Sample Category Title

Euro and Sterling Falter Amid Dismal Data; Dollar Finds Buyers, Gold Tumbles

Euro and Sterling stumbled today as they responded to less than impressive economic indicators. Despite a slight uplift in German economic sentiment, the broader picture reflected deteriorating current situation, adding pressure on the common currency. Concurrently, the Pound exhibited a steeper reaction to the shrinking payroll employment coupled with the decelerated wage growth noted in August, accentuating the weak undercurrents plaguing the currency. Swiss Franc seemed to benefit, albeit modestly, from purchases made against its two European peers.

Shifting focus to Dollar, it is overturning the setback it encountered earlier this week, even though it is kept within familiar range against other majors currencies for now. Riding closely on the heels of Dollar, Canadian emerged as the day's second best performer.

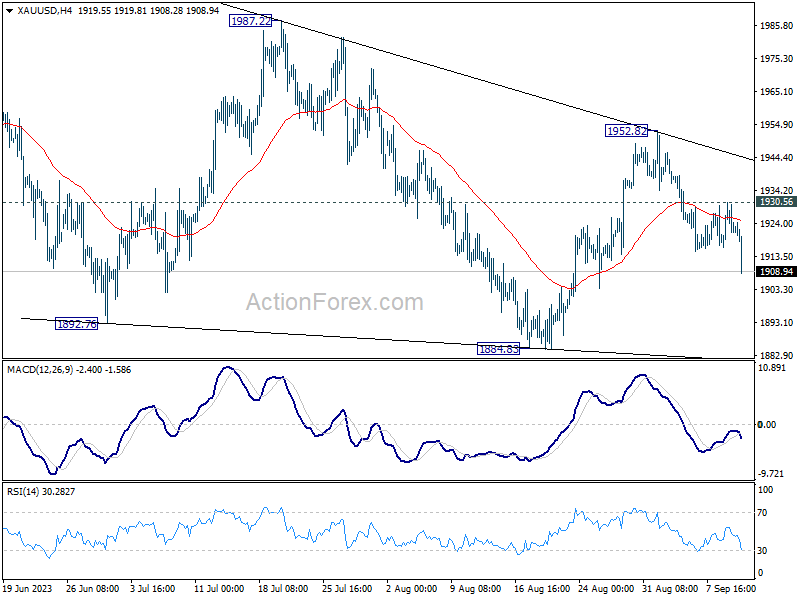

On the technical side, Gold's decline from 1952.82 resumed by breaking through 1915.10 support today, on the back of Dollar's rebound. For now, further fall is expected as long as 1930.56 resistance holds. The fall from 1952.82 should target 1900 psychological, and likely further to 1884.83 support. Subsequent reactions around this level will be crucial in assessing whether Gold is on a prolonged decline from its 2062.95 peak.

In Europe, at the time of writing, FTSE is up 0.39%. DAX is down -0.50%. CAC is down -0.27%. Germany 10-year yield is down -0.012 at 2.629. Earlier in Asia, Nikkei rose 0.95%. Hong Kong HSI dropped -0.39%. China Shanghai SSE dropped -0.18%. Singapore Strait Times dropped -0.12%. Japan 10-year JGB yield rose 0.0048 to 0.710.

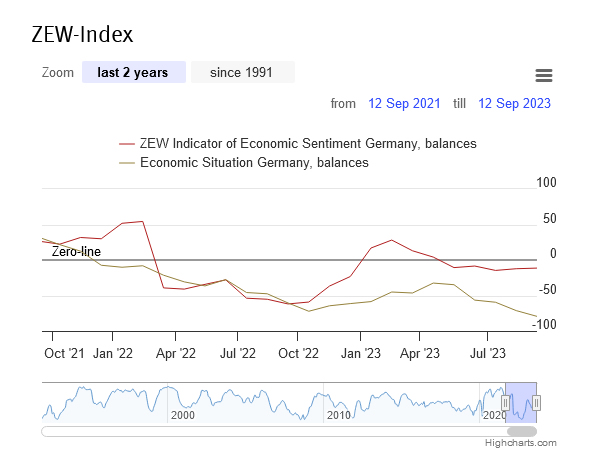

German ZEW improves to -11.4, but situation tumbles to -79.4

Germany's ZEW Economic Sentiment for September experienced an uptick, rising from -12.3 to -11.4, surpassing the anticipated drop to -15.0. However, not all was rosy for the nation, as Current Situation index witnessed a downturn, descending from -71.3 to -79.4, which was a more significant dip than forecasted 75.0.

On a broader scale, Eurozone's ZEW Economic Sentiment slid from -5.5 to -8.9, trailing the predicted -6.2. Current Situation for the zone also decreased marginally, moving by -0.6 to rest at -42.6.

Shedding light on these figures, ZEW President Professor Achim Wambach remarked, "The assessment of the current economic situation in Germany by the financial market experts is even more pessimistic than in August 2023." While this paints a subdued picture of the present scenario, Wambach highlighted a silver lining, pointing to the "slight improvement in expectations regarding Germany's economic situation over the next six months."

Drawing connections to the international arena, Wambach added, "The brighter economic prospects for Germany align with a notably more optimistic view of international stock market developments." He attributed this, in part, to the growing segment of respondents who foresee stability in interest rates within both Eurozone and US. Furthermore, experts are looking eastwards, projecting a relaxation in China's interest rate policy.

Incoming BoE Breeden sees relatively flat UK GDP growth next few years

Sarah Breeden, the incoming Deputy Governor for BoE, shared her economic forecast during a parliamentary Treasury Committee approval hearing today. She is slated to replace Jon Cunliffe as come November.

Breeden conveyed her anticipation for the inflation rate to be near the 2% target within a span of two years, an outlook that is based on the premises outlined in BoE's August forecast.

Despite the somewhat optimistic perspective on inflation, Breeden aired her expectation of "relatively flat GDP in the UK over the next couple of year".

