Sample Category Title

GBP/USD Recovery Could Soon Fade, UK Jobs Report Next

Key Highlights

- GBP/USD is attempting a recovery wave from the 1.2445 zone.

- A key bearish trend line is forming with resistance near 1.2600 on the 4-hour chart.

- EUR/USD is consolidating losses below the 1.0800 pivot level.

- USD/JPY failed to surpass 147.80 and corrected gains.

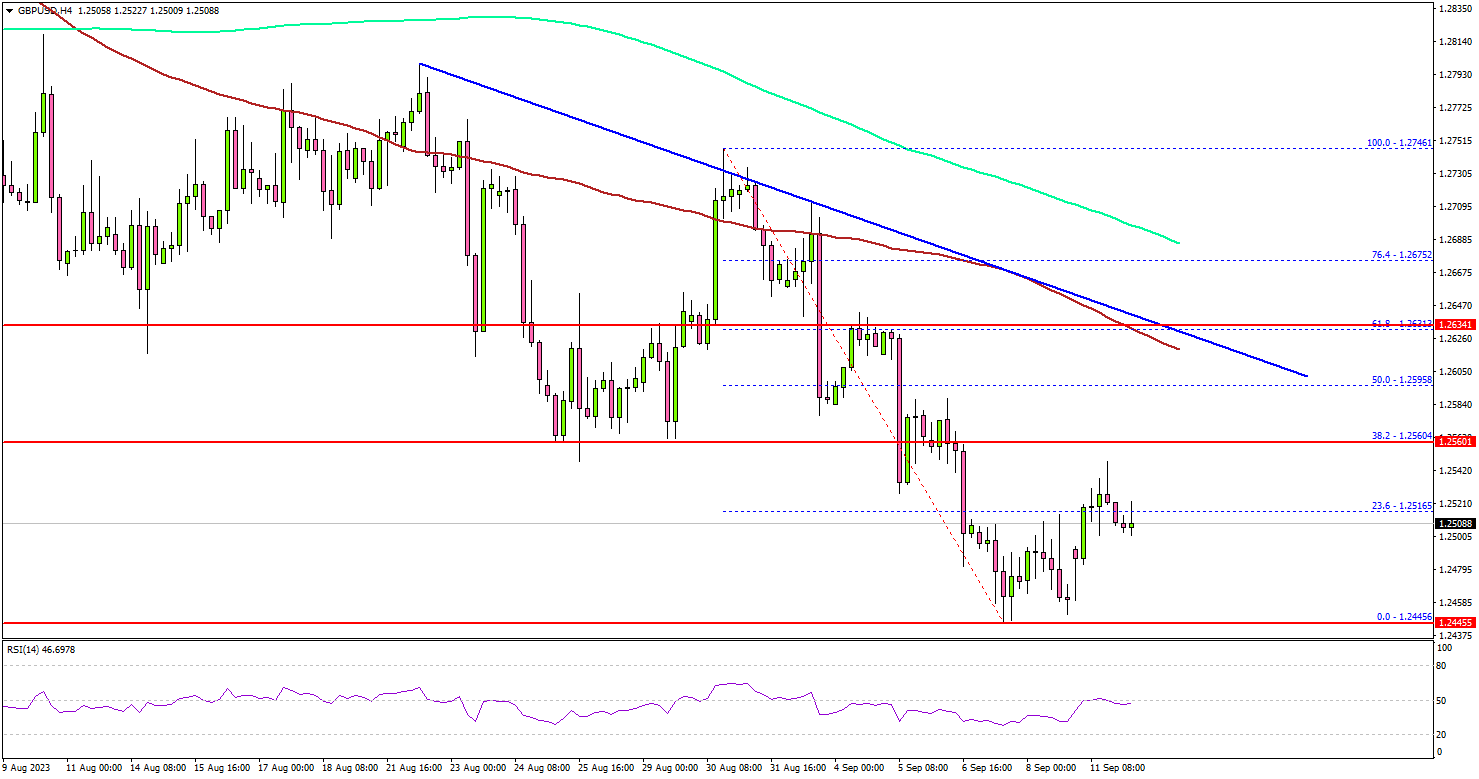

GBP/USD Technical Analysis

The British Pound found support near the 1.2445 zone against the US Dollar. GBP/USD formed a short-term base and recently started an upside correction above 1.2480.

Looking at the 4-hour chart, the pair was able to clear the 1.2500 level but is still well below the 100 simple moving average (red, 4 hours) and the 200 simple moving average (green, 4 hours).

