2022 high). Further rally would be seen to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160). Strong resistance could be seen there to limit upside, at least on first attempt.

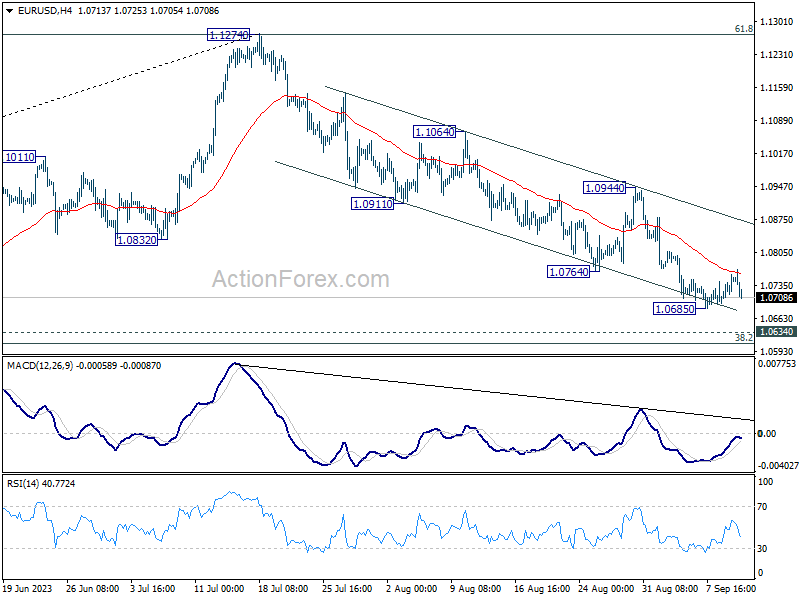

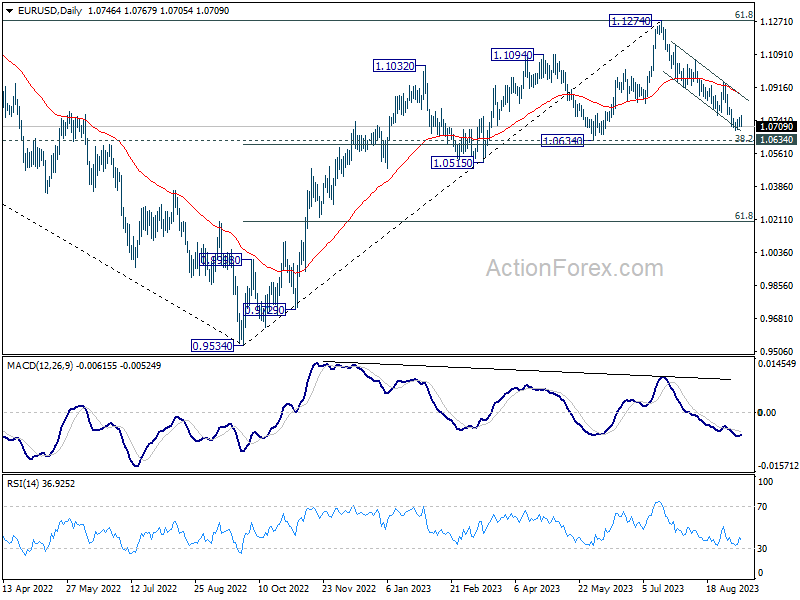

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0719; (P) 1.0739; (R1) 1.0770; More...

EUR/USD weakened after failing to sustain above 55 4H EMA, but stays above 1.0685 temporary low. Intraday bias remains neutral for the moment. Outlook will stay bearish as long as 1.0944 resistance holds. On the downside, below 1.0685 will resume the fall from 1.1274 to 1.0609/34 cluster support zone next.

In the bigger picture, fall from 1.1274 medium term top is seen as a correction to up trend from 0.9534 (2022 low). Strong support could be seen from 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609) to bring rebound, at least on first attempt. Break of 1.0944 will indicate the start of the second leg, and target retest of 1.1274. However, sustained break of 1.0609/0634 will raise the chance of bearish trend reversal, and target 61.8% retracement at 1.0199.

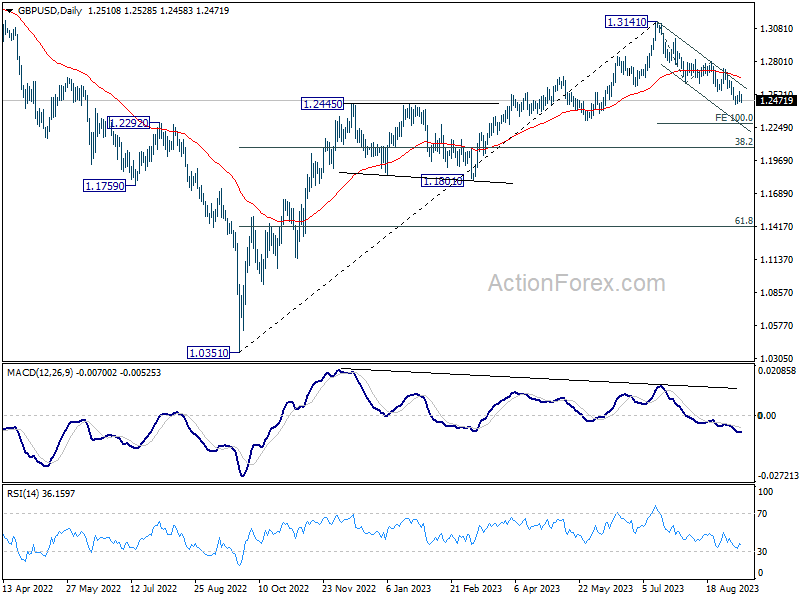

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2471; (P) 1.2509; (R1) 1.2547; More...

GBP/USD falls notably today but stays above 1.2443 temporary low. Intraday bias remains neutral first. In case of another recovery, upside should be limited by 1.2618 support turned resistance to bring another fall. Break of 1.2443 will resume the decline from 1.3141 and target 100% projection of 1.3141 to 1.2618 from 1.2799 at 1.2276.

In the bigger picture, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. But outlook will be neutral at best as long as 1.3141 resistance holds, and consolidation from there is set to extend, until further development.