The expectation for a subdued GDP is rooted in the "impact of past increases in Bank Rate increasingly push down on demand, and supply remains very weak."

Breeden concurred with the MPC's perspective that inflation risks pertaining to the August forecasts are "skewed to the upside". She acknowledged that "second-round effects via price and wage setting are stronger than had previously been expected." When it comes to growth and unemployment, Breeden sees a pathway filled with "balanced risks", which could swing in either direction.

UK payrolled employment down -1k in Aug, median monthly pay growth slowed

In August, UK saw a minimal decline in payrolled employment by -1,000 (-0.0% mom) bringing the total to 30.1 million. In a positive revision, prior month's figures were adjusted from a -4k decrease to a substantial increase of 97k. Despite this, there is no dismissing the slowed momentum in the job market as reflected in the slight decline in August.

Dive deeper into the earnings, and one notices a yoy rise of 6.7% for the median monthly pay, touching GBP 2,260. The service activities sector led this growth, clocking an 8.7% yoy rise, while the finance and insurance sector recorded the lowest at 3.2% yoy. However, there was a perceptible deceleration in the growth rate of median monthly pay, down from July's 7.6% yoy and notably from June's 9.6% yoy, with the latter month having a peak of GBP 2,305.

Turning to median monthly pay, service activities sector spearheaded growth, showcasing an 8.7% yoy increase, attaining the highest growth rate across sectors. Contrastingly, finance and insurance sector lagged, recording the lowest annual growth rate at 3.2% yoy. Overall, median monthly pay elevated by 6.7% yoy to GBP 2,260. However, there was a perceptible deceleration in growth rate of median monthly pay, down from July's 7.6% yoy and notably from June's 9.6% yoy, with the latter month having a peak of GBP 2,305.

The three months leading to July painted a similar picture of mixed outcomes. Unemployment settled at 4.3%, rising by 0.5% from the previous quarter, in line with market anticipations. Meanwhile, employment rate dropped by 0.5% to 75.5% alongside a modest increase in economic inactivity rate to 21.1%, up by 0.1%.

Total weekly hours dropped -18.5% over the three-month period. Average earnings excluding bonus was unchanged at 7.8% 3moy, matched expectations. Average earnings including bonus rose to 8.5% 3moy, above expectations of 8.2%.

Japan's FM Suzuki expects BoJ to liaise with government closely

In the wake of the spike in Yen, prompted by BoJ Governor Kazuo Ueda's remarks, Finance Minister Shunichi Suzuki made clarifying comments today. Yen's climb was chiefly attributed to Ueda's interview with Yomiuri Shimbun, where he hinted at the possibility of exiting negative rates policy in the coming year.

At a regular press conference, Suzuki underlined the autonomy of BOJ, stating that the "specific monetary policy conduct is up to the BOJ to decide."

However, the minister did not hold back from expressing the government's expectations . Suzuki conveyed his aspirations for BOJ, emphasizing its collaboration with the government. He said, "I expect the BOJ to continue to liaise with the government closely and conduct monetary policy appropriately."

The guiding principle for this collaboration, as Suzuki suggests, should be a comprehensive evaluation of the economy, considering factors like pricing and prevailing financial conditions. The ultimate aim is to "achieve its price stability target in a stable and sustainable way."

The remarks by the Finance Minister, while emphasizing BoJ's autonomy, also subtly convey the weight of responsibility the central bank carries in managing the nation's economic health, especially in unpredictable financial climates.

Australia consumer sentiment fell to 79.7, languishes at deeply pessimistic levels

Australia's consumer sentiment, as depicted by Westpac Consumer Sentiment Index, witnessed a dip of -1.5% mom, settling at 79.7 in September. The sentiment has been gloomily "languished at deeply pessimistic levels".

Westpac draws attention to the historical context, pointing out that since the initiation of the survey back in 1974, such enduring periods of pessimism have been rare. The most notable instance was during early 1990s' recession when sentiments dipped even lower and remained so for a duration exceeding two years.

On the brighter side, households showcased reduced apprehension about potential rate hikes, with noticeable surge in confidence, up 7.8%, particularly among mortgagors. However, looming worries about cost of living and inflation continue to weigh down on consumer spirits. Although job confidence has steadied itself, it has drastically plummeted, down -33% from its peak levels. One silver lining is the buoyed expectations around house prices.

Westpac expects RBA to maintain their status quo until August 2024. By this timeframe, Westpac envisions inflation receding to 3.4%, a jump in unemployment rate to 4.5%, and a noticeable slowdown in the annual growth rate of consumer spending, tapering to a mere 0.8%.

Also released, NAB Business Conditions rose from 11 to 13 in August. Business Confidence rose from 1 to 2.

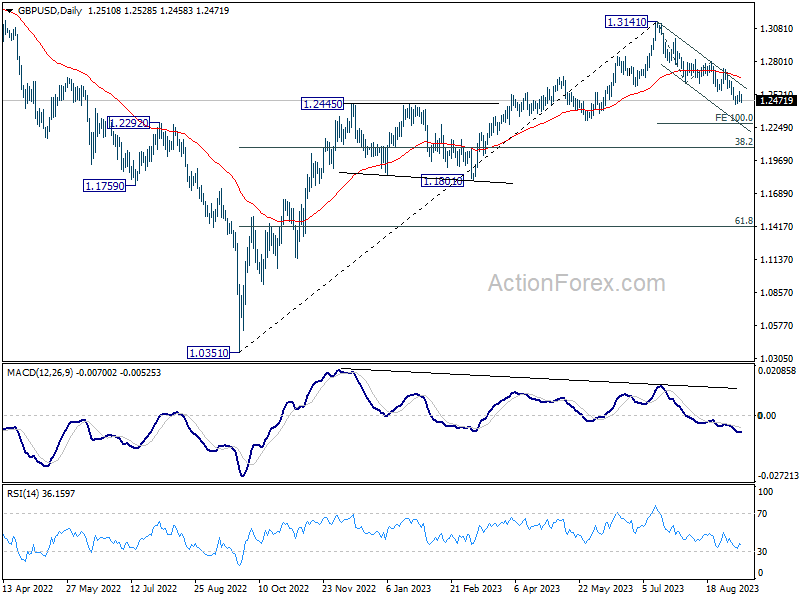

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2471; (P) 1.2509; (R1) 1.2547; More...