It broke the 23.6% Fib retracement level of the downward move from the 1.2746 swing high to the 1.2445 low. On the upside, an initial resistance is near the 1.2560 level.

The first major resistance is near the 1.2600 handle. There is also a key bearish trend line forming with resistance near 1.2600 on the same chart. The trend line is close to the 50% Fib retracement level of the downward move from the 1.2746 swing high to the 1.2445 low.

The next major resistance is near the 1.2635 level. A close above 1.2635 could start another decent increase. In the stated case, the pair could rise toward the 1.2700 level.

On the downside, immediate support is near 1.2480. The next key support is seen near the 1.2445 level. The first major support is near 1.2420. If there is a move below 1.2420, the pair could dive toward 1.2340. Any more losses might send the pair toward the 1.2250 level.

Looking at EUR/USD, the pair is attempting a short-term upside correction but upsides might be limited above 1.0800.

Economic Releases

- German ZEW Business Economic Sentiment Index for Sep 2023 – Forecast -15.0, versus -12.3 previous.

- UK Claimant Count Change for Aug 2023 – Forecast 12.0K, versus 29.0K previous.

- UK ILO Unemployment Rate for July 2023 (3M) – Forecast 4.3%, versus 4.2% previous.

AUD/JPY: Make or Break Time as China’s Economy Appears to be Stabilizing

- China’s new yuan loans skyrocketed to 1.36 trillion yuan in August, much higher than the prior month’s 345 billion yuan.

- Optimism grows for China’s outlook as stimulus appears to filtering throughout the economy

- Dollar has biggest drop in two months as yen and yuan gain

The big risk aversion trade over the summer has seen AUD/JPY consolidate around the 94.00 level. A downbeat outlook for China kept the Australian dollar heavy, while US economic resilience has kept yen softer on a widening interest rate differential. The AUD/JPY daily highlights a global growth picture that is either looking for a China rebound, which should help Australia’s growth momentum or a Japan recovery that is not on solid footing.

The AUD/JPY daily displays a symmetrical triangle that shows price has converged towards the 94.00 region. The bullish trend that started in the spring ended mid-June ahead of the 97.70 level. Price is poised to either resume the longer-term bullish trend that started after the pandemic low was made in March 2020 or potentially show the start of a significant bearish reversal.

The Australian dollar and Japanese yen seems likely to remain a key risk barometer, which means it could react strongly with what happens with this week’s US inflation data and with China’s decision on rates and their activity data. If bullishness emerges, price could initially targets the 95.50 region, while downside support would come from the 200-day SMA level, which currently resides at the 92.00 level.

This week the Australian economic calendar is filled with economic data that might take a backseat to everything that happens from the US and China. The main Australian data release of the week is Australia jobs, which could show job growth rebounded, but will unlikely bring back rate hike expectations for the RBA.

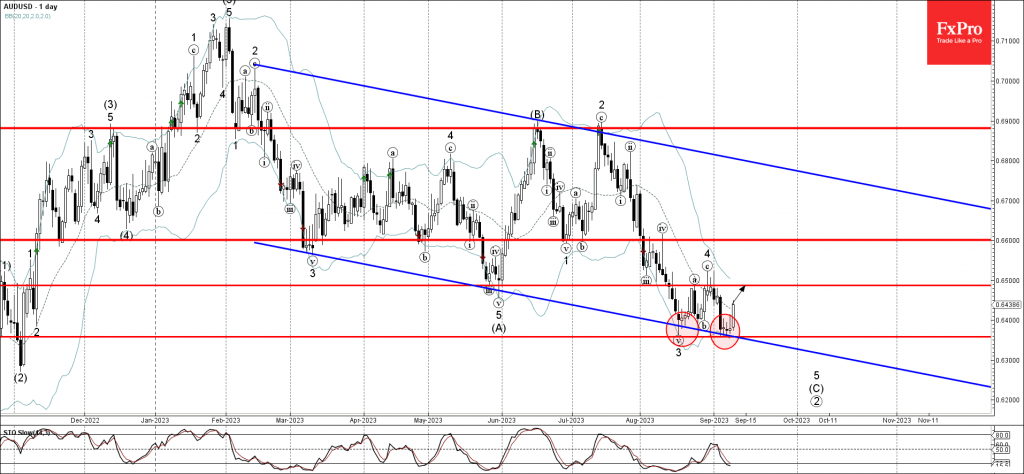

AUDUSD Wave Analysis

- AUDUSD reversed from support level 0.6360

- Likely to rise to resistance level 0.6500

AUDUSD today reversed up strongly from the strong support level 0.6360 (pervious monthly low from August), intersecting with the lower daily Bollinger Band and the support trendline of the wide down channel from February.