GBP/USD falls notably today but stays above 1.2443 temporary low. Intraday bias remains neutral first. In case of another recovery, upside should be limited by 1.2618 support turned resistance to bring another fall. Break of 1.2443 will resume the decline from 1.3141 and target 100% projection of 1.3141 to 1.2618 from 1.2799 at 1.2276.

In the bigger picture, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. But outlook will be neutral at best as long as 1.3141 resistance holds, and consolidation from there is set to extend, until further development.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Westpac Consumer Confidence Sep | -1.50% | -0.40% | ||

| 01:30 | AUD | NAB Business Conditions Aug | 13 | 10 | 11 | |

| 01:30 | AUD | NAB Business Confidence Aug | 2 | 2 | 1 | |

| 06:00 | GBP | Claimant Count Change Aug | 0.9K | 29K | ||

| 06:00 | GBP | ILO Unemployment Rate (3M) Jul | 4.30% | 4.30% | 4.20% | |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jul | 7.80% | 7.80% | 7.80% | |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Jul | 8.50% | 8.20% | 8.20% | |

| 09:00 | EUR | Germany ZEW Economic Sentiment Sep | -11.4 | -15 | -12.3 | |

| 09:00 | EUR | Germany ZEW Current Situation Sep | -79.4 | -75 | -71.3 | |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Sep | -8.9 | -6.2 | -5.5 | |

| 10:00 | USD | NFIB Business Optimism Index Aug | 91.3 | 91.6 | 91.9 |

A Dovish Hike or a Hawkish Pause Coming from ECB?

- The ECB rate-setting meeting dominates this week’s busy schedule

- Market split between a dovish 25bps rate hike and a hawkish pause

- Decision will be announced on Thursday 12.15 GMT, press conference at 12:45 GMT

All eyes are on Thursday's ECB rate meeting

The ECB holds its sixth rate-setting meeting for 2023 with the market mostly split on its outcome. The probability assigned for the tenth consecutive rate hike has varied greatly over the past 40 days and it is currently standing at 57% for a 25bps move. The battle between the hawks and doves has intensified recently as the upcoming “round table” discussion is expected to be extremely heated regarding the ECB’s next move.