The upward reversal from the support level 0.6360 stopped the active short-term impulse wave 5, which belongs to wave (C) from the end of August.

Given the strength of the support level 0.6360, AUDUSD can be expected to rise further toward the next resistance level 0.6500 (top of the pervious waves a and 4 from the end of August).

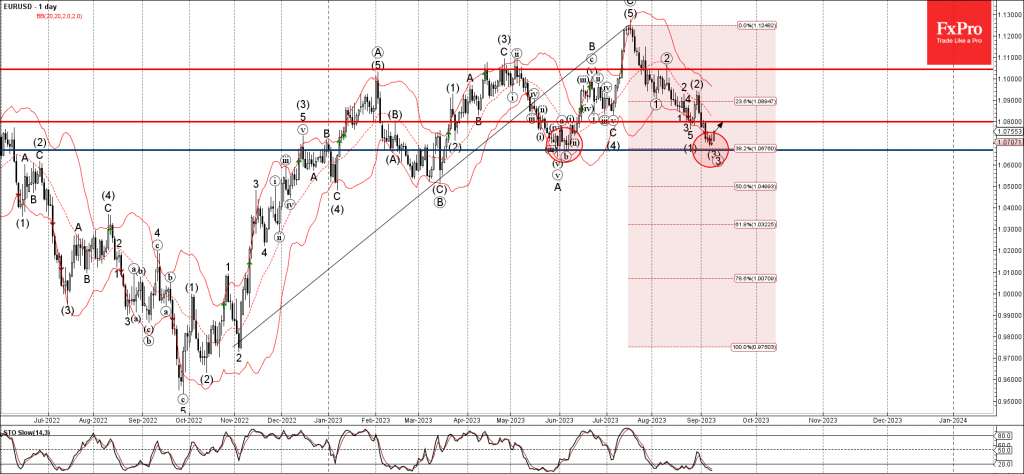

EURUSD Wave Analysis

- EURUSD reversed from key support level 1.0665

- Likely to rise to resistance level 1.0800

EURUSD currency pair recently reversed up from the key support level 1.0665 (former strong support from April and May), intersecting with the lower daily Bollinger Band and the 38.2% Fibonacci correction of the upward impulse from November of 2022.

The upward reversal from the support level 1.0665 stopped the previous short-term impulse wave 3.

Given the oversold daily Stochastic and the strong USD sales seen across the FX markets today, EURUSD can be expected to rise further toward the next resistance level 1.0800 (former low of wave 3 from the end of last month).

New York Fed Survey: Consumer inflation expectations rise slightly

The August 2023 New York Fed Survey of Consumer Expectations has revealed a moderate increase in the median one- and five-year-ahead inflation expectations, both witnessing a rise of 0.1% to sit at 3.6% and 3.0%, respectively. However, expectations for three-year-ahead inflation demonstrated a dip, dropping by -0.1% to 2.8%.

On the unemployment front, there was a noticeable increase in mean unemployment expectations, with the mean probability of a higher unemployment rate one year from now spiking by 1.8%, settling at 38.5%. Despite this increase, the figure remains beneath its 12-month trailing average which stands at 40.2%.

Median expectation for growth in household income experienced a decrement, falling by -0.3% to arrive at 2.9% in August, marking the lowest figure since July 2021.

Australian Dollar Jumps as Chinese Deflation Eases

- Australian dollar jumps 1%

- Australia releases consumer and business confidence on Tuesday

The Australian dollar is sparkling on Monday, with massive gains of 1% against the US dollar. In the North American session, AUD/USD is trading at 0.6441.

China inflation numbers boost Aussie

The Australian dollar received a major boost after China’s inflation release over the weekend. CPI for August rose 0.1% y/y, following a -0.3% reading in July, which marked the first monthly decline in over two years. On a monthly basis, August CPI rose 0.3%, higher than the July gain of 0.2% and matching the consensus. As well, producer prices fell 3%, down from -4.4% in August. The inflation data didn’t knock anyone off their seats, but the fact that deflation showed signs of easing raised risk appetite and boosted the Australian dollar.