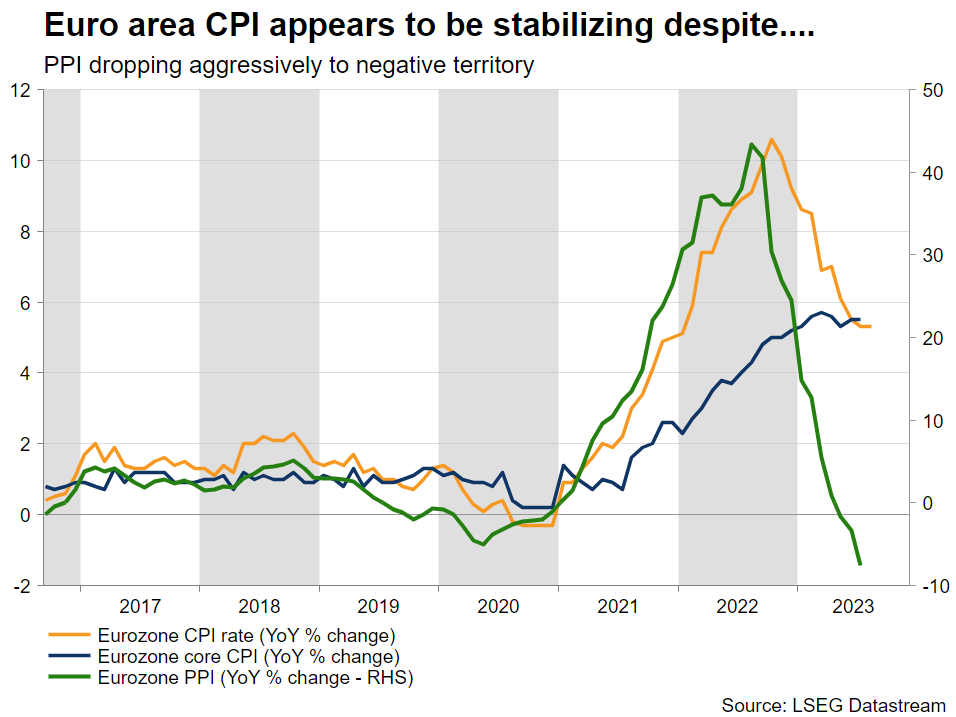

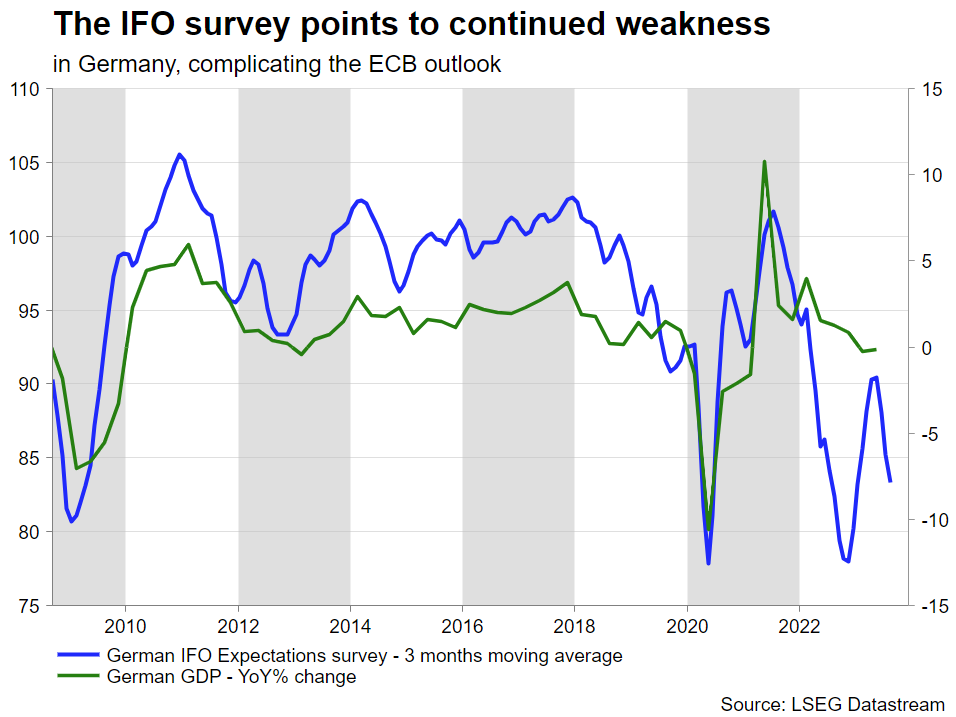

Scanning through the economic data one can reach two unbiased conclusions: (1) the euro area continues to experience very weak growth, and even negative growth as in the case of Germany, in 2023. In the meantime, the forward-looking indicators are equally bleak.

And (2) the inflation rate remains elevated with the August CPI figures holding a small negative surprise for the doves as the euro area aggregate headline annual figure accelerated, instead of recording another drop. Additionally, the recently published ECB Consumer survey showed 12-month expected inflation at 3.4%, and the 3-year inflation expectation rising to 2.4% from 2.3% in June 2023. Most hawks appear to be extremely uncomfortable with these figures.

Price stability is ECB’s only target

Contrary to the Fed’s dual mandate, the ECB has one target: price stability in the medium term. This is engraved in the ECB’s DNA despite the diverse comments from the various ECB members hitting the airwaves since the Jackson Hole gathering. The hawks, most notably Wunsch, Knot and Nagel, are clearly supporting another rate hike on Thursday. On the flip side, the ECB doves are gaining momentum from the recent disappointing growth figures and hence probably feel confident that they have the votes to block a 25bps move at the meeting.

Crucially, we will also get the ECB staff projections on Thursday. The inflation figures will be under the spotlight as the June 2023 projections showed headline euro area inflation and its core subcomponent slowing to 2.2% and 2.3% YoY respectively by 2025. The new projections will play a crucial role in the ECB discussions, especially if the inflation figures are not revised lower and thus pointing to the need for further monetary policy moves.

Dovish hike or hawkish pause?

As per usual, the behind-closed-doors bargaining will dominate the ECB meeting. The two most likely outcomes appear to be a dovish hike and a hawkish pause. The hawks would clearly prefer a rate hike but could eventually settle with a pause that is accompanied by a hawkish statement, along the lines of president Lagarde’s appearance at the Jackson Hole gathering, and an accelerated reduction of the various support programmes holdings, and predominantly the PEPP.

In addition, the hawks are aware that the stance of the ECB members voting at the October meeting is much more hawkish leaning. This means that they could push for an October rate hike if the data continues to support their case.

On the other hand, the doves could begrudgingly accept the above “deal” in their attempt to avoid another rate hike, but clearly express their concerns on the impact of the already elevated bond yields across the periphery. At the end, a compromise will be reached, and a common statement will be prepared, keeping everyone happy.