China’s economy has deteriorated more sharply than expected, raising alarm bells about the strength of the world’s second-largest economy. The government has responded by injecting stimulus including interest rate cuts and tax breaks but will need to do more to boost economic activity. Manufacturing continues to decline and growth in the services sector has been weakening. China is Australia’s largest trading partner and the Australian dollar is sensitive to economic developments, as we saw earlier today with the Aussie’s sharp gains.

Australian consumers and businesses have been squeezed by high inflation and interest rates, which has taken a toll on confidence. We’ll get a look at consumer and business confidence on Tuesday. Westpac Consumer Confidence Change slipped 0.4% in August but is expected to rebound to 0.6% in September. The NAB Business Confidence index is projected to dip to 1 in August, up from 2 in July. A reading above zero points to improving conditions and below zero to worsening conditions..

AUD/USD Technical

- AUD/USD pushed above resistance at 0.6405 and 0.6453. Above, there is resistance at 0.6528

- There is support at 0.6330 and 0.6282

BoE Mann: Risk of tightening too little more salient

BoE MPC member Catherine Mann expressed a potent concern regarding the UK's current economic landscape, emphasizing the "salient" risk of "tightening too little" in her speech today.

Mann cited alarming data where inflation in core and services has consistently remained above 6% for over a year now. Drawing from econometric analyses which break down inflation dynamics into components of "expectations and inertia", she highlighted an unsettling trend — a steady increase in these components, encouraging continuation of inflation persistence. "Worrying to me," Mann noted, "is that a statistically-derived time-varying trend of inflation has drifted above 2%."

Mann elucidated the channels through which monetary policy transmits its effects on financial markets, influencing price settings and impacting the real economy prominently through an "expectations channel".

She emphasized that "duration above target matters for policy risk assessment", pointing out that the longer the inflation rates hover markedly above target levels, the more challenging and costly it becomes to rein it back to the desired target.

In her assessment, "to pause or to hold the policy rate lower for longer" poses a substantial risk, potentially embedding inflation more deeply and necessitating a more intensive future tightening to alter inflationary expectations and to eliminate the ingrained inflation resulting from a prolonged above-target duration.

To mitigate such adverse outcomes, she championed an approach inclined towards over-tightening, arguing that this strategy would act as a preventive measure against the deeper entrenchment of inflation.

However, Mann remained adaptive to changing economic narratives. She conveyed a readiness to "not hesitate to cut rates" if she observes faster deceleration in inflation paired with notable dip in economic activities.

Sunset Market Commentary

Markets

The dollar taking a breather against the likes of the yen and the yuan this morning helped to smoothen global sentiment even as the move was mainly inspired by potential action of the respective central banks (BOJ, PBOC) to prevent a further decline of their currencies, rather than a ‘natural risk-on’ correction of the dollar. Admittedly, optimists also saw better Chinese lending data as a tentative sign that the economy might be nearing a bottom. Whatever the driver, the EurosStoxx 50 at some point gained about 1.0%, but there was too little news to support follow-through gains (currently +0.5%). The S&P 500 opened 0.5 % higher. In its summer forecast update, the European Commission as expected downwardly revised its 2023 (0.8% from 1.1%) and to 2024 (1.3% from 1.6%) growth forecasts as consumption is still held back by the ongoing increase in prices for most goods and services even as the labour market stays strong. The EC slightly reduced the EMU 2023 inflation forecast from 6.7% in the spring update to currently 6.5%. However, a sustained return of inflation to the 2.0% ECB target isn’t in the cards yet with the 2024 outlook put slightly higher at 3.2% (from 3.1% ). The trends of the EC forecast didn’t come as a big surprise and had limited impact on markets. In a tentatively steepening move, German yields add between 1.0 bp (2-y) and 4.5 bps (30-y). The US curve show a similar move with the 2-y little changed but the 30-y gaining 4.7 bps. For now, the downside in oil looks well protected. Any attempt of Brent to return below $90 p/b is still met by a solid bid.

As indicated, a CB-driven decline in USD/JPY (currently 146.50) and USD/CNY (currently 7.294 compared to 7.344 on Friday) also weighed on the dollar overall. DXY dropped back below the 105 handle (104.67). EUR/USD tries to hold north of 1.07(3). However, from a technical point of view, the USD uptrend remains intact. A mild risk-on today favours sterling against the euro with EUR/GBP drifting back to then 0.8560 area. UK labour data to be published tomorrow morning are the next point of reference for the BoE (and for markets).