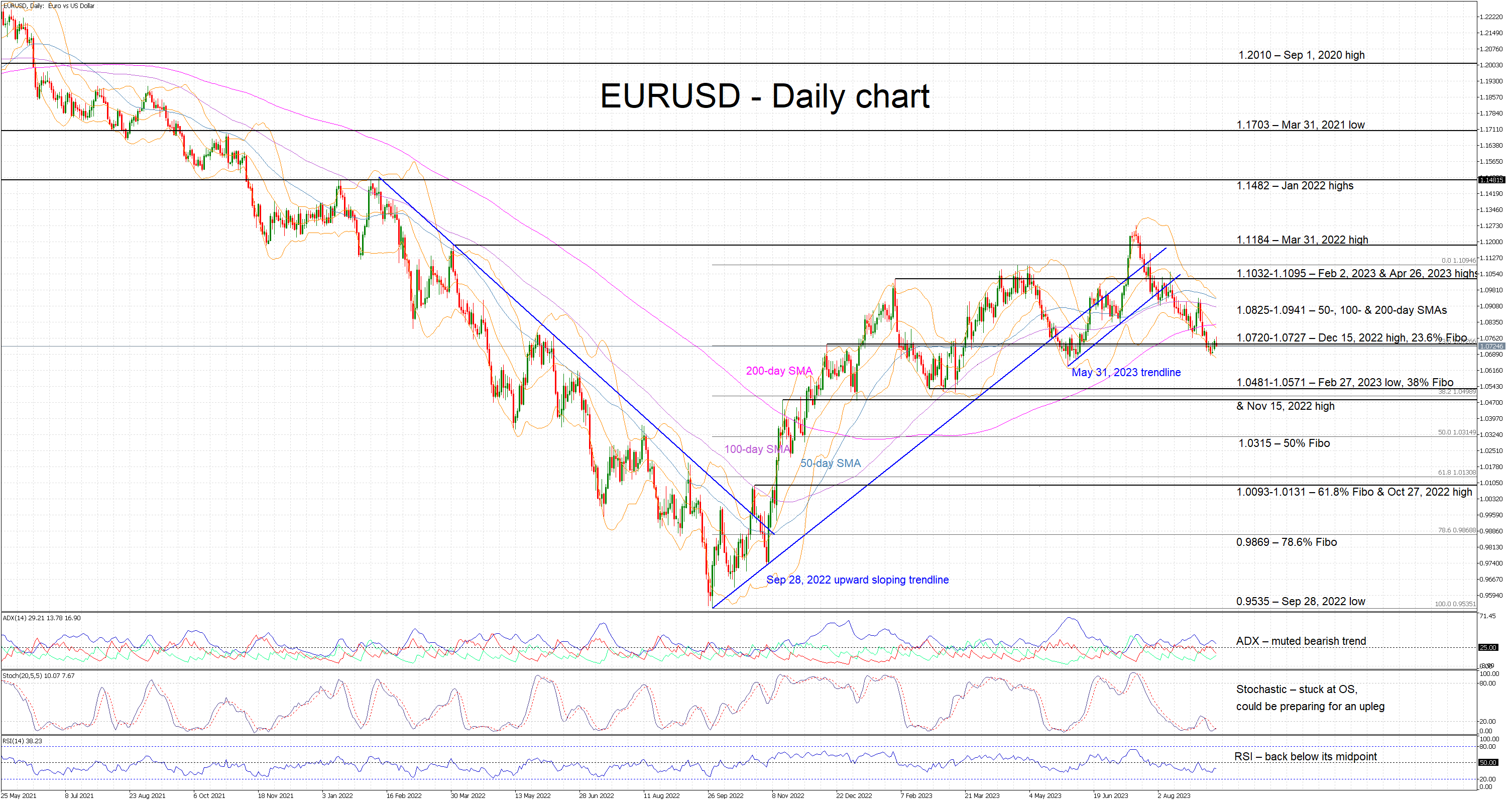

Euro trying to maintain some of its 2023 gains against dollar

After a difficult August of strongly underperforming against the dollar, the euro is anxiously waiting for the ECB meeting outcome. Considering the very weak growth outlook, a possible rate hike could only provide short-term relief to euro bulls as the market is ready to accept that the ECB has probably concluded its rate-hiking cycle, thus removing the euro’s main tailwind. A possible move higher in the euro-dollar pair could meet strong resistance at the busy 1.0825-1.0941 range, while the path lower looks clear until the 1.0571 area.

Incoming BoE Breeden sees relatively flat UK GDP growth next few years

Sarah Breeden, the incoming Deputy Governor for BoE, shared her economic forecast during a parliamentary Treasury Committee approval hearing today. She is slated to replace Jon Cunliffe as come November.

Breeden conveyed her anticipation for the inflation rate to be near the 2% target within a span of two years, an outlook that is based on the premises outlined in BoE's August forecast.

Despite the somewhat optimistic perspective on inflation, Breeden aired her expectation of "relatively flat GDP in the UK over the next couple of year".

The expectation for a subdued GDP is rooted in the "impact of past increases in Bank Rate increasingly push down on demand, and supply remains very weak."

Breeden concurred with the MPC's perspective that inflation risks pertaining to the August forecasts are "skewed to the upside". She acknowledged that "second-round effects via price and wage setting are stronger than had previously been expected." When it comes to growth and unemployment, Breeden sees a pathway filled with "balanced risks", which could swing in either direction.

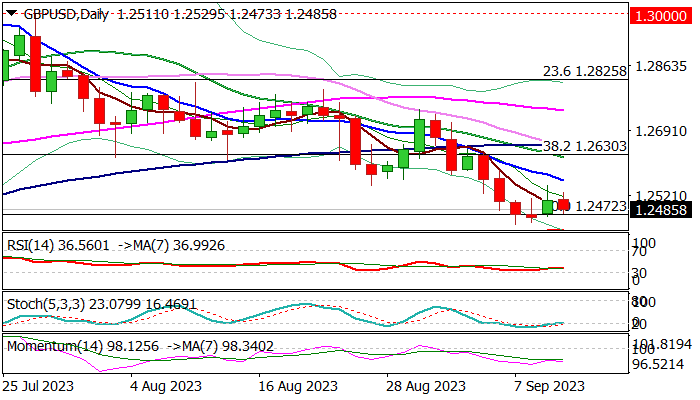

GBP/USD: Dips After Weak Jobs Data But Still Looks for Clearer Direction Signal

Cable loses traction after weak UK jobless data and dips below 1.2500 mark on Tuesday morning.

Fresh weakness adds to signals that brief recovery is likely over, after Monday’s strong upside rejection which left daily candle with long upper shadow.

Overall picture is firmly bearish on daily chart, though headwinds on approach to pivotal 200DMA support (1.2424) may keep the action in extended consolidation.

Close below cracked Fibo support at 1.2472 (50% retracement of 1.8026/1.3141 upleg) is needed to generate initial bearish signal, which will look for confirmation on sustained break below 200DMA to signal continuation of the downtrend from 1.3141 (2023 high posted on July 14) and unmask next strong supports at 1.2314/07 (Fibo 61.8% / May 25 higher low).

Falling 10DMA (1.2560) offers initial resistance, guarding upper pivots at 1.2630 zone (20DMA / broken Fibo 38.2%).

Sideways mode to remain while the action stays between 10 and 200DMA’s.

Traders shift focus on BOE’s policy meeting next week, with growing bets that the MPC would deliver another rate hike.

Res: 1.2547; 1.2560; 1.2630; 1.2653.

Sup: 1.2445; 1.2424; 1.2368; 1.2314.

German ZEW improves to -11.4, but situation tumbles to -79.4

Germany's ZEW Economic Sentiment for September experienced an uptick, rising from -12.3 to -11.4, surpassing the anticipated drop to -15.0. However, not all was rosy for the nation, as Current Situation index witnessed a downturn, descending from -71.3 to -79.4, which was a more significant dip than forecasted 75.0.

On a broader scale, Eurozone's ZEW Economic Sentiment slid from -5.5 to -8.9, trailing the predicted -6.2. Current Situation for the zone also decreased marginally, moving by -0.6 to rest at -42.6.

Shedding light on these figures, ZEW President Professor Achim Wambach remarked, "The assessment of the current economic situation in Germany by the financial market experts is even more pessimistic than in August 2023." While this paints a subdued picture of the present scenario, Wambach highlighted a silver lining, pointing to the "slight improvement in expectations regarding Germany's economic situation over the next six months."

Drawing connections to the international arena, Wambach added, "The brighter economic prospects for Germany align with a notably more optimistic view of international stock market developments." He attributed this, in part, to the growing segment of respondents who foresee stability in interest rates within both Eurozone and US. Furthermore, experts are looking eastwards, projecting a relaxation in China's interest rate policy.

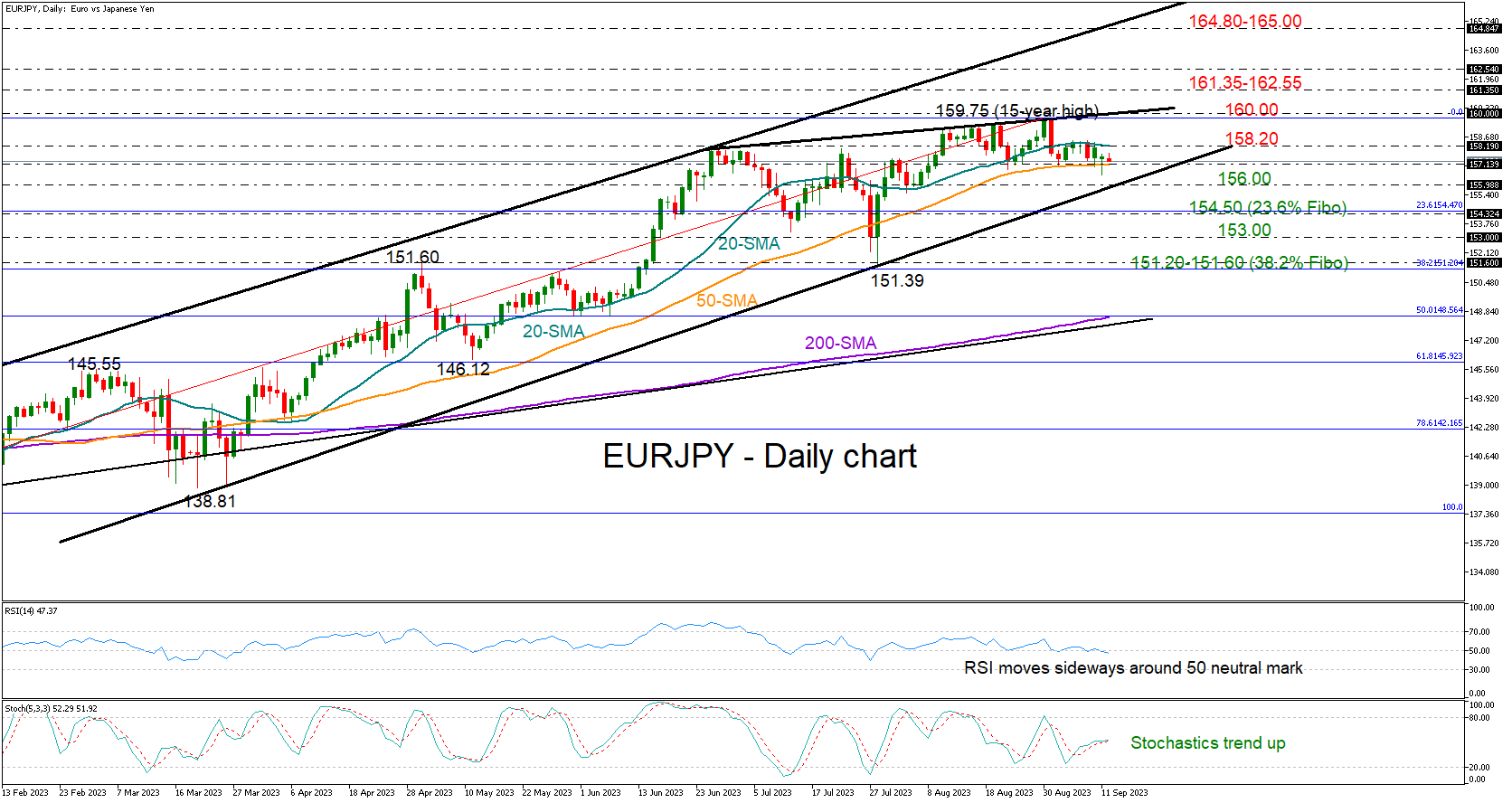

EURJPY Sails Sideways as ECB Rate Decision Looms

- EURJPY eases into range-bound trading after 15-year high

- Short-term outlook neutral, but will the bears return?

- ECB policy announcement scheduled for Thursday 12:15 GMT

EURJPY has been moving back and forth between its 20- and 50-day simple moving averages (SMAs) following the pullback from a 15-year high of 159.75.

The short-term signals are mixed as the RSI is hovering around its 50 neutral mark, while the stochastic oscillator is trending higher. In the weekly chart, though, the indicators have peaked in the overbought region and are reversing south, reflecting a bearish bias.

Support is currently provided around the 50-day SMA at 157.13, while slightly lower, the ascending trendline drawn from the March lows at 156.00 could be the last opportunity for a rebound before selling pressure intensifies towards the 154.50 zone. The latter overlaps with the 23.6% Fibonacci retracement of the 137.37-159.75 uptrend. If the bears breach that floor too, the 153.00 round level could calm downside pressures ahead of the 38.2% Fibonacci mark of 151.20.

Should the bulls claim the 20-day SMA at 158.20, all eyes would turn to the short-term resistance line at 160.00. Running higher, the pair could enter a new consolidation phase within the 161.35-162.55 region, where the price stalled at the end of August 2008 and peaked in August-October 1998. Another success there might lift the price straight up to the 2023 resistance line at 164.80-165.00.

In brief, EURJPY is lacking direction in short-term picture, awaiting fresh volatility below 156.00 or above 160.00.