News & Views

Norwegian inflation unexpectedly decelerated in August. Prices fell -0.8 m/m, bringing the headline y/y figure from 5.4% to 4.8% and defying expectations for a status quo. A core gauge adjusted for tax changes and excluding energy products dropped 0.6% m/m. The yearly figure eased from 6.4% to 6.3% while consensus anticipated a further rise to 6.6%. Furnishings, household equipment & routine maintenance (-3.2%) as well as housing, water and other utilities (-1.3%) registered the biggest monthly declines. The Norwegian krone briefly dipped following the release before paring losses back to EUR/NOK 11.42. That’s about the same low (NOK) level when the Norges Bank lifted rates in August to 4%. The central bank then said it “The future policy rate path will depend on economic developments. If the economy evolves as currently anticipated, the policy rate will be raised further in September”. Inflation has undershot June expectations but hangs in the balance with the ongoing weak Norwegian krone. A final September hike to 4.25% is therefore still likely.

August Inflation in the Czech Republic came in close to expectations with prices pressures easing to 8.5% (from 8.8%) on a 0.2% monthly pace. Housing, water, energy & fuel (0.3%), transport (1.7%) and especially domestic fuels (7.7%) were among the strongest drivers on a monthly basis. The Czech National Bank said today’s numbers were in line with the summer forecast made in August. Core inflation even came in slightly below expectations, at 6% vs a 6.2% estimate. The ongoing decline in the latter reflects “a fading of growth in prices of foreign inputs and a cooling of domestic demand.” The CNB expects yearly inflation to ease further in September before temporarily halting this trend in October due to statistical base effects. Inflation should be close to the 2% target early next year, it concluded. The Czech crown reacted stoic on the publication at first before extending a losing streak. The CNB’s statement added to the losses, with the CZK probably eying the core inflation miss. EUR/CZK rallies from 24.37 at the open to 24.53 currently. The CZK came in markets’ crosshair after the NBP shocked with a 75 bps rate cut last week, sending shockwaves through regional markets outside Poland too. The numbers today add fuel to the fire, even as governors (eg. deputy governor Zamrazilova) already said the CNB won’t be hasty in cutting rates. Czech swap rates tumble by double digits at the front end of the curve. More than 50 bps of cuts are priced in by year’s end.

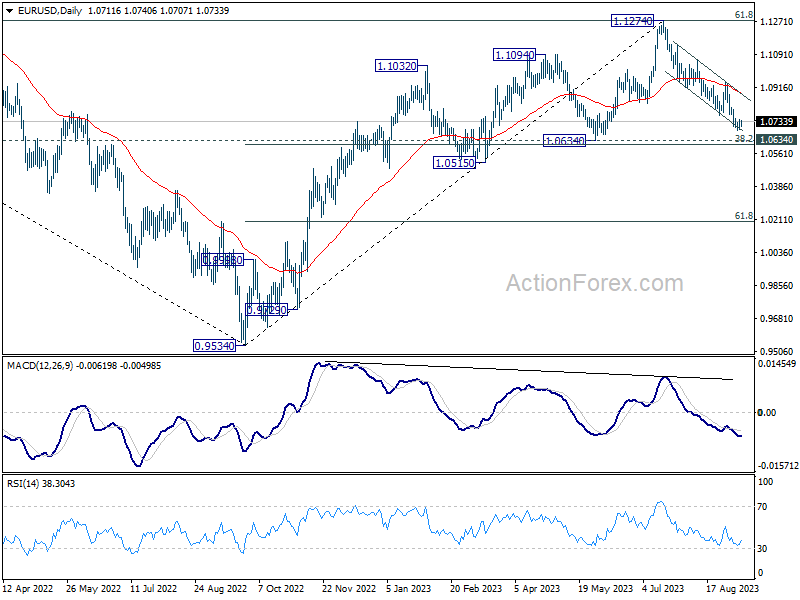

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0681; (P) 1.0713; (R1) 1.0731; More...

EUR/USD is extending the consolidation from 1.0685 and intraday bias stays neutral. Outlook will stay bearish as long as 1.0944 resistance holds. On the downside, below 1.0685 will resume the fall from 1.1274 to 1.0609/34 cluster support zone next.

In the bigger picture, fall from 1.1274 medium term top is seen as a correction to up trend from 0.9534 (2022 low). Strong support could be seen from 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609) to bring rebound, at least on first attempt. Break of 1.0944 will indicate the start of the second leg, and target retest of 1.1274. However, sustained break of 1.0609/0634 will raise the chance of bearish trend reversal, and target 61.8% retracement at 1.0199.