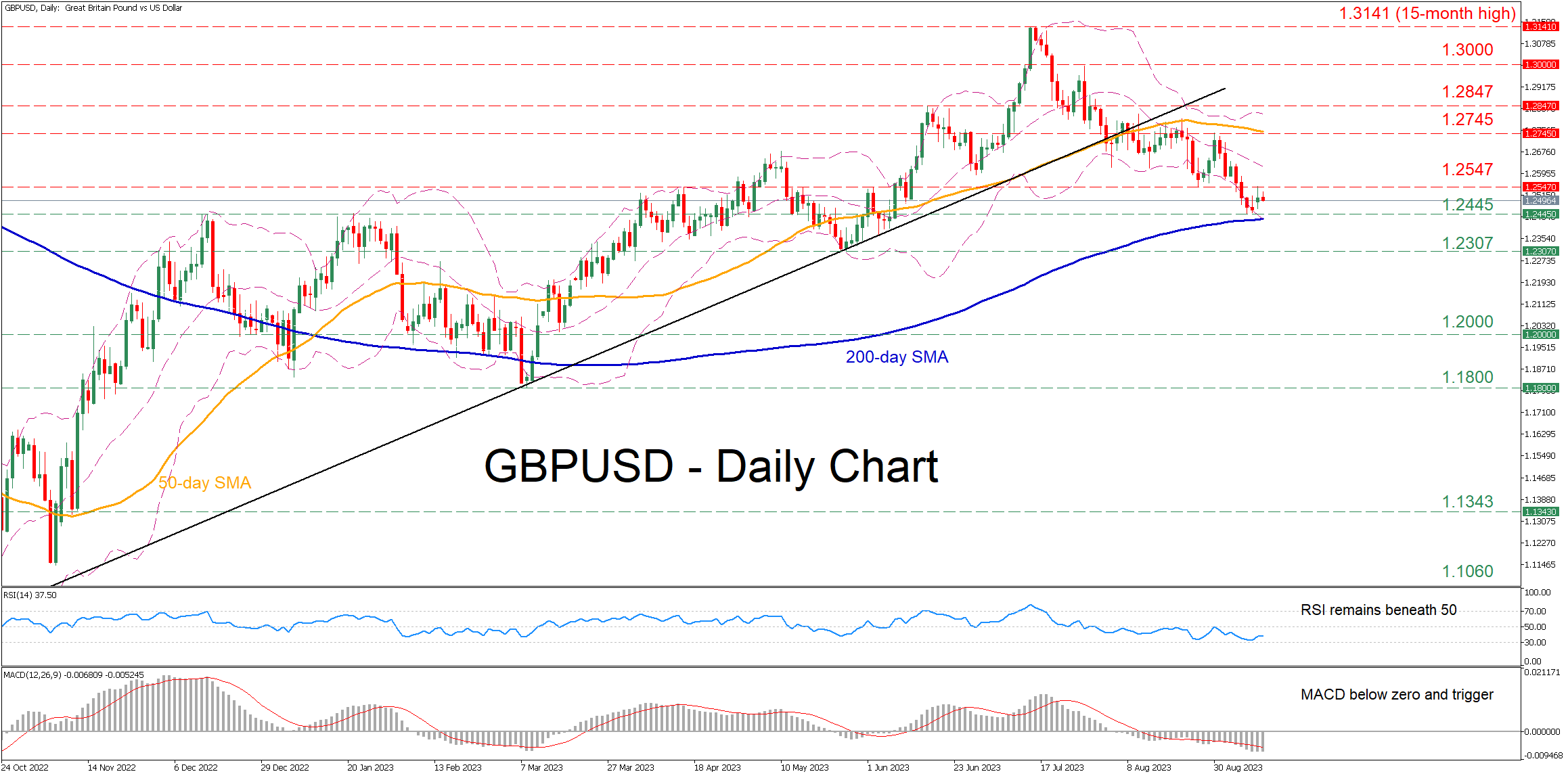

GBPUSD Bounces Off 3-month Low; Bearish Bias Holds

- GBPUSD in a steady decline since mid-July

- Found its footing just shy of the 200-day SMA

- Can the bulls stage a comeback?

GBPUSD has been forming a structure of lower highs and lower lows since its 15-month peak of 1.3141. Despite the latest rebound from a three-month low, the short-term oscillators are pointing to further downside as both the RSI and MACD are well within their negative territories.

If the selling interest intensifies, the pair could face the recent support of 1.2445, which acted as resistance in January and also coincides with the 200-day simple moving average (SMA). Sliding beneath that floor, the price might descend towards the May bottom of 1.2307. Further declines could then cease at the 1.2000 psychological mark.

On the flipside, should the recent bounce extend, the bulls may target 1.2547, which has acted both as support and resistance in the past month. A break above that region could open the door for the August resistance of 1.2745, which overlaps with the 50-day SMA. Even higher, the June peak of 1.2847 could curb further upside attempts.

In brief, it seems that the GBPUSD’s pullback is starting to lose steam, but it’s too early to call for a reversal. Indeed, the short-term decline could even accelerate in the case that the pair profoundly closes below the 200-day SMA.

Oil Price Stabilizes Near Year’s Highs

Last week, the Russian Federation and Saudi Arabia confirmed plans to reduce production by the end of the year, which contributed to an increase in oil prices.

At the beginning of this week, the WTI price stabilized in the range of 85.50 - 87.50. Will the upward trend continue, which will benefit oil producers?

On Tuesday morning, the price is within the triangle formed from the median line of the ascending channel (shown in blue) and the level of 87.50. A breakout of this triangle can occur in both directions.

Bullish arguments:

→ The price is within the ascending channels, both short-term (built on the 1h and 4h charts) and long-term (built on the daily chart).

→ A series of rising lows is forming on the chart, indicating that demand is active.

→ Technically, the market may be supported by the level of 85.50, which previously served as resistance.

→ Oil supplies may be disrupted due to various storms. For example, in eastern Libya, 4 ports were closed due to flooding and a storm, which killed about 2,000 people.

Bearish arguments:

→ News about economic slowdown in various regions (China, Europe) should weaken demand.

→ On September 11, the price of oil renewed its multi-month high, but retreated very quickly. The behavior was similar to a bull trap — a sign of a weak market that could be a harbinger of downward momentum.

→ High oil prices are unprofitable for governments of countries (including the United States) struggling with high inflation.

Tomorrow, at 11:00 GMT+3, the publication of a monthly report on oil prices from the International Energy Agency is scheduled, which could greatly affect the current exchange rate and disrupt the consolidation triangle that is currently in effect.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Markets Rise As Spotlight Shines On US CPI

Asian markets were a mixed bag on Tuesday despite the broadly positive cues from Wall Street overnight as a surge in Tesla powered a rally in tech stocks.

Despite the shaky sentiment across Asia amid lingering concerns about China’s economy, European futures are pointing to a positive open as focus falls on the pending Germany ZEW survey expectations. Shares across the region could see heightened volatility this week due to the ECB meeting on Thursday. Looking at currencies, the British Pound briefly jumped after UK wage data beat market expectations. In the commodity space, oil is hovering near its highest level this year ahead of key monthly reports from the IEA and OPEC.

Dollar steady ahead of US Inflation data

The August US Consumer Price Index (CPI) report will act as a critical piece of information that determines whether the Fed will keep rates higher for longer.

Headline inflation is expected to jump thanks to energy costs with markets projecting monthly prices to accelerate 0.6% in August, but the core is seen stable at 0.2%. Ultimately, further signs of cooling inflationary pressures may feed the argument around the Fed already concluding its hiking cycle. As of writing, traders are currently pricing in a 7% probability of a 25-basis point hike next week, with this jumping to 46% by November, according to Fed funds futures.

Should the inflation numbers print below market forecasts, this could reinforce the argument around the Fed being done with its hiking cycle in 2023, weakening the US Dollar. However, a sticky inflation print could inject dollar bulls with more strength as expectations rise around the Fed having headroom to hike one more time this year.

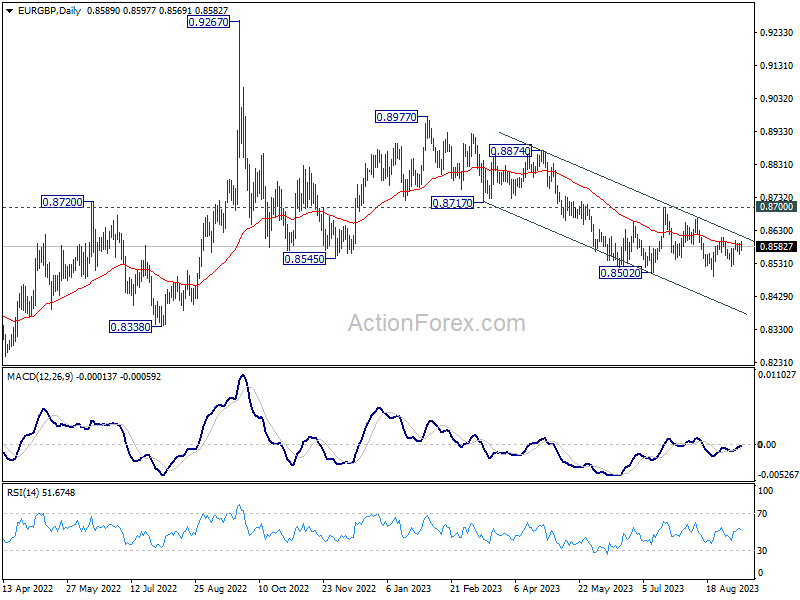

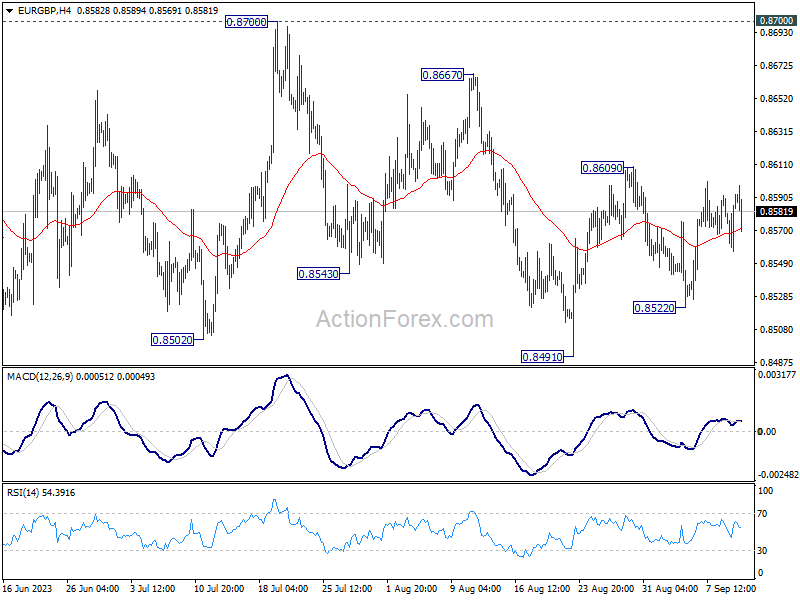

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8570; (P) 0.8582; (R1) 0.8606; More...

Sideway trading continues in EUR/GBP and intraday bias remains neutral. Current rise from 0.8941 could be the third leg of the corrective pattern from 0.8502. On the upside, above 0.8609 would resume the rebound and target 0.8667 resistance, possibly further to 0.8700. On the downside, however, break of 0.8522 will bring retest of 0.8491 low.

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Fall from 0.8977 is seen as the third leg. As long as 0.8700 resistance holds, further decline is still expected. Break of 0.8491 will resume the fall towards 0.8201 (2022 low). Nevertheless, firm break of 0.8700 will now be a sign of bullish reversal.